Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

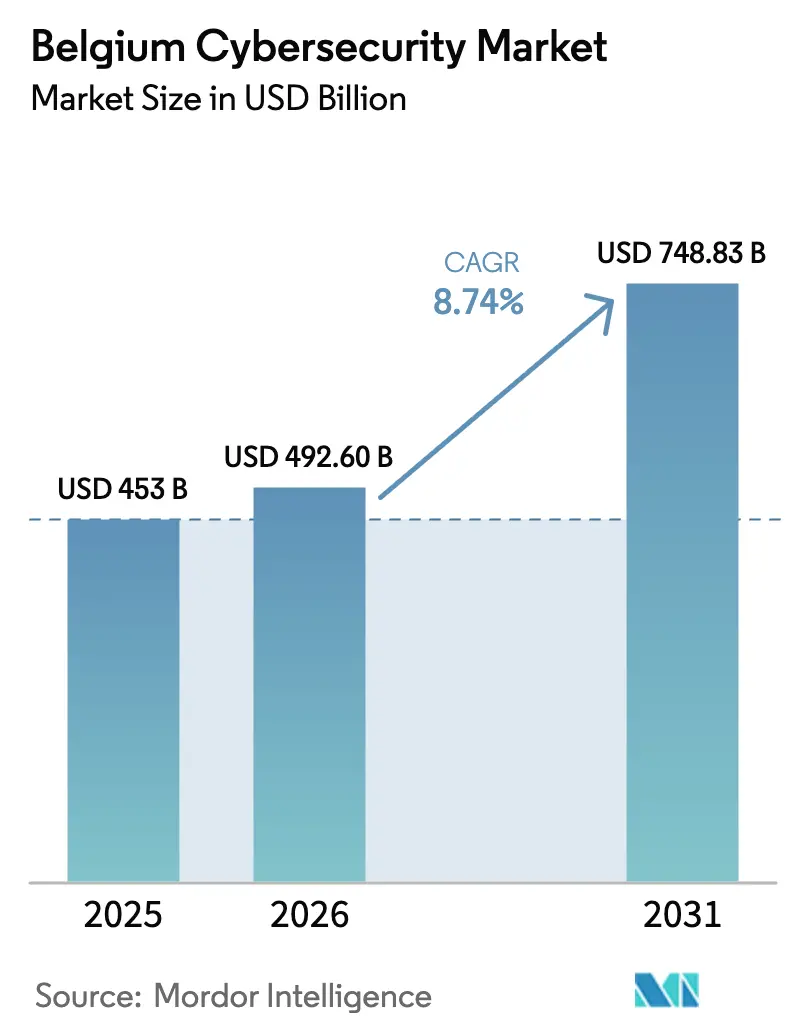

| Base Year Market Size (2025) | USD 453 Billion |

| Market Size (2026) | USD 492.6 Billion |

| Market Size (2031) | USD 748.83 Billion |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Cybersecurity Market Analysis by Mordor Intelligence

The Belgium cybersecurity market size is expected to grow from USD 453 million in 2025 to USD 492.6 million in 2026 and is forecast to reach USD 748.83 million by 2031 at 8.74% CAGR over 2026-2031. Robust digital-economy policies, early transposition of the EU NIS2 directive and strong sovereign-cloud programmes are lifting corporate security budgets, while a rising cadence of sophisticated attacks is forcing board-level attention on cyber risk. Vendor competition remains moderate; global suppliers such as Thales and Fortinet are embedding artificial-intelligence analytics into their Belgian portfolios, while home-grown players including NVISO and Aikido Security focus on tailored compliance and managed services. End-user demand is led by financial services, but healthcare, manufacturing and public sector workloads show the steepest outlay increases as regulation tightens. Government financing, notably the EUR 390 million allocation under the Digital Europe Programme, helps smaller organisations upgrade defences and offsets part of the national skills gap.

Key Report Takeaways

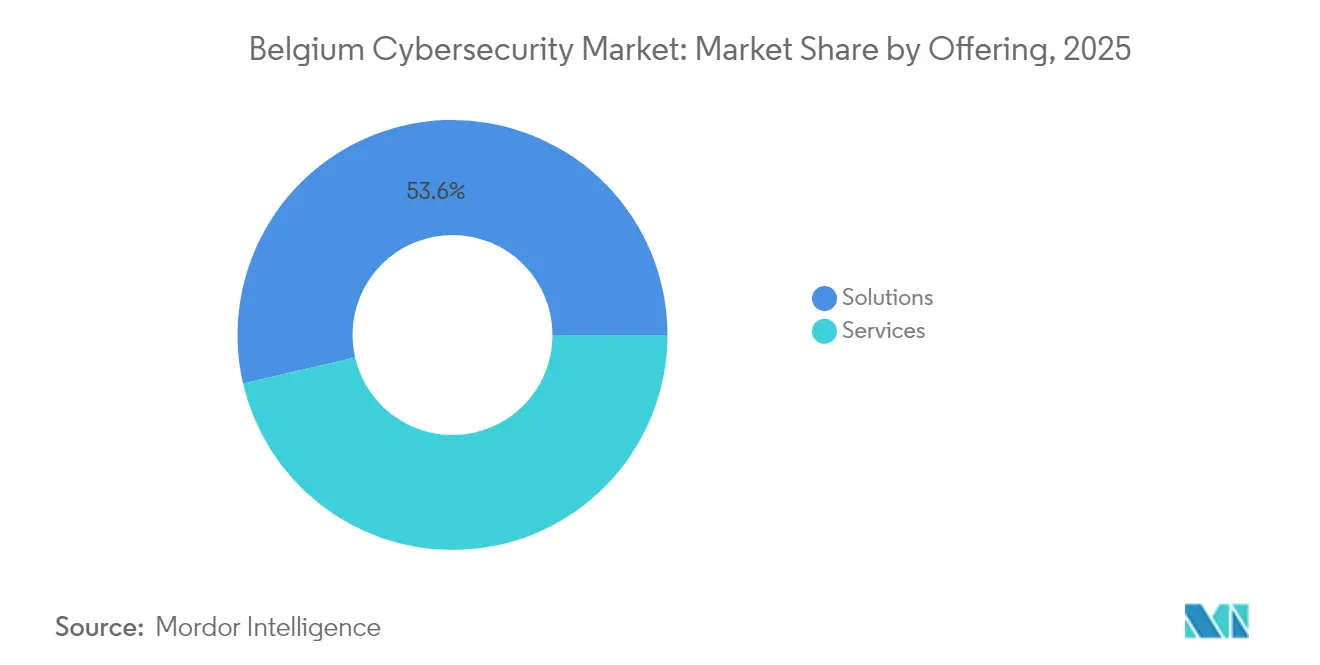

- By offering, solutions retained 53.62% revenue share in 2025, while services are set to accelerate at a 10.08% CAGR through 2031.

- By deployment mode, cloud security captured the highest 56.48% slice of the Belgium cybersecurity market share in 2025 and will advance at a 12.44% CAGR to 2031.

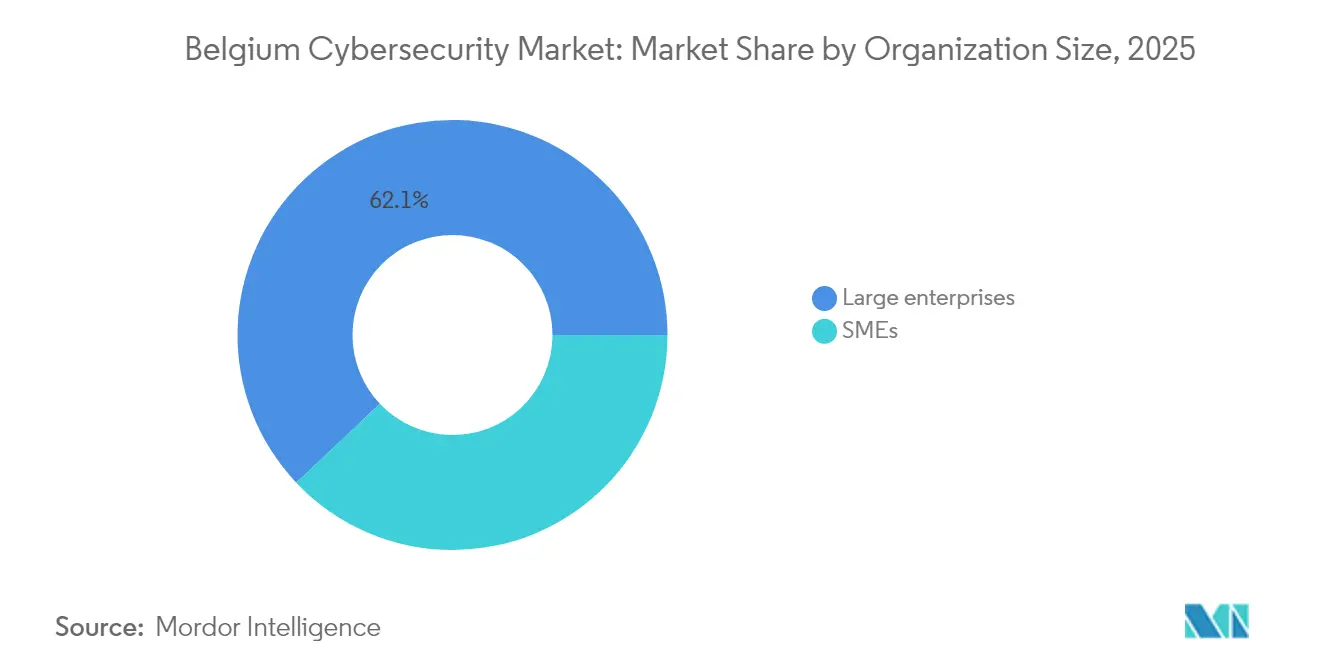

- By organisation size, large enterprises controlled 62.05% of the Belgium cybersecurity market size in 2025; the SME segment is projected to grow at 11.05% CAGR during 2026-2031.

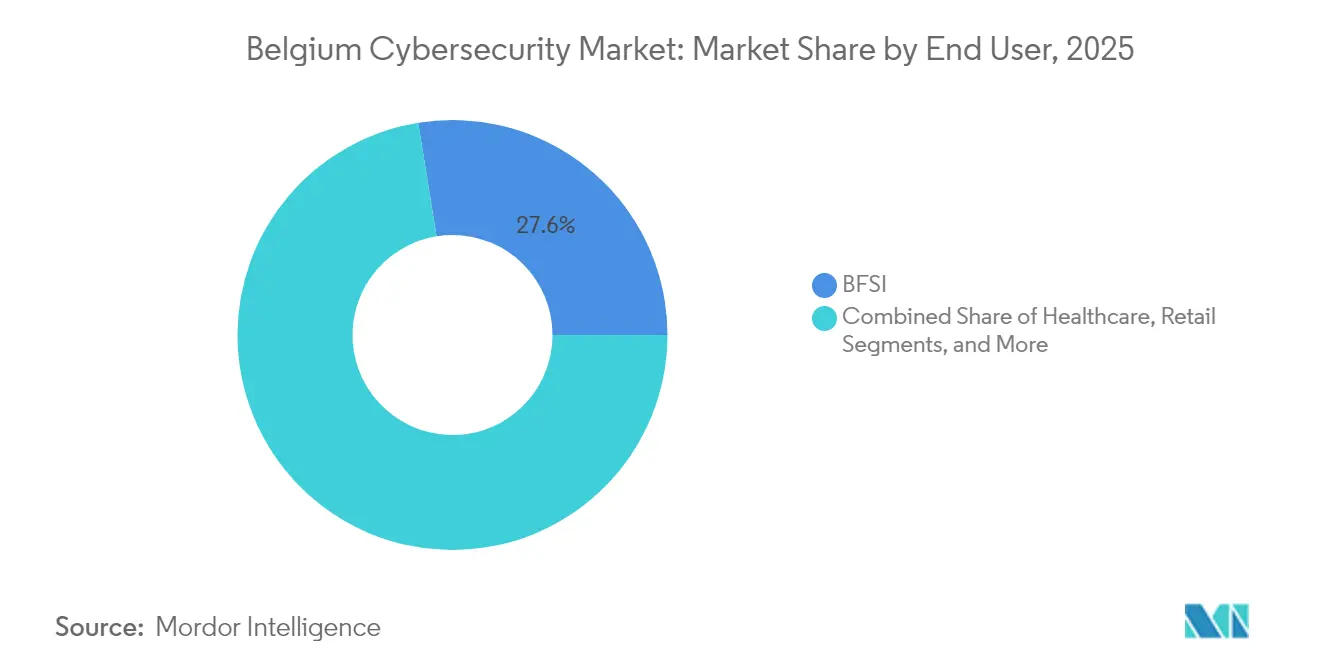

- By end user, BFSI led with 27.55% of 2025 revenue, while healthcare is forecast to post the fastest 11.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Belgium Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU NIS2-driven mandatory security upgrades | +2.1% | National, with concentration in Brussels, Antwerp, Ghent | Short term (≤ 2 years) |

| Low cybersecurity awareness among non-digital native SME leadership | +1.8% | National, particularly Wallonia and rural Flanders | Medium term (2-4 years) |

| Accelerating cloud adoption among Belgian SMEs | +1.4% | National, with early gains in Brussels, Antwerp | Medium term (2-4 years) |

| Emergence of regional MSSP ecosystems (e.g., Proximus ICT) | +1.2% | National, with hub concentration in Brussels | Long term (≥ 4 years) |

| AI-powered threat-hunting platforms lowering SOC costs | +0.9% | National, with enterprise focus in Brussels, Antwerp | Medium term (2-4 years) |

| Cyber-insurance premium incentives for zero-trust architectures | +0.8% | National, with BFSI sector concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU NIS2-driven Mandatory Security Upgrades

Belgium began enforcing the NIS2 directive in October 2024, obliging 2,410 essential and important entities to implement structured risk-management controls and report incidents within 24 hours. Penalties of up to EUR 10 million (USD 11.73 million)or 2% of global turnover have shifted cyber risk to board agendas, spurring multi-year platform refresh projects. The Centre for Cybersecurity Belgium’s CyberFundamentals framework provides a tiered certification path that lowers compliance friction and quickens vendor selection cycles. Hospitals such as UZA Antwerp now run centralised SOCs and have trimmed phishing-email click-rates from 30% to 8% after mandatory staff awareness campaigns. Spending momentum is expected to hold through 2027 as utilities, postal operators and digital-service providers finalise alignment plans.

Accelerating Cloud Adoption Among Belgian SMEs

Seventy-four-and-a-half percent of Belgian SMEs achieved basic digital intensity in 2023, surpassing the EU average and creating steady demand for cloud-native security stacks. Sovereign-cloud agreements, notably the Proximus-Google Cloud initiative, embed locality controls while offering elastic workloads, improving uptake in regulated verticals. Digital-only banks such as NewB operate cloud-first architectures paired with PSD2-compliant strong authentication systems, setting precedents for fintech peers. SMEs now earmark 10-15% of their IT budgets for cybersecurity, channelled mainly toward SaaS-delivered identity, data-protection and micro-segmentation tools. AI-enabled threat analytics bundled into these platforms reduce operational complexity and narrow the capability gap between small firms and large enterprises.

Emergence of Regional MSSP Ecosystems

Proximus Ada and other Brussels-centred service hubs pool scarce security talent and supply 24/7 monitoring, incident-response and compliance-as-a-service packages.[1]Proximus, “Proximus and Google Cloud launch sovereign cloud in Belgium,” proximus.com Partnerships such as Orange Cyberdefense with CrowdStrike extend managed detection and response (MDR) to mid-market manufacturers and logistics operators. MSSPs increasingly embed local regulatory knowledge—especially around NIS2—and offer tiered subscription models aligned to risk appetites. Demand is strongest among organisations with under 250 employees that cannot justify dedicated SOC staffing but must satisfy regulatory baselines.

AI-powered Threat-hunting Platforms Lowering SOC Costs

AI automation is cutting investigation cycles and per-alert handling costs. Proximus’ 365guard blocks SMS spam by continuously learning regional patterns, while FortiSOAR supplies 800+ playbooks for unified case management.[2]Fortinet, “FortiSOAR solution brief,” fortinet.com Belgian hospitals deploy anomaly-detection engines that snapshot clinical systems and flag suspicious behaviours in real time, safeguarding patient records without adding analyst headcount. Adoption is fastest in finance and healthcare where alert volumes are high and compliance timelines short.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute 10k-person cybersecurity talent gap | -1.9% | National, with concentration in Brussels, Antwerp | Long term (≥ 4 years) |

| High reliance on legacy industrial OT in Flanders manufacturing | -1.3% | Flanders region, manufacturing corridors | Long term (≥ 4 years) |

| Budget saturation in public-sector IT refresh cycles | -0.8% | National, with federal and regional government focus | Medium term (2-4 years) |

| Fragmented local vendor landscape limiting platform consolidation | -0.7% | National, with SME sector concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute 10k-person Cybersecurity Talent Gap

Forecasts indicate Belgium will lack about 21,000 technology specialists by 2026, with cyber roles the hardest to fill. Average security-analyst salaries exceed EUR 85,000 (USD 91,800), pitting local firms against multinationals and EU agencies headquartered in Brussels. Skills scarcity is most severe in OT security, cloud architecture and AI-based analytics. Enterprises respond by upsizing MSSP contracts and funding university programmes such as KU Leuven’s master in Cybersecurity Engineering. Despite these measures, the labour pipeline will take several years to stabilise, keeping wage inflation and project delays elevated.

High Reliance on Legacy Industrial OT in Flanders Manufacturing

Many process-control networks in petrochemicals, food and metals plants remain unsegmented and run outdated protocols, exposing critical infrastructure to lateral-movement attacks. Internet-facing scans have revealed vulnerable programmable-logic controllers and HMI dashboards across Flanders.[3]Van Impe, “Industrial Control Systems Exposure Report,” vanimpe.eu Operators hesitate to patch or replace equipment that must run near-continuous production cycles, prolonging risk windows. Specialised integrators such as Soteria retrofit passive-monitoring sensors and anomaly-detection nodes, yet full remediation often coincides with 10-15-year capex refresh intervals, tempering near-term security spend.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Accelerate as Skills Gap Widens

Solutions retained 53.62% of 2025 revenue, anchored by firewall, endpoint and identity suites procured to satisfy NIS2 baselines. In value terms, solutions accounted for USD 242.9 million of the Belgium cybersecurity market size in 2025. Growth, however, tilts toward services at a 10.08% CAGR because outsourcing offsets the labour deficit and offers predictable costs. Managed detection and response, incident readiness assessments and compliance workshops draw the bulk of new contracts. Eye Security’s expansion across the Benelux exemplifies rising interest in tailored MDR packages for mid-sized firms.

Services revenue climbed as clients requested continuous monitoring, threat-intelligence feeds and red-teaming exercises. The Belgium cybersecurity market share of managed services is projected to approach 48.35% by 2031, narrowing the gap with product sales. Vendor success increasingly hinges on integrating automation, analytics and frontline expertise into cohesive service bundles that map directly to regulatory controls.

By Deployment Mode: Cloud Security Dominates Digital Transformation

Cloud-delivered controls captured 56.48% of 2025 spend, equivalent to USD 255.9 million of the Belgium cybersecurity market size, and are forecast to grow at 12.44% CAGR. Sovereign-cloud zones operated by Proximus, paired with Google’s disconnected services, address data-residency mandates and enable regulated workloads. On-premises investments persist in defence, critical infrastructure and certain public entities, yet comprise a shrinking allocation of new budgets.

Cloud uptake is fastest among fintechs and healthcare start-ups that leverage container security, micro-segmentation and DevSecOps pipelines to accelerate product cycles. Multi-cloud and hybrid governance frameworks gain traction in large enterprises seeking unified policy enforcement across Amazon Web Services, Microsoft Azure and private-cloud assets. Automated posture-management tools help resource-constrained teams visualise misconfigurations and policy drift.

By Organization Size: SMEs Drive Growth Despite Enterprise Dominance

Large organisations held 62.05% of 2025 expenditure, underpinned by consolidated SOCs and layered defence platforms. They continue to invest in attack-surface management and zero-trust segmentation, but their incremental budget growth trails that of smaller firms. SMEs generate the highest 11.05% CAGR as the NIS2 scope now encompasses medium-sized businesses in energy, logistics and digital services.

Subscription-based SaaS models and bundled MDR contracts make enterprise-grade controls financially viable for organisations with fewer than 250 employees. Funding rounds for Aikido Security illustrate investor belief that intuitive developer-centric security tooling matches SME requirements. Government voucher schemes in Wallonia further defray adoption costs, stimulating demand across rural municipalities.

By End User: Healthcare Emerges as Fastest-Growing Vertical

BFSI contributed 27.55% of 2025 turnover; its compliance-driven posture keeps spend per employee among the highest in Europe. Banks such as KBC automate behavioural-biometrics and AI-driven fraud analytics to satisfy PSD2 strong-customer-authentication rules. Healthcare, however, is projected to chart an 11.18% CAGR through 2031 on the back of electronic-health-record rollouts and ransomware exposure.

Hospitals deploy phishing-resilience platforms and immutable backup services after a series of 2024 disruptions. Industrial enterprises in Flanders prioritise OT-network segmentation, while telecom operators guard national fibre backbones with high-capacity DDoS scrubbing centres. Retail chains fortify point-of-sale endpoints and e-commerce APIs as transaction volumes climb.

Geography Analysis

Brussels hosts EU institutions, global headquarters and Belgium’s principal cyber-talent pool. The concentration translates into the country’s densest cluster of solution integrators, incident-response firms and research laboratories. Thales alone maintains 1,200 employees across eleven Belgian sites, with flagship CyberIT and CyberOT competence centres in the capital. The city will pilot biometric digital-identity cards from November 2026, injecting fresh investment into encryption, key-management and citizen-data protection frameworks.

Antwerp and Ghent anchor Flanders’ industrial corridor, where manufacturers face legacy-OT risk and port authorities secure maritime logistics chains. InvestAI programme grants, designed to mobilise EUR 200 billion for AI projects, earmark funding for predictive maintenance and cyber-resilience of production lines. Antwerp’s port authority has expanded its cyber-fusion centre to monitor vessel-tracking systems and automate threat-intelligence sharing with freight forwarders.

Wallonia emphasises SME digitalisation under the 2024-2029 Digital Wallonia roadmap, offering “Chèque-Entreprise” subsidies that refund up to 80% of cybersecurity audits. Cross-border ties with France and Luxembourg enable regional MSSPs to service multilingual client bases and standardise compliance tooling across jurisdictions. Emerging projects in renewable-energy storage and smart-grid orchestration are spawning demand for niche OT-security solutions that integrate with real-time SCADA environments.

Competitive Landscape

The Belgium cybersecurity market contains a balanced mix of global platform vendors, regional service providers and niche specialists. Thales, Fortinet, Palo Alto Networks and Cisco leverage scale and multicloud integration to capture complex enterprise deployments. Local champions such as NVISO focus on penetration testing and incident forensics, while Sweepatic’s external-attack-surface mapping broadens Outpost24’s European reach following its 2023 acquisition.

Artificial-intelligence capability is a primary differentiator. Thales works with Google Cloud to embed Chronicle SecOps analytics into its Belgian SOC, enabling sub-minute alert triage. Proximus Ada bundles proprietary AI data-lakes with partner telemetry to feed behavioural-anomaly engines that auto-contain endpoint threats. Competition in managed services intensifies as Orange Cyberdefense doubles MDR headcount, and Sophos integrates Secureworks’ telemetry to support 28,000 MDR customers worldwide.

White-space opportunities persist in OT security for manufacturing and energy, as well as compliance-as-a-service solutions that translate NIS2 clauses into automated control libraries. Partnerships between niche technology vendors and MSSPs are expected to accelerate to bridge capability gaps and satisfy mid-market demand for integrated, outcome-based offerings.

Belgium Cybersecurity Industry Leaders

IBM Corporation

Cisco Systems, Inc.

Thales

Sweepatic

RHEA Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CGI entered exclusive talks to acquire Apside, adding 2,500 European engineers and reinforcing CGI’s Belgian cybersecurity and digital-manufacturing portfolio.

- May 2025: Proofpoint agreed to purchase Hornetsecurity for more than USD 1 billion, broadening Proofpoint’s European email-security base, including Belgian SME customers.

- February 2025: Sophos completed its USD 859 million acquisition of Secureworks, creating the world’s largest pure-play managed-detection-and-response provider.

- August 2024: VaultSpeed raised USD 15.9 million to scale its automated data-transformation platform for finance and healthcare customers.

Belgium Cybersecurity Market Report Scope

Cybersecurity solutions help an organization monitor, detect, report, and counter cyber threats that are internet-based attempts to damage or disrupt information systems and hack critical information using spyware and malware, and phishing, to maintain data confidentiality. The study is structured to track the revenues accrued by cybersecurity vendors through sales of various solutions and allied services.

The Belgium cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Solutions | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-premise |

By Organisation Size

| SMEs |

| Large Enterprises |

By End User

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defence |

| Retail |

| Energy and Utilities |

| Manufacturing |

| Others |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Solutions | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-premise | ||

| By Organisation Size | SMEs | |

| Large Enterprises | ||

| By End User | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defence | ||

| Retail | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

Key Questions Answered in the Report

What is the size of the Belgium cybersecurity market in 2026?

The Belgium cybersecurity market size reached USD 492.6 million in 2026 and is forecast to climb to USD 748.83 million by 2031.

Which segment is growing the fastest?

Cybersecurity services show the highest momentum, expanding at a projected 10.08% CAGR as organisations outsource monitoring and compliance workloads.

Why is cloud security so dominant in Belgium?

Rapid SME digitalisation and sovereign-cloud offerings that ensure data residency have pushed cloud-delivered controls to 56.48% of 2025 spend, with a 12.44% forecast CAGR.

How does the EU NIS2 directive influence spending?

NIS2 imposes mandatory risk controls and strict fines, elevating cybersecurity to a board-level issue and adding an estimated 2.1 percentage points to the market’s CAGR.

What is the main challenge hindering market growth?

Belgium faces a prolonged shortage of about 10,000 cybersecurity professionals, driving labour costs up and extending project timelines.

Page last updated on: