United Kingdom Discrete GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

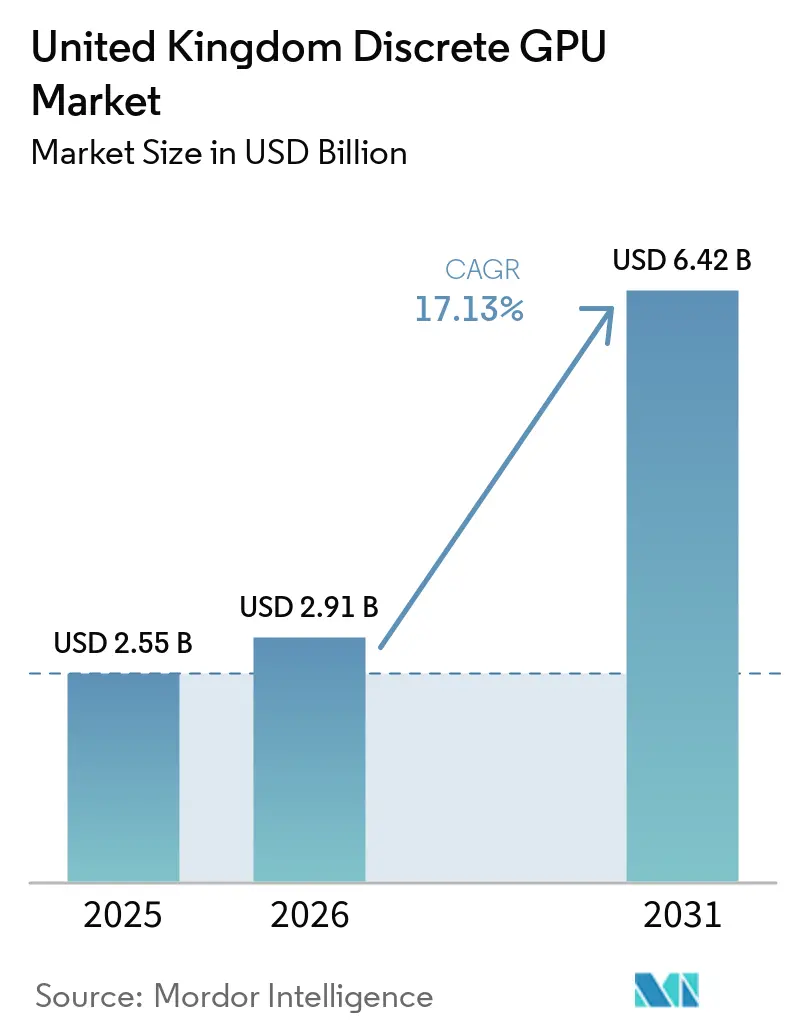

| Base Year Market Size (2025) | USD 2.55 Billion |

| Market Size (2026) | USD 2.91 Billion |

| Market Size (2031) | USD 6.42 Billion |

| Growth Rate (2026 - 2031) | 17.13% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Discrete GPU Market Analysis by Mordor Intelligence

The United Kingdom discrete GPU market size is expected to grow from USD 2.55 billion in 2025 to USD 2.91 billion in 2026 and is forecast to reach USD 6.42 billion by 2031 at a 17.13% CAGR over 2026-2031. A surge in sovereign artificial intelligence programs, public supercomputing rollouts, and edge-inference workloads is reshaping demand curves. Private and public capital commitments exceeding GBP 4 billion (USD 4.9 billion) for new GPU clusters between 2024 and 2026 guarantee long-run visibility for semiconductor suppliers. Datacenter operators secure priority allocations of NVIDIA’s Blackwell Ultra and H200 accelerators, while venture capital-backed start-ups concentrate orders in London and Cambridge hubs. GDDR devices remain the incumbent volume driver, yet high-bandwidth memory designs win a growing share of enterprise builds as model sizes escalate. Elevated power tariffs and multi-year grid connection queues temper on-premise expansions, nudging smaller buyers toward cloud-hosted GPU capacity.

Key Report Takeaways

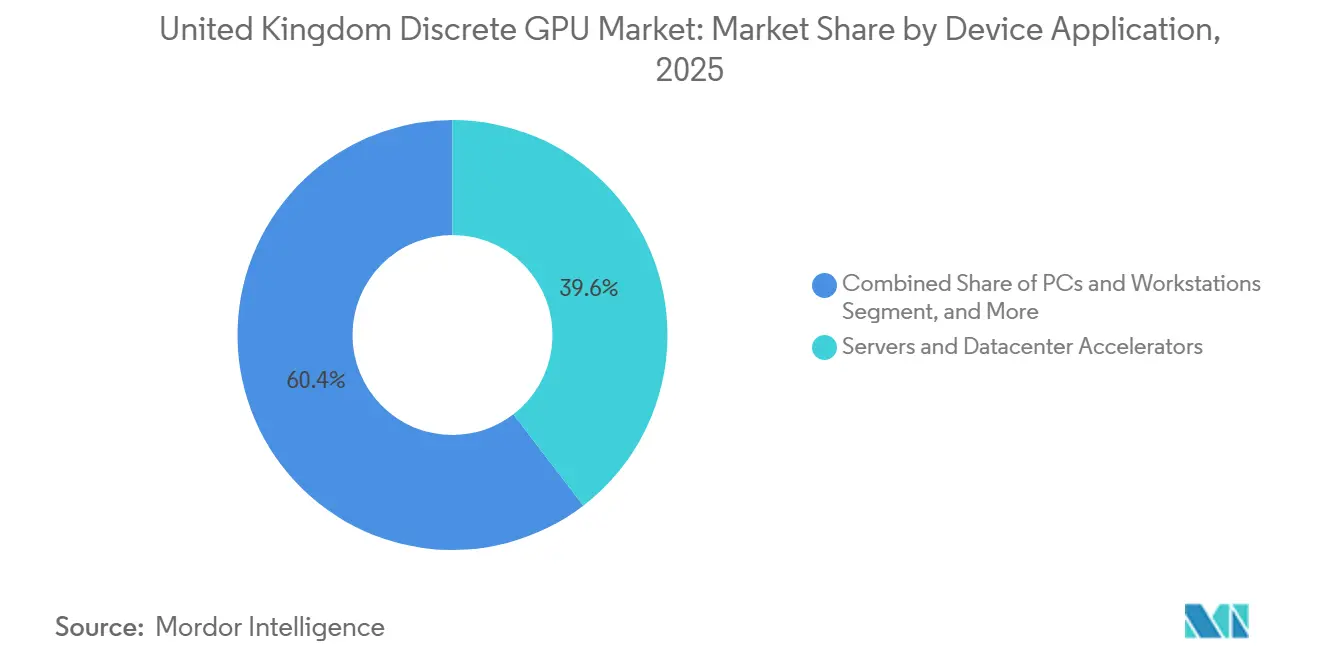

- By device application, servers and datacenter accelerators led with a 39.59% revenue share in 2025, while expanding at a 17.55% CAGR through 2031.

- By memory type, GDDR products commanded 70.39% of the United Kingdom discrete GPU market share in 2025, whereas HBM devices recorded the fastest projected growth at 17.97% CAGR to 2031.

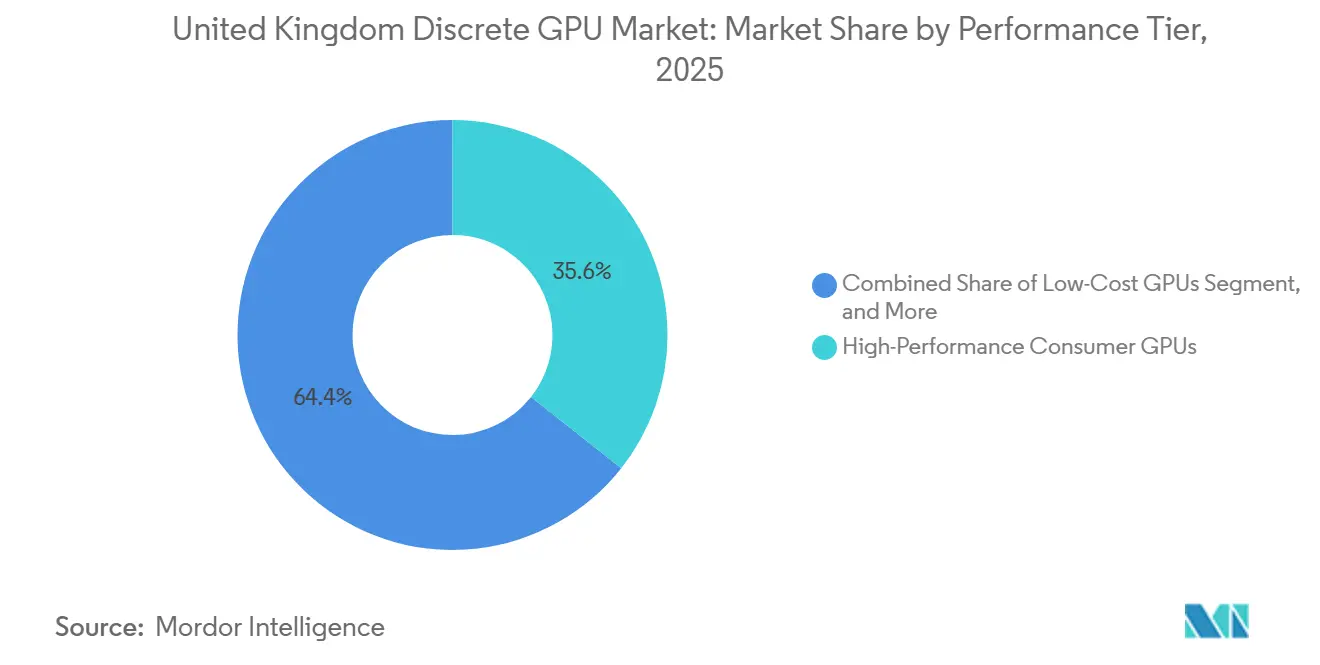

- By performance tier, high-performance consumer GPUs accounted for 35.63% of the United Kingdom discrete GPU market in 2025, yet Data Center and AI Accelerator GPUs are projected to grow at a 17.91% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Discrete GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Explosive Growth in UK AI Start-Ups Demanding High-End GPUs | +4.2% | National, concentrated in London and Cambridge | Medium term (2–4 years) |

| Government Supercomputing Investments | +3.8% | National hubs in Bristol, Edinburgh, Oxford | Long term (≥ 4 years) |

| Rising Cloud Gaming Adoption Across the UK | +2.5% | National, urban-centric | Short term (≤ 2 years) |

| Automotive OEMs Shift to Centralized ADAS Compute Platforms | +2.1% | UK and broader European automotive corridors | Medium term (2–4 years) |

| Consumer Demand for 4K, 8K and VR-Ready Gaming Experiences | +1.9% | National, affluent demographics | Short term (≤ 2 years) |

| Expansion of Edge AI Inference in NHS Diagnostics | +1.6% | National pilot sites in Leeds, London, Bristol | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth in UK AI Start-Ups Demanding High-End GPUs

Venture funding peaked in 2025 as Nscale closed GBP 1.6 billion (USD 2.0 billion) to deploy GPU-dense clusters that serve foundation-model developers.[1]Natasha Lomas, “Nscale Raises $2B for UK GPU Cloud,” techcrunch.com Capital concentration in London and Cambridge triggers localized rack-space shortages, pushing datacenter utilization above the industry norm of 60%. Fractile AI’s low-precision arithmetic reduces power draw by up to 90%, widening the addressable base for cost-sensitive training workloads. NVIDIA pledged to deliver more than 120,000 H200 and Blackwell Ultra units to UK customers by late 2026, locking in supply despite global shortages.

Government Supercomputing Investments

The GBP 2 billion Compute Roadmap scales national AI Research Resource twenty-fold by 2027, anchored by Isambard-AI and the Edinburgh International Data Facility.[2]UK Government, “National Quantum Strategy and Compute Roadmap,” gov.uk Isambard-AI has already delivered one million GPU hours to Nightingale AI’s federated learning pilot across 14 NHS. Regulatory guidance from the AI Safety Institute requires transparent model risk assessments, rewarding hardware vendors that offer turnkey compliance tooling.

Rising Cloud Gaming Adoption Across the UK

Cloud gaming reached penetration with NVIDIA GeForce NOW claiming a subscriber share by streaming RTX 4080 and RTX 4090 instances from regional points of presence. Retail sellouts of RTX 5090 systems in January 2026 indicate that enthusiasts continue to value local rendering. This shift highlights the coexistence of traditional hardware preferences alongside the growing adoption of streaming platforms, creating parallel demand streams in the gaming market.

Automotive OEMs Shift to Centralized ADAS Compute Platforms

Jaguar Land Rover’s December 2025 alliance with NVIDIA will embed DRIVE Orin GPUs in 2027 Range Rover models, satisfying Level 3 autonomy rules under the Automated Vehicles Act 2024. ARM’s Immortalis-G925 IP recorded 41% greater peak performance and 44% lower power in MediaTek’s Dimensity Auto chipset, enabling real-time 4K sensor fusion. Lengthy automotive design cycles, however, delay silicon volume until 2029, muting short-run revenue.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply Chain Exposure to Taiwan Foundries | -2.3% | National, European spillover | Medium term (2–4 years) |

| High Electricity Costs Limiting On-Prem GPU Farms | -1.9% | National, acute in Southeast England | Short term (≤ 2 years) |

| Skills Shortage in Parallel-Programming Talent Pool | -1.4% | National tech hubs | Long term (≥ 4 years) |

| Import Tariff Uncertainty Post Brexit Trade Deals | -1.1% | National, cross-border components | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Exposure to Taiwan Foundries

UK customers source a significant portion of their advanced GPUs from Taiwan Semiconductor Manufacturing Company, a reliance that officials deem "very exposed" to geopolitical upheavals. Due to Brexit's rules of origin thresholds, partially assembled boards face hurdles to achieving duty-free status, resulting in customs delays and straining inventory buffers. Even with plans for diversification through EU fabs, relief isn't expected until 2028.

High Electricity Costs Limiting On-Prem GPU Farms

In the UK, industrial power prices averaged GBP 0.25 per kWh in 2025. This increase significantly impacted operational costs, pushing annual energy expenses for a 1,000-GPU H200 cluster above GBP 2 million. In Southeast England, National Grid connection queues range from 3 to 8 years, forcing operators to either burn diesel or reduce capacity during peak times.[3]National Grid ESO, “Quarterly Connections Progress Report,” nationalgrideso.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Application: Datacenter Dominance Reshapes Allocation

Servers and Datacenter Accelerators controlled 39.59% of the United Kingdom discrete GPU market in 2025, eclipsing all other categories as CoreWeave earmarked GBP 1 billion (USD 1.27 billion) for London facilities powered by H200 silicon. The United Kingdom's discrete GPU market for server-class boards is projected to grow at a 17.55% CAGR to 2031, driven by AI sovereignty mandates. PCs and Workstations, once the shipment leader, slipped to about 28% share as enterprises stream desktop environments from GPU-enabled virtual machines. Gaming Consoles and Handhelds contributed to the total revenue. Meanwhile, Automotive and ADAS devices secured a share, bolstered by Jaguar Land Rover's adoption of the DRIVE Orin silicon.

Datacenter build-outs funnel demand toward power-hungry, HBM-equipped cards, tilting the mix toward premium average selling prices. NHS diagnostic pilots, however, prefer mid-tier boards that balance watt draw with sufficient tensor throughput, signaling pockets of diversified adoption. As London rack space tightens, hyperscalers are positioning new clusters in Scotland and the North to exploit shorter wait times for grid connections, redistributing regional card allocations without denting national volume growth.

By Memory Type: HBM Gains Despite GDDR Incumbency

GDDR-based boards accounted for 70.39% of the United Kingdom's discrete GPU market share in 2025 because gamers and creative professionals prioritize cost-per-frame metrics. Ampere-era RTX 5090 units featured 32 GB of GDDR7 and retailed for GBP 1,499 to GBP 6,999 (USD 1,900-8,900).[4]Overclockers UK, “RTX 5090 Launch Day Pricing,” overclockers.co.uk HBM designs held a 29.61% share, yet grew the fastest at a 17.97% CAGR, as SK Hynix’s HBM4 backlog runs through 2026.

HBM’s 4.8 TB s⁻¹ bandwidth on NVIDIA’s H200 slashes inference latency for billion-parameter models, enticing venture-funded start-ups to pay a 3-4x memory premium. Intel’s Arc B580, priced at GBP 227 (USD 288) with GDDR6, competes on value and anchors the mainstream tier. The divergent cost profiles lock GDDR into consumer and budget-enterprise pools while HBM marches deeper into scientific computing and sovereign AI facilities.

By Performance Tier: AI Accelerators Outpace Consumer Segments

High-Performance Consumer GPUs, priced between USD 400 and USD 1,200, held 35.63% share in 2025 as RTX 4070 Ti and RX 7900 XT headlined 4K gaming builds. Data Center and AI Accelerator boards above USD 1,200 are advancing at a 17.91% CAGR, driving total market value. Mainstream boards (USD 100-400) account for a significant share of shipments, with Intel’s Arc B570 at GBP 199 (USD 252) as the main defender. Low-Cost cards under USD 100 shrink to a single-digit share as integrated graphics cannibalize entry-level demand.

Cloud gaming’s user penetration trims mid-tier hardware replacement cycles, but enthusiast sell-outs of RTX 5090-rigs underscore persistent appetite for flagship silicon. Enterprises, universities, and public agencies gravitate toward accelerator-grade SKUs capable of training multi-billion-parameter language models, reinforcing bifurcated growth paths in the United Kingdom's discrete GPU market.

Geography Analysis

London and the Southeast absorbed shipments in 2025 owing to dense venture funding, hyperscale campuses, and latency demands from financial services. Sites near the M25 corridor enjoy abundant dark fiber yet face the nation’s longest grid-connection queues, prompting developers to contract temporary diesel capacity. Scotland accounted for shipments after the GBP 750 million (USD 883.09 million) Edinburgh facility began operating in 2026, offering lower electricity tariffs and surplus wind generation to power new GPU clusters. The Midlands and Northern England received shipments on the strength of the University of Sheffield and Leeds Teaching Hospitals' AI rollouts, while Wales and Northern Ireland shared the remaining shipments.

Transmission bottlenecks redirect some expansion plans northward, where connection wait times fall below 4 years, but latency-sensitive finance workloads still gravitate to London. Brexit customs friction has raised buffer inventories near Dover and Folkestone, adding costs but not derailing supply. Regional renewable mandates requiring 50% zero-carbon power by 2027 incentivize colocated battery storage and demand-response contracts, inflating opex yet aligning with national net-zero goals.

Competitive Landscape

NVIDIA retained a significant position in the datacenter and consumer segments in 2025, supported by a September 2025 pledge to invest GBP 2 billion (USD 2.5 billion) and ship Blackwell Ultra GPUs into the United Kingdom discrete GPU market. AMD gained traction in consumer sales by pricing the RX 9070 XT at GBP 569-779 (USD 720-990) and offering parity ray-tracing performance. Intel focused on value with Arc B580 and B570 mainstream cards but faced challenges in datacenter silicon deliveries.

Domestic challengers expand: Graphcore, which was acquired by SoftBank in 2024, increased its headcount to 750 and launched the wafer-stacked Bow IPU at 350 TFLOPS, targeting AI training clusters. Imagination Technologies raised USD 100 million to ship E-Series GPU IP, delivering AI uplift for licensees in mobile and edge form factors. Fractile AI’s ultra-low-precision coprocessors promise significant power cuts, a disruptive lever in a high-tariff energy market. Compliance with AI Safety Institute documentation rules favors incumbents able to bundle mature software and audit suites, creating barriers for newer entrants.

White-space opportunities span industrial edge inference, quantum-GPU hybrids, and automotive zonal controllers. Supply security, power efficiency, and open-source software maturity differentiate vendor roadmaps as sovereign compute strategies elevate national interest in onshore innovation pipelines.

United Kingdom Discrete GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Qualcomm Technologies Inc.

ARM Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: NVIDIA detailed deployment of 120,000 Blackwell Ultra GPUs across Nscale, CoreWeave, and Microsoft Azure United Kingdom regions under its GBP 2 billion (USD 2.70 billion) commitment.

- January 2026: SK Hynix confirmed HBM4 allocations sold out through 2026, with Samsung and Micron accelerating competing nodes.

- January 2026: AMD introduced RX 9070 XT in the United Kingdom, retailing at GBP 569-779 (USD 720-990) and challenging RTX 4070 Ti volumes.

- December 2025: Jaguar Land Rover partnered with NVIDIA to integrate DRIVE Orin GPUs in 2027 Range Rover models for Level 3 motorway autonomy.

United Kingdom Discrete GPU Market Report Scope

The United Kingdom Discrete GPU Market Report is Segmented by Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, and Other Embedded and Edge Devices), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), and Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs). The Market Forecasts are Provided in Terms of Value (USD).

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| GDDR-Based GPUs |

| HBM-Based GPUs |

| Low-Cost GPUs (Less than USD 100) |

| Mainstream GPUs (USD 100-USD 400) |

| High-Performance Consumer GPUs (USD 400-USD 1,200) |

| Data Center / AI Accelerator GPUs (Greater than USD 1,200) |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices | |

| By Memory Type | GDDR-Based GPUs |

| HBM-Based GPUs | |

| By Performance Tier | Low-Cost GPUs (Less than USD 100) |

| Mainstream GPUs (USD 100-USD 400) | |

| High-Performance Consumer GPUs (USD 400-USD 1,200) | |

| Data Center / AI Accelerator GPUs (Greater than USD 1,200) |

Key Questions Answered in the Report

How large will the United Kingdom's discrete GPU demand be by 2031?

It is projected to reach USD 6.42 billion on a 17.13% CAGR over 2026-2031.

Which application currently drives the majority of shipments?

Servers and Datacenter Accelerators led with a 39.59% revenue share in 2025 and continued to expand fastest through 2031.

Is HBM memory overtaking GDDR in the United Kingdom?

HBM held a 29.61% share in 2025 but, with a 17.97% CAGR, is the fastest-growing memory class for AI and scientific workloads.

What regional factors limit on-premises GPU farms?

High electricity tariffs and grid connection delays of three to eight years, especially in Southeast England, raise operating costs and slow expansion.

Will cloud gaming hurt consumer GPU sales?

Casual gamers shift toward streaming, yet enthusiast demand for high-performance cards such as RTX 5090 remains strong, sustaining the premium consumer segment.

Page last updated on: