Bagasse And Agricultural-Fiber Molded Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

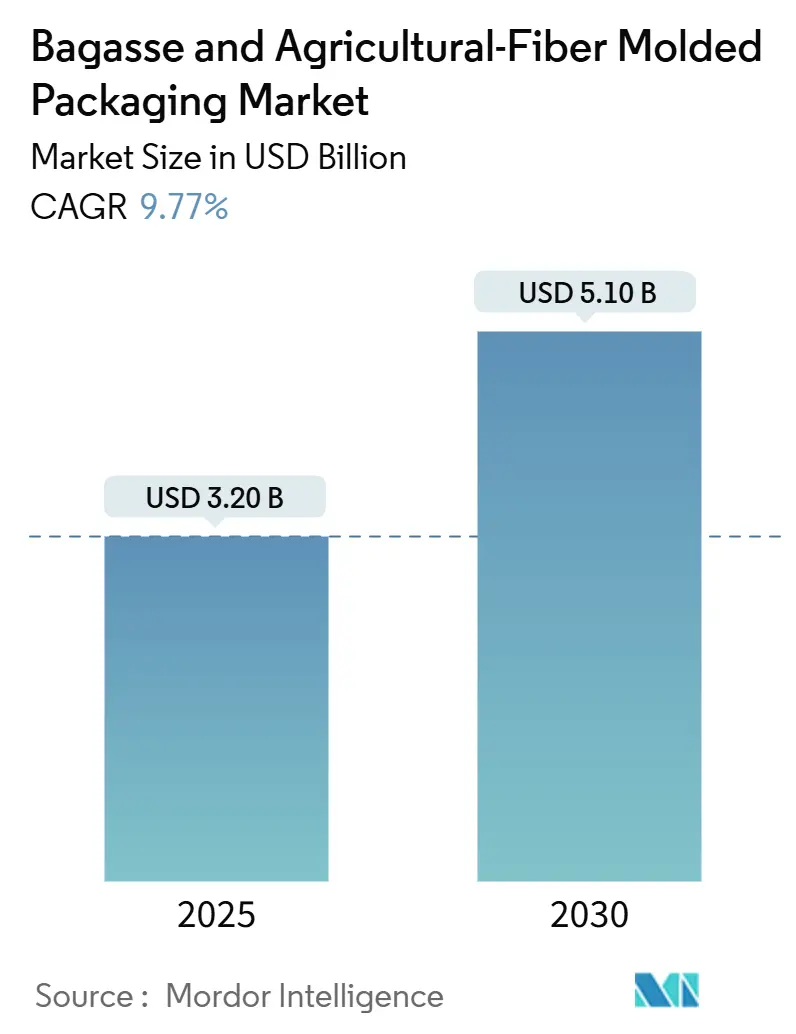

| Market Size (2025) | USD 3.20 Billion |

| Market Size (2030) | USD 5.10 Billion |

| Growth Rate (2025 - 2030) | 9.77% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bagasse And Agricultural-Fiber Molded Packaging Market Analysis by Mordor Intelligence

The bagasse and agricultural-fiber molded packaging market size stands at USD 3.2 billion in 2025 and is projected to reach USD 5.1 billion by 2030, registering a 9.77% CAGR across the period. Converging shifts in environmental regulation, raw-material localization, and carbon pricing narrow the historical cost gap versus plastics and anchor multi-year growth visibility. Asia-Pacific remains the supply chain fulcrum because sugarcane mills, bamboo plantations, and export-oriented converting hubs operate within a single logistics radius, compressing fiber procurement costs and cycle times. Middle East and Africa, although smaller in absolute terms, records double-digit expansion as new agro-processing zones in the Gulf and North Africa elevate rural incomes while solving agricultural waste disposal. Product innovation pivots toward leak-resistant coatings, enabling the bagasse and agricultural-fiber molded packaging market to capture beverage and hot-food formats once considered out of technical reach. Competitive dynamics are fragmented, yet vertical integration around raw-material sources, patented barrier technologies, and carbon-credit monetization increasingly differentiate profitable operators.

Key Report Takeaways

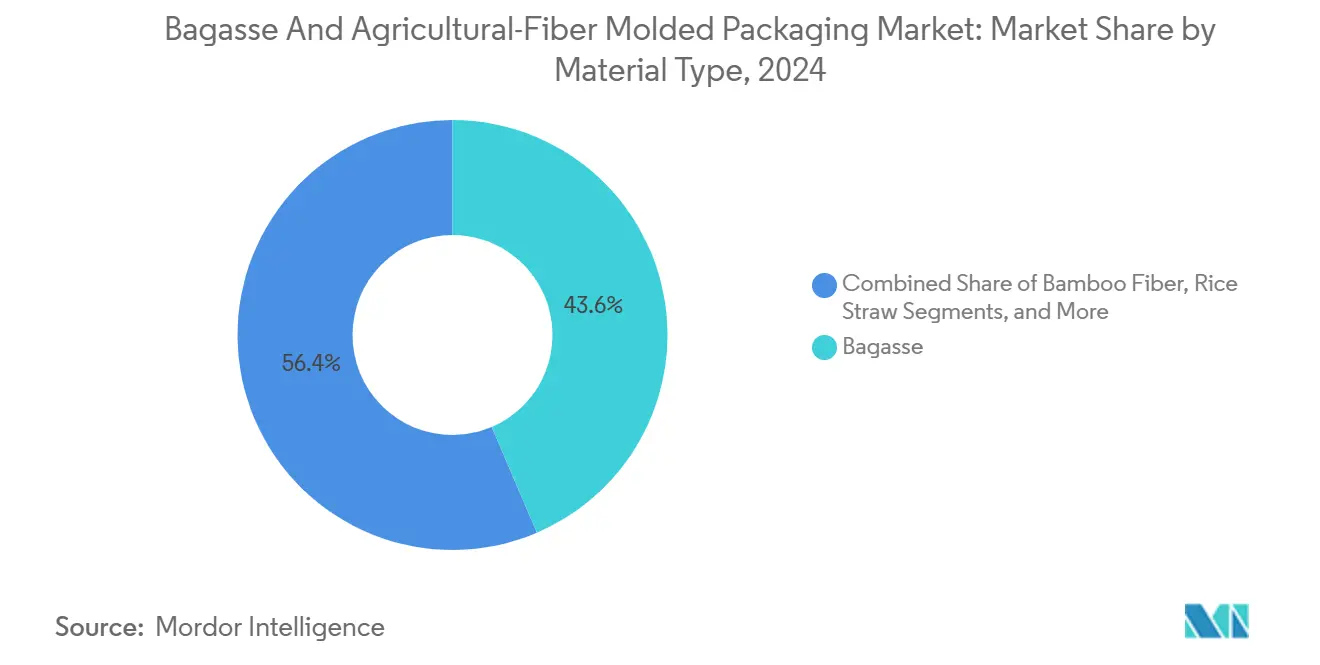

- By material type, bagasse accounted for 43.58% of the bagasse and agricultural-fiber molded packaging market share in 2024.

- By product type, the bagasse and agricultural-fiber molded packaging market size for cups and lids is expected to expand at an 11.28% CAGR between 2025-2030.

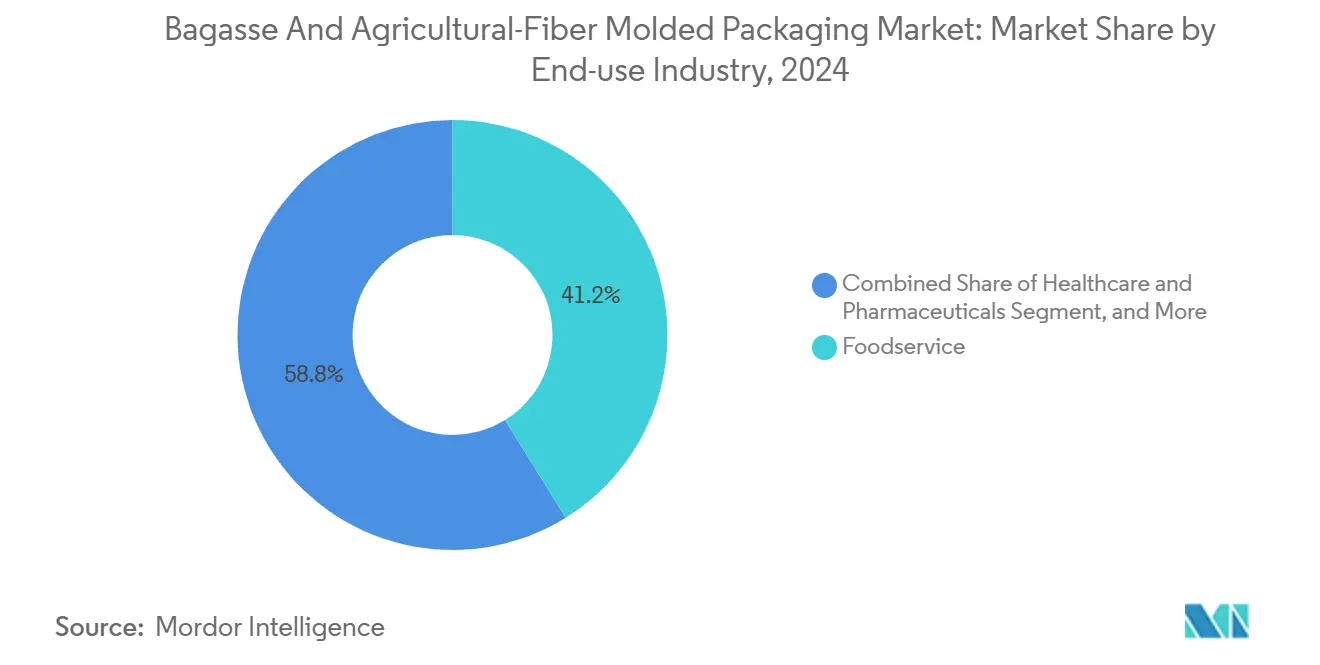

- By end-use industry, foodservice captured 41.18% of the bagasse and agricultural-fiber molded packaging market share in 2024.

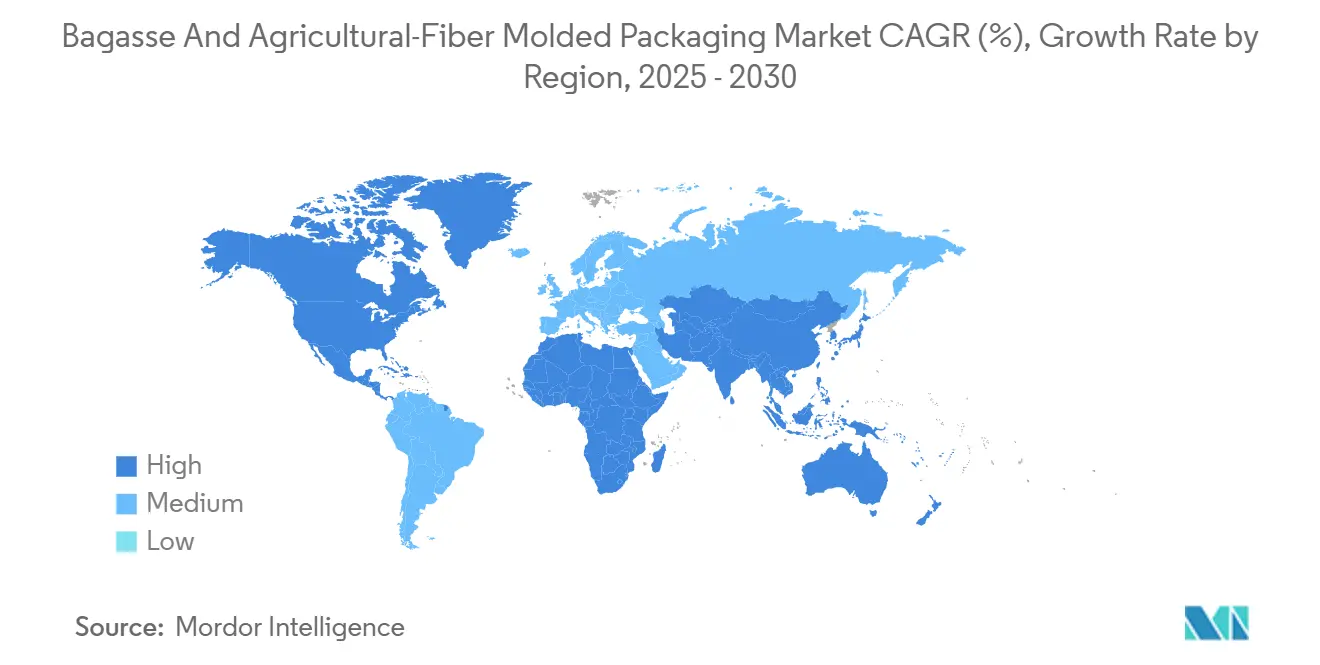

- By geography, the bagasse and agricultural-fiber molded packaging market size for the Middle East and Africa is expected to expand at a 10.91% CAGR between 2025-2030.

Global Bagasse And Agricultural-Fiber Molded Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bans on single-use plastics | +2.8% | Global with early adoption in European Union and North America | Short term (≤ 2 years) |

| Consumer preference for sustainable packaging | +2.1% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expansion of food-delivery and QSR networks | +1.9% | Asia-Pacific core, spill-over to Middle East and Africa and Latin America | Medium term (2-4 years) |

| Government incentives for agro-waste valorization | +1.6% | India, Brazil, China | Long term (≥ 4 years) |

| Localized supply chains near sugarcane mills | +1.2% | Brazil, India, Thailand, Philippines | Long term (≥ 4 years) |

| Carbon-negative packaging credits | +0.9% | European Union, California, emerging carbon markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Bans On Single-Use Plastics

Global plastics regulation has swiftly shifted from bag fees to outright restrictions on food-contact items, placing agricultural fibers at the forefront of the compliance queue. The European Union’s Single-Use Plastics Directive, fully enforced in 2024, imposes extended producer responsibility fees that escalate the true cost of conventional polymers, rendering bagasse-based trays economically competitive.[1]European Commission, “Single-Use Plastics Directive,” ec.europa.eu California’s 25% reduction mandate exempts ASTM D6868-certified compostables, creating a volume pull for molded fiber converters that can validate industrial compost performance. Multinational restaurant chains mitigate regulatory risk by standardizing compliant formats across continents, thereby accelerating global demand convergence and increasing switching costs for late-adopting suppliers.

Consumer Preference For Sustainable Packaging

Corporate sustainability position statements have hardened into contractual sourcing requirements that prioritize life-cycle carbon emissions over unit cost. McDonald’s public pledge to shift all packaging to renewable, recycled, or certified inputs by 2025 crystallizes how brand risk management and social license now dictate material choice.[2]McDonald’s Corporation, “Packaging and Waste,” corporate.mcdonalds.com Consumer willingness to pay a premium for eco-friendly formats reaches 73% in high-income markets, giving retailers headroom to absorb current molded-fiber cost differentials without margin erosion. Packaging-as-a-service subscription models convert capex into opex for restaurants, coupling waste-reduction analytics with molded-fiber supply contracts and unlocking stickier revenue for converters.

Expansion Of Food-Delivery And QSR Networks

Third-party delivery platforms raised global restaurant revenue exposure to off-premise channels, multiplying touchpoints where leak-proof, stackable, and heat-stable containers are non-negotiable. Worldwide online food-delivery sales surpassed USD 165 billion in 2024, placing continuous replenishment pressure on disposable packaging inventories, particularly across dense Asian megacities. Coated bagasse lids retain beverage warmth yet avoid lid-cup separation failures common in early molded designs, driving repeat orders among coffee chains. The geometric expansion of ghost kitchens further shortens procurement lead times, nudging operators toward regionally integrated suppliers who can mass-customize shapes with rapid-tooling equipment.

Government Incentives For Agro-Waste Valorization

Agro-circularity policies now treat molded packaging as a higher-value endpoint compared to open-field burning, triggering direct subsidies and tax incentives. India’s National Policy on Biofuels allocates up to 50% capital grants for non-fuel residue utilization plants, thereby reducing the payback periods for new molded-fiber lines. In China, circular-economy zones offer discounted electricity tariffs to mills that convert at least 30% of their pulp from farm residues, thereby lowering variable costs per ton. Brazil’s sugarcane association structures multi-year offtake contracts to hedge fiber price volatility, allowing converters to lock in input spreads and underwrite long-horizon plant debottlenecking.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher cost versus conventional plastics | -1.8% | Global, particularly price-sensitive emerging markets | Short term (≤ 2 years) |

| Moisture / oil-resistance limitations | -1.2% | Global, affecting premium food applications | Medium term (2-4 years) |

| Competition with bio-fuel producers for bagasse | -0.9% | Brazil, India, Thailand | Medium term (2-4 years) |

| Crop-yield variability affecting fiber quality | -0.7% | Climate-sensitive agricultural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Cost Versus Conventional Plastics

Despite abundant fiber feedstock, molded-fiber plants incur 15-25% higher conversion costs because pulping, drying, and forming stages rely on thermal energy and specialized tooling. Energy expenses alone account for as much as 40% of total production cost, exposing small plants to utility price shocks and limiting economies of scale. Capital outlays for automated thermoforming presses still exceed USD 7 million per 10,000-ton annual line, a hurdle that sidelines under-capitalized entrants. That said, EPR fees on virgin plastic and widening carbon taxes compress the cost delta in Europe and select U.S. states, thereby narrowing the severity of this restraint over the medium term.

Moisture / Oil-Resistance Limitations

Standard bagasse fiber begins to absorb water within two hours of continuous liquid contact, degrading its structure and limiting its use in frozen-food applications. Bio-based PLA or nano-cellulose coatings extend shelf life to 48 hours but layer 20-30% extra cost and risk compromising backyard-compost claims if barrier additives are misaligned with certification protocols. Oil permeability challenges remain acute for grease-heavy items such as fried chicken, where bagasse containers may leach oil and weaken integrity. While pilot-scale wax emulsions show promise, the stability-versus-compostability trade-off keeps commercialization tentative and slows adoption in upmarket food categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bagasse Dominance Faces Fiber Diversification

Bagasse contributed 43.58% of the bagasse and agricultural-fiber molded packaging market size in 2024, as sugar-rich economies, from India to Brazil, channeled mill by-products directly into adjacent molding plants with minimal preprocessing. This dependable supply chain translated into lower variable costs and predictable pulp furnish quality, allowing converters to standardize throughput and amortize capital more quickly. Yet, the segment’s growth decelerates as single-fiber dependency raises procurement risk amid bio-ethanol policy swings that occasionally divert bagasse to fuel production. Bamboo fiber, clocking an 11.61% CAGR, unlocks tensile strength up to two times that of bagasse and regrows in twelve-month cycles, appealing to high-impact packaging applications in electronics and premium takeaway beverages. Wheat and rice straw unlock participation for regions with limited sugarcane output; however, sporadic harvest windows prompt mills to invest in seasonal warehousing or risk idling capacity.

Processing innovations lean heavily on multi-fiber blends that pair bagasse’s lignin content with bamboo’s long fibers, optimizing sheet strength while tamping raw-material volatility. ISO’s latest draft standard on agro-fiber grading introduces harmonized metrics for brightness, water retention, and microbial load, enabling cross-border fiber trading without extensive incoming QC procedures.[3]International Organization for Standardization, “Packaging Materials Standards,” iso.org Blending also fosters product differentiation: a 70-30 bagasse-bamboo matrix achieves crush strength suitable for wine-bottle shippers, while 50-50 bagasse-straw mixes strike the right balance for quick-service entrees, where stiffness outweighs translucence. Emerging candidates, such as coconut coir, add hydrophobic traits that could ultimately reduce coating usage and lower costs. Collectively, these developments diversify feedstock resilience, pull new agrarian regions into the supply map, and extend the addressable scope of the bagasse and agricultural-fiber molded packaging market.

By Product Type: Cups Drive Innovation Beyond Traditional Tableware

Cups and lids are expanding at an 11.28% CAGR, outpacing historic tableware volumes by answering coffee-chain mandates to replace polyethylene-lined fiber cups before 2028. Early design challenges related to lid fit and steam venting have been mitigated after the introduction of precision forming dies and micro-flute locking ribs, enabling molded-fiber lids to withstand 95 °C beverage temperatures without warping. Meanwhile, plates and bowls still held 31.58% of the bagasse and agricultural-fiber molded packaging market share in 2024, favored by institutional caterers and QSR buffets that value stackability and portion-control dividers. The growth lag evident in legacy plates is more attributable to market maturity than to substitution risk; yet, differentiation is re-emerging through embossed branding, pigment-free tinting, and built-in cutlery slots.

Tray and clamshell formats ride the wave of normalizing food delivery. Converters experiment with vent-control perforations that keep fried foods crisp, a property once exclusive to perforated plastic. Container sub-segments court the CPG aisle by demonstrating drop-height protection comparable to that of expanded polystyrene, while displaying compostability logos that reinforce retailer ESG badges. High-precision molding enables complex geometries such as snap-fit closures on salad bowls, previously unthinkable in coarse-fiber substrates. Across categories, additive manufacturing shortens development cycles by producing pilot molds in under two weeks, allowing rapid iteration and closer co-design with brand owners. Together these advances enlarge the practical canvas on which the bagasse and agricultural-fiber molded packaging market can paint differentiated value propositions.

By End-Use Industry: Healthcare Acceleration Transforms Market Dynamics

Healthcare and pharmaceuticals are projected to accelerate at an 11.36% CAGR as hospitals transition from multi-use plastic trays to single-use, sterile fiber packs for surgical kits and diagnostic sample transport. Post-pandemic infection-control updates recommend minimizing surface re-use, and molded fiber satisfies incineration-compatibility needs without emitting dioxins, unlike PVC-lined disposables. Packaging validation under ISO 11607 for sterile barriers has been achieved for select bagasse-bamboo blends, broadening regulatory acceptance and reducing procurement cycles in the life sciences vertical. Foodservice remains the workhorse, retaining 41.18% of 2024 revenue, although its share is inching down as other sectors grow faster. Restaurants are integrating molded fiber as a risk hedge against plastic bans, while benefiting from the shelf-ready aesthetics and microwavability that foam clamshells lack.

Consumer goods tap molded fiber for fragile e-commerce shipments, such as cosmetics, smartwatches, and small appliances, because the cushion element replaces bubble wrap without the downstream landfill backlash. Electronics brands test antistatic additives that disperse micro-charge potential, thereby widening the utility of high-value consumer electronics. Industrial demand is nascent but rising for loose-fill and edge protectors where load absorption metrics surpass corrugated pads at identical basis weights. Meanwhile, FDA guidance endorsing plant-based food-contact substances emboldens grocery chains to swap out petroleum-based deli trays. The diverse end-use tapestry cushions cyclical swings, anchoring a broad runway for the bagasse and agricultural-fiber molded packaging industry.

Geography Analysis

The Asia-Pacific region captured 36.91% of the 2024 revenue in the bagasse and agricultural-fiber molded packaging market, driven by contiguous raw-material basins, maturing equipment clusters in Southeast Asia, and export linkages to North America and Europe. China’s 14th Five-Year Plan broadens agricultural waste valorization quotas, compelling provincial sugar, rice, and wheat millers to allocate residues to pulp furnish rather than low-value combustion. India’s Uttar Pradesh state rolled out stamp-duty concessions on land purchases for molded-fiber plants, triggering a string of greenfield investments near sugar belts. Japan and South Korea employ differentiated strategies, focusing on high-precision thermoformers to meet the small but high-margin domestic demand for premium bento, convenience-store sushi, and specialty cosmetics trays.

The Middle East and Africa are expected to register the fastest regional CAGR of 10.91% through 2030. Gulf states channel petrodollar diversification funds into date-palm waste-to-fiber complexes, while Egypt and Morocco legislate airport plastic bans that immediately pivot airline-catering contracts toward molded fiber. South Africa’s Western Cape becomes an export springboard to EU supermarkets, leveraging duty-free trade corridors and reciprocal sustainability standards. Nigeria and Kenya, although still emerging, present compelling long-term demand given their young demographics and digital food delivery uptake, but infrastructure constraints around fiber preprocessing and cold-chain logistics temper near-term volumes.

Europe and North America command stable but regulation-driven demand curves. The European Climate Law’s carbon-budget caps prompt retailers to decarbonize their packaging portfolios, leading to supplier audits that now assess upstream feedstock traceability alongside mechanical performance. U.S. federal policy remains patchy; however, state-level legislation in California, New York, and Washington has imposed EPR fees, which have quietly mainstreamed molded fiber across grocery deli counters and meal-kit subscription boxes. Latin America relies on Brazil’s sugar dominance; by colocating plants within 30 km of mills, converters reduce inbound freight and secure steady bagasse supplies, even during ethanol demand spikes. Argentina follows suit, leveraging wheat-straw residues and targeting domestic meat-exporters whose European clients now specify compostable trays.

Competitive Landscape

The market structure remains fragmented, with no single player exceeding 5% of global revenue, creating a low-concentration landscape where regional champions coexist with diversified multinationals. Established fiber giants like Huhtamaki, Sonoco, and Greif deploy their global sales reach and R&D budgets to secure front-of-queue positions on multinational tenders, yet niche regional converters defend their turf through proximity to raw material sources and custom tooling agility. Vertical integration trends accelerate: leading firms either buy stakes in sugar mills or ink decade-long bagasse offtake agreements, insulating themselves from biomass price whipsaws. Patent filings cluster in three domains: bio-based barrier coatings, rapid-cycle drying ovens, and AI-enabled vision systems for defect detection, illustrating how technology points rather than raw scale confer pricing power.

Strategic investment themes include line automation to offset labor shortages and meet the ISO 9001 repeatability thresholds demanded by pharmaceutical clients. Sonoco’s South Carolina capacity upgrade increases throughput by 40% by switching from steam hot-pressing to radio-frequency drying, reducing cycle time from 11 minutes to 4 minutes and freeing up floor space for in-line die-cutting. Smurfit WestRock’s Latin American acquisition spree secures bagasse at origin, blending supply security with carbon-footprint minimization claims that resonate in EU retailer audits. Huhtamaki’s joint venture with AgriTech Solutions develops real-time fiber grading that adjusts forming-water chemistry, slashing reject rates and energy per unit.

Emerging disruptors use previously ignored agricultural residues banana stems in Ecuador, pineapple leaves in the Philippines, and hemp stalks in Canada to generate novel fiber chemistries and bypass incumbent feedstock competition. Meanwhile, carbon-credit monetization fosters a new revenue layer: converters in the European Union now earn up to EUR 35 (USD 38.5) per metric ton of verified CO₂ sequestration embodied in compostable packaging. The optionality to sell credits cushions margin compression when resin prices tumble and encourages accelerated rollout of negative-emission production lines. Overall, operational excellence around feedstock integration, barrier-coating IP, and carbon-credit arbitrage determines which competitors move from regional relevance to global leadership in the bagasse and agricultural-fiber molded packaging market.

Bagasse And Agricultural-Fiber Molded Packaging Industry Leaders

Sonoco Products Company

Greif, Inc.

Mondi plc

Smurfit WestRock plc

CPS Paper Products Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Sonoco Products Company announced a USD 45 million expansion of its molded-fiber facility in South Carolina, raising annual capacity 40% and adding specialty food-contact lines.

- September 2024: Smurfit WestRock completed the USD 85 million acquisition of Brazilian producer Fibra Sul, securing three bagasse-based plants and deepening Latin American reach.

- August 2024: Mondi plc received FDA clearance for a bio-based barrier coating suitable for refrigerated foods, overcoming moisture limitations in premium meal kits.

- July 2024: Huhtamaki Oyj partnered with AgriTech Solutions to codify a standardized fiber grading protocol that harmonizes multi-fiber blends across global sites.

Global Bagasse And Agricultural-Fiber Molded Packaging Market Report Scope

| Bagasse |

| Wheat Straw |

| Rice Straw |

| Bamboo Fiber |

| Other Material Types |

| Plates and Bowls |

| Trays and Clamshells |

| Cups and Lids |

| Containers |

| Other Product Types |

| Food and Beverages |

| Consumer Goods |

| Foodservice |

| Healthcare and Pharmaceuticals |

| Industrial |

| Other End-use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | Bagasse | ||

| Wheat Straw | |||

| Rice Straw | |||

| Bamboo Fiber | |||

| Other Material Types | |||

| By Product Type | Plates and Bowls | ||

| Trays and Clamshells | |||

| Cups and Lids | |||

| Containers | |||

| Other Product Types | |||

| By End-use Industry | Food and Beverages | ||

| Consumer Goods | |||

| Foodservice | |||

| Healthcare and Pharmaceuticals | |||

| Industrial | |||

| Other End-use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast value of the bagasse and agricultural-fiber molded packaging market in 2030?

The sector is projected to reach USD 5.1 billion by 2030, reflecting a 9.77% CAGR over 2025-2030.

Which material currently leads share in global shipments?

Bagasse accounts for 43.58% of 2024 volume thanks to proximity to sugar mills and established processing know-how.

Which product segment is expanding fastest?

Cups and lids are advancing at an 11.28% CAGR because beverage operators are shifting away from PE-lined paper cups.

Why is Asia-Pacific the largest regional base?

The region integrates abundant agricultural waste streams, skilled labor, and export-oriented converting hubs, enabling cost-competitive supply.

What key restraint limits adoption in premium food applications?

Moisture and oil-resistance constraints still restrict molded-fiber penetration into refrigerated and grease-intensive formats, although new bio-based coatings are narrowing the gap.

Page last updated on: