Germany GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

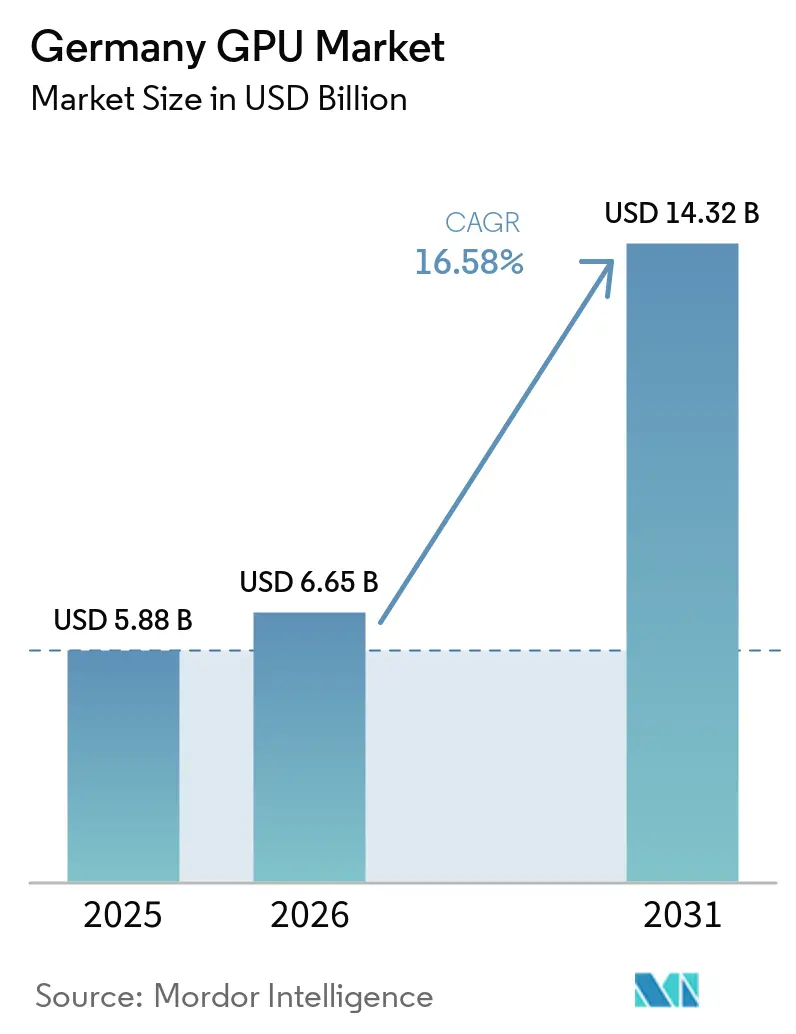

| Base Year Market Size (2025) | USD 5.88 Billion |

| Market Size (2026) | USD 6.65 Billion |

| Market Size (2031) | USD 14.32 Billion |

| Growth Rate (2026 - 2031) | 16.58% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany GPU Market Analysis by Mordor Intelligence

The Germany GPU market size is expected to increase from USD 5.88 billion in 2025 to USD 6.65 billion in 2026 and reach USD 14.32 billion by 2031, growing at a CAGR of 16.58% over 2026-2031. Sovereign artificial-intelligence infrastructure projects, stringent EU data-residency rules, and an expanding base of high-performance computing centers are the core factors pushing demand. Automotive original-equipment manufacturers (OEMs) are scaling datacenter-grade simulation farms for autonomous-driving validation, while esports events such as ESL One Cologne boost consumer appetite for high-refresh-rate gaming rigs. Renewable-energy operators adopt digital-twin models that shorten commissioning cycles and cut unplanned downtime, and federal incentives covering up to 25% of eligible R&D outlays reduce the effective cost of new GPU clusters.

Key Report Takeaways

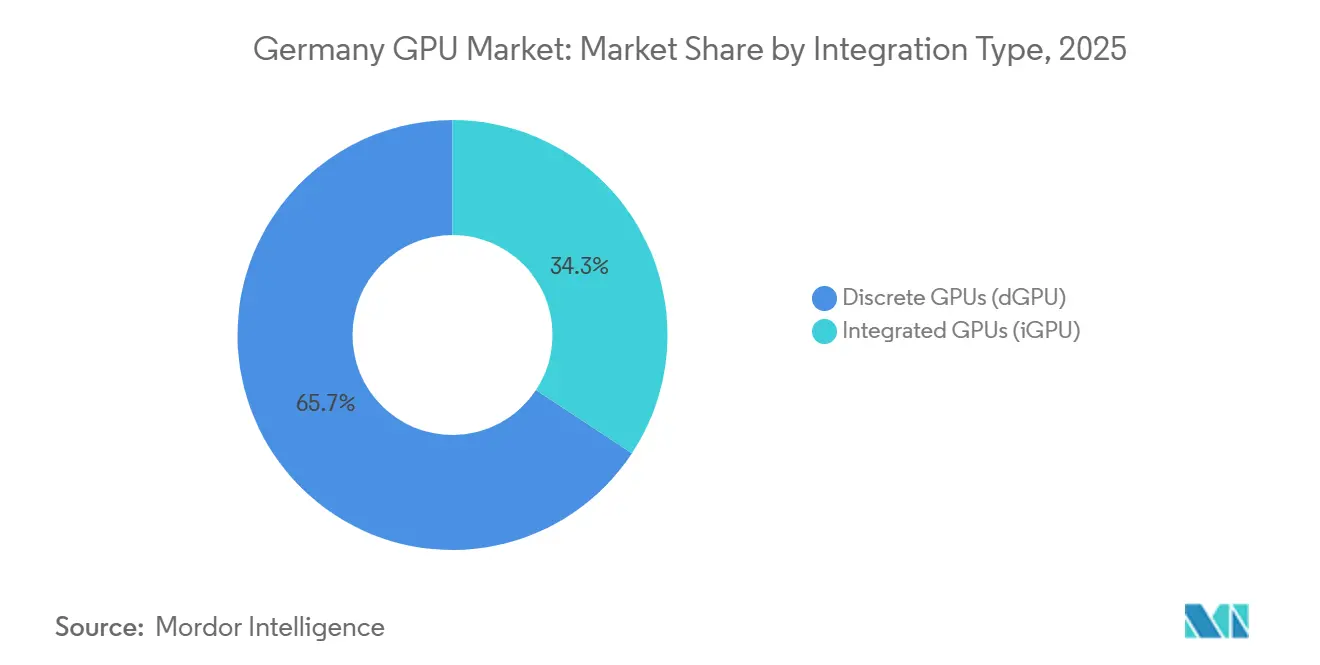

- Discrete GPUs held 65.73% of the Germany GPU market share in 2025 and are forecast to grow at a 17.11% CAGR through 2031.

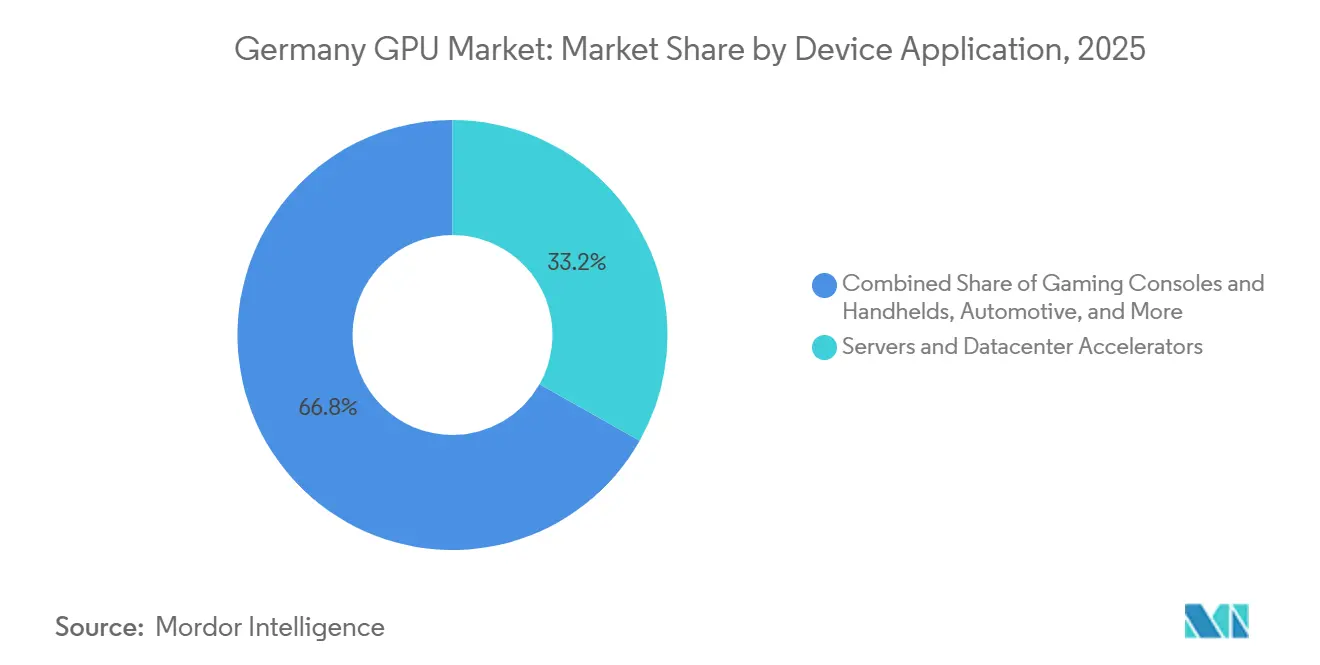

- Servers and datacenter accelerators accounted for 33.18% of the Germany GPU market size in 2025 and are projected to expand at a 16.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of AI and HPC Workloads | +6.20% | Germany-wide, led by Munich, Frankfurt, Stuttgart | Medium term (2-4 years) |

| Esports Expansion Driving High-End Gaming GPUs | +2.10% | Urban clusters, notably Berlin, Hamburg, Cologne | Short term (≤2 years) |

| Automotive OEM Adoption for ADAS Visualization | +3.80% | Baden-Württemberg, Bavaria, Lower Saxony | Long term (≥4 years) |

| Aerospace and Defence Simulation Workloads | +1.50% | Bavaria, North Rhine-Westphalia | Medium term (2-4 years) |

| Renewable-Energy Digital-Twin Simulations | +1.70% | Northern coastal states, Bavaria | Medium term (2-4 years) |

| German R&D Tax Incentives for Semiconductor IP | +1.30% | Nationwide, concentrated in SMEs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of AI and HPC Workloads

German enterprises are prioritizing on-premises GPU clusters to comply with the EU AI Act and avoid extraterritorial data requests. Deutsche Telekom’s Industrial AI Cloud in Munich, operational since February 2026 with 10,000 NVIDIA Blackwell GPUs, has pre-sold more than one-third of its capacity to anchor tenants that include Siemens and EY.[2]NVIDIA Blog, “BMW Expands DGX AI Training Cluster,” nvidia.com The Schwarz Group earmarked EUR 11 billion (USD 12.65 billion) for sovereign AI infrastructure, while national subsidies under the IPCEI Microelectronics program lower capital costs by 20-30%. Research centers inside the Gauss Center for Supercomputing are concurrently upgrading to the latest NVIDIA and AMD accelerators, underscoring how high-bandwidth-memory designs are now indispensable for climate modeling, drug discovery, and materials science.

Esports Expansion Driving High-End Gaming GPUs

Germany’s recognition of esports as an official sport has unlocked public funding for arenas and training facilities, institutionalizing GPU-intensive infrastructure. More than 45 million active gamers drive steady refresh cycles for discrete graphics cards capable of 240 Hz output and real-time ray tracing. Professional teams, G2 Esports, Berlin International Gaming, and SK Gaming, run training centers equipped with NVIDIA GeForce RTX 5080 and AMD Radeon RX 9070 XT boards that deliver sub-10-millisecond latency. Streaming creators often use dual-GPU setups for 4K60 encoding while maintaining 144-plus frame rates, reinforcing the market for high-end add-in-boards.[3]European Purpose, “Sovereign AI Infrastructure Gains Momentum in Germany,” european-purpose.eu

Automotive OEM Adoption for ADAS Visualization

Mercedes-Benz, BMW, and Volkswagen embed GPUs in both vehicle cockpits and centralized datacenter farms. Mercedes-Benz integrated NVIDIA DRIVE AV into flagship models for Level-3 autonomy, while BMW leverages NVIDIA DGX clusters to train perception models on petabyte-scale logs. Volkswagen’s 2026 pact with Qualcomm adds Snapdragon Ride Elite platforms across multiple brands, diversifying supply beyond NVIDIA. Continental and ZF Friedrichshafen benefit from centralized compute, amortizing capital expenditure across vehicle platforms and enabling faster over-the-air updates.

Aerospace and Defence Simulation Workloads

Rheinmetall training simulators for the C-390 Millennium, A400M, and Puma infantry vehicle use GPU-accelerated physics engines to render multi-spectral environments in real time. Airbus Defense and Space runs computational-fluid-dynamics workloads on GPU clusters to trim wind-tunnel costs by up to 40%.[1]Rheinmetall, “Next-Generation Training Simulators,” rheinmetall.com Bundeswehr digitalization contracts prescribe NATO STANAG 4586 compliance, which sets explicit GPU performance thresholds for synthetic-environment generation, propelling continued accelerator spending among defense contractors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Supply-Chain Disruptions | −2.8% | Global, impacting German buyers via TSMC and Samsung | Short term (≤2 years) |

| Escalating Average Selling Prices of dGPUs | −1.9% | Nationwide consumer and SME segments | Short term (≤2 years) |

| Energy-Efficiency Caps on Datacentre Hardware | −1.2% | Germany-wide, EU-mandated | Medium term (2-4 years) |

| Talent Shortage in GPU Software Optimisation | −1.5% | Major tech hubs, notably Munich and Berlin | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply-Chain Disruptions

TSMC’s fully booked CoWoS advanced-packaging lines extend GPU lead times beyond 12 months, delaying German deployments slated for early 2026. Shortfalls in HBM3e modules raise spot prices and compel enterprises to ration allocations among hyperscaler contracts, automotive projects, and sovereign AI clusters. Although the EU Chips Act commits EUR 43 billion to onshore fabs, new facilities will not come online before 2027, leaving near-term supply tight.

Escalating Average Selling Prices of dGPUs

Flagship discrete GPUs have launched at record price points, with NVIDIA’s GeForce RTX 5090 debuting at more than EUR 2,300. Persistent demand from AI researchers, paired with shortages in advanced DRAM and GPU dies, forces add-in-board partners to pass higher costs downstream. Small and medium-sized enterprises reliant on GPUs for CAD, video editing, and simulation are deferring refresh cycles by up to a year, slowing unit shipments in lower volume tiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Integration Type: Discrete GPUs Dominate Training and Inference

Discrete GPUs held 65.73% of the Germany GPU market share in 2025 and remain the workhorse for large-language-model training clusters. The Germany GPU market size for discrete accelerators benefits from Deutsche Telekom’s 10,000-GPU Munich installation and the Schwarz Group’s multi-site build-out, each designed to meet EU data-sovereignty rules. Integrated GPUs are nonetheless gaining ground in power-constrained automotive cockpits and Copilot+ laptops that rely on Qualcomm, AMD, and Intel SoCs delivering up to 80 TOPS on die.

Gaming and content-creation workloads reinforce discrete demand, as enthusiasts prioritize larger frame buffers and certified drivers. Conversely, sustained loads expose thermal throttling in integrated solutions, trimming real-world throughput. Integrated devices shine where energy budgets are fixed, yet for multi-hour ray-traced sequences or AI inference on 7-billion-parameter models, discrete cards still carry the performance edge.

By Device Application: Servers and Data Centers Lead Growth

Servers and datacenter accelerators represented 33.18% of the Germany GPU market size in 2025, and their 16.87% projected CAGR outstrips the consumer segments. Blackwell GPUs furnish 50 PFLOPS of inference per card, and AMD’s MI455X—with 432 GB of HBM4—persuades enterprises that need larger model checkpoints. PCs and workstations remain essential for architecture, engineering, and media, thanks to NVIDIA RTX 6000 Ada and AMD Radeon Pro W7900 boards with certified application drivers.

Automotive compute platforms consolidate ADAS, infotainment, and telematics on single boards, reducing wiring harness weight and enabling faster over-the-air updates. Mobile devices and tablets rely on integrated GPUs from Qualcomm, Apple, and Samsung for on-device language translation and image generation. Embedded modules such as NVIDIA Jetson Orin satisfy industrial vision and edge-AI needs in retail and logistics.

Geography Analysis

Bavaria and Baden-Württemberg anchor automotive-centric GPU demand, with OEMs operating vast simulation farms in Munich, Stuttgart, and Ingolstadt. North Rhine-Westphalia’s strong defense and industrial base drive uptake for virtual-reality training and plant-simulation clusters. Frankfurt’s banks maintain on-premises GPU grids for risk modeling to satisfy BaFin data-residency rules, while Berlin’s startup scene leans on Deutsche Telekom’s Industrial AI Cloud for reinforcement-learning workloads.

The Munich facility keeps sensitive data inside German jurisdiction, allowing SAP’s Business Technology Platform users to build AI solutions without crossing national borders. Northern states such as Schleswig-Holstein and Lower Saxony leverage GPUs for wind-farm digital twins, optimizing turbine placement and scheduling predictive maintenance. Grid operators TenneT and 50Hertz employ double-precision GPU clusters to stress-test networks under high renewable penetration.

Federal incentives, including the Research Allowance Act and InvestBooster, cover up to 25% of eligible GPU spend, propelling adoption among medium-sized manufacturers. Operators planning new datacenters weigh EU Directive 2023/1791, which caps power-usage effectiveness at 1.3 by 2030; liquid cooling and GPU frequency limits are increasingly standard as a result.

Competitive Landscape

NVIDIA retains dominance, controlling about 94% of desktop add-in-boards and 80% of datacenter accelerators; however, AMD and Intel nibble at price-sensitive tiers. Blackwell GPUs supply 22 TB per second of HBM4 bandwidth, securing anchor sales in sovereign clouds. AMD counters with MI455X chiplets and 432 GB of memory, appealing to enterprises wary of vendor lock-in. Intel’s Arc Pro B70 offers low entry prices but is still building a reputation for workstation driver stability.

Qualcomm’s Snapdragon Ride Elite gains traction in cost-sensitive ADAS designs as Volkswagen and ZF Friedrichshafen diversify supplier risk. Emerging players such as Tenstorrent market open-architecture accelerators that bypass CUDA dependencies, while Huawei positions Ascend GPUs for European customers seeking alternatives free from U.S. export controls. Competitive focus now centers on interconnect bandwidth, memory capacity, and transparent model-audit tooling demanded by the EU AI Act.

Germany GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Qualcomm Technologies, Inc.

Arm Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- Apr 2026: Qualcomm and Volkswagen Group deepened collaboration to integrate Snapdragon Cockpit and Ride Elite platforms across upcoming vehicle lines, naming ZF Friedrichshafen as a key Tier-1 supplier.

- Mar 2026: Intel released the Arc Pro B70 GPU targeting professional desktops, featuring 16 GB of GDDR6 and the Battlemage architecture, at a launch price of EUR 599 (USD 651).

- Feb 2026: Deutsche Telekom commenced operations at its Industrial AI Cloud in Munich, outfitted with 10,000 NVIDIA Blackwell GPUs delivering 0.5 exaFLOPS.

- Jan 2026: NVIDIA introduced the Vera Rubin NVL72 rack featuring 72 Rubin GPUs and 36 Vera CPUs, each GPU providing 50 PFLOPS of inference.

Germany GPU Market Report Scope

The Germany GPU Market Report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs) and Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) |

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacentre Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| By Integration Type | Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) | |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacentre Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices |

Key Questions Answered in the Report

How large will German demand for GPUs become by 2031?

The Germany GPU market is forecast to reach USD 14.32 billion by 2031, expanding at a 16.58% CAGR between 2026 and 2031.

Which GPU segment grows fastest inside German borders?

Servers and datacenter accelerators grow at a 16.87% CAGR through 2031 as enterprises shift AI workloads to sovereign on-premises clusters.

What share do discrete GPUs hold today?

Discrete GPUs captured 65.73% of the Germany GPU market share in 2025 and remain the dominant choice for training and inference clusters.

Why are German automakers investing in GPUs?

Mercedes-Benz, BMW, and Volkswagen use GPU-driven simulation farms to accelerate validation of Level-3 autonomous-driving stacks and reduce on-road testing time.

Page last updated on: