Market Overview

| Study Period | 2020 - 2031 |

|---|---|

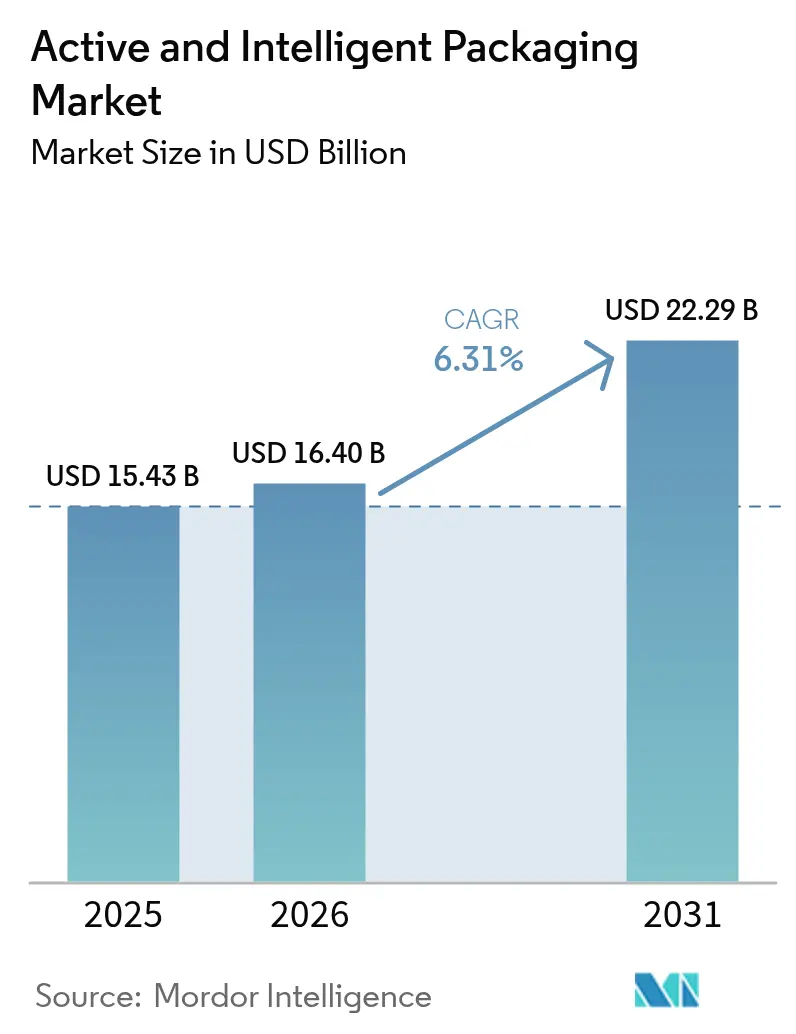

| Market Size (2026) | USD 16.4 Billion |

| Market Size (2031) | USD 22.29 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

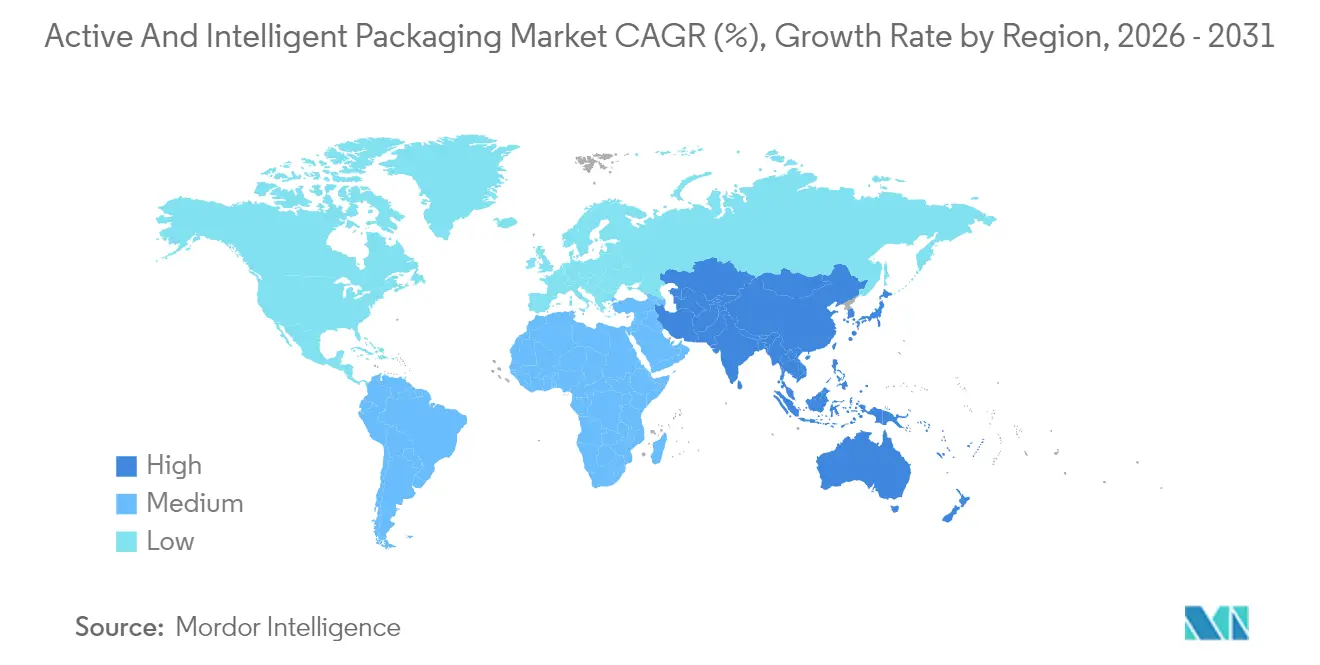

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Active And Intelligent Packaging Market Analysis by Mordor Intelligence

The active and intelligent packaging market size in 2026 is estimated at USD 16.4 billion, growing from 2025 value of USD 15.43 billion with 2031 projections showing USD 22.29 billion, growing at 6.31% CAGR over 2026-2031. Sustained adoption across food, pharmaceutical, and industrial supply chains underpins this momentum as manufacturers shift from passive barrier structures to solutions that sense or respond to their environment. Supermarket chains are rolling out oxygen-scavenging film to curb spoilage, pharmaceutical firms are embedding RFID inlays to comply with serialization 2.0, and e-commerce grocery platforms are specifying smart labels that flag temperature abuse in real time. Brand owners view these functions as insurance against reputational damage and recall costs, so demand continues even when resin prices fluctuate. The pivot also dovetails with legislation phasing down single-use plastics, motivating companies to pursue thinner smart laminates that deliver equivalent or better product protection.

Key Report Takeaways

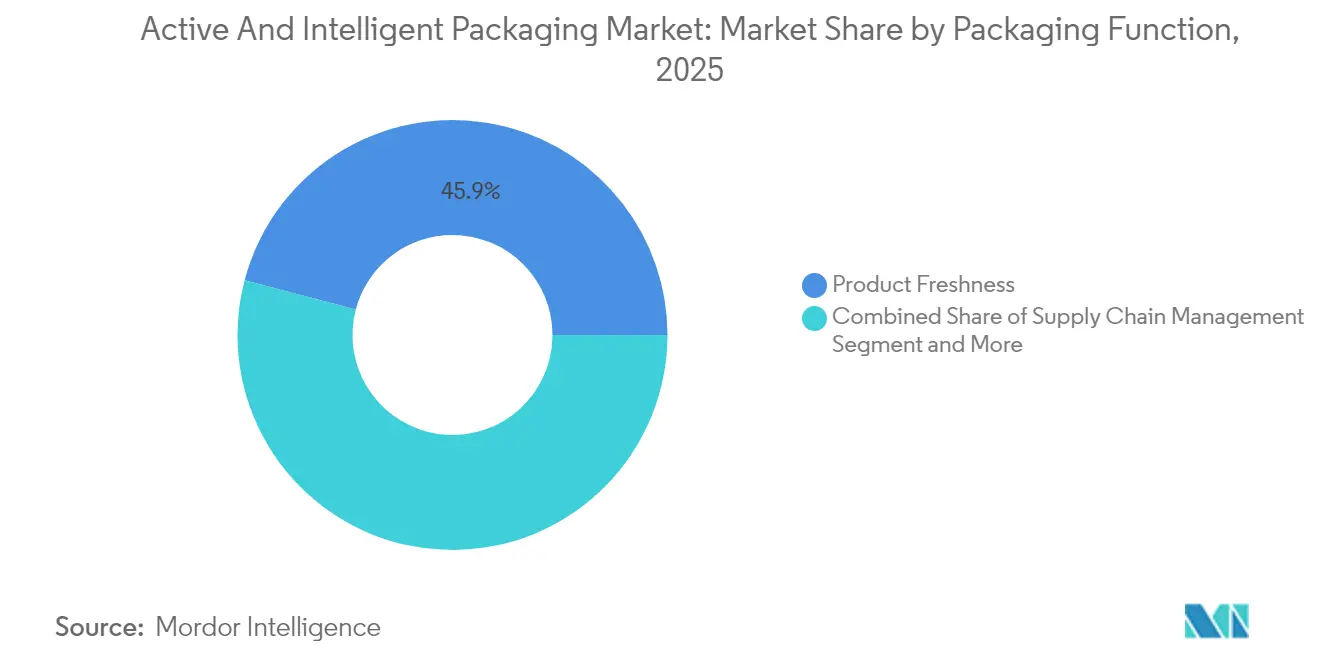

- By packaging function, product freshness captured 45.90% of the active and intelligent packaging market share in 2025, whereas the brand protection segment is projected to grow at an 8.42% CAGR between 2026-2031.

- By packaging technology, the active packaging segment captured 62.70% of the active and intelligent packaging market share in 2025, whereas the intelligent packaging segment is projected to grow at a 7.56% CAGR between 2026-2031.

- By active packaging type, gas scavengers captured 37.65% of the active packaging market size in 2025. The moisture scavengers segment is projected to grow at a 7.98% CAGR between 2026-2031.

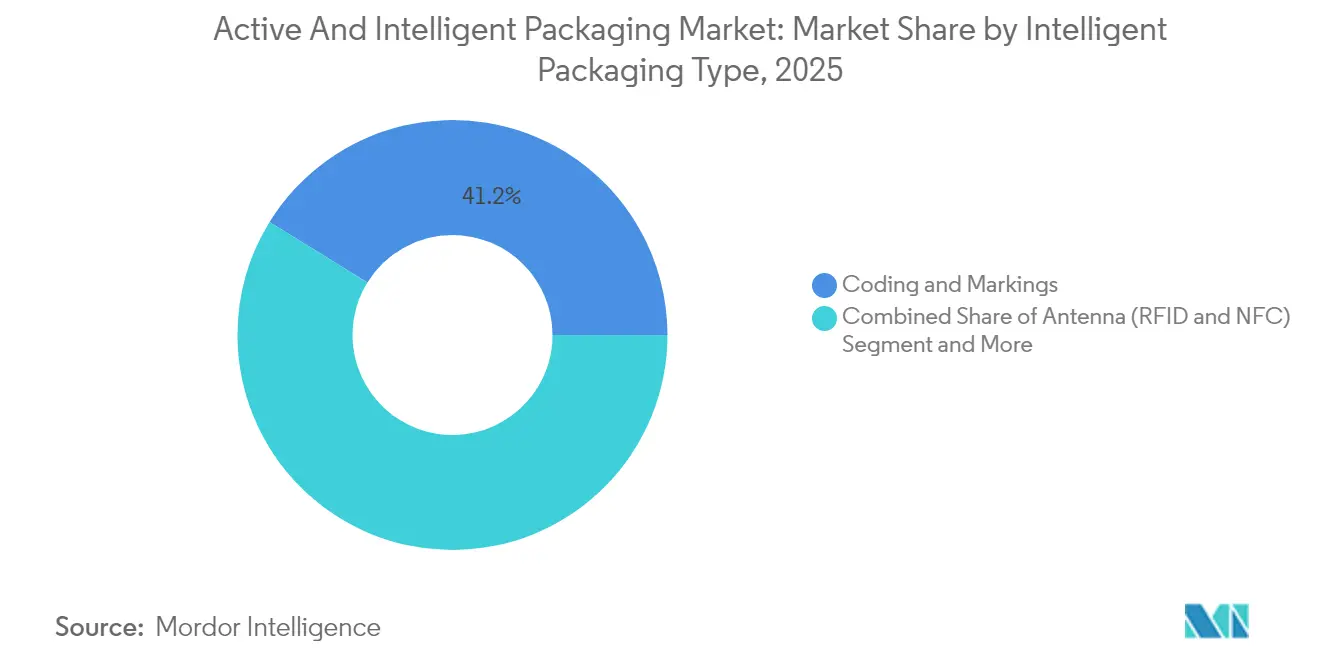

- By intelligent packaging type, coding and markings captured 41.20% of the intelligent packaging market size in 2025. The antenna (RFID and NFC) segment is projected to grow at a 9.02% CAGR between 2026-2031.

- By end-user industry, the food segment captured 35.20% of the intelligent packaging market size in 2025, whereas the pharmaceuticals segment is projected to grow at a 7.23% CAGR between 2026-2031.

- By geography, North America captured 34.00% of the intelligent packaging market size in 2025, and Asia-Pacific is projected to grow at a 9.45% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Active And Intelligent Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supermarket Demand for Longer Shelf-Life Fresh Produce | +1.8% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Brand-Owner Push for Real-Time Cold-Chain Visibility | +1.5% | Global, spill-over to emerging markets | Short term (≤ 2 years) |

| Regulatory Shift Toward Single-Use Plastic Reduction | +1.2% | Europe, North America, APAC core markets | Long term (≥ 4 years) |

| E-Commerce Boom Creating Last-Mile Freshness Challenges | +1.0% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Integration of Printed Electronics in Flexible Films | +0.7% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Pharmaceutical Serialization 2.0 Mandates | +0.6% | Global, regulatory compliance-driven | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supermarket Demand for Longer Shelf-Life Fresh Produce

Large grocery chains reported 15-25% spoilage reduction after adopting oxygen and moisture scavengers, translating into better margins and fewer out-of-stocks.[1]Journal of Food Engineering editorial board, “Active Packaging Performance in Supermarket Supply Chains,” sciencedirect.com Enzymatic scavengers activate only in the presence of oxygen, so the package headspace remains balanced throughout distribution. Multiple retailers are now integrating smart indicators that change color once scavenger capacity is exhausted, giving store associates a visual cue for stock rotation. FDA and EFSA approvals of newer iron-polymer composites accelerated commercial launch schedules, while in-line sachet placement equipment lowered changeover time on high-speed lines. The benefit is most pronounced in regions with long distribution distances, such as North America, yet adoption is expanding in Europe and urban Asia as retailers target waste reduction mandates.

Brand-Owner Push for Real-Time Cold-Chain Visibility

RFID-enabled temperature loggers capable of ±0.5 °C accuracy record data every five minutes, providing granular thermal histories for vaccines and biologics.[2]U.S. Food and Drug Administration, “Regulatory Information: Guidance Documents,” fda.gov Pharmaceutical companies integrate these logs with cloud platforms that send automatic alerts when cumulative thermal exposure reaches warning thresholds. Food brands are following suit in frozen desserts and seafood, leveraging predictive analytics to reroute at-risk pallets before quality deteriorates. Capital outlays are declining as tag costs fall below USD 0.05, making item-level deployment feasible for high-value SKUs. The business case hinges on recall avoidance rather than pure logistics optimization, so ROI remains compelling even under conservative spoilage assumptions.

Regulatory Shift Toward Single-Use Plastic Reduction

California’s SB 54 targets a 65% cut in single-use packaging by 2032, prompting brands to substitute conventional rigid tubs with thinner smart films outfitted with freshness indicators. The European Union’s directive spurred commercial trials of compostable NFC tags produced on cellulose substrates that disintegrate in industrial composters within 180 days. Certification under ISO 17088 is emerging as a procurement prerequisite for multinational grocery chains. Concurrently, Asia-Pacific nations such as Japan are testing laser-etched smart codes that eliminate adhesive labels, trimming overall material intensity. These policy signals are shifting R&D budgets toward high-function, low-mass laminates.

E-Commerce Boom Creating Last-Mile Freshness Challenges

Meal-kit providers now ship proteins across multiple temperature zones, so phase-change liners paired with time-temperature integrators mitigate spoilage in extended delivery windows. IoT gateways embedded in parcel lockers relay condition data to customer smartphones, allowing refusal of compromised shipments. Urban micro-fulfillment centers analyze aggregated excursion data to fine-tune route planning, thereby cutting dry-ice consumption. Smaller local brands piggyback on third-party logistics platforms that offer smart-label options as a value-added service. As same-day grocery delivery expands to second-tier cities, demand for affordable freshness monitoring is scaling quickly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Equipment and Retrofit Costs | -1.4% | Global, particularly emerging markets | Medium term (2-4 years) |

| Human Toxicology Concerns around Scavenger Chemistries | -0.9% | Global, regulatory oversight intensive | Long term (≥ 4 years) |

| Fragmented Recycling Infrastructure for Smart Labels | -0.7% | Europe, North America, spill-over to APAC | Long term (≥ 4 years) |

| Semiconductor Supply Bottlenecks for RFID Inlays | -0.5% | Global, concentrated in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Equipment and Retrofit Costs

A mid-sized converter spends USD 2-8 million to add multilane oxygen-scavenger insertion systems, vision inspection, and RFID encoding stations.[3]U.S. Securities and Exchange Commission, “Amcor plc Form 10-K 2025,” sec.gov Payback stretches past four years if output volumes stay modest, so small firms often postpone investment. Financing options remain limited in emerging markets, where commercial lenders perceive smart-pack assets as niche collateral. Training expenses further inflate capital outlays because technicians must master both packaging mechanics and electronics troubleshooting. OEMs are responding with modular retrofits that clip onto existing form-fill-seal machines, lowering entry thresholds but still leaving a sizable cash hurdle.

Human Toxicology Concerns around Scavenger Chemistries

EFSA and FDA require exhaustive migration studies before new scavenger formulations reach the market, a process that can span 18-24 months and cost over USD 1 million. Consumer watchdogs scrutinize iron-based systems for possible metal leaching, prompting retailers to favor enzymatic alternatives despite higher unit costs. As analytical instruments become more sensitive, permissible exposure limits may tighten further, prolonging dossier preparation. Start-ups sometimes pivot away from direct-food contact applications toward secondary packaging to sidestep these hurdles. The perception of chemical risk slows speed-to-market for innovative actives, particularly in baby food and nutraceutical categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Function: Product Freshness Drives Innovation

Product freshness applications captured 45.90% share of the active and intelligent packaging market in 2025, underscoring the premium retailers' place on extending perishable shelf life. This dominance reflects the broad utility of oxygen scavengers, moisture absorbers, and ethylene inhibitors that operate without power and integrate easily into existing lines. The active and intelligent packaging market size for freshness solutions is forecast to grow toward USD 10.23 billion by 2031, propelled by stricter waste-reduction targets in North America and Europe. Retailers' benchmarking shrink rates are assigning cost savings directly to active formats, drawing follow-on investment from produce packers seeking preferred-supplier status. Consumer behavior aligns with this priority as surveys indicate freshness is the top driver of repeat purchase across refrigerated categories.

The fastest-growing functional segment is brand protection at an 8.42% CAGR, buoyed by counterfeit risks in pharmaceuticals and luxury cosmetics. NFC tags embedded under tamper-evident seals enable one-tap authentication, while UV-responsive inks add covert security layers. Global authorities confiscated fake drugs, intensifying pressure on legitimate manufacturers to safeguard supply chains. By integrating serialized identifiers with cloud dashboards, companies gain real-time diversion alerts and market intelligence on gray-market flows. These combined dynamics position freshness and security as dual pillars of functional demand, ensuring diversified revenue streams for solution providers.

By Packaging Technology: Active Solutions Lead Market

Active technologies held a 62.70% share in 2025 as its passive mode of action suits high-volume commodities. They require no batteries and minimal supply-chain modification, reducing implementation friction. Iron-based scavengers remain cost leaders at less than USD 0.02 per sachet, sustaining uptake in value-driven segments such as bakery and snack foods. The active and intelligent packaging market is witnessing hybridization, with active films now incorporating printed temperature strips that darken after cumulative exposure thresholds. Intelligent technologies, although on a smaller base, are advancing at a 7.56% CAGR as unit economics improve and 5G connectivity lowers data-transmission costs.

Emerging printed-electronics platforms blur the lines between the two camps. Roll-to-roll gravure presses can deposit conductive traces alongside gas-absorbing chemistries in a single pass, creating self-regulating packs that vent CO₂ when fermentation begins. Standards bodies like ISO 15378 are updating guidance to cover such multifunctional constructs, giving early movers regulatory clarity. This convergence widens the moat for converters with both chemistry and electronics expertise, reinforcing the competitive advantage of integrated players in the active and intelligent packaging market.

By Active Packaging Type: Gas Scavengers Dominate Applications

Gas scavengers represented 37.65% of segment revenue in 2025, largely due to their versatility across meats, snacks, and pharmaceuticals. Oxygen scavengers, the flagship subset, prevent lipid oxidation and microbial growth, extending ambient shelf life by up to 12 months in some dry snack formats. The active and intelligent packaging market share for scavengers remains resilient because performance is quantifiable through headspace analysis, simplifying ROI calculations. Moisture scavengers follow closely, riding a wave of demand in electronics and powdered nutraceuticals where humidity compromises efficacy.

Microwave susceptors continue serving ready-meal niches but face substitution from ovenable barrier trays that eliminate ancillary films. Innovation in polymer-integrated scavengers is cutting out sachets altogether, pleasing brand managers keen on uncluttered pack aesthetics. Patent filings surged 18% in 2024, emphasizing polymer-matrix solutions that generate no loose components, thereby reducing FOD (foreign-object debris) risk on high-speed lines.

By Intelligent Packaging Type: Digital Integration Accelerates

Coding and markings commanded a 41.20% share because infrastructure exists worldwide to read barcodes and QR codes. Brands employ dynamic QR links that update provenance or promotional content without reprinting, maximizing post-launch agility. The active and intelligent packaging industry leverages these low-cost gateways to transition consumers toward richer NFC-based interactions. Antenna technologies, chiefly RFID and NFC, exhibit a robust 9.02% CAGR, underpinned by pharmaceutical serialization deadlines and omnichannel retail models that demand omnipresent inventory visibility.

Printed sensor arrays detecting temperature, gas, and microbial spoilage are now roll-to-roll manufactured at up to 500 m/min, slashing unit costs. Some dairy brands trial colorimetric freshness labels that change from blue to white when cumulative chill exposure exceeds safe thresholds, opening a visible feedback loop for consumers. Blockchain-anchored authentication services integrate with these sensors, producing immutable records that regulators can audit instantly.

By End-user Industry: Food Applications Lead Adoption

Food applications accounted for a 35.20% share of the active and intelligent packaging market in 2025, a reflection of high perishability and consumer sensitivity to freshness. Grocery retailers insist suppliers adopt active oxygen absorbers to extend chilled meat shelf life from 12 to 18 days, easing replenishment scheduling. Dairy processors layer antimicrobial peptides into inner films to delay mold growth, while produce growers add ethylene absorbers inside clamshells to slow ripening.

Pharmaceuticals register the highest 7.23% CAGR as biologics, vaccines, and personalized therapies demand item-level monitoring at sub-zero temperatures. Serialization 2.0 forces every saleable unit to carry a digital identity, making intelligent features non-negotiable. Beverage and industrial users deploy smart packaging mainly for anti-counterfeit and condition monitoring in extended ocean freight, whereas logistics firms harness RFID for pallet-level visibility to optimize hub routing. The diverse uptake across sectors insulates solution providers from demand swings in any single vertical.

Geography Analysis

North America led the active and intelligent packaging market with 34.00% share in 2025 as FDA serialization and mature cold chains gave early impetus. Retailers employ embedded freshness indicators to verify supplier performance, and venture capital continues funding start-ups that merge IoT with flexible packaging. Smart-label penetration surpassed 18% of chilled meat packs in the United States by late 2025, cementing user familiarity.

Europe remains a technology crucible where sustainability legislation drives rapid iteration. The Single-Use Plastics Directive stimulated R&D into compostable NFC tags and solvent-free laminations. Germany piloted digital watermarks for automatic pack sorting, achieving 95% detection accuracy during municipal trials. France’s extended producer responsibility fees, tiered by recyclability and recycled content, indirectly nudge converters toward mono-material smart films.

Asia-Pacific is the fastest grower at a 9.45% CAGR, powered by China’s upgraded food labeling law and India’s “Make in India” push that now hosts regional RFID chip production. The active and intelligent packaging market size in Asia-Pacific could overtake Europe by 2028 if current capital expenditure plans materialize. Japan’s convenience-store channel is piloting time-temperature integrators on premium bento boxes, while South Korea mandates serialization for select biologics, pushing intelligent adoption deeper into healthcare.

Competitive Landscape

Moderate concentration defines the active and intelligent packaging market, with the top players collectively holding significant market revenue share. Amcor plc, Sealed Air Corporation, and Avery Dennison Corporation allocate millions annually to smart-pack R&D, often partnering with semiconductor fabricators to secure RFID chip access.

Avery Dennison opened its first ARC-certified RFID inlay plant in India in April 2025, cementing supply resilience and tapping regional demand. Mid-tier firms target niches such as antimicrobial films or compostable smart labels, gaining traction with agility and specialized expertise. Patent races intensify around energy-harvesting inks that draw power from ambient RF signals, a breakthrough that could eliminate thin-film batteries altogether. Competitive pressure now hinges on software ecosystems as much as material innovation, steering strategic alliances between packaging converters and cloud-service providers.

Emerging disruptors experiment with SaaS-bundled packaging, selling freshness data subscriptions rather than physical labels alone. Investors back companies integrating AI-driven demand forecasting with smart-pack signals, promising inventory reductions across downstream nodes. As a result, incumbents are re-skilling workforces toward data science and mechatronics, signaling a long-term pivot toward tech-centric business models.

Active And Intelligent Packaging Industry Leaders

Avery Dennison Corporation

Multisorb Technologies Inc.

Amcor plc

Sealed Air Corporation

Coveris Holding SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: FreshInset reported that its Vidre+ complex turns clamshells into active packages, preserving cherries with minimal weight loss and better stem color.

- April 2025: Avery Dennison announced the opening of its first RFID inlay and label plant in Pune, India, supporting the “Make in India” initiative.

- April 2025: AIPIA launched the Interactive Brand Packaging Network to position packaging as a strategic media channel.

- November 2024: VarieT Technology unveiled the Smart Heat Battery, a self-heating insert aimed at on-demand warming of canned food and beverages.

Global Active And Intelligent Packaging Market Report Scope

Active and intelligent packaging refers to a package that may detect environmental changes and notify users of those changes. Advanced packaging systems perform tasks such as detecting, sensing, recording, tracing, communicating, extending shelf life, improving safety and quality, providing information, and alerting users to potential issues. The study considers the revenue generated from selling various types of active and intelligent packaging products/solutions provided by vendors operating in the market.

The active and intelligent packaging market is segmented by active packaging market (type (gas scavengers/emitters, moisture scavengers, microwave susceptors), end-user industry (food, beverages)), intelligent packaging market (type (coding and markings, antenna (RFID & NFC), sensors and output devices), end-user industry (food, beverages, pharmaceuticals, industrial, logistics)), and geography.

By Packaging Function

| Supply Chain Management |

| Product Freshness |

| Consumer Convenience |

| Brand Protection |

| Product Information |

By Packaging Technology

| Active Packaging |

| Intelligent Packaging |

By Active Packaging Type

| Gas Scavengers/Emitters |

| Moisture Scavengers |

| Microwave Susceptors |

| Other Active Packaging Technologies |

By Intelligent Packaging Type

| Coding and Markings |

| Antenna (RFID and NFC) |

| Sensors and Output Devices |

| Other Intelligent Packaging Technologies |

By End-user Industry

| Food |

| Beverages |

| Pharmaceuticals |

| Industrial |

| Logistics |

| Other End-user Industries |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Function | Supply Chain Management | ||

| Product Freshness | |||

| Consumer Convenience | |||

| Brand Protection | |||

| Product Information | |||

| By Packaging Technology | Active Packaging | ||

| Intelligent Packaging | |||

| By Active Packaging Type | Gas Scavengers/Emitters | ||

| Moisture Scavengers | |||

| Microwave Susceptors | |||

| Other Active Packaging Technologies | |||

| By Intelligent Packaging Type | Coding and Markings | ||

| Antenna (RFID and NFC) | |||

| Sensors and Output Devices | |||

| Other Intelligent Packaging Technologies | |||

| By End-user Industry | Food | ||

| Beverages | |||

| Pharmaceuticals | |||

| Industrial | |||

| Logistics | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the active and intelligent packaging market in 2026?

It is valued at USD 16.4 billion, with a projected rise to USD 22.29 billion by 2031 at a 6.31% CAGR.

Which application currently drives the highest revenue?

Product freshness commands a 45.90% share thanks to the wide adoption of oxygen and moisture scavengers at retail and processor levels.

What region leads the adoption of intelligent packaging?

North America holds a 34.00% share due to FDA serialization rules and mature cold-chain networks.

Which technology segment is growing fastest?

Antenna-based intelligent packaging, such as RFID and NFC inlays, is forecast to grow at a 9.02% CAGR through 2031.

What is the key restraint for small converters?

Up-front equipment and retrofit costs of USD 2-8 million per facility extend payback periods beyond four years.

Page last updated on: