Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

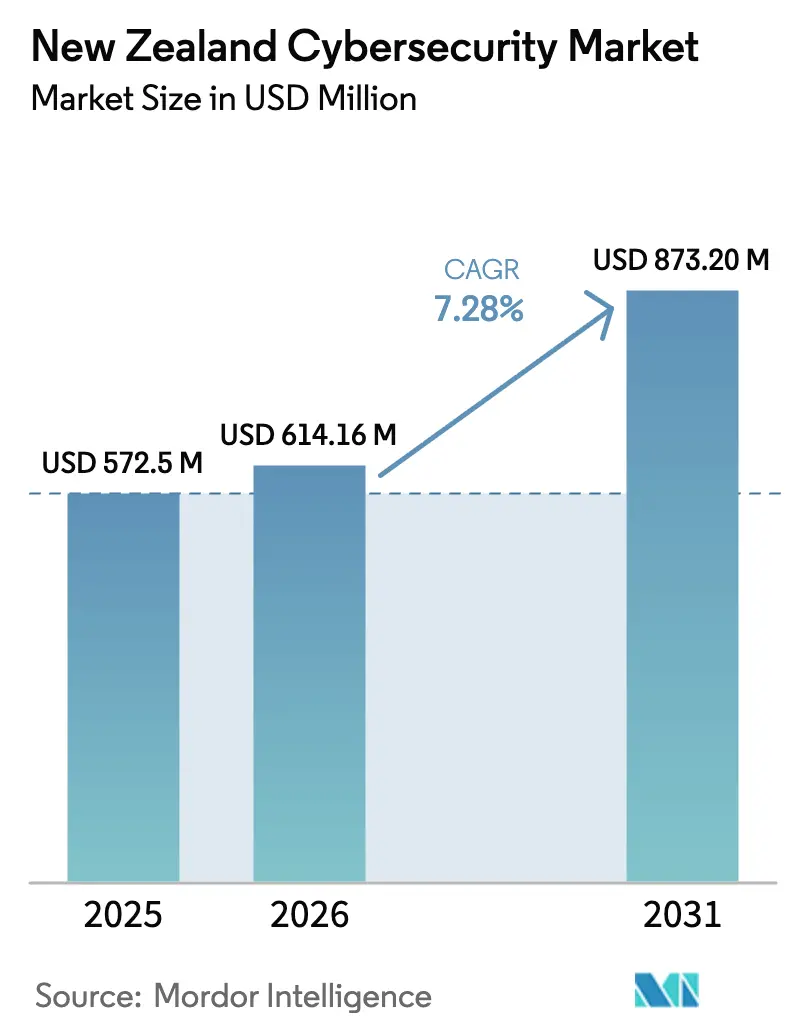

| Base Year Market Size (2025) | USD 572.5 Million |

| Market Size (2026) | USD 614.16 Million |

| Market Size (2031) | USD 873.2 Million |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

New Zealand Cybersecurity Market Analysis by Mordor Intelligence

New Zealand cybersecurity market size in 2026 is estimated at USD 614.16 million, growing from 2025 value of USD 572.5 million with 2031 projections showing USD 873.2 million, growing at 7.28% CAGR over 2026-2031. Rising cloud‐first transformations, the first recorded dominance of financially motivated intrusions, and policy mandates that integrate indigenous data sovereignty are together lifting yearly security allocations. Boards now treat prevention and resilience as recurring operating expense, locking in multi-year revenue visibility for vendors while insulating budgets from conventional economic cycles. Intensified regulatory oversight—spanning privacy breach notification to critical-infrastructure directives—has also enlarged the total addressable pool, because every supplier to the Crown must now furnish audited assurance frameworks. With insurers requiring zero-trust evidence before renewing cover, underwriting questionnaires have effectively become sector-wide compliance gatekeepers. These converging forces confirm that the New Zealand cybersecurity market is progressing from episodic project spending to a durable, structurally funded investment path.

Key Report Takeaways

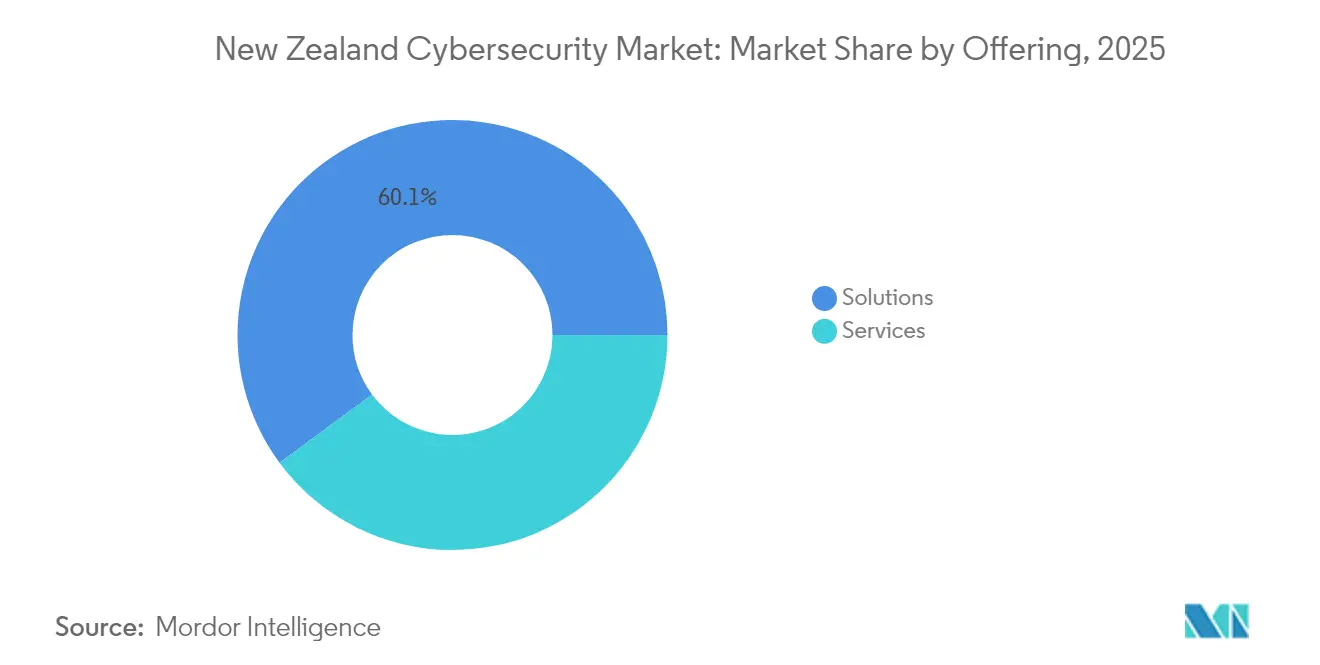

- By offering, services overtook solutions in growth tempo, advancing at 11.1% CAGR to 2031 while solutions retained a 60.12% 2025 revenue lead in the New Zealand cybersecurity market share.

- By deployment mode, on-premise controlled 51.60% of 2025 spend, yet cloud security is the fastest-rising slice at 10.1% CAGR through 2031 as hybrid workplaces normalise.

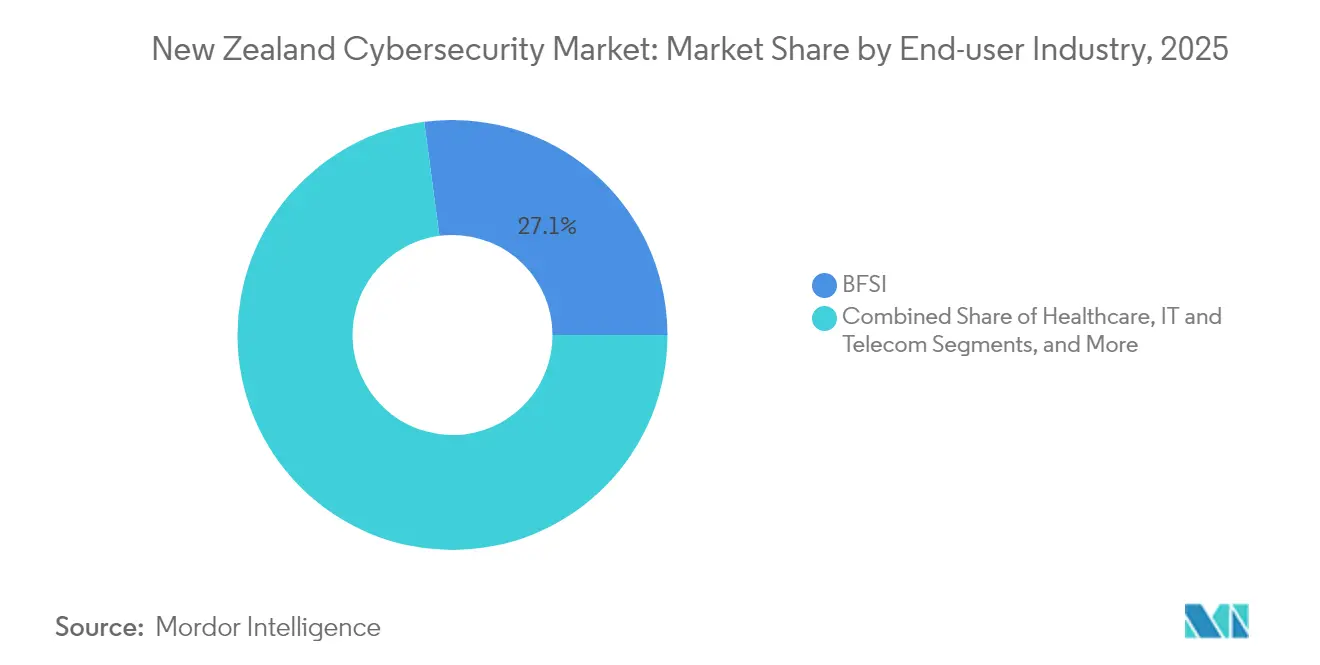

- By end-user industry, BFSI remained the largest buyer with 27.10% of 2025 revenue, whereas healthcare posts the highest 2026-2031 CAGR at 11.7% after headline ransomware events.

- By end-user enterprise size, large enterprises commanded 69.70% of 2025 spend, but SMEs will grow fastest at 10.4% CAGR as subscription MSSP bundles lower entry barriers.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

New Zealand Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government’s 2023 Cyber Security Strategy Stimulating Enterprise Spending | +2.10% | Nationwide; focus on Auckland, Wellington, Christchurch | Medium term (2-4 years) |

| Mandatory Privacy Breach Notification (Privacy Act 2020) Accelerating Adoption | +1.80% | Nationwide | Short term (≤ 2 years) |

| Surge in Ransomware Attacks Affecting Critical Infrastructure and SMEs | +1.50% | Nationwide; acute in healthcare & utilities | Short term (≤ 2 years) |

| Rapid Cloud Migration and Remote Workforce Dependence | +2.30% | Nationwide; strongest in urban centres | Medium term (2-4 years) |

| Cyber-Insurance Premium Inflation Driving Proactive Security Investment | +1.20% | Nationwide | Short term (≤ 2 years) |

| Demand for Zero-Trust Architecture and XDR Platforms | +1.40% | Financial services & public sector hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government’s 2023 Cyber Security Strategy Stimulating Enterprise Spending

The National Security Strategy published in 2023 elevates cyber risk to a core national-security pillar and directs agencies to pursue early action rather than reactive containment [1]Department of the Prime Minister and Cabinet, “New Zealand National Security Strategy 2023,” dpmc.govt.nz. The guidance binds crown entities to specific assurance baselines, which private-sector suppliers must also satisfy to preserve eligibility for contracts. One result is accelerated tender timelines bundling multiyear support, lifting lifetime values for compliant vendors. Local councils now tap co-funding pools patterned on disaster-resilience grants, broadening regional demand. Crucially, the strategy embeds indigenous data stewardship into standard risk-assurance frameworks, so that every new workload touching Māori data invokes culturally aligned governance checks. These aligned incentives enlarge the New Zealand cybersecurity market because compliance becomes a prerequisite to trading with government or its tier-one contractors.

Mandatory Privacy Breach Notification (Privacy Act 2020) Accelerating Adoption

The Privacy Act 2020 obliges organisations to disclose serious breaches within prescribed windows or face penalties. Healthcare outlays rose 22% in 2024 as hospitals linked patient-safety arguments to breach-notification risk, legitimising budget reallocation. Boards therefore install extended detection-and-response (XDR) stacks and commission 24×7 monitoring to document diligence. MSSPs now bundle breach-report templates and regulator-ready artefacts into baseline packages, converting legal exposure into productised features. Planned legislative refreshes that envisage larger monetary fines and biometric-data safeguards will tighten the compliance net further, magnifying downstream demand for process automation and encryption.

Surge in Ransomware Attacks Affecting Critical Infrastructure and SMEs

Financially motivated attackers executed 28% of significant incidents logged by NCSC last fiscal year, outstripping state-linked operations for the first time. Waikato DHB’s protracted outage and Bloom Hearing’s data leak crystallised the business-continuity stakes for boards across sectors. Gen Digital’s Q2 2024 threat report recorded a 24% jump in consumer ransomware within New Zealand, underlining breadth of exposure. Insurers now scrutinise segmentation, immutable backup, and incident-response runbooks before underwriting. Organisations conclude that paying ransoms fails to offset reputational and operational fallout, so prevention budgets soar, reinforcing growth momentum across the New Zealand cybersecurity market.

Rapid Cloud Migration and Remote Workforce Dependence

Remote-work normalisation pushes organisations toward secure-access-service-edge (SASE) overlays bundling network and security functions. Kordia’s 2024 merger of cloud and cyber units typifies supplier moves to capture converged demand. As Microsoft, AWS, and Spectrum Consulting stand up sovereign zones, localisation of control planes boosts consumption of cloud-native posture-management tools. The migration dynamic therefore acts as a structural accelerator for the New Zealand cybersecurity market size trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Shortage of Advanced Cyber Talent Inside NZ | −1.9% | Nationwide; sharper outside tier-one cities | Long term (≥ 4 years) |

| Budget Constraints of SMEs | −1.7% | Nationwide | Medium term (2-4 years) |

| High Reliance on Imported Solutions Exposed to NZD Volatility | −1.1% | Nationwide | Medium term (2-4 years) |

| Fragmented Tooling Creating Integration Complexity | −1.3% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Advanced Cyber Talent Inside NZ

New Zealand requires around 3,500 additional security professionals. SMEs and regional councils struggle to compete for expertise, delaying roll-outs beyond budgeted cycles. Providers compensate by leveraging offshore SOC resources, but that workaround clashes with data-residency promises central to many contracts. Universities have synchronised coursework with international certifications; however, graduation intake still trails demand. The shortage curbs the New Zealand cybersecurity market’s expansion rate because projects stall for people rather than money.

Budget Constraints of SMEs

SMEs compose 90% of domestic SaaS exporters, yet cyber-insurance premiums spiked through 2024, consuming scarce working capital [2]KiwiSaaS, “State of the SaaS Sector 2024,” kiwisaas.com. Banks increasingly bake security posture into credit risk, raising borrowing costs for under-protected firms. Managed service bundles starting at low monthly rates are emerging, but micro-businesses with sub-10 staff still find fees daunting. Uptake therefore remains uneven, muting the otherwise vast SME contribution to overall market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Narrow the Lead of Solutions

Solutions held 60.12% of 2025 spending, equating to roughly USD 344.3 million of the New Zealand cybersecurity market size. However, services will compound at 11.1% to 2031, steadily eroding the historical solutions lead. Organisations outsource 24×7 monitoring and threat hunting because talent scarcity makes internal operations impractical. MSSPs differentiate by folding privacy-compliance attestations and indigenous governance artefacts into service-level agreements, turning legislative burden into subscription value. Cloud-security and identity-and-access management licences now account for highest solution growth, spurred by zero-trust roll-outs linked to insurance renewals.

Professional-services revenue rises as boards seek strategic risk mapping against evolving directives. Consultants versed in Māori data protocols secure advisory retainers that global majors cannot easily replicate, redistributing fees toward local boutiques. AI-driven analytics, while promising scale efficiencies, still require human validation to curb false-positive fatigue, ensuring ongoing demand for tier-two incident analysts. Hardware gateway refresh cycles flatten as funds pivot to SaaS-delivered controls. Overall, the shift in mix signals that the New Zealand cybersecurity market is converting one-off product margins into dependable service annuities.

By Deployment Mode: Cloud Gains Despite On-Premise Dominance

On-premise architectures held 51.60% of spending during 2025, reflecting entrenched sovereignty sensitivities and sunk data-centre investment. Nonetheless, cloud-based controls are forecast to rise at 10.1% CAGR, elevating their slice of the New Zealand cybersecurity market share beyond 48% by 2031. Adoption typically starts with secure email gateways or identity federation, then expands into full SASE frameworks once trust builds. Indigenous co-governance agreements require providers to host primary and secondary replicas domestically, spurring sovereign-cloud innovation such as Spectrum’s Lantern AI platform.

Legacy appliance vendors hedge by offering virtualised firewalls cross-licensed for major IaaS environments, reducing switching friction. Yet buyers increasingly benchmark them against native-cloud posture tools integrated into hyperscaler consoles. Integration complexity remains purchase-critical: platforms sporting pre-built connectors to Microsoft 365, AWS, or GCP win shorter deployment cycles, which is pivotal for projects racing to hit breach-notification compliance. Cloud adoption therefore acts as both demand generator and competitive filter, shaping evolution of the New Zealand cybersecurity market size.

By End-User Industry: Healthcare Tops the Growth Charts

BFSI commanded 27.10% of 2025 spend anchored by stringent prudential oversight and customer trust imperatives. Yet healthcare is forecast to lead expansion at 11.7% CAGR, reflecting post-incident urgency to safeguard patient records and clinical workflows. Waikato DHB’s multi-month recovery became a national case study that linked operational resilience to direct patient outcomes, moving cybersecurity from IT cost to clinical-safety budget.

Government departments wield the National Security Strategy to justify stepped-up investments in secure collaboration platforms that facilitate cross-agency data sharing. Industrial and defence operators prioritise operational-technology visibility, evidenced by Dragos-Yokogawa collaborations embedding threat intelligence into SCADA fabrics. Retail and manufacturing lines deploy supplier-risk solutions to pre-empt cascade breaches that could stall fulfilment. Energy utilities overlay zero-trust on IoT sensors monitoring grid assets, effectively converging cyber and operational reliability. These multi-sector drivers keep the New Zealand cybersecurity market diversified, mitigating over-reliance on any single vertical.

By End-user Enterprise Size: SMEs Fastest-Growing Cohort

Large enterprises delivered 69.70% of 2025 revenue, an expected outcome given their wider digital footprints and regulatory exposure. Even so, SME spend will grow 10.4% CAGR, the highest among size tiers, as subscription MSSP offerings democratise access to enterprise-grade protection. Government co-funding vouchers for export-oriented start-ups offset initial onboarding fees, accelerating uptake. CyberCX and Datacom have launched SME-focused service tiers with simplified dashboards and predictable per-user pricing, making budgeting easier for firms under 100 staff.

A secondary growth lever is customer pressure: multinational buyers increasingly stipulate ISO 27001 or NZISM alignment in supply-chain contracts, forcing SMEs to invest or risk revenue loss. AI-powered toolsets that automate baseline hygiene—patching, MFA enforcement, privileged-access alerts—let small IT teams manage complexity without deep specialist headcount. Collectively, these factors underline that closing the SME adoption gap could add more than USD 100 million incremental spend to the New Zealand cybersecurity market by decade’s end.

Geography Analysis

New Zealand cybersecurity demand naturally clusters within the Auckland–Wellington–Christchurch triangle where headquarters, data centres, and hyperscaler regions reside. Auckland’s role as commercial epicentre generates high-volume MSSP contracts, particularly in transport logistics and retail. Wellington’s dense aggregation of ministries fuels year-round advisory pipelines as agencies align with the National Security Strategy. Christchurch leverages quake-hardened infrastructure and R&D precincts to pilot high-availability disaster-recovery blueprints, exporting those playbooks to Pacific neighbours.

Beyond metro hubs, regional councils in Bay of Plenty and Northland channel central-government co-funding into cyber ranging from secure Wi-Fi projects up to water-utility OT segmentation. Vendors with on-the-ground field engineers gain competitive edge because clients prize rapid site visits during incidents. Indigenous communities in Waikato and Taranaki are asserting control over tribal datasets, prompting on-premise sovereign micro-clouds housed within rohe. This localisation shifts a slice of recurring revenue from international hosts to regional integrators and data-centre co-los, subtly rebalancing the New Zealand cybersecurity market size map.

Cross-border ties with Australia foster trans-Tasman managed-service offerings that treat both nations as one logical coverage zone. While this expands export revenue for Kiwi providers, it also imports competition from Australian MSPs keen on New Zealand growth. Government procurement still privileges domestic capability where sensitive data is involved, but multinational enterprises increasingly negotiate single-contract SOC coverage spanning Sydney and Auckland nodes. The interplay of localisation mandates and regional service consolidation ensures geographic growth remains broad-based rather than strictly urban.

Competitive Landscape

Global platform players—IBM, Cisco, Palo Alto Networks—leverage expansive threat-intelligence feeds to pitch integrated stacks, securing multi-year deals with banks and utilities. Domestic specialists such as CyberCX, Kordia, and Datacom counter via deep regulatory fluency, local SOC presences, and culturally competent engagement. Kordia’s unification of cloud and cybersecurity teams in 2024 enabled bundled proposals that deliver lower total cost while ensuring single-throat accountability, a value proposition resonating with mid-market firms.

M&A momentum is rising: Being AI’s partial acquisition of Spectrum Consulting funds development of Lantern AI, a sovereign-cloud platform embedding Māori governance in its control fabric. Start-ups like Watchful attract venture capital for AI-native analytics that promise reduced mean-time-to-detect for SMEs [3]Watchful Security, “Seed Funding Announcement 2024,” watchful.co.nz. These new entrants spur incumbents to refresh product roadmaps, preserving healthy innovation churn inside the New Zealand cybersecurity market.

The acute talent gap forces service providers to automate tier-one SOC tasks; savings are reinvested into premium advisory and penetration-testing practices. Customers, wary of lock-in, value open-standards architectures that ease toolchain swaps. Consequently, cooperative ecosystems—not single-vendor dominance—define competition. With the top six suppliers aggregating 48% revenue, the landscape remains moderately concentrated yet sufficiently open to reward niche differentiation and cultural alignment.

New Zealand Cybersecurity Industry Leaders

CyberCX NZ Ltd.

Kordia Limited

Datacom Group Ltd.

Spark New Zealand Ltd.

PwC New Zealand

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cybersecurity platform Coro has made its debut in the Australian and New Zealand markets, sealing an exclusive distribution agreement with Bluechip Infotech.

- June 2025: In response to escalating cyberattacks in the region, Harbor Solutions has made its debut in Australia and New Zealand, teaming up with Rubrik to bolster cyber recovery efforts.

- January 2025: Dragos and Yokogawa integrate OT telemetry with threat intelligence, enhancing industrial-sector visibility

- November 2024: Kordia merges cloud and cyber divisions, reporting revenue growth to USD 149.1 million

New Zealand Cybersecurity Market Report Scope

The study analyzes the current market scenario and growth trends related to cybersecurity technology in New Zealand, which has emerged as one of the major hotspots for investments, aided by strong M&A activity, partnerships, and supportive governmental policies. The study tracks the country-level market dynamics and the major implementation use cases for cybersecurity.

The New Zealand cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the current New Zealand cybersecurity market size?

The New Zealand cybersecurity market size is estimated at USD 614.16 million for 2026.

How fast will the New Zealand cybersecurity market grow through 2031?

It is forecast to expand at a 7.28% CAGR, reaching USD 873.2 million by 2031.

Which segment holds the largest New Zealand cybersecurity market share?

Solutions remain the largest offering segment with 60.12% share in 2025, but services are growing faster.

Why is healthcare the fastest-growing vertical?

High-profile ransomware incidents and stringent privacy rules are driving healthcare security budgets up at 11.7% CAGR.

Page last updated on: