Drug Discovery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

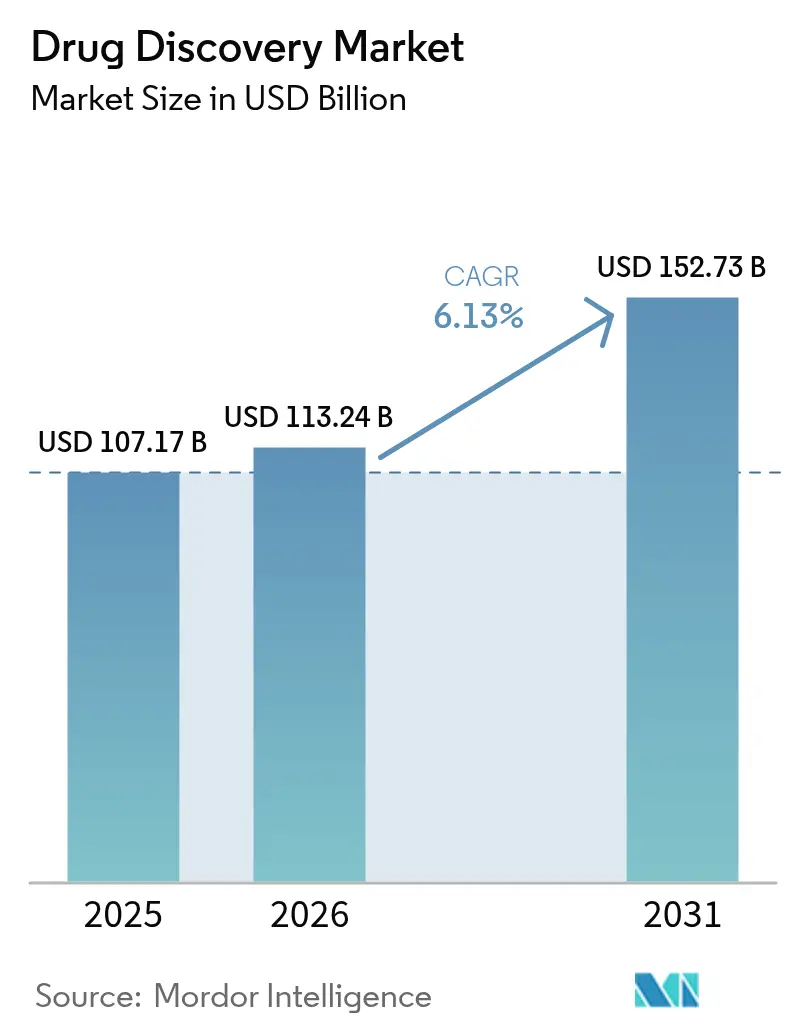

| Market Size (2026) | USD 113.24 Billion |

| Market Size (2031) | USD 152.73 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

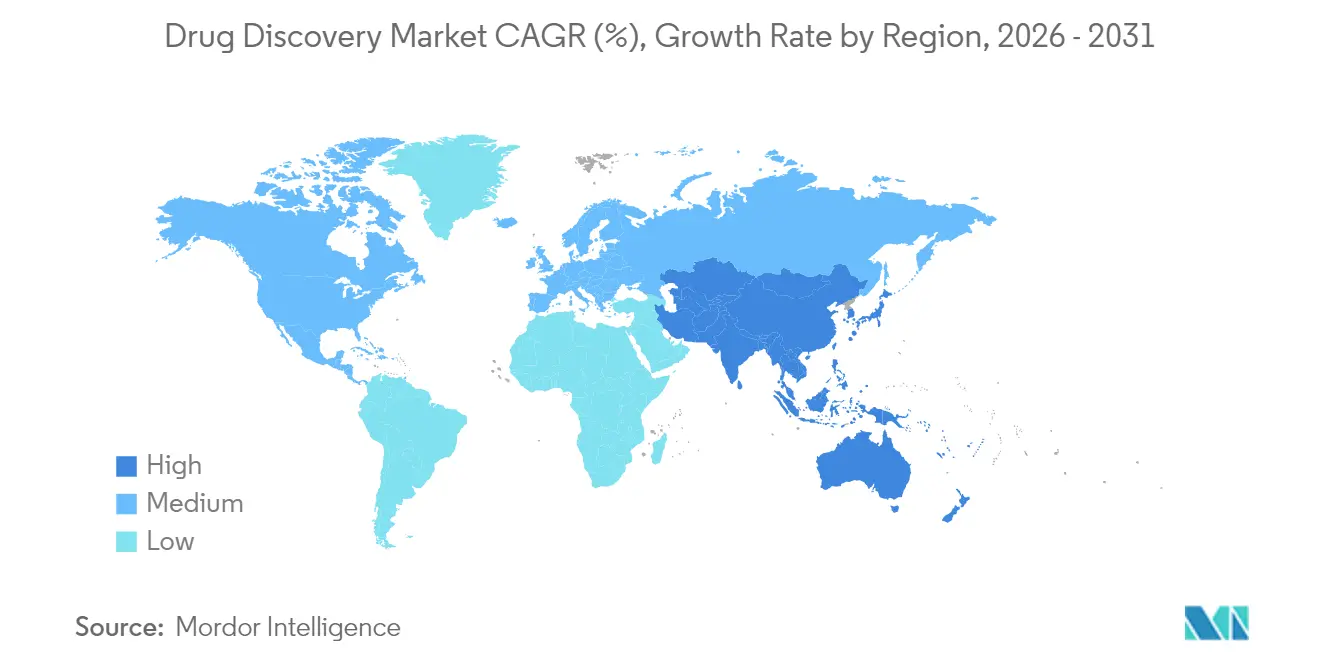

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drug Discovery Market Analysis by Mordor Intelligence

The Drug Discovery Market size is projected to be USD 107.17 billion in 2025, USD 113.24 billion in 2026, and reach USD 152.73 billion by 2031, growing at a CAGR of 6.13% from 2026 to 2031.

Large venture infusions, led by a USD 1 billion Series A for Xaira Therapeutics, confirm that investors view outsourced discovery and generative AI as the fastest route to validated candidates, especially as biologics pipelines outgrow the capacity of in-house teams. The U.S. FDA granted 45 fast-track designations for rare-disease assets in 2024, up from 37 in 2023, rewarding sponsors that can select superior pre-clinical candidates earlier in the funnel. Meanwhile, DNA-encoded libraries and high-throughput automation compress hit-to-lead timelines, while AI platforms such as Eli Lilly’s TuneLab show 30% to 50% cycle-time reductions. Cyber-biosecurity incidents and macro-inflation have lifted discovery costs by up to 12% since 2023, pushing many mid-tier sponsors toward contract research organizations that offer integrated services and zero-trust architectures.

Key Report Takeaways

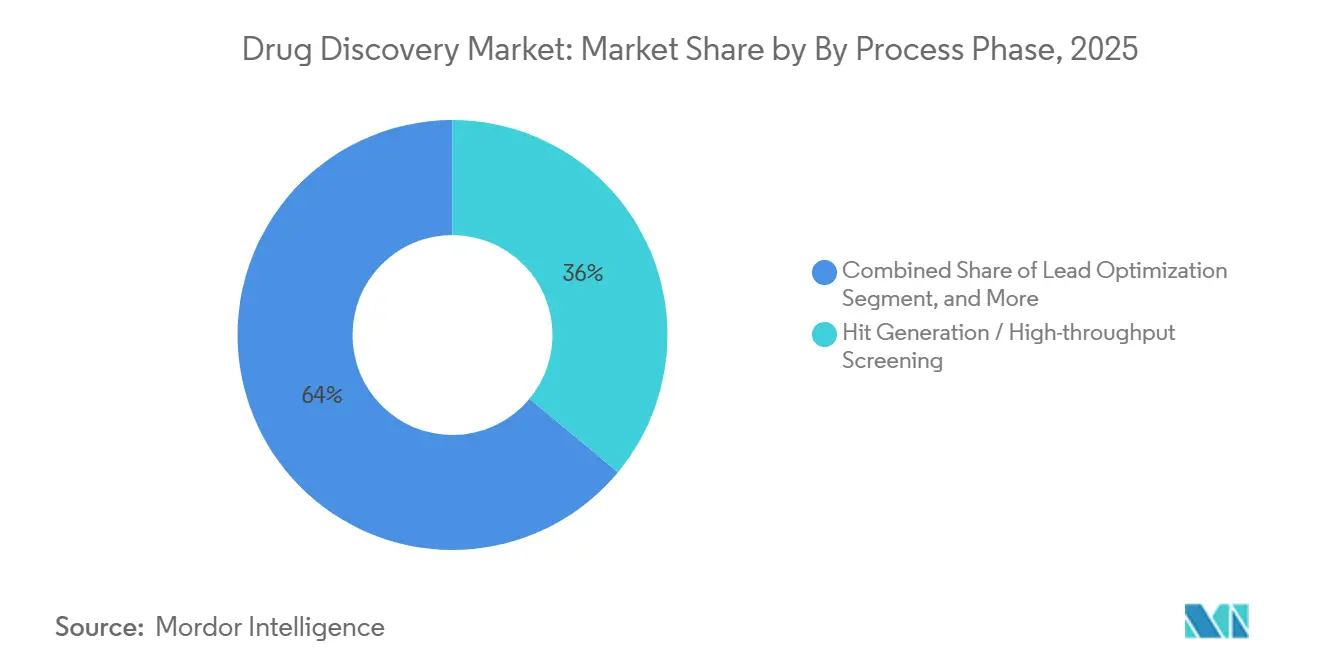

- By process phase, hit generation and high-throughput screening led with 36.02% of drug discovery market share in 2025, and pre-clinical candidate selection is forecast to expand at a 7.06% CAGR through 2031, the fastest among process phases.

- By technology, high-throughput screening controlled 34.27% of 2025 revenue, while AI and machine-learning platforms are projected to grow at 9.63% over 2026-2031.

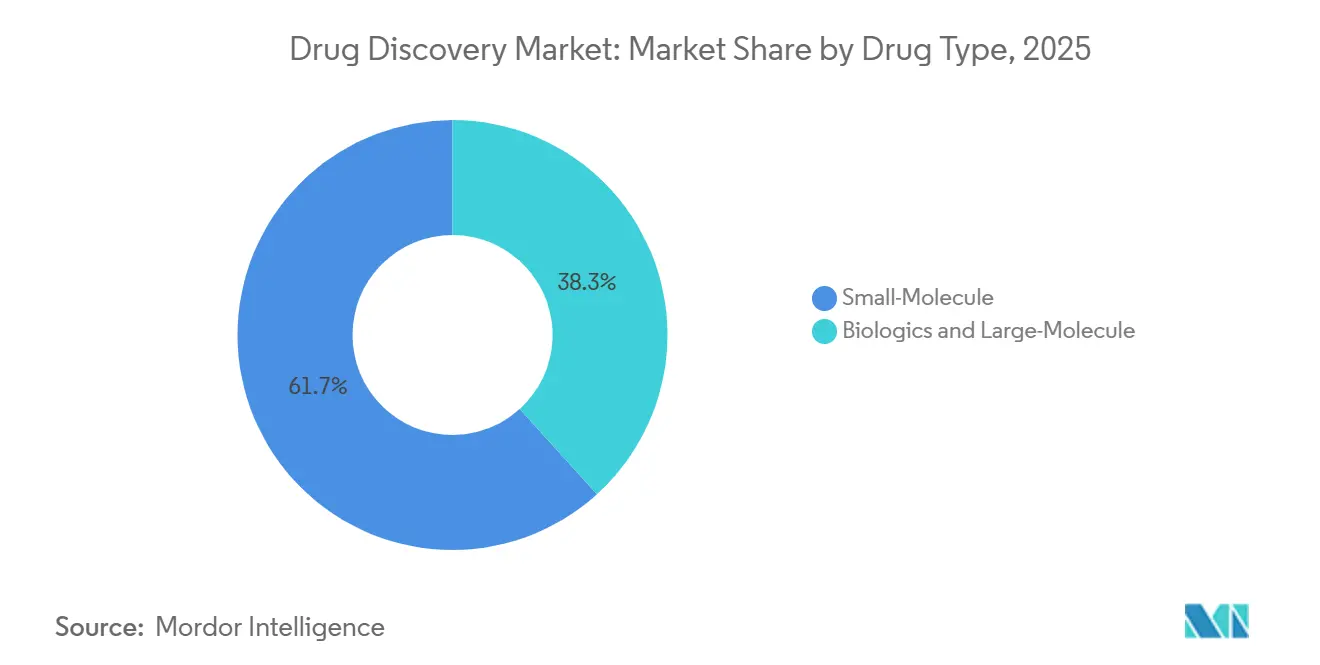

- By drug type, small-molecule programs accounted for 61.72% of 2025 revenue; biologics and large molecules are advancing at an 8.18% CAGR.

- By therapeutic area, oncology accounted for 27.78% of 2025 spend, while metabolic disorders are set to grow at an 8.41% CAGR through 2031.

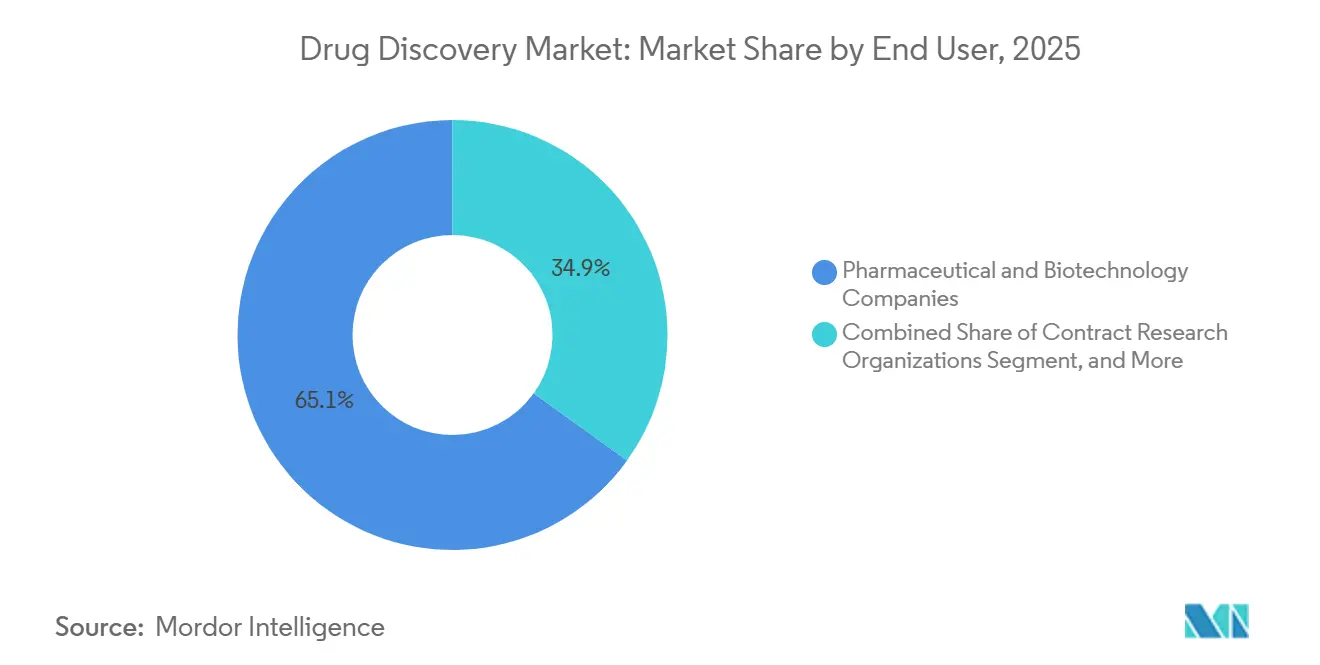

- By end user, pharmaceutical and biotechnology companies accounted for 65.08% of revenue in 2025; contract research organizations are growing at 8.52% annually.

- By geography, North America accounted for 43.78% of 2025 revenue, but Asia-Pacific is projected to expand at a 11.27% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Drug Discovery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven target identification gains mainstream adoption | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising biologics pipeline complexity boosts outsourced discovery | +0.9% | North America, Europe, Asia-Pacific core | Long term (≥4 years) |

| Venture-capital funding surge for platform biotech (post-2025) | +0.8% | North America, spill-over to Europe and select Asia-Pacific hubs | Short term (≤2 years) |

| Accelerated FDA fast-track designations for rare-disease assets | +0.7% | North America and EU, with reciprocal recognition in Japan | Medium term (2-4 years) |

| DNA-encoded libraries slash early-stage cycle-times | +0.6% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Open-science consortia lowering IP barriers in pre-competitive space | +0.5% | North America, Europe, expanding to Asia-Pacific | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Target Identification Gains Mainstream Adoption

Generative platforms reduced target-to-hit timelines by up to half during 2024-2025, as shown by TuneLab, which relied on large language models to predict binding affinities and ADMET profiles. Xaira Therapeutics demonstrated the commercial traction of this approach by announcing its first oncology candidate only 14 months after founding. NVIDIA joined forces with Eli Lilly in a USD 1 billion initiative that combines genomic and proteomic datasets to pinpoint novel targets in metabolic and neurodegenerative diseases.[1]NVIDIA Corporation, “Lilly and NVIDIA to Build AI Drug Discovery Lab,” nvidia.com Start-ups such as Chai Discovery and Genesis Therapeutics attracted USD 130 million and USD 200 million, respectively, in 2024, validating the appetite for transformer-based models that flag off-target liabilities early. The FDA issued draft guidance in 2025 that requires sponsors to document model provenance, favoring platforms with transparent data pipelines.

Rising Biologics Pipeline Complexity Boosts Outsourced Discovery

Biologics accounted for 38.28% of drug-type revenue in 2025 and are projected to grow at 8.18% through 2031, driven by antibody-drug conjugates, bispecific formats, and cell therapies that require specialized infrastructure. Contract development and manufacturing organizations responded by adding capacity; WuXi Biologics commissioned 12,000 liters of bioreactor volume in Ireland, while Lonza opened a USD 400 million facility in Singapore to support antibody discovery. High costs for post-translational optimization and immunogenicity testing have driven many sponsors to partner with external providers that maintain validated expression systems. With biologics requiring greater discovery investment yet enjoying higher clinical success rates, the economic rationale for outsourcing is growing stronger.

Venture-Capital Funding Surge for Platform Biotech

Platform biotech firms raised USD 3.2 billion across 22 early-stage rounds during 2024-H1 2025, more than doubling the capital deployed in the prior 18 months. Investors back the idea that AI-native discovery can serve several sponsors at once, capturing services revenue while retaining equity upside in each candidate. Chai Discovery, Genesis Therapeutics, Excelsior Oncology, and Basecamp Research together raised over USD 485 million to build proprietary libraries and secure high-performance compute clusters. The ability to integrate multimodal datasets, genomic, transcriptomic, and clinical, has become the decisive pitch for investors seeking scalable platforms.

Accelerated FDA Fast-Track Designations for Rare-Disease Assets

Fast-track designations climbed to 45 in 2024, compressing regulatory timelines through rolling review and more frequent sponsor meetings.[2]U.S. Food and Drug Administration, “Fast Track Designation Statistics 2024,” fda.gov The U.S. Orphan Drug Act, which provides seven-year market exclusivity and sizeable tax credits, continues to steer discovery toward diseases affecting fewer than 200,000 patients. The European Medicines Agency granted 89 orphan designations the same year, while Japan introduced a conditional pathway that accepts single-arm trials for ultra-rare conditions. These synchronous reforms encourage sponsors to file in multiple regions with one data package, shaving months off commercialization timelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating discovery costs amid macro-inflationary pressure | -0.8% | Global, acute in North America and Europe | Short term (≤2 years) |

| Clinical translation failures in novel modalities | -0.6% | Global, concentrated in gene and cell therapy programs | Medium term (2-4 years) |

| Data-integrity gaps in AI training sets | -0.4% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growing cyber-biosecurity threats to proprietary pipelines | -0.3% | Global, highest impact in North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Escalating Discovery Costs Amid Macro-Inflationary Pressure

Discovery spending per candidate rose between 8% and 12% from 2023 to 2025 as wages for specialist scientists increased and reagent supply chains tightened. Smaller biotechs with market capitalizations below USD 500 million felt the squeeze most acutely; 18 such firms exited the market in 2024 because they could not fund programs to investigational new drug filing. Contract research organizations also raised fees as they encountered higher utility and instrumentation costs, and sponsors with pre-inflation agreements saw immediate margin erosion. Many firms now consolidate work with fewer vendors and relocate early-stage activities to lower-cost science parks in India and Eastern Europe.

Clinical Translation Failures in Novel Modalities

Gene and cell therapies continue to show high attrition in human studies. Bluebird Bio paused its sickle-cell gene therapy in 2024 after two patients developed myelodysplastic syndrome, while uniQure halted a Huntington’s program following adverse events. An analysis in Nature Biotechnology found that gene-therapy approval rates were only 6% for candidates entering Phase I between 2015-2023, roughly half the success rate for small molecules.[3]Nature Biotechnology, “Gene Therapy Attrition Rates,” nature.com/nbt Manufacturing challenges add further risk, since both autologous CAR-T runs and allogeneic platforms require extensive pre-clinical validation, extending discovery timelines by as much as a year.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Phase: Pre-Clinical Validation Becomes the Focal Point

Hit generation and high-throughput screening commanded 36.02% of 2025 revenue, demonstrating the capital intensity of robotic liquid handlers and compound warehouses that dominate early discovery. Sponsors acknowledge, however, that physical assays alone cannot sustain speed in the drug discovery market, so virtual screens now filter libraries before reagents are consumed. Target identification and validation, roughly 22% of spend, benefits from consortia that release validated chemical probes, reducing redundant experiments. Lead optimization, about 28% of budgets, now couples structure–activity relationships with AI-guided ADMET profiling to mitigate downstream failure risk.

Pre-clinical candidate selection is the only phase projected to outpace the overall drug discovery market at a 7.06% CAGR, reflecting pressure to enter the clinic with greater confidence. Charles River Laboratories expanded its capacity in the United Kingdom and China by 15% to offer integrated toxicology, pharmacokinetics, and formulation packages. Thermo Fisher Scientific introduced a cloud-linked optimization toolkit that integrates in vitro screens with in silico pharmacophore modeling, reducing lead refinement time by 20%. Sponsors frequently invest an additional USD 2-5 million during this stage to avert a USD 50 million Phase II setback, a trade-off that tilts budgets toward late-stage discovery services.

By Technology: AI Platforms Tip the Scales

High-throughput screening delivered 34.27% of technology revenue in 2025, yet growth is tapering as machine-learning triage reduces laboratory throughput pressures. The drug discovery market size tied to AI platforms is projected to grow fastest, with a 9.63% CAGR, more than offsetting incremental cloud compute costs. Bioinformatics and in-silico modeling, 24% of technology spend, now ride on hyperscale infrastructure; AWS released life-sciences-tuned instances that cut molecular-dynamics simulation prices by 40%. Combinatorial chemistry’s renaissance is evident in DNA-encoded libraries that assign a unique oligonucleotide barcode to each compound, enabling sponsors to screen billions of variants in a single experiment.

HitGen’s USD 100 million funding round and DyNAbind’s USD 45 million infusion in 2024 expanded global DEL capacity. Schrödinger’s physics-based algorithms guided eight pre-clinical candidates to IND filing in 2024, a milestone that elevates virtual screening credibility beyond proof-of-concept. Exscientia dosed a first patient with an AI-designed molecule in 2024, marking a watershed moment for software-led chemistry. These wins cement AI as a defining feature of platform differentiation.

By Drug Type: Biologics Complexity Drives Outsourcing

Small molecules maintained 61.72% of 2025 revenue, anchoring the drug discovery market with advantages in oral absorption and cost of goods. However, biologics and large molecules register the swiftest climb, with an 8.18% CAGR, as antibody-drug conjugates and bispecific formats deliver potent, selective mechanisms. WuXi Biologics confirmed that 78% of its discovery clients are small- to mid-sized firms lacking mammalian cell line know-how.

Targeted protein degradation blurs modality lines. Arvinas moved three PROTAC candidates into human trials during 2024, while Nurix Therapeutics dosed its first molecular-glue program. The FDA issued draft expectations that demand characterization of both on-target and off-target degradation, elevating the analytical rigor of discovery. As a result, CROs that host proteomics platforms and ubiquitination assays secure long-term master service agreements, ensuring steady demand throughout the forecast window.

By Therapeutic Area: Metabolic Disorders Attract Renewed Capital

Oncology accounted for 27.78% of therapeutic spending in 2025, driven by immuno-oncology and precision approaches that match drugs to biomarkers. Metabolic disorders, however, are forecast to be the fastest mover at an 8.41% CAGR as GLP-1 receptor agonists expand beyond diabetes into obesity, non-alcoholic steatohepatitis, and cardiovascular disease.

Eli Lilly’s tirzepatide posted USD 5.2 billion in 2024 sales and helped open additional therapeutic avenues for dual incretin agonists. Novo Nordisk’s semaglutide generated USD 21 billion the same year, setting a commercial benchmark that shifted venture dollars toward metabolic pipelines. Central nervous system drug discovery remains challenging due to blood-brain barrier hurdles, yet sponsors continue to invest because the unmet need is massive. Cardiovascular programs explore RNA-interference and antisense oligonucleotides on the heels of positive real-world data for inclisiran, while antimicrobial resistance initiatives leverage the FDA’s QIDP incentives to secure exclusivity extensions.

By End User: CROs Capitalize on the Outsourcing Wave

Pharmaceutical and biotechnology enterprises accounted for 65.08% of end-user revenue in 2025, underscoring the continued dominance of in-house discovery among top-tier sponsors. Contract research organizations, though, are projected to grow by 8.52% and offer a safety valve for companies seeking variable-cost structures. Charles River Laboratories bought Cognate BioServices for USD 875 million to add cell-therapy capabilities and deliver end-to-end packages.

The NIH’s NCATS funded 18 such projects in 2024, allocating USD 120 million to help universities advance basic discoveries toward preclinical candidates. WuXi AppTec provides an integrated suite spanning target identification through Phase III clinical supply, while Evotec shares milestone upside in multi-partner deals. The BIOSECURE Act prompted many U.S. sponsors to steer work away from mainland China, opening opportunities for Indian CROs such as Syngene and Jubilant Biosys, each of which posted more than 25% revenue growth in 2024.

Geography Analysis

North America accounted for 43.78% of 2025 revenue in the drug discovery market, driven by venture capital density, a deep talent pool, and proximity to the FDA. Cost inflation plus talent shortages, however, constrain further acceleration and make outsourcing attractive.

Asia-Pacific is projected to climb at an 11.27% CAGR, the fastest regional clip, driven by India’s 40% to 50% cost advantage and China’s domestic demand following the BIOSECURE Act sanctions. Indian players hired an additional 2,200 scientists and expanded laboratory space by 1.2 million square feet in 2024 alone. Japan funds biotech innovation hubs that anchor joint academic–industry projects, and Singapore offers tax holidays for biologics investment, strengthening regional competitiveness.

Competitive Landscape

The top ten service providers controlled significant outsourced revenue in 2025, leaving the drug discovery market moderately fragmented. Acquisition activity, therefore, functions as a hedge against margin compression. Charles River Laboratories acquired Cognate BioServices, while Thermo Fisher Scientific bought CorEvitas for USD 912 million to infuse discovery with real-world evidence analytics.

Technology integration is the prime differentiator. Evotec’s model of co-investing alongside sponsors generated EUR 680 million in 2024, underscoring that risk-sharing can out-earn pure fee-for-service contracts. Patent filings for AI-based discovery tools jumped 120% from 2022 to 2024, with Schrödinger, Exscientia, and Recursion together submitting 340 applications. Platforms that document data lineage now enjoy a regulatory edge under the FDA draft guidance on AI-generated candidates.

Market newcomers such as Xaira Therapeutics, Chai Discovery, and Genesis Therapeutics harness generative algorithms to slash timelines, yet they must still prove that in-silico predictions translate into clinical success. White space remains in rare-disease discovery, where small patient cohorts discourage Big Pharma from pursuing in-house programs. As sponsors demand cradle-to-IND capabilities, vendors that combine bioinformatics, wet-lab automation, and regulatory expertise are likely to consolidate share over the forecast horizon.

Drug Discovery Industry Leaders

Eli Lilly and Company

Bristol-Myers Squibb Company

Novartis AG

Bayer AG

AbbVie Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mount Sinai launched the AI Small Molecule Drug Discovery Center to fast-track molecule design against oncology and neurodegenerative targets.

- January 2025: Johnson & Johnson acquired Intra-Cellular Therapies for USD 14.6 billion, fortifying its neuroscience franchise with Caplyta and pipeline assets.

Global Drug Discovery Market Report Scope

As per the scope of the report, drug discovery is a process aimed at identifying a compound that is therapeutically useful in treating and curing diseases. Typically, a drug discovery effort addresses a biological target that has been shown to play a role in the development of the disease or starts from a molecule with interesting biological activities. In the recent past, drug discovery has evolved significantly with emerging technologies, helping the process become more refined, accurate, and time-consuming.

The drug discovery market is segmented by drug type (small molecule drugs and biologic drugs), technology (high throughput screening, pharmacogenomics, combi natorial chemistry, nanotechnology, and other technologies), end user (pharmaceutical companies, contract research organizations (CROs), and other end users), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers market forecasts and revenues in terms of value in USD million for the above segments.

| Target Identification & Validation |

| Hit Generation / High-throughput Screening |

| Lead Optimization |

| Pre-clinical Candidate Selection |

| High-throughput Screening (HTS) |

| Bioinformatics & In-silico Modelling |

| Artificial Intelligence & Machine Learning |

| Combinatorial Chemistry |

| DNA-Encoded Libraries & Other Emerging Tech |

| Small-Molecule |

| Biologics & Large-Molecule |

| Oncology |

| Central Nervous System Disorders |

| Cardiovascular Diseases |

| Infectious Diseases |

| Metabolic Disorders |

| Other Therapeutic Areas |

| Pharmaceutical & Biotechnology Companies |

| Contract Research Organizations (CROs) |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Process Phase | Target Identification & Validation | |

| Hit Generation / High-throughput Screening | ||

| Lead Optimization | ||

| Pre-clinical Candidate Selection | ||

| By Technology | High-throughput Screening (HTS) | |

| Bioinformatics & In-silico Modelling | ||

| Artificial Intelligence & Machine Learning | ||

| Combinatorial Chemistry | ||

| DNA-Encoded Libraries & Other Emerging Tech | ||

| By Drug Type | Small-Molecule | |

| Biologics & Large-Molecule | ||

| By Therapeutic Area | Oncology | |

| Central Nervous System Disorders | ||

| Cardiovascular Diseases | ||

| Infectious Diseases | ||

| Metabolic Disorders | ||

| Other Therapeutic Areas | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Contract Research Organizations (CROs) | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is spending on outsourced discovery expected to grow through 2031?

Contract research organizations are projected to post an 8.52% CAGR, outpacing the overall drug discovery market.

Which region is forecast to record the quickest revenue growth?

Asia-Pacific shows the fastest trajectory with an 11.27% CAGR as sponsors leverage India’s cost advantage and China’s domestic capacity.

What technology segment is expanding the most rapidly?

AI and machine-learning platforms are advancing at 9.63% because they cut target-to-candidate timelines by up to half.

Why are biologics programs driving greater outsourcing?

Complex requirements for antibody engineering and cell-line development make external providers with specialized infrastructure more cost-effective than in-house labs.

What is the outlook for metabolic disorder programs?

Metabolic disorders are forecast to grow at an 8.41% CAGR as GLP-1 receptor agonists expand into obesity and cardiovascular indications.

Page last updated on: