Bubble Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

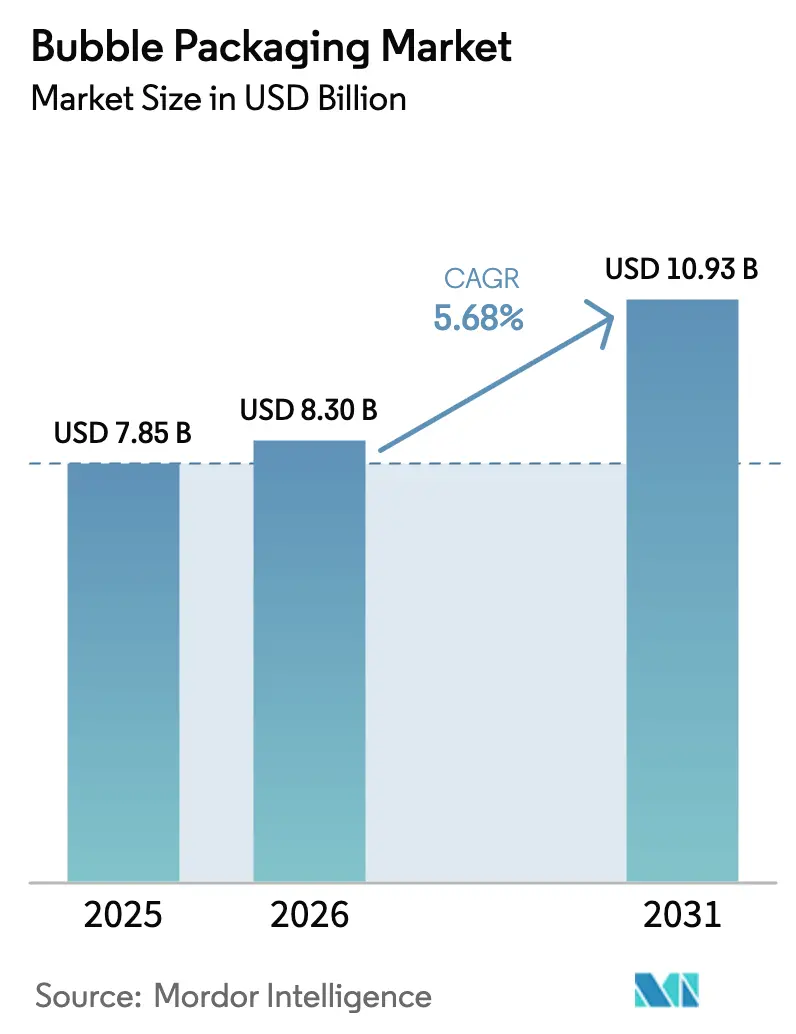

| Market Size (2026) | USD 8.3 Billion |

| Market Size (2031) | USD 10.93 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

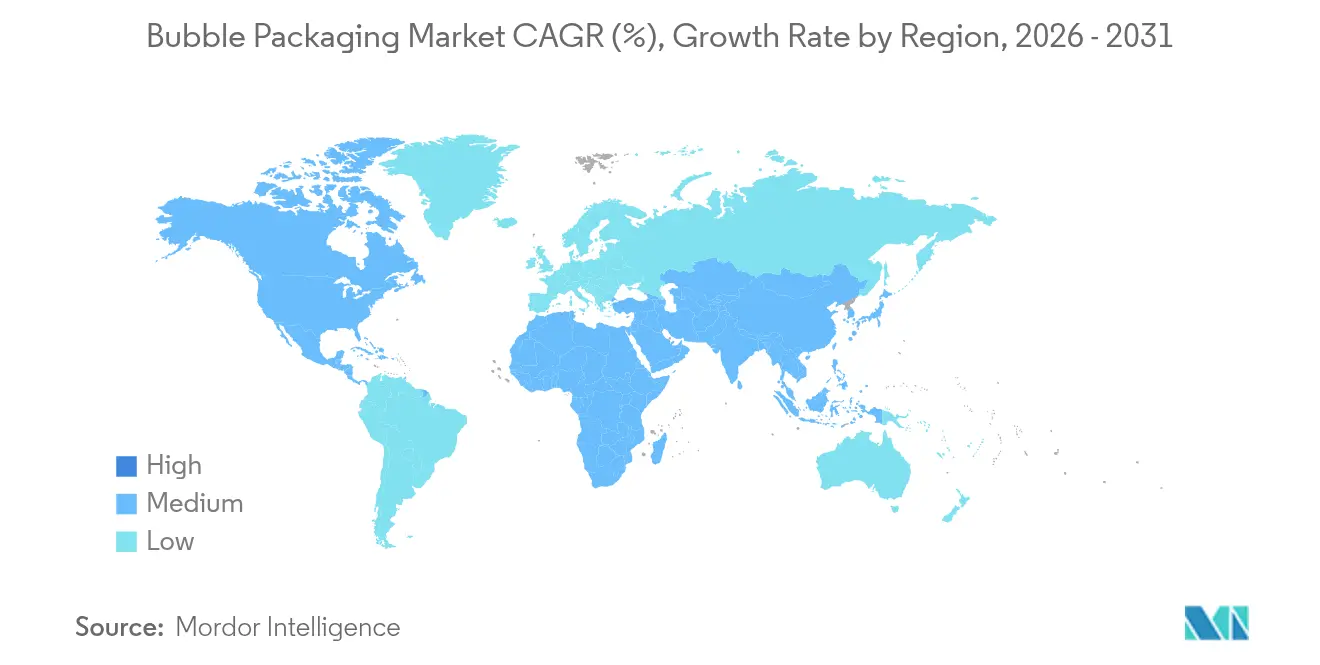

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bubble Packaging Market Analysis by Mordor Intelligence

The bubble packaging market size is expected to grow from USD 7.85 billion in 2025 to USD 8.3 billion in 2026 and is forecast to reach USD 10.93 billion by 2031 at 5.68% CAGR over 2026-2031. Rising parcel volumes in online retail, pressure to cut freight costs, and mandates that all consumer packaging be recyclable by 2030 are moving manufacturers toward lighter, right-sized, and increasingly paper-based formats. Production is shifting from pre-made sheets to on-demand inflation systems that ship flat, limit warehouse space, and integrate with fulfillment software. At the same time, producers must hedge against volatile polyethylene prices and plan capital for recycled-content lines ahead of upcoming minimum-content targets. Overall, demand continues to outpace macro-economic headwinds because stakeholders view reliable cushioning as essential for damage-free deliveries and cold-chain compliance.

Key Report Takeaways

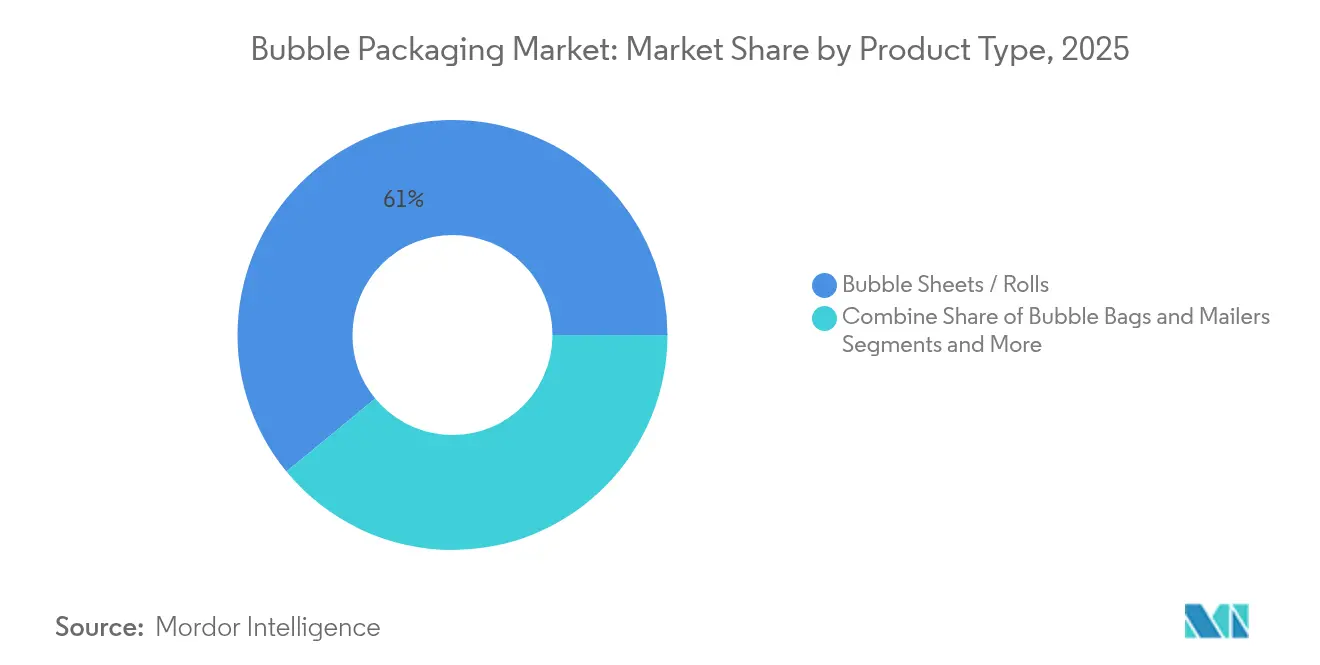

- By product type, bubble sheets and rolls held 60.95% of bubble packaging market share in 2025; inflatable on-demand systems are projected to expand at an 8.41% CAGR to 2031.

- By material, plastics accounted for 64.30% of bubble packaging market size in 2025, while paper and paperboard are set to grow at a 7.22% CAGR through 2031.

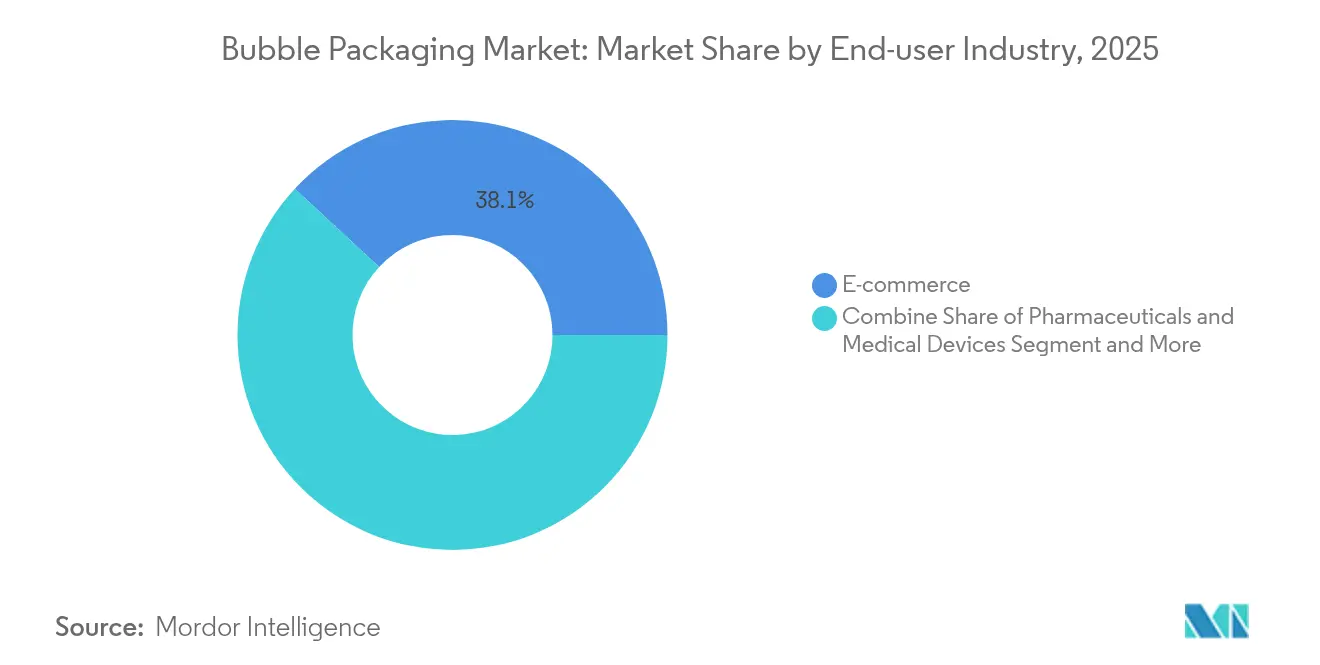

- By end-user industry, pharmaceuticals and medical devices posted a 9.85% CAGR, the fastest pace among all sectors between 2026 and 2031.

- By distribution channel, indirect sales captured 55.80% revenue share of the bubble packaging market in 2025 and are advancing at a 7.10% CAGR.

- By geography, Asia-Pacific commanded 38.15% of global revenue in 2025 and is forecast to grow at 7.58% annually through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bubble Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive e-commerce parcel volumes | +1.8% | Global, with APAC and North America leading | Short term (≤ 2 years) |

| Shift toward lightweight protective formats in fulfillment centers | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Growing demand for curb-side-recyclable paper-bubble hybrids | +0.9% | EU core, spill-over to North America | Medium term (2-4 years) |

| Rapid uptake of right-size automated inflatable systems | +0.7% | North America & EU, early adoption in APAC | Long term (≥ 4 years) |

| Brand-owner focus on unboxing experience and consumer engagement | +0.5% | Global, premium segments first | Medium term (2-4 years) |

| Emerging cold-chain last-mile networks for meal-kit and biologics | +0.4% | North America & EU, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive E-commerce Parcel Volumes

Global parcel traffic keeps climbing as online retail moves deeper into food, pharmaceutical, and cross-border categories. Parcel numbers reached the tens of billions in 2024, and the e-commerce packaging sector is projected to rise from USD 77.4 billion in 2024 to USD 124.9 billion by 2029. Each shipment needs shock-absorbent padding, and bubble sheets or ready-to-use mailers often offer the lowest-cost solution per shipped unit. Nations where retail infrastructure is leaping straight to mobile commerce, such as India, illustrate the trend: domestic e-commerce packaging demand more than doubled between 2019 and 2025. Because courier charges hinge on weight and size, sellers search for thinner bubbles that maintain protective performance yet lower dimensional-weight fees, sustaining robust consumption of roll and bag formats.

Shift Toward Lightweight Protective Formats in Fulfillment Centers

High-throughput warehouses constantly recalibrate pack sizes to trim freight outlays that can reach 50% of a parcel’s landed cost. Right-size software linked to on-demand inflatable lines lowers void space and has shown freight savings of up to 25% per order. [1]Brian McCarson, “Optimizing Packaging: Unleashing the Power of Artificial Intelligence,” Supply & Demand Chain Executive, sdcexec.com Inflatable systems such as Sealed Air’s Flex platform run 90 linear ft/min and store flat, freeing about 80% of floor space compared with pre-slit rolls.[2]Sealed Air, “BUBBLE WRAP brand Flex Inflatable Cushion System,” sealedair.com Labor savings matter as well because repetitive void-fill tasks in North American centers cost over USD 20/hour. As more facilities adopt advanced WMS and machine-learning tools, demand moves toward programmable inflators that integrate seamlessly.

Growing Demand for Curb-side-Recyclable Paper-Bubble Hybrids

Europe’s newly enacted Regulation (EU) 2025/40 stipulates every consumer package must be recyclable by 2030 and plastic must contain 65% recycled content by 2040.[3]European Union, “European Union Finalizes New Rules for Packaging and Packaging Waste Reduction,” fas.usda.gov Brands therefore trial paper-based cushions that consumers can place in municipal recycling bins. German start-up Papair has begun commercial runs of 100% paper bubble at its Lower Saxony plant, shipping pilot lots to more than 150 customers.[4]Packaging Europe, “Papair Commences Production of ‘100 % Paper’ Bubble Wrap Solution at Lower Saxony Site,” packagingeurope.comDemand for recyclable alternatives therefore rises fastest where regulators and consumers align, spurring traditional suppliers to blend paper facings with thinner polymer cores that still hold air.

Rapid Uptake of Right-size Automated Inflatable Systems

Logistics hubs that process tens of thousands of multi-SKU orders daily require modular equipment capable of ramping output as peaks hit. Sealed Air’s Bubble Wrap Flex and Rocket inflators preserve more than 90% of air after drop testing while letting operators dial in cell size per item. Managers cite the ability to run flat rolls through narrow docks and feed multiple pack stations from one unit as a decisive factor. As labor shortages widen in North America and Europe, automated inflation moves from optional to standard, with payback typically realized inside 18 months through reduced material waste and overtime costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extended Producer-Responsibility (EPR) fees on single-use plastics | -1.4% | EU leading, North America following | Short term (≤ 2 years) |

| Volatility in LDPE and LLDPE resin prices | -0.8% | Global, with North America most affected | Short term (≤ 2 years) |

| Rising adoption of fiber-based molded cushioning substitutes | -0.6% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Carrier dimensional-weight surcharges on bulky void-fill | -0.4% | Global, with e-commerce segments most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extended Producer-Responsibility (EPR) Fees on Single-use Plastics

Under the EU’s EPR framework, producers must finance end-of-life management of their packaging beginning 2025. Fees escalate for non-recyclable materials, directly lifting the cost of single-use plastic bubbles by an estimated 15–20% in the near term. Several US states have already enacted similar statutes, and more are drafting bills, forcing companies that ship nationwide to track divergent reporting rules. Compliance outlays divert capital from growth and discourage price-sensitive buyers who may shift toward molded-fiber or paper-pad substitutes until recycled-content bubbles scale up.

Volatility in LDPE and LLDPE Resin Prices

Polyethylene accounts for roughly two-thirds of a traditional bubble’s cost, so swings in resin pricing quickly compress margins. In early 2025 North American suppliers attempted increases of USD 0.05/lb, only to reverse course as inventories built and buyers resisted. Policy proposals for a 25% tariff on Canadian and Mexican resin further cloud visibility, while capacity expansions in China and Southeast Asia deepen the global supply overhang. To hedge, converters carry higher inventories and adopt formula-based pricing with customers, yet these strategies tie up working capital and can stall project rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Inflatable Systems Drive Innovation

Bubble sheets and rolls captured 60.95% of bubble packaging market size in 2025, reflecting decades-long familiarity among shippers. Their unit price advantage secures bulk contracts in electronics, homeware, and general merchandise channels. However, the 8.41% CAGR forecast for inflatable on-demand formats signals a decisive pivot toward automation. Inflatable equipment produces cushions precisely when needed, reducing both floor space and transport emissions linked to bulky roll deliveries. Because one pallet of flat film can replace up to 25 pallets of pre-inflated product, logistics savings often offset the equipment lease within a year. Users also value consistency; computer-controlled inflators hold air pressure inside each cell within narrow tolerances, minimizing breakage claims on fragile SKUs.

Inflatable adoption reshapes competitive dynamics. Large integrated vendors bundle film supply contracts with machinery support, locking in multi-year relationships. Mid-sized converters counter by promoting hybrid solutions such as sheet-in-box dispensers that add speed without large capital. Bubble bags and mailers sustain their niche in direct-to-consumer channels thanks to self-seal strips and brandable exteriors. Bubble insulation panels, though a small slice of the bubble packaging market, remain stable as construction and HVAC trades favor easy-cut radiant-barrier materials. Meanwhile, research into origami-inspired folding structures at VTT suggests future options that combine thinness, strength, and aesthetic appeal.

By Material: Sustainability Reshapes Composition

Plastics still dominated at 64.30% bubble packaging market share in 2025 because LDPE and LLDPE deliver high air retention and tensile strength. Yet paper and paperboard variants post a 7.22% CAGR through 2031, far above the overall 5.68% growth, as regulators and consumers push the sector toward curb-side recycling. Manufacturers respond with co-extruded structures containing up to 90% post-consumer resin that help them meet minimum-content thresholds without sacrificing cushioning. Bio-based PE from sugarcane ethanol is gaining pilot orders among cosmetics brands pursuing carbon-neutral pledges, but premium pricing remains a barrier for mass adoption.

In practice, ship-from-store and returns programs create mixed-stream recycling challenges, so brand owners experiment with thermo-laminated paper bubbles that separate easily in pulpers. Early trials demonstrate comparable drop-test results for non-hazardous items, though water-vapor barrier properties lag polymer benchmarks. The material transition invites fresh supply-chain collaborations: polymer suppliers expand washing and pelletizing capacity, while pulp producers invest in surface-coating lines capable of forming micro-pockets that trap air. The outcome will be a multi-material landscape in which each format carves out specific performance-cost niches rather than a single-material takeover.

By End-user Industry: Pharmaceuticals Lead Growth

E-commerce accounted for 38.10% revenue in 2025, underscoring the ubiquity of bubble cushioning in omnichannel retail parcels. However, pharmaceutical and medical device shippers are set to outpace all peers with a 9.85% annual clip between 2026 and 2031. Vaccine vials, autoinjectors, and diagnostic kits require ISTA and FDA-validated packaging that remains intact across cold-chain handoffs. Bubble liners engineered with proprietary barrier films meet these criteria and permit rapid kitting on automated lines. Veritiv’s TUFflex bubble fulfills healthcare standards while offering zip-seal options for point-of-care convenience.

Electronics stay resilient because handheld devices and accessories need abrasion resistance during last-mile drops. Cosmetics and personal care leverage colored or printed bubbles to elevate the unboxing moment, translating protective media into a branding canvas. Food and beverage volumes trend upward in tandem with meal-kit and specialty grocery subscriptions; Sealed Air’s temperature-assurance bubble sleeves illustrate how thermal elements integrate with cushioning. Industrial machinery parts round out the mix by demanding thicker, multi-layer bubbles that shield heavy metal components against vibration during sea transit.

By Distribution Channel: Indirect Sales Maintain Dominance

Distributors, value-added resellers, and packaging wholesalers controlled 55.80% of 2025 revenue, reinforcing their importance in a fragmented customer base where average order sizes remain modest. Many SMEs lack the scale to negotiate directly with resin converters, so they rely on distributors for consolidated shipments, technical advice, and localized inventories. Growth at 7.10% through 2031 suggests the channel’s appeal endures despite digital disintermediation efforts. Notably, hybrid models emerge in which manufacturers host e-commerce portals but fulfill via regional distributors, maintaining market coverage while retaining data on end-user trends.

Large accounts in electronics, pharma, and third-party logistics often bypass intermediaries to secure bespoke specifications and direct technical support. Even here, some suppliers embed account-dedicated representatives within customer facilities, blurring traditional channel definitions. Consolidation in distribution underscores its strategic value: Veritiv’s USD 1.19 billion purchase of Orora Packaging Solutions brings nearly 70 facilities under one roof, enabling broader SKUs and faster lead times. As regional compliance rules tighten, distributors able to certify local recycled-content thresholds strengthen their competitive edge.

Geography Analysis

Asia-Pacific held 38.15% of global revenue in 2025 and is rising at an 7.58% CAGR through 2031, the fastest among all regions. Nations such as India, whose total packaging sector is forecast to quadruple from USD 50.5 billion in 2019 to USD 204.81 billion in 2025, drive volume thanks to expanding middle-class consumption and smartphone penetration. Domestic parcel networks in Southeast Asia upgrade from jiffy-bag-only policies to mixed bubble formats suitable for electronics, apparel, and chilled goods, lifting regional supply needs. Local converters meanwhile capture customers through shorter lead times and familiarity with country-specific tax regimes.

North America represents a mature but innovation-intensive arena where right-size machinery and recycled-content mandates propel product upgrades. State-by-state EPR legislation obliges producers to source traceable inputs, favoring suppliers that operate internal recycling plants. Carrier surcharges tied to dimensional weight also encourage lightweight cushioning, so the bubble packaging market progressively tilts toward thinner co-extrusions and inflatables. Europe enforces the strictest sustainability rules, accelerating paper-bubble trials and joint ventures between polymer and pulp companies. Because each EU member state must translate Regulation 2025/40 into local law, suppliers tailor portfolio mixes by country, complicating pan-European rollouts but rewarding flexible manufacturing strategies.

Elsewhere, Middle East & Africa and South America contribute smaller bases yet post solid growth as cross-border e-commerce platforms partner with local logistics providers. Infrastructure investments in refrigerated warehousing across Gulf economies bolster pharmaceutical and meal-kit demand, stimulating higher-value applications. In Latin America, domestic electronics assembly hubs in Mexico and Brazil require steady protective-packaging inflows for export shipments to North America. Across regions, harmonization of ISTA thermal and shock standards levels requirements for global suppliers, fostering gradual convergence in performance benchmarks.

Competitive Landscape

The bubble packaging market features moderately fragmented with technology and sustainability leadership determining wallet share. Sealed Air stands out through an integrated offer that spans classic Bubble Wrap rolls, Flex and Rocket inflators, and 90% recycled-content films. Its USD 31 million capacity expansion at Iowa Park underpins expected growth while embedding recycled resin lines on-site. Competitors respond by bundling equipment leasing, maintenance, and consumables into subscription contracts that lock in multiyear volumes and simplify customer budgeting.

Material innovation drives fresh entrants. Papair commercialized the first 100% paper bubble produced in continental Europe, winning pilots with appliance and apparel brands keen to pre-empt EU recycled-content quotas. Molded-fiber specialists push lightweight pulp cushions for electronics, encroaching on lower-performance bubble use cases. To defend share, incumbents highlight superior drop resistance, moisture barriers, and lower breakage claims on glass or pharma SKUs. Partnerships illustrate strategic repositioning: Sealed Air teamed with Qosina to co-develop sterile medical pack formats that carry high margins and stringent certification hurdles.

M&A activity intensifies as companies broaden footprints and vertically integrate. Novolex’s USD 6.7 billion merger with Pactiv Evergreen knits together food-service disposables and protective packaging expertise, creating cross-selling avenues. Sonoco’s acquisition of metal-packager Eviosys fuels a 30.6% jump in Q1 2025 sales, exemplifying how diversified packagers chase resilient end-market categories. Smaller regional players defend niche positions by offering short lead times, bespoke print, and lower minimum order quantities, especially in Asia where industrial clusters value proximity and service responsiveness.

Bubble Packaging Industry Leaders

Veritiv Corporation

Sealed Air Corporation

Abriso Jiffy

IVEX Protective Packaging Inc.

Pregis LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Novolex completed its USD 6.7 billion merger with Pactiv Evergreen, creating a leading manufacturer in food, beverage, and specialty packaging with over 250 brands and 39,000 SKUs.

- January 2025: Sealed Air launched Bubble Wrap products containing 80% recycled content and expanded recycling programs to more than 18,000 retail drop-off points.

- December 2024: VTT Technical Research Centre of Finland unveiled origami-inspired protective packaging technology under the FOLD project.

- July 2024: Papair began producing 100% paper bubble wrap at its Lower Saxony site.

Global Bubble Packaging Market Report Scope

Bubble packaging, or bubble wrap, is a protective packaging material consisting of small air-filled bubbles enclosed between two layers of transparent plastic film. This lightweight and flexible material is designed to cushion and safeguard fragile items during storage, handling, and transportation. The air-filled bubbles provide shock absorption and insulation, helping to prevent damage from impacts, vibrations, and temperature fluctuations.

The bubble packaging market is segmented by product (bubble sheet, bubble bag/mailer), material (paper and paperboard, plastic [LDPE, LLDPE, and other plastics], end-user industry (manufacturing and warehousing [electronics and electricals, pharmaceutical, cosmetics and personal care, food and beverages], e-commerce, logistics and transportation, and other end-user industries), and geography(Europe, North America, Latin America, Asia, Middle East and Africa, and Rest of the World). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Bubble Sheets / Rolls |

| Bubble Bags and Mailers |

| Inflatable Bubble-on-Demand Systems |

| Bubble Wrap Insulation Panels |

| Other Product Types |

| Paper and Paperboard | |

| Plastics | Low-Density Polyethylene (LDPE) |

| Linear Low-Density Polyethylene (LLDPE) | |

| Recycled / Bio-based PE |

| Electronics and Electricals |

| Pharmaceuticals and Medical Devices |

| Cosmetics and Personal Care |

| Food and Beverages |

| Industrial and Machinery Parts |

| E-commerce |

| Other End-user Industry |

| Indirect Sales |

| Direct Slaes |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Bubble Sheets / Rolls | ||

| Bubble Bags and Mailers | |||

| Inflatable Bubble-on-Demand Systems | |||

| Bubble Wrap Insulation Panels | |||

| Other Product Types | |||

| By Material | Paper and Paperboard | ||

| Plastics | Low-Density Polyethylene (LDPE) | ||

| Linear Low-Density Polyethylene (LLDPE) | |||

| Recycled / Bio-based PE | |||

| By End-user Industry | Electronics and Electricals | ||

| Pharmaceuticals and Medical Devices | |||

| Cosmetics and Personal Care | |||

| Food and Beverages | |||

| Industrial and Machinery Parts | |||

| E-commerce | |||

| Other End-user Industry | |||

| By Distribution Channel | Indirect Sales | ||

| Direct Slaes | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the bubble packaging market?

The bubble packaging market is valued at USD 8.3 billion in 2026.

How fast will the market grow through 2031?

Revenue is forecast to expand at a 5.68% CAGR, reaching USD 10.93 billion by 2031.

Which product segment is growing the fastest?

Inflatable on-demand systems post the highest growth at an 8.41% CAGR thanks to warehouse automation benefits.

Why are pharmaceutical applications expanding rapidly?

Cold-chain drugs and regulatory test kits demand ISTA-compliant cushioning, driving a 9.85% CAGR in the segment.

How are sustainability regulations affecting material choices?

EU and state-level mandates for recyclability and minimum recycled content accelerate adoption of paper bubbles and high-recycled-content PE films.

Which region leads global sales?

Asia-Pacific holds 38.15% of worldwide revenue and is the fastest-growing region at 7.58% annual growth.

Page last updated on: