North America GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

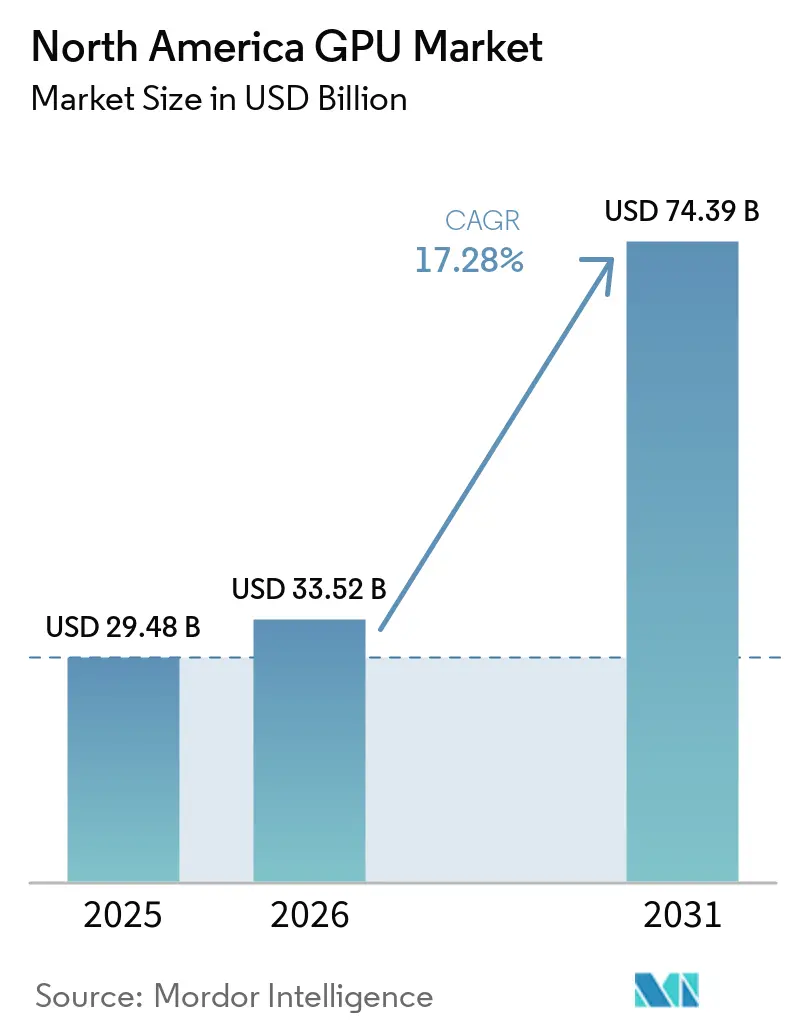

| Base Year Market Size (2025) | USD 29.48 Billion |

| Market Size (2026) | USD 33.52 Billion |

| Market Size (2031) | USD 74.39 Billion |

| Growth Rate (2026 - 2031) | 17.28% CAGR |

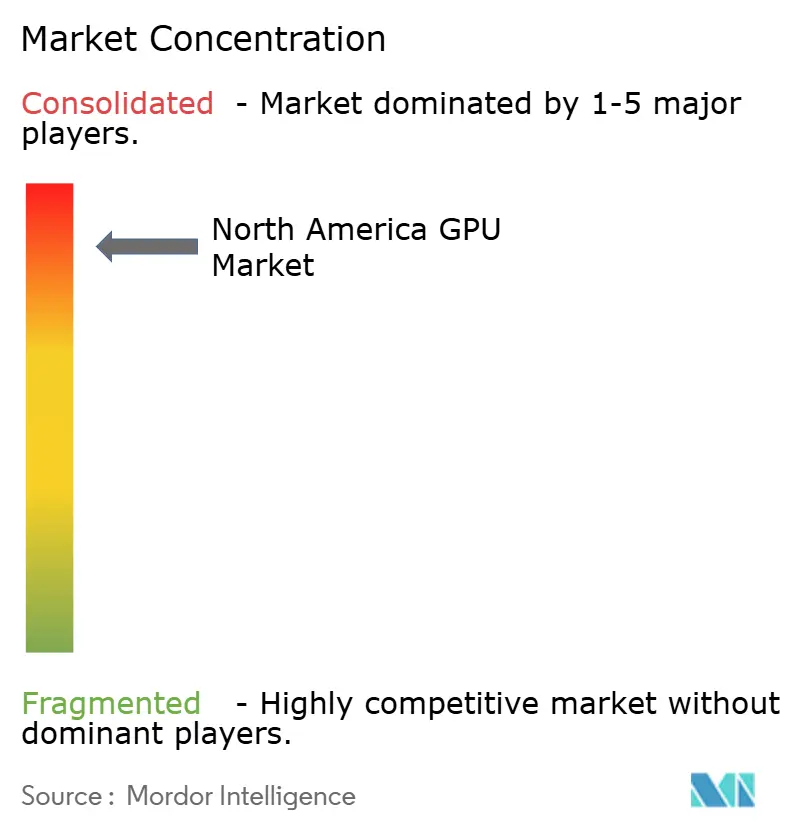

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America GPU Market Analysis by Mordor Intelligence

The North America GPU market size is projected to expand from USD 29.48 billion in 2025 and USD 33.52 billion in 2026 to reach USD 74.39 billion by 2031, registering a CAGR of 17.28% between 2026-2031. Robust datacenter capital-expenditure plans, an accelerated refresh of enterprise PCs that embed neural processing units, and growing graphics requirements in automotive advanced driver-assistance systems are powering revenue momentum. Procurement patterns are consolidating around fewer hyperscale buyers, which concentrates shipment risk even as average selling prices rise. Meanwhile, on-device inference in Copilot+ certified PCs is redirecting part of the addressable consumer-graphics budget toward low-power accelerators built into central processors. These forces combine to create a landscape in which the North America GPU market experiences simultaneous scale-up in datacenters and scale-out at the edge.

Key Report Takeaways

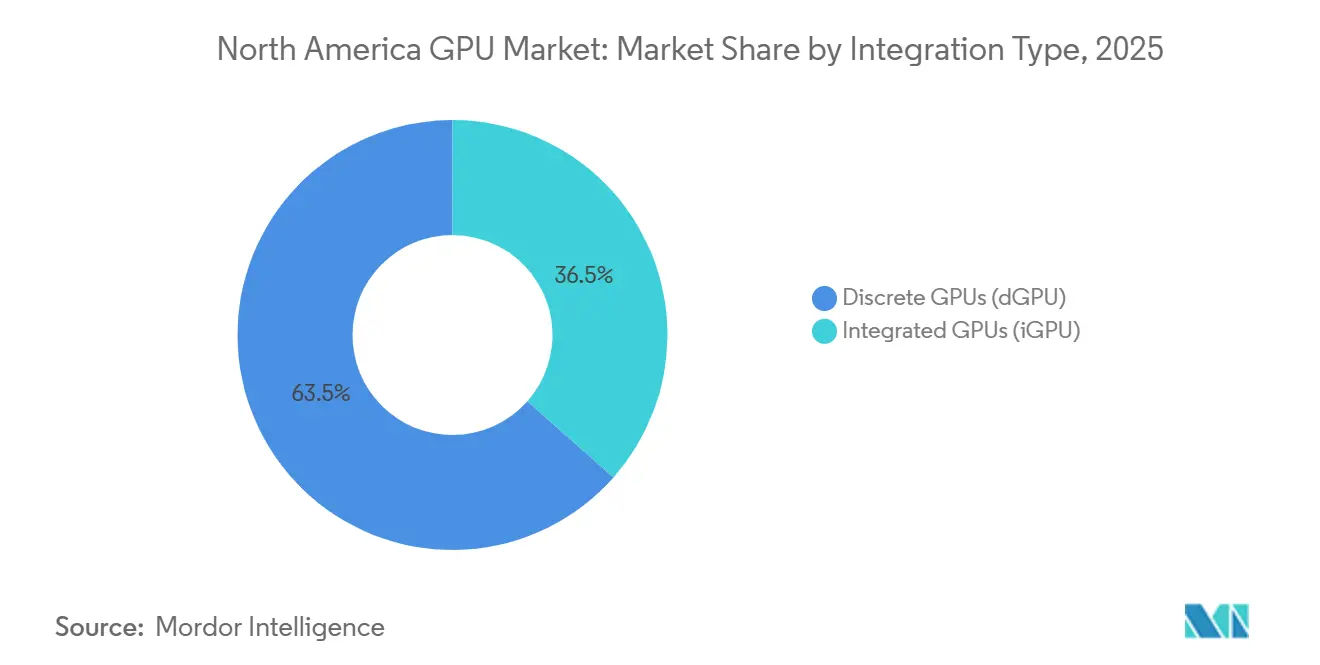

- By integration type, discrete GPUs led the North America GPU market with 63.48% market share in 2025 and are advancing at a 17.77% CAGR through 2031.

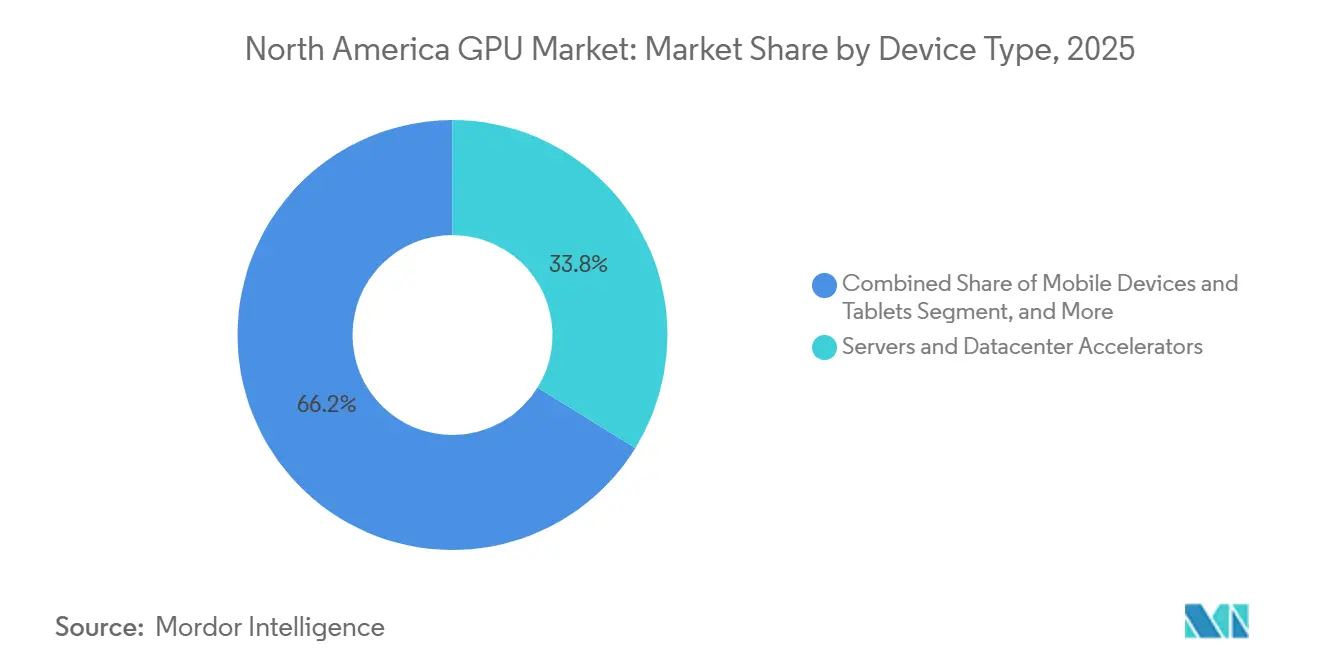

- By device type, servers and datacenter accelerators commanded 33.81% of the North America GPU market in 2025 and are expanding at a 17.94% CAGR through 2031.

- By geography, the United States contributed 44.73% of regional revenue in 2025, while Mexico is projected to grow at a 17.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surging AI-driven datacenter GPU procurement | +5.2% | United States, spillover to Canadian AI hubs | Short term (≤ 2 years) |

| Proliferation of high-fidelity cloud gaming services | +2.1% | United States and Canada, with limited Mexico | Medium term (2-4 years) |

| Rapid adoption of generative-AI PCs in enterprise fleets | +3.8% | United States and Canada enterprise segments | Short term (≤ 2 years) |

| Expanding automotive ADAS compute requirements | +1.9% | United States and Mexican manufacturing corridors | Long term (≥ 4 years) |

| Advancements in chiplet and 3D-stacked GPU architectures | +2.4% | North America design centers, global fabs | Medium term (2-4 years) |

| Government incentives for domestic semiconductor capacity | +1.8% | United States CHIPS Act facilities, with selective Canada and Mexico spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging AI-Driven Datacenter GPU Procurement

Hyperscalers are compressing multi-year hardware refresh cycles to 18 months as AI model sizes grow. xAI commissioned the Colossus complex in Memphis, comprising 555,000 NVIDIA H100 GPUs that draw 150 MW and require USD 12,000 in liquid-cooling loops per rack. IREN’s order for 150,000 GPUs in Texas leverages USD 0.018 kWh power, cutting operating costs by 70% relative to coastal sites.[1]Financial Times Reporters, “Energy arbitrage drives Texas datacenter boom,” ft.com Amazon split a one-million-unit purchase between NVIDIA H200 and AMD MI325X parts to dilute supply risk and extract volume discounts. Such megablock deals raise average selling prices but make quarterly shipments volatile, as a single project delay can wipe out double-digit demand. This concentration gives the North America GPU market rapid topline growth alongside elevated forecasting risk.

Proliferation of High-Fidelity Cloud Gaming Services

Cloud platforms are shifting from shared virtualization to dedicated accelerators that sustain 4K 120 fps streams. NVIDIA’s GeForce NOW Ultimate tier, built on RTX 5080 nodes, hit 15-minute queues within eight weeks, prompting a USD 400 million Oregon expansion. Microsoft’s Xbox Cloud Gaming added 2.8 million regional subscribers in 2025, yet it needs 40% more GPUs per user than its rival, raising concerns about unit economics. Because each subscriber consumes disproportionate capital, operators restrain scaling until utilization models stabilize. Even so, enthusiast pricing at USD 24.99 per month keeps revenue per GPU attractive enough to sustain steady North America GPU market demand.

Rapid Adoption of Generative-AI PCs in Enterprise Fleets

Microsoft’s Copilot+ badge mandates 40 TOPS NPUs, pushing Intel’s Lunar Lake and AMD’s Strix Point to integrate larger AI blocks. Dell shipped 3.2 million Copilot+ units in the region during 2025 for regulated industries that require on-device inference. AMD’s Strix Point reached 18% share of enterprise notebook designs by Q4 2025, while Qualcomm’s Snapdragon X Elite gained 9% in sub-USD 1,000 tiers. Enterprises that skipped refreshes during 2020-2023 shortages are now buying three-year inventories, front-loading demand into 2026-2027. This surge helps the North America GPU market but may create an air pocket in 2028 if replacement cycles lengthen.

Expanding Automotive ADAS Compute Requirements

Vehicle makers are over-provisioning graphics compute to prepare for Level 2+ autonomy. NVIDIA’s Drive Thor delivers 2,000 TOPS and consolidates multiple ECUs, cutting cabling but lifting board thermal loads beyond 800 W.[2]NVIDIA Blog Editors, “GeForce NOW Ultimate tier launches,” nvidia.com Tesla’s Hardware 4 triples GPU throughput over prior systems, yet current Autopilot features use less than 30% of capacity. Qualcomm’s Snapdragon Ride secured wins at General Motors and Stellantis for 2026 launches with 700 TOPS budgets. If promised software upgrades slip, automakers could trim GPU content, but near-term designs lock in silicon orders, lifting regional unit volumes.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply-chain fragility for advanced HBM and GDDR7 memory | -2.6% | North American datacenter and high-end gaming GPU supply | Short term (≤ 2 years) |

| Escalating thermal-design power limits in high-end GPUs | -1.4% | United States and Canada datacenter and workstation deployments | Medium term (2-4 years) |

| Intensifying US-China tech export controls | -1.9% | United States compliance costs and design constraints | Medium term (2-4 years) |

| Volatility in esports and consumer upgrade cycles | -1.2% | The United States and Canada gaming GPU segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Fragility for Advanced HBM and GDDR7 Memory

High-bandwidth memory is now the bottleneck, not lithography. SK Hynix’s HBM4 yields stay below 60%, allowing only 12,000 wafer starts a month, roughly half of NVIDIA’s demand for H200 accelerators. Samsung’s contamination event in Q3 2025 delayed HBM3E qualification for AMD MI325X by three months. Micron's share is too small to ease shortages. GDDR7 debuted at USD 18 per GB, squeezing add-in-board margins. With three suppliers controlling the HBM market, any hiccup reverberates through the North America GPU market and curtails shipment growth.

Escalating Thermal-Design Power Limits in High-End GPUs

Next-generation accelerators exceed the cooling envelopes of most facilities. NVIDIA’s GB200 NVL72 rack draws 120 kW and needs 40 L min-¹ liquid-to-chip loops, a retrofit that costs USD 800,000 per MW of IT load. AMD’s forthcoming MI400 has a 750 W TDP and requires dual 12VHPWR connectors, which add USD 300 at the board level. Professional graphics cards like the RTX 6000 Ada already exceed stock-air-cooler specs, forcing integrators to void warranties with aftermarket solutions. Every 100 W increase adds USD 50-80 in power-delivery and cooling expense, eroding the cost advantage that once favored GPU acceleration over CPU-only servers in the North America GPU market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Integration Type: Discrete GPUs Anchor Datacenter Expansion

Discrete accelerators captured 63.48% of the North America GPU market share in 2025 and are projected to expand at a 17.77% CAGR through 2031, underscoring their central role in hyperscale build-outs. NVIDIA’s Blackwell GB200 NVL72 rack package bundles 72 GPUs and 36 Grace CPUs to deliver 1.4 exaflops of FP4 compute, a configuration that compresses cluster footprints while boosting average selling prices. AMD’s MI325X, shipping since December 2025 with 192 GB of HBM3E, targets memory-bound inference tasks in which bandwidth above 5 TB s-¹ becomes decisive.[3]AMD Investor Relations, “MI325X technical briefing,” amd.com Intel’s Ponte Vecchio seized 22% of U.S. national-lab high-performance-computing deployments during 2025, proving that an open-standard interconnect can coexist with proprietary CUDA clusters.[4]Intel Investor Relations, “Ponte Vecchio deployment update,” intel.com

Beyond data centers, discrete GPUs power gaming and professional-visualization refreshes. Intel’s Battlemage B580, priced at USD 249, captured a share of sub-USD 300 desktop units within 90 days, demonstrating price elasticity among cost-sensitive gamers. Rumors place NVIDIA’s RTX 5090 at 24,576 CUDA cores and 28 GB of GDDR7, a 40% compute leap over the RTX 4090, widening the gap with integrated solutions.[5]Tom’s Hardware Team, “Intel Battlemage B580 review,” tomshardware.com Apple’s M-series iGPUs now offer hardware ray tracing, but thermal constraints limit their performance to workloads below 75 W, leaving high-end rendering and simulation to discrete GPUs. As a result, the discrete tier remains the revenue locomotive for the North America GPU market, even as integrated NPUs shoulder light generative AI tasks.

By Device Application: Servers and Datacenter Accelerators Lead Revenue

Servers and datacenter accelerators generated 33.81% of the North America GPU market size in 2025 and are advancing at a 17.94% CAGR, the fastest clip among all device categories. A single H100 rack can generate USD 250,000 in annual inference revenue, dwarfing the USD 1,200 three-year contribution of a premium gaming card and validating hyperscalers’ capital intensity. Microsoft Azure deployed 180,000 NVIDIA Rubin R100 GPUs in early 2026 to boost transformer throughput per watt, while Amazon’s EC2 P6 instances integrate AMD MI325X parts to diversify away from CUDA lock-in. Google Cloud’s TPU v6 claimed regional AI training cycles in 2025, illustrating buyers' willingness to bypass graphics silicon when proprietary accelerators achieve cost parity.

Client form factors still make notable contributions. Dell’s Precision 7780 workstation, offered with RTX 6000 Ada boards, lifted the segment in 2025 compared with the year before. Sony’s PlayStation 5 Pro introduced RDNA 3-based machine-learning upscaling, but console GPU expansion was limited as replacement cycles stretched. Automotive and edge devices post growth off small bases as ADAS and IoT inference proliferate, giving vendors optionality beyond hyperscale contracts. Together, these varied demand vectors ensure that the North America GPU market remains broad-based, even as data centers dominate absolute dollars.

Geography Analysis

The United States dominated the North America GPU market in 2025, with 44.73% revenue share, driven by hyperscale data center clusters that absorbed an estimated 2.1 million accelerators. California, Texas, and Virginia combined for over half of shipments as operators chased inexpensive renewable power and dense fiber backbones. Federal incentives accelerated local fabrication: Intel secured USD 8.5 billion under the CHIPS and Science Act for Arizona and Ohio fabs, while TSMC and Samsung collectively garnered USD 12 billion for advanced-node capacity, indirectly bolstering GPU assembly ecosystems. Updated export rules in October 2025 imposed licensing on H200 and MI325X shipments to China, redirecting output toward domestic customers and allied nations.

Mexico, although accounting for a smaller slice today, is the fastest-growing component of the North America GPU market with a 17.68% CAGR to 2031. Foxconn’s USD 500 million Guadalajara facility, operational since Q4 2025, assembles 12,000 GB200 racks annually, translating to 864,000 GPUs and generating regional supply without incurring import tariffs. Component suppliers are as follows: ATP Electronics opened a USD 35 million Monterrey test-and-packaging line tailored for automotive-grade GPU modules. Datacenter demand inside Mexico remains under 8,000 units, yet cloud providers are scouting Querétaro and Monterrey for greenfield builds that capitalize on renewable power corridors.

Government-backed AI research clusters anchor Canada. Scale AI disbursed USD 200 million to subsidize accelerator access for startups, distributing 22,000 A100 and H100 hours during the year. Cohere raised USD 500 million to expand a 15,000-GPU Toronto cluster, the largest privately held training array in the nation. The Vector Institute diversified its hardware stack by incorporating AMD MI300X boards, reflecting a broader trend to avoid single-vendor dependence. These initiatives position Canada as a test bed for next-generation GPU software ecosystems, though absolute unit volumes remain modest compared with U.S. hyperscalers.

Competitive Landscape

Datacenter accelerators are highly concentrated: NVIDIA controls a significant portion of the segment, a position built on the network externalities of its CUDA software stack, which now counts more than 4 million developers. Migration cost shields this lead, yet adjacent battlegrounds tell a different story. Intel’s Battlemage series seized unit share in the budget desktop tier within one quarter, proving that performance-per-dollar can dent incumbency when software lock-in is weaker. AMD adopted an open-ecosystem stance by partnering with Nutanix and investing USD 150 million to integrate MI325X accelerators into hyperconverged infrastructure that appeals to enterprises wary of proprietary interconnects.

Foundry dynamics are also reshaping alliances. NVIDIA signed a contract with Intel Foundry Services to fabricate custom x86 CPUs for Grace-Blackwell platforms, reflecting NVIDIA’s decision to insource CPU competencies while leveraging Intel’s process roadmap. Emerging challengers target specialized corners: Tenstorrent’s RISC-V Wormhole chip samples at 5 W TDP for edge inference, undercutting Jetson Orin on list price. Mythic’s analog compute-in-memory architecture, validated by the U.S. Department of Defense for vision tasks, claims an energy-efficiency advantage, though commercial scalability remains untested.

Add-in-board partners are consolidating to capture value through vertical integration. ASUS increased its North America discrete-GPU unit share by designing proprietary cooling solutions that support 450 W cards without liquid cooling. Export-control carve-outs have created a niche for downgraded “China-compliant” GPUs, an opportunity that NVIDIA addresses via H20 variants while AMD and Intel focus on unrestricted SKUs. The strategic picture thus bifurcates: datacenter compute will likely consolidate around a trio of vendors with the scale to fund bleeding-edge nodes, whereas gaming, workstation, and edge sectors fragment as buyers weigh ecosystem openness, thermals, and cost of ownership.

North America GPU Industry Leaders

NVIDIA Corporation

Arm Holdings plc

Qualcomm Technologies Inc.

Intel Corporation

Advanced Micro Devices Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NVIDIA and Intel formalized a USD 5 billion partnership for Intel Foundry Services to manufacture custom x86 CPUs that interface with NVLink-C2C on Grace-Blackwell server platforms, targeting 2027 production.

- February 2026: AMD introduced Radeon RX 9070 XT with RDNA 4 architecture, 60 compute units, and 16 GB GDDR7 at USD 649, shipping 180,000 units in 30 days.

- January 2026: Microsoft Azure deployed 180,000 NVIDIA Rubin R100 GPUs across United States regions to support OpenAI and GitHub Copilot enterprise tiers.

- December 2025: Mythic closed a USD 125 million Series D to commercialize analog compute-in-memory GPUs after U.S. Department of Defense validation.

North America GPU Market Report Scope

The North America GPU Market Report is Segmented by Integration Type (Integrated GPUs and Discrete GPUs), Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive and ADAS, and Other Embedded and Edge Devices), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) |

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| United States |

| Canada |

| Mexico |

| By Integration Type | Integrated GPUs (iGPU) |

| Discrete GPUs (dGPU) | |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America GPU market expected to become by 2031?

The North America GPU market is forecast to reach USD 74.39 billion by 2031, reflecting a 17.28% CAGR over 2026-2031.

Which product category currently holds the highest revenue share?

Discrete accelerators held 63.48% of regional revenue in 2025, thanks to rapid hyperscale datacenter adoption.

What is the fastest-growing geographic market through 2031?

Mexico is projected to expand at a 17.68% CAGR, driven by nearshoring of assembly and new datacenter builds.

Why are high-bandwidth-memory shortages a risk factor?

SK Hynix, Samsung, and Micron control 94% of HBM capacity, so any yield disruption constrains GPU shipments and dampens revenue momentum.

How dominant is NVIDIA in datacenter accelerators?

NVIDIA commands about 88% of North American datacenter GPU revenue because its CUDA ecosystem imposes high switching costs on developers.

What cooling challenges face next-generation GPUs?

Racks like NVIDIA’s GB200 NVL72 draw up to 120 kW, requiring liquid-to-chip cooling retrofits that cost roughly USD 800,000 per MW of IT load.

Page last updated on: