Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

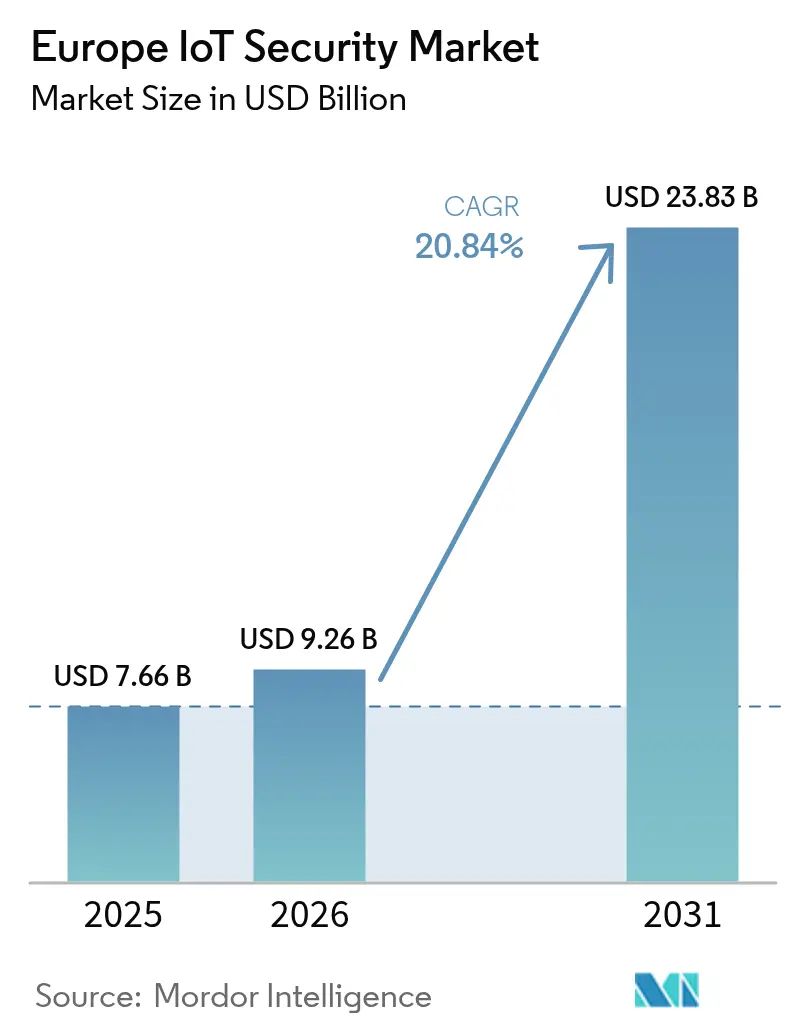

| Base Year Market Size (2025) | USD 7.66 Billion |

| Market Size (2026) | USD 9.26 Billion |

| Market Size (2031) | USD 23.83 Billion |

| Growth Rate (2026 - 2031) | 20.84% CAGR |

| Market Concentration | Medium |

Major Players_Security_Market_-_Key_Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe IoT Security Market Analysis by Mordor Intelligence

Europe IoT Security market size in 2026 is estimated at USD 9.26 billion, growing from 2025 value of USD 7.66 billion with 2031 projections showing USD 23.83 billion, growing at 20.84% CAGR over 2026-2031. Rising cyber-attacks on connected devices, stringent regulatory mandates and fast adoption of Industrie 4.0 solutions in manufacturing combine to accelerate spending on specialised security platforms. Demand concentrates on network-centric defences that safeguard operational technology, while quantum-safe cryptography investments signal long-term resilience priorities. Vendors offering hybrid cloud-edge security analytics gain traction as enterprises balance data-sovereignty rules with the need for scalable threat intelligence. Intensifying competition from niche start-ups and semiconductor players is prompting incumbents to acquire specialised capabilities, especially around AI-driven detection and secure-element design.

Key Report Takeaways

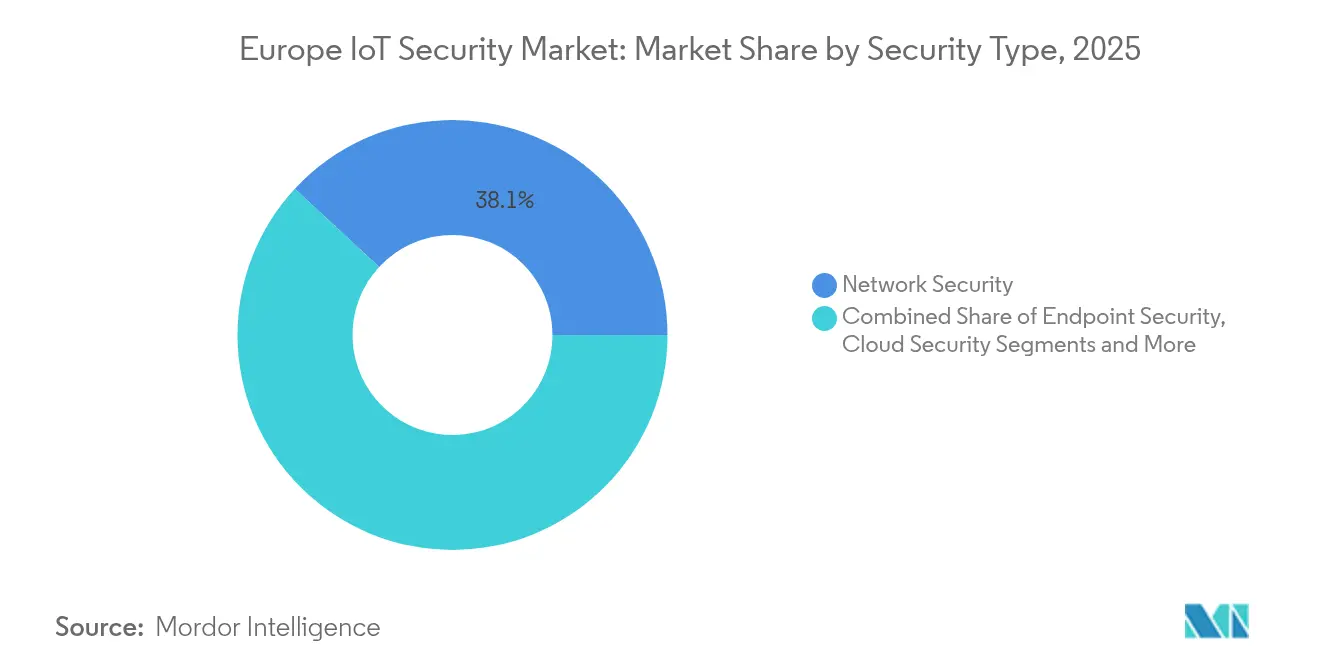

- By security type, Network Security led with 38.10% of the Europe IoT Security market share in 2025, while Cloud Security is projected to grow at 21.08% CAGR through 2031.

- By solution, Software accounted for 65.80% of the Europe IoT Security market size in 2025; Services record the highest forecast CAGR at 22.15% to 2031.

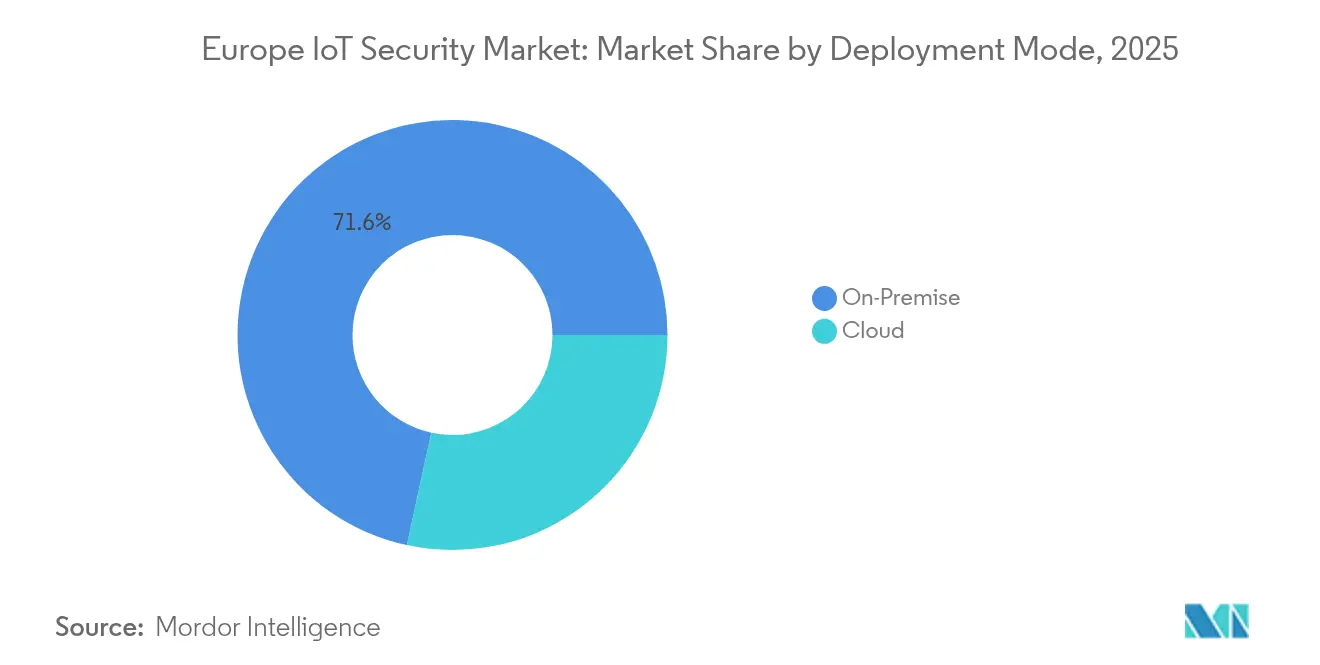

- By deployment mode, On-Premise installations held 71.60% revenue share in 2025, whereas Cloud deployment is advancing at 22.35% CAGR.

- By end-user industry, Manufacturing & Industrial commanded 35.70% share of the Europe IoT Security market size in 2025; Healthcare & Life Sciences is growing the fastest at 21.25% CAGR.

- By country, Germany captured 41.30% revenue share in 2025; the United Kingdom shows the strongest outlook with 21.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe IoT Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of IoT endpoints enlarging attack surface | +4.2% | Global | Medium term (2-4 years) |

| EU-wide data-protection mandates accelerating security spend | +5.8% | EU-wide | Short term (≤ 2 years) |

| Rapid industrial-IoT adoption in smart factories | +3.9% | Germany, France, Italy | Medium term (2-4 years) |

| Sophisticated cyber-attacks on critical infrastructure | +4.5% | Global, with focus on Western Europe | Short term (≤ 2 years) |

| Post-quantum-ready cryptography initiatives | +2.1% | EU-wide, with early adoption in France, Germany | Long term (≥ 4 years) |

| Horizon Europe and national grants subsidising SME security upgrades | +1.8% | EU-wide, particularly Central and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of IoT Endpoints Enlarging Attack Surface

European enterprises added millions of sensors, gateways and robotics units during 2024, driving a 107% spike in IoT-focused attacks. Manufacturing recorded more than 500 ransomware incidents that disrupted discrete production lines and forced costly downtime. Legacy brownfield machinery integrating with IP-based networks dissolves traditional perimeters, compelling CISOs to deploy scalable zero-trust agents and secured device-management overlays. Demand for endpoint protection platforms that remotely enforce firmware integrity and detect anomalous behaviour therefore rises across the Europe IoT Security market. Vendors that can monitor heterogeneous devices without impacting operational throughput gain competitive advantage among Industrie 4.0 adopters.

EU-wide Data-Protection Mandates Accelerating Security Spend

The NIS2 Directive, effective from October 2024, extended breach-reporting and risk-management obligations to about 350,000 European organisations[1]ENISA, “NIS2 Directive Explained,” enisa.europa.eu. Parallel enactment of the Cyber Resilience Act compels manufacturers to embed security-by-design and maintain software bills of materials, with fines reaching EUR 15 million. Healthcare and telecom operators in France already face active audits by ANSSI following several multi-million-record breaches during 2024. Compliance urgency is translating into immediate budget reallocations toward managed detection, vulnerability management and supply-chain assessment solutions, fuelling short-term growth across the Europe IoT Security market.

Rapid Industrial-IoT Adoption in Smart Factories

Germany’s Industrie 4.0 roadmap sustains annual digitalisation investments approaching EUR 40 billion, prompting factories to converge IT and OT environments. UN Regulation 155 on automotive cybersecurity further mandates secure software-update capabilities for vehicle manufacturers, magnifying demand for specialised OT firewalls, protocol-aware intrusion detection and digital-twin testing platforms. The EUR 33 million DAIS project illustrates the strategic push toward AI-enabled edge computing that processes industrial data locally, thereby reducing cloud exposure yet requiring robust on-premise cryptography.

Sophisticated Cyber-Attacks on Critical Infrastructure

Ransomware campaigns against European utilities grew 19% in 2023, with 80% of incidents inducing physical consequences from halted production to regional power outages. Investigations in Spain and Portugal into GPS spoofing and suspected sabotage underline the geopolitical stakes of IoT vulnerabilities. Governments now mandate real-time incident disclosure and advocate cyber-informed engineering approaches that embed security principles at design time. This heightens procurement of anomaly-based monitoring and secure-boot chipsets, propelling the Europe IoT Security market over the forecast horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented security standards across heterogeneous devices | -2.1% | EU-wide | Medium term (2-4 years) |

| High integration cost for legacy brown-field assets | -1.8% | Germany, France, Industrial regions | Long term (≥ 4 years) |

| Scarcity of IoT-security talent in European SMBs | -1.5% | EU-wide, particularly Central and Eastern Europe | Medium term (2-4 years) |

| Semiconductor supply-chain bottlenecks delaying secure-element roll-outs | -1.2% | Global, with EU dependency concerns | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Security Standards Across Heterogeneous Devices

While ETSI EN 303 645 defines baseline controls such as removal of default passwords, differing sectoral frameworks and national certification schemes add layers of complexity[2]ETSI, “EN 303 645 Consumer IoT Security Standard,” etsi.org. The forthcoming EU Cybersecurity Certification Scheme builds on Common Criteria but introduces new assurance classes, leaving SMEs juggling overlapping audits and spiralling consultancy fees. The SMESEC project found that 43% of attacks now target small businesses whose device portfolios span consumer and industrial categories, delaying large-scale security roll-outs.

High Integration Cost for Legacy Brown-Field Assets

Industrial plants operating machinery with decades-long lifecycles must retrofit security on protocols such as CAN or MVB that were never designed for authentication. Network segmentation gateways, secure protocol translators and bespoke firmware patches all command premium prices and specialist labour in short supply. European initiatives like VE-ASCOT underline the technical depth needed to build chains of trust inside semiconductor fabs, where downtime carries seven-figure hourly costs. High capital intensity therefore tempers adoption rates among mid-tier manufacturers and constrains portions of the Europe IoT Security market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Security Type: Network Dominance Meets Cloud Acceleration

Network Security generated 38.10% revenue in 2025, underlining its foundational role in isolating industrial traffic and enforcing least-privilege segmentation. Deep-packet inspection engines tuned for Modbus, PROFINET and OPC UA mitigate lateral movement risks across converged IT-OT backbones. Inside the Europe IoT Security market size for connectivity defences, protocol-aware threat analytics are expected to grow parallel to 5G private networks that connect autonomous mobile robots on factory floors. Cloud Security, although smaller today, grows at 21.08% CAGR as enterprises shift data pipelines to hyperscale and sovereign regional clouds. Secure access service edge (SASE) offerings that converge zero-trust networking and cloud-native firewalls rank high on 2025 procurement roadmaps, positioning Cloud Security to narrow the revenue gap before 2031.

Demand for Endpoint and Application Security follows the proliferation of smart cameras, wearable sensors and micro-services that require continuous software-integrity validation. Embedded or chip-level controls such as physically unclonable functions (PUFs) appear in new automotive and healthcare devices, with semiconductor programmes co-funded under the Important Project of Common European Interest (IPCEI) fuelling uptake. Vendors delivering holistic portfolios across these layers will capture a larger slice of the Europe IoT Security market.

By Solution: Software Leadership Versus Services Growth

Software accounted for 65.80% of total spending in 2025 because enterprises prefer licence-based analytics engines that scale across hundreds of thousands of devices. Behavioural anomaly detection, secure orchestration of firmware updates and cryptographic key-lifecycle management are increasingly delivered as containerised modules easy to deploy in Kubernetes clusters. Consequently, platform suppliers that package threat intelligence feeds and vulnerability scanners within a unified console retain high renewal rates across the Europe IoT Security market size.

Services, however, post the fastest 22.15% CAGR as SMEs lacking in-house specialists outsource threat hunting, incident response and compliance reporting. Managed security service providers (MSSPs) bundle 24×7 monitoring, penetration testing and regulatory gap assessments into subscription models attractive under tight capital budgets. Vendor-agnostic consultants that can integrate disparate security controls inside complex brownfield environments and document Cyber Resilience Act compliance are poised for sustained demand within the Europe IoT Security industry. Hardware sales remain steadier, anchored by trusted-platform modules and secure elements mandated for high-risk medical implants and automotive ECUs.

By Deployment Mode: On-Premise Prevalence Versus Cloud Migration

On-Premise solutions retained 71.60% market share in 2025, a reflection of strict EU data-protection norms and operational-safety priorities in critical infrastructure. Hospitals and energy plants insist on local packet inspection and offline patch repositories to guarantee deterministic latencies and regulatory auditability. Mature German manufacturers extend existing demilitarised zones with hardware isolation appliances rather than forwarding telemetry to external SOCs, preserving dominance of on-premise spending in the Europe IoT Security market share category.

Yet Cloud deployments are climbing at 22.35% CAGR. The European Cybersecurity Competence Centre has earmarked EUR 390 million for AI-based detection platforms under the Digital Europe Programme, accelerating research into scalable SaaS defences. Enterprises increasingly adopt hybrid blueprints in which edge gateways perform real-time filtering while metadata streams to regional clouds for heavy analytics. This dual-layer model strikes a balance between sovereignty and elasticity, expanding addressable revenue for cloud-native security startups within the Europe IoT Security market.

By End-User Industry: Manufacturing Leadership Versus Healthcare Surge

Manufacturing and Industrial verticals delivered 35.70% of 2025 revenue thanks to large-scale retrofits of robotics lines, connected CNC machinery and automated warehouses. NIS2 extends risk-management obligations deep into supply chains, compelling Tier-2 and Tier-3 suppliers to adopt unified security configurations or risk contract penalties. Consequently, platform vendors offering asset-discovery, protocol translation and secure remote maintenance unlock multi-plant roll-outs across the Europe IoT Security market.

Healthcare and Life Sciences grows fastest at 21.25% CAGR as hospitals digitise patient monitoring and tele-surgery. Over 581 cybersecurity incidents in the French health sector during 2024 prompted ANSSI to issue sector-specific guidelines that elevate demand for encrypted device-to-cloud connections and real-time anomaly detection. Medical Device Regulation provisions requiring security risk analysis throughout product lifecycles further stimulate uptake of chip-level secure boot and update validation. Transportation, Government and Defence, and Energy and Utilities each contribute steady growth trajectories, shaped by individual regulatory frameworks and national infrastructure-protection programmes.

Geography Analysis

Germany anchors the Europe IoT Security market through its 41.30% revenue share, sustained by EUR 9.2 billion cybersecurity outlays in 2023 that mirrored continued public concern around data sovereignty. Federal projects fostering Industrie 4.0 adoption commit roughly EUR 40 billion annually to digitalisation, translating into pervasive demand for OT-centric intrusion prevention and cryptographic firmware signing services. Deutsche Telekom’s expansion of managed IoT security products following revelations of extra-continental surveillance has heightened corporate investment readiness. As spending crosses EUR 10.3 billion in 2024, Germany remains the primary revenue and innovation hub inside the Europe IoT Security market.

The United Kingdom escalates its role by growing at 21.90% CAGR. Recent policy emphasis on digital-infrastructure autonomy drives aggressive roll-outs of sovereign SOC capabilities and quantum-safe pilot programmes across energy grids and rail signalling. The financial-services sector further catalyses secure API gateways for open banking and real-time fraud analytics, with regulatory backing from the Bank of England’s CBEST framework encouraging proactive cyber testing. This blend of policy momentum and sectoral urgency positions the UK as a pivotal growth catalyst for the broader Europe IoT Security market.

France blends state-driven initiatives with rising threat awareness to broaden uptake. The France 2030 plan finances start-ups in secure edge chiplets and post-quantum VPN stacks, while ANSSI wields audit authority across healthcare and telecoms following several headline breaches in 2024. Creation of INESIA, a national institute tasked with certifying AI systems, underscores governmental commitment to trustworthy automation. Growing ecosystem support across Bordeaux, Rennes and Sophia Antipolis tech clusters thus channels venture funding into niche IoT-security propositions that directly elevate the France component of the Europe IoT Security market.

Southern Europe follows, with Italy improving cyber-preparedness among automotive suppliers integrating UN Regulation 155, and Spain upgrading grid-security postures after high-profile outages linked to suspected sabotage. Meanwhile, the Nordics leverage advanced 5G uptake and government e-service penetration to pilot zero-trust architectures that will inform continent-wide standards harmonisation. Collectively, EU structural funds and horizon grants channelled into Central and Eastern Europe begin narrowing capability gaps, lifting adoption among SMEs and broadening the geographic base of the Europe IoT Security market.

Regulatory Landscape

The Europe IoT Security market operates under a tightening, product- and operator-facing regulatory stack led by the EU Cyber Resilience Act (CRA), Regulation (EU) 2024/2847, which entered into force on 10 December 2024 and sets horizontal cybersecurity requirements for products with digital elements placed on the EU market. A key near-term compliance anchor is 11 September 2026, when CRA incident and actively exploited vulnerability reporting obligations apply, pushing manufacturers and software suppliers to formalize disclosure workflows and telemetry-backed vulnerability handling aligned to EU reporting expectations.

The CRA is being operationalized through follow-on instruments and guidance that affect IoT product categorization, assurance, and update obligations. Commission Implementing Regulation (EU) 2025/2392 (adopted 28 November 2025) defines technical categories for important and critical products with digital elements, influencing conformity assessment depth and procurement screening. In May 2026, ENISA issued a draft technical advisory on secure update mechanisms, reinforcing practical controls such as integrity protection, secure distribution, and user notification, and shaping how vendors design firmware update and patch management capabilities.

Value Chain Analysis

The Europe IoT security value chain spans upstream security building blocks, including secure elements/TPMs, cryptographic libraries, and embedded OS components, through midstream platform layers such as device identity, key management, firmware update orchestration, network segmentation, and cloud/edge analytics. Downstream delivery is handled through MSSPs, systems integrators, telecom operators, and OEM channels that embed security into industrial, healthcare, automotive, and critical-infrastructure deployments. A distinctive Europe-specific layer is conformity assessment and compliance documentation, where notified bodies and testing labs interface with manufacturers to validate security-by-design controls and evidence packages under evolving EU requirements.

CRA deadlines are reshaping handoffs across the chain by increasing the importance of continuous vulnerability management, SBOM/VEX practices, and secure update supply chains that can support the 11 September 2026 reporting obligation and the broader transition to full CRA application from 11 December 2027. EU-funded initiatives such as the Horizon Europe DOSS project (Supply Trust Chain methodology using Device Security Passports based on OSCAL) indicate a shift toward machine-processable security evidence shared across component suppliers, OEMs, and assessors. At the same time, heterogeneous device fleets and semiconductor supply constraints keep secure-element rollouts and retrofit security projects dependent on close coordination between silicon vendors, firmware teams, and integrators supporting brownfield OT environments.

Competitive Landscape

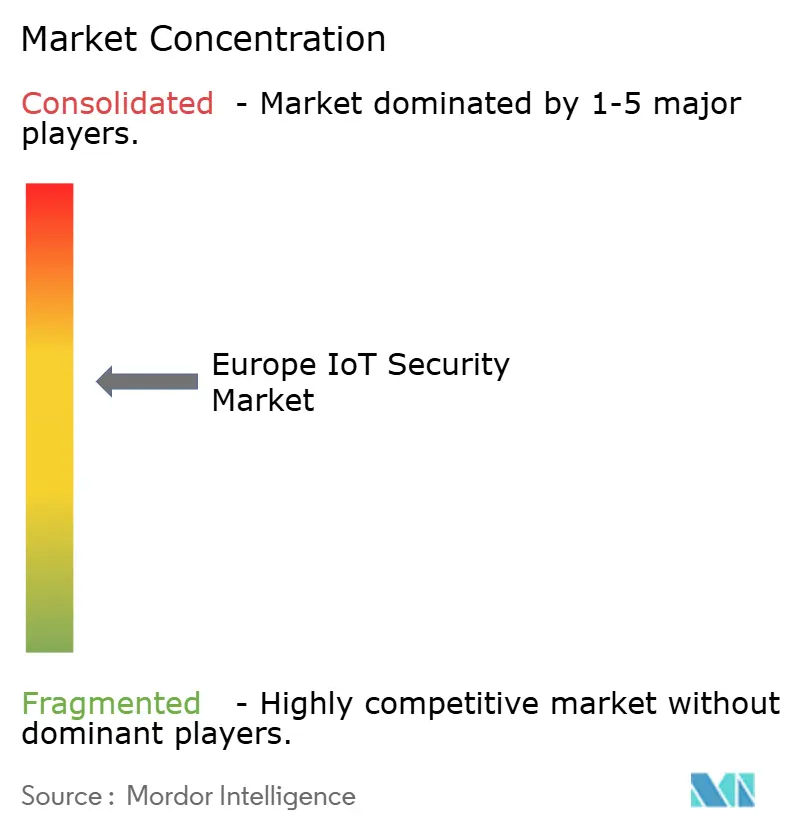

The regional landscape displays moderate concentration as large multi-national cybersecurity vendors extend established client relationships into IoT-specific offerings. Trend Micro, Cisco and Fortinet bundle endpoint detection, micro-segmentation and SOC orchestration into unified suites, leveraging global threat-intelligence infrastructures. Concurrently, semiconductor firms such as NXP and Infineon deepen their foothold by embedding secure-element IP into automotive and medical chips, often in co-development with OEMs to satisfy Cyber Resilience Act high-risk classifications. Partnerships typified by Crypto Quantique, ZARIOT and Kigen integrating quantum-safe roots-of-trust for cellular IoT illustrate collaborative innovation aimed at future-proofing devices.

Competitive intensity is amplified by venture-backed specialists targeting niche gaps. London-based qomodo secured USD 1.6 million in 2025 to refine platform-agnostic agents for extended IoT (XIoT) environments, emphasising AI-powered anomaly detection. Italian start-up Exein’s USD 15 million Series B funding expands secure OS components for robotic arms, reflecting investor interest in firmware-level defences tailored to industrial robotics. Meanwhile, managed service providers like AddSecure accelerate inorganic expansion, acquiring Netherlands-based Clifford Group to enter new verticals and supplement regional coverage.

Consolidation will likely continue as vendors seek scale, evidenced by Netmore’s acquisition of US-based Senet, which doubled its LoRa network and extended reach to 11 European markets. Top providers differentiate through AI-driven behavioural analytics, post-quantum key-management roadmaps and edge-to-cloud policy orchestration layers. Given steadily rising compliance thresholds and customer preference for single-pane-of-glass management, players capable of integrating device-level certificates with cloud-native SOCs maintain a defensible position in the Europe IoT Security market.

Europe IoT Security Industry Leaders

Symantec Corporation

Sophos Ltd.

IBM Corporation

Intel Corporation

Hewlett Packard Enterprise Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

CRA compliance milestones create near-term whitespace for platforms that operationalize product security into repeatable workflows, particularly tooling that connects device telemetry to vulnerability intake, SBOM management, and secure update enforcement to support the 11 September 2026 incident and vulnerability reporting requirement. Vendor offerings that package automated firmware vulnerability scanning, SBOM integration, and fleet-level remediation are being positioned as compliance enablers for device makers and operators managing large installed bases across manufacturing, healthcare, and critical infrastructure.

Connectivity and industrial automation programs are also opening opportunities at the intersection of telecom-grade identity and OT-grade security. Telefónica and Thales have launched a GSMA SGP.32-based global eSIM solution aimed at secure, multi-operator IoT connectivity, pointing to demand for standardized, policy-driven identity and lifecycle control in global deployments. In parallel, Siemens has introduced verified AI-driven cybersecurity capabilities for Industrial 5G within its Xcelerator portfolio aligned with IEC 62443, supporting buyers converging IT and OT networks and seeking scalable monitoring and segmentation controls that work across on-premise and hybrid architectures.

Recent Industry Developments

- July 2026: Nordic Semiconductor expanded nRF Cloud with automated firmware vulnerability scanning and SBOM integration aimed at helping device makers operationalize CRA-aligned monitoring and remediation. The release strengthens cloud-delivered device security management for fleets that need continuous software visibility and faster patch workflows as reporting obligations approach.

- December 2025: IBM was designated as a critical ICT third-party provider under the EU Digital Operational Resilience Act (DORA), bringing it under European Supervisory Authorities oversight for services used by the financial sector. The designation elevates assurance and audit expectations for large providers and reinforces demand for demonstrable controls across managed security and cloud-adjacent platforms used in regulated European environments.

- July 2024: IBM won a five-year USD 26 million USAID contract to support the Cybersecurity Protection and Response (CPR) program across Europe and Eurasia. The program strengthens regional incident response capacity and threat-handling practices, underpinning wider adoption of managed detection and response capabilities relevant to connected and critical digital infrastructure.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated in Europe from solutions and services that protect IoT devices, networks, and connected applications, including security that is deployed at the device, gateway, network, and cloud layers.

Scope exclusions: We exclude general enterprise IT security that is not tied to IoT environments and hardware-only device sales where no security software or security service revenue is attached.

Segmentation Overview

- By Security Type

- Network Security

- Endpoint Security

- Application Security

- Cloud Security

- Embedded/Chip-level Security

- Other Niche Security Types

- By Solution

- Hardware

- Software

- Services

- By Deployment Mode

- On-Premise

- Cloud

- By End-User Industry

- Automotive and Transportation

- Healthcare and Life Sciences

- Government and Defence

- Manufacturing and Industrial

- Energy and Utilities

- Other End-User Industries

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the guardrails for what gets counted and to anchor the model with public demand signals. We typically refer to sources such as the European Commission publications on cybersecurity policy, ENISA threat landscape work, Eurostat digital economy and ICT adoption series, and OECD digital security indicators to understand device growth and risk trends.

To further ground assumptions, we also review company annual reports and investor presentations, country-level cybersecurity agency updates, and credible press coverage on large IoT related incidents and compliance timelines. Where needed, a paid subscription covering company financials and another one covering patents were used to cross-check vendor exposure to IoT security and to track technology focus areas over time. These sources are illustrative only, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with a mix of security solution providers, managed security service teams, IoT platform stakeholders, telecom and connectivity ecosystem participants, and large end users deploying IoT at scale. Coverage was balanced across major European countries, and it was used to confirm adoption timing, typical pricing behavior, and which security layers are bought together versus sourced separately, before final assumptions were locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | |

| Mid tier: 59% | Functional/Unit leaders: 29% | |

| Smaller Players: 15% | Managers: 58% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where IoT device and connection footprints in Europe are translated into a secured-addressable demand pool using adoption rates by industry and deployment pattern. Once that demand pool is set, we apply solution mix and price logic across key security layers that are commonly procured for IoT environments, and then the totals are rebuilt country by country to ensure realistic regional distribution.

To keep the model practical, several inputs are tracked as checks, such as installed IoT device base growth, cloud versus on-premises security preference shifts, frequency of firmware and software update cycles, the share of deployments requiring identity and access controls, and average contract durations for managed security. Forecasts were developed using scenario analysis, where adoption and pricing paths are stress-tested with expert feedback, and then a single base case is selected for the report. Results are corroborated with selective bottom-up approximations, such as sampling vendor revenue exposure to IoT security, channel checks on managed service attach rates, and simple ASP x volume sanity tests, with gaps handled by using conservative ranges when primary inputs vary by country.

Data Validation & Update Cycle

Validation is done through multiple passes, starting with internal consistency checks across countries, security layers, and end-user group totals so the same demand is not counted twice. Outliers are reviewed against external signals like policy timelines, cyber incident intensity, and reported enterprise security spending direction, and then assumptions are re-checked with follow-up calls when the variance is material.

Before sign-off, a second analyst reviews the model logic, unit economics, and key drivers, and any changes are documented so the build stays repeatable. Reports refresh annually, and interim updates are made when major regulatory events, security incidents, or step-changes in IoT adoption materially shift the outlook. Right before delivery, a final quick refresh pass is completed so the published view reflects the latest available information.

Mordor Intelligence's Europe Internet of Things IOT Security Market Size Versus Other Published Estimates

Different published market sizes for Europe IoT security can vary a lot because each study draws the boundary differently and also chooses a different base year and forecast ramp. In this market, the biggest swings usually come from what is counted as IoT-specific security versus broader cybersecurity, plus how services and recurring cloud security are treated.

Enterprise IoT device base growth, country-level cybersecurity policy timelines, and interview-led checks on solution mix and service attach rates are the evidence points that keep Mordor Intelligence's estimate tied to IoT-specific security spending rather than overall IT security. Gaps also appear when some publishers assume faster price increases for cloud security, apply aggressive penetration in late-adopting industries, or do not clearly separate multi-year managed security contracts from one-time software deployments.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.66 B (2025) | |

| Regional Consultancy A | USD 4.31 B (2024) | Uses an earlier base year and a broader component split that can understate later-stage IoT security service revenue, especially where managed offerings are bundled inside wider IT security budgets. |

| Trade Journal B | USD 12.42 B (2026) | The 2026 figure is positioned as a single-point market value, and the definition appears to include a wider set of IoT security functions and applications, which can lift totals if adjacent cybersecurity spend is not cleanly excluded. |

Taken together, the spread is mainly explained by boundary choices, the year used for the headline number, and how recurring security services are recognized. By keeping the inputs traceable to device growth, adoption rates, and practical pricing checks, the sizing steps stay transparent and can be repeated when assumptions need to be updated.

Key Questions Answered in the Report

What is the current value of the Europe IoT Security market?

The market stands at USD 9.26 billion in 2026 and is projected to climb to USD 23.83 billion by 2031.

Which segment leads by security type?

Network Security leads with 38.10% revenue share, reflecting its critical role in safeguarding converged IT-OT environments.

Why is Healthcare the fastest-growing vertical?

Connected medical device uptake and strict patient-data regulations propel the vertical at a 21.25% CAGR, the highest among all industries.

Which country contributes the most revenue?

Germany commands 41.30% of regional spending due to strong Industrie 4.0 investments and the largest cybersecurity budget in Europe.

How do EU regulations influence spending?

Frameworks such as NIS2 and the Cyber Resilience Act impose mandatory risk management and security-by-design, immediately driving extra budget allocation across all sectors.

What technology trends will shape the market next?

Quantum-safe cryptography, AI-driven anomaly detection and secure edge computing are set to dominate R&D investment through 2030.

Page last updated on: