United Kingdom GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

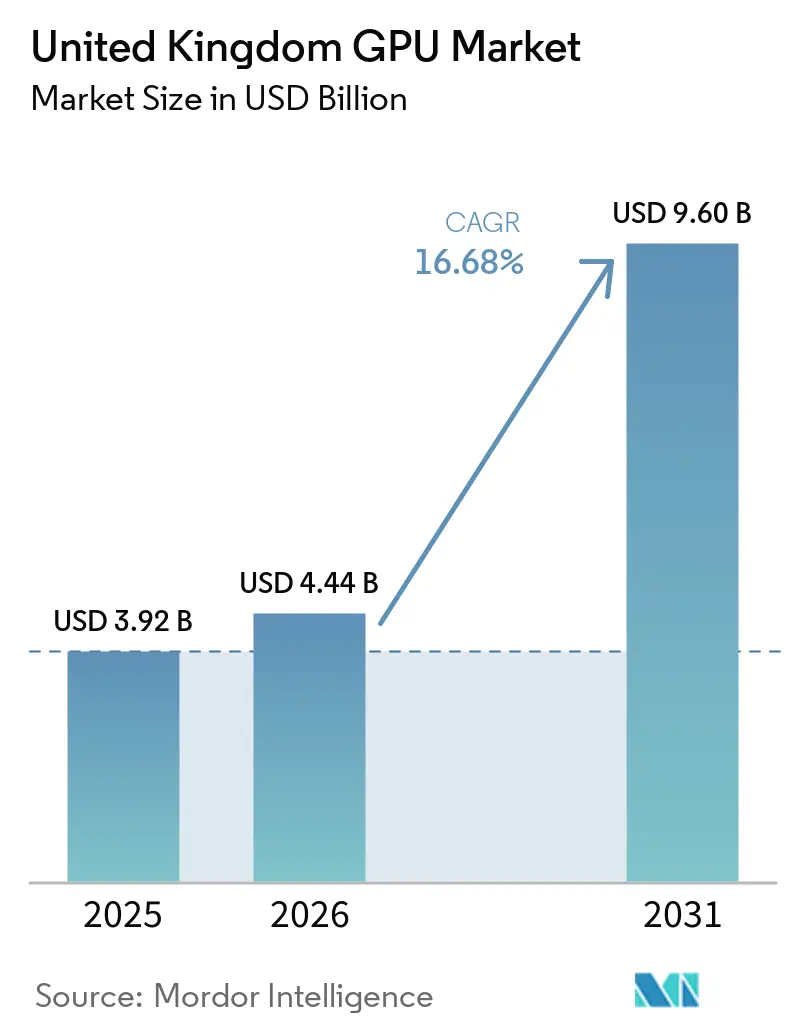

| Base Year Market Size (2025) | USD 3.92 Billion |

| Market Size (2026) | USD 4.44 Billion |

| Market Size (2031) | USD 9.60 Billion |

| Growth Rate (2026 - 2031) | 16.68% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom GPU Market Analysis by Mordor Intelligence

The United Kingdom GPU market size expanded from USD 3.92 billion in 2025 to USD 4.44 billion in 2026 and is projected to reach USD 9.60 billion by 2031, registering a 16.68% CAGR over 2026-2031. Momentum comes from sovereign-AI mandates that favor domestic compute, hyperscale roll-outs of Blackwell-class accelerators, and rising enterprise appetite for local inference at regulated institutions. Within the broader digital-economy landscape, escalating datacenter investments collide with grid bottlenecks, elevating power costs yet simultaneously catalyzing renewable procurement. Hardware vendors respond with higher-bandwidth memory stacks and liquid-cooling reference designs, while system integrators position modular GPU clusters as compliance-ready building blocks for finance, healthcare, and critical infrastructure. These intertwined forces reinforce a virtuous cycle in which policy, technology, and capital coalesce around high-density compute hubs, anchoring the United Kingdom GPU market as a bellwether for edge-heavy architectures.

Key Report Takeaways

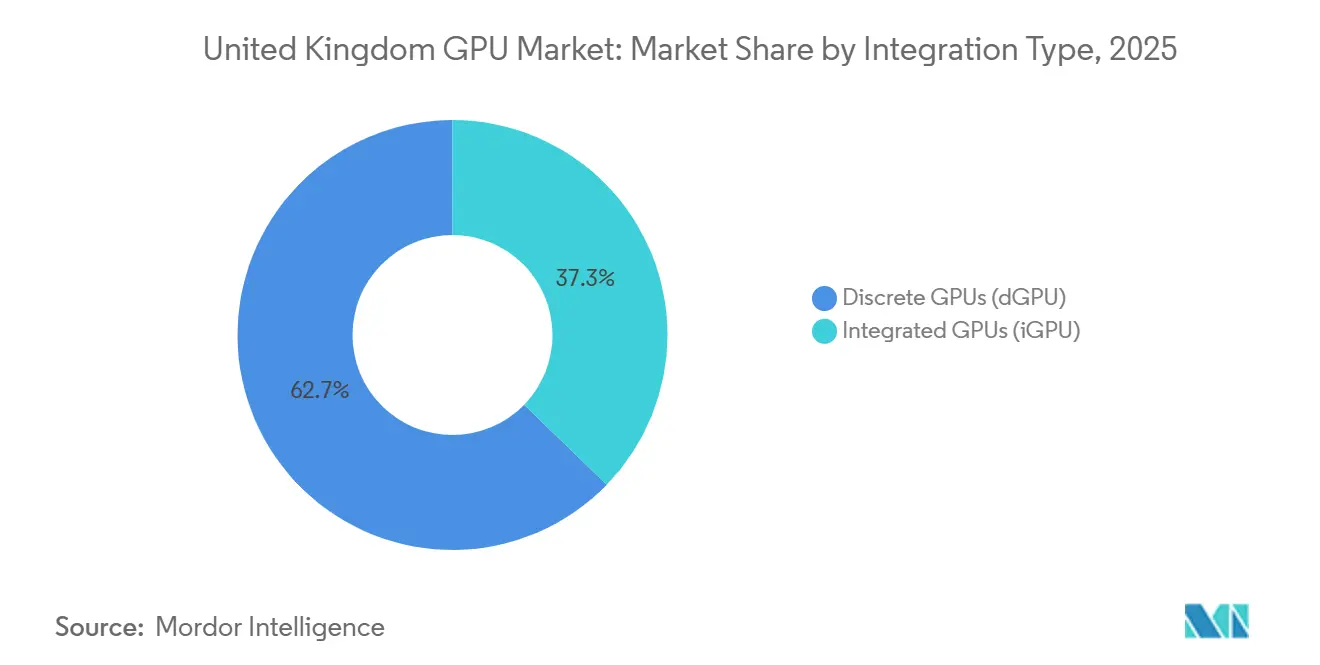

- By integration type, discrete GPUs captured 62.73% value in 2025 and are advancing at a 16.93% CAGR through 2031, the fastest pace among form factors.

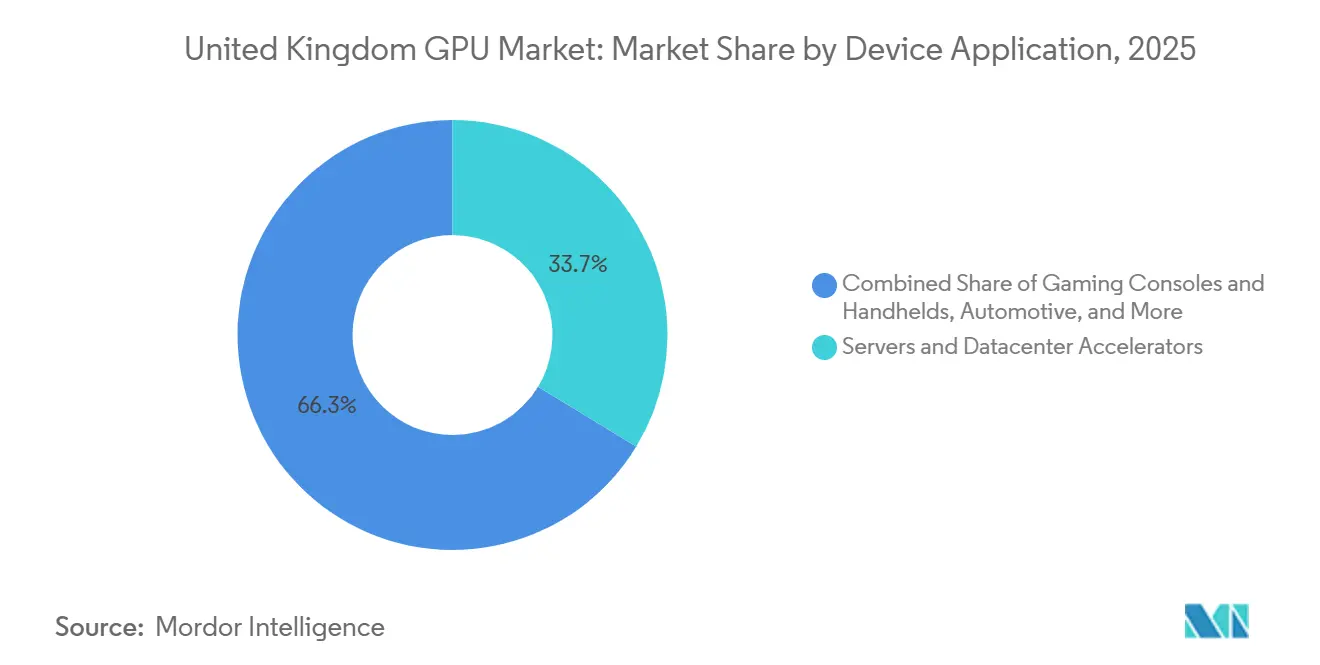

- By device application, servers and datacenter accelerators commanded 33.68% share in 2025 and are expanding at a 17.05% CAGR, outstripping every other usage segment.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for AI Training Accelerators in UK Data Centers | +4.50% | National, concentrated in London, Manchester, Edinburgh, South Wales | Medium term (2-4 years) |

| UK Sovereign-AI Initiatives Fueling Domestic GPU Clusters | +3.50% | National, priority zones in South Wales, Scotland, North England | Short term (≤ 2 years) |

| Enterprise Adoption of GPU-Accelerated Analytics and HPC | +2.20% | National, strongest in London finance and Cambridge-Oxford life-sciences corridor | Short term (≤ 2 years) |

| Growth of Cloud Gaming and eSports Ecosystem | +1.80% | National, urban hubs in London, Birmingham, Manchester | Medium term (2-4 years) |

| Expansion of Autonomous Vehicle R&D and ADAS Programs | +1.50% | National, early gains in London, Cambridge, Milton Keynes | Long term (≥ 4 years) |

| Shift Toward On-Device Inference for Privacy Compliance | +1.20% | National, rapid pickup in finance, healthcare, critical infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging demand for AI Training Accelerators in UK Data Centers

Hyperscale operators have booked up to 120,000 Blackwell-generation GPUs for United Kingdom facilities by late 2026, with one provider alone targeting 60,000 Grace Blackwell units. Public-sector projects such as Isambard-AI and Dawn upgrades illustrate the government's resolve to anchor sovereign compute domestically, while economic studies suggest even modest capacity additions could inject billions of pounds into annual GDP.

UK Sovereign-AI Initiatives Fueling domestic GPU Clusters

The 2025 AI Growth Zones Initiative streamlines planning approvals and grid connections, pairing fiscal incentives with a GBP 1 billion public investment and a GBP 1.5 billion industry pledge from the Sovereign AI Industry Forum. These measures shorten project lead times, steer workloads to regions rich in renewable potential, and create a policy backstop that underwrites long-cycle capital commitments. [1]U.K. Department for Science, Innovation and Technology, “AI Growth Zones Initiative,” gov.uk

Enterprise adoption of GPU-Accelerated Analytics and HPC

Regulatory sandboxes run by the Financial Conduct Authority use GPU-powered testbeds to let banks prototype models under supervisory oversight, while capital-markets vendors incorporate GPU acceleration to compress risk-calculation windows from hours to minutes. Academic-industry partnerships, exemplified by University College London’s quantum-GPU hybrid demo, point toward heterogeneous compute stacks that keep the United Kingdom GPU market at the frontier of scientific discovery. [2]Financial Conduct Authority, “Regulatory Sandbox for AI,” fca.org.uk

Growth of Cloud Gaming and Esports Ecosystem

Online gamers increase steadily, and eSports prize pools exceed USD 47 million, nurturing a performance-conscious enthusiast tier that values high-refresh displays and discrete silicon. Yet improved fiber backbones and 5G coverage enable low-latency streaming, nudging casual players toward subscription services and concentrating hardware demand among competitive gamers and content creators.[3]Esports Earnings LLC, “Global Esports Rankings,” esportsearnings.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Global GPU Supply Chain Constraints and Elevated Pricing | -2.50% | Global, acute in UK owing to import dependence and currency swings | Short term (≤ 2 years) |

| High Power and Cooling Costs in UK Data Centers | -1.80% | National, most severe in South-East England | Medium term (2-4 years) |

| Talent Shortage in GPU Programming and CUDA Expertise | -0.80% | National, tech clusters in London, Cambridge, Edinburgh | Medium term (2-4 years) |

| Regulatory Scrutiny on AI Energy Use and Carbon Emissions | -0.60% | National, focus on datacenter permits | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Global GPU Supply Chain Constraints and Elevated Pricing

High-bandwidth memory shortages and year-long advanced-node lead times force enterprises to lock in allocations far ahead of deployment, inflate street prices of flagship cards to USD 3,500-4,000, and delay AI projects across finance and healthcare by several quarters.[4]TrendForce, “HBM Supply Monitor 2025,” trendforce.com

High Power and Cooling Costs In UK Data Centers

Electricity near GBP 0.42 per kilowatt-hour, coupled with average rack densities heading toward 11 kilowatts, drives annual per-rack energy spend close to GBP 30,000 and pressures operators to locate farther from demand centers where renewable availability is higher but network latency rises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Integration Type: Discrete GPUs Dominate Training and Inference

Discrete accelerators captured 62.73% of the total value in 2025 as enterprises gravitated toward modular architectures suited for large-scale transformer training. The segment benefits from continual core-count increases, higher bandwidth memory, and software ecosystems tightly coupled to proprietary toolchains, effectively making the United Kingdom GPU market the proving ground for efficiency-ranked datacenter designs.

Integrated graphics continue to climb in mobile devices, strengthened by next-generation system-on-chips from Apple and AMD. While these embedded units will not displace discrete cards in multi-petaflop clusters, they satisfy everyday productivity and 1080p gaming, thereby lengthening consumer replacement cycles. The shift tempers unit volume for entry-level boards but raises the premium-tier average selling price, sustaining overall revenue momentum within the United Kingdom GPU market.

By Device Application: Servers and Datacenters Accelerate Fastest

Servers and datacenter accelerators held 33.68% of the 2025 value and are expanding at a 17.05% CAGR as hyperscalers prioritize compute-dense racks to meet Offline-First resilience rules and large-language-model demand. Early deployments of NVLink-connected Blackwell Ultra clusters signal a generational jump in throughput, prompting derivative demand for liquid cooling and high-efficiency power modules.

Desktop and workstation shipments soften as attach rates fall, yet specialized content-creation rigs remain indispensable for professional studios. Mobile form factors flourish on the back of integrated GPU gains, while automotive inference accelerators emerge as a nascent growth vector thanks to autonomous-driving pilots in London. Together, these trends create a diversified revenue mix that cushions the United Kingdom GPU market against cyclical swings in any single device class.

Geography Analysis

London and the South-East continue to dominate installed compute, but power-connection queues and land constraints redirect incremental capacity to South Wales, Scotland, and the North of England, regions prioritized under the AI Growth Zones scheme. Cardiff’s proximity to offshore wind and relatively inexpensive real estate underpins several 100-megawatt projects slated to break ground before 2027, reinforcing geographic dispersion while maintaining fiber backhaul to major conurbations.

Scotland leverages abundant onshore wind to attract liquid-cooled supercomputers supporting weather modeling, life sciences analytics, and emerging quantum-classical hybrid workloads. Availability of renewable certificates enhances corporate emissions reporting, a non-trivial factor as regulators scrutinize AI energy footprints. Northern Ireland, though smaller in absolute terms, positions edge nodes near telecommunication landing stations to serve latency-sensitive fintech applications that must comply with the 72-hour Offline-First mandate.

These regional dynamics yield a mosaic in which each nation within the United Kingdom claims a distinct specialization—London in financial inference, Wales in hyperscale training, Scotland in scientific HPC, and Northern Ireland in resilient edge services—collectively sustaining balanced expansion of the United Kingdom GPU market.

Competitive Landscape

A handful of global vendors supply the lion’s share of discrete accelerators, with one provider estimated to control well over four-fifths of shipments to United Kingdom datacenters. Strategic collaborations multiply: an agreement signed in 2025 pairs a leading CPU manufacturer’s chiplet strategy with a dominant GPU vendor’s cores for next-generation laptops, while the same GPU supplier secures processor volumes for its sovereign-compute customers.

Alternative architectures target price-performance niches. An American startup financed by more than USD 1 billion touts software-programmable ASICs that promise superior inference efficiency, whereas a Bristol-founded specialist now owned by a Japanese conglomerate shifts fabrication focus to India yet retains research staff in Cambridge. Hyperscalers hedge supply risk by co-developing custom accelerators with multiple silicon partners, signaling readiness to diversify away from single-vendor ecosystems whenever tooling support matures.

Regulators, investors, and academia increasingly converge on ecosystem lock-in as a competitive lever. An FCA sandbox built on one vendor’s software stack embeds that toolchain into compliance workflows, raising switching costs for financial institutions. University-led quantum-GPU pilots expand total-addressable compute without encroaching on incumbent vendor roadmaps, illustrating how public-private consortia shape the next era of heterogeneous processing inside the United Kingdom GPU market.

United Kingdom GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Imagination Technologies Limited

Arm Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: NVIDIA highlighted Wayve’s generative-AI training on Blackwell GPUs, confirming London robotaxi pilots in partnership with Uber.

- March 2026: University College London showcased a hybrid 54-qubit quantum processor linked to 120 H100 GPUs at NVIDIA GTC, underscoring sovereign AI ambitions.

- March 2026: Ofgem disclosed that datacenter grid-connection requests reached 125 gigawatts, triple the late-2024 levels, spotlighting strain on energy infrastructure.

- February 2026: Wayve secured USD 1.2 billion in Series D funding at an USD 8.6 billion valuation, the largest autonomous-driving raise in UK history.

United Kingdom GPU Market Report Scope

The United Kingdom GPU Market Report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs) and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) |

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| By Integration Type | Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) | |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices |

Key Questions Answered in the Report

What is driving most new demand for GPUs in the United Kingdom?

Sovereign-AI mandates and hyperscale datacenter expansions that require high-density training clusters.

How large can power costs grow for GPU racks located in the South-East?

Annual electricity spend approaches GBP 30,000 (USD 38,100) per rack at current tariffs.

Which GPU form factor is growing fastest?

Discrete accelerators used in servers and datacenters, advancing at a 16.93% CAGR through 2031.

Where are new hyperscale facilities being sited?

South Wales and Scotland, regions offering abundant renewable power and streamlined planning approvals.

Page last updated on: