Electronics And Semicon Devices (ESD) Transport Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

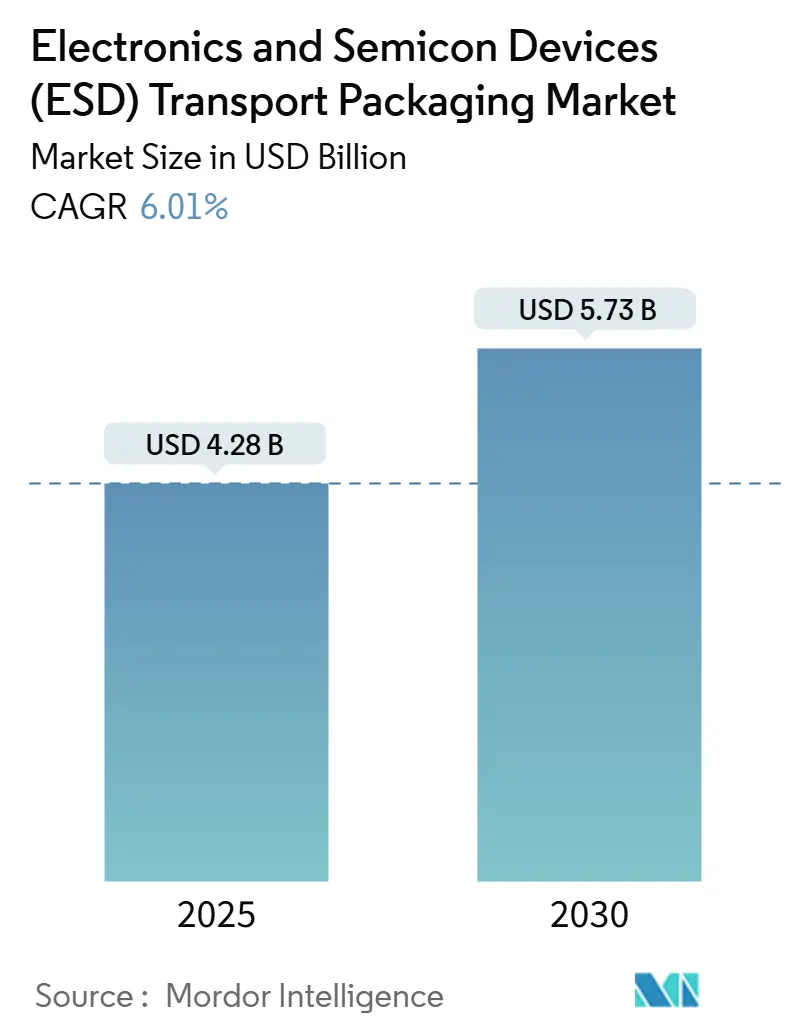

| Market Size (2025) | USD 4.28 Billion |

| Market Size (2030) | USD 5.73 Billion |

| Growth Rate (2025 - 2030) | 6.01% CAGR |

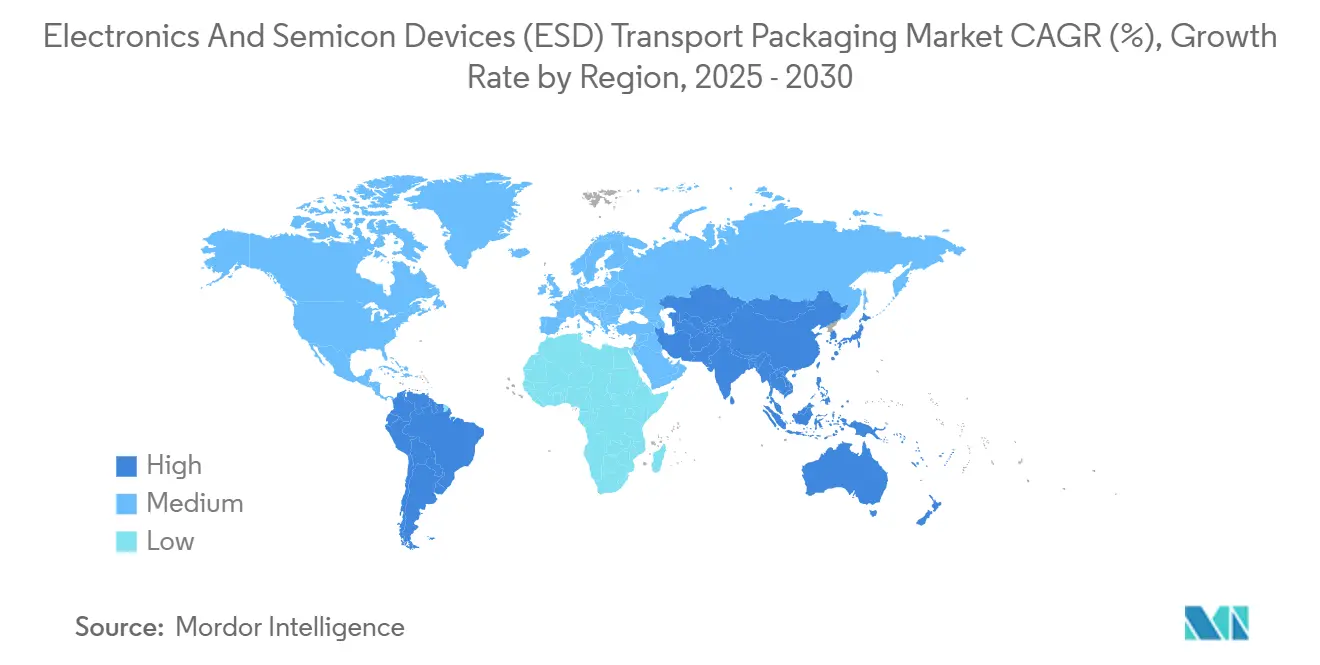

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronics And Semicon Devices (ESD) Transport Packaging Market Analysis by Mordor Intelligence

The electronics and semicon devices (ESD) transport packaging market size is valued at USD 4.28 billion in 2025 and is forecast to reach USD 5.73 billion in 2030, advancing at a 6.01% CAGR over the period. This acceleration reflects record fab construction, a wave of artificial-intelligence hardware rollouts, and tighter quality mandates that elevate demand for high-integrity static-shield solutions. Semiconductor makers now ship ultra-miniaturized 3 nm processors that require packaging with orders-of-magnitude tighter surface-resistivity safeguards, while automotive suppliers ramp wide-bandgap power devices that need robust shielding and thermal management. The global diversification of chip production, most visibly the simultaneous expansion of new fabs in India, Vietnam, and the United States, draws packaging providers closer to assembly lines, enabling just-in-time drop-ship models. Materials innovation is equally pivotal: metal-in-shield films and biodegradable conductive foams are penetrating new use cases as buyers balance ESD safety, sustainability, and electromagnetic interference mitigation. Competitive intensity remains moderate because scale, testing infrastructure, and certification breadth still limit fast entry; however, firms offering integrated sensor-embedded cartons or RFID-enabled traceability capture share as OEMs enforce zero-defect contracts.

Key Report Takeaways

- By product type, trays accounted for 38.26% of the electronics and semicon devices (ESD) transport packaging market share in 2024.

- By material type, the electronics and semicon devices (ESD) transport packaging market size for metal-in shield films is forecast to post the fastest growth at a 7.31% CAGR through 2030.

- By end-user industry, consumer electronics held 36.01% of the electronics and semicon devices (ESD) transport packaging market share in 2024.

- By geography, the electronics and semicon devices (ESD) transport packaging market size for South America is on track to grow at the strongest 7.81% CAGR through 2030.

Global Electronics And Semicon Devices (ESD) Transport Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for ultra-miniaturized ICs driving stringent ESD integrity in logistics | +1.2% | Global with Asia-Pacific core | Medium term (2-4 years) |

| Rapid fab expansion in India and Vietnam creating green-field packaging demand | +0.8% | Asia-Pacific emerging hubs, spillover to Middle East and Africa | Short term (≤ 2 years) |

| OEM-mandated zero-defect supply contracts elevating specialty packaging adoption | +1.0% | Global with North America and Europe leadership | Medium term (2-4 years) |

| Rise of automotive SiC and GaN power devices needing higher shielding levels | +0.9% | Automotive hubs in Germany, Japan, China | Long term (≥ 4 years) |

| Government-funded chip-resilience programmes subsidising domestic ESD supply chains | +0.7% | North America, Europe, selective Asia-Pacific | Medium term (2-4 years) |

| Industry pivot to direct-to-foundry drop-ship models shortening packaging cycles | +0.6% | Global manufacturing regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Ultra-Miniaturized ICs Driving Stringent ESD Integrity in Logistics

Ever-smaller node geometries make modern processors acutely vulnerable to latent electrostatic events, compelling semiconductor firms to specify packaging whose surface resistivity is an order tighter than the previous generation. The 2024 ESD Association roadmap identifies packaging weaknesses as a primary bottleneck for 3 nm and future stacked-chip architectures, particularly those powering hyperscale data center AI accelerators. Device makers, therefore, adopt multi-zone cartons that isolate dies with differing voltage tolerances while embedding sensor strips that record charge exposure in transit, ensuring warranty compliance once parts reach contract assemblers. Premium cost acceptance is highest in data-center and automotive safety-critical lines, where component values outweigh packaging outlays.

Rapid Fab Expansion in India and Vietnam Creating Green-Field Packaging Demand

India’s USD 10 billion incentive program, coupled with Micron’s USD 2.75 billion assembly hub in Gujarat, catalyzes a supplier ecosystem that includes localized ESD foam, tray, and metal-in-pouch production.[1]Micron Technology, “Micron Announces Investment in Gujarat, India to Build New Semiconductor Assembly and Test Facility,” MICRON.COM Vietnam attracts parallel investment as Intel enlarges its assembly capacity, forming electronics and semicon devices (ESD) transport packaging market clusters near Ho Chi Minh City that shorten lead times for foundries. Providers establishing facilities within these industrial parks gain freight savings and quicker prototype validation, features valued by new fabs that lack legacy supplier ties.

OEM-Mandated Zero-Defect Supply Contracts Elevating Specialty Packaging Adoption

Automotive and consumer-electronics leaders hardened procurement rules after the 2021-2023 chip shortage, shifting performance liability onto tier-one suppliers. Contracts now embed six-sigma escape-rate clauses and require blockchain-logged traceability of carton integrity. Packaging lines integrate inline optical inspection, humidity sensors, and RFID tags that upload condition data to cloud dashboards, allowing buyers like Tesla to quarantine suspect lots before board-mounting. Providers that can certify zero-defect lanes secure multiyear volume locks, squeezing incumbents with older equipment.

Rise of Automotive SiC and GaN Power Devices Needing Higher Shielding Levels

Electric-vehicle platforms adopting 800 V architectures rely on SiC and GaN transistors that must tolerate up to 8 kV static events. Conventional dissipative bags insufficiently shield devices during maritime shipping, pushing engineers toward co-extruded metal-in films with dual ESD-and-EMI layers plus thermal-absorbent liners. Research published in 2024 confirmed that composite foil pouches reduce device failure rates by 38% compared to plain conductive plastic when exposed to simulated rail vibrations and coastal humidity.[2]IEEE Authors, “ESD Protection for Wide Bandgap Power Devices in Automotive Applications,” IEEEXPLORE.IEEE.ORG As automakers align on common wide-bandgap specifications, volume orders for these hybrid materials accelerate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of conductive polymer resins | -0.4% | Global with acute impact on cost-sensitive lines | Short term (≤ 2 years) |

| Recycling complexity of multi-layer static-shield pouches | -0.3% | Europe and North America due to regulatory pressure | Medium term (2-4 years) |

| Limited standardisation across regional compliance codes | -0.2% | Global with fragmentation between JEDEC and IEC regions | Long term (≥ 4 years) |

| Supply shortages of carbon black and intrinsically conductive fibres | -0.5% | Global, especially Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Conductive Polymer Resins

A handful of upstream suppliers control specialty conductive additives, resulting in frequent quarter-over-quarter price swings of 15-25% that small packaging firms struggle to absorb. Visibility remains low because capacity expansions lag petrochemical demand, and emerging bio-based fillers command premiums but lack proven consistency. This volatility forces mid-tier converters to hedge their purchases or seek pass-through clauses, eroding competitiveness where consumer electronics clients emphasize cost.

Recycling Complexity of Multi-Layer Static-Shield Pouches

European and U.S. recyclability directives pressure electronics brands to reduce landfill waste, yet most static-shield bags combine metal-in layers, adhesives, and colored polymers that complicate material separation. Extended producer responsibility fees incentivize mono-material alternatives, but these often compromise the moisture-barrier ratings required for high-reliability integrated circuits.[3]JEDEC Committee, “JEDEC Standards Documents,” JEDEC.ORG Packaging vendors invest in reversible lamination processes and take-back programs, yet adoption remains slow, given higher unit costs and limited downstream recycling infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Foam Innovations Drive Protective Packaging Evolution

Trays accounted for 38.26% of 2024 revenue as fabs continue to rely on stackable, chip-level carriers that maintain positional accuracy during robotic handling. The electronics and semicon devices (ESD) transport packaging market sees foams sprint ahead at an 8.04% CAGR because polyurethane formulations now incorporate vapor-phase corrosion inhibitors alongside static-dissipative agents, safeguarding both copper pillars and delicate solder balls. EcoSonic biodegradable foam, launched in 2024, demonstrates the commercial viability of such multi-function solutions. As buyers seek sustainability without performance trade-offs, foam converts experiment with starch-based resins that meet automotive flammability codes.

Demand for bags and pouches remains steady in consumer electronics service centers, where single-board computers and smartphone modules are shipped in bulk. Boxes and containers expand within industrial drives and telecom-infrastructure lanes that require rugged corner crush strengths and humidity control during ocean freight. The electronics and semicon devices (ESD) transport packaging market thus witnesses suppliers bundling kits trays inside antistatic boxes lined with moisture-indicator cards to present turnkey drop-ship formats that bypass central distribution.

By Material Type: Metal-In Shield Films Capture Advanced Packaging Growth

Conductive plastics held a 42.51% share in 2024, as their formulation flexibility allows manufacturers to mold totes, reels, and tapes in high volumes with predictable resistivity. Yet, as 5G radios and autonomous-vehicle lidar modules converge, ESD and EMI concerns, metal-in-shield films surge at a 7.31% CAGR, lifting their slice of the electronics and semicon devices (ESD) transport packaging market size. These laminate structures layer vapor-deposited aluminum between dissipative polyolefins, creating Faraday-cage performance in packages thinner than 75 µm.

Dissipative plastics serve niches such as surgical robotics, where a slow bleed-off prevents arcing. Conductive paper, although attractive for its recyclability, is often used in lower-value aftermarket parts because moisture absorption compromises high-frequency semiconductor wafers. Suppliers nonetheless co-develop paper-based totes with silicone coatings to chase European environment credits, a sign the electronics and semicon devices (ESD) transport packaging industry is increasingly merging material science with regulatory foresight.

By End-User Industry: Automotive Electronics Accelerate ESD Protection Demand

Consumer electronics accounted for the largest 36.01% share of 2024 revenue, driven by unrelenting smartphone and laptop shipments. Standardized pink static bags and injection-molded clamshells still dominate because cost per unit overrides ultra-low failure-rate requirements. Conversely, automotive electronics advance at a 7.29% CAGR as each electric vehicle integrates multiple powertrain inverters, battery-management boards, advanced driver-assistance radar, and cockpit infotainment SOCs. These densely packed modules raise the electronics and semicon devices (ESD) transport packaging market share allocated to higher-spec cartons that also resist temperature swings from -40 °C to 125 °C.

Industrial electronics utilize reinforced corrugated boxes with internal foam cushioning for programmable logic controllers and factory automation drives. Aerospace and defence customers pay premiums for metal-lined bins certified under MIL-PRF-81705, demanding triple-bag sequences inside humidity-indicator desiccant canisters. Healthcare device makers procure sterilizable clamshells that survive gamma irradiation, reflecting the breadth of performance windows required across the electronics and semicon devices (ESD) transport packaging market.

Geography Analysis

The Asia-Pacific region retained 54.31% of 2024 revenue, led by Taiwan Semiconductor Manufacturing Company, Samsung, and SK Hynix, which ramped up advanced-node production lines that procure millions of pocketed waffle trays monthly. The electronics and semicon devices (ESD) transport packaging market size in the region benefits from vertically integrated plastics, film, and foam supply chains that compress lead times. China’s Phase III National IC Fund allocation of USD 47.5 billion extends subsidy coverage to auxiliary materials, encouraging domestic converters to localize the fabrication of antistatic bags. India and Vietnam are expected to add incremental demand as their first generation of fabs opens between 2025 and 2027, prompting packaging firms from Malaysia and Singapore to set up satellite plants for overnight cross-border truck deliveries.

South America is expected to register the fastest growth rate of 7.81% from 2020 to 2030. Brazil’s Manaus Industrial Pole offers tax incentives that attract contract manufacturers of set-top boxes, telecom switches, and automotive dashboards, each of which requires ESD-safe kitting. Argentina’s Tierra del Fuego cluster sources conductive foam for extended-distance shipments that endure both Atlantic humidity and rugged road transit to final assembly. The electronics and semicon devices (ESD) transport packaging market thus expands alongside regional electronics portfolios even as macroeconomic swings periodically slow discretionary production.

North America and Europe maintain mature yet innovation-oriented bases. The United States CHIPS and Science Act stimulates onshoring of advanced-packaging lines, directly lifting demand for trays compatible with high-density fan-out wafer-level packaging. The European Chips Act funds pilot lines in Germany and France, where automakers test integrated ESD-and-EMI cartons tailored to SiC power modules. Environmental regulations also catalyze recyclable-film development, compressing time-to-market for mono-material solutions capable of matching legacy shielding benchmarks.

Competitive Landscape

The electronics and semicon devices (ESD) transport packaging market remains moderately fragmented. Global multinationals, such as Sealed Air Corporation and 3M, leverage broad portfolios and testing laboratories to service tier-one OEMs across three continents, while regionally focused specialists, like Desco Industries and Botron, differentiate themselves through customized foam inserts and rapid prototyping. Intellectual property filings focus on composite shield films and sensorized cartons; the United States Patent and Trademark Office reported a 22% increase in ESD packaging patents in 2024. Providers capable of embedding humidity, shock, and charge sensors within cartons gain share as zero-defect clauses become procurement norm.

Mergers center on filling portfolio gaps: Sealed Air acquired a European static-shield film maker for USD 85 million in June 2024 to expand its automotive coverage, while mid-cap converters form joint ventures in Vietnam to secure proximity to Intel’s new test lines. Material innovation shapes differentiation. 3M’s metal-oxide-infused polymer films pass both JEDEC and IEC discharge tests at thinner gauges, cutting plastic use by 18% per bag, an advantage with European eco-taxes looming. Foam suppliers collaborate with corrosion-inhibitor chemists to develop multi-functional pads ideal for copper-pillar chiplets targeting data center AI boards.

Certification across both JEDEC JESD 625-B and IEC 61340 series costs upward of USD 0.5 million per product line, deterring small entrants. Capital-intensive inline inspection machine-vision scanners, Faraday cage test chambers, and traceability software further raise breakeven volume thresholds. Nonetheless, demand niches emerge. Direct-to-foundry logistics models reward vendors that can operate consignment hubs adjacent to clean rooms, reducing in-process inventory while guaranteeing component integrity.

Electronics And Semicon Devices (ESD) Transport Packaging Industry Leaders

Sealed Air Corporation

Smurfit Westrock plc

Conductive Containers Inc.

Storopack Hans Reichenecker GmbH

Botron Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: TSMC announced a 60% expansion of its CoWoS advanced-packaging capacity to meet surging AI chip demand, creating substantial downstream demand for specialized ESD solutions capable of protecting complex multi-chiplet assemblies during transport and storage phases.

- September 2024: Cortec Corporation launched EcoSonic foam packaging technology, combining biodegradable materials with enhanced ESD protection capabilities specifically designed for automotive electronics applications requiring environmental compliance and superior static-discharge protection.

- August 2024: Micron Technology broke ground on its USD 2.75 billion semiconductor assembly and test facility in Gujarat, India, representing the first major greenfield investment that will require comprehensive ESD-packaging infrastructure development to support both domestic and export markets.

- July 2024: 3M Company received FDA approval for its medical-grade ESD packaging materials designed for implantable-device manufacturing, expanding the company’s addressable market into high-value healthcare applications with stringent biocompatibility requirements.

Global Electronics And Semicon Devices (ESD) Transport Packaging Market Report Scope

| Trays |

| Bags and Pouches |

| Foams |

| Boxes and Containers |

| Tapes and Labels |

| Conductive Plastics |

| Dissipative Plastics |

| Conductive Paper and Fibreboard |

| Metal-in Shield Films |

| Consumer Electronics |

| Automotive Electronics |

| Industrial Electronics |

| Aerospace and Defence |

| Healthcare Devices |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Trays | ||

| Bags and Pouches | |||

| Foams | |||

| Boxes and Containers | |||

| Tapes and Labels | |||

| By Material Type | Conductive Plastics | ||

| Dissipative Plastics | |||

| Conductive Paper and Fibreboard | |||

| Metal-in Shield Films | |||

| By End-User Industry | Consumer Electronics | ||

| Automotive Electronics | |||

| Industrial Electronics | |||

| Aerospace and Defence | |||

| Healthcare Devices | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the electronics and semicon devices (ESD) transport packaging market in 2030?

The market is forecast to reach USD 5.73 billion by 2030, reflecting a 6.01% CAGR from 2025.

Which product category is growing fastest in ESD packaging?

Foams lead growth with an 8.04% CAGR, driven by biodegradable and corrosion-inhibiting innovations.

Why is South America considered an emerging hotspot for ESD packaging?

Supply-chain diversification draws electronics assembly to Brazil and Argentina, pushing regional packaging demand to a 7.81% CAGR.

How are zero-defect supply contracts changing the sector?

OEMs now require sensor-equipped, traceable cartons that prove ESD integrity, favoring suppliers with advanced quality systems.

Which material is gaining traction for 5G and electric-vehicle applications?

Metal-in shield films combine ESD and EMI protection and are expanding at a 7.31% CAGR through 2030.

What sustainability challenges face multi-layer static-shield pouches?

Their mixed-material construction complicates recycling, prompting research into mono-material alternatives and take-back schemes.

Page last updated on: