United States Pouch Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

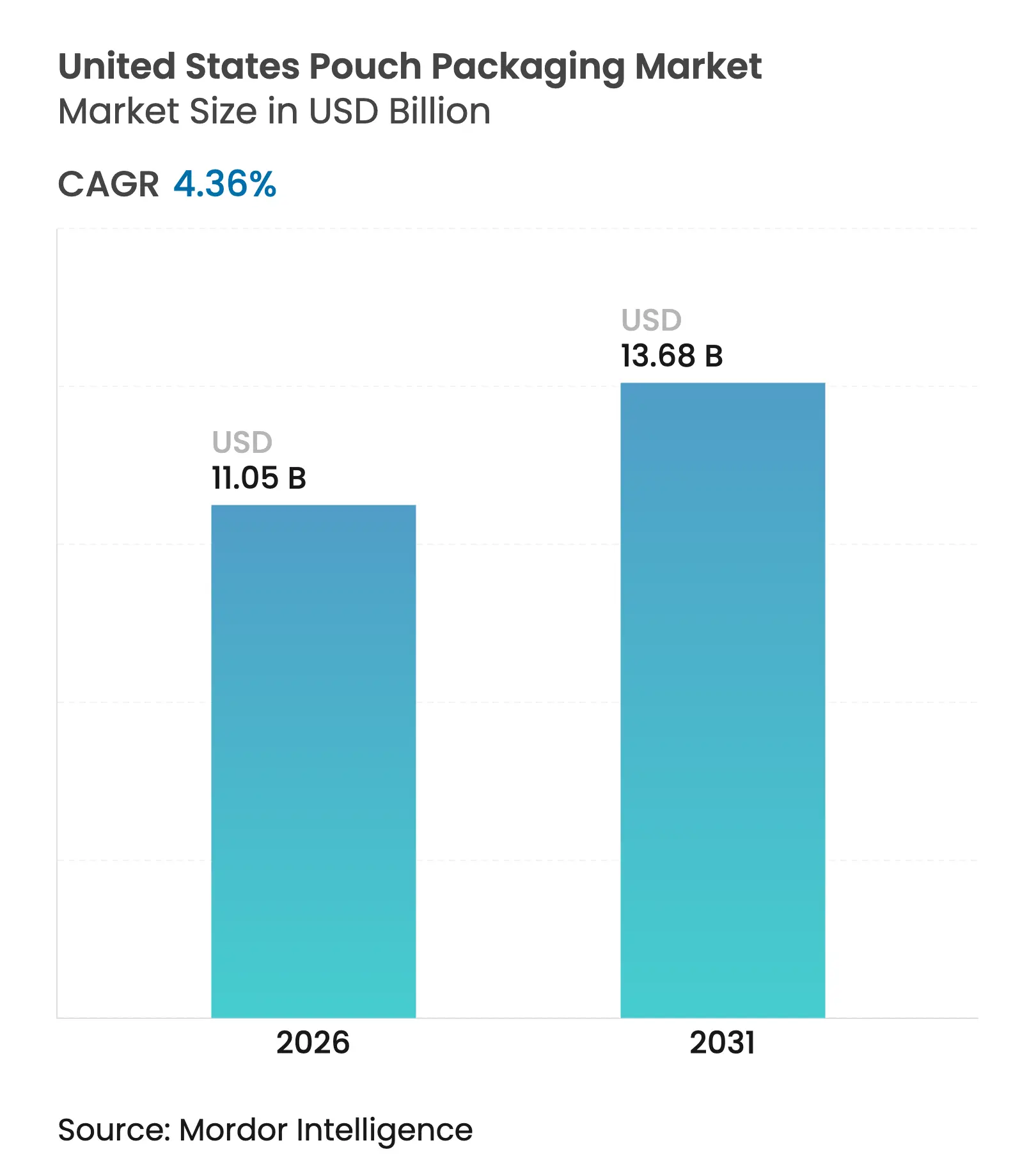

| Market Size (2026) | USD 11.05 Billion |

| Market Size (2031) | USD 13.68 Billion |

| Growth Rate (2026 - 2031) | 4.36 % CAGR |

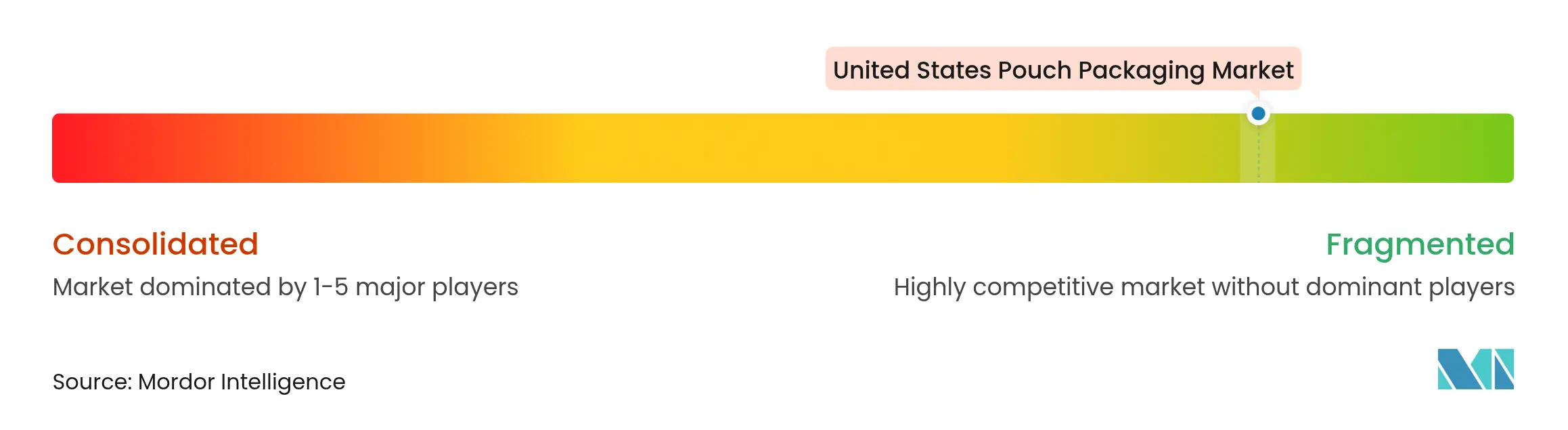

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

United States Pouch Packaging Market Analysis by Mordor Intelligence

The United States pouch packaging market size is expected to grow from USD 10.59 billion in 2025 to USD 11.05 billion in 2026 and is forecast to reach USD 13.68 billion by 2031 at 4.36% CAGR over 2026-2031. Rising compliance costs under California’s Extended Producer Responsibility (EPR) law, rapid growth of e-commerce, and the continued shift from rigid to flexible formats are reshaping material choices, production processes, and pricing strategies. Digital-print capacity, mono-material film development, and recycled-content integration have become core investment themes as converters balance sustainability mandates with brand owners’ shelf-impact demands. Meanwhile, supply-chain volatility in polyethylene and polypropylene is accelerating vertical integration and consolidation, enabling scale players to hedge resin risk and secure feedstock. These factors, coupled with the growth of refill formats and high-barrier retort pouches, point to a market that is maturing beyond traditional snack applications and expanding into personal care, pet nutrition, and defense rations.

Key Report Takeaways

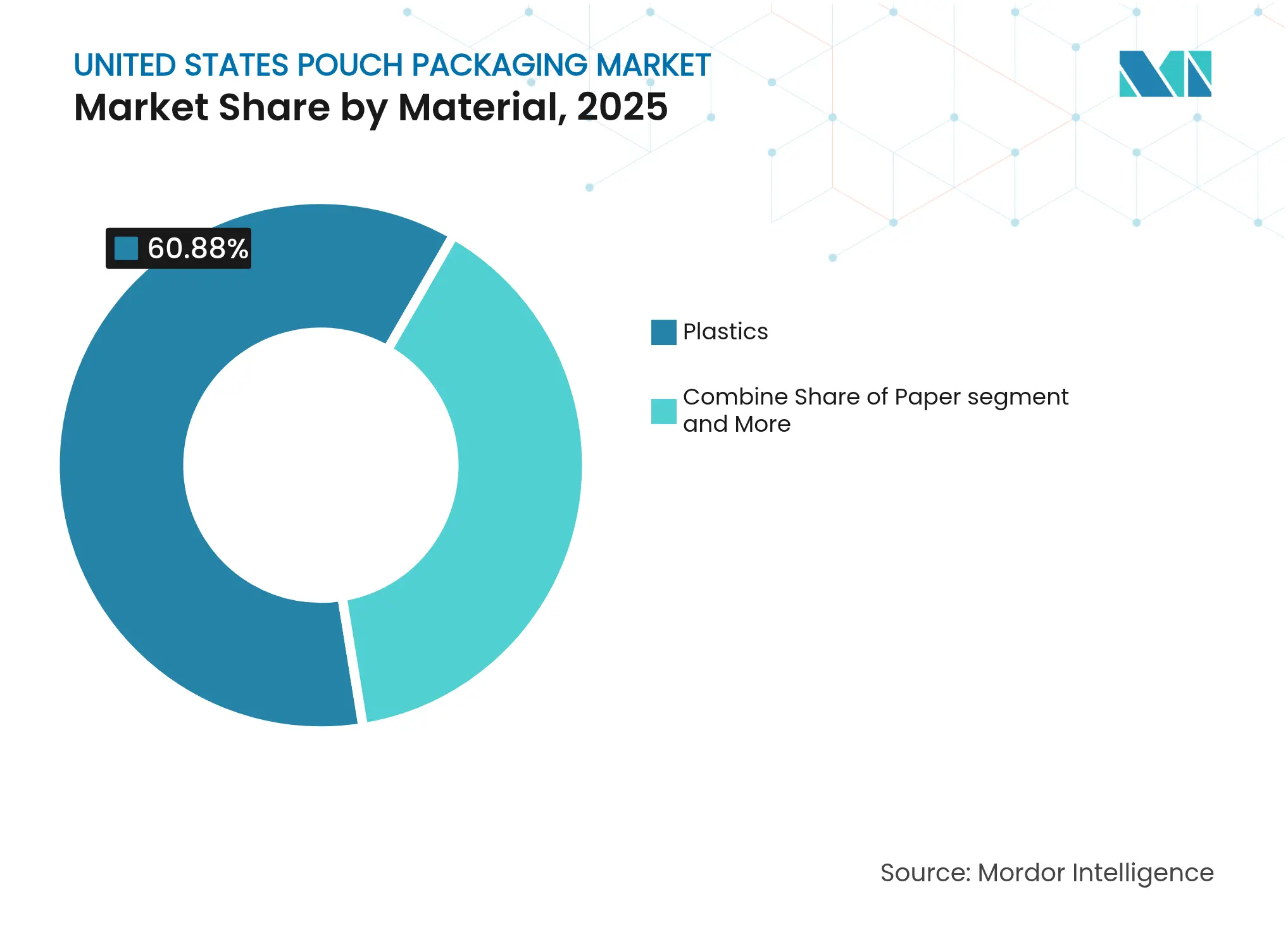

- By material, plastics led with 60.88% revenue share in 2025, while paper alternatives are projected to expand at a 7.21% CAGR to 2031.

- By product type, flat pouches captured 35.68% of United States pouch packaging market share in 2025; stand-up formats deliver the fastest growth at 6.18% CAGR through 2031.

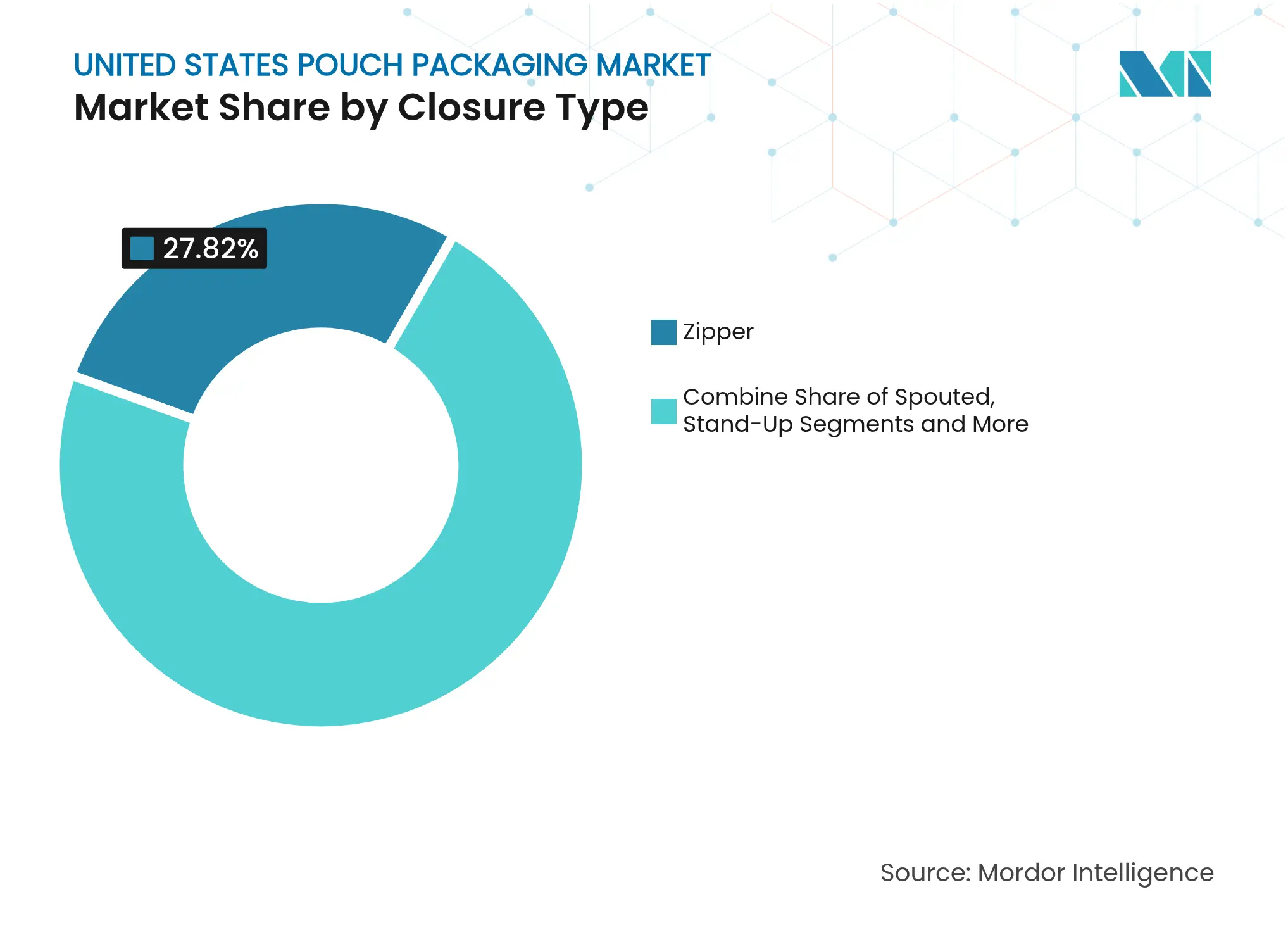

- By closure type, zipper mechanisms retained 27.82% share of the United States pouch packaging market size in 2025, with spout-and-cap systems advancing at an 7.94% CAGR to 2031.

- By end-user industry, food continued to command 40.53% of the market in 2025, whereas personal care and cosmetics is growing at a 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Pouch Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Consumer snacking culture fueling single-serve pouches via e-commerce fulfillment Consumer snacking culture fueling single-serve pouches via e-commerce fulfillment | +0.8% | National, urban markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.8% | Geographic Relevance:National, urban markets | Impact Timeline:Medium term (2-4 years) |

California EPR and plastics fees accelerating mono-material pouch conversions California EPR and plastics fees accelerating mono-material pouch conversions | +0.6% | CA, OR, CO with national spillover | Short term (≤ 2 years) | |||

Premium wet and treat pet-food moving to retort and spouted pouches Premium wet and treat pet-food moving to retort and spouted pouches | +0.5% | National, premium Northeast & West Coast | Medium term (2-4 years) | |||

Refill-format initiatives by US HPC brands (Target Zero, Walmart Circular Connector) Refill-format initiatives by US HPC brands (Target Zero, Walmart Circular Connector) | +0.4% | National retail chains | Long term (≥ 4 years) | |||

Military and outdoor MRE shift from cans to high-barrier retort pouches Military and outdoor MRE shift from cans to high-barrier retort pouches | +0.3% | Defense and recreation channels | Long term (≥ 4 years) | |||

Digital-print short-run pouch converting enabling SKU proliferation for DTC brands Digital-print short-run pouch converting enabling SKU proliferation for DTC brands | +0.7% | National, packaging hubs | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Consumer Snacking Culture Fueling Single-Serve Pouches via E-Commerce Fulfillment

Single-serve formats are gaining traction because they travel efficiently through automated sortation systems and reduce breakage compared with rigid containers. Brands are pairing high-barrier substrates with reinforced seals to guarantee freshness despite extended delivery cycles. Snack companies are also exploiting variable-data digital print to personalize graphics for subscription boxes; American Packaging Corporation’s HP Indigo 200K platform was installed specifically for these short-run, high-mix orders. The economics are compelling because single-serve pouches reduce food waste, command premium price points, and compress secondary-packaging needs.

California EPR and Plastics Fees Accelerating Mono-Material Pouch Conversions

California’s law imposes heavy eco-modulation fees on multilayer structures beginning 2027, prompting converters nationwide to pursue polyethylene-only laminates. Circular Action Alliance has issued recyclability testing protocols that now influence design briefs from coast to coast. [1]Circular Action Alliance, “California — Circular Action Alliance,” circularactionalliance.org Lead times for specialty mono-material films have doubled, pushing large buyers to lock-in resin volumes through multi-year supply agreements. Investments such as NOVA Chemicals’ Indiana mechanical-recycling plant aim to address film waste but will only partially offset the emerging material tightness.

Premium Wet and Treat Pet-Food Moving to Retort and Spouted Pouches

Premium pet-food brands are migrating from cans to high-barrier retort pouches that deliver equivalent shelf life with up to 70% weight reduction. Sonoco’s custom high-barrier laminate for pet nutrition leverages retort resistance and pet-owner convenience. Spouted fitments allow precise portion control for gravy-style treats and reinforce premium positioning. Amcor’s recycle-ready retort structure now offers barrier parity with traditional foil laminates while remaining compatible with mechanical recycling streams.

Refill-Format Initiatives by US HPC Brands

Household and personal-care players continue to test concentrated refills in pouches that consumers transfer into durable dispensers, cutting packaging weight by up to 80%. SC Johnson’s Refillution program illustrates willingness to pay for sustainability when convenience thresholds are met. Retail platforms such as Target Zero give refill pouches premium shelf space, catalyzing broader adoption across mid-tier brands.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Inadequate U.S. film-recycling infrastructure for multilayer pouches Inadequate U.S. film-recycling infrastructure for multilayer pouches | -0.9% | National, rural limitations | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-0.9% | Geographic Relevance:National, rural limitations | Impact Timeline:Long term (≥ 4 years) |

Volatile PE and PP resin prices compressing converter margins Volatile PE and PP resin prices compressing converter margins | -1.2% | National, regional feedstock variance | Short term (≤ 2 years) | |||

FDA migration-test hurdles for PCR content in food-contact pouches FDA migration-test hurdles for PCR content in food-contact pouches | -0.7% | National, food-contact lines | Medium term (2-4 years) | |||

Paper and molded-fiber alternatives cannibalizing snack pouches Paper and molded-fiber alternatives cannibalizing snack pouches | -0.5% | National, premium organic snacks | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Inadequate U.S. Film-Recycling Infrastructure for Multilayer Pouches

Flexible packaging recycling rates remain below 5%, largely because most material recovery facilities lack delamination and washing capabilities required for films. While NOVA Chemicals and Winpak are piloting dedicated reclamation for recycled polyethylene streams. the capacity gap is sizeable. Brand owners therefore hesitate to specify recycle-ready films at scale, slowing mono-material adoption outside regulatory hotspots.

Volatile PE and PP Resin Prices Compressing Converter Margins

Feedstock tariffs and global supply disruptions have elevated resin price swings beyond historical norms. Sterling Plastics estimates that 2025 tariffs on Chinese plastic imports alone added 10% to average converter resin costs. Converters are responding with shorter price-validity windows and raw-material surcharges, yet long-term contracts with big CPGs often restrain pass-through.

Segment Analysis

By Material: Paper Alternatives Challenge Plastic Dominance

Plastics maintained a 60.88% share of the United States pouch packaging market in 2025, reflecting entrenched supply chains and established FDA pathways. Polyethylene continues to anchor snack, frozen, and ambient foods thanks to sealability and cost advantages, whereas polypropylene is favored for higher-temperature applications. Yet the growth curve tells a different story: paper substrates are accelerating at 7.21% CAGR to 2031, propelled by EPR mandates and retailer scorecards that reward curbside recyclability. This divergence signals a structural realignment toward fiber and mono-material formats, even as legacy multilayer films persist in oxygen-sensitive applications.

Innovations such as Amcor’s AmFiber Performance Paper have validated paper’s ability to compete in barrier performance without foil layers.New aqueous coatings offer water vapor transmission rates suitable for dry snacks, further eroding plastic dominance. On the plastic side, resin suppliers are tailoring metallocene PE grades that boost toughness and gloss in single-polymer laminates. These developments mean converters can now deliver recycle-ready designs without sacrificing machinability, tightening the economic case for brand transition. Overall, material substitution remains the most visible sign of evolving sustainability economics within the United States pouch packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Stand-Up Formats Gain Shelf Presence

Flat pouches secured 35.68% of United States pouch packaging market share in 2025 because they run efficiently on high-speed form-fill-seal lines and minimize material usage. However, stand-up variants are pacing the field with a 6.18% CAGR through 2031, driven by retail end-cap visibility and consumer preference for reclosable convenience. Retort pouches, once confined to military rations, are permeating premium pet food and ready-meal aisles, while spouted designs unlock dispensing functionality in broths and smoothies.

Stick-packs and sachets remain staples in powdered sports nutrition, but volume growth is tapering as brands consolidate flavor lines to rein in packaging complexity. Meanwhile, aseptic pouches are carving a foothold in shelf-stable dairy, combining sterilization efficiency with reduced logistics costs. The rise of digital printing further tilts the field toward premade stand-up pouches because converters can capitalize on shorter runs, limiting waste and enabling SKU rotation. These cross-currents underscore how product-configuration choice is now inseparable from brand marketing strategy in the United States pouch packaging market.

By Closure Type: Innovation Drives Functionality

Zipper closures retained their leadership at 27.82% of 2025 sales, reflecting trusted functionality in snacking, frozen produce, and household cleaners. Spout-and-cap systems, though representing a smaller base, are registering an 7.94% CAGR by 2031, propelled by liquid detergents, baby foods, and puree snacks. Slider devices have also gained momentum in premium cheese and frozen entrées where effortless opening outweighs added cost.

Fitment suppliers are introducing narrower-gauge threaded spouts that cut plastic weight without compromising flow control. Winpak’s recent fitment launch targets recyclable polyethylene laminates, removing metal springs and compatibilizing with existing recycling streams. Emerging child-resistant and tamper-evident features are widening flexible entry into over-the-counter pharmaceuticals. As closures now account for a growing slice of bill-of-materials costs, brand owners scrutinize resealability as a core determinant of overall pack value in the United States pouch packaging market size calculations.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Personal Care Drives Premium Growth

Food applications continued to claim 40.53% of 2025 revenues, cemented by extensive co-packing infrastructure and consumer familiarity with flexible snack formats. Yet personal care and cosmetics are expanding at a 7.55% CAGR to 2031, powered by refill pouches for lotions, shampoos, and concentrated cleaning tablets. Alcoholic beverage makers are experimenting with single-serve cocktail pouches for event venues, while pharma demand grows for unit-dose gels and transdermal patches.

Pet nutrition is fast emerging as a bellwether category for high-barrier retort innovation that subsequently migrates to human food. Home-care brands are rolling out stand-up refill pouches that lock into reusable rigid dispensers, aligning with retailer sustainability scorecards. Meanwhile, defense procurement continues to influence civilian outdoor markets through specification trickle-down. These shifts illustrate how usage diversification is raising the ceiling for value-added formats across the United States pouch packaging market.

Geography Analysis

The Midwest and Southeast house much of the nation’s form-fill-seal capacity, benefiting from proximity to Gulf-Coast resin crackers and interstate logistics hubs. This concentration provides cost advantages for resin-intensive applications; however, it also exposes facilities to hurricane-driven supply disruptions that periodically tighten feedstock availability. The West Coast tells a different story: California’s EPR law forces converters to test mono-material structures well before national rollouts, effectively turning the state into a regulatory sandbox. Oregon and Colorado are poised to replicate similar frameworks, suggesting the policy gradient will widen rather than narrow.

In the Northeast corridor, the density of premium personal-care and specialty-food brands fuels demand for digital-print and short-run capabilities. American Packaging Corporation’s Rochester and Wisconsin plants, equipped with HP Indigo presses, actively court these direct-to-consumer launches, illustrating how regional converters wield speed-to-market as a competitive weapon. Conversely, rural Mountain states lack robust recycling collection for films, which stymies full-circle sustainability claims for national brands.

Tariff dynamics have distinct geographic footprints. West-Coast importers face the steepest cost bump from 2025 tariffs on Chinese specialty films, nudging buyers toward domestic alternatives or shifting inbound routes through Gulf ports. Meanwhile, the Midwest benefits from early investments in mechanical recycling; NOVA Chemicals’ Connersville plant targets polyethylene film reclamation for flexible packaging. Overall, geographic variances in regulation, feedstock access, and recycling assets are amplifying regional specialization within the United States pouch packaging market.

Competitive Landscape

Market Concentration

Amcor’s all-stock merger with Berry Global created a powerhouse spanning extrusion, lamination, and converting, with anticipated USD 650 million in annual cost synergies. Sonoco’s USD 3.9 billion purchase of Eviosys strengthened its metal and aerosol breadth and signaled willingness to invest aggressively in adjacent formats. These moves elevate minimum viable scale, forcing mid-tier converters to differentiate via sustainability certifications, niche barrier technology, or ultra-responsive service models.

Technology adoption underscores competitive fault lines. Large players deploy robotics and inline inspection to squeeze labor cost and guarantee quality at multi-plant networks. ProAmpac positions itself as an innovation leader through its Fiberization initiative, targeting fiber-based conversion for on-the-go food wrappers. Smaller specialists, meanwhile, secure loyalty by navigating FDA food-contact submissions for PCR resins, an area where regulatory expertise trumps sheer scale.

Vertical integration into recycling signals the next frontier. Amcor’s memorandum with NOVA Chemicals commits to a pipeline of mechanically recycled polyethylene, hedging EPR risk and enhancing brand credibility. Novolex’s merger with Pactiv Evergreen creates a diversified fiber-and-flexibles portfolio exceeding 39,000 SKUs, giving it unique cross-material leverage at retail. Collectively, these maneuvers indicate a market where competitive advantage hinges on the ability to deliver regulatory-ready, circular-economy solutions at commercial scale within the United States pouch packaging market.

United States Pouch Packaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amcor completed its merger with Berry Global, projecting USD 650 million in annual synergies.

- April 2025: Novolex finalized its combination with Pactiv Evergreen, forming a USD 6.7 billion food and specialty-packaging group.

- February 2025: Mondi commissioned a new extrusion line at Štĕtí to boost recyclable flexible capacity.

- January 2025: American Packaging Corporation unveiled an HP Indigo 200K digital unit for on-demand pouch printing.

Table of Contents for United States Pouch Packaging Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Consumer snacking culture fueling single-serve pouches via e-commerce fulfilment

- 4.2.2California EPR and plastics fees accelerating mono-material pouch conversions

- 4.2.3Premium wet and treat pet-food moving to retort and spouted pouches

- 4.2.4Refill-format initiatives by US HPC brands (Target Zero, Walmart Circular Connector)

- 4.2.5Military and outdoor MRE shift from cans to high-barrier retort pouches

- 4.2.6Digital-print short-run pouch converting enabling SKU proliferation for DTC brands

- 4.3Market Restraints

- 4.3.1Inadequate U.S. film-recycling infrastructure for multi-layer pouches

- 4.3.2Volatile PE and PP resin prices compressing converter margins

- 4.3.3FDA migration-test hurdles for PCR content in food-contact pouches

- 4.3.4Paper and molded-fiber alternatives cannibalising snack pouches

- 4.4Supply-Chain Analysis

- 4.5Regulatory and Policy Landscape

- 4.6Technology Landscape

- 4.7Porter's Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Rivalry

- 4.8Sustainability and Circular-Economy Initiatives

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Material

- 5.1.1Plastics

- 5.1.1.1Polyethylene (PE)

- 5.1.1.2Polypropylene (PP)

- 5.1.1.3Polyethylene Terephthalate (PET)

- 5.1.1.4Polyvinyl Chloride resin (PVC)

- 5.1.1.5Other Plastics

- 5.1.2Paper

- 5.1.3Aluminum Foil

- 5.1.4Other Materials

- 5.2By Product Type

- 5.2.1Flat (Pillow and Side-Seal)

- 5.2.2Stand-Up

- 5.2.3Spouted

- 5.2.4Retort

- 5.2.5Aseptic

- 5.2.6Stick-Pack / Sachet

- 5.2.7Rollstock / Premade Pouch

- 5.3By Closure Type

- 5.3.1Zipper

- 5.3.2Spout and Cap

- 5.3.3Tear-Notch

- 5.3.4Slider

- 5.3.5Other Closure Type

- 5.4By End-User Industry

- 5.4.1Food

- 5.4.1.1Candy and Confectionery

- 5.4.1.2Frozen Foods

- 5.4.1.3Fresh Produce

- 5.4.1.4Dairy Products

- 5.4.1.5Dry Foods and Cereals

- 5.4.1.6 Meat, Poultry and Seafood

- 5.4.1.7Pet Food

- 5.4.1.8 Other Foods (Sauces, Condiments, Spreads)

- 5.4.2Beverage

- 5.4.2.1Alcoholic

- 5.4.2.2Non-Alcoholic

- 5.4.3Medical and Pharmaceutical

- 5.4.4Personal Care and Cosmetics

- 5.4.5Home Care and Household

- 5.4.6Other End-User Industry

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Rank/Share, Products and Services, Recent Developments)

- 6.4.1Amcor PLC

- 6.4.2Mondi PLC

- 6.4.3Sealed Air Corporation

- 6.4.4Sonoco Products Company

- 6.4.5ProAmpac LLC

- 6.4.6PPC Flex Company Inc.

- 6.4.7LPS Industries

- 6.4.8Smurfit Westrock

- 6.4.9Huhtamaki Oyj

- 6.4.10Clondalkin Group

- 6.4.11Glenroy Inc.

- 6.4.12Printpack Inc.

- 6.4.13Bryce Corporation

- 6.4.14Constantia Flexibles

- 6.4.15American Packaging Corp.

- 6.4.16C-P Flexible Packaging

- 6.4.17Coveris

- 6.4.18Winpak Ltd.

- 6.4.19ePac Flexible Packaging

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-Space and Unmet-Need Assessment

United States Pouch Packaging Market Report Scope

Pouch packaging is a flexible product made from barrier films, paper, or foil, depending on the end user’s requirement. The report analyzes the factors that impact geopolitical developments in the studied market based on the prevalent base scenarios, key themes, and end-user industries-related demand cycles. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the pouch market in terms of drivers and restraints. The estimates exclude the weight and the cost of the content that is or is to be packed inside the pouch packaging solution. The scope of the study is limited to B2B demand.

The United States Pouch Packaging Market is Segmented by Material Type ( Paper, Plastic and Aluminum), by Resin Type - Plastic ( Polyethylene, Polypropylene, PET, PVC, EVOH, Other Resins), by Product ( Flat ( Pillow and Side Seal), Stand Up), by End-User Industry (Food (Candy & Confectionery, Frozen Foods, Fresh Produce, Dairy Products, Dry Foods, Meat, Poultry, And Seafood, Pet Food, Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)), Beverage, Medical and Pharmaceutical, Personal Care and Household Care, and Other End-User Industries). The report offers market forecasts and size in volume (Units) and value (USD) for all the above segments.