Aseptic Sampling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 2.49 Billion |

| Growth Rate (2026 - 2031) | 12.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aseptic Sampling Market Analysis by Mordor Intelligence

The aseptic sampling market size is expected to grow from USD 1.26 billion in 2025 to USD 1.41 billion in 2026 and is forecast to reach USD 2.49 billion by 2031 at 12.05% CAGR over 2026-2031. Rapid investment in contamination-free bioprocessing, tighter sterility regulations, and wider adoption of single-use assemblies underpin this expansion. Pharmaceutical producers see automated devices as a reliable guardrail against human error, while growing cell and gene therapy pipelines force sterility controls earlier in development. Digital process analytical technology (PAT) now pairs with sampling hardware to deliver real-time quality data that protects multimillion-dollar biologic batches. Regionally, North American manufacturers defend leadership through mature infrastructure and FDA oversight, yet Asia-Pacific facilities add capacity faster on the back of state incentives and lower operating costs. Competition intensifies as integrated solution providers couple hardware, analytics, and data management into unified platforms that shorten validation timelines.

Key Report Takeaways

- By type of sampling, manual systems held 71.62% of the aseptic sampling market share in 2025, while automated systems post the highest 17.72% CAGR to 2031.

- By sampling technique, on-line methods led with 46.05% revenue share in 2025; at-line is projected to expand at a 13.53% CAGR through 2031.

- By application, upstream processing accounted for a 60.94% share of the aseptic sampling market size in 2025 and is advancing at a 11.88% CAGR through 2031.

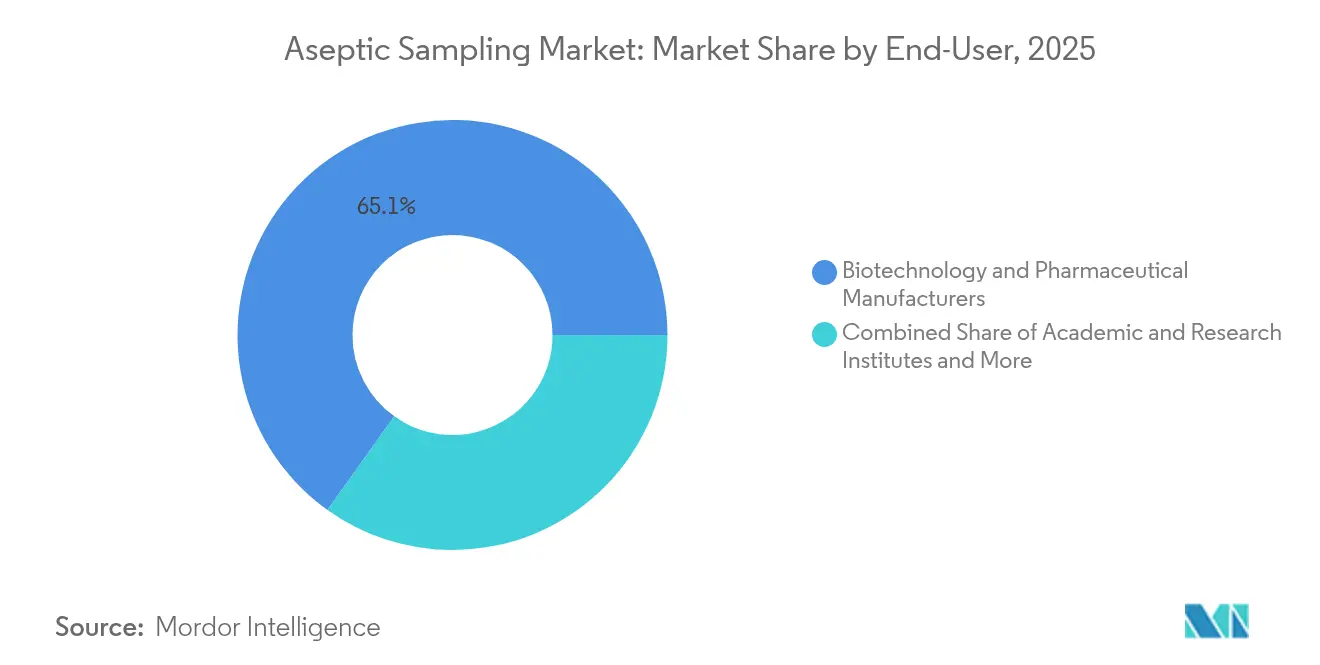

- By end-user, biotechnology and pharmaceutical manufacturers commanded 65.12% of the aseptic sampling market size in 2025, while CDMOs are rising at a 14.09% CAGR.

- By component material, single-use assemblies captured 64.05% revenue share in 2025; reusable stainless-steel systems record a 13.08% CAGR to 2031.

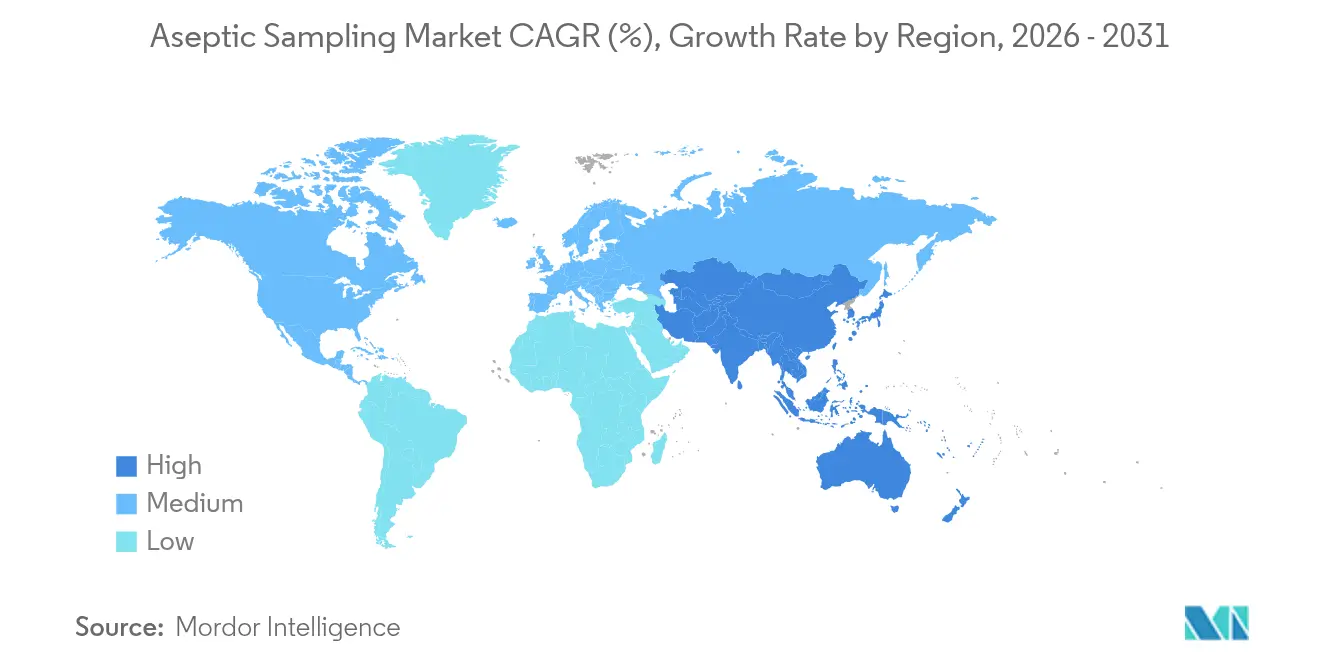

- By geography, North America led with 41.35% revenue share in 2025; Asia-Pacific exhibits the fastest 13.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Aseptic Sampling Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations for sterility assurance | +1.8% | North America & Europe | Medium term (2-4 years) |

| Rapid scale-up of cell & gene therapy pipelines | +2.2% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Shift toward closed-loop, single-use bioprocessing | +2.0% | Global, led by North America | Medium term (2-4 years) |

| In-line and at-line PAT adoption improving batch yields | +1.5% | North America & Europe, selective Asia-Pacific | Medium term (2-4 years) |

| AI-driven contamination prediction platforms | +1.0% | North America & Europe early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Government Regulations For Sterility Assurance

Global regulators now require tighter sampling frequency and traceability in aseptic production. The revised FDA guidance extends to advanced therapy medicinal products and mandates routine environmental monitoring with documented validation. Equivalent EU GMP Annex 1 revisions align expectations across regions, prompting manufacturers to replace paper logs with electronic audit trails and automated devices that record every intervention. This pressure accelerates upgrades in legacy plants and prescribes closed, single-use pathways in greenfield sites to minimize contamination risks[1]U.S. Food and Drug Administration, “PAT — A Framework for Innovative Pharmaceutical Development, Manufacturing, and Quality Assurance,” fda.gov.

Rapid Scale-Up Of Cell & Gene Therapy Pipelines

Commercialization of autologous and allogeneic therapies exposes sterility weak points, as each patient batch carries zero tolerance for cross-contamination. Producers therefore specify automated, closed sampling that secures chain-of-custody documentation and supports diverse viral vectors and cell types. As approvals approach 3,000 therapies by 2030, capacity build-outs demand modular skids that drop into multiproduct suites without lengthy validation cycles[2]Cytiva, “Cytiva Opens New Korea Manufacturing Facility,” cytiva.com.

Shift Toward Closed-Loop, Single-Use Bioprocessing

Disposable bioreactors, filters, and tubing dominate new plant builds because they remove cleaning validation and shorten changeovers. Their proliferation forces compatible sampling interfaces that preserve bag integrity and maintain low extractables. Contract manufacturers favor these platforms to toggle between client programs quickly, yet they must still satisfy polymer characterization scrutiny under evolving leachables guidance.

In-Line, At-Line PAT Adoption Improving Batch Yields

Real-time analytics move quality control from end-point testing to continuous insight. At-line probes now feed data every few minutes without exposing the process, allowing operators to adjust nutrients or pH before deviations propagate. FDA encouragement through PAT frameworks reduces regulatory resistance and positions automated sampling plus spectroscopy as co-pillars of modern biologic manufacturing.

Restraints Impact Analysis of Aseptic Sampling Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Leachables & extractables risk in polymeric assemblies | -0.7% | North America & Europe | Short term (≤ 2 years) |

| High CAPEX of automated aseptic sampling skids | -1.0% | Global, stronger in emerging markets | Medium term (2-4 years) |

| Complex validation for multi-use connectors | -0.5% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Leachables & Extractables Risk In Polymeric Assemblies

Disposable manifolds can release organic acids, plasticizers, or trace metals that destabilize sensitive biologics, requiring exhaustive chemical profiling. Firms often run multi-week extractables studies at several temperatures and solvents, adding cost and delaying product launch schedules. The absence of harmonized global test standards also multiplies analytical workloads.

High CAPEX Of Automated Aseptic Sampling Skids

Turnkey skids range from USD 500,000 to USD 2 million and call for specialized maintenance teams, making ROI unclear for small biotechs with low annual batch counts. Emerging-market facilities often postpone purchases in favor of validated manual kits, especially when loan financing is scarce. Vendors respond with leasing models and modular upgrades that allow incremental automation[3]Danaher Corporation, “Danaher Invests USD 1.5 Billion in Manufacturing Capacity,” danaher.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Aseptic Sampling Market Segment Analysis

By Type of Sampling:

Automation Gains GroundManual systems commanded a 71.62% share of the aseptic sampling market in 2025. Their low capital outlay and proven compliance records maintain widespread usage, especially in legacy plants where infrastructure changes invite downtime. However, automated modules exhibit the fastest 17.72% CAGR as producers target lower operator exposure and stronger data integrity. Automated skids integrate with manufacturing execution systems to log every grab and immediately archive results for audit review. That capability relieves documentation fatigue and elevates confidence during FDA inspections. Rising batch values in cellular therapies sharpen demand for solutions that remove human interventions entirely, reinforcing the long-term tilt toward automation in the aseptic sampling market.

Manual kits still occupy niches such as early R&D or low-volume biologics where budget trumps throughput. Vendors now position hybrid platforms that accept manual triggers yet automate sterilization between uses. This bridge strategy helps price-sensitive buyers migrate gradually without scrapping existing protocols. Over the forecast window, wider harmonization of electronic records standards is set to catalyze a decisive inflection toward automated devices as the default for commercial production lines within the aseptic sampling market.

By Sampling Technique:

At-Line SurgesOn-line instruments represented 46.05% of global revenue in 2025 due to their real-time feedback. They continuously pull micro-aliquots under closed conditions, enabling immediate pH or nutrient adjustments. At-line devices, posting the brisk 13.53% CAGR, attract operators who want frequent analytics without the engineering complexity of fully integrated on-line loops. At-line probes station adjacent to the vessel, keep tubing lengths short, and permit rapid sensor swaps. This reduces risk of clogging and simplifies calibrations.

Off-line grabs persist for advanced analytics such as viral clearance assays that cannot be miniaturized. Yet every off-line transfer involves open handling, elongates turnaround, and risks deviations. As PAT guidelines and real-time release testing mature, at-line units will likely siphon incremental share from off-line workflows. Standardized mechanical interfaces and disposable flow paths now make retrofits easier, bolstering adoption across mid-tier plants in the aseptic sampling market.

By Application:

Upstream Dominates, Downstream AcceleratesUpstream processes absorbed 60.94% revenue in 2025. Cell culture stages can last weeks, during which microbial intrusion jeopardizes entire bioreactor volumes worth USD 10 million. Consequently, operators schedule multiple sterile draws each day for metabolic profiling. Trending dissolved oxygen, glucose, and viable cell counts permits early corrective action, protecting titers and glycosylation patterns. Downstream purification registers the highest 15.14% CAGR as chromatography steps multiply for complex modalities. Viral filtration now mandates batch-wise integrity checks that demand aseptic sampling immediately before and after the filter train. The cumulative need for sterility confirmation at every hold point resets sampling frequency upward.

Formulation and fill-finish also intensify controls for high-value personalized doses measured in milliliters. Closed-vial sampling adaptors allow quality teams to test potency after fill yet before lyophilization without breaching containers. This activity shows how downstream stages increasingly mirror upstream vigilance, driving holistic adoption throughout the aseptic sampling market.

By End-User:

Manufacturers Hold Lion’s ShareIntegrated biotechnology and pharmaceutical firms retained 65.12% share in 2025 because they manage discovery through fill-finish under one quality system. They deploy sampling strategies early and scale them across multiple plants to standardize audits. CDMOs, advancing at 14.09% CAGR, benefit from sponsor outsourcing. Their competitive edge hinges on fast tech-transfer and multiproduct flexibility, both of which rely on modular, single-use samplers that minimize change-over downtime.

Academic institutes apply compact, manual kits for exploratory work where budgets remain tight. Although this segment is smaller, its role in proof-of-concept studies means early brand exposure for vendors that later upsell commercial-scale equipment. Patient advocacy groups funding gene therapy trials also partner with CDMOs, further amplifying contracts for comprehensive sampling suites within the aseptic sampling market.

By Component Material:

Disposable Assemblies PrevailSingle-use hardware represented 64.05% of global revenue in 2025, reflecting universal industry migration away from fixed stainless networks. Plastic manifolds arrive pre-sterilized, slash cleaning chemicals and water usage, and support speedier line turnover. Given rising environmental scrutiny, producers weigh plastic waste against water and steam consumption. Still, the total cost of ownership often favors disposables once savings in labor, validation, and downtime are tallied. Reusable stainless sets, however, record a notable 13.08% CAGR where continuous processing or very large batch volumes reward long-lived assets with minimal consumables cost.

Recent supplier innovation introduced gamma-stable fluoropolymer liners and recyclable bag materials that promise to temper sustainability debates. Parallel investment in integrity-testing sensors that verify bag performance before each run augments confidence. Over the next five years, the aseptic sampling market anticipates coexistence of both material classes, segmented by plant scale, sustainability targets, and regulatory preferences.

Geography Analysis

North America Aseptic Sampling Market

North America captured 41.35% revenue in 2025 and defends its lead through deep biopharmaceutical pipelines, benchmarking FDA guidance, and a density of CDMOs. The United States hosts most commercial cell therapy facilities and invests heavily in PAT. Canada builds biosimilar capacity under targeted federal grants, while Mexico’s cost-effective labor spurs generic drug output. Demand rises further due to venture capital backing first-in-class biologics that demand heightened sterility.

APAC Aseptic Sampling Market

Asia-Pacific records the strongest 13.2% CAGR as governments subsidize capacity and enforce quality uplift. South Korea’s SK Pharmteco placed USD 260 million into peptide synthesis lines equipped with closed samplers. China’s localization policies call for domestic supply security, fueling new biologics parks that standardize single-use sampling from the outset. India remains a powerhouse for active pharmaceutical ingredients, where cost-sensitive plants mix manual and disposable kits. Collectively, these programs push the aseptic sampling market deeper into the region and establish local manufacturing bases for global vendors.

Europe Aseptic Sampling Market

Europe remains stable, anchored by Germany’s engineering clusters and France’s biologics expansions. Post-Brexit United Kingdom facilities align with updated Annex 1, driving retrofits of automated sampling loggers. Sustainability regulations pressure producers to explore hybrid metal-plastic manifolds and to document lifecycle impacts. Italian and Spanish vaccine manufacturers similarly upgrade equipment to secure pandemic preparedness grants. These investments deliver steady, if less dramatic, growth that keeps the region an innovation hub for the aseptic sampling market.

Regulatory Landscape

Aseptic sampling in drug and biopharmaceutical manufacturing is governed by current good manufacturing practice requirements, including US FDA cGMP under 21 CFR 211 (notably expectations around in-process controls and sampling plans) and FDA guidance for sterile drug products produced by aseptic processing. These requirements make validated sampling procedures, traceability, and data integrity central to compliance, which in turn drives manufacturers toward closed sampling designs and electronic documentation that can be supported during inspections.

In Europe, the European Commission's EudraLex Volume 4, EU GMP Annex 1 (2022 revision) is the central reference for sterile manufacturing. Annex 1 requires a documented Contamination Control Strategy (CCS) and emphasizes barrier approaches such as RABS or isolators in critical zones. The Annex 1 transition included staged implementation, with a noted final phase for certain lyophilization-related provisions effective in August 2024, which reinforces investment in aseptic sampling procedures, environmental monitoring programs, and risk-based validation. Supporting standards such as USP chapters used for microbiological control and sterile compounding further anchor expectations for cleanroom monitoring and sampling practices across regulated operations.

Competitive Landscape

The aseptic sampling market shows moderate fragmentation, with the top five suppliers holding a significant share. Merck KGaA, Sartorius, and Thermo Fisher Scientific leverage broad portfolios that pair sampling probes with bioreactors, sensors, and data software. Merck’s EUR 300 million biologics expansion in Korea embeds its Mobius single-use samplers to secure reference installs. Sartorius scales its TakeOne portfolio toward gene therapy needs by adding micro-volume ports that fit small, high-value batches. Thermo Fisher integrates sampling valves into its HyPerforma bioreactors, offering turnkey qualification that shortens plant commissioning.

Mid-tier specialists such as Saint-Gobain Life Sciences focus on polymer innovation, rolling out multilayer films with lower additive profiles. Asahi Kasei targets viral filtration lines with sampling adaptors that pair to its Planova filters. Start-ups deliver AI analytics that overlay equipment data onto contamination risk dashboards. Acquisition activity stays brisk as full-line suppliers seek to fold niche technologies into end-to-end suites. Danaher’s Aldevron purchase widens its biologics ecosystem and cross-sells sampling skids through existing genomic medicine customers.

Pricing competition intensifies mainly on consumables, whereas capital equipment differentiation rests on validation documentation, sensor integration, and local support. Vendors that streamline extractables dossiers and offer cloud-ready data outputs gain an edge under tightening regulatory expectations. Over the forecast horizon, collaborative development between suppliers and CDMOs is expected to spawn standardized connector formats that advance interoperability across the aseptic sampling market.

Aseptic Sampling Industry Leaders

GEA Group

Merck KGaA

Keofitt A/S

Saint-Gobain Life Sciences

Sartorius AG

- *Disclaimer: Major Players sorted in no particular order

Aseptic Sampling Market Companies Covered in this Report

- Merck

- Sartorius

- Thermo Fisher Scientific

- Danaher Corp (Pall & Cytiva)

- Lonza Group

- Keofitt

- Saint-Gobain Life Sciences

- GEA Group

- Gemu Group

- Qualitru Sampling Systems

- W. L. Gore & Associates

- Avantor (VWR)

- Repligen Corp

- Solventum Corporation

- Parker Hannifin (domnick hunter)

- Colder Products Company (CPC)

- Mettler-Toledo

- PendoTECH

- Bbi-Biotech GmbH

- Advanced Microdevices Pvt Ltd

Market Opportunities and Future Outlook

Compliance-driven upgrades create whitespace for suppliers that bundle aseptic sampling hardware with audit-ready qualification artifacts, including standardized documentation packs, consumable traceability, and validation support mapped to EU GMP Annex 1 CCS requirements. Merck Life Science provides a clear signal through its 2026 communications on expanded documentation support for its NovaSeptum GO sterile sampling systems, which reflects buyer demand to reduce risk-assessment and qualification workload alongside the physical sampler.

The technology opportunity is strongest around automated, low-dead-volume sampling that can support PAT and higher sampling frequency without adding operator interventions. Industry work highlighted in 2025 around automated sampling validation at frequent intervals, including periodic sampling at 15-minute intervals in vendor validation studies, points to pull from upstream and advanced modalities that need tighter process understanding and chain-of-custody. On the supply side, capacity investments that localize production of sterile sampling solutions in Asia-Pacific, such as Merck Life Science's Daejeon bioprocessing production center build-out, widen the addressable base among regional manufacturers and CDMOs standardizing single-use and closed sampling from facility design onward.

Recent Industry Developments in Aseptic Sampling Market

- May 2026: Merck Life Science highlighted expanded documentation support for its NovaSeptum GO sterile sampling systems to help users accelerate risk assessment and qualification. The update aligns product positioning with Annex 1-driven demands for contamination-control documentation and audit-ready validation packages, not only hardware performance.

- May 2025: Merck Life Science reaffirmed the timeline for its Daejeon, South Korea bioprocessing production center to reach full GMP operational status by 2026, including capacity for NovaSeptum sampling solutions. This adds regional manufacturing depth for sterile sampling components and supports supply chain resilience for Asia-Pacific bioprocessing build-outs.

- March 2024: Merck Life Science initiated an investment of more than EUR 300 million to build a 43,000 square meter bioprocessing production center in Daejeon, South Korea, covering essential biotech products including sterile sampling systems. The project strengthens vertically integrated supply for single-use and sterile manufacturing consumables that support closed, contamination-resistant sampling workflows.

Aseptic Sampling Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the aseptic sampling market is defined as the revenue generated from products and systems used to collect sterile samples from bioprocessing and related sterile manufacturing environments, so contamination risks are minimized and quality checks can be done reliably.

Scope exclusions: It excludes general lab sample-prep tools that are not designed for sterile process sampling, along with broader process equipment that does not perform a sampling function.

Segments Covered in This Report

- By Type of Sampling

- Manual Aseptic Sampling

- Bags

- Bottles

- Other Containers

- Automated Aseptic Sampling

- Manual Aseptic Sampling

- By Sampling Technique

- On-line Sampling

- At-line Sampling

- Off-line Sampling

- By Application

- Upstream Process

- Downstream Process

- By End-User

- Biotechnology & Pharmaceutical Manufacturers

- Contract Research & Manufacturing Organizations

- Academic & Research Institutes

- By Component Material

- Single-Use Assemblies

- Reusable (Stainless-Steel-Based) Systems

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the industry boundaries clearly and to build a realistic demand story tied to biopharma manufacturing activity. We referred to public sources such as the US FDA and EMA guidance libraries for sterility expectations, USP chapters for microbiology and sampling related references, and WHO publications for GMP practices used across countries.

To put numbers behind the demand pool, we also checked sources such as OECD and World Bank macro indicators, UN Comtrade trade statistics for relevant sterile components, and peer-reviewed journals covering bioprocess contamination control and single-use adoption. Company annual reports, investor presentations, and press releases were then used to map product positioning and typical pricing logic, and a paid subscription for company financials and patent intelligence supported cross-checks on portfolios and innovation activity. These desk research sources are illustrative, and many other public documents and datasets were also used to collect, validate, and clarify information.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with a mix of manufacturers, integrators, and end users involved in bioprocess sampling, including quality, manufacturing, and procurement roles. We covered the main regions to test assumptions on single-use penetration, typical replacement cycles, and the balance between manual and automated sampling in upstream and downstream steps.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | APAC: 47% |

| Mid tier: 45% | Functional/Unit leaders: 36% | EMEA: 31% |

| Smaller Players: 22% | Managers: 50% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up logic, where sterile manufacturing activity and bioprocess capacity signals were first used to reconstruct the addressable sampling demand by region and then validated through selective roll-ups. In practice, we tied the model to indicators such as biopharmaceutical production intensity, single-use assembly adoption, counts of sterile sampling points per process train, typical sampling frequency in upstream and downstream operations, and observed price bands for sampling devices and accessories.

Bottom-up checks were run using sampled vendor catalogs and channel feedback to convert a realistic mix of manual versus automated systems into an average selling price progression, which helped adjust for mix shifts over time. When direct visibility was limited for smaller facilities or emerging markets, gaps were handled using proxy assumptions from similar plant types and then corrected through primary feedback.

For forecasting, scenario analysis was used around sterility compliance intensity and single-use conversion speed, and then the trajectory was smoothed using short historical run rates where available. The final forecast reflects expert consensus on how quickly automation is being adopted to reduce human error and how procurement cycles impact annual purchasing patterns.

Data Validation & Update Cycle

Validation was done through multiple checks so the final output stays consistent with real market signals. We compared modeled totals against independent indicators like regional biomanufacturing expansion news, trade movement for sterile components, and shifts in single-use related demand, and then followed up on outliers with re-contacts when the variance was material.

Before sign-off, the model is reviewed in steps by more than one analyst, and assumptions that drive large parts of the total are challenged and rewritten if needed. The report is refreshed annually, and interim updates are made when major events occur that can change capacity, regulatory expectations, or pricing. Right before delivery, a final pass is completed to make sure clients receive the most current view available.

Mordor Intelligence's Aseptic Sampling Market Sizing Compared With Other Published Estimates

Published market values for aseptic sampling can look far apart because each publisher draws the boundary differently and also picks different time windows for the same demand cycle. Differences also come from how manual tools, automated systems, and single-use assemblies are counted, and whether estimates stay tied to bioprocess usage or drift into broader lab supplies.

By tracking upstream and downstream sampling points, and refreshing mix and pricing assumptions with primary inputs, Mordor Intelligence keeps the model anchored to process sampling demand rather than adjacent sterile consumables that do not perform a sampling function. In contrast, some estimates appear to use wider inclusion rules or base-year anchors that shift the 2025 to 2026 level, which then changes the compounding effect over longer forecast periods.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.26 B (2025) | |

| Industry Publisher A | USD 0.94 B (2025) | Uses a narrower counted set of products and appears to treat automated systems and single-use sampling assemblies more conservatively, which pulls down the 2025 level and reduces the implied run-rate entering the forecast. |

| Industry Publisher B | USD 1.79 B (2024) | Anchors the series on a different base year and likely applies a broader scope that can blend adjacent sterile consumables and lab handling items into the total, which inflates the starting point before forecast growth is applied. |

The table shows that most of the spread is explained by boundary setting and base-year anchoring, and not by a single growth assumption. When the counted items are kept specific to process sampling and the pricing and mix are checked against how facilities actually buy and replace these components, the resulting number is easier to trace and replicate year to year for planning.

Key Questions Answered in the Report

What is the current size of the aseptic sampling market?

The aseptic sampling market is valued at USD 1.41 billion in 2026 and is forecast to reach USD 2.49 billion by 2031.

Which segment grows fastest within the aseptic sampling market?

Automated aseptic sampling systems expand at an 17.72% CAGR through 2031, outpacing manual alternatives.

Why are single-use assemblies popular for aseptic sampling?

They eliminate cleaning validation, cut change-over times, and minimize contamination risk, giving them 64.05% revenue share in 2025.

Which region leads aseptic sampling adoption?

North America holds 41.35% global revenue due to mature bioprocessing infrastructure and stringent FDA oversight.

How do regulatory changes affect aseptic sampling demand?

Updated FDA and EU GMP Annex 1 guidelines raise sampling frequency and documentation requirements, driving investment in automated, closed systems.

What is the main restraint to wider automation?

High capital expenditure of USD 500,000 to USD 2 million per skid deters smaller firms, especially in emerging markets.

Page last updated on: