Germany Discrete GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

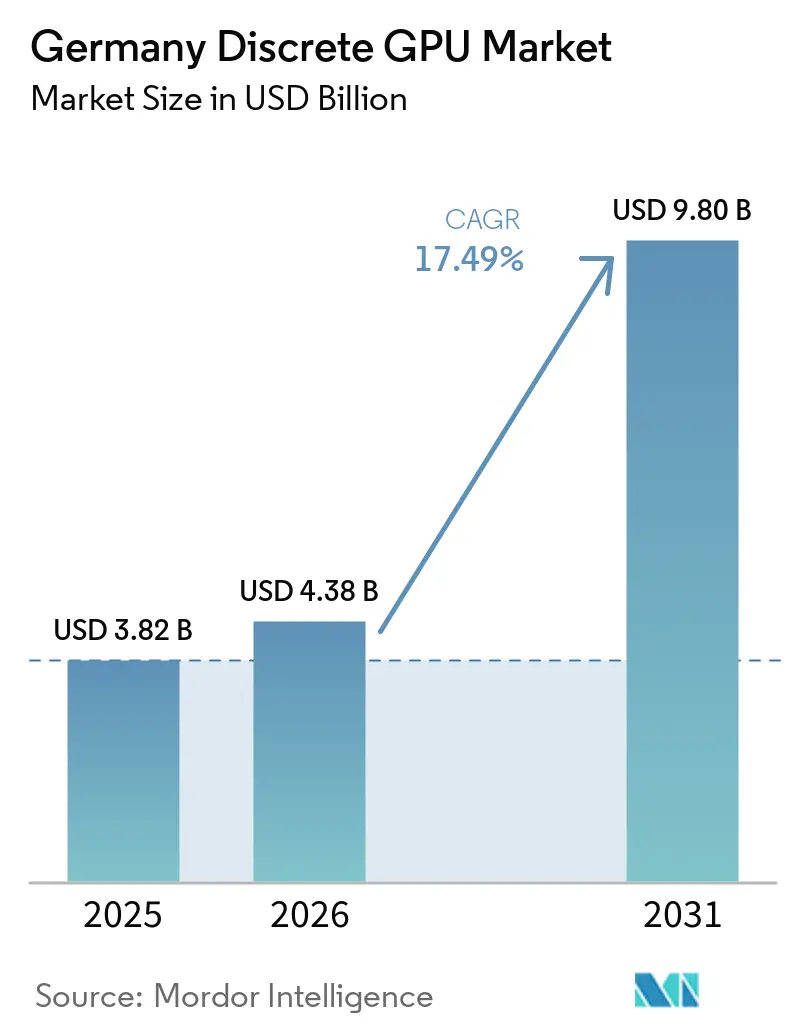

| Base Year Market Size (2025) | USD 3.82 Billion |

| Market Size (2026) | USD 4.38 Billion |

| Market Size (2031) | USD 9.80 Billion |

| Growth Rate (2026 - 2031) | 17.49% CAGR |

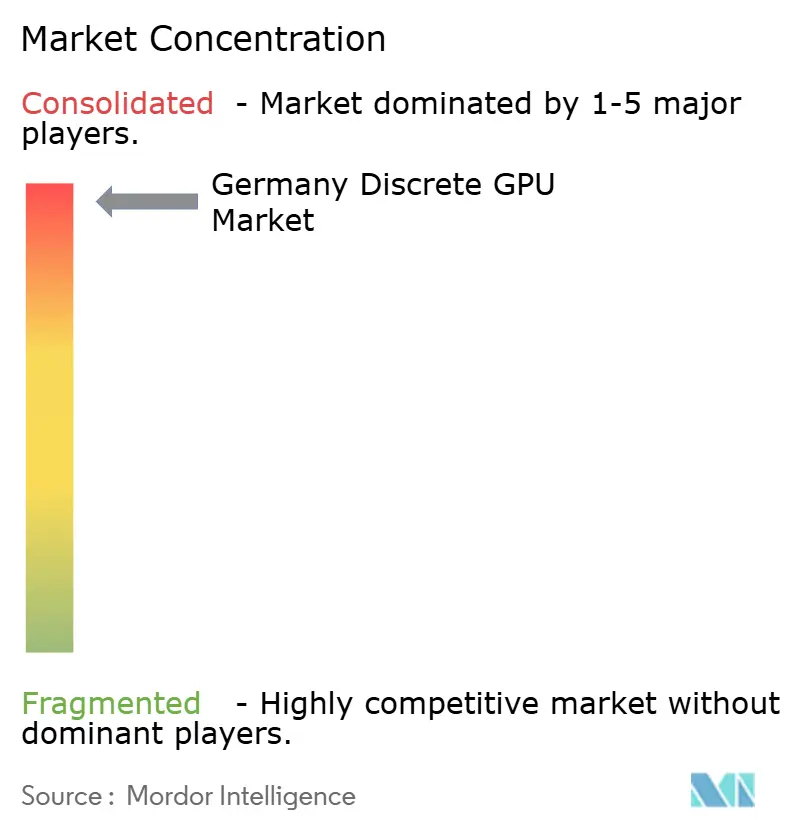

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Discrete GPU Market Analysis by Mordor Intelligence

The Germany discrete GPU market size is expected to increase from USD 3.82 billion in 2025 to USD 4.38 billion in 2026 and reach USD 9.80 billion by 2031, growing at a CAGR of 17.49% over 2026-2031. A surge in sovereign-AI investments, rapid upgrades of in-country data centers, and strict energy-efficiency mandates are reshaping demand patterns. Enterprise buyers now command priority allocation, and more than 35,000 Blackwell-class accelerators entered German server rooms between late 2025 and early 2026, lifting national AI compute capacity by roughly 50%. In parallel, the federal IPCEI Microelectronics program earmarked over EUR 3 billion (USD 3.39 billion) to stimulate domestic chip production, favoring projects that target AI, sensor fusion, and power electronics. Gaming and professional visualization still underpin a vibrant consumer base, yet retail GPU volumes fell by more than 70% as distributors diverted shipments to cloud operators. Memory architecture is bifurcating: while GDDR accounts for most unit sales, HBM-equipped accelerators are the clear growth engine as bandwidth gains outweigh cost premiums.

Key Report Takeaways

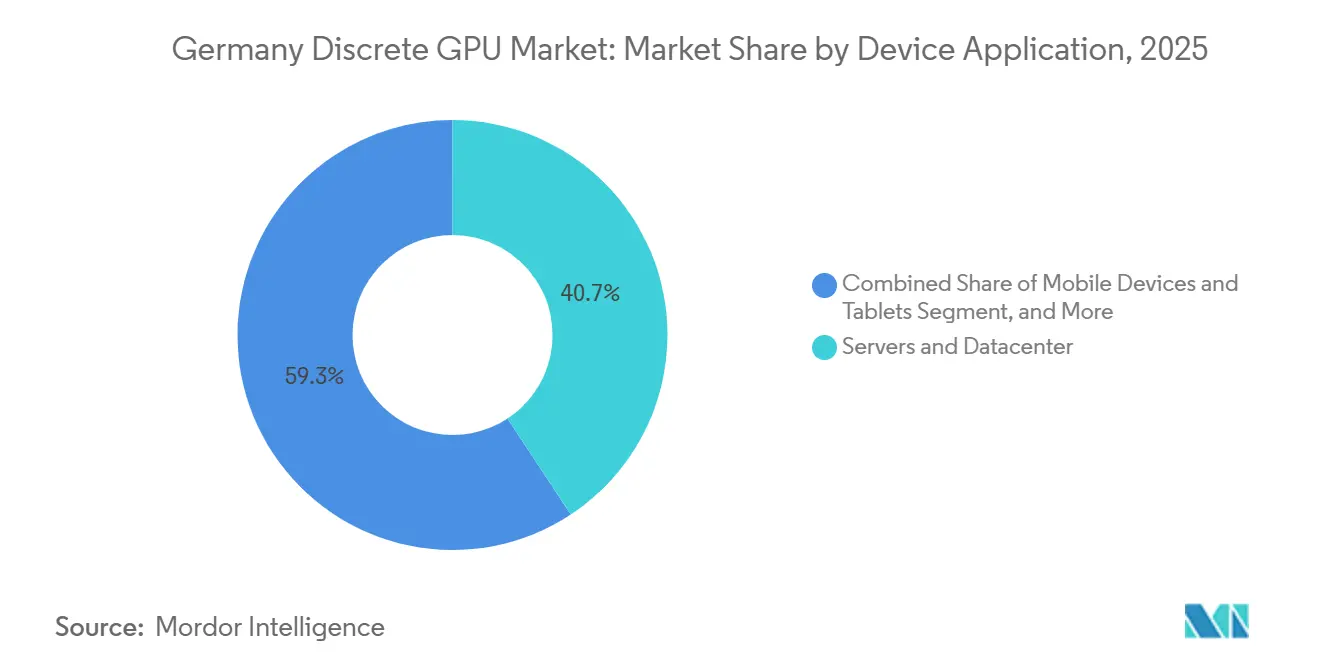

- By device application, servers and datacenter accelerators led with 40.73% revenue share in 2025, whereas the same segment is projected to expand at a 17.75% CAGR through 2031.

- By memory type, GDDR-based products captured 71.29% of 2025 revenue, while HBM-equipped GPUs are forecast to achieve a 17.93% CAGR to 2031.

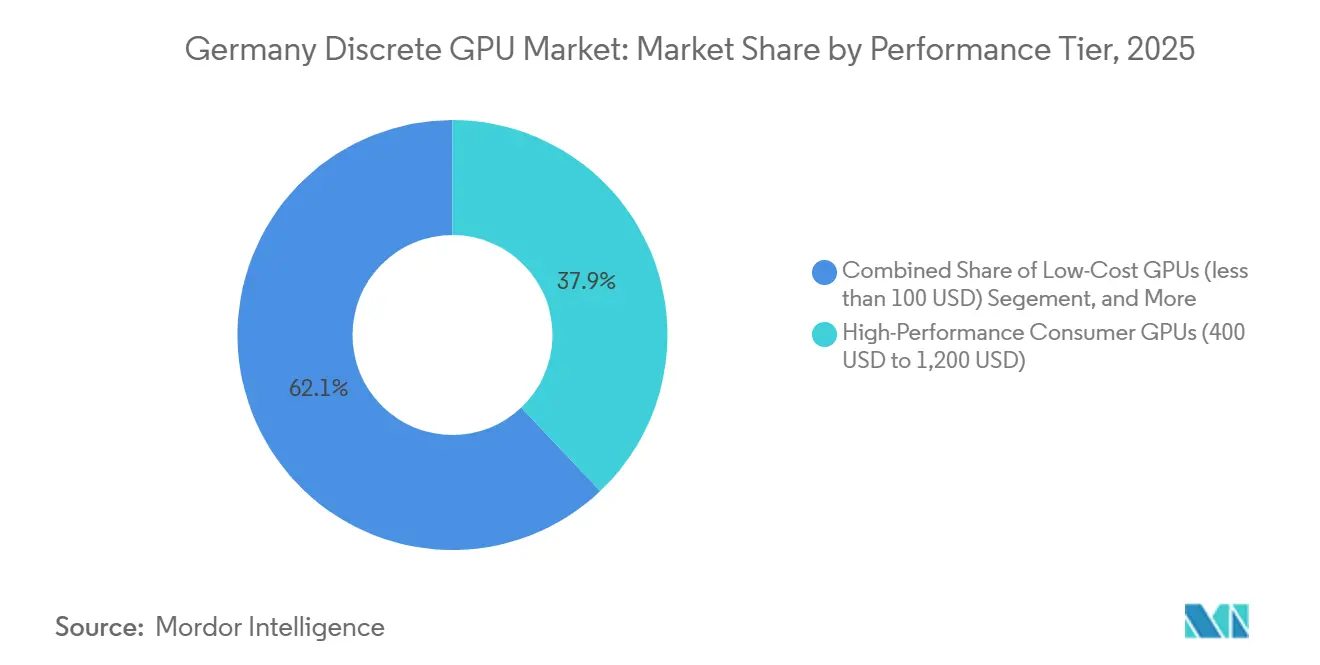

- By performance tier, high-performance consumer cards accounted for 37.93% of 2025 revenue, while data-center GPUs priced above USD 1,200 hold the fastest growth outlook at 17.98% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Discrete GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact |

|---|---|---|---|

| Surging Demand for AI and HPC Workloads in German Data Centers | +5.8% | Germany (Munich, Frankfurt, Lübbenau) and wider EU sovereign-cloud projects | Medium term (2-4 years) |

| Robust PC Gaming and Esports Ecosystem in Germany | +3.2% | National gaming hubs | Short term (≤ 2 years) |

| Growing Adoption of GPU-Accelerated Workstations for Professional Visualization | +2.9% | Automotive clusters in Stuttgart and Munich | Medium term (2-4 years) |

| Energy-Efficiency Mandates Driving Upgrades to Advanced GPU Nodes | +2.4% | Germany/EU compliance-driven builds | Medium term (2-4 years) |

| Federal Subsidies for Semiconductor Investment Under IPCEI | +1.8% | Nationwide | Long term (≥ 4 years) |

| Industry 4.0 Edge Computing Pilots Requiring Embedded Discrete GPUs | +1.4% | Manufacturing regions (Baden-Württemberg, NRW, Bavaria) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for AI and HPC Workloads in German Data Centers

Germany’s sovereign-AI strategy has tilted GPU supply toward enterprise racks. Deutsche Telekom’s Tucherpark campus in Munich operates more than 1,000 DGX B200 systems, each drawing 12 MW of renewable power and delivering almost half an exaflop of compute. Early adopters, including Siemens, Agile Robots, and Quantum Systems, train digital twins and simulation workloads locally to comply with EU data-residency rules. Similar GPU clusters at Jülich, Freiburg, and Hamburg bring the national total to nearly 40,000 new accelerators, prompting consumer shortages as retail allocations shrink.

Robust PC Gaming and Esports Ecosystem in Germany

German gamers spent EUR 9.4 billion (USD 10.6 billion) in 2025, with hardware outlays up 12% year on year. Despite the enthusiasm, weekly discrete GPU sales at top retailers slid from roughly 2,800 cards to 675, evidencing a 76% unit collapse. Price elasticity remains high: average selling prices rose to EUR 1,100 (USD 1,243) for NVIDIA and EUR 585 (USD 661) for AMD, yet revenue still advanced.[2]Game – Verband der deutschen Games-Branche, “Marktdaten 2025,” game.deFederal grants for game studios climbed to EUR 125 million (USD 141 million) in 2026, ensuring a steady pipeline of domestic titles that rely on high-end graphics.[1]NVIDIA Corporate Blog, “Introducing DGX B200 and Blackwell Architecture,” nvidia.com

Growing Adoption of GPU-Accelerated Workstations for Professional Visualization

Automotive and engineering firms are shifting crash simulation, aerodynamics modeling, and digital-twin creation onto local RTX PRO and Radeon PRO workstations. An RTX PRO 4000 Blackwell board now delivers up to 1,000 INT8 TOPS, compressing prototype cycles from weeks to hours. OEMs prefer on-premise hardware to safeguard intellectual property and meet ISO 26262 requirements. This shift lifts workstation GPU average selling prices to EUR 2,500-4,000 (USD 2,825-4,520) and cements Germany discrete GPU market demand among professional users.

Energy-Efficiency Mandates Driving Upgrades to Advanced GPU Nodes

The Energy Efficiency Act enforces a PUE ceiling of 1.2 for new data centers from July 2026 and drives liquid-cooling adoption. Operators that fail to hit the threshold face EUR 100,000 (USD 113,000) fines. Blackwell-based systems consume 30-40% less power per compute unit than prior Hopper cards, allowing data centers to hit compliance without scaling back capacity. Waste-heat reuse goals, set at a 20% Energy Reuse Factor by 2028, further accelerate replacement cycles of 2019-vintage GPUs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Disruptions and GPU Shortages | -3.6% | Global, acute in Germany | Short term (≤ 2 years) |

| High Up-Front Cost of High-Performance GPUs | -2.8% | Germany, especially SMEs and consumers | Medium term (2-4 years) |

| Stringent EU Environmental Regulations Raising Lifecycle Costs | -1.9% | Germany and EU | Medium term (2-4 years) |

| Competition from Integrated GPUs in Entry-Level Segments | -1.2% | Mobile and notebook categories | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions and GPU Shortages

TSMC’s limited CoWoS packaging lines and tight HBM3E supply from SK Hynix, Micron, and Samsung have pushed German retail inventories to historic lows. Street prices for an RTX 5090 exceed USD 4,000, double the launch MSRP, and even AMD’s mid-range cards face multi-week backorders. The government’s sovereign-cloud push intensifies the squeeze as operators lock in bulk orders, sidelining consumer channels.

High Up-Front Cost of High-Performance GPUs

An eight-GPU DGX B200 node lists above USD 300,000, placing ownership beyond the reach of most mid-market enterprises. While GPU-as-a-service offerings lower entry hurdles, they introduce vendor lock-in and opaque pricing. In gaming, a three-year replacement cycle is at risk as top-tier cards now cost multiples of historic norms.[3]TechInsights Analysts, “Global HBM Market Share 2025,” techinsights.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Application: Datacenter Accelerators Drive the Upswing

Servers and datacenter accelerators contributed 40.73% of 2025 revenue to the Germany discrete GPU market share, reflecting the rapid installation of sovereign-AI clusters. The segment is projected to post a 17.75% CAGR to 2031, ensuring it remains the linchpin of Germany discrete GPU market growth. Consumer PCs and professional workstations together form the second pillar, yet their volumes have fallen sharply as supply diverts toward enterprise racks. Gaming consoles and handhelds remain niche because they bundle custom APUs rather than discrete cards, while integrated GPUs in thin-and-light notebooks further erode entry-level demand.

Germany discrete GPU market size for servers will continue to swell as Deutsche Telekom, Google, and Schwarz Group collectively add another 30,000-plus accelerators in sites scheduled for completion by 2027. Automotive edge servers running digital twins, along with Industry 4.0 gateways that need local inferencing, strengthen long-tail adoption. Conversely, mobile and tablet categories lean on ARM-based SoCs with embedded GPUs, undercutting discrete attach rates.

By Memory Type: HBM Ascends Amid GDDR Dominance

GDDR-equipped boards captured 71.29% of 2025 revenue and still dominate volume shipments, anchoring mainstream gaming rigs and mobile workstations. Early GDDR7 devices clock 32-48 Gbps per pin, but cost considerations keep many cards on GDDR6. HBM-based accelerators, however, are forecast to grow at 17.93%, outpacing every other memory segment in the Germany discrete GPU market.

Germany discrete GPU market size tied to HBM stacks is rising because large-language-model training needs 1 TB/s-plus bandwidth per package. NVIDIA’s H200 and AMD’s MI300X, both outfitted with HBM3E, headline enterprise orders, while HBM4 sampling signals another bandwidth leap to 2-2.5 TB/s. Supply bottlenecks persist since SK Hynix alone controls roughly 62% of the wafer starts, but long-term contracts with German hyperscalers ensure a growing footprint.

By Performance Tier: Enterprise-Grade Cards Take the Lead

High-performance consumer products, priced USD 400-1,200, retained 37.93% revenue share in 2025 yet confront supply and affordability headwinds. The mainstream bracket sees AMD’s RX 9060 XT and Intel’s Arc B70 wrestling for budget-conscious buyers. Meanwhile, data-center GPUs above USD 1,200 will log the fastest 17.98% CAGR to 2031, making them the primary driver of Germany discrete GPU market expansion.

Germany discrete GPU market share commanded by ultra-high-end accelerators is swelling because each sovereign-AI build absorbs thousands of boards at USD 30,000-40,000 apiece. Financing models such as reserved capacity and lease-back agreements widen access for mid-tier firms, yet price sensitivity still limits reach into smaller enterprises. Integrated graphics encroach on sub-USD 100 territory, effectively capping discrete uptake in entry-level laptops.

Geography Analysis

Munich anchors the German discrete GPU market as Deutsche Telekom’s EUR 1 billion (USD 1.13 billion) Tucherpark hub delivers 10,000 Blackwell cards for the local industry. Frankfurt follows, where Google’s EUR 5.5 billion (USD 6.21 billion) facility deploys up to 15,000 GPUs to extend its European cloud footprint. Lübbenau in Brandenburg houses Schwarz Group’s EUR 11 billion (USD 12.4 billion) complex for retail AI, signaling an eastward shift in data-center gravity.

Stuttgart’s automotive corridor propels workstation sales as Mercedes-Benz, Porsche, and Bosch adopt RTX PRO setups for ADAS simulation. Bavaria and Baden-Württemberg enjoy spillover benefits from IPCEI grants, whereas North Rhine-Westphalia and Saxony lag in fresh GPU capacity despite strong manufacturing bases. The JUPITER supercomputer in Jülich mitigates some latency concerns for Western SMEs, but firms in Saxony still rely on Munich cloud slices, which adds cost overhead.

Regulation shapes geographic deployment. New sites must reach PUE 1.2 and ERF 10% from mid-2026, driving liquid-cooling adoption and co-location with district-heating networks. Operators in colder regions, such as Leipzig, can exploit ambient temperatures to meet targets more easily, whereas urban Munich facilities invest heavily in advanced cooling loops tapping the Eisbach stream. These compliance dynamics further concentrate Germany discrete GPU market investments in areas with renewable energy access and municipal heat-reuse schemes.

Competitive Landscape

NVIDIA controls an estimated 80-85% of the German datacenter segment through a strategy of vertical integration and exclusive supply agreements. Its Vera Rubin platform blends custom CPUs, GPUs, and Ethernet fabrics, tightening ecosystem lock-in for customers that already rely on CUDA. AMD challenges through price-performance plays: the Radeon RX 9070 XT undercuts NVIDIA’s RTX 5080 by roughly 20% at launch, while MI300X pushes 192 GB HBM3E to differentiate on memory capacity. Intel leverages the Arc Pro B70 and its EUR 30 billion (USD 33.9 billion) Magdeburg fab plan to signal long-term supply security, appealing to workstation buyers wary of allocation shocks.

Add-in-board partners such as Palit, Gainward, Sapphire, and PowerColor sustain retail availability, yet their fate hinges on upstream chip allocations. In professional visualization, NVIDIA maintains dominance by offering certified drivers for Siemens NX and Autodesk Inventor, but AMD secures incremental share in automotive clusters thanks to competitive ISV validation. Intel’s oneAPI toolchain gains traction in university labs seeking an open-standards alternative.

Disruptive entrants, Graphcore, Tenstorrent, SiPearl, court niche HPC deployments but struggle with software maturity. Compliance has become a differentiator: vendors that provide ISO 26262 safety stacks, liquid-cooling-ready reference designs, and PUE calculators win bids from operators racing to meet the Energy Efficiency Act. Consequently, the Germany discrete GPU market is consolidating around suppliers that control both silicon and the surrounding ecosystem.

Germany Discrete GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Imagination Technologies Limited

ARM Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Deutsche Telekom and NVIDIA completed a EUR 1 billion (USD 1.13 billion) AI datacenter in Munich, installing 10,000 Blackwell GPUs for sovereign-cloud workloads.

- March 2026: Intel unveiled the Arc Pro B70 at USD 949, bundling 32 GB GDDR6 and targeting AI inference in German workstations.

- March 2026: AMD released Radeon RX 9070 XT at USD 599 and RX 9070 at USD 549, both with second-generation AI accelerators.

Germany Discrete GPU Market Report Scope

A discrete GPU, or discrete graphics processing unit, is a dedicated hardware component designed exclusively to handle graphics rendering and parallel computational tasks, operating independently from the central processing unit (CPU) with its own dedicated video memory (VRAM) and power circuitry.

The Germany Discrete GPU Market Report is Segmented by Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, and Other Embedded and Edge Devices), Memory Type (GDDR-based GPUs, and HBM-based GPUs), Performance Tier (Low-Cost GPUs (less than 100 USD), Mainstream GPUs (100 USD to 400 USD), High-Performance Consumer GPUs (400 USD to 1,200 USD), and Data Center / AI Accelerator GPUs (greater than 1,200 USD)). The Market Forecasts are Provided in Terms of Value (USD).

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| GDDR-based GPUs |

| HBM-based GPUs |

| Low-Cost GPUs (less than 100 USD) |

| Mainstream GPUs (100 USD to 400 USD) |

| High-Performance Consumer GPUs (400 USD to 1,200 USD) |

| Data Center / AI Accelerator GPUs (greater than 1,200 USD) |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices | |

| By Memory Type | GDDR-based GPUs |

| HBM-based GPUs | |

| By Performance Tier | Low-Cost GPUs (less than 100 USD) |

| Mainstream GPUs (100 USD to 400 USD) | |

| High-Performance Consumer GPUs (400 USD to 1,200 USD) | |

| Data Center / AI Accelerator GPUs (greater than 1,200 USD) |

Key Questions Answered in the Report

How large will Germany discrete GPU market spending be by 2031?

The Germany discrete GPU market size reaching about USD 9.80 billion by 2031, driven by sovereign-AI datacenter roll-outs and workstation refresh cycles.

Which application captures the most value in Germany for discrete GPUs?

Servers and datacenter accelerators already hold roughly 41% of revenue and are projected to grow the fastest at a 17.75% CAGR, reflecting enterprise preference for on-premise AI compute.

Why are retail GPU prices in Germany so high in 2026?

Supply is constrained by HBM shortages and datacenter pre-orders, pushing street prices for flagship consumer cards such as the RTX 5090 above USD 4,000.

What role do energy-efficiency regulations play in German GPU demand?

The Energy Efficiency Act requires new data centers to operate at PUE 1.2 or better from mid-2026, prompting rapid adoption of liquid-cooled Blackwell and MI300X boards that deliver superior performance per watt.

Page last updated on: