Composite Cans And Fiber Drums Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

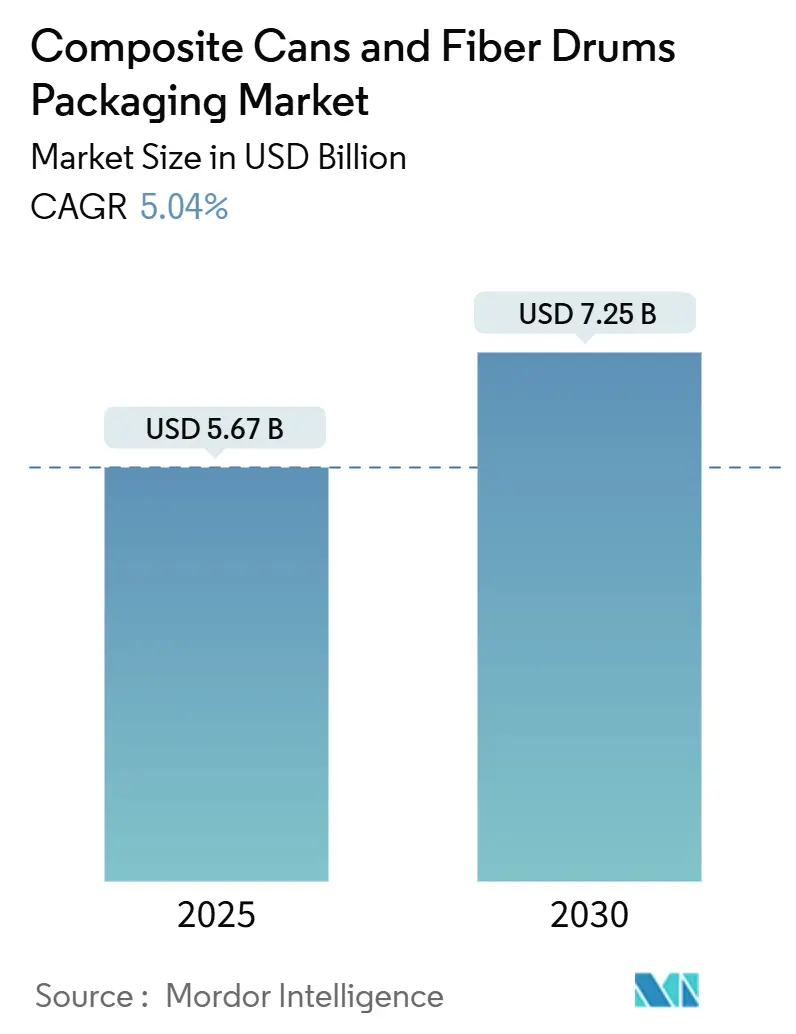

| Market Size (2025) | USD 5.67 Billion |

| Market Size (2030) | USD 7.25 Billion |

| Growth Rate (2025 - 2030) | 5.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Composite Cans And Fiber Drums Packaging Market Analysis by Mordor Intelligence

The Composite Cans and Fiber Drums Packaging Market size is estimated at USD 5.67 billion in 2025, and is expected to reach USD 7.25 billion by 2030, at a CAGR of 5.04% during the forecast period (2025-2030). This trajectory reflects how brand owners align packaging specifications with sustainability mandates while minimizing logistics costs. E-commerce growth, regulatory curbs on single-use plastics, and rising consumer preference for curbside recyclable formats converge to keep demand buoyant, even as raw material prices fluctuate. Composite containers deliver high axial strength at a low gram weight, enabling freight cost reductions that protect brand margins when postal dimensional-weight rules become stricter. Advances in barrier coatings now enable fiber-based structures to meet the performance-life requirements of metals and plastics, opening up premium use cases in cosmetics, nutraceuticals, and functional foods. Incumbent suppliers widen their moat by integrating upstream recycled-fiber sourcing, stabilizing input prices, and accelerating the automation of right-sized production lines near fulfillment centers, which shortens lead times and lowers inventory risk.

Key Report Takeaways

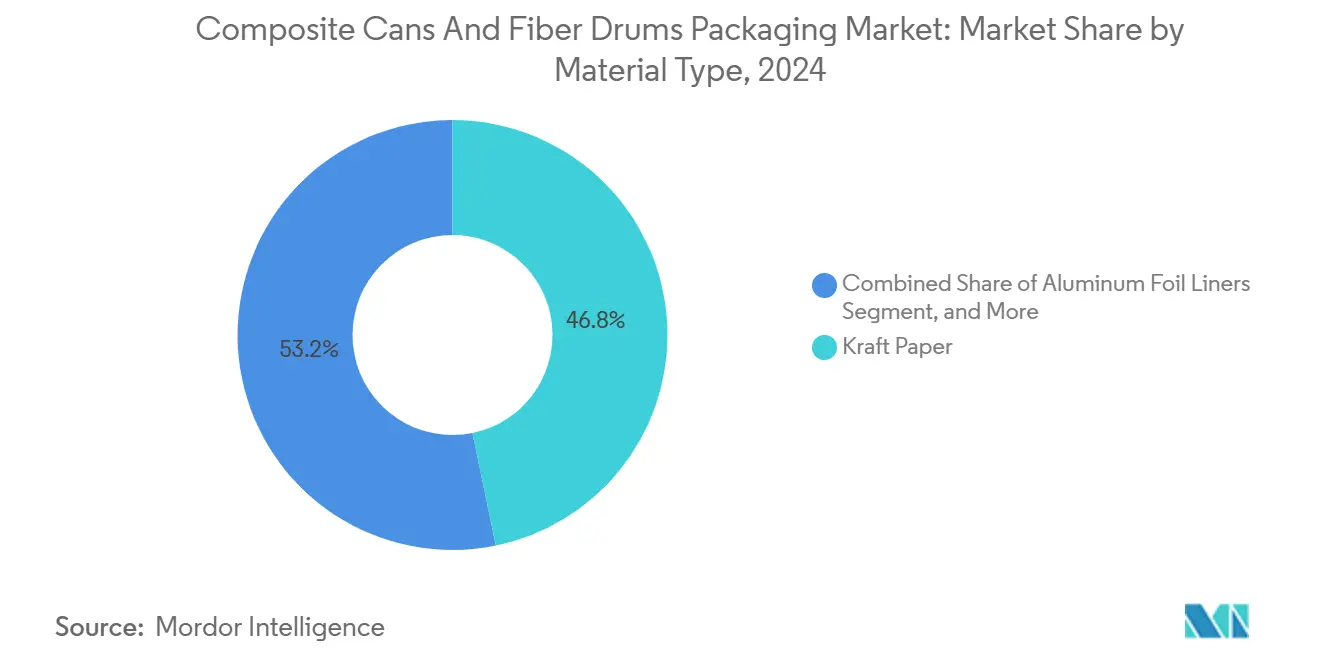

- By material type, kraft paper captured 46.78% of the composite cans and fiber drums packaging market share in 2024.

- By capacity, the composite cans and fiber drums packaging market size for up to 10 liters is projected to grow at a 6.78% CAGR between 2025–2030.

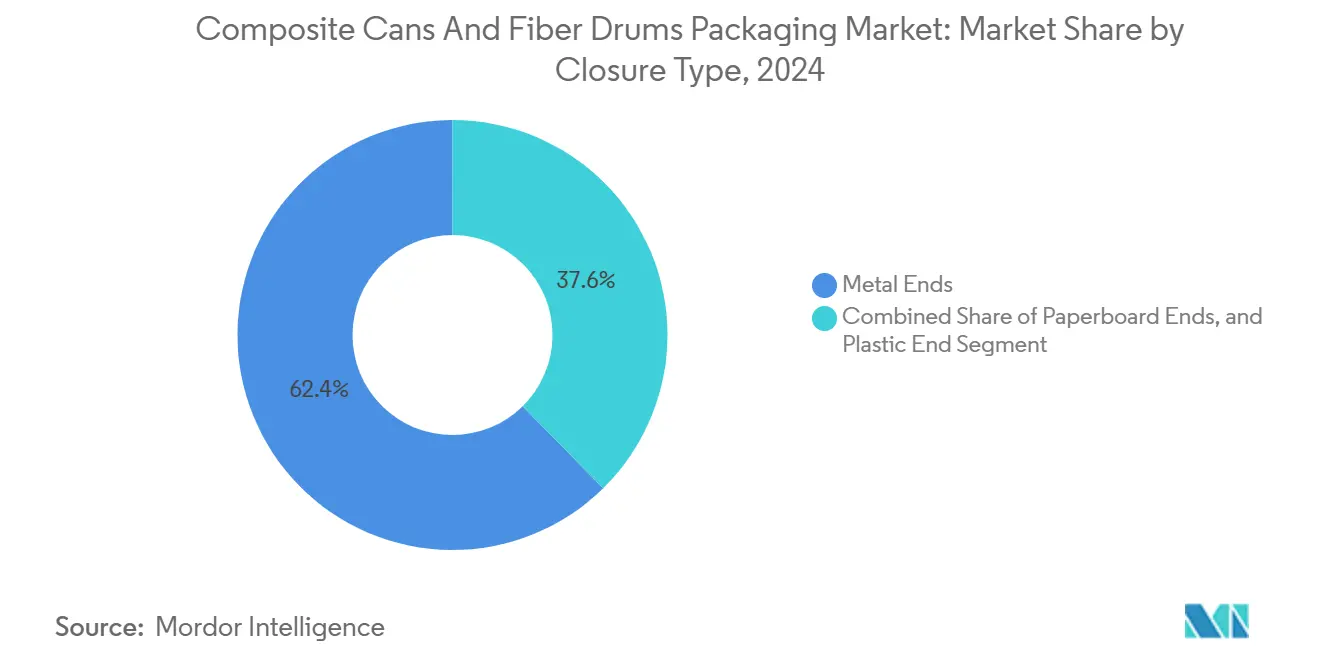

- By closure type, metal ends captured 62.37% of the composite cans and fiber drums packaging market share in 2024.

- By end-use industry, the composite cans and fiber drums packaging market size for cosmetics and personal care is projected to grow at a 8.16% CAGR between 2025–2030.

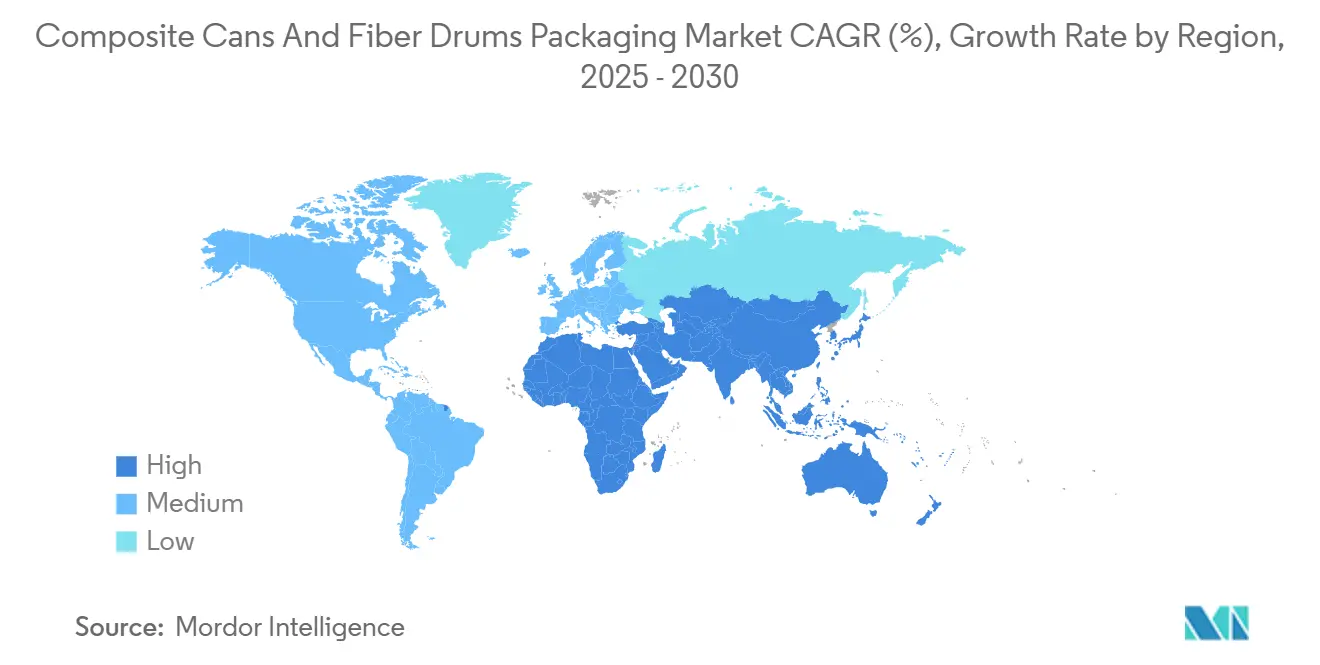

- By geography, Asia-Pacific captured 41.45% of the composite cans and fiber drums packaging market share in 2024.

Global Composite Cans And Fiber Drums Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce parcel volumes | +1.2% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Shift toward curbside-recyclable packaging | +0.9% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Dim-weight postal cost savings | +0.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Plastic-reduction regulations and retailer mandates | +1.1% | Europe and North America, spillover to Middle East and Africa | Medium term (2-4 years) |

| On-site automated right-size mailer production | +0.6% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Honeycomb cushioning innovations with lower CO₂ | +0.4% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in E-Commerce Parcel Volumes

Global online retail is forecast to exceed one-quarter of all sales by 2027, driving unprecedented parcel throughput and forcing fulfillment centers to prioritize right-sized packaging solutions. Cylindrical composite cans offer a superior strength-to-weight ratio, allowing shippers to reduce package volume without compromising protective performance. Brands in personal care, specialty foods, and nutraceuticals now rely on automated can-forming equipment that receives real-time order dimensions and produces custom heights on demand, eliminating void fill and cutting freight spend. The format’s rigidity also lowers product damage rates, which carries a significant cost in reverse-logistics-intensive e-commerce channels. As postal operators worldwide extend dimensional-weight pricing to smaller thresholds, composite cans capture volume from oversized corrugated boxes that no longer meet cost-to-serve requirements.

Shift Toward Curbside-Recyclable Packaging

The European Union’s Packaging and Packaging Waste Regulation sets a 90% recyclability target by 2030, prompting brand owners to transition from multilayer plastics to fiber-dominant structures that integrate seamlessly into municipal waste collection streams.[1]Source: European Commission, “Packaging and Packaging Waste Regulation,” EUROPA.EU Major U.S. retailers reinforce the push through supplier scorecards that award shelf space to products shipped in recyclable packaging. Because composite cans combine paperboard body walls with single-material closures, they meet design-for-recycling criteria and avoid the cost of specialty recovery systems. Consumer research shows that recyclability claims now rival price in household purchase decisions, so marketers leverage the can’s smooth, printable surface to highlight environmental credentials. As regulations tighten beyond Europe, early-stage pilots in India and Brazil suggest that developing markets will replicate curbside collection incentives, expanding the global addressable base for fiber-centric cans.

Dim-Weight Postal Cost Savings

Carriers such as the United States Postal Service price parcels on whichever is greater—actual mass or calculated volume, and they lowered divisor thresholds in 2024, effectively raising fees on low-density shipments. A cylinder encloses a given volume with less surface area than a rectangular box, so composite cans routinely cut dimensional weight by up to 15%. This advantage is particularly pronounced for high-margin items, such as skincare creams, where a compact pack not only preserves product aesthetics but also keeps shipping charges in check. Fulfillment operations integrate volumetric algorithms that flag SKUs eligible for cylindrical conversion, creating predictable demand for standardized diameters supplied in high cadence. Because logistics savings accrue immediately, converters find it easier to pass modest material premiums through to the cost of goods.

Plastic-Reduction Regulations and Retailer Mandates

California Senate Bill 54 requires a 25% reduction in single-use plastic packaging by 2032 and extends producer responsibility fees to non-recyclable formats. Global consumer-goods leaders have echoed the policy, pledging to replace or redesign hard-to-recycle packaging. Fiber-based composite cans meet these pledges while maintaining barrier performance through thin aluminum or bio-based coatings, thereby avoiding the use of multilayer plastic laminates. Retailers use packaging scorecards that penalize mixed-material packs lacking end-of-life pathways, so suppliers adopting composite cans gain a listing advantage. As mandatory take-back schemes proliferate across Canada and parts of Europe, the cost of non-compliant plastic rises, making composite cans a financially attractive alternative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled paper feedstock price volatility | -0.7% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Moisture-resistance limitations vs. poly mailers | -0.5% | Global, acute in humid climates in Asia-Pacific and Africa | Medium term (2-4 years) |

| Price competition by poly-bubble mailers | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Postal-sorting jams and surcharge risks | -0.3% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recycled Paper Feedstock Price Volatility

Spot recycled-fiber prices swung 35% in 2024 as collection rates stagnated and alternative corrugated demand surged, lifting input costs for can winders. China’s import restrictions further tightened global supply, compelling smaller converters to buy on spot markets at unfavorable rates. Vertically integrated majors, such as Sonoco, own reclaim plants, which buffer volatility and widen cost advantages. Energy inflation compounds uncertainty because recovered-fiber pulping is a thermally intensive process. When mills pass higher pulp prices through to converters, margin pressure slows the adoption of new technologies in price-sensitive emerging markets.

Moisture-Resistance Limitations vs. Poly Mailers

Uncoated kraft absorbs ambient humidity, which can lead to panel swell or delamination during ocean freight and tropical warehousing. While thin polyethylene terephthalate or polylactic acid layers provide a barrier, they increase material costs by 20-30% and may complicate recyclability. Electronics and pharmaceutical fillers, which require desiccant-grade packaging, often continue to use poly mailers or foil pouches for added peace of mind. Research into cellulose nanomaterial coatings promises moisture vapor transmission rates approaching those of plastics, yet scale-up costs remain prohibitive. Until bio-based barriers reach parity economics, moisture-sensitive verticals will temper overall growth momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Kraft Paper Dominance Faces Barrier Innovation

Kraft paper delivered 46.78% of 2024 revenue thanks to established supply networks and competitive cost structures that align with sustainability pledges. Its high tear index and printability enable converters to achieve retail shelf aesthetics while maintaining a low grammage. The composite cans market size for kraft-based variants is projected to climb steadily as regulatory favor tilts toward renewable inputs, although share growth moderates as barrier-critical niches demand advanced liners. Aluminum-foil-lined constructions, although comprising a smaller base, are projected to register a 7.34% CAGR to 2030, as they unlock the cosmetics, coffee, and infant formula segments that require oxygen and moisture protection. Producers often integrate ultrathin foils, typically below 12 µm, to reduce material expenditure while maintaining hermetic seals, especially when paired with induction-sealed metal ends.

Bleached paperboard captures designers seeking a bright, uniform surface for luxury giftable SKUs. Although the substrate commands a price premium, marketers justify the outlay through enhanced brand perception and high-definition flexo graphics. Plastic films retain niche relevance where drop-test compliance or oil resistance outweighs the demands for recyclability. Bio-based adhesive chemistries and waterborne primers broaden the renewable narrative; however, they must meet bond strength specifications set by food-safety regulators. The European Single-Use Plastics Directive presses material engineers to decrease polymer layer thickness, prompting accelerated R&D into water-borne and cellulose-derived dispersion coatings that uphold barrier integrity while keeping the pack in the paper recycling stream.[2]Source: European Environment Agency, “Single-Use Plastics Directive Implementation Report,” EEA.EUROPA.EU

By Capacity: Small-Format Acceleration Challenges Mid-Range Leadership

Mid-capacity fiber drums, ranging from 26 liters to 50 liters, claimed a 39.78% share in 2024, as chemical, agricultural, and bulk food producers have decades of design validation experience with this footprint. Older filling lines, pallet patterns, and warehouse racking are designed to these dimensions, resulting in high switching costs that preserve incumbent volumes. Nevertheless, e-commerce demand for subscription boxes and direct-to-consumer shipping propels the market for up to 10-liter cans at a 6.78% CAGR through 2030. Small diameters reduce void fill, raise cube efficiency, and delight consumers who perceive compact packaging as eco-friendly. Automated right-size platforms drive procurement teams to standardize on a library of narrow diameters that can be sawn to precise heights on the fly, cutting SKUs and holding costs.

Large drums exceeding 50 liters remain prevalent in petrochemical intermediates and seed-treatment concentrates, where forklift handling efficiency outweighs concerns about pallet density. Their high wall thickness delivers exceptional stacking strength, though growth is slower because substitution by returnable plastic intermediate bulk containers partially offsets new demand. The 11-25 liter band plays in premium consumer channels, including protein blends and specialty coffee clubs, where pack size cues product exclusivity. Research at TU Dresden demonstrates adhesive-free honeycomb cores can shave 25% weight without sacrificing crush resistance, a breakthrough that could propel light-gauge formats into mainstream industrial adoption.

By Closure Type: Metal Ends Stability Meets Paperboard Sustainability

Metal ends accounted for 62.37% of sales in 2024, as they deliver unrivaled sealing torque and tamper-evident features crucial to high-value powders and desiccated ingredients. Their compatibility with induction linings extends shelf life and supports hot-fill processes, making them indispensable in nutraceutical and foodservice channels. However, the mixed-material nature complicates municipal recycling streams, prompting CSR-driven brands to explore single-material solutions. Paperboard ends are forecast to rise 7.28% annually to 2030 as laminated tear-tape membranes and sonically welded pull tabs close the performance gap. By maintaining full fiber construction, these closures satisfy retailer scorecards that penalize packages requiring material separation.

Plastic ends, typically made from high-density polyethylene or polypropylene, serve low-margin mass-market lines where seal performance requirements are modest. Regulatory headwinds from plastic-reduction acts limit their upside, though they remain cost leaders in climates where moisture barrier trumps recycling rhetoric. Guala Closures’ move into pharmaceutical snap-fit systems illustrates its continued investment in precise dosing spouts and child-resistant features, which command premium unit margins. Fibrous lid substrates coated with bio-based dispersion barriers are in pilot scale, signaling a medium-term migration path toward mono-material cans that meet both performance and recycling mandates.

By End-Use Industry: Food-Beverage Stability Contrasts Personal-Care Acceleration

Food and beverage fillers accounted for 37.14% of the global volume in 2024, driven by their long-standing use in powdered dairy, drink mixes, and dehydrated soups. Specifications for oxygen and moisture ingress are well understood, enabling high line efficiencies and low scrap rates. This anchor segment generates steady replacement demand, even during economic slowdowns, thanks to pantry-stocking behavior. The composite cans market size for food-grade SKUs is forecast to advance modestly, constrained mainly by the maturity of traditional categories. In contrast, cosmetics and personal care formulations are projected to grow at an 8.16% CAGR to 2030, as prestige brands utilize fiber-based cylinders to convey clean-beauty positioning. Embossed paper wraps and soft-touch coatings provide sensory cues that plastic jars cannot replicate, while maintaining a similar carbon footprint.

Household chemicals, from polishes to insecticides, exploit the rigid wall construction to prevent denting during transport, while agriculture applications rely on moisture-resistant liners to protect micronutrient seed coatings. Pharmaceutical fillers evaluate composite cans when humidity-barrier performance meets USP monograph standards, primarily for effervescent tablets and probiotic powders. Electronics accessories and hobby products, such as specialty paints, round out a diverse tail where print real estate functions as a billboard, turning every shipment into a marketing touchpoint.

Geography Analysis

The Asia-Pacific region led with 41.45% of global revenue in 2024 and is projected to track a 7.68% CAGR as manufacturers in China, India, and Thailand scale modern winding lines that convert locally sourced kraft into export-ready packaging. Government incentives under China’s circular-economy roadmap and India’s extended producer responsibility rules create a demand pull for recyclable formats that composite cans fulfill. Regional e-commerce giants capitalize on low labor costs and proximity to consumer clusters to introduce fiber drums for bulk staples, such as protein powders, thereby accelerating domestic adoption. Local converters also export cans to Oceania and the Middle East, taking advantage of low shipping rates and duty-free ASEAN agreements.

North America remains an innovation hotbed where fulfillment networks invest in right-size automation that pairs well with variable-height cylinders. The region’s mature retail landscape prioritizes shelf differentiation, and U.S. plastic-reduction legislation is expected to boost fiber adoption among national brands. Canada’s carbon pricing regime favors material-efficient pack designs; thus, brand owners integrate life-cycle assessment data into packaging selection. Europe posts steady growth anchored by stringent waste directives and robust curbside collection that minimize consumer confusion at end-of-life. Germany, France, and the Nordics deploy deposit-return systems that financially reward brand owners for mono-material formats.

South America’s emerging middle class drives packaged food upgrades, especially in Brazil, where state bans on expanded-polystyrene trays spill over into broader plastic-reduction campaigns. Composite cans gain share in powdered chocolate drinks and instant coffee, aided by established aluminum-mining clusters that supply cost-competitive foil liners. The Middle East and Africa, though a smaller base, see strong adoption in UAE specialty food exports and South African personal-care lines, where retailers differentiate on sustainability claims. Infrastructure projects such as Kenya’s expanded port facilities cut inbound freight cost for wound-paper cores, improving local economics for converters.

Competitive Landscape

The composite cans market features moderate fragmentation. Sonoco Products, Greif, and Mondi utilize captive recycled-fiber mills and multi-continent converting plants to ensure supply consistency, a crucial factor for multinational CPG procurement teams. Their scale allows unit cost advantages and funds R&D into water-based barrier technologies that future-proof portfolios against plastic levy escalation. Industry consolidation accelerated: International Paper purchased DS Smith for USD 7.2 billion, forming a cross-Atlantic giant with expanded composite capacity. Meanwhile, Smurfit and WestRock combined their operations to unlock in procurement and digital printing.

Mid-cap specialists, such as VPK Group and Corex, focus on narrow-format, spirally wound cans for nutraceutical and cosmetics applications, where quick art changeovers and tight tolerance lead times secure premium pricing.[3]Source: VPK Group, “Tupak Composite Packaging Acquisition,” VPKGROUP.COM Venture-backed start-ups experiment with cellulose-nanomaterial coatings and induction-sealable paper ends, targeting blue-ocean opportunities in pharmaceutical and moisture-sensitive food niches. Strategic priorities across the top tier include installing high-speed robotic palletizers, integrating RFID for enhanced inventory visibility, and adopting carbon capture credits to meet the Scope 3 reporting demands of global clients.

Patent filings highlight honeycomb-core light-weighting, extrusion-bonded bio-adhesives, and AI-driven height-cut optimization. Suppliers enter joint development agreements with barrier-chemistry specialists to fast-track commercialization. In Asia-Pacific, domestic leaders capitalize on proximity to petrochemical clusters for competitive resin supply, though they face rising wage costs that erode historical labor advantages. Overall, competition centers on balancing unit economics with recyclability; players that can decouple performance from polymer content stand to capture outsized share as sustainability standards intensify.

Composite Cans And Fiber Drums Packaging Industry Leaders

Sonoco Products Company

Greif, Inc.

Mondi plc

Smurfit WestRock plc

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Mondi completed its EUR 634 million (USD 692 million) acquisition of Schumacher Packaging assets, boosting European composite can capacity to serve premium consumer goods.

- September 2025: International Paper finalized its USD 7.2 billion acquisition of DS Smith, creating the world’s largest packaging group with expanded composite capability.

- August 2025: VPK Group acquired Tupak’s composite can operations for EUR 85 million (USD 93 million), adding narrow-diameter cylinders for luxury food brands.

- July 2025: The Smurfit WestRock merger gained final regulatory clearance, unlocking joint R&D resources for fiber-based barrier solutions.

Global Composite Cans And Fiber Drums Packaging Market Report Scope

| Kraft Paper |

| Bleached Paperboard |

| Aluminum Foil Liners |

| Plastic Films |

| Adhesives and Resins |

| Up to 10 Liters |

| 11-25 Liters |

| 26-50 Liters |

| Above 50 Liters |

| Metal Ends |

| Plastic Ends |

| Paperboard Ends |

| Food and Beverages |

| Cosmetics and Personal Care |

| Consumer Goods |

| Agriculture |

| Pharmaceuticals |

| Other End-use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | Kraft Paper | ||

| Bleached Paperboard | |||

| Aluminum Foil Liners | |||

| Plastic Films | |||

| Adhesives and Resins | |||

| By Capacity | Up to 10 Liters | ||

| 11-25 Liters | |||

| 26-50 Liters | |||

| Above 50 Liters | |||

| By Closure Type | Metal Ends | ||

| Plastic Ends | |||

| Paperboard Ends | |||

| By End-use Industry | Food and Beverages | ||

| Cosmetics and Personal Care | |||

| Consumer Goods | |||

| Agriculture | |||

| Pharmaceuticals | |||

| Other End-use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the composite cans market in 2025?

The composite cans market reached USD 5.67 billion in 2025 and is forecast to hit USD 7.25 billion by 2030, reflecting a 5.04% CAGR.

Which material leads to current adoption?

Kraft paper maintains its leadership with a 46.78% revenue share, thanks to its cost efficiency, printability, and established recycling infrastructure.

Why are brands shifting from plastic closures to paperboard ends?

Paperboard ends enable a mono-material pack that facilitates curbside recycling, helping brands meet retailer scorecards and upcoming plastic reduction regulations.

What drives the fastest growth segment?

Cosmetics and personal care fillings are expanding at an 8.16% CAGR because premium brands are leveraging fiber cans to signal sustainability and elevate shelf appeal.

Which region shows the highest growth?

The Asia-Pacific region posts the fastest regional expansion at a 7.68% CAGR, owing to its large consumer bases, rapid e-commerce adoption, and supportive circular economy policies.

How do dimensional weight charges influence packaging choice?

Carrier pricing based on parcel volume makes cylindrical composite cans more attractive, as they can reduce dimensional weight by up to 15%, directly lowering freight costs.

Page last updated on: