Europe Precision Medicine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

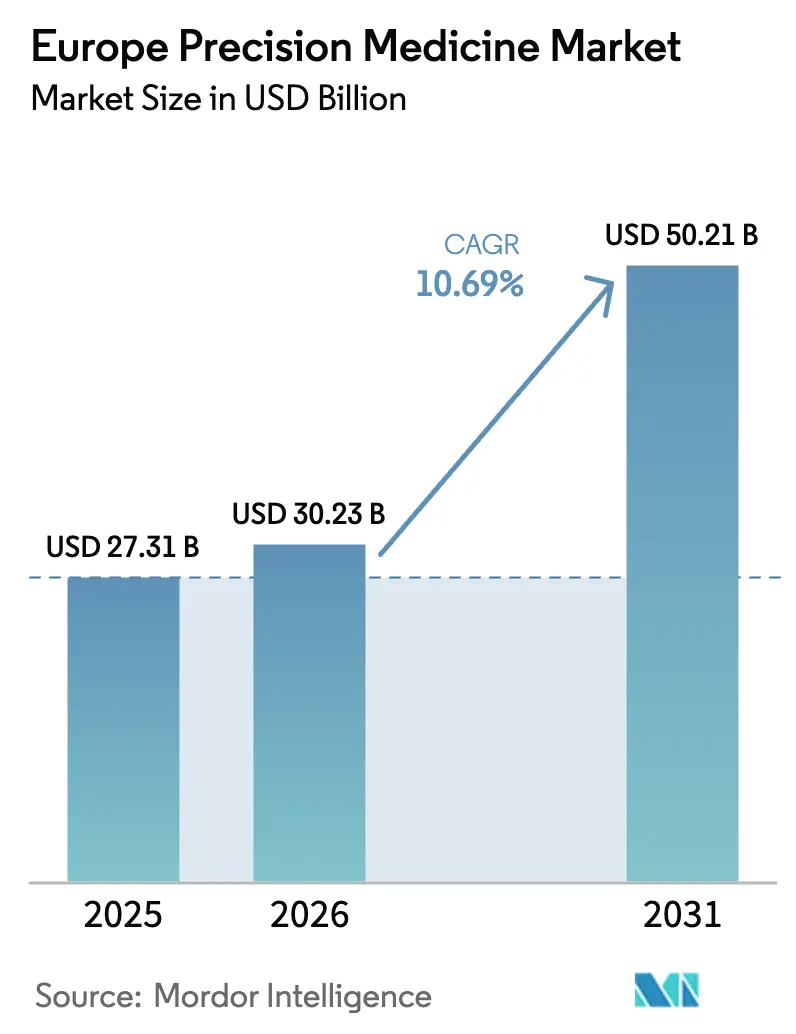

| Base Year Market Size (2025) | USD 27.31 Billion |

| Market Size (2026) | USD 30.23 Billion |

| Market Size (2031) | USD 50.21 Billion |

| Growth Rate (2026 - 2031) | 10.69% CAGR |

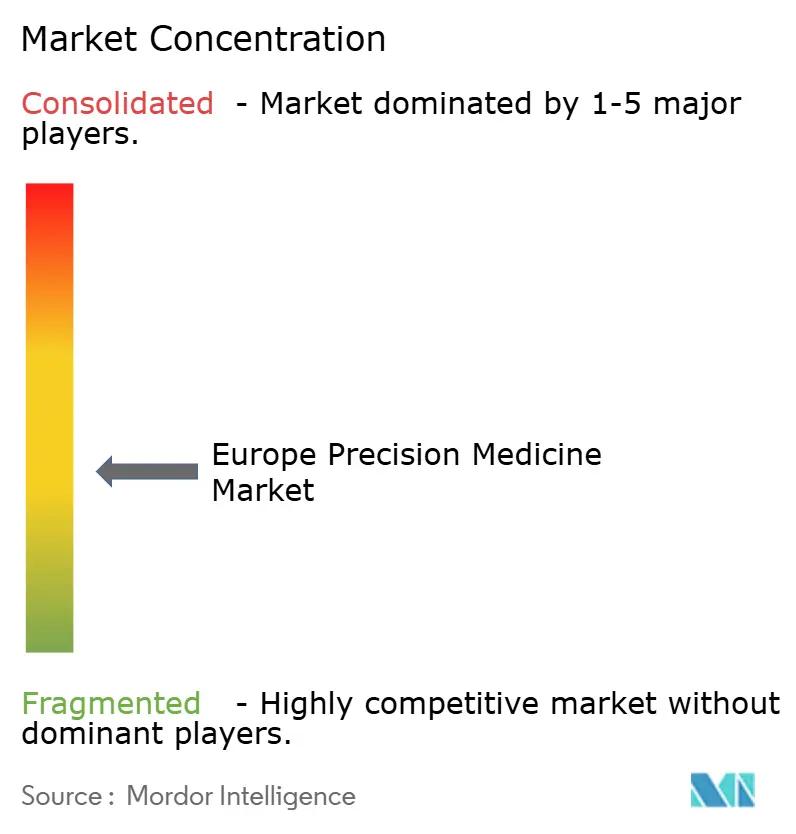

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Precision Medicine Market Analysis by Mordor Intelligence

The Europe Precision Medicine Market size is expected to grow from USD 27.31 billion in 2025 to USD 30.23 billion in 2026 and is forecast to reach USD 50.21 billion by 2031 at 10.69% CAGR over 2026-2031.

This rapid expansion stems from three intersecting forces: the European Health Data Space introduces cross-border data liquidity; population-scale genomic programs such as the Genome of Europe improve research depth; and regulatory streamlining under the EU Health Technology Assessment framework accelerates clinical adoption across 27 member states. Strong venture capital appetite for AI-native platforms amplifies the growth trajectory, while laboratory automation cuts diagnostic error rates by up to 50% and reduces turnaround times, positioning the Europe precision medicine market for resilient gains. Pharmaceutical incumbents respond through strategic acquisitions that bundle AI interpretation engines with sequencing technologies, whereas hospital groups scale multidisciplinary tumor boards to mainstream genomic profiling across oncology pathways.

Key Report Takeaways

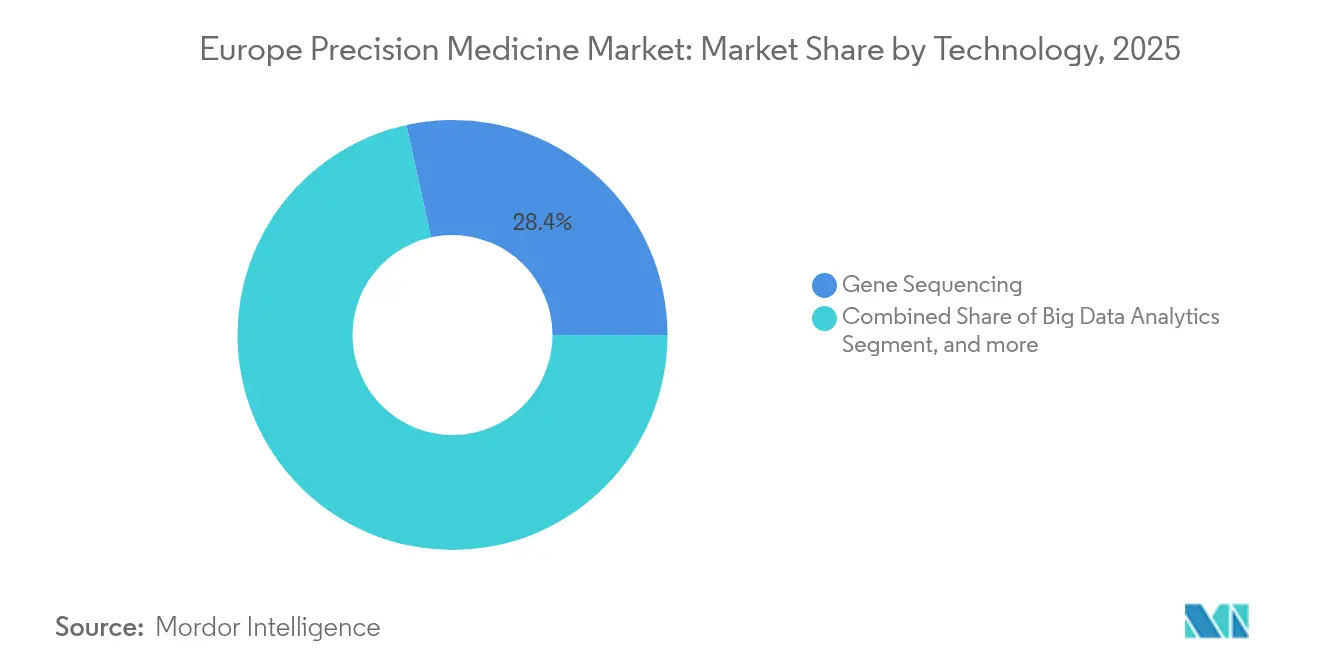

- By technology, gene sequencing led with 28.44% revenue share of the Europe precision medicine market size in 2025, while CRISPR gene editing is projected to register the fastest 13.75% CAGR through 2031.

- By application, oncology captured 39.21% share of the Europe precision medicine market size in 2025; infectious & rare diseases are forecast to expand at an 11.52% CAGR to 2031.

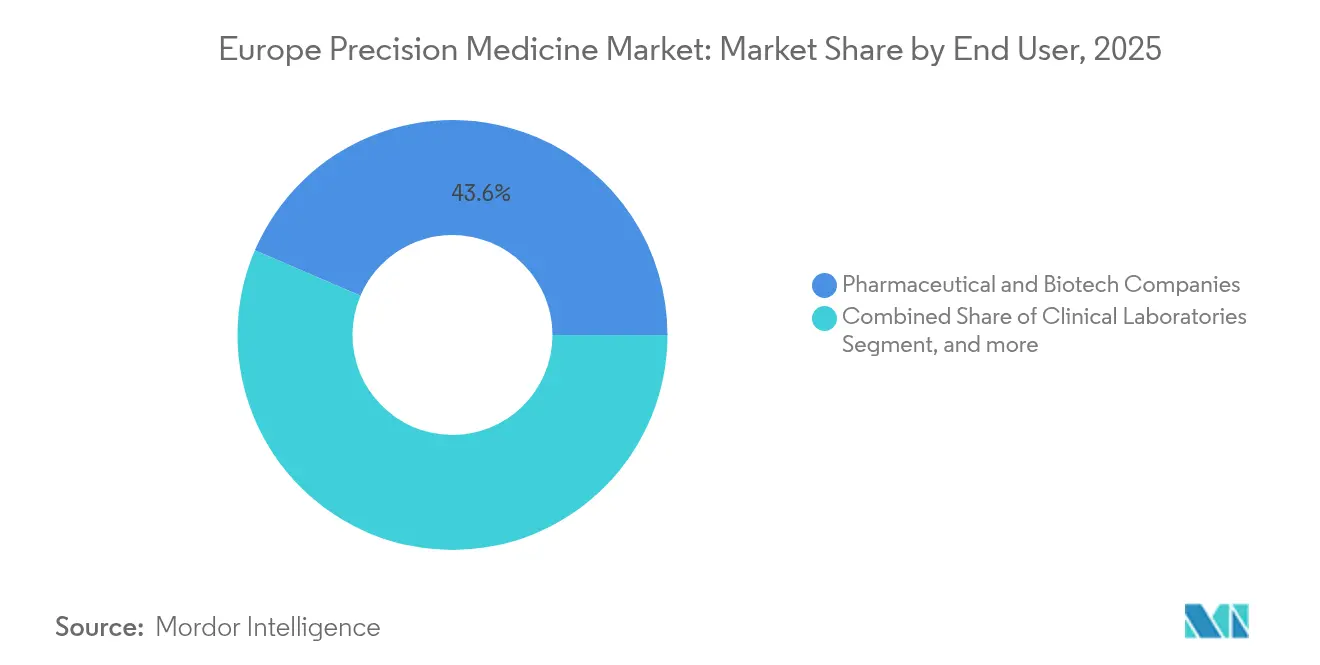

- By end user, pharmaceutical & biotech companies commanded 43.56% of the Europe precision medicine market share in 2025 as clinical laboratories recorded the highest 13.08% CAGR expected through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global precision medicine market size report represents that cumulative total.

Europe Precision Medicine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of National Genome & Biobank Programmes | +2.1% | Global, with early gains in Germany, UK, France | Medium term (2-4 years) |

| Rising Cancer & Chronic-Disease Burden in Ageing Population | +2.8% | Global, particularly acute in Western Europe | Long term (≥ 4 years) |

| Accelerated Uptake of NGS-Based Companion Diagnostics | +1.9% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| EU Health Data Space Unlocking Cross-Border Data Liquidity | +2.3% | EU core, with potential extension to associated countries | Medium term (2-4 years) |

| VC Surge into AI-Native Precision-Oncology Start-Ups | +1.2% | Global, concentrated in US, EU, China | Short term (≤ 2 years) |

| Expansion of Multidisciplinary Molecular-Tumour Boards in Hospitals | +1.4% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of National Genome & Biobank Programmes

European governments co-fund continental genomic initiatives to standardize datasets and improve healthcare equity. The Genome of Europe targets sequencing of more than 100,000 genomes, thereby resolving data fragmentation and delivering interoperable reference cohorts.[1]European Commission, “European Health Data Space,” europa.eu Germany’s TRANSLATE NAMSE study already demonstrates how integrated frameworks can secure 32% molecular diagnostic yield in ultrarare disorders.[2]Nature Genetics, “Translational diagnostics for rare diseases,” nature.com These population-scale cohorts underpin AI-driven drug discovery because diverse, well-annotated datasets improve algorithm performance and clinical trial stratification. As data custodians adopt harmonized consent procedures, start-ups gain the raw material needed to train deep-learning models for variant interpretation. Collectively, these programs establish the baseline infrastructure required for the Europe precision medicine market to shift from fragmented research toward pan-regional clinical utility.

Rising Cancer & Chronic-Disease Burden in Ageing Population

Cancer incidence across Europe is projected to increase 55% by 2040, with 2.74 million new cases already registered in 2022.[3]Economist Impact, “Cancer in Europe,” economist.com Structured molecular tumor boards improve treatment matching; Belgium’s BALLETT study reported 93% success in obtaining comprehensive genomic profiles and identified actionable markers in 81% of patients. Pharmaceutical trade groups predict that precision oncology will be standard of care beyond 2025 as evidence continues to show higher response rates and fewer adverse events E. The demographic shift thus reinforces demand for personalized therapeutics and supports sustained expansion of the Europe precision medicine market.

Accelerated Uptake of NGS-Based Companion Diagnostics

Roughly 30% of European clinical trials used precision approaches in 2024; that proportion is expected to rise to 80% by 2030. Precision trials already demonstrate 26% success compared with 10% for conventional designs, which motivates pharmaceutical firms to co-develop tests alongside therapeutics. QIAGEN plans three automated sample-prep systems by 2026 able to handle up to 192 samples in a single run, cutting plastic consumption by 50%. Laboratories pursue “Dark Lab” concepts where robotics combined with AI govern high-throughput sequencing workflows that alleviate workforce shortages. Regulatory bodies acknowledge the trend: France introduced new CCAM codes for companion diagnostics in February 2025, illustrating payer adaptation to molecular testing demands. The cumulative effect accelerates test adoption, thereby expanding the Europe precision medicine market.

EU Health Data Space Unlocking Cross-Border Data Liquidity

The European Health Data Space regulation in force since March 2025 creates the first sector-specific legal mechanism for cross-border health data exchange. Economic modeling indicates savings over 10 years and an uplift of 20-30% in the digital health sector. Promptly Health and Datavant formed an alliance to operationalize these principles, beginning in Iberia with rollouts planned for the UK and Sweden. Pharmaceutical sponsors gain access to pan-European real-world evidence that strengthens clinical development strategies, reinforcing the appeal of the Europe precision medicine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-Driven Data-Privacy & Interoperability Hurdles | -1.8% | EU core, with regulatory spillover effects | Long term (≥ 4 years) |

| Fragmented Reimbursement for Biomarker Testing | -2.1% | Global, particularly challenging in emerging markets | Medium term (2-4 years) |

| PFAS-Linked Cost Spike for Single-Use Sequencing Consumables | -0.9% | Global, with acute impact in regulated markets | Short term (≤ 2 years) |

| Bioinformatics-Talent Shortage in CEE Laboratories | -1.3% | Central and Eastern Europe, expanding westward | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GDPR-Driven Data-Privacy & Interoperability Hurdles

Genetic data classification under GDPR requires explicit consent, creating operational friction for cross-border research consortia. Although the Health Data Space aims to streamline secondary-use provisions, divergent national interpretations persist, raising compliance costs. Industry leaders invest in federated learning that trains algorithms without centralizing raw data, yet the technical overhead may deter small laboratories. Legal uncertainty can delay multi-site trials and restrict the scale of real-world evidence studies, tempering momentum in the Europe precision medicine market.

Fragmented Reimbursement for Biomarker Testing

Member-state reimbursement policies vary widely, undermining equal access. France’s provisional CCAM codes for companion diagnostics illustrate incremental progress but remain time-limited, adding unpredictability for clinical laboratories. Italy shows inconsistent pharmacogenetics coverage even though genotype-guided prescribing reduced adverse drug reactions by 30% in the PREPARE trial. These disparities compel pharmaceutical firms to negotiate country-by-country market access, slowing test diffusion and constraining growth of the Europe precision medicine market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Gene Sequencing Anchors Infrastructure as CRISPR Catalyzes Clinical Translation

Gene Sequencing contributed 28.44% of the Europe precision medicine market size in 2025, underpinned by long-term investments such as the Genome of Europe reference cohort. Population-scale projects stabilize reagent demand and encourage platform upgrades that increase throughput and reduce per-sample cost. Vendors co-develop bioinformatics pipelines with healthcare providers, ensuring seamless workflow integration.CRISPR Gene Editing is forecast to post a 13.75% CAGR through 2031 on the back of approvals for therapies like Casgevy addressing sickle cell disease and beta-thalassemia. Early clinical successes validate in-vivo editing for hematologic disorders, prompting trial expansion into solid tumors. Europe precision medicine market share gains will continue as hospitals adopt point-of-care manufacturing models.

Big Data Analytics and AI decision-support systems register rapid uptake because laboratories seek to alleviate bottlenecks in interpretation. “Dark Labs” deploy robotics to link sample prep, sequencing, and result reporting in a closed loop that trims error rates and frees personnel for complex cases. Companion Diagnostics growth accelerates following France’s code updates, signaling payer readiness across the bloc. Downstream, Drug Discovery Platforms harness multi-omics datasets to shorten target validation timelines, while Biomarker Platforms gain traction through acquisitions such as bioMérieux securing SpinChip Diagnostics for 10-minute assays that integrate seamlessly with existing chemistry analyzers. Collectively, these trends sustain technology diversification inside the Europe precision medicine industry.

By Application: Oncology Dominance Parallels Infectious & Rare Disease Acceleration

Oncology held 39.21% of the Europe precision medicine market share in 2025 as demographic trends drove expansion of screening programs and adjuvant therapy pipelines. Tumor boards translate molecular profiles into therapeutic plans, boosting treatment uptake and improving survival outcomes. Companion tests for immune-checkpoint inhibitors now include multi-gene panels, broadening revenue streams.

Infectious & Rare Diseases will grow at an 11.52% CAGR, benefiting from real-time genomic surveillance that identifies antibiotic resistance with higher sensitivity than conventional culture. Central Nervous System applications advance as blood-based Alzheimer’s biomarkers reduce reliance on expensive PET scans. Cardiovascular use cases adopt continuous biosensing patches that feed AI models to personalize statin therapy. Immunology pipelines explore cytokine-targeted biologics, and Respiratory segments integrate genomic risk scores into COPD management, reinforcing functional breadth across the Europe precision medicine market.

By End User: Pharmaceutical Leadership Paired with Laboratory Acceleration

Pharmaceutical & biotech companies retained 43.56% stake in the Europe precision medicine market share in 2025, buoyed by acquisitions such as GeneDx purchasing Fabric Genomics to embed AI interpretation engines within commercial sequencing workflows. Firms co-develop drugs and diagnostics, extracting additional value from intellectual property and accelerating regulatory review timelines.

Clinical Laboratories will grow at a 13.08% CAGR through 2031. Automation initiatives, including QIAGEN’s upcoming sample-prep systems, increase capacity without proportional staffing increases. AI tools verify results in real time, which lowers retest rates and optimizes reagent use. Hospitals and Diagnostic Centres expand in-house NGS to support tumor boards, while Academic Institutes tap EU Framework funds for translational research. Contract Research Organisations specialize in precision trials, delivering rapid patient enrolment through genotype pre-screening. Payers and Regulatory bodies progressively align reimbursement with demonstrated clinical utility but require continuous evidence generation, shaping post-market surveillance protocols across the Europe precision medicine industry.

Geography Analysis

Germany anchors regional leadership by integrating genomic medicine into statutory insurance coverage and hosting the annual GenomDE symposium under the banner “Genommedizin. Chancen nutzen. Menschen helfen”. TRANSLATE NAMSE exemplifies the national framework by diagnosing 32% of ultrarare cases via structured workflows. Federal funding programs also equip university hospitals with high-throughput sequencers, bolstering the Europe precision medicine market size contribution from Germany.

The United Kingdom capitalizes on NHS Genome Medicine Service rollouts that embed whole-genome sequencing into routine care pathways. Policy think tanks predict strong AI adoption in the NHS through 2025 as Oracle’s acquisition of TPP consolidates electronic health records. Scotland and Wales replicate similar models to harmonize access.

France modifies reimbursement via new CCAM codes effective February 2025, easing hospital adoption of multi-gene panels. Government grants fund cell-and-gene therapy centers, while collaborations such as Euformatics and Ouilab improve NGS data pipelines. Italy contributes to the Genome of Europe by supplying reference genomes through Human Technopole’s high-capacity platforms. National studies confirm pharmacogenetic testing cuts ADRs by 30% yet reimbursement inconsistency persists.

Spain sequences 12,000 genomes within Genome of Europe under ISCIII coordination, while Basque Country centers at UPV-EHU integrate findings into regional health IT frameworks. The Netherlands and Switzerland support edge innovation, from Scailyte’s single-cell analytics to NANOSPRESSO’s decentralized gene therapy production. Sweden’s PROMISE initiative links omics researchers with hospitals to standardize pipelines. Collectively, these national actions propel the Europe precision medicine market toward cohesive yet competitive advancement across the continent.

Coverage of the precision medicine market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America, alongside detailed country-level intelligence for China, each shaped by local operating conditions.

Competitive Landscape

Competitive intensity is moderate as incumbents acquire specialized assets to broaden capabilities rather than engage in price wars. Werfen bought Omixon to add transplant diagnostics, illustrating vertical integration strategies.Partnerships gain favor over standalone development. Owkin collaborates with AWS to power generative AI pipelines that model patient genomics at scale, accelerating biomarker discovery. Hospitals enter co-development agreements with diagnostics firms to expedite test adoption.

Emerging disruptors target rare diseases and AI analytics. Intelliseq leverages cloud-native workflows to deliver turnkey genomic interpretation for small labs, while One Biosciences applies single-cell transcriptomics to drug discovery. NANOSPRESSO proposes in-hospital nanomedicine manufacturing, promising decentralized gene therapy supply chains. The Europe precision medicine market thus balances consolidation among established players with vibrant start-up formation, ensuring sustained innovation.

Europe Precision Medicine Industry Leaders

AstraZeneca PLC

Danaher Corporation

Thermo Fisher Scientific Inc.

Abbott

Qiagen N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NANOSPRESSO gene therapy delivery device project advanced toward clinical implementation, enabling hospital pharmacies to create personalized nanomedicines on-demand for rare diseases affecting 36 million EU citizens.

- June 2025: GeneDx announced acquisition of Fabric Genomics for USD 33 million, expanding access to AI-powered genomic interpretation and enhancing decentralized testing capabilities with centralized intelligence.

- September 2024: CardiaTec, a tech firm unraveling the biology of cardiovascular diseases, successfully raised EUR 5.8 million (USD 6.4 million) in seed funding. This fresh capital infusion will enable CardiaTec to broaden its platform and advance its proprietary drug targets into the preclinical phase. To facilitate this endeavor, CardiaTec has forged partnerships with 65 hospitals in the US and the UK, enabling tailored collections of human hearts for data generation.

- June 2024: The National Health Service (NHS) reported the successful treatment of its inaugural patient in England with a tailored vaccine targeting bowel cancer. This milestone is part of a clinical trial under NHS England's newly introduced Cancer Vaccine Launch Pad initiative.

Europe Precision Medicine Market Report Scope

As per the scope of the report, precision medicine, a combination of molecular biology techniques and system biology, is an emerging approach to disease treatment and prevention.

The Europe Precision Medicine Market is Segmented by Technology, Application, and Geography. By technology, the market is segmented into Big Data Analytics, Bioinformatics, Gene Sequencing, Drug Discovery, Companion Diagnostics, and Other Technologies. Other technologies are Omics Technologies, Biomarkers, etc. By application, the market is segmented into Oncology, CNS, Immunology, Respiratory, and Other Applications. Other Applications include Pharmacogenomics and Rare Diseases. By geography, the market is segmented into Germany, United Kingdom, France, Italy, Spain, Rest of Europe. The report offers the value (in USD) for the above segments.

| Big Data Analytics |

| Bioinformatics |

| Gene Sequencing |

| Companion Diagnostics |

| Drug Discovery Platforms |

| Omics Technologies |

| Biomarker Platforms |

| AI-driven Clinical Decision Support |

| CRISPR Gene Editing |

| Oncology |

| Central Nervous System (CNS) Disorders |

| Immunology & Auto-immune |

| Respiratory Diseases |

| Cardiovascular & Metabolic |

| Infectious & Rare Diseases |

| Pharmaceutical & Biotech Companies |

| Clinical Laboratories |

| Hospitals & Diagnostic Centres |

| Academic & Research Institutes |

| Contract Research Organisations |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Switzerland |

| Sweden |

| Rest of Europe |

| By Technology | Big Data Analytics |

| Bioinformatics | |

| Gene Sequencing | |

| Companion Diagnostics | |

| Drug Discovery Platforms | |

| Omics Technologies | |

| Biomarker Platforms | |

| AI-driven Clinical Decision Support | |

| CRISPR Gene Editing | |

| By Application | Oncology |

| Central Nervous System (CNS) Disorders | |

| Immunology & Auto-immune | |

| Respiratory Diseases | |

| Cardiovascular & Metabolic | |

| Infectious & Rare Diseases | |

| By End User | Pharmaceutical & Biotech Companies |

| Clinical Laboratories | |

| Hospitals & Diagnostic Centres | |

| Academic & Research Institutes | |

| Contract Research Organisations | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Switzerland | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe precision medicine market in 2026?

The Europe precision medicine market size stands at USD 30.23 billion in 2026.

What is the projected value of precision medicine across Europe by 2031?

The market is forecast to reach USD 50.21 billion by 2031, reflecting a 10.69% CAGR.

Which technology leads revenue generation?

Gene sequencing holds the largest share at 28.44% of 2025 revenue.

Which application segment is expanding fastest?

Infectious & rare diseases is set to grow at an 11.52% CAGR through 2031.

Why is CRISPR significant for precision medicine in Europe?

Regulatory approvals like Casgevy validate CRISPR therapies, driving a 13.75% segment CAGR.

How do EU regulations support market growth?

The European Health Data Space enables cross-border data sharing, improving research efficiency and market scalability.

Page last updated on: