Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

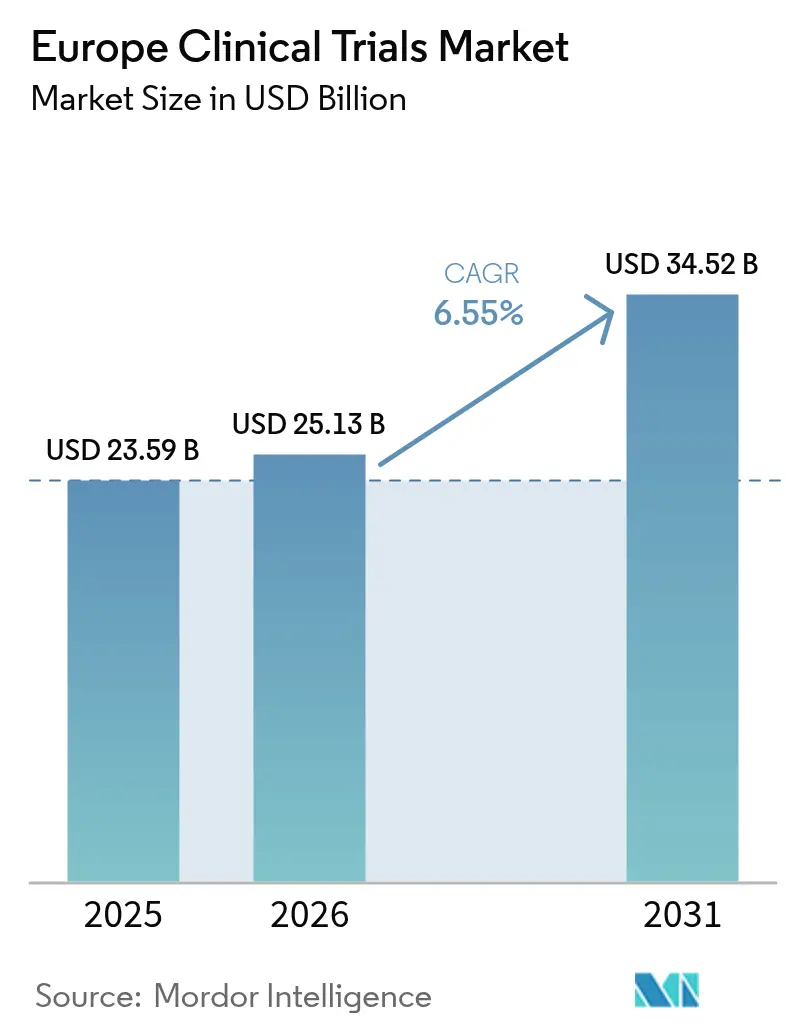

| Base Year Market Size (2025) | USD 23.59 Billion |

| Market Size (2026) | USD 25.13 Billion |

| Market Size (2031) | USD 34.52 Billion |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

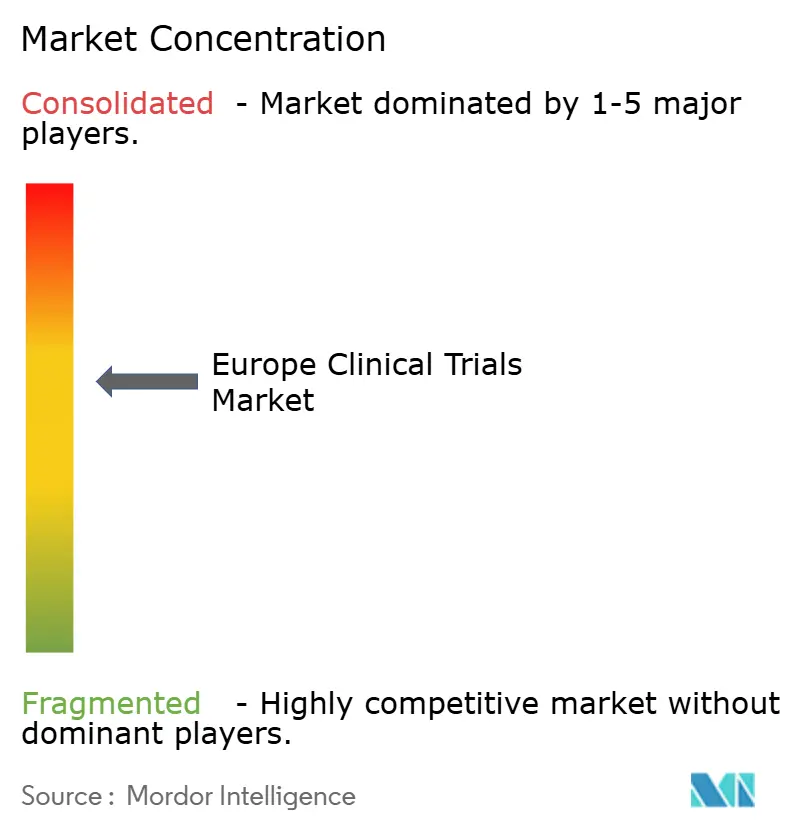

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Clinical Trials Market Analysis by Mordor Intelligence

Europe clinical trials market size in 2026 is estimated at USD 25.13 billion, growing from 2025 value of USD 23.59 billion with 2031 projections showing USD 34.52 billion, growing at 6.55% CAGR over 2026-2031. Expansion rests on sustained pharmaceutical R&D investment, faster study start-up under the Clinical Trials Regulation, and wide adoption of decentralized and hybrid designs that lower patient-access barriers. Oncology programs keep capital flowing into late-stage studies, while neurology pipelines grow as Europe’s population ages. Hybrid outsourcing models that blend large contract research organizations (CROs) with technology-enabled niche vendors help sponsors trim costs and shorten timelines. Competitive pressure from Asia–Pacific remains intense, yet Europe’s regulatory reforms and deep investigator networks underpin a steady flow of high-value studies needed to retain global relevance.

Key Report Takeaways

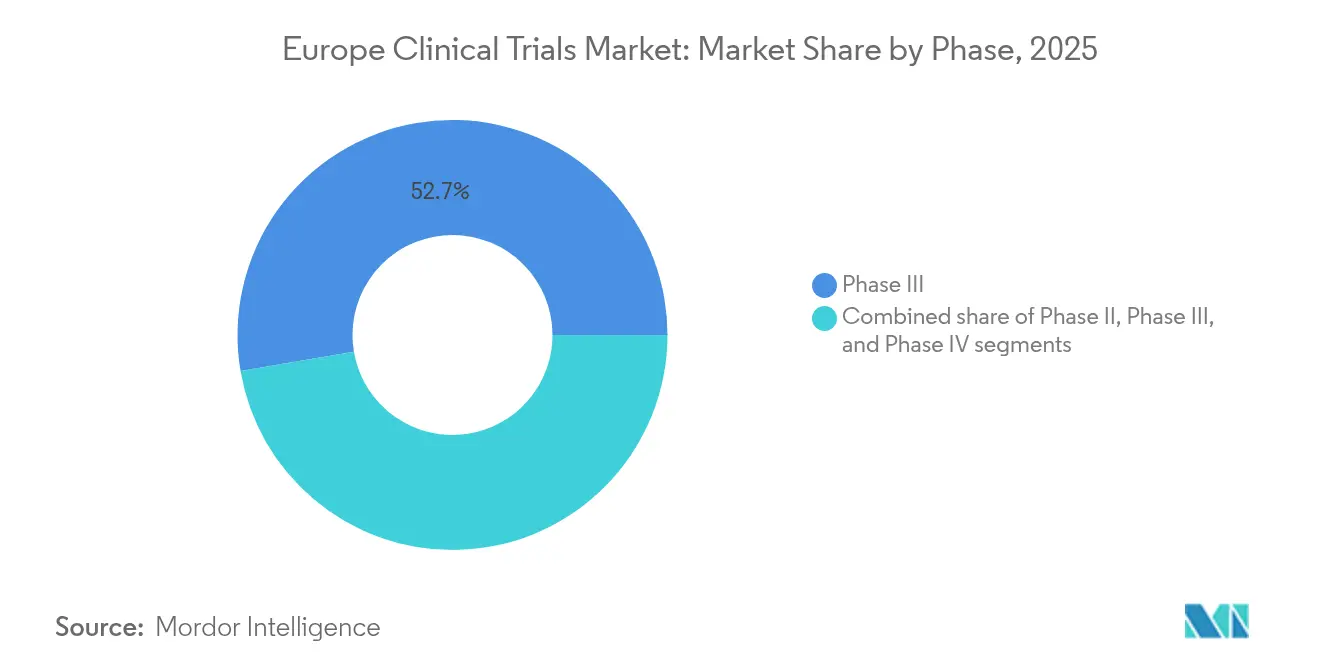

- By phase, Phase III trials captured 52.68% revenue share in 2025; Phase II is the fastest-growing segment, advancing at a 7.55% CAGR through 2031.

- By study design, interventional studies accounted for 79.85% of the Europe clinical trials market size in 2025, whereas adaptive designs are set to grow at an 7.66% CAGR.

- By service type, clinical trial monitoring held 30.12% share of the Europe clinical trials market size in 2025, and decentralized trial services are accelerating at a 13.45% CAGR.

- By therapeutic area, oncology dominated with 35.92% Europe clinical trials market share in 2025; neurology programs are climbing at an 8.01% CAGR.

- By sponsor type, pharmaceutical companies retained 59.02% share of the Europe clinical trials market size in 2025; government and non-profit sponsors are expanding at a 7.62% CAGR.

- By geography, Germany led with 18.21% of Europe clinical trials market share in 2025, while Spain is projected to expand at a 6.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Clinical Trials Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High pharmaceutical-biotech R&D intensity | +1.2% | Germany, UK, France, Switzerland | Medium term (2-4 years) |

| Rising prevalence of chronic & infectious diseases | +0.9% | EU-wide, aging populations | Long term (≥ 4 years) |

| Growing orphan-drug incentives & rare-disease focus | +0.7% | Germany, France, UK | Medium term (2-4 years) |

| ACT-EU & CTIS accelerating trial start-ups | +1.1% | All EU/EEA states | Short term (≤ 2 years) |

| Rapid adoption of decentralized / hybrid trial models | +1.3% | Northern Europe leading, Southern Europe following | Medium term (2-4 years) |

| Central & Eastern Europe’s cost-efficient patient recruitment | +0.6% | Poland, Czech Republic, Hungary, Romania | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Pharmaceutical-Biotech R&D Intensity in Europe

Major multinationals have pledged more than EUR 2 billion of fresh investment across France, with Pfizer alone earmarking EUR 500 million to expand late-stage trials in hematology and rare cancers. Germany’s Medical Research Act, effective 2025, allows parallel scientific and ethics reviews and permits confidential reimbursement talks that attract complex studies. Although European R&D spending still trails growth rates in the United States and China, policy makers are coupling tax credits with infrastructure grants to keep next-generation modalities—mRNA, cell, and gene therapies—onshore. Industry consolidation is speeding up as cash-strapped biotechs partner with CROs that already own pan-EU investigator networks. As a result, the Europe clinical trials market is witnessing more seamless, platform-based development programs that can move from Phase I through Phase III within integrated frameworks.

Rising Prevalence of Chronic & Infectious Diseases

An aging continent and lingering pandemic threats push demand for novel medicines, with more than 40 new products slated for German launch in 2025, most aimed at Alzheimer’s disease, oncology, and genetic disorders. Oncology applications make up the largest share of submissions to the European Medicines Agency (EMA) pipeline, while vaccine and antiviral studies are leveraging compressed review timelines shaped during COVID-19. Digital biomarkers and home-based monitoring allow sponsors to integrate real-world data into study endpoints, raising recruitment efficiency among multimorbid patient pools. These factors collectively add buoyancy to the Europe clinical trials market even as recruitment grows more complex.

Growing Orphan-Drug Incentives & Rare-Disease Focus

CRISPR-enabled gene therapies for sickle-cell disease and hemophilia are approaching commercialization, buoyed by the EMA’s PRIME program that shortens scientific advice cycles for high-unmet-need products. Yet health-technology-assessment reforms taking effect in 2025 require joint clinical assessments for advanced-therapy products, adding evidence-generation pressure. Sponsors are opting for master-protocol and platform studies to pool scarce patient cohorts across borders, elevating the use of adaptive statistical methods. Demonstrating real-world value is becoming essential for orphan therapies to secure sustainable reimbursement in publicly financed systems.

ACT-EU & CTIS Accelerating Trial Start-Up Timelines

Full enforcement of the Clinical Trials Regulation on 31 January 2025 obliges sponsors to use the CTIS portal for all studies, enabling a single dossier across member states and cutting administration by as much as 50%[1]Nature Editors, “Regulatory Shake-Up Speeds EU Trials,” nature.com. The United Kingdom, outside the EU, is countering with a 50% faster MHRA notification scheme that keeps the country attractive despite divergent legislation. Early movers that invested in regulatory-information-management systems now enjoy faster multi-country approvals, thus capturing a larger slice of the Europe clinical trials market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-layered approval processes | -0.8% | All EU states | Short term (≤ 2 years) |

| Europe’s falling share of global patient enrollment | -0.9% | EU-wide | Long term (≥ 4 years) |

| Lower reimbursement levels in parts of Southern / CEE Europe | -0.5% | Southern Europe, Central & Eastern Europe | Medium term (2-4 years) |

| Fragmented trial-data standards across EU study sites | -0.4% | All EU Member States, varying by therapeutic area | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Layered Approval Processes

The ICH E6(R3) Good Clinical Practice guideline, effective July 2025, brings tougher data-integrity and computer-system-validation demands that lengthen sponsor checklists eca.de. National nuances in ethics-committee opinions generate unpredictable timelines, especially for digitally enabled or adaptive designs. Germany’s new reporting duties for study participants add to monitoring overhead. These factors collectively suppress near-term growth even as harmonization efforts progress.

Europe’s Falling Share of Global Patient Enrollment

Europe counted 60,000 fewer trial seats in 2024 than a year earlier, while worldwide numbers rose, underscoring recruitment drift toward Asia–Pacific settings that promise faster timelines and lower costs[2]European Federation of Pharmaceutical Industries and Associations, “Clinical Trial Participation Gap,” efpia.eu. Brexit-induced dual submissions and divergent data-protection rules raise complexity for sponsors running cross-channel studies. Precision-medicine protocols, which require smaller, biomarker-defined populations, tighten the pool further. Unless Europe adopts more flexible consent and data-sharing frameworks, patient leakage will continue to erode its global standing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Phase: Late-Stage Dominance Drives Market Maturity

Phase III studies represented 52.68% of the Europe clinical trials market in 2025, confirming the region’s role in confirmatory evidence generation. Sponsors leverage Europe’s dense hospital networks and seasoned investigators to run pivotal oncology and immunology programs that feed EMA submissions. Adaptive Phase II designs, growing at a 7.55% CAGR, let companies kill or pivot assets sooner, a critical hedge against soaring development costs. Seamless II/III platforms and real-time analytics are blurring traditional phase boundaries, tightening cycle times, and reinforcing the Europe clinical trials market as a preferred venue for integrated programs.

Second-generation cell and gene therapies now benefit from EMA’s advanced-therapy guidance, which allows conditional approvals supported by robust post-marketing data. The Europe clinical trials market size for Phase II work is projected to expand materially as sponsors align biomarker discovery with proof-of-concept studies. Post-authorization Phase IV programs are also growing because payers increasingly demand real-world evidence before green-lighting reimbursement.

By Study Design: Interventional Trials Lead Digital Transformation

Interventional designs accounted for 79.85% of the Europe clinical trials market size in 2025, underlining regulators’ continued preference for randomized evidence. Adaptive designs are climbing at an 7.66% CAGR thanks to Bayesian statistics and interim-data modeling that support early futility stops and dose re-optimizations. Pragmatic and decentralized models are now acceptable under EMA guidance, broadening participation among rural and mobility-challenged patients.

Observational cohorts complement interventional work by harvesting long-term safety and comparative-effectiveness data from electronic health records. Master protocols, including umbrella and basket trials, reduce administrative duplication when sponsors test multiple drugs across biomarker subsets. Together, these methodologies keep the Europe clinical trials market agile amid rising cost pressures.

By Service Type: Monitoring Evolves Toward Digital Excellence

Monitoring services held 30.12% Europe clinical trials market share in 2025, but field monitors are moving from on-site checks toward central, risk-based analytics that flag anomalies in real time. Remote source-data verification cuts travel costs and allows earlier query resolution. Decentralized trial services, rising at a 13.45% CAGR, bundle eConsent, tele-visits, medication delivery, and at-home phlebotomy, making participation easier for diverse populations.

Protocol-design and feasibility consultancies now rely on predictive modeling to select sites that can enroll rare-disease patients quickly. Data-management providers are embedding machine learning to automate query detection and expedite database lock. These developments collectively enlarge the Europe clinical trials market size in the services arena while reshaping vendor hierarchies.

By Therapeutic Area: Oncology Leadership Faces Neurological Acceleration

Oncology accounted for 35.92% of Europe clinical trials market share in 2025. Immunotherapies and antibody-drug conjugates dominate the pipeline, benefiting from EMA’s accelerated-assessment procedures. Neurology studies, growing at an 8.01% CAGR, target Alzheimer’s, Parkinson’s, and ALS with gene-editing and anti-tau approaches. Cardiovascular and metabolic disorders continue to integrate digital biosensors that deliver richer endpoint data at lower burden.

Infectious-disease attention remains elevated as governments finance next-generation vaccine platforms to shore up pandemic readiness. Metabolic trials exploit closed-loop glucose monitoring and digital coaching, features that appeal to regulators looking for holistic outcome evidence. Collectively, these dynamics keep the Europe clinical trials market diversified across disease areas.

By Sponsor Type: Public-Private Partnerships Accelerate Innovation

Pharmaceutical companies held 59.02% of market spending in 2025, retaining control of large pivotal programs that demand global coordination. Yet cash-efficient pipelines rely on CRO alliances, academic collaborations, and artificial-intelligence start-ups to de-risk assets early. Government and non-profit bodies, rising at a 7.62% CAGR, channel grants into neglected diseases and preparedness projects, bringing new funding streams into the Europe clinical trials industry.

Academic medical centers remain crucial for first-in-human oncology and rare-disease trials, often partnering with biotechs that lack internal infrastructure. Medical-device sponsors expand neuromodulation and digital-therapeutic candidates, leaning on Europe’s class-III regulatory expertise. The resulting blend of actors enriches the Europe clinical trials market with complementary skills and capital.

Geography Analysis

Germany, with an 18.21% stake in 2025, continues to anchor the Europe clinical trials market through high R&D spend, over 16,000 registered studies, and newly enacted rules that permit confidential price talks during trial planning. Its mandatory participant-reporting after January 2025 will raise documentation needs, yet the Medical Research Act promises quicker approvals, likely sustaining double-digit study inflows.

The United Kingdom preserves a top-tier research ecosystem by slashing MHRA review times and offering adaptive-licensing pilots that compensate for post-Brexit regulatory divergence. Rapid scientific-advice mechanisms now pull oncology and advanced-therapy sponsors that might otherwise look to Netherlands or Belgium. France secured more than EUR 2 billion in 2024 capital commitments from leading pharma groups, strengthening early-stage translational hubs in Paris and Lyon. Spain is the fastest climber, forecast at a 6.78% CAGR through 2031, buoyed by cost-efficient enrollment, simplified ethics-committee coordination, and strong patient-advocacy networks. Poland, Czech Republic, and Hungary attract treatment-naïve volunteers and deliver 15%–20% cost savings versus Western Europe, though variable site quality still deters some oncology sponsors. Italy leverages academic-industry clusters in Milan and Rome to secure niche oncology and immunology projects, while Scandinavian countries pair digital-health penetration with registry linkages that make them ideal test beds for decentralized models.

Regulatory Landscape

The EU Clinical Trials Regulation (EU) No 536/2014 is the single legal framework for interventional clinical trials across the EU/EEA, with the full transition completed on 30 January 2025 and mandatory use of the Clinical Trials Information System (CTIS) for submissions and oversight. As CTIS matures under the Accelerating Clinical Trials in the EU (ACT-EU) program, operational activity is visible in the platform, with CTIS averaging 208 new clinical trial application submissions per month in Q1 2026.

In 2026, the rule-and-platform environment continued to tighten around data and lifecycle controls. The EMA introduced CTIS changes in early 2026, including a February 2026 update that added a mandatory field for substantial modifications when trial extensions exceed two years (capturing recruitment start or restart dates), which strengthens auditability for long-running studies. Separately, Regulation (EU) 2026/771, in force since 7 April 2026, established governance for the European Health Data Space (EHDS) via the EHDS Council and national Health Data Access Bodies, creating an EU-level pathway for secondary use of health data in research under defined access and interoperability conditions.

Competitive Landscape

Europe’s clinical-research providers are moderately consolidated as full-service CROs acquire niche digital and biomarker firms. Thermo Fisher Scientific’s USD 3.1 billion Olink purchase adds high-throughput proteomics into its development suite, letting sponsors correlate protein signatures with treatment response. Italian CDMOs Doppel Farmaceutici and Mipharm merged into Domixtar, creating a EUR 180 million entity that can absorb end-to-end projects[3]Trilantic Europe, “Domixtar CDMO Formed in Italy,” trilanticeurope.com.

Technology ingenuity is now a key differentiator. AI-native vendors model patient trajectories to optimize eligibility, while eSource platforms automate data capture and reduce monitoring bills. The BioNTech–CureVac all-stock deal worth USD 1.25 billion removes patent overhang and folds together mRNA know-how for oncology vaccines. Strategic CRO–pharma alliances, such as LEO Pharma’s dermatology pact with ICON, highlight a move toward therapeutic-area specialization that promises deeper investigator engagement and faster enrollment.

White-space remains in rare diseases, pediatric trials, and digital therapeutics. New entrants flaunt remote-first operating models, undercutting incumbents by blending telehealth, home nursing, and direct-to-patient logistics. Incumbent CROs react by spinning out virtual-trial units or partnering with eClinical vendors. Competitive intensity keeps service prices keen even as the Europe clinical trials market expands.

Europe Clinical Trials Industry Leaders

IQVIA

Parexel International (MA) Corporation

ICON plc

Thermo Fisher Scientific Inc.

Laboratory Corporation of America Holdings

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Cross-country trial execution is emerging as a practical opportunity enabled by the fully mandatory CTR and CTIS workflow, which reduces prior Directive-era fragmentation for multi-member-state studies. Platform adoption is measurable, with CTIS processing an average of 208 new CTA submissions per month in Q1 2026, supporting sponsors that run harmonized country activation strategies and vendors that industrialize EU-wide regulatory operations and study start-up services.

A second opportunity track is forming at the intersection of advanced modalities, evidence standards, and data access. Gene therapy and other advanced programs are adding Europe-focused evidence-generation steps, illustrated by Roche's April 2026 announcement of intent to initiate a new global pivotal Phase III study for Elevidys to generate additional placebo-controlled data for an EMA resubmission. In parallel, EHDS governance taking effect in April 2026 opens room for compliant data-access, linkage, and analytics offerings (via national Health Data Access Bodies), particularly for oncology (a leading CTIS therapeutic category) and for rare-disease and neurology trials that depend on distributed patient identification across borders.

Recent Industry Developments

- June 2026: IQVIA published analysis of the European Union's proposed Biotech Act changes, highlighting reforms that target simplification of clinical trial authorization under the Clinical Trials Regulation. The work signals where large service providers are steering regulatory and operational investments as sponsors prioritize faster, pan-EU study start-up pathways.

- June 2025: BioNTech completed an all-stock acquisition of CureVac for USD 1.25 billion, adding CureVac's mRNA platform and early-stage oncology pipeline. The deal expands Europe-based development programs and increases capacity for late-stage clinical execution in oncology and next-generation vaccines.

- July 2024: Thermo Fisher Scientific closed its USD 3.1 billion acquisition of Olink Holding, bringing proximity extension assay proteomics into its portfolio. The expanded biomarker and proteomics capability supports more biomarker-driven trial designs in Europe and increases bundled offerings spanning translational work through clinical development services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Europe clinical trials market is defined as total sponsor-billed spending to plan, run, and close human clinical studies for drugs and medical devices conducted within Europe, counted once at contract value across major trial activities.

Scope exclusions: We exclude animal pre-clinical work and stand-alone post-marketing real-world evidence registries that are not part of a clinical trial program.

Segmentation Overview

- By Phase

- Phase I

- Phase II

- Phase III

- Phase IV

- By Study Design

- Interventional / Treatment Studies

- Observational Studies

- Expanded Access Studies

- By Service Type

- Protocol Design & Feasibility

- Site Identification & Start-up

- Regulatory Submission & Approval

- Clinical Trial Monitoring

- Data Management & Biostatistics

- Medical Writing

- Other Service Types

- By Therapeutic Area

- Oncology

- Cardiovascular

- Neurology

- Infectious Diseases

- Metabolic Disorders (Diabetes, Obesity)

- Immunology / Autoimmune

- Other Therapeutic Areas

- By Sponsor Type

- Pharmaceutical & Biopharmaceutical Companies

- Medical Device Companies

- Academic & Research Institutes

- Government & Non-profit Organizations

- Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by aligning the Europe geography and what counts as a clinical trial expense, before any numbers are modeled. We rely on public and official reference points such as the EU Clinical Trials Information System (CTIS), the European Medicines Agency (EMA), EudraVigilance safety reporting, OECD health and R&D statistics, and Eurostat datasets to understand trial activity signals and healthcare research patterns.

Next, we review supporting materials such as annual reports, investor presentations, association pages, and reputable press coverage to understand outsourcing intensity, service mix, and pricing direction. When it is needed to cross-check company exposure and timeline signals, we also use paid subscriptions for company financials and intelligence, along with patent databases to understand pipeline direction. The sources mentioned above are illustrative and not exhaustive, and many other references were also used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary inputs come from interviews and surveys with trial sponsors, CRO-side delivery teams, clinical operations vendors, and site-level experts across key European countries. These discussions help confirm what is actually billed into trial budgets, including site set-up, patient recruitment, monitoring, data services, and close-out, and then reconcile mismatches between public activity signals and desk assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 17% | |

| Mid tier: 43% | Functional/Unit leaders: 31% | |

| Smaller Players: 21% | Managers: 52% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up logic, where Europe trial activity and spend signals are reconstructed into a demand pool, then translated into sponsor-billed cost buckets. After the topline is built, selective bottom-up checks are used to keep the outputs realistic, for example by applying sampled service pricing to expected volumes for monitoring visits, patient recruitment work, and data management loads.

Inputs used in the model include the count and mix of interventional studies, the share of trials outsourced, typical budget split across start-up versus conduct tasks, cost progression by phase, and the timing impact of enrollment speed. When a country or phase has limited public detail, we fill gaps using ranges validated in interviews and apply conservative midpoints until an independent signal supports narrowing the input. For forecasting, scenario analysis is applied around pipeline momentum, regulatory timelines, and cost inflation, and then the selected path is aligned with what primary respondents expect for near-term contracting and study starts.

Data Validation & Update Cycle

Model outputs are compared against independent signals such as study start volumes, sponsor budget direction, and observed outsourcing intensity, and any large variance is re-checked at the country and phase level. Before sign-off, anomalies are reviewed in multiple steps, including peer checks for logic, unit consistency, and currency handling, followed by a final analyst pass.

Reports are refreshed annually, and interim updates are triggered when material events shift budgets or trial activity patterns, such as major regulatory changes or sharp pricing movement. Before delivery, a fresh review is completed so clients receive the latest updated view instead of an older snapshot.

Mordor Intelligence's Europe Clinical Trials Market Size Compared Against Other Published Estimates

Published market sizes for Europe clinical trials can differ even when they appear to cover the same topic, because the spend boundary and the stated year are often not aligned. Differences also show up when sources treat only outsourced service revenue as the market, or when they mix drug and device studies differently in the total.

CTIS trial activity counts and sponsor contracting checks across Phase I to Phase IV services are the evidence that keeps Mordor Intelligence's total tied to sponsor-billed trial delivery in EU-27, the UK, EFTA, and candidate countries, with protocol design, site set-up, recruitment, monitoring, data services, and close-out counted once at contract value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.13 B (2026) | |

| Global Consultancy A | USD 22.01 B (2024) | Uses an earlier base year and may apply a different inflation and pricing path between years, which shifts the stated value even if the longer-term direction is similar. |

| Industry Publisher B | USD 15.84 B (2024) | Often reflects a tighter spend scope and lower assumed budget per study, which can undercount sponsor-billed activities like monitoring, data services, and close-out when modeled with conservative averages. |

The spread across sources mainly comes from two practical differences: the year used for the headline number and the cost buckets treated as part of a clinical trial budget. By keeping geography explicit and checking key cost inputs against activity and contracting signals, the final market value stays traceable to clear drivers and repeatable steps.

Key Questions Answered in the Report

How large is the Europe clinical trials market in 2026?

The market stands at USD 25.13 billion in 2026 and is on track to reach USD 34.52 billion by 2031.

Which country commands the biggest share of Europe’s clinical trial activity?

Germany leads with an 18.21% share in 2025, supported by strong infrastructure and new legislation that streamlines approvals.

What is driving the shift toward decentralized and hybrid trials?

Pandemic-era lessons, EMA guidance on remote elements, and technology that enables tele-visits and at-home sampling are fueling a 13.45% CAGR for decentralized services.

Why are Phase II studies growing faster than other phases?

Adaptive designs and biomarker-based enrollment let sponsors validate proof-of-concept more efficiently, pushing Phase II activity at a 7.55% CAGR.

Which therapeutic area attracts the most trials in Europe?

Oncology retains top position with 35.92% market share, thanks to immunotherapy and precision-medicine pipelines.

How will the Clinical Trials Regulation impact study start-up?

Mandatory CTIS use from January 2025 enables a single submission for multi-country trials, cutting administrative workload by up to 50%.

Page last updated on: