Europe GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

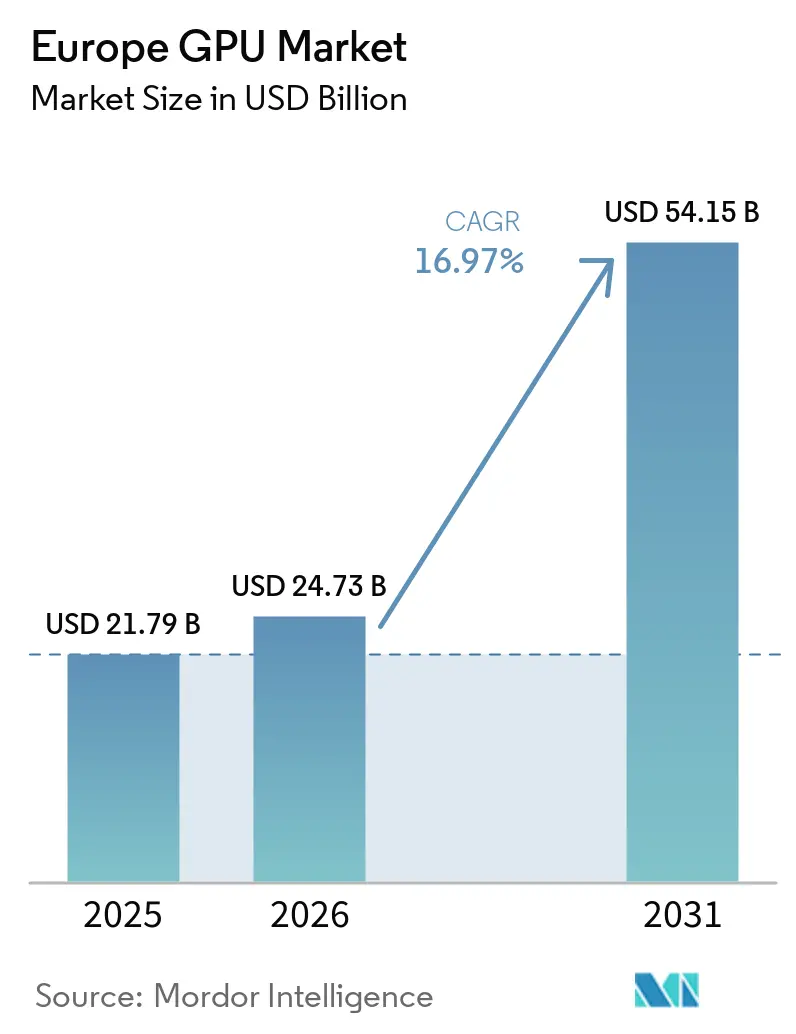

| Base Year Market Size (2025) | USD 21.79 Billion |

| Market Size (2026) | USD 24.73 Billion |

| Market Size (2031) | USD 54.15 Billion |

| Growth Rate (2026 - 2031) | 16.97% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe GPU Market Analysis by Mordor Intelligence

The Europe GPU market size is projected to be USD 21.79 billion in 2025, USD 24.73 billion in 2026, and reach USD 54.15 billion by 2031, growing at a CAGR of 16.97% from 2026 to 2031. Demand accelerates as hyperscale operators, research institutes, and automotive OEMs expand artificial-intelligence (AI) deployments, pushing discrete accelerator volumes well ahead of integrated graphics. Governments in the United Kingdom, France, and Germany are earmarking multi-billion-dollar sovereign AI programs that prioritize on-premises compute, thereby tightening the supply of datacenter-grade GPUs. Supply dynamics remain sensitive to the availability of high-bandwidth memory and advanced packaging capacity, prompting vendors to favor strategic customers who commit to long-term contracts. At the same time, rising electricity costs and forthcoming European Union energy-efficiency rules are steering buyers toward architectures that deliver higher performance per watt.

Key Report Takeaways

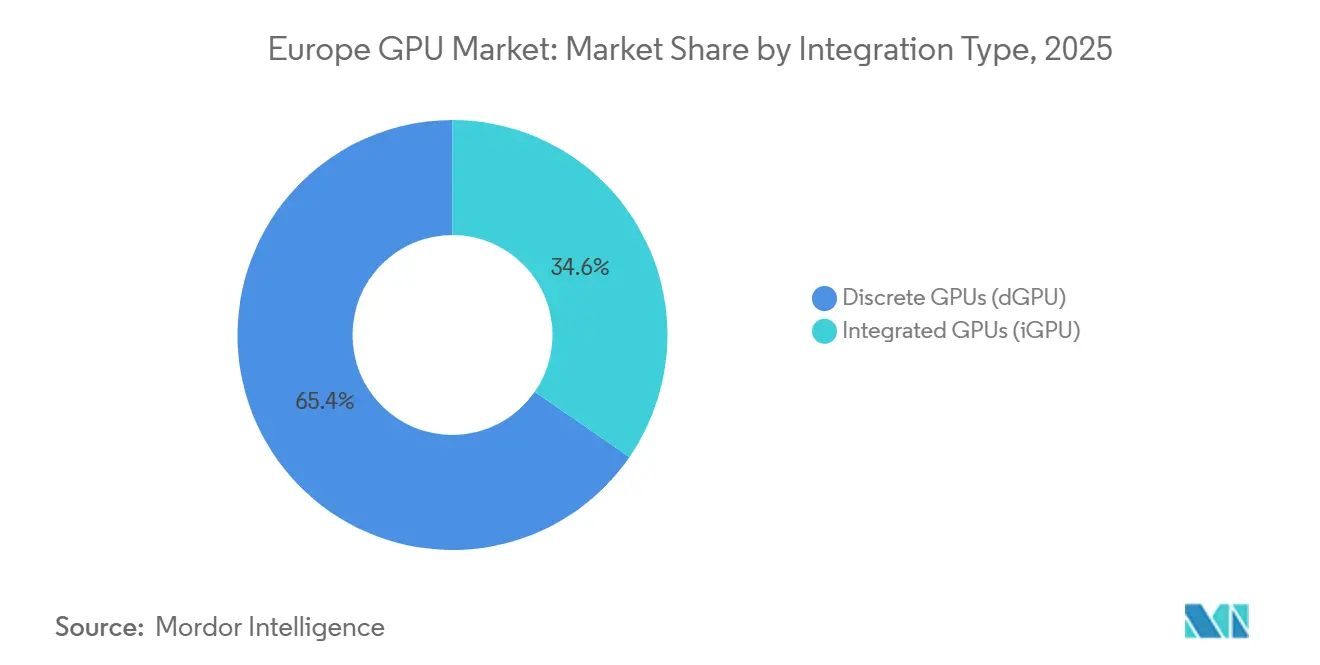

- By integration type, discrete GPUs led the European GPU market with 65.38% market share in 2025 and are projected to expand at a 17.74% CAGR through 2031.

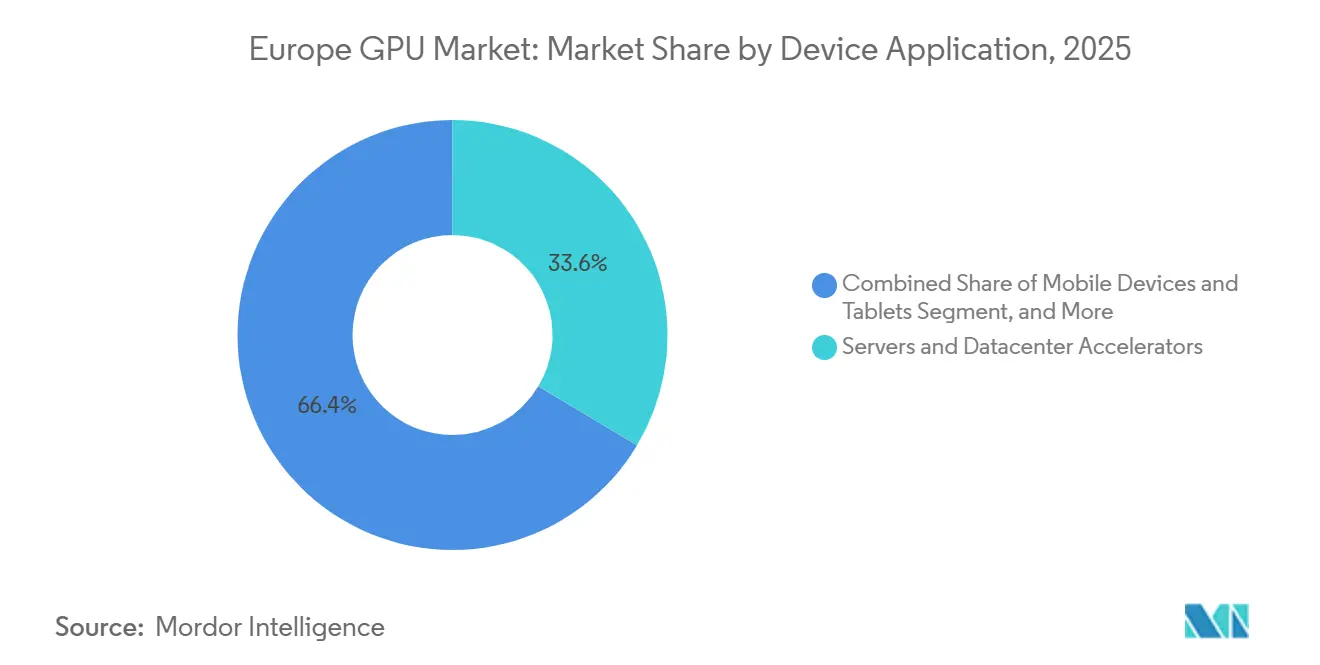

- By device application, servers and datacenter accelerators accounted for 33.57% of the Europe GPU market size in 2025 and are advancing at a 17.58% CAGR over 2026-2031.

- By geography, Germany accounted for 27.83% of regional revenue in 2025, whereas France is forecast to grow the fastest, with a 15.83% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerated Adoption of AI and ML Workloads in European Datacenters | +6.2% | United Kingdom, France, Germany; spillover to Nordic and Benelux | Medium term (2–4 years) |

| EU Chips Act Incentives Boosting Local GPU Manufacturing Investments | +2.8% | Germany, France, Italy; wider EU ecosystem | Long term (≥ 4 years) |

| Rise of Cloud Gaming and Subscription Platforms | +1.9% | United Kingdom, Germany, France; expanding to Southern Europe | Short term (≤ 2 years) |

| Electric Vehicle Infotainment and ADAS Compute Demand | +2.4% | Germany, France, Italy; United Kingdom for design and software | Medium term (2–4 years) |

| Migration to 4K–8K Content Creation Workflows Across Media Sector | +1.6% | United Kingdom, France, Germany; Spain for production | Short term (≤ 2 years) |

| Open-source GPU Drivers and Ecosystems Lowering TCO for Enterprises | +1.3% | Pan-European, early adoption in Germany, United Kingdom, Nordic countries | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of AI And ML Workloads in European Datacenters

Large-scale commitments totaling USD 42.3 billion from the United Kingdom, together with multi-gigawatt projects in France, are adding tens of thousands of NVIDIA Blackwell and AMD Instinct accelerators to regional server racks. OpenAI’s Stargate UK, Microsoft’s supercomputer build-out, and France-based deployments by Mistral AI and Sesterce illustrate how public and private investments align with data-sovereignty mandates. Operators favor liquid-cooled GPU clusters to meet power-usage-effectiveness thresholds and curb operating expenses driven by high electricity tariffs. The scale of these purchases is pulling forward demand that once sat in the second half of the decade, thereby raising near-term shipment forecasts. Collectively, these rollouts anchor the European GPU market on a trajectory in which datacenter accelerators account for a majority of regional revenue before 2028.

EU Chips Act Incentives Boosting Local GPU Manufacturing Investments

The EUR 43 billion (USD 46.4 billion) European Chips Act offers first-of-a-kind facility grants, tax credits, and pilot-line funding to revive continental semiconductor capacity.[1]European Commission, “European Chips Act: State of play,” ec.europa.eu Although only two sub-5 nm projects have cleared approval, related packaging and heterogeneous-integration lines in Dresden, Grenoble, and Novara are underway. Silicon Box’s EUR 3.2 billion (USD 3.5 billion) advanced-packaging plant in Italy and STMicroelectronics’ wafer-fab expansions in France signal momentum on supporting infrastructure that discrete GPU vendors rely on for chiplet assembly. Fabless startups such as SiPearl tap these resources to pair European CPUs with imported accelerators, reinforcing a local supply chain that modestly buffers geopolitical risk. While volume output remains years away, the policy framework has already influenced sourcing strategies for hyperscalers planning 2028-2031 deployments.

Rise of Cloud Gaming and Subscription Platforms

Subscription services shift GPU ownership from consumers to providers that operate centralized or edge servers capable of streaming high-fidelity gameplay.[2]NVIDIA, “GeForce NOW expands European datacenters,” nvidia.com Europe-based nodes added by GeForce NOW and Microsoft Xbox Cloud Gaming require RTX 4090-class performance per user pod to keep sub-40 ms latency targets. Telecom operators bundle cloud gaming with 5G, driving incremental GPU rollouts across metropolitan edge locations. The pay-per-month model lowers up-front costs for players, shortening upgrade cycles as datacenters, rather than end users, absorb hardware refreshes. Parallel growth in handheld gaming PCs, notably Steam Deck and ASUS ROG Ally, sustains integrated-GPU shipping volumes but does not offset the magnitude of server demand.

Electric Vehicle Infotainment and ADAS Compute Demand

Automotive OEMs increasingly consolidate cockpit, cluster, and driver-assistance workloads on a single GPU-centric system-on-chip such as NVIDIA DRIVE Thor, which delivers up to 2,000 TOPS and supports ISO 26262 ASIL-D safety certification.[3]NVIDIA, “NVIDIA DRIVE Thor announced for next-gen EVs,” nvidia.com Mercedes-Benz and BMW intend to introduce Level 3 features in 2026 German models, while Stellantis and Renault adopt Qualcomm Snapdragon Ride to satisfy the European General Safety Regulation. The shift from distributed electronic control units to centralized GPU compute lifts silicon content per vehicle, and European automakers’ preference for local validation introduces a pipeline of hardware procurement commitments through 2030. Unique thermal and lifetime requirements spanning −40 °C to 125 °C limit the number of feasible suppliers and thereby concentrate share among a handful of GPU vendors.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply Chain Disruptions from Geopolitical Tensions on Advanced Nodes | −3.4% | Global TSMC dependency; acute in Germany, France, United Kingdom | Short term (≤ 2 years) |

| Escalating Energy Costs in Europe Impacting GPU TCO | −2.7% | Germany, Italy high tariffs; moderate in France, Nordic countries | Medium term (2–4 years) |

| Regulatory Scrutiny over GPU Power Consumption Standards | −1.8% | EU-wide Ecodesign compliance | Long term (≥ 4 years) |

| Talent Shortage in Advanced Semiconductor Design in Europe | −1.5% | Germany, France, Italy design hubs; broader Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions from Geopolitical Tensions on Advanced Nodes

The majority of leading-edge GPU wafers originate from Taiwanese fabs that rely on helium, high-NA EUV scanners, and advanced packaging capacity concentrated at a handful of subcontractors. Helium shortages tied to Gulf-region conflicts curtailed 3 nm wafer starts in late 2024, extending lead times for NVIDIA Blackwell and AMD MI300X shipments to European integrators. Scarcity of high-bandwidth memory further constrains board-level availability, forcing system vendors to pay 30%-50% premiums on the spot market. With no European fab expected to ship sub-5 nm volume before 2028, hyperscalers maintain contingency buffers yet still risk multi-month project delays should another geopolitical event disrupt Taiwanese foundries.

Escalating Energy Costs in Europe Impacting GPU TCO

Electricity prices vary from EUR 0.18 per kWh (USD 0.19 per kWh) in Nordic markets to EUR 0.30 per kWh (USD 0.33 per kWh) in Germany, a differential that raises annual operating expense per NVIDIA H100 to EUR 1,840 (USD 2,018) versus roughly USD 490 in the United States.[4]International Energy Agency, “Data centres and energy demand in Europe,” iea.org The European Union Ecodesign Regulation 2024/1781 imposes a power-usage-effectiveness ceiling of 1.3 by 2027, obligating operators to deploy liquid cooling and waste-heat recovery. These requirements inflate capital budgets, slow construction timelines, and can tilt purchase decisions toward accelerators like Intel's Gaudi, which claim 30%-40% lower inference power draw. As data centers scramble to secure renewable energy power purchase agreements, energy costs remain a primary sensitivity in total-cost-of-ownership models for GPU deployments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Integration Type: Discrete GPUs Dominate Datacenter Acceleration

Discrete devices captured 65.38% of Europe GPU market share in 2025 and continue to widen the gap as hyperscalers place bulk orders for NVIDIA Blackwell and AMD Instinct accelerators. Europe GPU market size for discrete units is projected to expand at a 17.74% CAGR to 2031, supported by sovereign-compute mandates that prioritize on-premises hardware capable of multi-petaflop training. Blackwell B200 and B300 cards, paired in NVLink racks, let operators shrink model training cycles from weeks to days, directly boosting time-to-market for European large language models. AMD’s Instinct MI300X, with 192 GB of HBM3 at 5.2 TB/s, answers memory-bound inference challenges faced by broadcasters and defense agencies. Integrated GPUs remain critical in client PCs and handheld consoles, yet their share of the European GPU market size is projected to decline as compute-intensive workloads outpace their thermal budgets.

Intel’s Meteor Lake system-on-chips, though prevalent in laptops, cannot match the architectural headroom of discrete boards that now ship with 600 W-class liquid-cooling loops. Pricing dynamics also favor discrete parts; despite a 10%-15% list-price increase announced for consumer cards, datacenter SKUs enjoy steady allocation priority and premium margins. This shift elevates discrete designs from a traditional graphics accessory to a cornerstone of Europe’s digital-sovereignty strategy.

By Device Application: Servers And Datacenters Lead Growth

Servers and datacenter accelerators accounted for 33.57% of the European GPU market in 2025 and are poised to grow the fastest, advancing at a 17.58% CAGR through 2031 as AI training clusters transition from pilot phases to production scale. The United Kingdom alone plans to deploy more than 70,000 additional GPUs by 2027, while France is lining up roughly 67,000 new units across Mistral AI, Sesterce, and Fluidstack projects. These rollouts push the installed base of datacenter GPUs in Western Europe past 300,000 by 2028 and drive specialized demand for liquid-cooling infrastructure.

In contrast, PCs and workstations, which held about 28% of the market share, experience steady but slower refresh cycles tied to media-creation and simulation workloads. Automotive compute, though at just 5% today, is poised for double-digit growth as EU safety regulations mandate sensor fusion and real-time inference, benefiting vendors that certify GPUs to functional-safety standards. Handheld and console shipments add volume diversity but cannot match the revenue density of high-end boards priced north of USD 30,000 per card. Consequently, servers and datacenter accelerators set the tone for roadmap decisions, influence foundry allocation, and capture the most pressurized share of high-bandwidth-memory supply.

Geography Analysis

Germany contributed 27.83% of regional revenue in 2025, leveraging its automotive and industrial base along with a robust research network that deploys GPU-accelerated high-performance computing clusters. Persistent energy prices near EUR 0.30 per kWh are driving an aggressive pivot toward efficient architectures and renewable energy sourcing. The United Kingdom emerges as the next demand epicenter, propelled by the USD 42.3 billion AI-infrastructure commitment that earmarks more than 70,000 additional GPUs for deployment by 2027. Public-private partnerships such as Isambard-AI, which integrates 5,448 NVIDIA GH200 Grace Hopper chips, exemplify how national strategy translates into procurement scale.

France records the fastest trajectory, with a 15.83% CAGR outlook through 2031, anchored by Mistral AI’s 13,800-GPU build, Sesterce’s EUR 450 million (USD 486 million) Valence project, and Fluidstack’s one-gigawatt supercomputer blueprint that targets half-a-million chips by 2026. These initiatives dramatically expand France's share of the European GPU market and contribute to a competitive datacenter corridor stretching from Île-de-France to Auvergne-Rhône-Alpes. Italy gains strategic relevance via Silicon Box’s EUR 3.2 billion (USD 3.5 billion) advanced-packaging facility in Novara, which provides chiplet services aligned with GPU supply chains, while STMicroelectronics extends mature-node capacity that indirectly feeds board-level component sourcing.

Nordic countries and Benelux regions capitalize on renewable-energy abundance and lower electricity tariffs around EUR 0.18 per kWh to attract hyperscale edge nodes for cloud-gaming and AI-inference workloads. Spain and Poland supplement regional dynamics by offering cost-competitive labor pools and expanding R&D centers that specialize in driver development and workload optimization. Across the continent, the combination of sovereign-compute policies, energy-market differentials, and datacenter tax incentives determines the local cadence of GPU adoption and shapes the competitive map into the next decade.

Competitive Landscape

NVIDIA holds a significant share of discrete GPU shipments in Q4 2025, leveraging its CUDA software ecosystem and NVLink interconnect to build a formidable moat that shapes the European GPU market. AMD is gaining a foothold among customers that favor open-source ROCm and larger on-package memory, with visible wins at France’s Alice Recoque supercomputer and Ubuntu 26.04 LTS native integration. Intel remains a distant third in discrete accelerators but commands the integrated-graphics space through Meteor Lake and Lunar Lake mobile processors that ship in high volume across European OEM laptops.

Vertical-integration plays reinforce supplier leverage. NVIDIA’s Mellanox acquisition enables low-latency networking crucial for multi-GPU clusters, while AMD’s Xilinx purchase broadens its heterogeneous compute story with embedded FPGAs. SoftBank’s buyout of Graphcore introduces an Arm-based alternative that pairs Ampere CPUs with IPU accelerators and continues to court European public-sector workloads. Meanwhile, SiPearl’s Rhea1 and Athena1 processors represent early steps toward a sovereign accelerator stack that could, over time, moderate reliance on U.S. vendors.

Pricing pressure ripples across the channel. NVIDIA and AMD signaled price hikes on consumer cards in early 2026, squeezing margins for European system integrators already contending with elevated GDDR6 spot prices. Datacenter buyers mitigate exposure through long-term supply agreements that lock in allocations at predetermined rates. The overall landscape remains concentrated, yet pockets of opportunity exist for cloud providers such as Scaleway, which in December 2025 became the first European vendor to offer NVIDIA B300-based GPU-as-a-Service instances compliant with data-residency regulation.

Europe GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Qualcomm Technologies Inc.

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Canonical released Ubuntu 26.04 LTS with native AMD ROCm integration, offering up to 15 years of support for AI libraries and toolchains.

- April 2026: The European Broadcasting Union renewed its partnership with NVIDIA to advance sovereign AI infrastructure for member broadcasters.

- March 2026: AMD unveiled Ryzen AI 400 Series processors with integrated RDNA 4 graphics, delivering 50 TOPS of on-device inference and targeting Q2 2026 availability.

- February 2026: Samsung introduced the Exynos 2600 featuring the RDNA 4-based Xclipse 960 GPU, which debuts in Galaxy S26 smartphones for European markets.

Europe GPU Market Report Scope

The Europe GPU Market Report is Segmented by Integration Type (Integrated GPUs and Discrete GPUs), Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, and Other Embedded and Edge Devices), and Country (Germany, United Kingdom, France, Italy, and rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) |

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe |

| By Integration Type | Integrated GPUs (iGPU) | |

| Discrete GPUs (dGPU) | ||

| By Device Application | Mobile Devices and Tablets | |

| PCs and Workstations | ||

| Servers and Datacenter Accelerators | ||

| Gaming Consoles and Handhelds | ||

| Automotive / ADAS | ||

| Other Embedded and Edge Devices | ||

| By Geography | Europe | Germany |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the European GPU market expected to be by 2031?

The market is forecast to reach USD 54.15 billion by 2031, driven by sustained data center and automotive demand.

Which segment will add the most revenue to suppliers?

Servers and datacenter accelerators, already 33.57% of spending in 2025, are growing the fastest at a 17.58% CAGR through 2031.

Why are energy prices a concern for GPU operators?

Electricity in Germany can cost EUR 0.30 per kWh, making annual power bills for a single H100 roughly USD 2,018, far above U.S. costs.

What policy supports local semiconductor capacity?

The EUR 43 billion European Chips Act funds fabs and packaging lines to reduce reliance on overseas foundries.

Which country shows the fastest market growth?

France leads with a projected 15.83% CAGR through 2031, thanks to multi-gigawatt AI data center investments.

Page last updated on: