Fiber-Based Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 315.67 Billion |

| Market Size (2030) | USD 409.83 Billion |

| Growth Rate (2025 - 2030) | 5.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

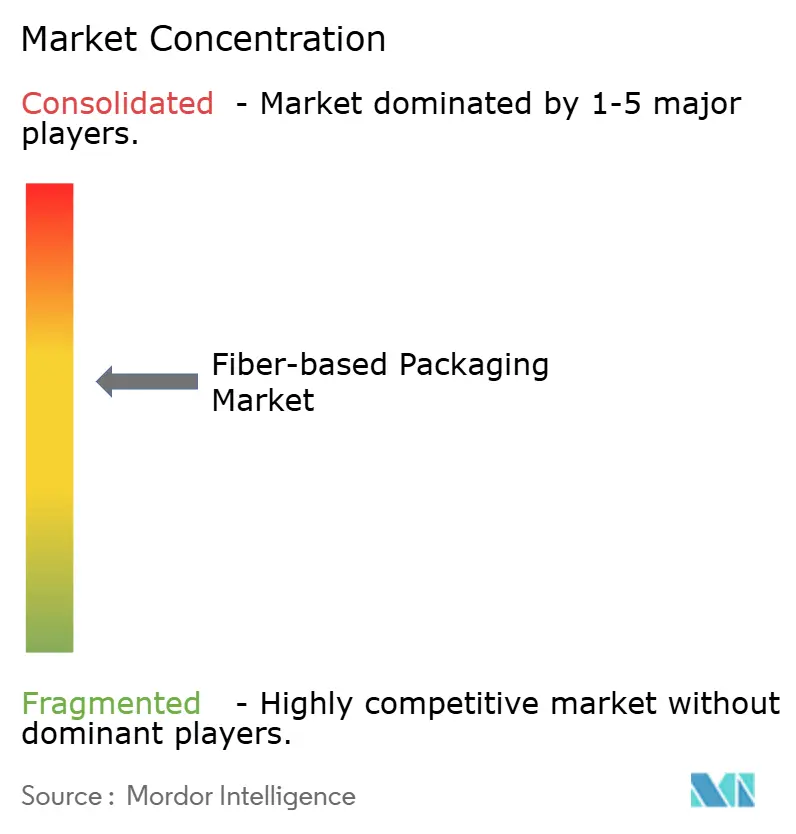

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fiber-Based Packaging Market Analysis by Mordor Intelligence

The fiber-based packaging market size reached USD 315.67 billion in 2025 and is forecast to expand to USD 409.83 billion in 2030, reflecting a 5.36% CAGR for the period. Regulatory pressure to curb single-use plastics, rapid growth in e-commerce, and brand-owner net-zero pledges are directing capital toward recyclable fiber substrates.[1]European Commission, “Packaging Waste,” environment.ec.europa.eu Meanwhile, advances in AI-guided structural design are reducing the intensity of raw materials and logistics costs. Supply-side investments in molded fiber technology, barrier coatings, and non-wood feedstocks are narrowing historical performance gaps against plastics; however, pulp price volatility and humidity-related barrier limitations continue to constrain margin expansion. Consolidation momentum among integrated players is reshaping competitive dynamics as the top five companies collectively hold around 35% of the fiber-based packaging market share. Emerging regional specialists remain attractive acquisition targets because they provide localized sourcing, proprietary forming know-how, and regulatory risk diversification.

Key Report Takeaways

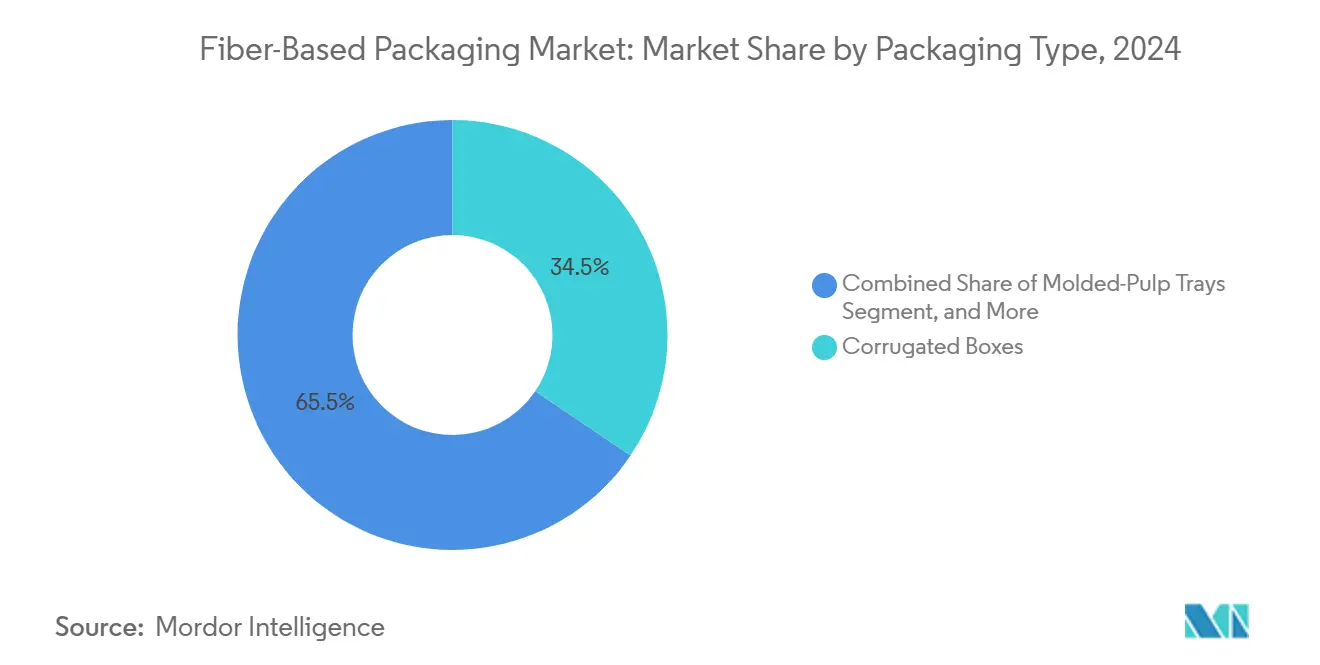

- By packaging type, the corrugated boxes segment captured 34.47% of the Fiber-Based Packaging Market share in 2024.

- By material type, the Fiber-Based Packaging Market size for molded fiber technologies is projected to grow at a 7.27% CAGR between 2025–2030.

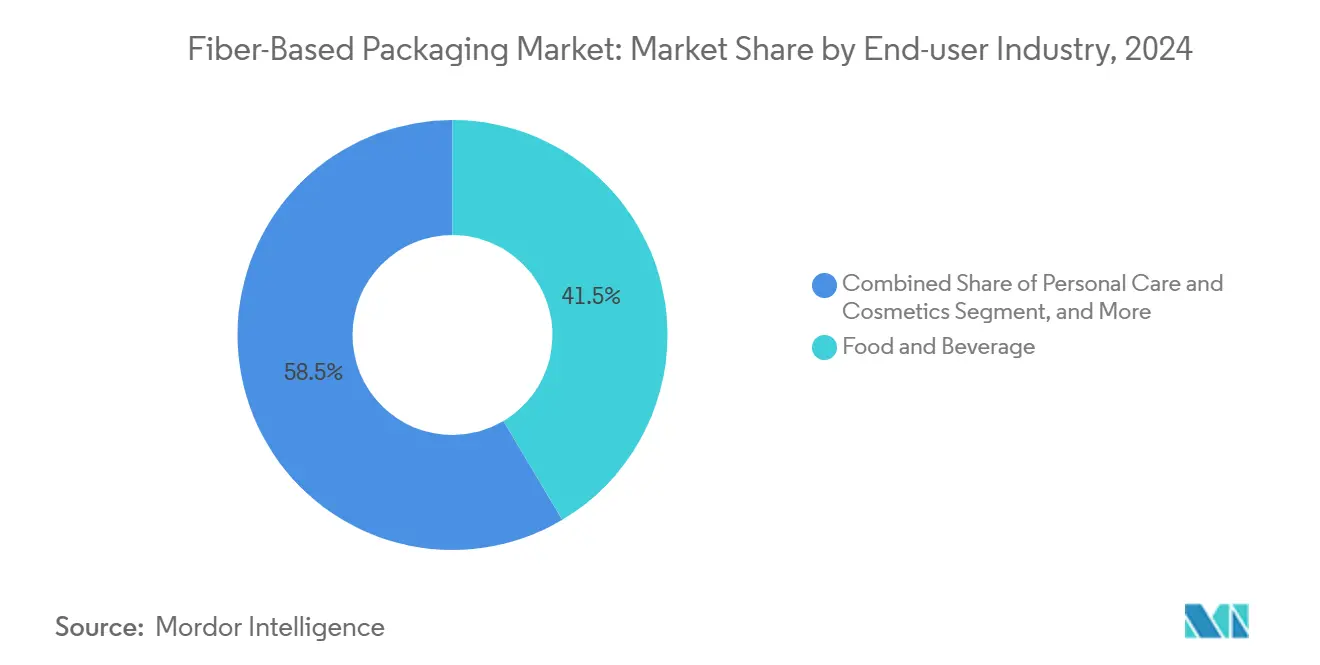

- By end-user industry, the food and beverage segment captured 41.47% of the Fiber-Based Packaging Market revenue share in 2024.

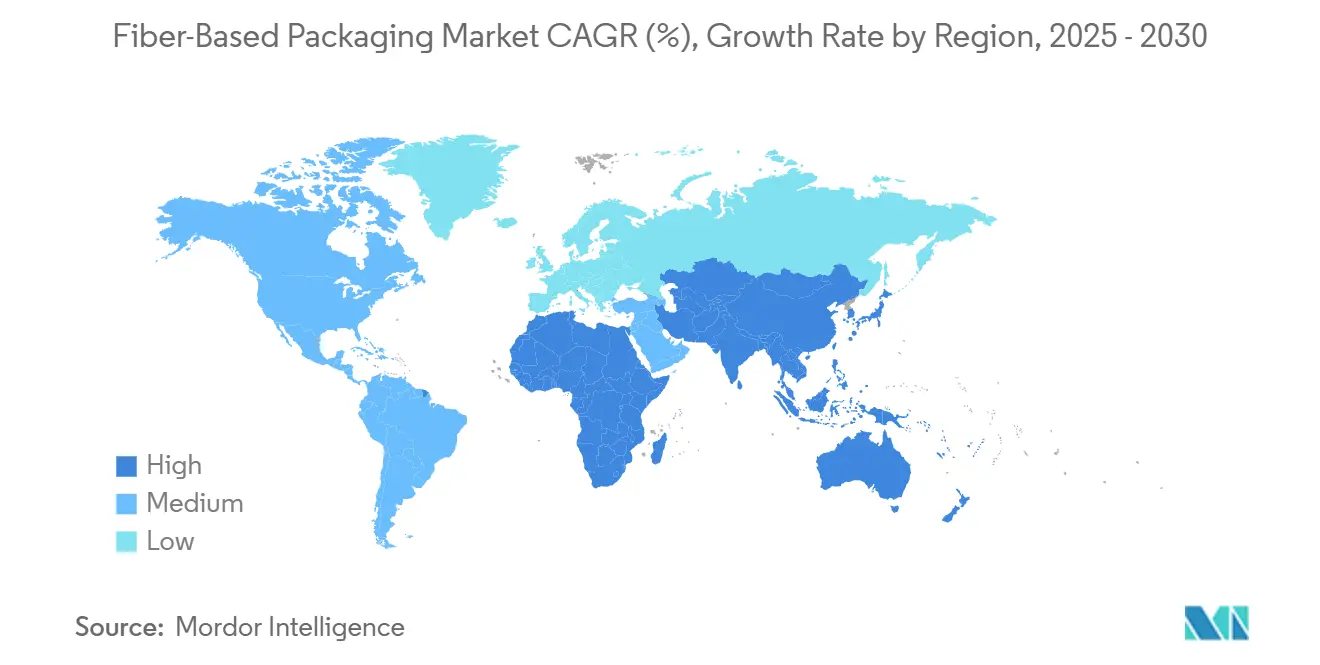

- By geography, the Fiber-Based Packaging Market size for Asia-Pacific is projected to grow at a 8.27% CAGR between 2025–2030.

Global Fiber-Based Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in single-use plastic bans and EPR mandates | +1.2% | Global, EU and North America leading | Short term (≤ 2 years) |

| Explosive e-commerce volume demanding durable fiber shippers | +0.8% | Global, APAC and North America core | Medium term (2-4 years) |

| Brand-owner net-zero targets accelerating paperization | +0.7% | Global, developed markets concentrated | Medium term (2-4 years) |

| AI-enabled design cutting fiber weight and logistics cost | +0.6% | North America and EU, spill-over to APAC | Long term (≥ 4 years) |

| Non-wood agro-waste fibers unlocking new capacity pools | +0.5% | APAC core, expansion to emerging markets | Long term (≥ 4 years) |

| Corporate carbon-pricing adoption boosting low-CO₂ substrates | +0.4% | Global, early adoption in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in single-use plastic bans and EPR mandates

Global legislative momentum accelerated after 2024, when California’s SB 54 and the European Union’s Packaging and Packaging Waste Regulation imposed aggressive recycling and reduction targets calrecycle.ca.gov environment.ec.europa.eu. The resulting fee spread USD 0.15-0.30 per package for non-recyclable formats versus USD 0.02-0.05 for recyclable fiber prompted procurement shifts across food service chains and fast-moving consumer-goods brands. More than 400 municipalities worldwide enacted outright bans on specific single-use plastics, instantly enlarging the addressable fiber-based packaging market. Compliance frameworks, such as ISO 14855 and ASTM D6868, have made certified compostability a purchasing prerequisite, redirecting R&D budgets toward fiber innovations. As regulatory coverage now spans over thirty jurisdictions, policy risk has shifted from possibility to inevitability, anchoring the medium-term demand baseline for fiber alternatives.

Explosive e-commerce volume demanding durable fiber shippers

Online retail sales hit USD 6.2 trillion in 2024, and marketplaces turned to algorithm-driven platforms like Amazon’s Package Decision Engine to down-gauge corrugated weight while preserving product integrity.[2]Amazon, “2023 Sustainability Report,” sustainability.aboutamazon.com Customized corrugated formats and molded fiber inserts displaced foam and plastic void fill, trimming damage rates to 0.8%. Cross-border e-commerce in Southeast Asia expanded at a 23% annual rate, favoring lightweight, fiber-based packaging market solutions that meet diverse recycling rules and lower freight costs. Advances in edge-crush strength and water-resistant coatings enabled the shipment of heavier or moisture-sensitive items without reverting to plastic. As omnichannel retailers align packaging KPIs with emissions goals, demand elasticity for recyclable substrates is rising even in price-sensitive categories.

Brand-owner net-zero targets accelerating paperization

Internal carbon pricing, averaging USD 25-30 per metric ton of CO₂, has been adopted by more than 1,400 corporations, making fiber’s 0.9 kg CO₂ advantage over plastic a direct cost lever. Consumer-goods leaders, such as Unilever and Nestlé, have embedded packaging emissions into supplier scorecards, triggering the accelerated qualification of molded fiber tubs, caps, and sleeves. Scope 3 disclosure mandates by securities regulators elevated packaging footprints to board-level priorities, leading brands to publicize milestones like “100% recyclable or compostable by 2025.” Consumer research showed willingness-to-pay premiums of 8-12% for certified sustainable packaging, strengthening revenue defense even as material costs fluctuate. The reputational upside has solidified paperization as a key component of multi-year procurement roadmaps.

AI-enabled design cutting fiber weight and logistics cost

Machine-learning optimization reduced corrugated board usage by 15-20% without sacrificing compression strength, as pilot lines transitioned to commercial-scale technology. Predictive analytics synchronized production schedules with e-commerce order spikes, cutting converter inventory by 25% and lowering working capital. Computer-vision quality systems achieved 99.7% defect-detection accuracy, reducing waste. These digital gains directly contribute to the total landed cost, thereby reinforcing competitiveness against plastic laminates. Over the long term, AI-guided micro-flute architectures and algorithmic flute orientation promise additional gram-level savings, a critical factor as pulp prices remain volatile.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pulp price volatility squeezing converter margins | -0.9% | Global, emerging markets most affected | Short term (≤ 2 years) |

| Moisture/grease barrier gaps versus plastics in humid markets | -0.6% | APAC and tropical regions | Medium term (2-4 years) |

| Cap-ex intensity of next-gen molded-fiber lines | -0.4% | Global, smaller players disproportionately | Long term (≥ 4 years) |

| Competition from recyclable mono-material flexible plastics | -0.3% | Developed markets with advanced recycling infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pulp price volatility squeezing converter margins

Hardwood pulp fluctuated between USD 580 and USD 720 per metric ton in 2024, eroding converters’ 8-12% EBITDA margins. Climatic disruptions, drought in Brazil, and Canadian wildfires curbed supply by 3.2%, while elevated natural-gas prices in Europe added USD 45-60 per metric ton to manufacturing overhead. Smaller converters lack hedging instruments and face quarterly price resets that test customer loyalty. The oligopolistic pulp supplier base constrains bargaining leverage, forcing downstream players to pursue vertical integration or long-term offtake contracts. Margin compression has already sparked wave-one consolidation, and further volatility could accelerate market exits among sub-scale operators.

Moisture/grease barrier gaps versus plastics in humid markets

Fiber substrates deliver only 65-75% of plastics’ moisture resistance, even with advanced coatings, which limits their adoption in tropical regions where the relative humidity exceeds 75%. Bio-based barriers that close the gap add USD 0.08-0.15 per square meter, a premium many food-service chains resist. Refrigerated distribution systems still rely on plastic laminates for shelf-life assurance, constricting fiber penetration in high-growth chilled categories. Research into cellulose nanofibers and plasma-enhanced layers indicates commercial readiness within two to three years; however, proof-of-scale pilots remain ongoing. Until cost-performance parity is achieved, humidity-exposed use cases will temper the trajectory of the fiber-based packaging market in equatorial economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Corrugated Strength Holds Even as Molded Innovation Gains Pace

Corrugated boxes accounted for 34.47% of the fiber-based packaging market size in 2024, reflecting their enduring dominance in omnichannel shipping. Their structural redesigns, micro-flute combinations, and algorithmic score-line placement cut basis weight by 12% and shaved freight spend for retailers. The fiber-based packaging market continues to benefit as molded-pulp trays advance at a 6.87% CAGR, propelled by plastic bans in QSR dine-in utensils and consumer electronics product launches that favor custom-fit packaging. Folding cartons register steady volume from confectionery, pharmaceuticals, and premium spirits, where printability and tamper evidence remain priorities. Paper bags and sacks are benefiting from legislative tailwinds stemming from grocery plastic-bag bans in more than 200 municipalities, although reuse cycles still lag behind aspirational targets.

Cost-effective 3D forming systems expanded geometric complexity in molded products, enabling nestable clamshells and intricate cushioning previously exclusive to plastic thermoforms. Precision hot-press drying reduced the moisture content, which in turn lowered warpage and enabled tighter dimensional tolerances essential for electronics. Bottles and cups represent an emerging niche; progress in internal barrier coatings suggests broader food-service substitution potential once cost normalization with PE-laminated paper obtains. Investment outlays of USD 8-12 million per molded line favor incumbents with scale, yet leasing models and government incentives in Asia-Pacific are gradually opening entry points for mid-tier converters.

By Material Type: Molded Fiber Disrupts Corrugated Leadership

Corrugated board retained 41.56% of the fiber-based packaging market share in 2024, underpinned by robust box plant networks and continuous flute-profile innovations that lifted edge-crush strength 15%. However, molded fiber is forecast to outpace the market with a 7.27% CAGR through 2030, reflecting its adoption in transit-protective inserts and shelf-ready trays, where dimensional stability now rivals that of EPS foam. Kraft paper remains pivotal for grocery, cement, and quick-service sacks, while cartonboard rides premiumization in cosmetics and luxury confectionery. Specialty composites integrating agro-waste fibers, such as wheat straw or bamboo, have emerged in Asia-Pacific mill trials, creating incremental capacity pools without adding to pulp-supply stress.

Hybrid structures that combine thin kraft outer plies with lightweight molded cores have shown 18% unit-weight savings and compliance with ASTM D5511 compostability criteria. Plasma and bio-resin barrier technologies are elevating grease resistance beyond 95 g m² KIT value, narrowing the functional gap with PE laminates. Circularity agendas favor materials that can be dismantled in conventional paper-mill pulpers; thus, investment intensity is shifting from single-use lamination lines to de-inkable water-based coating systems.

By End-user Industry: Premium Personal Care Holds the Upside

Food and beverage applications accounted for 41.47% of the fiber-based packaging market size in 2024, driven by public commitments to eliminate PFAS and municipal bans on polystyrene clamshells. Brand reformulations from global quick-service chains accelerated clamshell and cup trials that, once scaled, could unlock millions of incremental tons of fiber demand. Personal care and cosmetics register the most aggressive 7.79% CAGR as prestige and masstige brands deploy molded-fiber jars, sleeves, and inserts as tangible sustainability narratives. Consumer electronics have transitioned to anti-static molded fiber trays capable of dissipating charges below 200 V, safeguarding semiconductors during air freight.

Pharmaceutical adoption remains circumscribed by stability and moisture ingress requirements, but pilot programs in nutraceuticals demonstrate viability for non-critical SKUs. Omnichannel retail has catalyzed the deployment of smart packaging, incorporating QR codes printed directly on corrugated materials to facilitate reverse logistics authentication. The expanding fiber-based packaging industry is seeing cross-pollination in design motifs, embossed patterns, and soft-touch coatings transferred from luxury cartons to mainstream FMCG lines, raising aesthetic benchmarks.

Geography Analysis

North America retained 37.68% of the fiber-based packaging market share in 2024, catalyzed by state mandates including California’s EPR fee structures and PFAS prohibitions in food-contact packaging. Converter clusters in the U.S. Southeast leveraged integrated pulp mills to mitigate raw-material risk, while capital inflows from private equity financed upgrades to barrier coating.

Asia-Pacific is projected to post an 8.27% CAGR, the steepest regional growth, as China’s post-National Sword restrictions and India’s Single Use Plastic Management Rules funnel demand toward recyclable substrates.[3]Ministry of Environment, Forest and Climate Change, India, “Plastic Waste Management Amendment Rules 2022,” moef.gov.in Domestic pulp capacities expanded via joint ventures that valorize agro-residues, mitigating import dependence and foreign-exchange exposure. E-commerce giants in the region adopted right-sized corrugated formats to curb last-mile emissions, reinforcing volume expansion.

Europe maintains high single-digit growth as the Packaging and Packaging Waste Regulation drives 90% recycling-rate targets by 2029. Investments in molded fiber lines in Scandinavia and the Iberian Peninsula capitalize on the abundance of renewable energy and the integration of waste heat. South America and the Middle East, and Africa display emergent potential, driven by multinational brand compliance obligations and rising urban disposal fees that stigmatize single-use plastics.

Competitive Landscape

The fiber-based packaging market exhibits moderate fragmentation, with the top five players holding a roughly 35% combined share, leaving room for agile regional entrants. Vertical integration defines leading strategies: International Paper’s acquisition of Brazilian pulp assets secures upstream supply, while Smurfit Kappa’s 2024 merger with WestRock created a USD 34 billion revenue platform spanning forty countries. Mondi’s multi-site EUR 350 million (USD 385 million) coating investment underpins food-contact compliance without PFAS, positioning the company for premium margin segments.

Digitalization differentiates cost structures. AI-enabled predictive maintenance reduced unplanned downtime by 18% at early-adopter mills, resulting in faster customer lead times. Intellectual property activity remains vigorous; WIPO filings for barrier-coating and forming patents increased 23% year-over-year in 2024, signaling sustained innovation budgets despite pulp cost pressures.

Regional specialists exploit regulatory timing gaps: Indian molded-fiber start-ups leverage domestic single-use bans, while Japanese paper majors collaborate with electronics OEMs on anti-static solutions. Capital requirements of USD 15-25 million per next-generation molded line are nudging smaller converters toward joint ventures or licensing arrangements. The resultant deal pipeline suggests consolidation will continue, especially where currency weakness inflates imported pulp costs and compresses standalone profitability.

Fiber-Based Packaging Industry Leaders

International Paper Company

Smurfit WestRock plc

Mondi plc

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Smurfit WestRock completed its USD 20 billion merger, creating the world’s largest integrated packaging company with USD 34 billion revenue and operations across forty countries.

- September 2024: International Paper announced a USD 1.2 billion Brazilian pulp-mill expansion adding 1.5 million metric tons of annual capacity by 2027.

- August 2024: Mondi invested EUR 350 million (USD 385 million) in barrier-coating technology across European sites to eliminate PFAS in molded-fiber food packaging.

- July 2024: Stora Enso launched commercial production of micro-fibrillated cellulose coatings that improve corrugated moisture resistance by 90%.

Global Fiber-Based Packaging Market Report Scope

| Corrugated Boxes |

| Folding Cartons |

| Paper Bags and Sacks |

| Molded-Pulp Trays and Clamshells |

| Bottles and Cups |

| Other Packaging Types |

| Corrugated |

| Kraft Paper |

| Molded Fiber |

| Cartonboard/Boxboard |

| Specialty Fiber |

| Other Material Types |

| Food and Beverage |

| Consumer Electronics |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| E-commerce and Retail |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Type | Corrugated Boxes | ||

| Folding Cartons | |||

| Paper Bags and Sacks | |||

| Molded-Pulp Trays and Clamshells | |||

| Bottles and Cups | |||

| Other Packaging Types | |||

| By Material Type | Corrugated | ||

| Kraft Paper | |||

| Molded Fiber | |||

| Cartonboard/Boxboard | |||

| Specialty Fiber | |||

| Other Material Types | |||

| By End-user Industry | Food and Beverage | ||

| Consumer Electronics | |||

| Personal Care and Cosmetics | |||

| Pharmaceuticals | |||

| E-commerce and Retail | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the fiber-based packaging market?

The market stands at USD 315.67 billion in 2025 and is projected to reach USD 409.83 billion by 2030.

How fast is the sector growing?

It is forecast to expand at a 5.36% CAGR through 2030, supported by regulatory mandates and e-commerce demand.

Which packaging type holds the largest share?

Corrugated boxes lead with 34.47% revenue share in 2024 thanks to omnichannel shipping needs.

Which region offers the highest growth potential?

The Asia-Pacific region is set to grow at an 8.27% CAGR through 2030, driven by the implementation of single-use plastic restrictions in China and India.

What are the main restraints limiting adoption?

Pulp price volatility and gaps in moisture-barrier performance compared to plastics remain key challenges.

Who are the leading companies in the space?

International Paper, Smurfit WestRock, Mondi, Stora Enso, and Georgia-Pacific collectively command about 35% of global revenue.

Page last updated on: