Space Management And Desk Booking Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.86 Billion |

| Market Size (2031) | USD 7.04 Billion |

| Growth Rate (2026 - 2031) | 12.77% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Space Management And Desk Booking Software Market Analysis by Mordor Intelligence

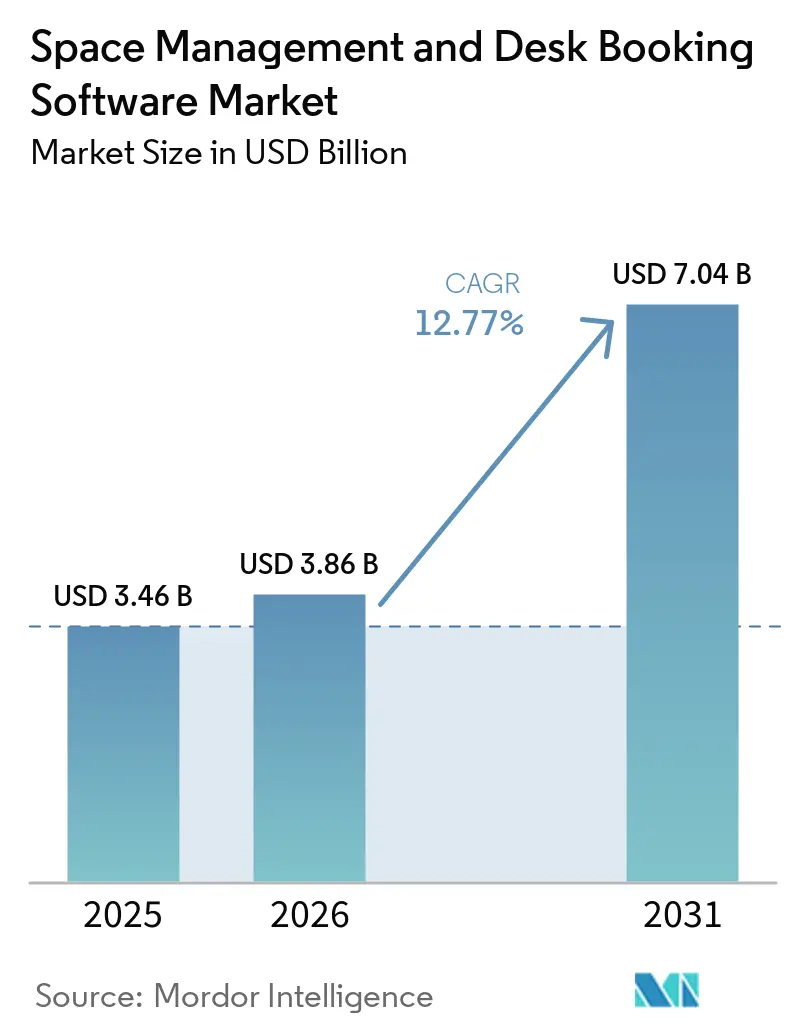

The space management and desk booking software market size was valued at USD 3.46 billion in 2025 and estimated to grow from USD 3.86 billion in 2026 to reach USD 7.04 billion by 2031, at a CAGR of 12.77% during the forecast period (2026-2031). Organizations across sectors are increasing spending on hybrid work infrastructure because space allocation, attendance control, and lease efficiency are now more closely tied to financial planning. Enterprise real estate teams are treating workplace software as a strategic tool for portfolio optimization, which is moving buying decisions beyond facilities departments and into senior management discussions. Competition is also shifting toward platforms that combine booking, occupancy analytics, planning, and workflow integration, as large buyers replace narrow point solutions with broader operational systems. AI-enabled automation inside collaboration tools is reducing user friction and making booking behavior easier to standardize across office networks. Growth remains moderated by integration work, privacy governance, budget review cycles, and resistance to hot-desking, which leaves the market split between fast-moving large enterprises and slower mid-market buyers.

Key Report Takeaways

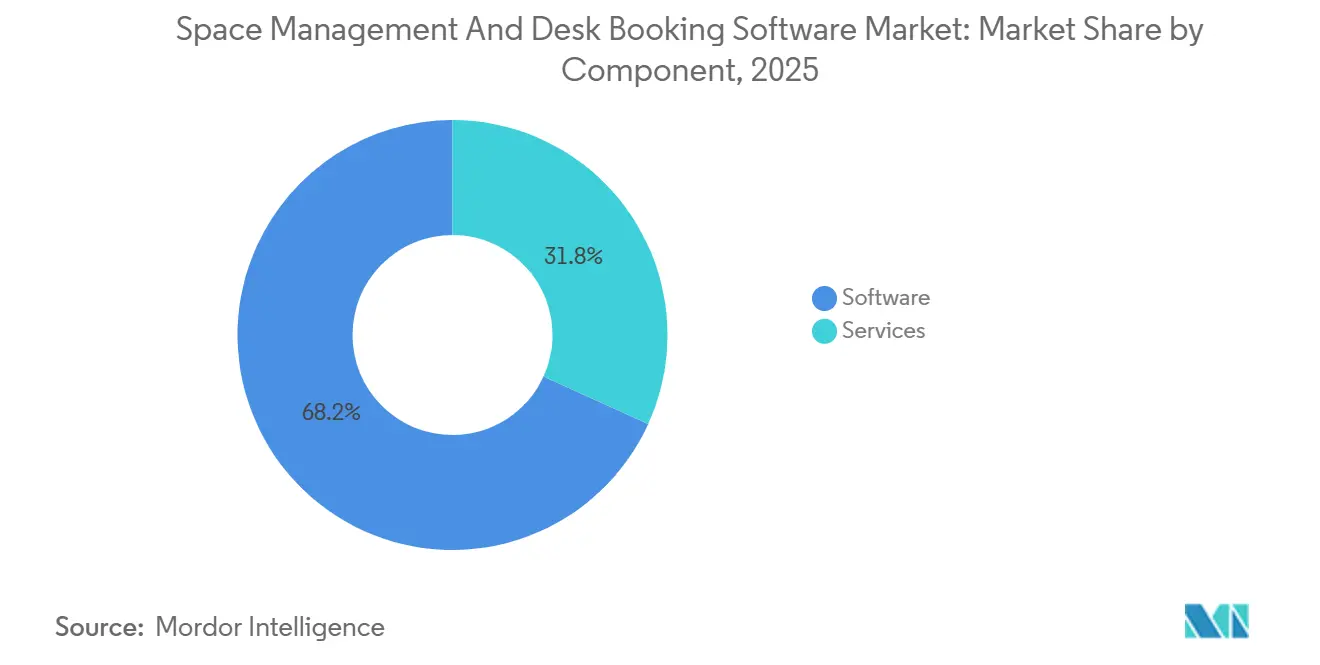

- By component, software held 68.21% share of the space management and desk booking software market in 2025, while services are projected to expand at a 16.94% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 64.71% of revenue in 2025, while hybrid deployment is projected to record the highest CAGR of 18.21% through 2031.

- By enterprise size, large enterprises held 60.92% share in 2025, while small and medium-sized enterprises are projected to grow at a 17.36% CAGR through 2031.

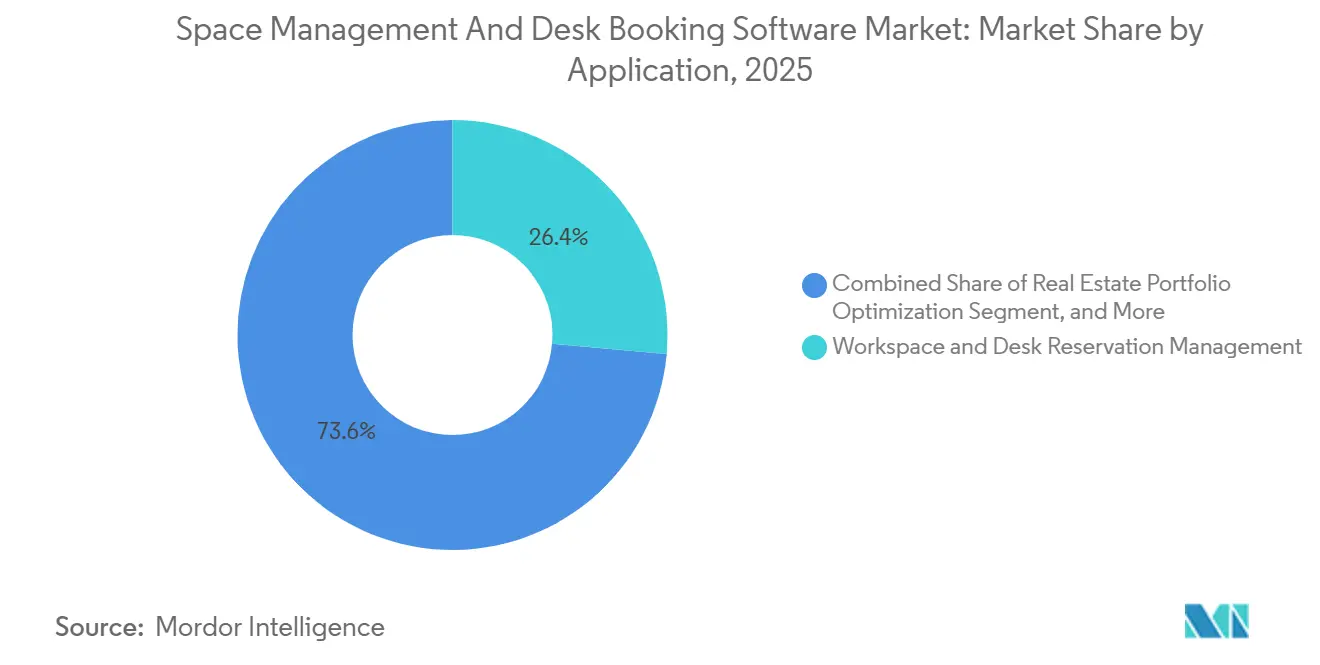

- By application, workspace and desk reservation management accounted for 26.41% of the space management and desk booking software market size in 2025, while real estate portfolio optimization is projected to expand at a 19.12% CAGR through 2031.

- By end-user industry, information technology and telecom held 28.31% share in 2025, while healthcare and life sciences are projected to grow at a 15.47% CAGR through 2031.

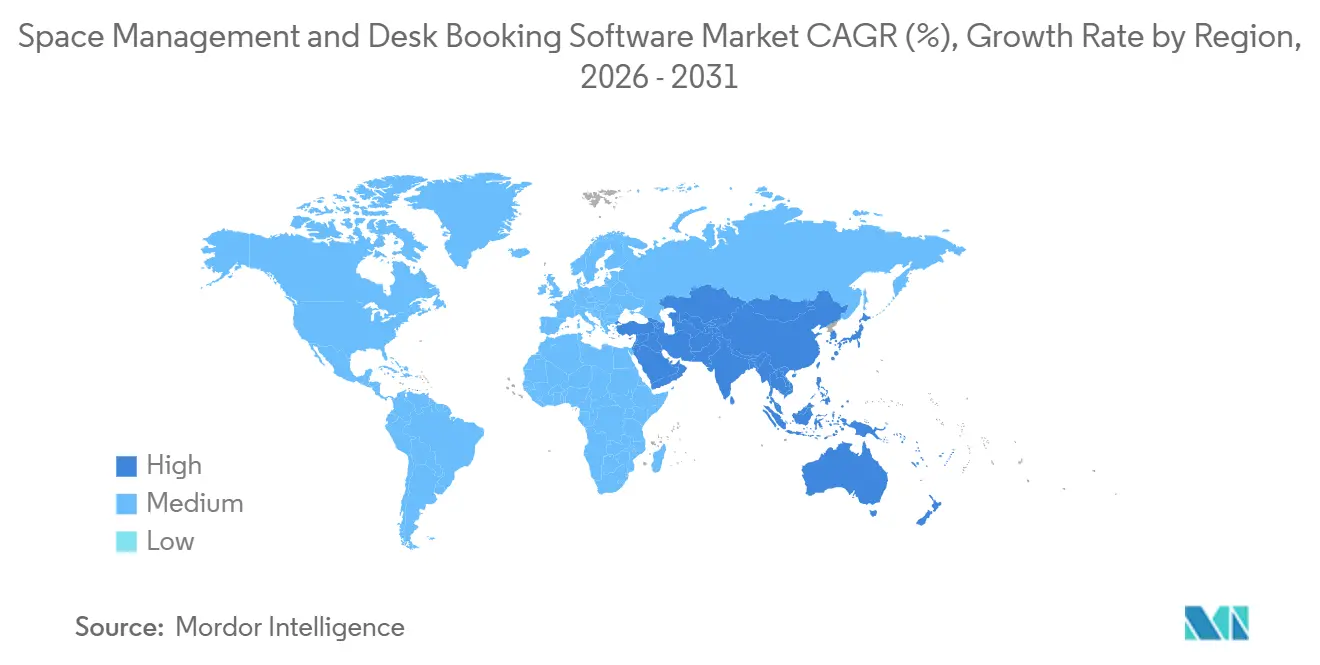

- By geography, North America held 39.63% of the space management and desk booking software market share in 2025, while Asia-Pacific is projected to advance at a 21.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Space Management And Desk Booking Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Hybrid Work Adoption and Desk Utilization Optimization | +3.2% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| AI-Driven Automation for Booking, Allocation, And Scenario Planning | +2.7% | Global, with early scale gains in North America and APAC tech hubs | Medium term (2-4 years) |

| Consolidation of Workplace, Visitor, and Facilities Workflows | +2.0% | North America and EU, spill-over to Middle East enterprise hubs | Medium term (2-4 years) |

| Sustainability Linked Space Rationalization and Energy Savings | +1.5% | EU-core and APAC, with growing influence in North America | Medium term (2-4 years) |

| Rising Enterprise Demand for Real Time Occupancy Analytics | +1.2% | Global, concentrated in large enterprise portfolios across the US, UK, and | Short term (≤ 2 years) |

| Growth in Subscription Based Workplace Software Procurement | +0.9% | North America and EU, accelerating in APAC and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Hybrid Work Adoption and Desk Utilization Optimization

Structured hybrid work is now an operating model rather than a trial, which keeps the space management and desk booking software markets tied to daily seat allocation needs across large office portfolios. Hybrid program prevalence reached 80% of organizations in 2026, up from 77% in 2025.[1]JLL, “Structured Hybrid Work Becomes the Global Norm as Strategic Focus Shifts to AI-Readiness,” JLL Newsroom, jll.com The same benchmark showed that 62% of employers now mandate a fixed number of in-office days, up from 28% in 2022. 80% of corporate real estate teams now rank portfolio optimization as their primary goal, tying attendance management more closely to broader space decisions. The gap between actual and target office utilization narrowed from 25 percentage points in 2025 to 18 percentage points in 2026. This combination is pushing the space management and desk booking software market beyond basic reservation tools and toward predictive allocation, peak-day balancing, and stronger portfolio discipline.

AI-Driven Automation for Booking, Allocation, and Scenario Planning

AI is changing how employees interact with space management and desk booking software by moving booking actions into the communication tools they already use every day. Its 2026 product rollout includes natural language booking workflows and live analytics for desk and meeting room usage. Kadence also expanded its workplace operations platform in March 2026, adding room displays, AI-powered no-show detection, and real-time synchronization with Outlook and Google Workspace. OfficeSpace Software introduced workplace agents inside AI Canvas in March 2026, aimed at automating decision workflows for real estate, facilities, and workplace leaders. More than 70% of organizations had not moved beyond the exploration stage for AI-specific workplace capabilities, and 45% cited system integration and compatibility as a barrier. That gap leaves room for the space management and desk booking software market to reward vendors that can turn AI from a demonstration feature into a working operational layer.

Consolidation of Workplace, Visitor, and Facilities Workflows

Enterprise buyers increasingly want fewer systems, which is pushing the space management and desk booking software market toward broader workplace operations platforms. Kadence launched a rebuilt Visitor Management System in January 2026 and connected it natively to its SpaceOps platform. Eptura announced AI workflows across workplace experience, asset management, and space planning in April 2026, which showed the same move toward unified operations. LumApps also agreed to acquire Comeen in April 2026 to bring space management, digital signage, and visitor services into its employee hub. When booking data, visitor traffic, service requests, and planning records sit in one system, enterprises gain a fuller view of real demand. That reduces switching costs and improves retention, which is why the space management and desk booking software market is favoring vendors that can consolidate adjacent workflows without making deployment more difficult.

Sustainability Linked Space Rationalization and Energy Savings

Sustainability goals are giving space management and desk booking software a broader role in energy management and reporting programs. The U.S. Green Building Council published LEED v5 O+M in February 2026, and the framework makes occupancy monitoring relevant to energy tracking compliance credits. In Australia, the NABERS Sustainable Portfolios Index covered 8.2 million sq. m. of rated office floor space in 2026, which kept performance measurement closely linked to operating data. This shift matters because space data can tell facilities teams when to condition floors, rooms, and services based on actual usage rather than fixed schedules.[2]U.S. Green Building Council, “LEED v5 O+M Rating System,” USGBC, usgbc.org It also broadens the buyer group beyond workplace managers, because finance and sustainability leaders now have a direct interest in procurement decisions. As a result, the space management and desk booking software market is gaining support from energy and compliance priorities that sit outside traditional desk reservation budgets.[3]NABERS, “NABERS Sustainable Portfolios Index 2026, A Tool for Transparency and Leadership,” NABERS, nabers.gov.au

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity With Legacy IWMS, HR, and Access Control Systems | -1.8% | Global, heaviest in North America and EU where legacy stack density is highest | Medium term (2-4 years) |

| Data Privacy, Employee Tracking, and Cybersecurity Concerns | -1.3% | EU-core, spill-over to India and the US | Short term (≤ 2 years) |

| Change Management Resistance to Hot Desking and Booking Discipline | -0.7% | North America, EU, APAC, particularly in firms with established assigned-desk cultures | Short term (≤ 2 years) |

| Budget Scrutiny from Slower Corporate Real Estate Decision Cycles | -0.4% | Global, with pronounced impact in South America and parts of Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy IWMS, HR, and Access Control Systems

Integration remains the hardest practical barrier in the space management and desk booking software market, especially inside large enterprises that still rely on older workplace systems. The supplied material shows that organizations with legacy estate stacks often need 12-16 weeks of custom middleware work before real-time data can move across systems. Eptura's API-first guidance warned that legacy IWMS environments often rely on batch exports and tightly coupled data models, making real-time integration difficult or impossible.[4]Eptura, “Building an API-First Workplace Technology Architecture,” Eptura, eptura.com The problem grows when HR, badge access, room scheduling, and space planning records use different identifiers and update cycles. It also changes buying behavior because vendors with pre-certified connectors for systems such as SAP, Workday, and major access control products face fewer qualification hurdles. This leaves the space management and desk booking software market divided between buyers who can fund integration programs and those who delay deployment until complexity drops.

Data Privacy, Employee Tracking, and Cybersecurity Concerns

Privacy governance is slowing adoption in parts of the space management and desk booking software market because booking and occupancy data can reveal sensitive patterns of employee behavior. California's SB-238 Workplace Surveillance Tools legislation created 2026 compliance obligations for employers that use software that collects workers' personal information. Data privacy and security ranked as the top barrier to AI adoption in workplace management, cited by 70% of organizations in the 2026 benchmark. In Europe, works council reviews and strict employee privacy checks can delay the rollout of features that involve monitoring. These rules affect product design because vendors need stronger consent controls, access governance, audit trails, and regional hosting options. The result is that the space management and desk booking software market favors vendors with mature security architecture, while weaker products struggle in regulated procurement cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Revenue While Services Gain Strategic Weight

Software solutions held 68.21% of the total space management and desk booking software market share in 2025, which made software the clear revenue base of the category. The space management and desk booking software market favored software, as most buyers preferred recurring subscriptions over large upfront deployments. Demand also favored platforms that combine desk booking, space planning, visitor management, and occupancy analytics, rather than separate tools for each workflow. Eptura and Kadence both widened their platform breadth in 2026, reflecting this broader buying preference across enterprise accounts. That pattern makes software revenue more durable because every added workflow increases the value of renewal and expansion.

Services are projected to grow at a 16.94% CAGR from 2026 to 2031, making them the fastest-growing segment of the space management and desk booking software market. Implementation demand remains high because many enterprises still need connector design, data cleanup, training, rollout support, and policy alignment before software can scale. Eptura's API-first architecture guidance explains why service demand persists, since legacy models still complicate real-time integration across workplace systems. The same dynamic creates a second revenue layer for vendors that can sell advisory support, managed analytics, and post-deployment optimization alongside subscriptions. In practice, this shows that the space management and desk booking software industry is maturing into a platform business that depends on both product depth and deployment capability.

By Deployment Mode: Cloud Leads While Hybrid Gains Ground On Governance Needs

Cloud-based deployment accounted for 64.71% of market revenue in 2025, keeping cloud as the primary delivery model across the space management and desk booking software markets. Buyers favored cloud tools because they reduce infrastructure maintenance and make it easier to distribute feature updates across locations. Mobile access also matters because reservation behavior is more consistent when employees can book desks and rooms inside daily workflows. Eptura's Microsoft 365 upgrade in March 2026 showed how closely adoption now depends on seamless calendar and resource booking integration. Faster rollouts also reinforce cloud leadership compared with older on-premises scheduling environments.

Hybrid deployment is projected to expand at an 18.21% CAGR from 2026 to 2031, making it the fastest-growing mode in the space management and desk booking software market. This model appeals to enterprises that want cloud analytics and employee-facing interfaces while keeping sensitive occupancy records under tighter internal control. Privacy rules and data residency requirements have made that balance more important in Europe, financial services, and public-sector settings. On-premises deployments still matter in highly regulated environments, but upgrade burdens, limited flexibility, and greater maintenance effort constrain their growth. As hybrid architectures improve, the space management and desk booking software industry is moving toward governance-friendly delivery models that preserve cloud benefits without forcing full migration.

By Enterprise Size: Large Organizations Lead Spend While Smaller Firms Accelerate Adoption

Large enterprises held 60.92% of the market in 2025, and that leadership reflects the economics of managing large seat portfolios across many locations. The space management and desk booking software market delivers clearer savings when real estate teams can rebalance thousands of desks, floors, and leases with reliable utilization data. Large buyers also tend to replace multiple tools at once, which increases contract value and favors vendors with broader product suites. 80% of corporate real estate teams now rank portfolio optimization as their primary goal, a priority that aligns closely with large-enterprise adoption patterns. That is why major accounts remain central to pricing, roadmap design, service packaging, and procurement standards in the space management and desk booking software market.

Small and medium-sized enterprises are projected to grow at a 17.36% CAGR from 2026 to 2031, making them the fastest-rising customer group. Subscription pricing lowers the entry barrier for these firms, especially when they need better attendance visibility without a full IWMS program. SMBs drove nearly 60% year-on-year growth in office utilization through 2025, reaching 35%. That shift suggests smaller firms are no longer treating flexible seating as an informal process and are now seeking measurable controls. The mid-market remains especially open in the space management and desk booking software market because these firms need more sophistication than lightweight booking tools but less complexity than legacy enterprise platforms.

By Application: Reservation Tools Lead While Portfolio Optimization Expands Fastest

Workspace and desk reservation management accounted for 26.41% of the total market in 2025, making it the largest application across the space management and desk booking software market. This segment stayed on top because reservation reliability is still the first problem most hybrid employers need to solve. Once employees trust that a desk or room will be available, organizations can build additional workflow layers on the same platform. Vendors then extend from booking into planning, analytics, visitor flows, and service coordination, which turns a simple feature into a broader workplace operating system. That expansion path helps explain why the space management and desk booking software market keeps adding adjacent applications around the core reservation use case.

Real estate portfolio optimization is projected to expand at a 19.12% CAGR from 2026 to 2031, making it the fastest-growing application in the space management and desk booking software market. CFO-led lease review is a major reason because attendance data now feeds space reduction and renegotiation decisions more directly. Portfolio optimization was the top goal for corporate real estate teams, which supports this application's faster growth. A narrowing gap between actual and target utilization also shows that occupancy data is becoming more actionable for lease planning. As a result, the strongest application growth is shifting from day-to-day booking toward higher-value decisions on footprint, lease timing, and capital use.

By End-User Industry: IT And Telecom Drives Volume While Healthcare Scales With Shared-Space Needs

Information technology and telecom accounted for 28.31% of total end-user demand in 2025, making it the largest vertical in the space management and desk booking software market. This group adopted hybrid work earlier than many other sectors and already had the software-purchasing culture needed for a fast rollout. Tech employers also tend to manage distributed teams across several offices, which makes standardized booking rules more valuable. Software companies kept 37% of desks free to book in 2025, well above the broader average. That creates richer behavior data and helps explain why the space management and desk booking software market sees strong analytics uptake in this vertical.

Healthcare and life sciences are projected to grow at a 15.47% CAGR from 2026 to 2031, making the segment the fastest-growing in the space management and desk booking software market. Growth is tied to extending booking logic beyond office materials. A representative return on investment of 172% and a payback period of into consultation rooms, exam spaces, and other shared clinical settings. A 2026 deployment at Ahvenisto Hospital automated room allocation using appointment and shift-scheduling data. Cisco’s 2025 healthcare material reported a representative return on investment of 172% and payback in under 6 months for Cisco Spaces in a healthcare setting. These examples show that the space management and desk booking software market is widening from office coordination into environments where room availability can directly affect service delivery.

Geography Analysis

North America accounted for 39.63% of global revenue in 2025, making it the largest region in the space management and desk booking software market. The region benefits from strong SaaS readiness, large headquarters portfolios, and employers that have formalized hybrid attendance policies. Office utilization across 303 million sq. ft. of client portfolios rose to 53% in 2025 from 38% in 2024. North and South America favored 3-to-4-day attendance patterns more than the lighter office schedules common in EMEA. South America remains smaller, but multinational shared-service hubs in Brazil and Argentina are creating selective demand for booking and occupancy tools.

Europe's position in the space management and desk booking software market is shaped by strong enterprise demand and a heavier compliance burden. In the DACH region, employee monitoring rules and GDPR-focused deployment checks can lengthen rollout timelines when platforms process behavioral occupancy data. That friction raises entry barriers, but it also favors vendors that can prove data residency, auditability, and secure access controls. Germany, the United Kingdom, France, and the Netherlands remain the main spending centers, while Spain, Italy, and the Nordic countries continue to expand adoption across financial services and public-sector accounts.

Asia-Pacific is projected to grow at a 21.18% CAGR through 2031, making it the fastest-growing region in the space management and desk booking software market. Growth is tied to expanding Grade A office stock, the adoption of flexible workspace, and rising enterprise demand across India, China, and Southeast Asia. Australia's NABERS Sustainable Portfolios Index covered 8.2 million sq. m. of rated office floor space in 2026, reinforcing the region's focus on occupancy-linked building performance. The Middle East is still earlier in adoption, yet Saudi Arabia's office development pipeline and the UAE's headquarters role are lifting interest from enterprise and government buyers. Africa also remains early-stage, with demand concentrated in banking, telecommunications, and government institutions in major cities such as Johannesburg, Cape Town, Lagos, and Abuja.

Competitive Landscape

The space management and desk booking software market remains moderately consolidated, with competition split between broad workplace platforms and specialist booking vendors. Larger vendors such as Eptura, Planon, Accruent, FM: Systems, and OfficeSpace Software compete on integrated portfolio management, occupancy intelligence, and depth of desk booking. Specialists such as Robin Powered, Skedda, Tribeloo, GoBright, Kadence, and Envoy compete on deployment speed, user simplicity, and flexible integrations. The line between these groups is narrowing as specialists add planning and analytics, while larger vendors improve the everyday user experience. This convergence means the space management and desk booking software market is no longer defined by booking alone, and platform coherence is becoming the main buying test.

Robin Powered said it was recognized as a Leader in the inaugural 2026 Gartner Magic Quadrant for Workplace Experience Applications, which strengthens its position in enterprise evaluations. Eptura expanded AI workflows and live space analytics in April 2026, showing how incumbents are deepening automation inside broader workplace platforms. LumApps signed a definitive agreement in April 2026 to acquire Comeen, signaling rising interest among employee experience platforms in physical workplace data. Kadence raised USD 20 million in January 2026 to scale its SpaceOps platform, underlining investor support for integrated workplace operations models. These moves show that the space management and desk booking software market is attracting capital and product expansion around unified operations rather than stand-alone reservation tools.

A clear white space remains in the mid-market, where companies need more than basic booking but cannot absorb the legacy complexity of an IWMS. Eptura's architecture guidance and Microsoft 365 product work both point to the same procurement reality: buyers increasingly reward proven connectors, data security, and easier deployment. Vendors that combine enterprise controls with consumer-grade workflows are likely to win longer contracts and broader usage across departments. Overall, the space management and desk booking software market favors vendors that reduce integration risk, support governance, and turn occupancy data into actionable decisions for senior real estate teams.

Space Management And Desk Booking Software Industry Leaders

Eptura, Inc.

OfficeSpace Software Inc.

Planon Group B.V.

FM:Systems Group LLC

Robin Powered, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Eptura announced enhanced capabilities across its workplace experience, asset management, and space planning portfolio, including AI workflows for natural language booking via collaboration tools, live analytics for desk and meeting room usage, and the Neighborhoods intelligent desk zone assignment feature. Rollout is scheduled to continue through July 2026, with capabilities targeting enterprise-scale hybrid work optimization.

- April 2026: LumApps entered into a definitive agreement to acquire Comeen, a workplace experience platform specializing in space management, digital signage, and visitor services. The transaction was expected to complete in May 2026, integrating Comeen's physical workplace capabilities into LumApps' AI employee hub to accelerate agentic AI deployment across digital and physical work environments.

- April 2026: Robin Powered was recognized as a Leader in the inaugural 2026 Gartner Magic Quadrant for Workplace Experience Applications. The recognition validated Robin's One Workplace Platform approach combining AI-driven resource booking, visitor management, space planning, and analytics within a single cohesive system architecture, making Robin one of the first workplace software vendors to receive this category designation.

- March 2026: Eptura advanced Eptura Engage's integration with Microsoft 365, following receipt of a Solutions Partner with Certified Software designation for Financial Services AI in the Microsoft AI Cloud Partner Program. The upgrade transitions calendar and resource booking access from Exchange Web Services to Microsoft Graph ahead of EWS retirement in October 2026, securing continuity for enterprise clients.

Global Space Management And Desk Booking Software Market Report Scope

The Space Management And Desk Booking Software Market comprises digital platforms that streamline employee service delivery by managing requests, automating workflows, and centralizing support via ticketing systems. These solutions provide applications such as employee service desk, request management, knowledge management and self-service portals, workflow automation, analytics and reporting, and advanced service management. Available through cloud-based, on-premises, and hybrid deployment models, they serve both large enterprises and SMEs across industries, including BFSI, healthcare, IT and telecom, retail, manufacturing, government, and others. The primary objective of this market is to enhance HR efficiency, reduce administrative overhead, improve employee experience, and deliver data-driven insights that support organizational productivity and compliance.

The Space Management And Desk Booking Software Market report is segmented by Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Application (Workspace and Desk Reservation Management, Space Planning and Utilization Management, Occupancy Analytics and Workplace Intelligence, Real Estate Portfolio Optimization, and Integrated Workplace Management Functions), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Workspace and Desk Reservation Management |

| Space Planning and Utilization Management |

| Occupancy Analytics and Workplace Intelligence |

| Real Estate Portfolio Optimization |

| Integrated Workplace Management Functions |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Application | Workspace and Desk Reservation Management | |

| Space Planning and Utilization Management | ||

| Occupancy Analytics and Workplace Intelligence | ||

| Real Estate Portfolio Optimization | ||

| Integrated Workplace Management Functions | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the space management and desk booking software market?

The space management and desk booking software market was valued at USD 3.46 billion in 2025, reached USD 3.86 billion in 2026, and is forecast to reach USD 7.04 billion by 2031 at a 12.77% CAGR.

What is driving demand for desk booking and space management platforms?

The strongest demand drivers are structured hybrid work, portfolio optimization, AI-enabled booking workflows, and the need to combine booking, analytics, and planning inside one operating system.

Which deployment model is growing fastest in this category?

Hybrid deployment is growing fastest, with an 18.21% CAGR through 2031, because it balances cloud functionality with tighter control over sensitive occupancy data.

Which customer group spends the most on these platforms?

Large enterprises led spending with 60.92% share in 2025, mainly because they manage bigger portfolios and can capture larger savings from utilization optimization.

Which application is expanding fastest beyond basic desk booking?

Real estate portfolio optimization is the fastest-growing application, with a 19.12% CAGR through 2031, as occupancy data is increasingly used for lease review and footprint planning.

Which region offers the strongest growth outlook through 2031?

Asia-Pacific has the strongest growth outlook, with a 21.18% CAGR, supported by Grade A office expansion, flexible workspace growth, and rising enterprise adoption across major urban markets.

Page last updated on: