Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

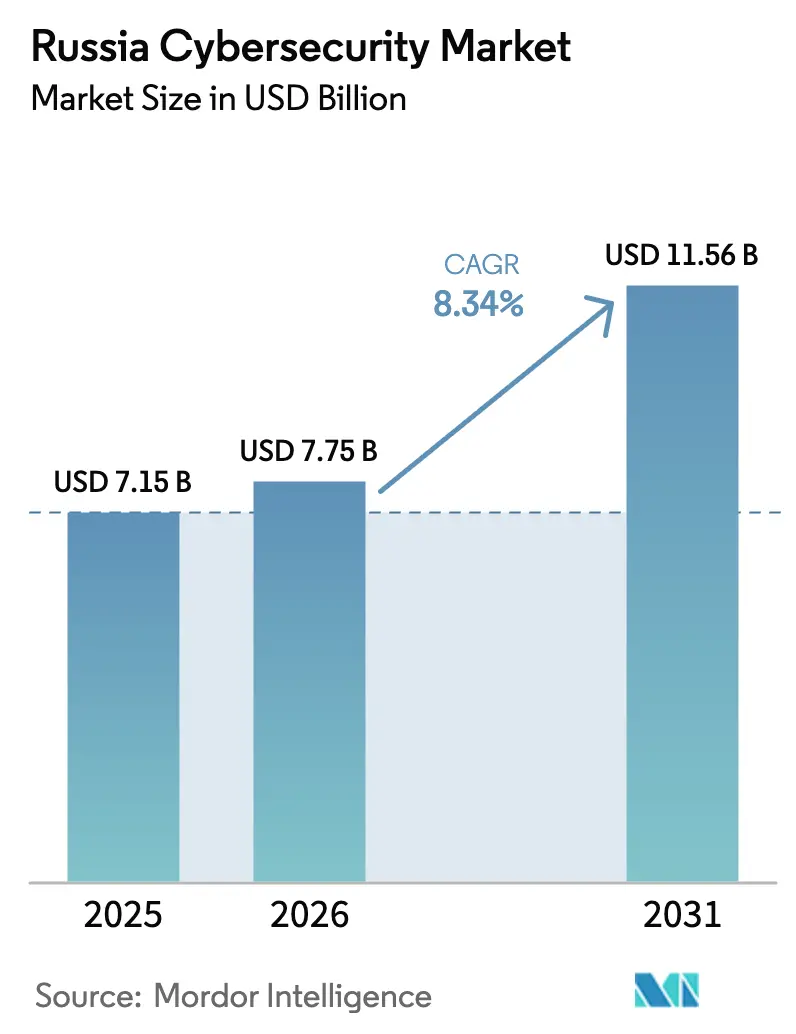

| Base Year Market Size (2025) | USD 7.15 Billion |

| Market Size (2026) | USD 7.75 Billion |

| Market Size (2031) | USD 11.56 Billion |

| Growth Rate (2026 - 2031) | 8.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Cybersecurity Market Analysis by Mordor Intelligence

The Russia cybersecurity market size was valued at USD 7.15 billion in 2025 and estimated to grow from USD 7.75 billion in 2026 to reach USD 11.56 billion by 2031, at a CAGR of 8.34% during the forecast period (2026-2031). Market expansion is propelled by the state’s digital-sovereignty agenda, which mandates certified Russian solutions across critical information infrastructure and drives steady budget allocations even in a constrained macroeconomic climate. Rising ransomware losses, stricter data-localisation rules, and compulsory annual security audits are prompting enterprises—especially in banking, energy, and healthcare—to prioritise cyber outlays over other IT spending. Domestic cloud-and-data-centre build-outs by players such as Rostelecom create fresh demand for zero-trust architectures, while import-substitution policies lift revenue visibility for Russian vendors that can replace sanctioned hardware.

Key Report Takeaways

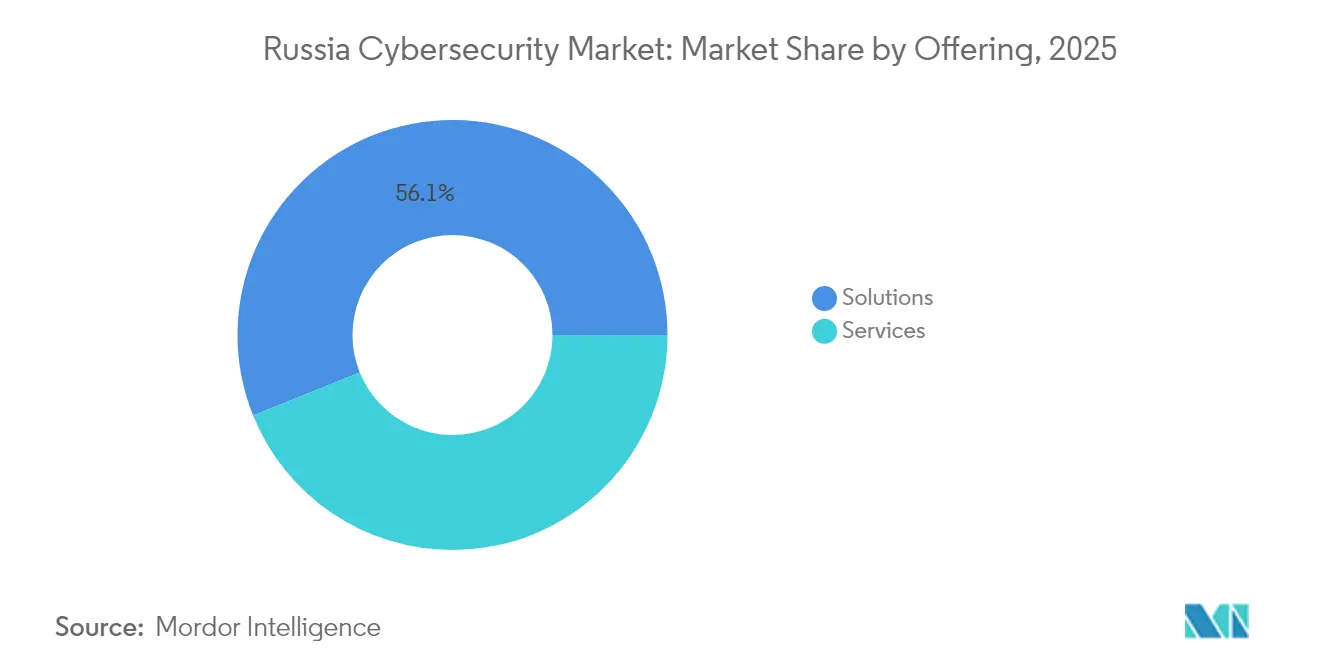

- By offering, solutions held 56.10% Russia cybersecurity market share in 2025; services post the fastest 2026-2031 CAGR at 9.75%.

- By deployment mode, on-premise accounted for 61.55% revenue share of the Russia cybersecurity market in 2025 and cloud deployment is forecast to grow at an 11.25% CAGR through 2031.

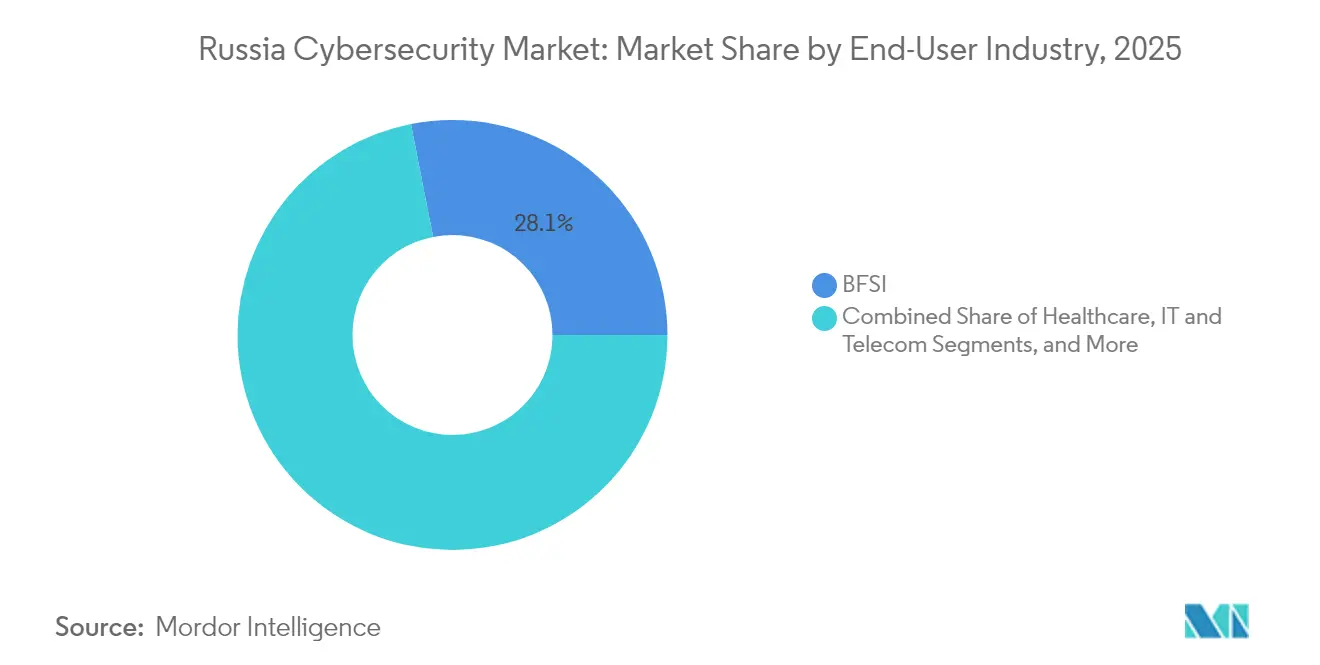

- By end-user industry, BFSI led with 28.10% share in 2025, while healthcare is projected to expand at a 12.05% CAGR to 2031.

- By end-user enterprise size, large enterprises controlled 66.60% of the Russia cybersecurity market in 2025; SMEs record the highest 10.35% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Sovereignty Push and Import Substitution Mandates in Russian IT Security Ecosystem | +2.1% | National | Medium term (2-4 years) |

| Surge in State-Led Critical Infrastructure Protection Programs Post-Ukraine Conflict | +1.8% | Moscow and St Petersburg first | Short term (≤2 years) |

| Rapid Expansion of Domestic Cloud and Data Center Footprint Driving Zero-Trust Adoption | +1.5% | Major urban hubs | Medium term (2-4 years) |

| Proliferation of Industrial IoT in Oil and Gas and Utilities Requiring OT Security Controls | +1.2% | Resource-rich regions | Medium term (2-4 years) |

| Escalating Ransomware-as-a-Service Attacks Targeting Russian SMEs | +0.9% | Nationwide | Short term (≤2 years) |

| Mandatory data-localisation laws raising on-prem demand | +0.7% | Nationwide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Digital Sovereignty Push and Import Substitution Mandates in Russian IT Security Ecosystem

Russia cybersecurity market participants are experiencing a structurally protected environment after the December 2024 import-substitution decree that blocks many foreign products. Decree 1875 bars many foreign IT goods from public procurement and enforces a “second-one-out” rule that privileges bids listing Russian origin. As a result, local vendors such as Kaspersky and Positive Technologies report pipeline growth that outstrips hiring capacity, while ministries require certified domestic crypto algorithms in every new deployment.

Surge in State-Led Critical Infrastructure Protection Programs Post-Ukraine Conflict

Regulatory updates issued by the Federal Security Service (FSB) have turned critical-infrastructure protection from an IT responsibility into a board-level compliance mandate. FSB Order 239 and the Ministry of Transport’s 2024 methodology oblige utilities, airports and railways to feed telemetry into a unified state platform. Incident data show average downtime per attack falling from 65 hours in 2018 to 1 hour in 2024, proving regulatory pressure accelerates defence maturity [1]Ministry of Transport of the Russian Federation, “Methodical Recommendations for Categorising Critical Information Infrastructure,” mintrans.gov.ru.

Rapid Expansion of Domestic Cloud and Data Center Footprint Driving Zero-Trust Adoption

Rostelecom’s July 2024 Moscow facility and BitRiver’s 100 MW Far-East campus expand national compute by more than 20 %, prompting enterprises to shift workloads off-premise. Each migration drives uptake of micro-segmentation and zero-trust controls certified under Russian standards. With each capacity increment, enterprises move non-critical workloads off-premise and then confront compliance clauses that require zero-trust segmentation. Early adopters such as Bank Primorye show that cloud-based web-application firewalls can neutralise millions of events per quarter without adding staff, which implies operating-cost efficiencies that incentivise further migration.

Proliferation of Industrial IoT in Oil and Gas and Utilities Requiring OT Security Controls

Kaspersky ICS-CERT uncovered CVE-2023-47610 in Cinterion modems, highlighting systemic OT exposure. Energy firms responded by fast-tracking protocol-aware intrusion-prevention systems, and plant audits report measurable reductions in unplanned downtime [2]Kaspersky ICS-CERT, “Advisory on CVE-2023-47610,” ics-cert.kaspersky.com. Following the advisory, several state-owned energy utilities accelerated procurement of protocol-aware intrusion-prevention systems, illustrating that headline vulnerabilities can move budgets at short notice.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent Drain Due to Emigration and Military Mobilization Impacting Cyber Workforce | -1.7% | Tech hubs | Long term (≥5 years) |

| US/EU Export Controls Limiting Access to Advanced Security Hardware and Updates | -1.5% | National | Medium term (2-4 years) |

| Budget Compression in Non-Resource Sectors Amid Macroeconomic Sanctions | -1.0% | Sector-specific | Short term (≤2 years) |

| Fragmented Federal Procurement Processes Delaying Security Modernization | -0.6% | Government verticals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Talent Drain Due to Emigration and Military Mobilization Impacting Cyber Workforce

Positive Technologies finds vacancy growth in information security outrunning graduate supply three-to-one, sending average security-analyst pay 25 % above national IT wages. Organisations compensate by automating tier-1 triage through ML-powered XDR platforms.

US/EU Export Controls Limiting Access to Advanced Security Hardware and Updates

September 2024 US Commerce rules pull selected enterprise software and firmware into licence regimes, freezing updates on Western appliances already installed in Russian networks. Operators resort to grey imports, which escalate maintenance costs and spur domestic ASIC design.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions Hold Leadership While Services Accelerate

Solutions generated 56.10% of Russia cybersecurity market share in 2025, underscoring the historic preference for capital purchases and in-house operation. Revenue remains anchored in network firewalls, endpoint protection and Secure Web Gateways that satisfy FSB certification protocols. Yet the addressable pool is gradually tilting toward services as enterprises struggle to staff 24/7 security centres. Managed detection and response packages priced on a per-node basis allow even mid-sized banks to activate threat hunting without hiring, a shift that lifts the services CAGR to 9.75% through 2031.

Rising adoption of service-bundled XDR platforms indicates that organisations value outcome-based billing more than feature counts. Vendors now bundle compliance audits, incident retainer hours and threat-intel feeds, positioning services as an operating-expense hedge against volatile hardware supply. As a result, annual recurring revenue grows faster than licence sales, and the Russia cybersecurity market size attached to services could exceed USD 5.4 billion by 2031 if current renewals hold.

By Deployment Mode: Cloud Momentum Outpaces On-Prem Dominance

On-premise deployment already captured 61.55% of the Russia cybersecurity market share in 2025, a pattern reinforced by strict data-sovereignty laws that keep sensitive workloads behind agency firewalls. Compliance requirements under FSB Order 239 mean that operators labelled as critical information infrastructure must store audit logs locally for multiple years, entrenching on-site storage demand. Domestic hyperscalers deliver isolated government regions that comply with data-localisation law, giving risk-averse ministries a migration path. This trust foundation drives an 11.25% CAGR for cloud-deployed controls, whereas on-prem investments plateau as amortised appliances reach end-of-life without Western firmware updates.

Hybrid blueprints that keep keys on premises but run analytics in sovereign clouds dominate new RFPs. Such patterns shorten patch cycles and reduce capex, proving attractive amid tight credit conditions. Consequently, Russia cybersecurity market references increasingly cite micro-segmentation and cloud Workload Protection Platforms as mandatory checklist items rather than advanced options.

By End-User Industry: BFSI Leads, Healthcare Races Ahead

The banking, financial services and insurance community accounted for 28.10% of Russia cybersecurity market revenue in 2025. Mandatory penetration tests under Central Bank Directive 683-P and the rollout of the digital ruble spur continuous refresh of fraud-analytics modules and behavioural biometrics . Despite that heft, the healthcare vertical is set to record the fastest 12.05% CAGR to 2031, propelled by electronic medical-record rollouts and telemedicine expansion into remote oblasts.

Hospitals now rank as critical information-infrastructure operators, subjecting them to FSB Order 239 log-retention and incident reporting rules. Procurement data show a pivot toward agentless network access-control and medical-device micro-segmentation. Vendors that embed HL7 protocol awareness secure strategic footholds, hinting that healthcare could overtake energy as the second-largest slice of the Russia cybersecurity market before 2031.

By End-user Enterprise Size: Large Enterprises Dominate While SMEs Pick Up Pace

Large organisations commanded 66.60% of 2025 spending, reflecting the deep pockets of oil majors, telcos and state banks. Framework contracts worth USD 50-100 million lock in multi-year refreshes of SIEM, vulnerability scanning and privileged-access management suites. These deals underscore the market’s dependence on a few hundred top-tier buyers.

SMEs, though smaller today, deliver a 10.35% CAGR through 2031 as ransomware insurance clauses demand basic controls. Government grants that subsidise up to 80 % of software-acquisition costs for small exporters further democratise protection. As subscription models proliferate, the Russia cybersecurity industry gains a long-tail revenue stream that cushions cyclical swings in mega-projects.

Geography Analysis

Moscow and the broader Central Federal District represent the single largest node of Russia cybersecurity market activity. Headquarters of banks, federal ministries and domestic hyperscalers concentrate procurement here, and pilot compliance frameworks often debut in the capital before national rollout. Contract data reveal that more than 45 % of new SOC build-outs in 2024 originated in Moscow, confirming the district’s bellwether status.

The Volga and Ural districts form the industrial engine room, covering refineries, automotive plants and metal smelters. Elevated OT-security demand follows highly publicised PLC vulnerabilities uncovered in 2024, pushing asset owners to deploy passive anomaly-detection sensors across production networks. Resultant orders boosted regional market value by double digits, strengthening the Russia cybersecurity market footprint beyond its administrative core.

The Far Eastern and Siberian districts, though less populous, gain strategic heft from energy-intensive data-centre projects leveraging surplus hydropower. BitRiver’s 100 MW campus near Irkutsk anchors a nascent high-performance-computing corridor, prompting specialised cybersecurity tooling for immersion-cooled racks and containerised edge nodes. Ongoing smart-port projects in Vladivostok add maritime-security niches, rounding out a geographically diversified revenue portfolio.

Competitive Landscape

Domestic champions continue to consolidate share as sanctions sideline many Western brands. Kaspersky remains the reference vendor, pairing endpoint dominance with an April 2024 XDR launch that auto-triages 70 % of alerts without analyst oversight [4]Kaspersky, “XDR Platform Technical White Paper,” kaspersky.com. Positive Technologies scales by integrating network sensors with its MaxPatrol SIEM, giving customers single-console visibility—a capability prized by resource-strained SOCs.

Partnerships with non-sanctioning countries accelerate product roadmaps. Rostelecom-Solar’s MoU with a Chinese chipset supplier enables next-gen firewall appliances optimised for Russian GOST crypto. Exclusive distribution clauses embedded in such deals grant early movers a scale moat, reinforcing their grip on the Russia cybersecurity market.

Talent scarcity drives a premium on automation. Vendors embedding machine-learning engines that draft incident-response playbooks win bids where buyers cannot fill Level-1 analyst roles. As a result, platform convergence intensifies: endpoint, network and cloud sensors now ship under unified licence contracts, ratcheting up switching costs and nudging the Russia cybersecurity industry toward an oligopolistic structure.

Russia Cybersecurity Industry Leaders

Kaspersky Lab

Positive Technologies

Solar Security

Group-IB

Bi.Zone

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kaspersky identified CVE-2025-2783, a Chrome zero-day that bypassed sandboxing; government agencies issued emergency patch directives within 24 hours.

- May 2024: Kaspersky disclosed active exploitation of Windows CVE-2024-30051 in QakBot campaigns, prompting regional banks to harden ATM fleets.

- April 2024: New Roskomnadzor rules forced hosting providers to register services and document security hygiene before go-live.

- April 2024: Kaspersky launched its Extended Detection and Response platform, cutting mean-time-to-detect by up to 40 % in pilot deployments.

Russia Cybersecurity Market Report Scope

Cybersecurity solutions enable an organization to monitor, detect, report, and counter cyber threats that are internet-based attempts to damage or disrupt information systems and hack critical information using spyware, malware, and phishing to maintain data confidentiality.

The Russia cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the projected value of the Russia cybersecurity market by 2031?

The market is forecast to reach USD 11.56 billion by 2031, growing at an 8.34% CAGR.

Which deployment mode shows the fastest growth in Russia’s cybersecurity landscape?

Cloud-based deployment leads with an 11.25% CAGR for 2026-2031 as domestic hyperscalers expand capacity.

Why is the healthcare sector the quickest-expanding end-user segment?

Electronic medical-record rollouts and telemedicine initiatives push healthcare spending at a 12.05% CAGR through 2031.

How do import-substitution mandates influence vendor selection?

Decree 1875 favours certified Russian solutions, boosting order pipelines for domestic providers and limiting foreign bids.

Page last updated on: