Neurology Clinical Trials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

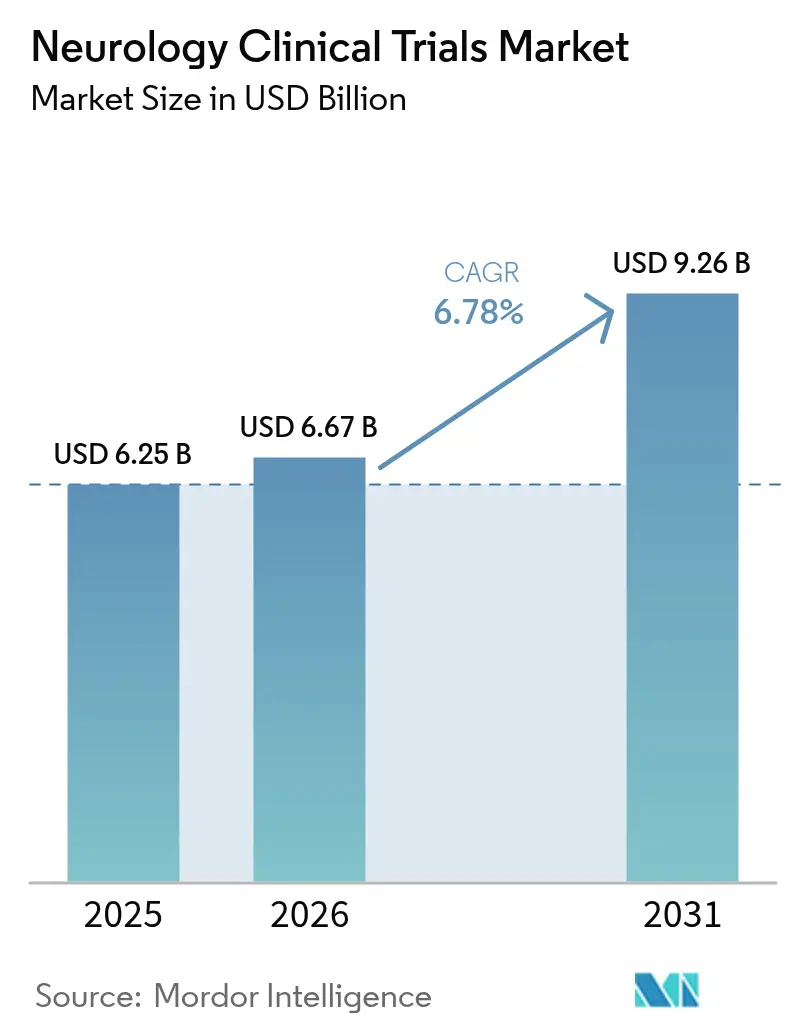

| Market Size (2026) | USD 6.67 Billion |

| Market Size (2031) | USD 9.26 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neurology Clinical Trials Market Analysis by Mordor Intelligence

The neurology clinical trials market size is expected to grow from USD 6.25 billion in 2025 to USD 6.67 billion in 2026 and is forecast to reach USD 9.26 billion by 2031 at 6.78% CAGR over 2026-2031. Growth stems from the convergence of regulatory modernization, expanding digital-health toolkits and intensified central nervous system (CNS) research spending that together accelerate time-to-market for breakthrough neurotherapies. Rapid uptake of decentralized and hybrid study models trims site-visit burdens, broadens geographic reach and improves data density, while validated fluid and imaging biomarkers streamline early-phase go/no-go decisions. Venture investment into neuro-start-ups hit record levels in 2025, propelled by confidence in gene, cell and brain-computer interface (BCI) platforms that promise disease-modifying effects in previously intractable indications. Contract research organizations (CROs) continue to widen neuroscience capabilities, providing end-to-end support—including adaptive-design statistics, decentralized operations and complex neurosurgical logistics—that smaller biotech sponsors increasingly outsource. Meanwhile, the U.S. Food and Drug Administration’s (FDA) accelerated pathways for neurodegenerative diseases shorten development timelines and encourage first-in-class approaches.

Key Report Takeaways

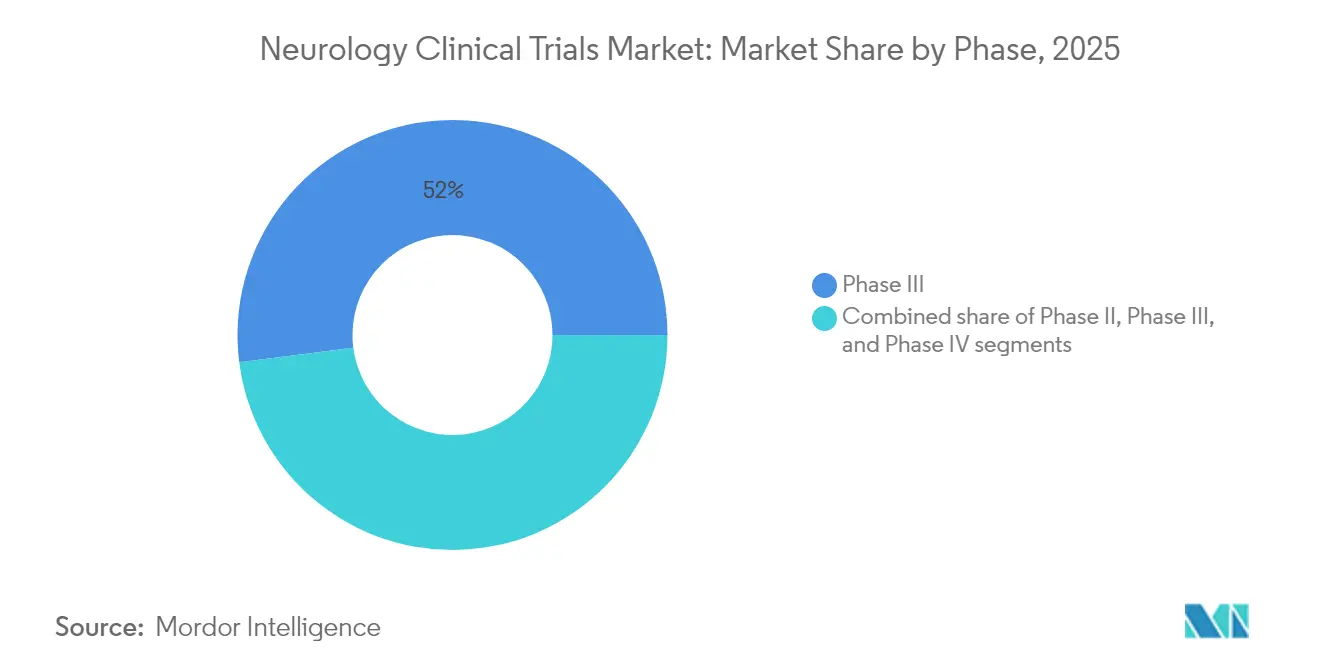

- By phase, Phase III studies led with 52.02% of the neurology clinical trials market share in 2025, while Phase I trials are projected to post the highest 17.35% CAGR through 2031.

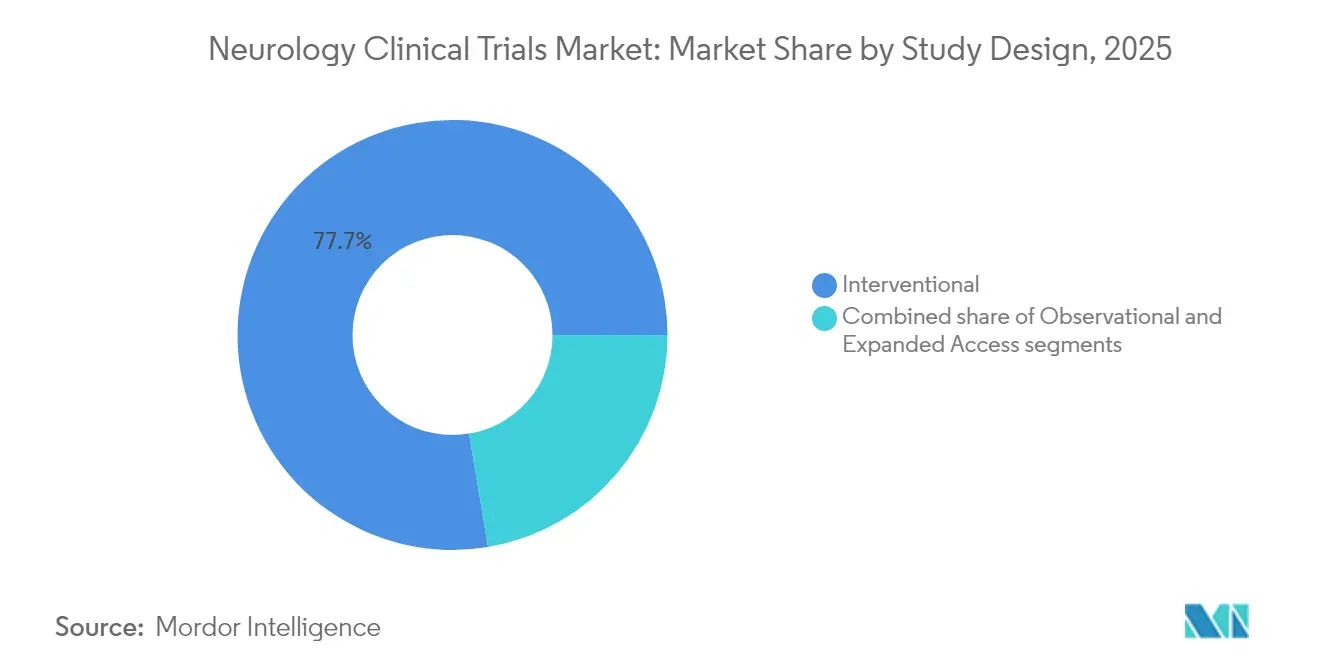

- By study design, interventional trials accounted for 77.65% revenue in 2025; decentralized and hybrid formats are poised to grow at a 21.05% CAGR to 2031.

- By indication, Alzheimer’s disease held 23.21% share of the neurology clinical trials market size in 2025; gene and cell therapy programs for amyotrophic lateral sclerosis (ALS) are expected to expand at a 23.60% CAGR to 2031.

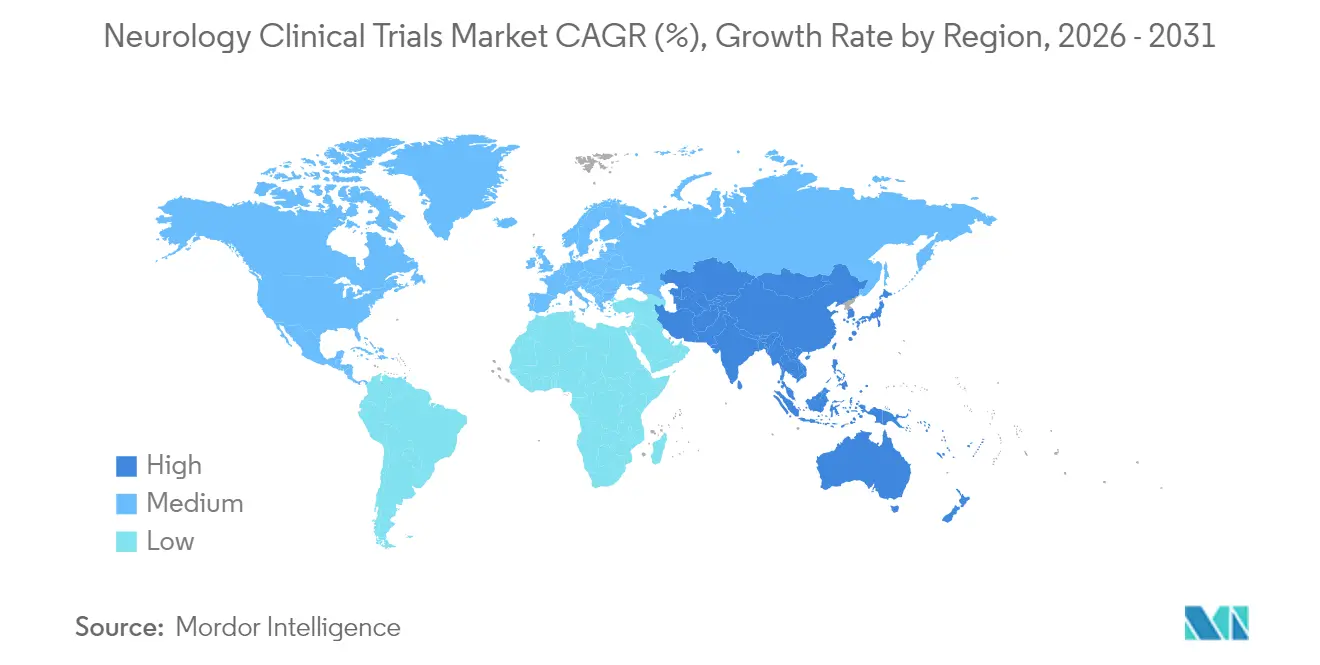

- By geography, North America captured 41.88% revenue in 2025, while Asia-Pacific is the fastest-growing region with a 6.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neurology Clinical Trials Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing global burden of neurological disorders | +1.8% | Global; strongest in aging North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Growing investment in CNS drug development | +1.5% | North America & EU core; spill-over to Asia-Pacific | Medium term (2-4 years) |

| Favorable regulatory initiatives for neurotherapeutics | +1.2% | US and EU early; global uptake | Short term (≤ 2 years) |

| Technological advancements in trial design and digital health | +1.0% | Developed markets first; global diffusion | Medium term (2-4 years) |

| Expansion of contract research organization capabilities | +0.8% | Major CRO hubs worldwide | Short term (≤ 2 years) |

| Rising adoption of precision medicine and biomarkers | +0.7% | North America & EU expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Global Burden of Neurological Disorders

Neurological conditions now affect more than 1 billion people worldwide, creating urgent demand for disease-modifying therapies that fuels clinical trial volume. Alzheimer’s disease alone impacts 55 million individuals and is projected to double by 2050, prompting a pipeline shift toward amyloid- and tau-targeting agents following FDA approvals of aducanumab and lecanemab[1]U.S. Food and Drug Administration, “Digital Health Policies for Neurological Devices,” fda.gov. Parkinson’s disease prevalence surpassed 10 million, and regenerative trials such as Kyoto University’s iPS-cell dopaminergic progenitors showed motor-score improvements in 4 of 6 patients[2]Center for iPS Cell Research and Application, “iPS Dopaminergic Progenitors in Parkinson’s Disease,” cira.kyoto-u.ac.jp. Stroke incidence continues rising, with the Chinese tirofiban study reducing early neurological deterioration by 68% versus aspirin across 10 stroke centers. Population aging therefore extends trial addressable pools and secures multi-year growth momentum for the neurology clinical trials market.

Growing Investment in Central Nervous System Drug Development

Pharmaceutical and venture investors committed record sums to CNS programs in 2025, attracted by clearer regulatory routes and transformative technology platforms. AbbVie launched a USD 2 billion alliance with Gilgamesh Pharmaceuticals to create non-hallucinogenic neuroplastogens for psychiatric disorders. Bayer advanced AB-1005 gene therapy for Parkinson’s into Phase II across four countries after favorable Phase Ib safety readouts. Eisai raised its annual venture allocation to JPY 4 billion, earmarking neurology start-ups. New specialist funds such as Nexus NeuroTech Ventures emerged to incubate BCI, gene-editing and neuro-immunology projects. Capital influx accelerates proof-of-concept timelines and diversifies modality choices.

Favorable Regulatory Initiatives for Neurotherapeutics

Global authorities introduced streamlined pathways that compress launch cycles without diluting safety oversight. The FDA re-classified digital therapeutic devices for ADHD into Class II with special controls effective September 2024, facilitating rapid clearance of software-based neuro interventions. Breakthrough Device badges for blood-based neurofilament light chain (NfL) assays and for multiple brain-computer interfaces underscore regulator openness to novel endpoints and platforms. NIH-FDA workshops in 2024 created draft frameworks for BCI clinical outcome assessments, enabling sponsors to align early with agency expectations[3]National Institutes of Health, “BRAIN Initiative Funding Opportunity 2025,” nih.gov. European harmonization projects, such as multinational protocols for transorbital electrical stimulation, further reduce bureaucratic drag. These moves lift the Neu¬ro¬science clinical trials market by clearing bottlenecks that once deterred high-risk programs.

Technological Advancements in Trial Design and Digital Health

Decentralized clinical trials (DCTs) leverage eConsent, tele-visits and wearable devices to reach immobile or cognitively impaired participants. The MIRAI Remote Study, a fully masked sham-controlled investigation of smartphone therapeutic CT-152 for major depressive disorder, validated DCT feasibility while maintaining data rigor. Precision Neuroscience obtained FDA clearance for a wireless cortical electrode array with 1,024 contacts that can reside intracranially for 30 days, supplying unprecedented neural telemetry. Virtual reality cognitive-training platforms and consumer-grade sleep-neurostimulation wearables further enrich outcome measures. Together, these tools raise data granularity, cut dropout rates and broaden recruitment catchments.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and complexity of late-phase neuroscience trials | -1.5% | Global; greatest in cost-sensitive markets | Medium term (2-4 years) |

| Stringent ethical and regulatory requirements | -1.2% | Worldwide, variable intensity | Long term (≥ 4 years) |

| Recruitment challenges due to narrow eligibility | -1.0% | Global; acute in rare diseases | Short term (≤ 2 years) |

| Limited predictive preclinical models | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost and Complexity of Late-Phase Neuroscience Trials

Large sample sizes, lengthy follow-up and intricate outcome assessments inflate per-patient costs. The HERCULES study enrolled 1,131 non-relapsing secondary progressive multiple sclerosis patients across 31 countries, illustrating the logistic scale required for progressive indications. Sanofi’s parallel Phase III trials for frexalimab further spotlight the financial load of testing novel mechanisms in both relapsing and progressive cohorts. Cell-therapy epilepsy studies demand neurosurgical centers and multi-year monitoring, compounding expenditure. These capital hurdles can deter smaller firms and limit geographic diversity of pivotal trials.

Stringent Ethical and Regulatory Requirements for CNS Studies

Cognitive impairment raises consent complexity, and implanted devices trigger long-term safety scrutiny. Neuralink’s PRIME BCI trial must observe participants for 72 months under an Investigational Device Exemption. Pediatric migraine trials like Pfizer’s BHV-3000 require dual assent processes and specialized monitoring. Such layers extend timelines and add administrative cost, tempering near-term growth in the neurology clinical trials market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Phase: Early-Stage Innovation Accelerates

Phase III held the dominant 52.02% neurology clinical trials market share in 2025, reflecting the high revenue weight of large confirmatory studies. Yet Phase I exhibits an 17.35% CAGR to 2031 as gene, cell and BCI programs proliferate. UniQure’s AMT-162 SOD1-ALS gene therapy moved into its second dosing cohort within one year, underscoring brisk early-phase throughput. Similarly, Precision’s Layer 7 safety trial exemplifies the front-loaded evaluation necessary for invasive neurotech. This burst of Phase I activity signals a robust pipeline that will replenish late-phase volumes after 2027.

Later-stage studies nonetheless remain pivotal for payer acceptance and guideline inclusion. The HERCULES success with tolebrutinib showed a 31% delay in disability progression, setting the stage for regulatory filing and commercial rollout. Post-marketing Phase IV studies—though smaller in spend—provide real-world evidence vital for label expansions, as illustrated by UCSF’s ocrelizumab lymph-node mechanism study.

By Study Design: Decentralized Models Transform Engagement

Interventional trials comprised 77.65% of 2025 revenue, anchored by drug and device efficacy evaluations. However, decentralized and hybrid formats are forecast to rise at 21.05% CAGR, propelled by digital platforms that enable remote cognitive testing, ePRO capture and telemedicine safety checks. The MIRAI Remote Study’s sham-controlled smartphone therapeutic for depression exemplified regulatory-grade decentralization. Wearable data streams—from ECG-enabled watches to home EEG headbands—feed into adaptive algorithms, facilitating earlier detection of efficacy signals and reducing site visits. Observational registries and expanded-access programs continue to yield hypothesis-generating insights but capture a smaller slice of the neurology clinical trials market size.

By Indication: Gene Therapy Drives ALS Innovation

Alzheimer’s disease retained 23.21% of 2025 revenue, buoyed by large patient numbers and new anti-amyloid approvals. Yet gene and cell therapy trials in ALS will log a 23.60% CAGR as precision approaches tackle monogenic forms. UniQure’s antisense vector AMT-162 and Biogen/Ionis’ Tofersen illustrate regulatory acceptance of nucleic-acid strategies. Parkinson’s disease benefits from cell-replacement efforts such as Kyoto University’s iPS grafts, while multiple sclerosis explores BTK inhibitors like tolebrutinib. Stroke and migraine programs progressively adopt AI imaging and digital-health adjuncts to refine endpoint measurement, keeping indication diversification high.

Geography Analysis

North America remains the gravitational center of high-complexity neuroscience research. FDA breakthrough designations for BCIs, digital therapeutics and fluid biomarkers lower regulatory opacity and entice multinational sponsors. AbbVie’s USD 2 billion neuroplastogen alliance and NIH’s USD 10 million annual BRAIN Initiative invasive-device program reinforce capital depth. Extensively networked CROs such as IQVIA and Syneos supply specialized neurosurgical and remote-monitoring logistics, sustaining regional dominance.

Asia-Pacific’s momentum derives from broad policy backing and cost-efficient infrastructure. Shanghai StairMed’s invasive BCI trial places China among the few nations executing cutting-edge neuroimplants. The 10-center Chinese tirofiban stroke study proved capability to manage >1,000-patient acute trials. Japan’s iPS Parkinson’s therapy successes ignite regenerative-medicine pipelines. Coupled with rising middle-class neurological disease burden, these factors shift sponsor footprints eastward.

Europe leverages pan-regional networks to run multi-country trials efficiently. Germany’s EPIsoDE psilocybin investigation, the UK’s temporal-interference Alzheimer’s stimulation project and EU-wide Long-COVID neuro-autoantibody trials illustrate breadth of therapeutic exploration. Harmonized ethics review under EMA guidelines shortens setup times, while Horizon Europe grants offset costs for academia–industry consortia.

Competitive Landscape

Market competition is balanced between large pharma incumbents and agile biotech innovators, with moderate overall concentration. Big-cap companies dominate late-phase programs in prevalent diseases: Sanofi in multiple sclerosis, Novartis in migraine and AbbVie in psychiatric neuroplastogens. Biotechs drive frontier modalities—UniQure in gene therapy, Precision Neuroscience in BCI and Neurona in cell therapy—often partnering to access scale manufacturing or global trial networks.

Strategic collaborations drive differentiation, with AbbVie's pact with Gilgamesh Pharmaceuticals providing early access to non-hallucinogenic psychedelics and helping distinguish it from traditional SSRI competitors. Charles River–Insightec and Bayer–AskBio illustrate horizontal alliances mixing CRO, device and gene-therapy expertise. Digital-health entrants compete by validating software therapeutics through randomized studies, with MIRAI Remote positioning to capture antidepressant adherence niches.

CROs increasingly shape outcomes by embedding decentralized capabilities and neuro-imaging analytics. IQVIA's proprietary patient-finding algorithms cut recruitment windows, while Syneos merges remote rater platforms with onsite neurosurgical oversight. Such service differentiation pressures smaller CROs, spurring niche specialization (e.g., seizure detection wearables).

Neurology Clinical Trials Industry Leaders

Novartis AG

Biogen

F. Hoffmann-La Roche Ltd

Eli Lilly & Co.

Abbvie, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nexus NeuroTech Ventures launched in San Francisco to back BCI and neuro-immune start-ups, offering lab space plus operational mentorship.

- May 2025: Shanghai StairMed Technology completed China’s first prospective invasive BCI trial, enabling game control via thought within one month of implantation.

- April 2025: Precision Neuroscience secured FDA clearance for its 1,024-electrode Layer 7 wireless cortical array permitting 30-day implantation.

- April 2025: Kyoto University reported 4-of-6 patient motor improvement in its Phase I/II iPS-cell Parkinson’s study without serious adverse events.

- February 2025: Neurona Therapeutics initiated the Phase 3 EPIC study of NRTX-1001 interneuron cell therapy for drug-resistant focal epilepsy.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the neurology clinical trials market as all value generated from Phase I-IV interventional, observational, and expanded-access studies that evaluate drugs or biologicals intended to treat, manage, or diagnose disorders of the central and peripheral nervous systems. Revenue reflects sponsor spend on investigator sites, contract research services, data management, and enabling technologies.

Scope exclusion: device-only neurodiagnostic trials and post-marketing registries are outside the baseline.

Segmentation Overview

- By Phase

- Phase I

- Phase II

- Phase III

- Phase IV

- By Study Design

- Interventional

- Observational

- Expanded Access

- By Indication

- Epilepsy

- Stroke

- Alzheimer's Disease

- Parkinson's Disease

- Multiple Sclerosis

- Migraine

- Amyotrophic Lateral Sclerosis

- Other Indications

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Telephone interviews and online surveys with medical directors at CROs, neurologists running major sites, and procurement managers at mid-size biopharma across North America, Europe, and Asia-Pacific clarify phase-wise cost curves, adoption of decentralized models, and average patient retention. These conversations fill data gaps and ground the desk findings in real-world practice before we finalize assumptions.

Desk Research

We begin with structured desk work that screens tier-1, publicly available sources such as ClinicalTrials.gov, the World Health Organization's ICTRP, FDA-CDER approval archives, OECD Health Statistics, and trial cost benchmarks from peer-reviewed journals like Neurology. Company 10-Ks and investor decks add pipeline visibility, while D&B Hoovers and Dow Jones Factiva supply spend signals for listed and private sponsors. Questel patent data help trace emerging modalities. The sources named illustrate the range we reference; many additional outlets are consulted for cross-checks and context.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid model is applied. We first reconstruct global spend from registered trial counts multiplied by region-specific average cost per patient, then corroborate totals through sampled CRO revenue roll-ups and anonymized contract checks. Key variables fed into the model include annual neurology trial starts, average enrollment size, cost-per-patient inflation, dropout rates, sponsor outsourcing ratios, and share of decentralized trials. Multivariate regression with scenario analysis projects each driver to 2030, and outputs are stress-tested against expert consensus. Where bottom-up samples under-represent smaller geographies, scaling factors based on historical enrollment shares bridge the gap.

Data Validation & Update Cycle

Outputs pass variance screens versus public sponsor spend and regulator fee data. A second analyst reviews formulas, after which variances above three percentage points trigger re-contact of at least one external expert. Reports refresh yearly, with interim updates when material events such as a pivotal Alzheimer's read-out move the market.

Why Mordor's Neurology Clinical Trials Baseline Stands Firm

Published estimates often differ; scope choices, cost inflation paths, and refresh timing usually explain the spread.

Key gap drivers include narrower indication baskets, omission of hybrid and decentralized spend, or the use of historical flat cost multipliers.

Mordor Intelligence applies a refreshed 2025 base, adjusts for country-level inflation, and captures technology-enabled services that some publishers still treat as ancillary.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.25 B (2025) | Mordor Intelligence | - |

| USD 5.84 B (2024) | Regional Consultancy A | Earlier base year and exclusion of Asia-Pacific tier-2 countries |

| USD 6.50 B (2024) | Global Consultancy B | Includes device-only neurodiagnostic trials and broader post-marketing registries |

The comparison shows how figures shift when scope or cost levers change. By grounding every step in auditable trial registries and live expert inputs, we deliver a balanced, transparent baseline that decision-makers can rely on.

Key Questions Answered in the Report

How large is the neurology clinical trials market today?

The neurology clinical trials market size is USD 6.67 billion in 2026 and is projected to reach USD 9.26 billion by 2031.

Which trial phase is growing fastest?

Phase I studies show the highest growth with an 17.35% CAGR as gene, cell and brain-computer interface programs multiply.

Which indication leads by revenue?

Alzheimer’s disease trials account for 23.21% of 2025 revenue, supported by recent disease-modifying approvals.

Why is Asia-Pacific considered the growth engine?

The region posts a 6.32% CAGR through 2031 due to expanding clinical infrastructure, supportive policies and lower operational costs.

What technologies are transforming trial execution?

Decentralized monitoring platforms, wearable sensors and FDA-cleared wireless cortical arrays are reshaping patient engagement and data capture.

How concentrated is the competitive landscape?

The top five sponsors control roughly 45.0% of late-phase neuroscience trials, indicating moderate concentration with ample room for biotech disruptors.

Page last updated on: