Anti-Aging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

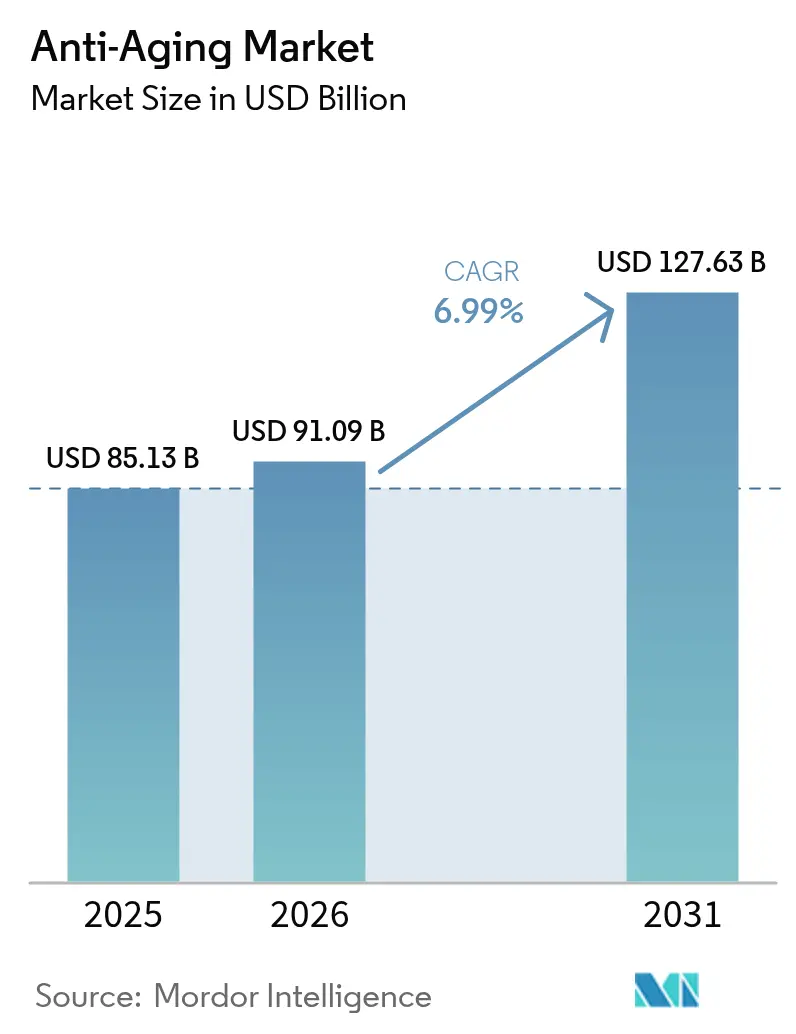

| Market Size (2026) | USD 91.09 Billion |

| Market Size (2031) | USD 127.63 Billion |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

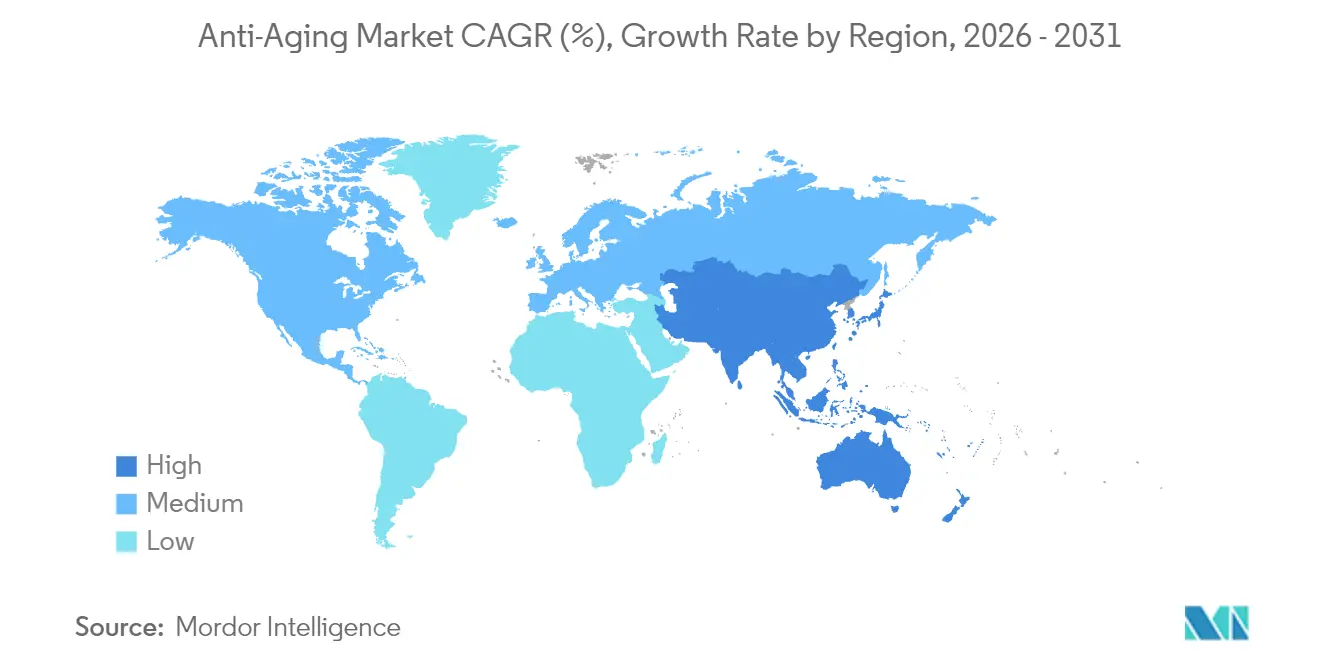

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Aging Market Analysis by Mordor Intelligence

The Anti-Aging Market size was valued at USD 85.13 billion in 2025 and estimated to grow from USD 91.09 billion in 2026 to reach USD 127.63 billion by 2031, at a CAGR of 6.99% during the forecast period (2026-2031).

Accelerated urbanisation, longer life expectancy, and digital commerce adoption are steering sustained spending on appearance-enhancing solutions. Demand is further lifted by rising male grooming participation, rapid uptake of minimally invasive procedures, and the mainstreaming of ingestible beauty products. Capital inflows into longevity science are broadening the innovation pipeline, while artificial-intelligence (AI) tools allow precise formulation, diagnosis, and direct-to-consumer engagement. At the same time, regulatory tightening in the United States and the European Union is elevating compliance costs, nudging the industry toward larger, better-resourced players.

Key Report Takeaways

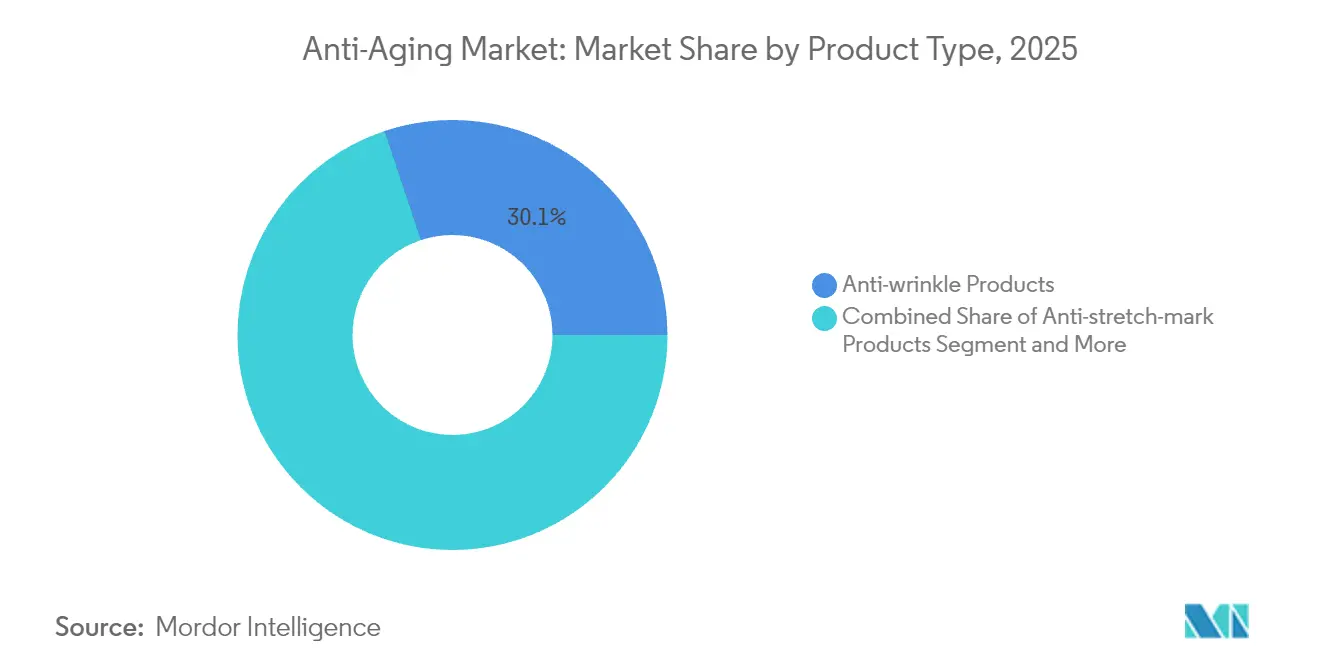

- By product type, anti-wrinkle products held 30.12% of anti-aging market share in 2025, whereas dermal fillers and injectables are projected to climb at a 9.78% CAGR to 2031.

- By device type, radio-frequency systems led with 27.10% revenue contribution in 2025; laser and light-based platforms are set to post a 10.31% CAGR through 2031.

- By application, anti-wrinkle treatment commanded a 35.74% of the market size in 2025, and cellulite reduction is advancing at a 12.66% CAGR to 2031.

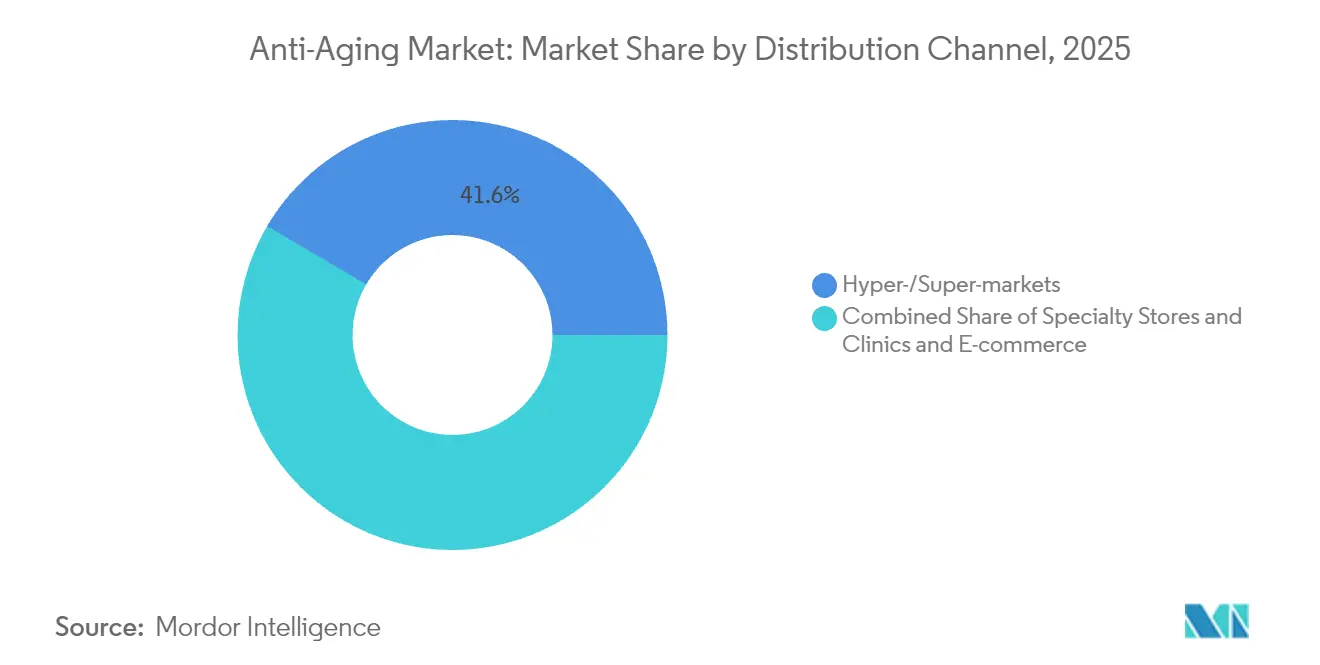

- By distribution channel, hyper-/supermarkets captured 41.55% of anti-aging market share in 2025, while e-commerce is expanding at a 14.95% CAGR from 2026–2031.

- By end-user, hospitals and surgery centres accounted for 41.40% of the market size in 2025; the at-home segment is growing at a 9.62% CAGR through 2031.

- By geography, North America retained 37.10% revenue share in 2025; Asia-Pacific is forecast to record a 9.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anti-Aging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population expansion | +1.8% | Global with peak effect in North America & Europe | Long term (≥ 4 years) |

| Rising demand for minimally invasive procedures | +1.5% | North America & Europe, spreading to Asia-Pacific | Medium term (2–4 years) |

| Growing male grooming & self-care spend | +1.2% | Asia-Pacific leading, followed by North America | Medium term (2–4 years) |

| AI-driven personalised skin-care algorithms | +0.9% | Global, early adoption in North America & Asia-Pac | Short term (≤ 2 years) |

| Nutricosmetics convergence | +0.7% | Europe & North America first, then worldwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Aging Population Expansion

The share of people aged 65 and above rose to 10.3% in 2024 and is forecast to double by 2074, lifting lifetime spending on appearance maintenance. Affluent retirees are prioritising prevention over correction, fuelling uptake of peptide-rich creams, collagen boosters, and energy-based treatments. Marketers now frame messaging around “healthy longevity” rather than “anti-wrinkle fixes”, encouraging regular routines earlier in life. Investments in age-modifying biotech rose markedly, pointing to sustained product replenishment cycles and premiumisation. Together, these factors create a durable consumption base that underpins long-range revenue certainty for the market.

Rising Demand for Minimally Invasive Aesthetic Procedures

Botulinum toxin, hyaluronic-acid fillers, and fractional devices have shifted from exclusive clinics to mainstream wellness centres. FDA clearance for Evolysse Form and Evolysse Smooth in February 2025 underscores regulatory acceptance of technology that preserves native hyaluronic structure for natural-looking outcomes. Social media normalisation drives first-time users in their thirties who see injectables as preventive. Procedure downtime has fallen, pricing is increasingly transparent, and loyalty programmes keep patients returning. These attributes collectively raise visit frequency and enlarge the total addressable market.

Growing Male Grooming & Self-Care Spend

Shifting masculinity norms, celebrity endorsements, and K-beauty influence have accelerated male skin-care adoption, especially in South Korea, where 75% of men apply cosmetics weekly. Brands now formulate lightweight textures, neutral scents, and quick-absorption serums to fit male routines. Subscription boxes and app-based skin analyses promote repeat purchasing, lifting unit volumes without heavy discounting. The gender-specific opportunity adds incremental users rather than cannibalising existing female consumers, enlarging the anti-aging market.

AI-Driven Personalised Skin-Care Algorithms

Hand-held scanners such as L’Oréal’s Cell BioPrint evaluate 20,000 skin proteins in five minutes and recommend ingredient combinations matched to individual responsiveness[1]L’Oréal Groupe, “L’Oréal Groupe Unveils L’Oréal Cell BioPrint…,” Loreal-finance.com. Retailers embed these tools in stores, driving high-ticket product bundles. Tele-dermatology apps extend reach, but a JAMA review found most still lack FDA clearance or clinician oversight, raising calls for clearer standards. Even so, AI-guided personalisation encourages premium spend and higher loyalty, strengthening the competitive position of data-rich incumbents in the anti-aging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-region cosmetic regulations | −0.8% | Highest in North America & Europe | Short term (≤ 2 years) |

| Adverse effects & efficacy scepticism | −0.6% | Global with trust differentials by region | Medium term (2–4 years) |

| Ethical sourcing & sustainability pressure | −0.5% | Europe leading, spreading worldwide | Long term (≥ 4 years) |

| Data-privacy concerns in skin-analysis apps | −0.4% | Stronger enforcement in Europe & North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Region Cosmetic Regulations

MoCRA, in force since December 2023, now obliges U.S. facilities to register and list formulas with the FDA, marking the first overhaul of American cosmetic law in 85 years[2]EcoMundo, “Understanding MoCRA: Key Changes in US Cosmetic Regulations,” Ecomundo.eu. Parallel EU rules restrict specific nano-materials and introduce new labelling for potential endocrine disruptors. Compliance demands extra toxicology dossiers, quality audits, and recall readiness. Smaller brands face launch delays, and global companies must align divergent databases, which tempers near-term anti-aging market growth.

Adverse Effects & Efficacy Scepticism

Consumer literacy rises with instant access to clinical papers, user reviews, and ingredient trackers. Allegations of over-promised results or irritation can swiftly erode trust. JAMA Dermatology notes that only two of 41 AI skin apps contain regulatory disclaimers. Brands responding with double-blind studies, peer-reviewed publications, and third-party certifications regain credibility but incur higher R&D outlays, moderating profit expansion within the anti-aging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Topicals Retain the Lead Amid Injectable Momentum

Anti-wrinkle creams preserved a 30.12% anti-aging market share in 2025, translating into the highest cash contribution among consumer goods lines. Their familiarity, affordability, and self-administered format support repeat sales and allow mass retail scaling. Conversely, injectables are projected to compound at 9.78% through 2031, mirroring broader acceptance of minimally invasive care. The anti-aging market size for injectables is forecast to rise markedly as innovators such as Evolus bring Cold-X-stabilised hyaluronic gels to U.S. clinics, giving patients smoother outcomes and fewer touch-ups.

Hair-colourants continue to address greying, while UV filters benefit from rising photoaging awareness. Nutricosmetic capsules augment topical routines, reflecting a holistic turn toward inside-out skin support. L’Oréal’s Melasyl ingredient, validated in 121 studies, showcases the shift to precision actives targeting localised pigmentation. Collectively, these sub-segments underpin a diversified revenue mix that cushions cyclical shocks in the market.

By Device Type: Radio-Frequency Rules, Lasers Surge

Radio-frequency (RF) systems represented 27.10% of 2025 revenue owing to proven collagen-remodelling efficacy, minimal downtime, and compatibility with varying skin tones. They are widely installed in med-spas and now infiltrate consumer gadgets for home use, broadening access. Nevertheless, lasers and light-based devices are set to climb at a 10.31% CAGR as fractional and picosecond innovations reduce thermal damage and extend indications to pigment correction and scar revision. The anti-aging market size generated by multi-modal consoles that fuse RF, ultrasound, and IPL technologies will accelerate because practitioners can offer personalised protocols in one sitting.

Micro-dermabrasion serves entry-level resurfacing, whereas ultrasound and plasma energy cater to niche tightening requests. Research into bioprinted sensory skin may soon refine efficacy testing, allowing device makers to iterate prototypes faster. As such, advanced platforms will likely displace stand-alone units over the forecast horizon, intensifying innovation rivalry in the anti-aging market.

By Application: Wrinkle Care Dominates; Cellulite Treatments Accelerate

Wrinkle reduction accounted for 35.74% of 2025 spending, reflecting universal concern across genders and ages. Continuous breakthroughs in peptide delivery, retinoid stabilisation, and neuromodulator duration reinforce its primacy. Meanwhile, cellulite reduction is on track for a 12.66% CAGR to 2031. Consumer interest surged after the commercialisation of subcision devices and injectable collagenase, which deliver visible smoothing with moderate downtime. Brands position these solutions alongside exercise and nutrition plans, underscoring body-positive yet results-oriented narratives that expand the anti-aging market.

Demand for pigmentation control remains high in Asia, where even tone signifies youthfulness. Novel actives such as Melasyl complement lasers and topical vitamin C for targeted therapy. Skin resurfacing and texture improvement attract millennials prioritising preventive maintenance. The cross-pollination of these applications ensures diversified growth strands within the anti-aging market.

By Distribution Channel: Store Dominance Faces Digital Disruption

Hyper-/supermarkets delivered 41.55% of 2025 revenue, leveraging foot traffic, price promotions, and private-label penetration. Yet e-commerce is predicted to rise at a 14.95% CAGR as mobile-first consumers seek convenience, wider assortments, and influencer validation. Asia-Pacific leads digital adoption, with platforms embedding live-stream demos and real-time AI skin diagnosis that converts viewers into buyers. Speciality stores retain authority through in-person consultations and professional-grade assortments co-developed with dermatologists. Hybrid click-and-collect models and in-store pickup anchor omnichannel engagement, safeguarding relevance across the anti-aging market.

By End-User: Hospitals Command Value; At-Home Devices Escalate Volume

Hospitals and surgery centres held 41.40% of the anti-aging market size in 2025. Board-certified specialists, anaesthesia facilities, and regulatory oversight make them hubs for complex injectables and combination laser therapies. Insurance seldom covers aesthetic services; nonetheless, patients accept facility premiums for perceived safety. In contrast, at-home devices are growing at 9.62% CAGR as manufacturers miniaturise LEDs, RF, and micro-needling into user-friendly gadgets sold online. COVID-19 lockdowns mainstreamed home-care rituals that persist post-pandemic. Dermatology clinics bridge both ends, offering expert-guided regimens and tele-follow-ups that blend clinical efficacy with lifestyle convenience, thereby expanding reach for the anti-aging market.

Geography Analysis

North America generated 37.10% of global sales in 2025, anchored by high disposable incomes, a robust clinical network, and media-driven beauty ideals. United States consumers spend heavily on neuromodulators and dermal fillers, while Canada’s market skews towards cosmeceuticals positioned for sensitive skin. MoCRA compliance costs, however, may reshape product portfolios, rewarding companies with strong regulatory teams. Cross-border e-commerce flows continue, but tariffs and labelling rules require agile supply-chain management.

Asia-Pacific is projected to log a 9.94% CAGR, benefiting from rising middle-class wealth, youth-laden populations actively adopting prevention, and social-media-driven beauty trends. Japan commands a mature USD 34 billion segment with science-oriented shoppers, whereas South Korea’s KRW 1-trillion men’s cosmetics arena showcases gender-inclusive growth. India’s anti-aging market could swell from USD 14 billion to USD 21 billion by 2027, powered by dermatology clinic chains and smartphone retail apps. Local ingredient stories—ginseng, green tea, niacinamide—differentiate brands and encourage export visibility.

Europe combines premiumisation with strict oversight. Clean beauty and ethical sourcing dominate decision criteria, aligning with the European Green Deal’s sustainability objectives. Germany and France champion natural actives, while the United Kingdom’s online channels outpace brick-and-mortar. Brexit complicates dual compliance with EU and UK statutes, pushing firms to establish parallel logistics. Mediterranean countries favour sun-care hybrids targeting photoaging, further fragmenting regional needs yet adding depth to the anti-aging market.

Competitive Landscape

The anti-aging market features moderate concentration: leading multinationals leverage scale, patents, and omnichannel footprints, yet niche challengers gain traction via focused science or demographic niches. L’Oréal, Estée Lauder, and Procter & Gamble co-invest in AI platforms to shorten formulation cycles and hyper-personalise routines. L’Oréal’s partnership with IBM models millions of ingredient permutations to cut prototype timelines by 60%. Acquisitions accelerate capabilities, typified by Bridgepoint’s USD 500 million RoC Skincare purchase that injects mature retinol franchises into a broader European network.

Device makers such as Galderma and AbbVie secure fresh indications for HA fillers targeting chin and temple hollows. Merz Aesthetics diversifies into regenerative cell banking by funding Acorn Biolabs, signalling convergence with regenerative medicine. Timeline’s CHF 56 million raise from L’Oréal and Nestlé underscores consumer-packaged-goods interest in cellular longevity actives.

E-commerce specialists gain ground through agility: Ulta Beauty’s tie-up with Haut.AI embeds AI skin diagnostics that lift average basket value. Regional independents win loyalty with culturally aligned narratives, yet escalating compliance and testing costs could prompt future consolidation, gradually raising entry barriers across the anti-aging market.

Anti-Aging Industry Leaders

L’Oréal SA

Estée Lauder Companies Inc.

Procter & Gamble Co.

Unilever PLC

Beiersdorf AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Evolus secured FDA approval for Evolysse Form and Evolysse Smooth injectable hyaluronic-acid gels featuring Cold-X technology that prolongs results within the USD 10.5 billion filler category.

- February 2025: Estée Lauder Companies partnered with Serpin Pharma to research anti-inflammatory peptides aimed at mitigating irritation and preserving skin resilience.

Global Anti-Aging Market Report Scope

As per the scope of the report, skin aging is a complex biological process, influenced by a combination of endogenous or intrinsic and exogenous or extrinsic factors. Because skin health and beauty are considered among the principal factors representing overall well-being in humans, several anti-aging strategies have been developed during the past years. The Anti-aging Market is segmented by Type (Products and Devices), Application (Anti-wrinkle Treatment, Anti-pigmentation, Skin Resurfacing, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Anti-wrinkle Products |

| Anti-stretch-mark Products |

| Hair-color Products |

| Sunscreen & UV Absorbers |

| Dermal Fillers & Injectables |

| Radio-frequency Devices |

| Laser & Light-based Devices |

| Micro-dermabrasion Devices |

| Ultrasound & Plasma Devices |

| Anti-wrinkle Treatment |

| Anti-pigmentation |

| Skin Resurfacing & Texture |

| Cellulite Reduction |

| Hyper-/Super-markets |

| Specialty Stores & Clinics |

| E-commerce |

| At-home |

| Dermatology Clinics |

| Hospitals & Surgery Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Anti-wrinkle Products | |

| Anti-stretch-mark Products | ||

| Hair-color Products | ||

| Sunscreen & UV Absorbers | ||

| Dermal Fillers & Injectables | ||

| By Device Type | Radio-frequency Devices | |

| Laser & Light-based Devices | ||

| Micro-dermabrasion Devices | ||

| Ultrasound & Plasma Devices | ||

| By Application | Anti-wrinkle Treatment | |

| Anti-pigmentation | ||

| Skin Resurfacing & Texture | ||

| Cellulite Reduction | ||

| By Distribution Channel | Hyper-/Super-markets | |

| Specialty Stores & Clinics | ||

| E-commerce | ||

| By End-user | At-home | |

| Dermatology Clinics | ||

| Hospitals & Surgery Centers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current anti-aging market size?

The anti-aging market size is USD 91.09 billion in 2026 and is projected to climb to USD 127.63 billion by 2031.

Which region is growing fastest in the anti-aging market?

Asia-Pacific is forecast to expand at a 9.94% CAGR between 2026 and 2031, outpacing all other regions.

Which product segment leads the anti-aging market?

Topical anti-wrinkle products remain the largest segment, holding 30.12% revenue share in 2025.

How are AI tools influencing the anti-aging market?

AI-powered diagnostics and formulation engines enable hyper-personalised regimens that boost basket value and brand loyalty, particularly in omnichannel retail.

What regulatory changes affect cosmetic companies today?

The U.S. MoCRA law and new EU ingredient restrictions impose mandatory facility registration, safety substantiation, and stricter labelling, increasing compliance costs for global operators.

Page last updated on: