Employee Helpdesk And Ticketing Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.10 Billion |

| Market Size (2031) | USD 11.67 Billion |

| Growth Rate (2026 - 2031) | 10.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Employee Helpdesk And Ticketing Software Market Analysis by Mordor Intelligence

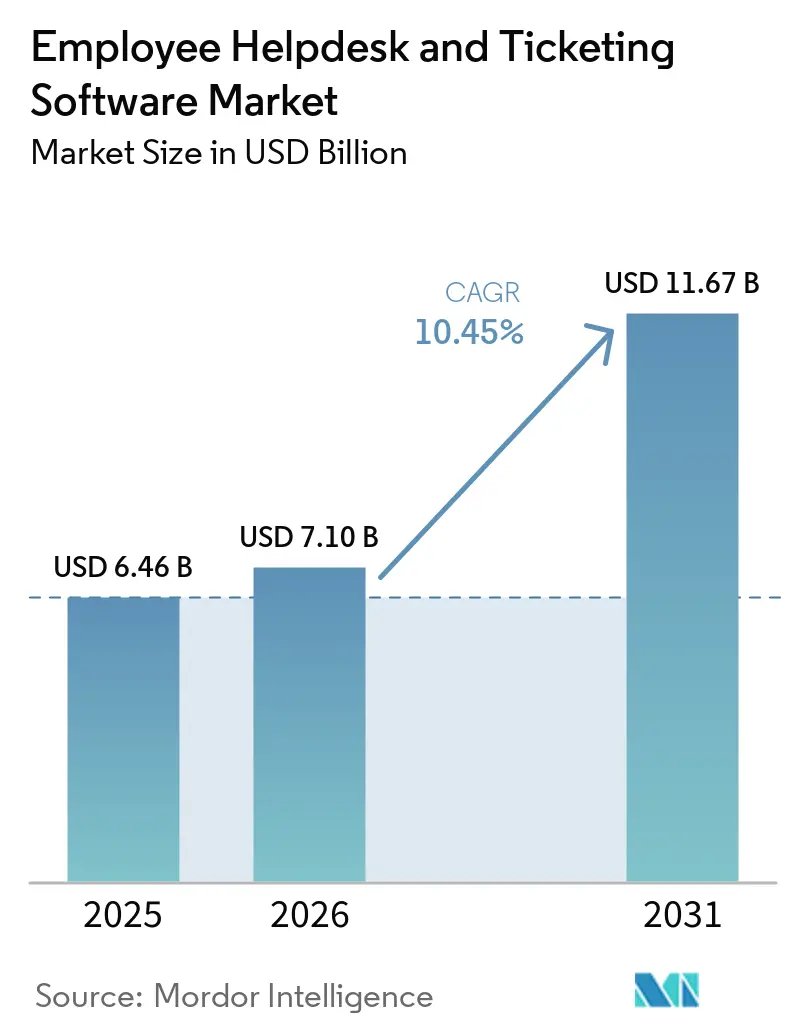

The Employee helpdesk and ticketing software market size is projected to be USD 6.46 billion in 2025, USD 7.10 billion in 2026, and reach USD 11.67 billion by 2031, growing at a CAGR of 10.45% from 2026 to 2031. The employee helpdesk and ticketing software market is expanding as enterprises move from basic ticket handling toward platforms that can automate resolution, document actions, and support cross-functional service delivery. Procurement criteria are also changing, because internal support systems are now being assessed as control environments for audit readiness, workflow governance, and policy enforcement rather than as standalone productivity tools. The employee helpdesk and ticketing software market is also seeing a sharper split between buyers who can adopt cloud-first models and those who still need hybrid designs to meet data residency and internal control requirements. Competitive advantage is shifting toward vendors that can combine AI, workflow design, low-code extensibility, and verifiable logging inside a single operating layer. This leaves the employee helpdesk and ticketing software market in a selective growth phase, where vendors with embedded governance, faster deployment models, and deeper service management are positioned to capture a larger share of the next buying cycle.

Key Report Takeaways

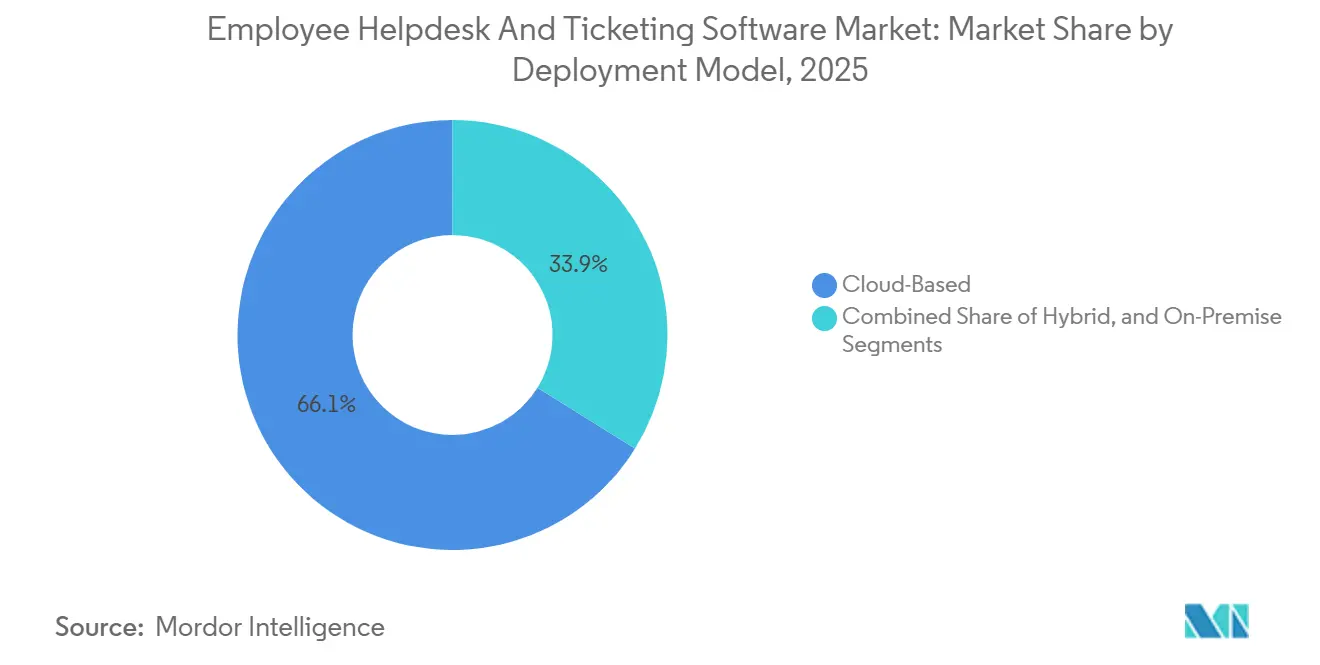

- By deployment model, cloud-based deployment accounted for 66.14% of the employee helpdesk and ticketing software market share in 2025, while hybrid deployment is projected to expand at a 11.73% CAGR through 2031.

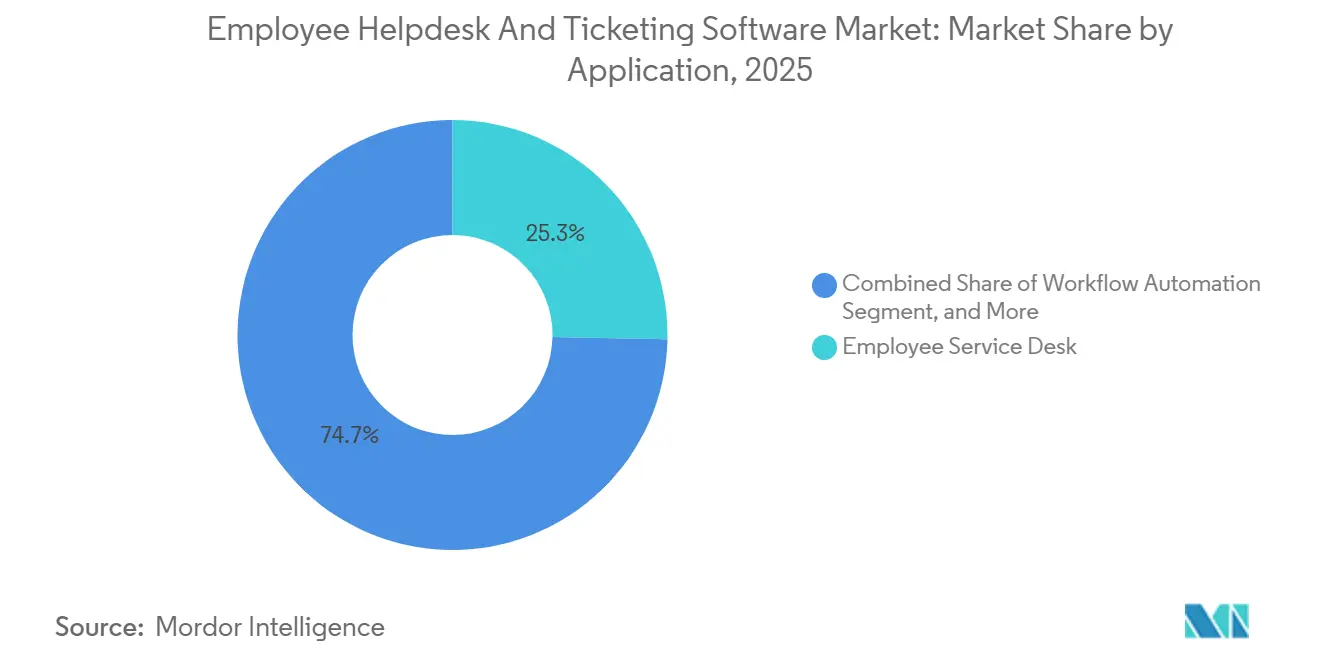

- By application, employee service desk accounted for 25.31% of the employee helpdesk and ticketing software market size in 2025, while workflow automation are projected to grow at a 13.17% CAGR through 2031.

- By end-user industry, information technology and telecom held 29.11% of the market in 2025, while healthcare and life sciences are expected to expand at a 12.89% CAGR through 2031.

- By enterprise size, large enterprises represented 62.32% of the market in 2025, while medium-sized enterprises are projected to record the fastest growth at a 12.31% CAGR through 2031.

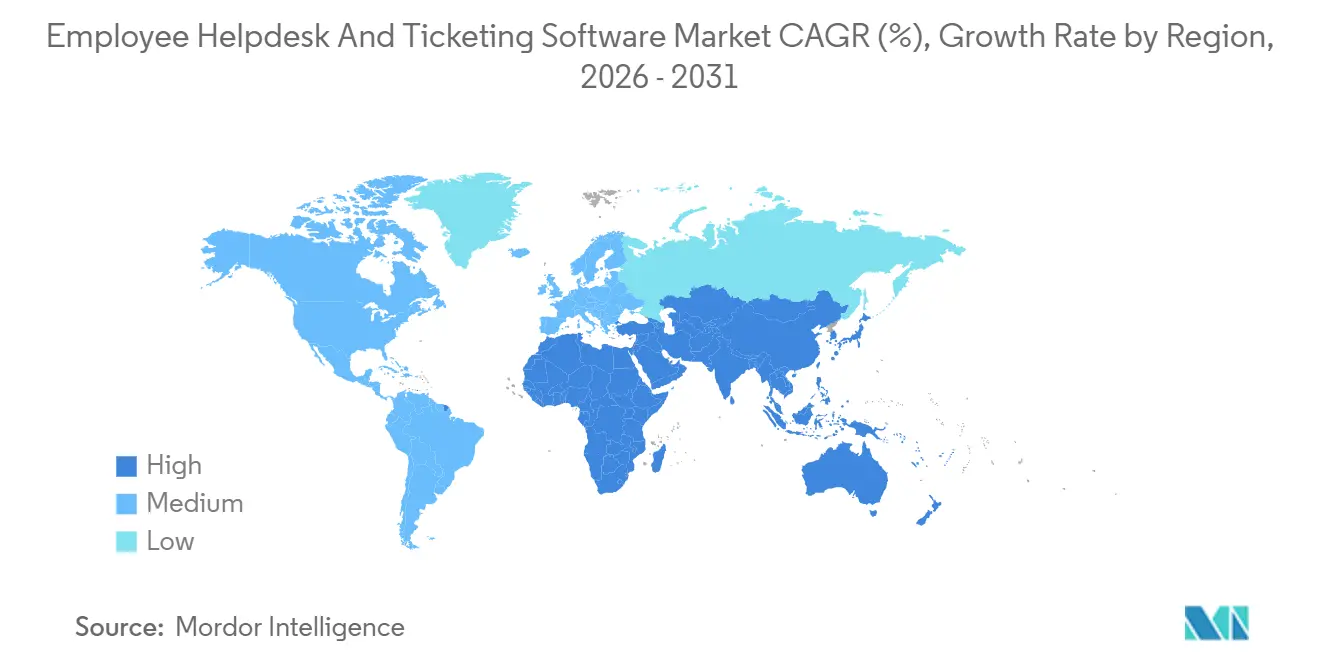

- By geography, North America held 42.31% of the market in 2025, while Asia-Pacific is projected to advance at a 14.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Employee Helpdesk And Ticketing Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Ticket Deflection and Agent Assist | +3.2% | Global | Medium term (2-4 years) |

| Expansion of Enterprise Service Management Beyond IT | +2.1% | Global | Medium term (2-4 years) |

| Cloud-Based and Hybrid Deployment Adoption | +1.8% | Global | Short term (≤ 2 years) |

| Self-Service and Knowledge-Centric Support Modernization | +1.4% | Global | Medium term (2-4 years) |

| Collaboration-Suite Embedded Support Inside Teams and Slack | +0.9% | North America and Europe | Short term (≤ 2 years) |

| DORA-Driven Incident Evidence and Workflow Traceability | +0.6% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Ticket Deflection and Agent Assist

AI is changing the commercial logic of the employee helpdesk and ticketing software market, as buyers now expect measurable resolution outcomes rather than simple chatbot deflection. Research showed that 87% of organizations were already deploying AI in ITSM or expected to do so within 24 months, and 97% said AI capabilities would influence their next platform decision, which shows how quickly AI moved from optional functionality to a baseline procurement filter. The same research found that organizations with broader AI deployment reported ticket deflection, faster resolution times, and better satisfaction outcomes, with better results when AI was embedded inside the core ITSM environment rather than added through external layers. Another report said its AI Agent delivered a 65.7% ticket deflection rate and helped save an estimated 431,270 work hours annually, which supports the shift toward outcome-based platform comparisons in the employee helpdesk and ticketing software market. One platform said its Level 1 IT Service Desk AI Specialist resolved more than 90% of employee IT requests and closed cases 99% faster than human agents, resetting executive expectations for what autonomous support should deliver at scale. As low-complexity requests are removed from the queue, the remaining tickets become harder and more dependent on permissions, workflow context, and system-level traceability, which raises the value of platforms that were designed for governed automation from the start.[1]ServiceNow, “ServiceNow Turns Enterprise AI Chaos into Control With the Platform for Governed, Autonomous Work,” ServiceNow Newsroom, newsroom.servicenow.com

Expansion of Enterprise Service Management Beyond IT

The employee helpdesk and ticketing software market is broadening because service management is moving into HR, finance, legal, facilities, and workplace operations. In May 2026, organizations expanding ESM programs were prioritizing common taxonomies, governance alignment, and operating readiness before choosing tools, which suggests that cross-functional process discipline is now central to vendor selection.[2]OpenText, “ESM Accelerates in 2026, It’s a Strategy, Not a Tool Choice,” OpenText Blogs, blogs.opentext.com This shift benefits vendors that can support multiple service domains on a single platform, as buyers increasingly want a single operating model for request intake, approvals, policy handling, and evidence retention. Freshworks launched AI-powered HR service delivery in May 2026 and said these capabilities would be available for Freshservice for Business Teams from June 30, 2026, showing how vendors are turning ITSM infrastructure into a broader employee service layer. Atlassian also extended Jira Service Management through its Service Collection to support HR, facilities, finance, and customer support under a unified service delivery model, widening its addressable spend beyond core IT service workflows. As ESM grows, the employee helpdesk and ticketing software market attracts new budget pools, but it also becomes more demanding, as platforms must support multiple service teams without losing governance consistency.[3]Freshworks, “Powered by AI, IT Service Delivery Hits All-Time Highs,” Freshworks, freshworks.com

Cloud-Based and Hybrid Deployment Adoption

Cloud remains the default route for new platform rollouts, but the employee helpdesk and ticketing software market is seeing some of its strongest incremental demand move toward hybrid designs. This pattern is strongest in regulated sectors where organizations want AI-native automation, analytics, and self-service functions, but still need tighter control over where sensitive records are stored and processed. ServiceNow highlighted protected deployment options, such as its Singapore Protected Platform and regional data residency configurations, demonstrating how sovereignty controls have become a competitive feature rather than a support add-on. Ivanti said its Neurons platform supports on-premises, SaaS, and hybrid deployment with the same AI capabilities across these models, which aligns with buyer demand for flexible architecture without losing automation functionality. TeamDynamix also found that organizations using AI natively within their ITSM environment reported stronger performance outcomes than those layering it through external middleware, reinforcing the advantage of tightly integrated architectures in the employee helpdesk and ticketing software market. The result is a more segmented deployment landscape where cloud-first, hybrid, and residual on-premises models each serve different control, compliance, and implementation needs.

Self-Service and Knowledge-Centric Support Modernization

The employee helpdesk and ticketing software market is also being reshaped by the rebuilding of knowledge systems that make self-service credible at scale. TeamDynamix found that knowledge base gap identification was the leading AI use case in ITSM deployments, cited by 88% of AI-adopting organizations, indicating that many enterprises are first improving content quality before pushing more employee-facing automation. Freshworks reported that service desks with knowledge bases containing 50 or more articles delivered average resolution times 5% faster, and that Freddy AI Copilot reduced ticket resolution time by 76.6% when paired with a strong knowledge foundation. Freshworks later launched Copilot Resolution Insights to integrate AI-generated summaries and root-cause analysis directly into the ticket, shortening the time between solving an issue and capturing reusable knowledge. This means the employee helpdesk and ticketing software market is no longer rewarding vendors that offer a chatbot without content discipline, because resolution quality still depends on how well knowledge is structured, updated, and surfaced. The platforms gaining traction treat knowledge capture, self-service search, and guided resolution as a single, connected workflow rather than separate product modules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security, Privacy, and Data Residency Concerns | -2.1% | Global, notably EU and APAC | Medium term (2-4 years) |

| Legacy Integration and Data Readiness Gaps | -1.5% | Global | Long term (≥ 4 years) |

| Shadow AI Bypassing Formal Ticket Capture | -0.9% | North America and Europe | Short term (≤ 2 years) |

| AI Governance, Logging, and Transparency Compliance Burden | -0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Security, Privacy, and Data Residency Concerns

Security and residency requirements are slowing parts of the employee helpdesk and ticketing software market because internal service tickets often contain identity data, access details, HR records, and workflow evidence. The Cloud Security Alliance said 80% of enterprises reported unintended AI agent actions, and 39% had encountered agents that accessed unauthorized systems, underscoring why support platforms are now being reviewed as sensitive control points for enterprise AI governance.[4]Cloud Security Alliance, “Shadow AI Infrastructure, Systemic Risk to the Enterprise,” Cloud Security Alliance, labs.cloudsecurityalliance.org The EU Digital Operational Resilience Act became fully applicable on January 17, 2025, and it requires financial entities to maintain structured ICT incident records and reporting discipline, which raises the importance of secure logging and traceable workflows in helpdesk environments. The European Banking Authority also details ICT-related incident management, classification, and reporting obligations under DORA, which makes real-time evidence capture more central to technology purchasing in Europe. In practice, this pushes buyers toward platforms that can separate data persistence, regional hosting, model execution, and access logging without creating operational friction. It also raises the cost of competition in the employee helpdesk and ticketing software market, as compliance certifications and regional architecture options have become minimum entry requirements for larger, regulated deals.

Legacy Integration and Data Readiness Gaps

Legacy integration problems remain a brake on the employee helpdesk and ticketing software market because AI performance still depends on the quality of CMDB records, asset data, workflow definitions, and historical service logic. TeamDynamix identified data quality as the top barrier to AI in ITSM and ranked integration complexity immediately behind it, confirming that many organizations are blocked by fragmented operational data rather than weak model capability. Enterprises with long-established service environments often carry years of customizations, disconnected workflows, and incomplete records, which make platform migration more difficult and make agent-based automation less reliable during early rollout phases. Ivanti has positioned identical AI functionality across on-premises, SaaS, and hybrid setups to address this integration reality, since customers often need staged modernization rather than a single-step replacement. Weak asset categorization, poor relationship mapping, and siloed configuration data limit the context available to automated agents, leading the same AI feature to perform very differently across enterprises. This creates a two-speed adoption pattern where organizations with stronger service data mature faster, while others delay expansion until foundational data and workflow hygiene improve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Surges as Regulated Sectors Navigate AI and Sovereignty

Cloud-based deployment accounted for 66.14% of the market in 2025, confirming that the employee helpdesk and ticketing software market still leans heavily toward scalable, remotely accessible, cloud-first operating models. That lead was built over multiple years as enterprises moved away from older on-premises tools to gain easier upgrades, faster rollout cycles, and better access to AI-native functionality. Hybrid deployment is projected to grow at a 11.73% CAGR through 2031, indicating where the next layer of demand is forming as regulated buyers seek greater architectural control without stepping away from automation. The employee helpdesk and ticketing software industry is therefore shifting from a single preferred model toward a more durable mix of cloud, hybrid, and smaller but still relevant on-premises estates. On-premises deployment continues to lose relative ground, but it remains important in defense, critical infrastructure, and government settings where air-gapped systems, classified data handling, or sovereign infrastructure policies still shape software selection. In the employee helpdesk and ticketing software market, this mix change matters because it expands eligibility among buyers who previously could not adopt cloud-only platforms.

Atlassian rolled out data residency controls for Rovo AI across supported regions in 2025, demonstrating how leading vendors adjusted their product architecture to meet privacy-sensitive enterprise requirements rather than treating residency as an afterthought. Ivanti said Neurons supports on-premises, SaaS, and hybrid deployments, with the same AI capabilities available across configurations, reducing compromise for customers that need flexibility during migration. ServiceNow also highlighted sovereign and protected environment options, including its Singapore Protected Platform, which reflects how regional control requirements are becoming a direct driver of product design and sales positioning. These moves show why hybrid is not a temporary bridge but a structural feature of the employee helpdesk and ticketing software market for sectors that need both AI utility and location-specific control. They also explain why vendors that maintain multi-modal deployment support are better placed to win public-sector, BFSI, and healthcare contracts.

By End User Enterprise Size: Medium Enterprises Drive the Next Growth Wave

Large enterprises accounted for 62.32% of the market in 2025, which means the employee helpdesk and ticketing software market still draws most of its revenue from complex organizations with broad service portfolios and large internal support operations. These buyers usually run several adjacent tools around their core service platform, so expansion often comes from vendor consolidation, deeper automation, and cross-domain workflow adoption rather than from first-time deployment. Medium-sized enterprises are projected to grow at a 12.31% CAGR through 2031, signaling that the next strong wave of adoption will come from organizations seeking enterprise-grade capabilities without long implementation cycles. In the employee helpdesk and ticketing software market, this group sits in a valuable middle zone where budget discipline is real, but process maturity and support complexity are high enough to justify platform standardization. Vendors are responding with no-code configuration, faster implementation packages, and prebuilt service templates that reduce the operational burden that once kept this cohort on lighter tools. This is one reason the employee helpdesk and ticketing software market is expanding below the largest enterprise tier, rather than relying solely on high-end replacement cycles.

ServiceNow announced its Enterprise Service Management Foundation in May 2026 to deliver IT, HR, legal, finance, procurement, and workplace services within weeks for mid-size organizations, directly addressing the deployment speed gap that has long blocked broader adoption. Freshworks also expanded its AI-first service delivery position in 2026 through Freshservice product additions aimed at faster, lower-complexity adoption across business teams, which fits the needs of organizations seeking shorter time to value. Small enterprises still represent a volume opportunity, especially as vertical templates and cloud deployment reduce setup time from months to days, but their average contract values remain lower. The employee helpdesk and ticketing software industry is therefore being pulled in 2 directions at once, with large enterprises supporting deep platform expansion and medium enterprises driving the most attractive growth rate. This balance supports durable demand because it spreads vendor opportunity across both high-value strategic accounts and a broader mid-market customer base

By Application: Workflow Automation Reshapes Service Delivery Economics

Employee Service Desk accounted for 25.31% of the market in 2025, indicating that foundational request handling still anchors the employee helpdesk and ticketing software market, even as platform scope broadens. Knowledge management and self-service followed with a 18.74% share, indicating that ticket intake and knowledge access remain closely linked in the current product mix. Workflow automation are expected to grow at a 13.17% CAGR through 2031, which marks the strongest expansion among application areas as organizations seek fewer manual handoffs and more connected service flows. Service request and catalog management are also projected to grow at a 12.09% CAGR, reflecting the role of standardized service catalogs in expanding support models into HR, legal, facilities, and other business teams. Together, these figures show that the employee helpdesk and ticketing software market is moving from case tracking toward orchestration, evidence generation, and system-aware resolution. Service desk remains the entry point, but the bigger spending opportunity increasingly sits in automation layers that connect request creation, approvals, asset context, change control, and post-incident review.

The European Banking Authority’s DORA rulebook places greater emphasis on ICT incident management, classification, and reporting, which supports the rise of analytics and reporting as core functional layers rather than optional dashboards. Freshworks launched Copilot Resolution Insights in May 2026, with AI-generated summaries and source-backed confidence scoring in tickets, demonstrating how reporting and root cause analysis are being embedded directly into frontline workflows. In practical terms, this means the application mix has become a useful signal of organizational maturity in the employee helpdesk and ticketing software market, because companies that move into workflow automation and advanced service management usually deepen their platform dependence. The employee helpdesk and ticketing software market size for service desk and incident management remained the largest in 2025, but the employee helpdesk and ticketing software market size for workflow automation and reporting is set to expand faster through 2031. That shift improves vendor upsell potential because automation-heavy customers tend to depend on deeper integrations, broader data access, and tighter workflow design.

By End-User Industry: Healthcare’s ESM Pivot Unlocks High-Value Expansion

Information technology and telecom accounted for 29.11% of the market in 2025, making it the largest vertical in the employee helpdesk and ticketing software market, thanks to its long-standing use of structured incident, request, and change processes. Healthcare and life sciences are projected to grow at a 12.89% CAGR through 2031, reflecting a faster shift toward service models that connect IT operations with clinical, administrative, and employee support needs. This vertical is demanding because healthcare environments must manage EHR-related integration complexity, classify operational issues by potential care impact, and support 24-7 service continuity. Those needs favor platforms that can extend IT-proven process discipline into broader operational settings rather than only logging general support tickets. The employee helpdesk and ticketing software market is therefore gaining high-value opportunities where workflow control matters as much as resolution speed. Healthcare growth also shows how ESM expansion can create new demand in environments where service interruptions affect both staff productivity and service quality.

Ireland’s Health Service Executive went live with Ivanti Neurons for ITSM in March 2026, introducing a redesigned National Service Desk interface and an advanced self-service portal to support national healthcare operations, providing a public-sector healthcare example at a meaningful scale. In Europe, DORA is also pushing BFSI organizations to replace manual incident processes with platforms that can maintain structured records and support faster evidence generation for ICT events. Retail and e-commerce buyers continue to focus on high-volume ticket handling and workforce-related integration needs, while industrial manufacturing is increasingly testing platforms against OT and IT coordination requirements. Government demand is rising through digital transformation programs, especially where sovereign cloud options, accessible interfaces, and public-sector references influence procurement credibility. The employee helpdesk and ticketing software market share remained highest in information technology and telecom in 2025, but sectors with stricter operating requirements and broader service management ambitions are clearly driving future growth.

Geography Analysis

North America held 42.31% of the market in 2025, making it the largest regional market for employee helpdesk and ticketing software. The region benefits from deep enterprise technology budgets, a high concentration of AI-ready IT organizations, and a vendor base that continues to reinvest local revenue into product development and go-to-market expansion. ServiceNow said it was targeting USD 30 billion or more in subscription revenue by 2030, with AI accounting for more than 30% of annual contract value, reflecting the scale and direction of investment flowing through the North American platform ecosystem. The United States drives most of the region’s enterprise and mid-market demand, while Canada and Mexico add growth through modernization programs and nearshore delivery trends. Government procurement also narrows the vendor field through filters such as FedRAMP, giving additional advantage to suppliers with strong compliance positions.

Asia-Pacific is projected to expand at a 14.27% CAGR through 2031, making it the fastest-growing regional market for employee helpdesk and ticketing software. Growth is supported by expanding digital service infrastructure in India, China, South Korea, Australia, and New Zealand, along with a broader base of enterprises formalizing internal support operations. Demand in the region is shaped by large domestic enterprises, global delivery centers, public-sector digitization, and a rising need for platforms that can support both cloud and controlled deployment models. Australia and New Zealand stand out for strong per-employee ITSM spending, while South Korea presents concentrated opportunities through large enterprise groups with mature IT operations.

Europe continues to hold a significant share of the employee helpdesk and ticketing software market, led by Germany, the United Kingdom, France, the Netherlands, and Italy. DORA has become one of the clearest catalysts in the region, because regulators moved from policy preparation toward active evidence and reporting expectations in 2026. The European Banking Authority’s rulebook reinforces the need for structured ICT incident classification and reporting, which supports demand for audit-ready service workflows. South America, the Middle East, and Africa remain smaller in absolute terms, but digital government programs and multinational enterprise expansion are creating a stronger pipeline of structured procurement. In the Middle East, sovereign deployment preferences and public-sector transformation plans are driving vendor opportunities, while parts of Africa remain early-stage markets with demand largely tied to financial services and telecommunications.

Competitive Landscape

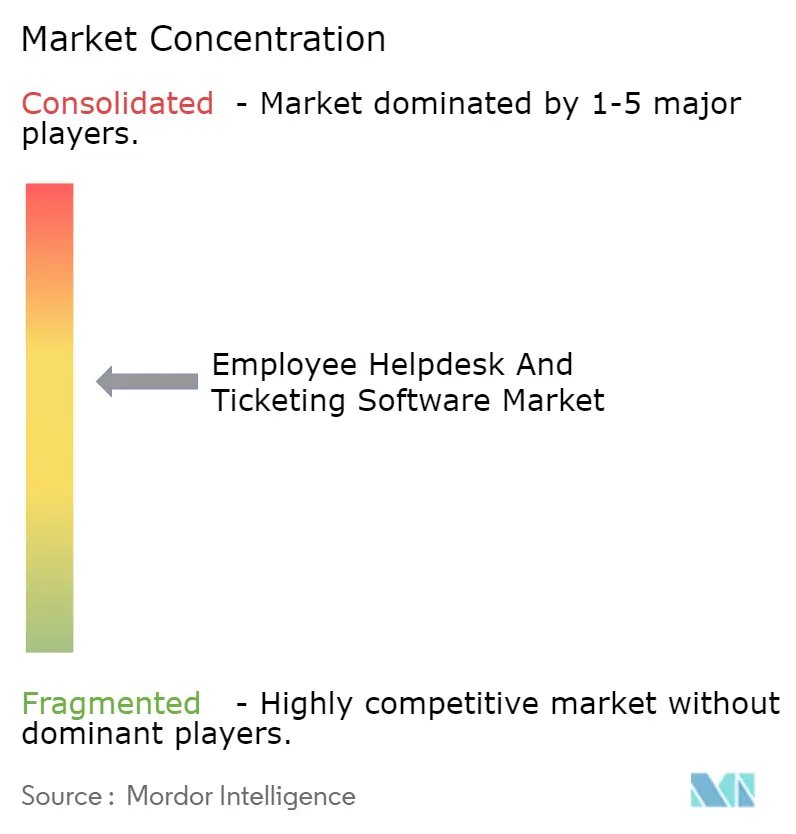

The employee helpdesk and ticketing software market remains moderately consolidated at the enterprise tier, with ServiceNow, Freshworks, and Zendesk positioned prominently, while Atlassian, Ivanti, SysAid, HaloITSM, HappyFox, TOPdesk, EasyVista, 4me, and other challengers keep the field competitive. The main line of competition has shifted away from simple feature breadth and toward governance architecture, deployment flexibility, workflow extensibility, and the ability to prove how AI actions are controlled. This matters because the employee helpdesk and ticketing software market now serves buyers that want autonomous support, but also need permission inheritance, logging, regional controls, and explainable execution. The presence of credible mid-market specialists prevents the market from tightening into a small closed group, even though scale still matters in large enterprises and regulated procurement. Large vendors keep an advantage through platform breadth, integration depth, and ecosystem reach, while smaller vendors compete by reducing deployment time and complexity.

ServiceNow introduced AI Control Tower at Knowledge 2026 and positioned it around per-interaction logging, enterprise policy enforcement, and decision explainability, demonstrating how it is using governance as a commercial differentiator rather than solely as a technical control. Zendesk launched its Autonomous Service Workforce in May 2026 and said it was trained on nearly 20 billion ticket interactions, which reinforces its strategy of competing on resolution quality and native collaboration-channel execution. Freshworks expanded its AI service operations stack in May 2026 with Freddy AI Agent Studio, IT and HR agents, and broader Freshservice capabilities, which strengthen its position with buyers seeking faster implementation and lower overhead. Atlassian also widened its scope through the Service Collection, Incident Command Center, Solution Composer, and new AIOps integrations, further pushing it into multi-domain service delivery.

The employee helpdesk and ticketing software market still has clear white space in healthcare-specific workflows, manufacturing environments that connect OT and IT service processes, and mid-market ESM buyers seeking a single service layer across disconnected business tools. Ivanti’s support for cloud, on-premises, and hybrid modes, with agentic AI capabilities, positions it well with customers that need staged modernization rather than cloud-only replacement. Atlassian’s continued residency and service-ops expansion also support its challenge in accounts where buyers want strong workflow flexibility and lower platform friction. Compliance baselines, such as GDPR alignment, ISO standards, and regional hosting expectations, increasingly act as table stakes, limiting the credible vendor pool for sensitive enterprise deals. That combination of scale leaders, active challengers, and rising compliance thresholds keeps the employee helpdesk and ticketing software market competitive, but not so fragmented as to erode the strategic advantage of the largest platform providers.

Employee Helpdesk And Ticketing Software Industry Leaders

Zendesk, Inc.

Freshworks Inc.

Freshworks Inc.

Atlassian Corporation Plc

Zoho Corporation Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ServiceNow launched ServiceNow Otto, a unified enterprise AI experience combining conversational AI, autonomous workflows, and enterprise search, alongside an expanded Autonomous Workforce that introduced AI specialists for IT, employee service, CRM, and security. The company's internal Level 1 IT Service Desk AI Specialist resolved over 90% of employee IT requests and closed cases 99% faster than human agents, setting an autonomous service desk benchmark.

- May 2026: Zendesk introduced its Autonomous Service Workforce at Relate 2026, replacing deflection-based bots with fully autonomous AI agents for employee service, powered by its Unleash acquisition and operating natively in Slack and Microsoft Teams with source-level permission enforcement. The company shifted to outcome-based pricing, charging only for verified resolutions, trained on approximately 20 billion ticket interactions.

- May 2026: Freshworks unveiled AI service operations at its annual Refresh conference, introducing Freddy AI Agent Studio for Freshservice with pre-built IT and HR agents and a no-code agent builder. Freshservice IT Asset Management reached general availability as of March 31, 2026, while AI-powered HR service delivery is planned for general availability on June 30, 2026.

- May 2026: Atlassian launched its Service Collection at Team '26 Anaheim, introducing the Incident Command Center, AI-native response hub, Solution Composer for designing AI-native service journeys, and new AIOps integrations with Lansweeper, Coralogix, and Honeycomb alongside existing New Relic and Dynatrace partnerships, expanding the platform from ITSM to a multi-domain service delivery system.

Global Employee Helpdesk And Ticketing Software Market Report Scope

The Employee Helpdesk and Ticketing Software market refers to technology solutions designed to manage employee service requests, streamline HR support operations, and enhance workforce experience through centralized ticketing and automation. These platforms provide functionalities such as employee service desk, service request management, knowledge management and self-service, workflow automation, analytics and reporting, and advanced service management. Delivered through cloud-based, on-premises, and hybrid deployment models, they cater to both large enterprises and SMEs across industries including BFSI, healthcare, IT and telecom, retail, manufacturing, government, and others. The core purpose of this market is to improve HR service delivery efficiency, reduce administrative overhead, ensure compliance, and provide data-driven insights that support employee engagement and organizational productivity.

The Employee Helpdesk and Ticketing Software market report is segmented by Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Application (Employee Service Desk, Service Request Management, Knowledge Management and Self-Service, Workflow Automation, Analytics and Reporting, Advanced Service Management), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa), The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Employee Service Desk |

| Service Request Management |

| Knowledge Management and Self-Service |

| Workflow Automation |

| Analytics and Reporting |

| Advanced Service Management |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Application | Employee Service Desk | |

| Service Request Management | ||

| Knowledge Management and Self-Service | ||

| Workflow Automation | ||

| Analytics and Reporting | ||

| Advanced Service Management | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the employee helpdesk and ticketing software market in 2026?

The employee helpdesk and ticketing software market is estimated at USD 7.10 billion in 2026 and is forecast to reach USD 11.67 billion by 2031 at a CAGR of 10.45%.

What is driving demand for employee helpdesk and ticketing software in 2026?

Demand is being driven by agentic AI adoption, broader enterprise service management use, stronger self-service expectations, and compliance needs such as structured ICT incident logging and audit trails.

Which deployment model is growing the fastest?

Hybrid deployment is the fastest-growing model, with an expected CAGR of 11.73% through 2031, as regulated sectors seek stronger data control without losing AI-enabled functionality.

Which application area is expanding the fastest?

Workflow automation is the fastest-growing application segment, with a projected CAGR of 13.17% through 2031, as organizations move beyond ticket triage toward connected service workflows.

Which end-user sector is showing the strongest growth?

Healthcare and life sciences is the fastest-growing end-user segment, with a projected CAGR of 12.89% through 2031, supported by integration complexity, clinical impact requirements, and broader ESM adoption.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to grow the fastest, with a CAGR of 14.27% through 2031, driven by enterprise digitization, public-sector modernization, and expanding internal service operations across major regional economies.

Page last updated on: