Europe GPU Cooling Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

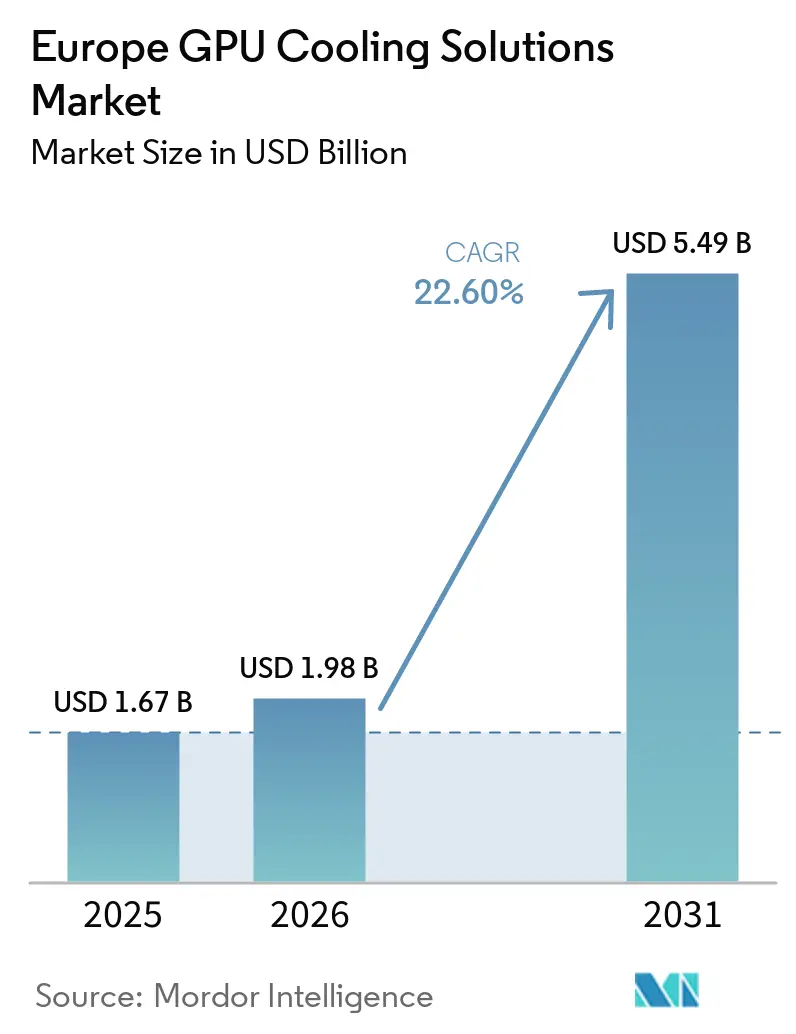

| Base Year Market Size (2025) | USD 1.67 Billion |

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 5.49 Billion |

| Growth Rate (2026 - 2031) | 22.60% CAGR |

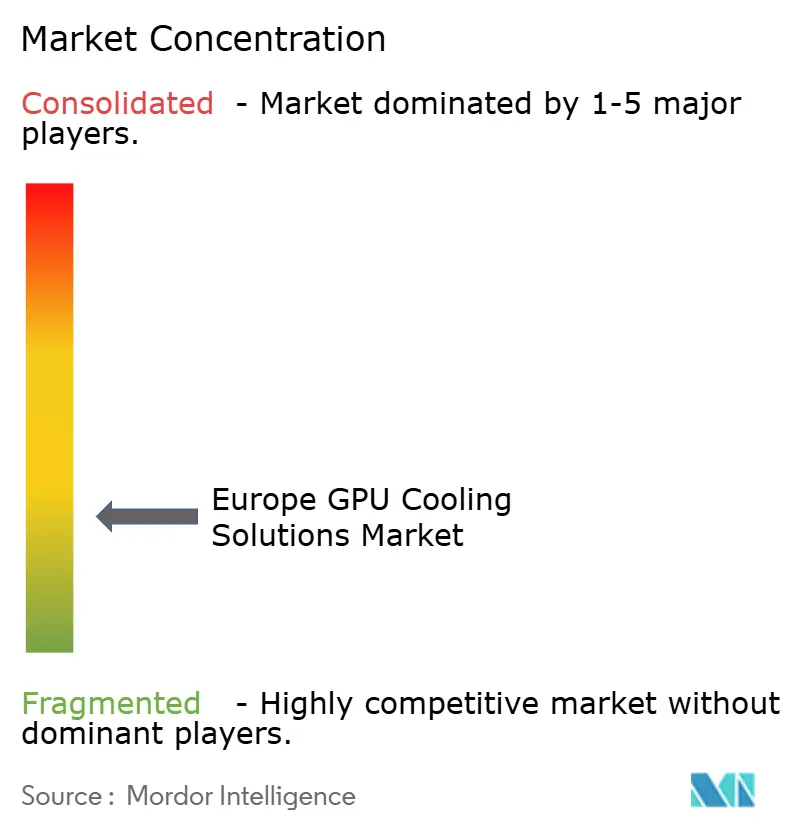

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe GPU Cooling Solutions Market Analysis by Mordor Intelligence

The Europe GPU Cooling Solutions market size is projected to be USD 1.67 billion in 2025, USD 1.98 billion in 2026, and reach USD 5.49 billion by 2031, growing at a CAGR of 22.6% from 2026 to 2031. The market is entering 2026 with strong momentum because new rack-scale AI systems are being deployed in liquid-cooled formats that move thermal design to the center of infrastructure planning rather than leaving it as a later facility choice. Mandatory EU reporting on data center energy performance is also making PUE, water use, and heat reuse more visible, which strengthens the case for more efficient cooling architectures across new and upgraded sites. Sovereign AI programs are adding to that demand, with projects such as Deutsche Telekom’s Industrial AI Cloud in Munich showing how large GPU deployments now translate directly into demand for advanced thermal systems. The Europe GPU Cooling Solutions market is also being supported by a large installed base of air-cooled facilities that now represent a clear retrofit pipeline for liquid and hybrid vendors. Growth is still tempered by the cost of brownfield conversion and by coolant procurement uncertainty linked to the PFAS review process in Europe.

Key Report Takeaways

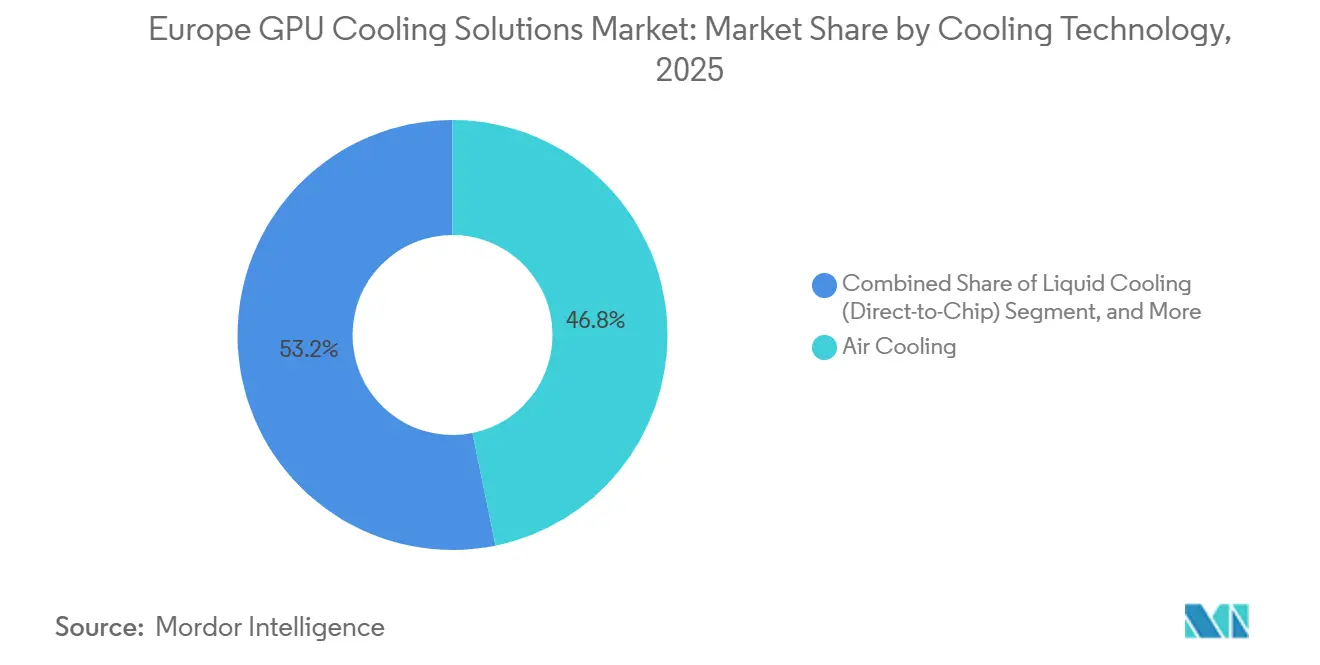

- By cooling technology, air cooling held 46.8% share of Europe GPU cooling solutions market in 2025, while immersion cooling is projected to expand at the 24.12% pace through 2031.

- By cooling level, server and rack-level cooling accounted for 59% share in 2025 and also remained the fastest-growing cooling level segment.

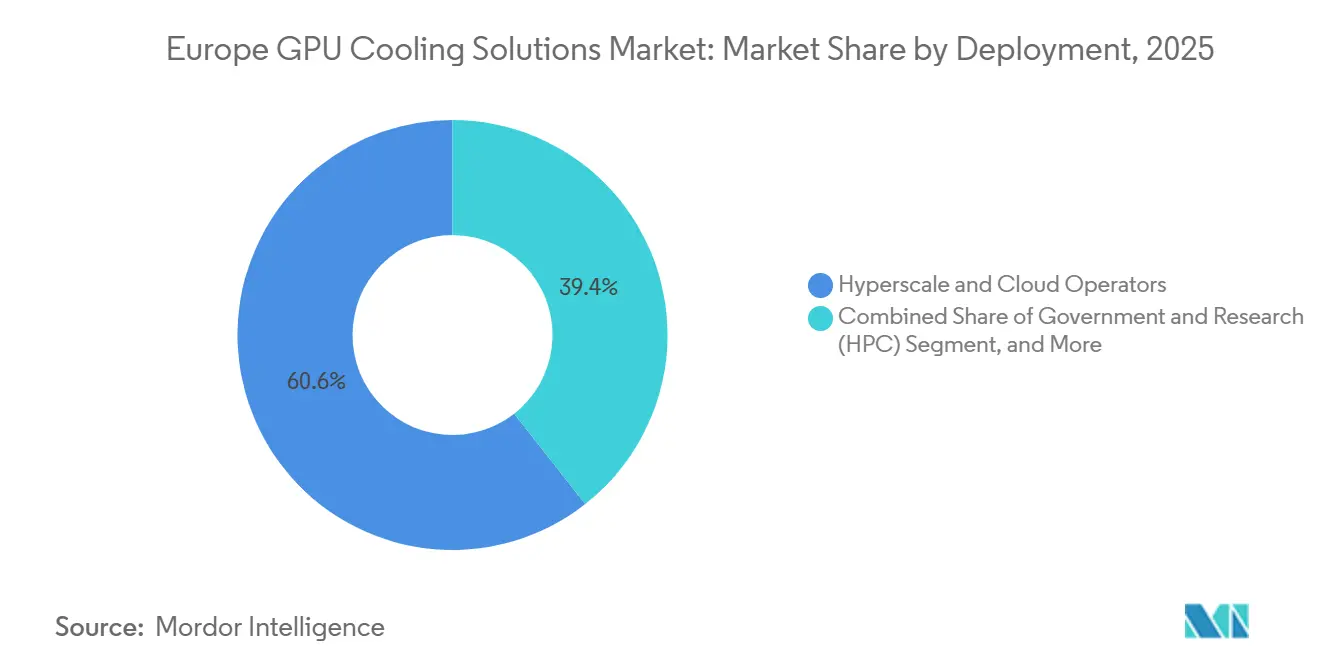

- By deployment, hyperscale and cloud held 60.6% share of Europe GPU cooling solutions market in 2025, while enterprise deployments are projected to post the 25.14% CAGR through 2031.

- By GPU power density, the 300W-700W band led with 48.8% share in 2025, while above-700 W systems are expected to expand at the 26.12% over 2026-2031.

- By country, Germany held 27.3% share of Europe GPU cooling solutions market in 2025, while France was the fastest-growing country market at 25.59% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe GPU Cooling Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated AI Adoption Driving GPU Shipments | +6.0% | Global, with concentrated impact in Germany, UK, France, and the Netherlands | Short term (≤ 2 years) |

| Stricter European Union Data-Center Efficiency Directives | +3.2% | EU-wide, early gains in Germany, Netherlands, and France | Medium term (2-4 years) |

| Mainstream Liquid Cooling Adoption in Hyperscale Facilities | +2.8% | FLAP-D markets, with spillover to the Nordics | Short term (≤ 2 years) |

| Rising Edge-AI Deployments in 5G Micro-Data Centers | +1.9% | Western and Northern Europe telco infrastructure | Medium term (2-4 years) |

| Surging Venture Capital Into Immersion-Cooling Start-ups | +1.3% | UK, Spain, Netherlands | Short term (≤ 2 years) |

| Heat-Reuse Contracts With District Heating Networks | +0.9% | Nordics, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated AI Adoption Driving GPU Shipments

The Europe GPU Cooling Solutions market is moving from single-GPU procurement toward rack-scale AI systems, and that shift is changing cooling from a support feature into a core design choice. HPE’s next-generation AI factory portfolio with NVIDIA includes liquid-cooled rack-scale systems built for very large models, which shows how advanced GPU deployments now depend on integrated thermal architecture from launch.[1]Source: Hewlett Packard Enterprise, “HPE Unveils Next-Generation AI Factory And Supercomputing Advancements With NVIDIA,” HPE Newsroom, hpe.com Deutsche Telekom’s Industrial AI Cloud in Munich, built around 10,000 Blackwell GPUs, shows how sovereign AI programs in Europe are already translating into immediate demand for high-density cooling infrastructure.[2]Source: Deutsche Telekom, “Germany’s First AI Factory For Industry Officially Goes Into Operation In Munich,” Deutsche Telekom, telekom.com As these systems scale, OEM-qualified cold plates, manifolds, and coolant delivery units become standard parts of the hardware stack in the Europe GPU Cooling Solutions market. That standardization should lower adoption friction for enterprise buyers over time because component qualification, servicing, and system familiarity improve as hyperscale deployments expand.

Stricter European Union Data-Center Efficiency Directives

The Europe GPU Cooling Solutions market is also being shaped by stricter disclosure rules around data center energy performance. The Energy Efficiency Directive requires data centers above 500 kW installed IT power to make energy performance data publicly available, and Delegated Regulation (EU) 2024/1364 sets the reporting framework for indicators such as PUE, water usage effectiveness, and heat reuse.[3]Source: European Commission, “Energy Performance Data For Data Centres,” European Commission, energy.ec.europa.eu Once operators must report these metrics every year, inefficient cooling choices become more visible to regulators, customers, and investors. That creates a stronger commercial case for liquid and hybrid systems, especially in facilities that can also monetize higher-grade waste heat. In practical terms, the Europe GPU Cooling Solutions market benefits because cooling upgrades now support both operational performance and compliance needs within the same investment cycle.

Mainstream Liquid Cooling Adoption in Hyperscale Facilities

The Europe GPU Cooling Solutions market is benefiting from the fact that liquid cooling is becoming the default path for new hyperscale AI deployments. HPE now offers rack-scale AI systems in liquid-cooled configurations, which confirms that high-density GPU clusters are being designed around thermal systems from the first planning stage rather than being retrofitted later. Trane completed its acquisition of LiquidStack in February 2026, combining direct-to-chip and immersion capabilities with a wider thermal management platform for data center customers. In the Europe GPU Cooling Solutions market, that kind of platform integration reduces procurement complexity because operators can source larger parts of the cooling stack from fewer vendors. It also reinforces the advantage of greenfield sites that can be planned from day 1 for high-density GPU loads, rather than adapted later at higher cost.

Rising Edge-AI Deployments in 5G Micro-Data Centers

The Europe GPU Cooling Solutions market is starting to expand beyond large campuses as edge AI workloads move into telecom and industrial environments. Submer and ZEDEDA announced a partnership in March 2026 to deliver modular liquid-cooled edge AI infrastructure for locations where conventional data center footprints are impractical. The EU-funded CAPE project has also demonstrated an edge micro data center platform that supports GPUs above 300W TDP with direct-to-chip liquid cooling and closed-loop heat pipes in constrained environments.[4]Source: CAPE Project, “CAPE Update #5, EMDC Edge Micro Data Center,” CAPE Project, cape-project.eu Asperitas presented its DFCX1 immersion cooling system for far-edge and on-site compute environments during Cisco Live Amsterdam 2026, which shows that product development is already moving into this use case. These deployments matter because they are pushing suppliers to build smaller, more modular cooling systems that can later serve enterprise facilities across the Europe GPU Cooling Solutions market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front CAPEX for Facility Retrofits | -2.8% | EU-wide, strongest in Germany, UK, and France | Medium term (2-4 years) |

| Supply-Chain Risk for Fluorocarbon-Free Coolants | -1.7% | Global, concentrated in EU immersion deployments | Medium term (2-4 years) |

| Limited Skilled Labor for Coolant-System Maintenance | -1.3% | EU-wide, particularly acute in Central and Eastern Europe | Long term (≥ 4 years) |

| Uncertain Standards for Direct-to-Chip Manifolds | -0.8% | Global, most relevant to enterprise operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front CAPEX for Facility Retrofits

The Europe GPU Cooling Solutions market still faces a clear cost barrier when operators try to convert older air-cooled halls into liquid-ready facilities. Brownfield upgrades often require structural reinforcement, new piping routes, revised fire suppression integration, and changes to aisle design, which makes the transition more complex than a simple equipment swap. That cost profile is especially difficult for enterprise buyers that do not have large internal thermal engineering teams or long capital approval windows. As a result, many operators are using rear-door heat exchangers and hybrid configurations as intermediate steps before moving to full liquid systems. This slows the pace of conversion in the Europe GPU Cooling Solutions market, even when the long-term operating economics of liquid cooling are more favorable.

Supply-Chain Risk for Fluorocarbon-Free Coolants

The Europe GPU Cooling Solutions market also faces uncertainty around immersion fluids and long-term coolant qualification. 3M’s withdrawal from Novec fluorocarbon production in Q4 2025 removed a major supply source and forced operators to assess replacement fluids on tighter timelines. At the same time, the European Chemicals Agency is advancing its PFAS restriction process, with a final opinion expected by the end of 2026. That uncertainty is hardest on two-phase immersion systems because fluid continuity, hardware compatibility, and service planning all depend on long-term chemistry stability. Single-phase and water-based approaches face less regulatory risk, which means the issue may shift competitive share inside the Europe GPU Cooling Solutions market more than it reduces demand overall.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooling Technology: Air Cooling Holds Ground as Immersion Scales Up

Air cooling held 46.8% of the European GPU Cooling Solutions market share in 2025, supported by the large installed base of enterprise and colocation facilities built before GPU power density moved materially higher, while immersion cooling is projected to expand at the 24.12% pace through 2031. In the European GPU Cooling Solutions market, the installed base still matters because it preserves near-term demand for air systems while creating a predictable retrofit pipeline for liquid and hybrid suppliers. New greenfield AI deployments are moving in a different direction, with rack-scale GPU systems now being designed around liquid cooling from launch. Hybrid layouts are becoming the practical bridge between those two realities because they let operators protect older halls while preparing new GPU pods for higher thermal loads.

Immersion cooling is the fastest-growing technology segment in the Europe GPU Cooling Solutions market because it can manage rack densities that stretch beyond the comfortable operating range of standard air layouts. That shift is being supported by product-level innovation such as Alphacool’s 2026 ES RTX 6000 Pro server-edition GPU cooler, which was engineered for dense rack environments. Submer also introduced an immersion-cooled AI inference reference design with 2CRSi and Eneos at OCP EMEA 2026, which points to a broader commercial ecosystem for immersion-based deployments. PFAS-related fluid uncertainty is still creating procurement caution for two-phase systems, but for now it is strengthening the position of single-phase solutions rather than stopping the Europe GPU Cooling Solutions market from moving toward liquid methods.

By Cooling Level: Rack-Scale Deployments Anchor Both Volume and Growth

Server and rack-level cooling accounted for 59% share of the Europe GPU Cooling Solutions market size in 2025 and remained the main buying unit for new AI infrastructure. In the Europe GPU Cooling Solutions market, that dominance reflects a rack-first design model in which servers, manifolds, and coolant distribution units are qualified as one operating package. HPE’s liquid-cooled NVL72 platforms show how thermal management is now embedded inside rack-scale procurement rather than added later as a facility accessory H. This keeps spending concentrated at the rack level even when the underlying parts are supplied by multiple vendors.

Component-level cooling still plays a meaningful role in the Europe GPU Cooling Solutions industry, especially in workstations, departmental HPC clusters, and custom GPU builds. Alphacool expanded that product space with new Core series GPU water coolers for NVIDIA RTX 5090 and 5080 cards in 2025, which shows that specialized component demand remains active. Over time, component-level demand is likely to narrow toward lower-power and specialized environments, while server and rack-level systems keep capturing the larger contracts in the Europe GPU Cooling Solutions market. That leaves the segment with a clear premium tier at rack scale and a more specialized tier at the component level.

By Deployment: Hyperscale Dominance Steady as Enterprise Accelerates

Hyperscale and cloud deployments held 60.6% of the Europe GPU Cooling Solutions market size in 2025, which made this the largest deployment segment by a wide margin, while enterprise deployments are projected to post the 25.14% CAGR through 2031. The Europe GPU Cooling Solutions market has been shaped by large campus designs where power, cooling, and rack density are planned together from the start. Deutsche Telekom’s Industrial AI Cloud in Munich, built around Blackwell GPUs, shows how sovereign AI programs can create hyperscale-class cooling demand within Europe very quickly. These buyers also move earlier on liquid systems because high-density AI clusters have limited thermal headroom under conventional air designs. As a result, hyperscale projects continue to set the technical standards that later spread across the Europe GPU Cooling Solutions market.

Enterprise is the fastest-growing deployment category in the Europe GPU Cooling Solutions market as more organizations bring inference, digital twin, and on-premise model workloads closer to their own facilities. That shift favors modular systems that can be installed faster than a full new campus build and operated with smaller in-house teams. Government and research demand remains smaller in revenue terms, but facilities such as the LUMI AI Factory in Finland show how public-sector procurement is linking advanced compute with heat reuse goals. Edge remains the smallest segment by revenue, yet it is becoming more relevant as telecom and industrial sites add GPU inference in space-constrained settings. This mix means the Europe GPU Cooling Solutions market is expanding from a hyperscale-led base into a broader demand structure without losing its dependence on large anchor contracts.

By GPU Power Density: 300W-700W Base Gives Way to Above-700W Frontier

The 300W-700W band accounted for 48.8% of the Europe GPU Cooling Solutions market in 2025, making it the largest power-density segment in the installed base, while above-700 W systems are expected to expand at the 26.12% over 2026-2031. In the Europe GPU Cooling Solutions market, that band reflects the broad commercial use of GPU generations that remain central to AI training and inference workloads. This installed base should continue to generate service, replacement, and incremental upgrade demand even as new systems move into higher thermal design power ranges. The above-700W tier is the fastest-growing segment because next-wave rack platforms are raising cooling requirements to a materially higher level.

HPE’s GB300 NVL72 platform is one of the clearest signs that above-700W GPU cooling demand is becoming commercial rather than experimental. At the other end, the below-300W segment still serves workstations, smaller HPC environments, and the enthusiast channel, where optimized air cooling remains viable. Noctua’s Computex 2025 showcase of high-end air-cooled graphics solutions illustrates why this lower-power tier still supports product innovation. Through 2031, the Europe GPU Cooling Solutions market is likely to separate more clearly between premium liquid systems for frontier AI compute and optimized air or hybrid options for the broader installed base.

Geography Analysis

Germany accounted for 27.3% of the Europe GPU Cooling Solutions market share in 2025, which made it the largest country market in the region. The Europe GPU Cooling Solutions market in Germany benefits from both a mature hyperscale base and a fresh wave of sovereign AI investment. Deutsche Telekom’s Munich Industrial AI Cloud is a clear example, with around 10,000 NVIDIA Blackwell GPUs pushing cooling design toward rack-scale liquid systems. Schwarz Digits also broke ground on a 200 MW campus in Lübbenau that is designed to host up to 100,000 GPUs, which reinforces Germany’s role in high-density infrastructure build-out. The UK and Italy remain important secondary demand pockets because both markets continue to benefit as European capacity expands beyond the most constrained hubs. France is the fastest-growing country in the Europe GPU Cooling Solutions market, supported by strong alignment between AI investment, power availability, and sovereign compute priorities. Large planned AI campus developments since 2025 have increased the country’s long-range need for rack, server, and facility-level cooling systems. France also benefits from a low-carbon electricity mix, which improves the case for dense liquid-cooled deployments over less efficient air-based layouts. That combination makes the country attractive for operators that want both scale and tighter energy performance. For vendors, France is likely to be one of the most important expansion markets in the Europe GPU Cooling Solutions market through the forecast period.

The Nordic region, within Rest of Europe, is an influential cluster for advanced cooling methods because heat reuse is moving from concept to operating practice. Fortum has started heat production at Microsoft data center sites in Finland, and the LUMI AI Factory in Kajaani will feed excess heat into the local district heating network through a 30 MW heat pump plant being delivered by Caverion. Denmark’s atNorth heat reuse agreement and the Netherlands-based scale-up activity of Asperitas show how the Europe GPU Cooling Solutions market is also being shaped by specialist ecosystems outside the largest country markets. These clusters matter because they help commercialize immersion, waste heat recovery, and other designs that can later scale across the Europe GPU Cooling Solutions market.

Competitive Landscape

The Europe GPU Cooling Solutions market remains moderately fragmented because no single vendor leads across air, direct-to-chip, immersion, and hybrid categories. Large infrastructure suppliers are still expanding their reach by tying cooling more closely to power, racks, and long-term service contracts. Trane completed its acquisition of LiquidStack in February 2026, which added direct-to-chip and immersion capabilities to its broader thermal management portfolio. Vertiv followed with an agreement to acquire ThermoKey in March 2026, expanding its European heat-rejection and heat-exchange footprint for AI data centers. These moves are pushing the European GPU Cooling Solutions market toward broader solution bundles, even though technology specialization still matters.

Platform integration is becoming just as important as corporate scale in the Europe GPU Cooling Solutions market. HPE’s rack-scale liquid-cooled AI systems show how server vendors are embedding cooling into the platform rather than treating it as a separate add-on. That approach favors suppliers that can qualify cold plates, manifolds, pumps, and control systems as one operating package for dense GPU clusters. It also raises the entry barrier for smaller firms that lack deep OEM validation or field integration support. Even so, specialist vendors keep their position when they can offer better efficiency, faster deployment, or a tighter application fit.

European specialists such as Submer and Asperitas continue to compete by focusing on immersion, modular edge systems, and integrated support services. Asperitas widened its commercial reach in February 2026 through its agreement with UNICOM Engineering, which simplified procurement for immersion-ready systems. Submer also expanded its UK coverage in March 2026 through new distribution partnerships while continuing to push reference designs for AI inference deployments. This keeps the Europe GPU Cooling Solutions market open to innovation even as larger vendors build scale through acquisition and platform control.

Europe GPU Cooling Solutions Industry Leaders

Asetek A/S

CoolIT Systems Inc.

Noctua GmbH

EKWB d.o.o

Arctic GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hewlett Packard Enterprise unveiled the NVIDIA Vera Rubin NVL72 by HPE rack-scale system, a liquid-cooled, 72-GPU AI platform engineered for models exceeding 1 trillion parameters, targeted at neo-clouds and sovereign AI deployments. Commercial availability is planned for December 2026.

- March 2026: Vertiv entered into an agreement to acquire ThermoKey S.p.A., a leading EMEA provider of heat rejection and heat-exchange technologies, to expand its thermal management portfolio and manufacturing capabilities specifically for AI factories and high-density data centers in Europe.

- February 2026: Trane Technologies completed its acquisition of LiquidStack, pairing LiquidStack's direct-to-chip and immersion cooling capabilities with Trane's end-to-end thermal management systems and global footprint to serve high-density AI-scale workloads.

Europe GPU Cooling Solutions Market Report Scope

GPU Cooling Solutions are integrated systems and technologies designed to dissipate heat generated by graphics processing units (GPUs) during operation, thereby maintaining optimal thermal performance, reliability, and longevity. These solutions encompass a range of methods, including air cooling, liquid cooling (direct-to-chip), immersion cooling, and hybrid approaches, and are implemented at various levels, such as component-level or server/rack-level architectures. They are critical in high-performance computing environments, data centers, hyperscale cloud platforms, and AI/ML workloads, where GPU power densities often exceed 300W, requiring efficient thermal management to prevent throttling and hardware failure and to ensure sustained computational throughput.

The Europe GPU Cooling Solutions Market Report is Segmented by Cooling Technology (Air Cooling, Liquid Cooling (Direct-to-Chip), Immersion Cooling, and Hybrid Cooling), Cooling Level (Component-Level Cooling and Server / Rack-Level Cooling), Deployment (Hyperscale / Cloud, Enterprise, Government and Research (HPC), and Edge), GPU Power Density (Below 300W, 300W - 700W, and Above 700W), and Country (Germany, UK, France, Italy, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Air Cooling |

| Liquid Cooling (Direct-to-Chip) |

| Immersion Cooling |

| Hybrid Cooling |

| Component-Level Cooling |

| Server / Rack-Level Cooling |

| Hyperscale / Cloud |

| Enterprise |

| Government and Research (HPC) |

| Edge |

| Below 300W |

| 300W - 700W |

| Above 700W |

| Germany |

| United Kingdom |

| France |

| Italy |

| Rest of Europe |

| By Cooling Technology | Air Cooling |

| Liquid Cooling (Direct-to-Chip) | |

| Immersion Cooling | |

| Hybrid Cooling | |

| By Cooling Level | Component-Level Cooling |

| Server / Rack-Level Cooling | |

| By Deployment | Hyperscale / Cloud |

| Enterprise | |

| Government and Research (HPC) | |

| Edge | |

| By GPU Power Density | Below 300W |

| 300W - 700W | |

| Above 700W | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

What is the size of the Europe GPU cooling solutions market in 2026 and 2031?

The Europe GPU Cooling Solutions market is valued at USD 1.98 billion in 2026 and is forecast to reach USD 5.49 billion by 2031, growing at a 22.6% CAGR.

Which cooling technology currently leads in Europe?

Air cooling led in 2025 with 46.8% share, largely because of the region’s installed base of legacy enterprise and colocation facilities.

Which part of the market is growing the fastest?

Immersion cooling is the fastest-growing cooling technology, enterprise is the fastest-growing deployment segment, and the above-700W GPU tier is the fastest-growing power-density band.

Why are liquid systems gaining adoption so quickly?

New rack-scale AI systems are being launched in liquid-cooled formats, and EU energy reporting rules are making efficiency, water use, and heat reuse more important in purchase decisions.

Which country is leading regional demand?

Germany held 27.3% share in 2025, supported by a strong hyperscale base and large sovereign AI deployments such as Deutsche Telekom’s Munich project.

What are the main risks for suppliers and operators?

The main risks are the high upfront cost of retrofitting older air-cooled sites and the uncertainty around immersion fluid supply and PFAS-related regulation.

Page last updated on: