Smart Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.84 Billion |

| Market Size (2031) | USD 36.94 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

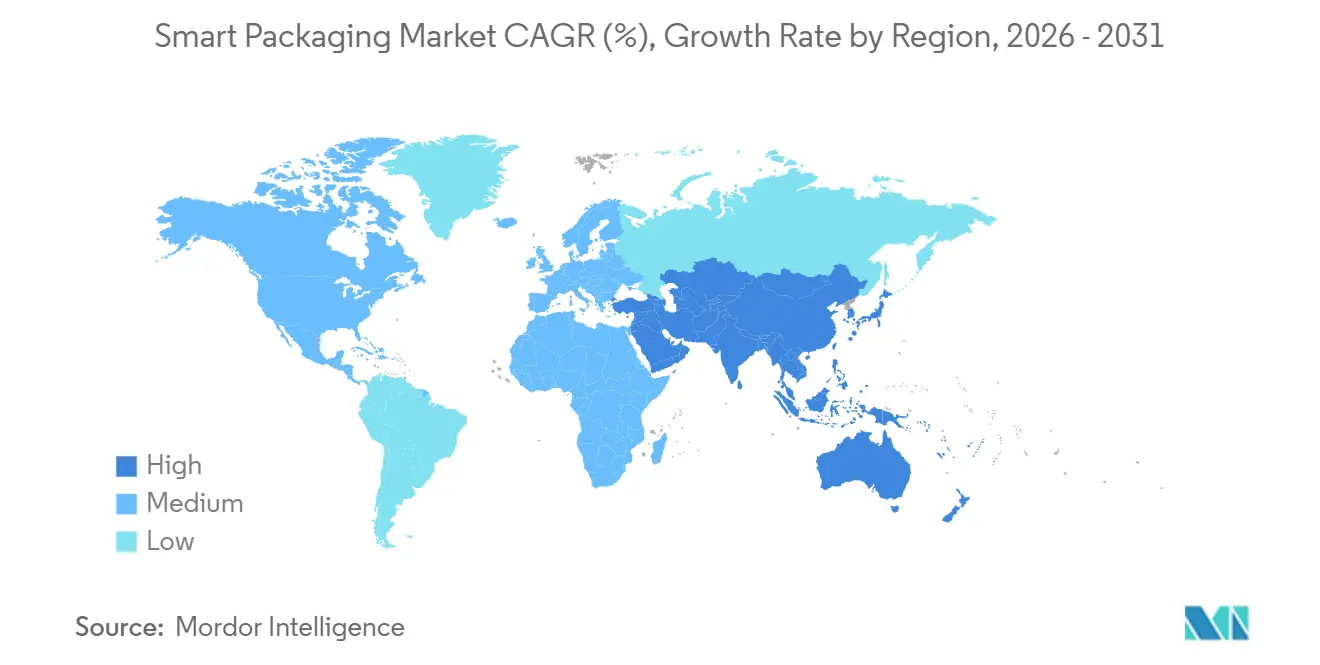

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

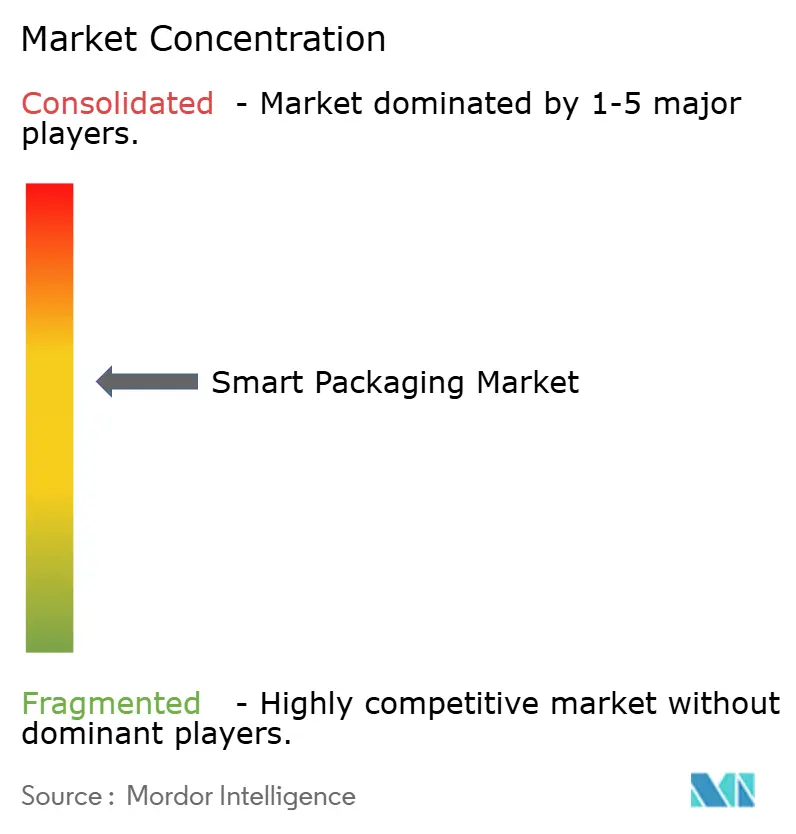

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Packaging Market Analysis by Mordor Intelligence

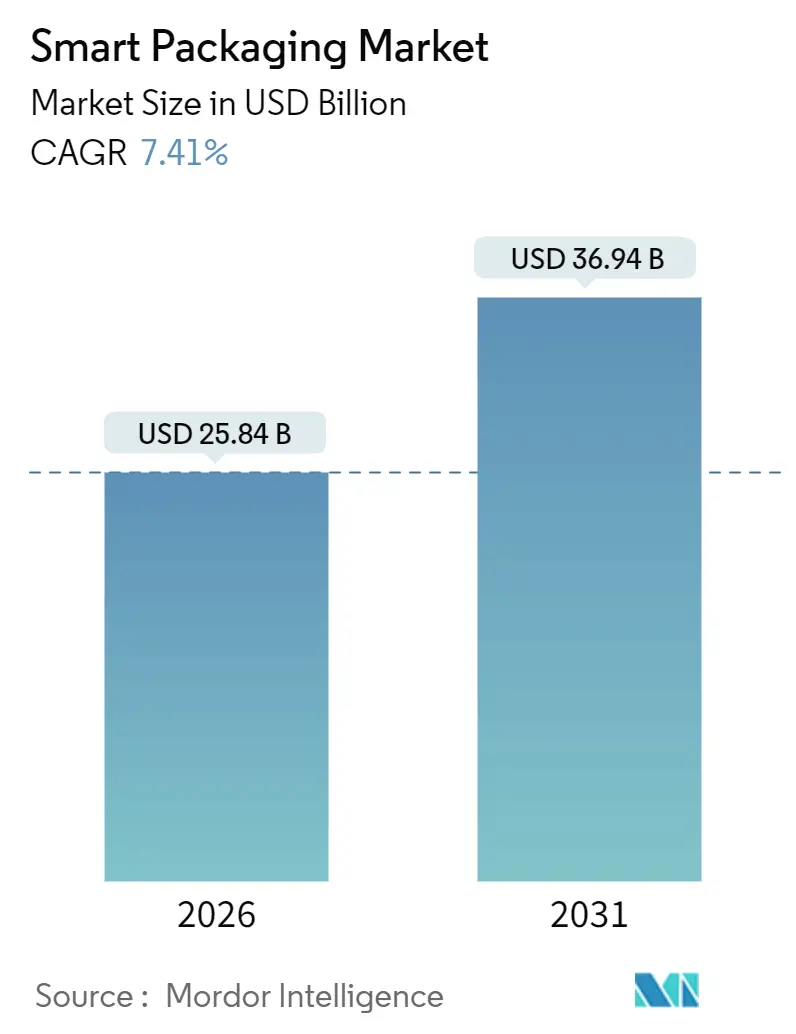

The smart packaging market size stood at USD 25.84 billion in 2026 and is projected to reach USD 36.94 billion by 2031, reflecting a 7.41% CAGR over the forecast period. The current smart packaging market size demonstrates how printed electronics, antimicrobial coatings, and IoT connectivity are redefining packages as active data points across digitized supply chains. Steady demand for shelf-life extension films in online grocery, falling RFID tag costs, and serialization mandates in pharmaceuticals jointly reinforce growth momentum. In parallel, European circular-economy rules, China’s cold-chain modernization, and item-level inventory strategies in North American retail are widening the addressable base for technology vendors. Brands also view connected packs as a gateway to first-party consumer insights, an advantage that gains importance as browser cookies fade.

Key Report Takeaways

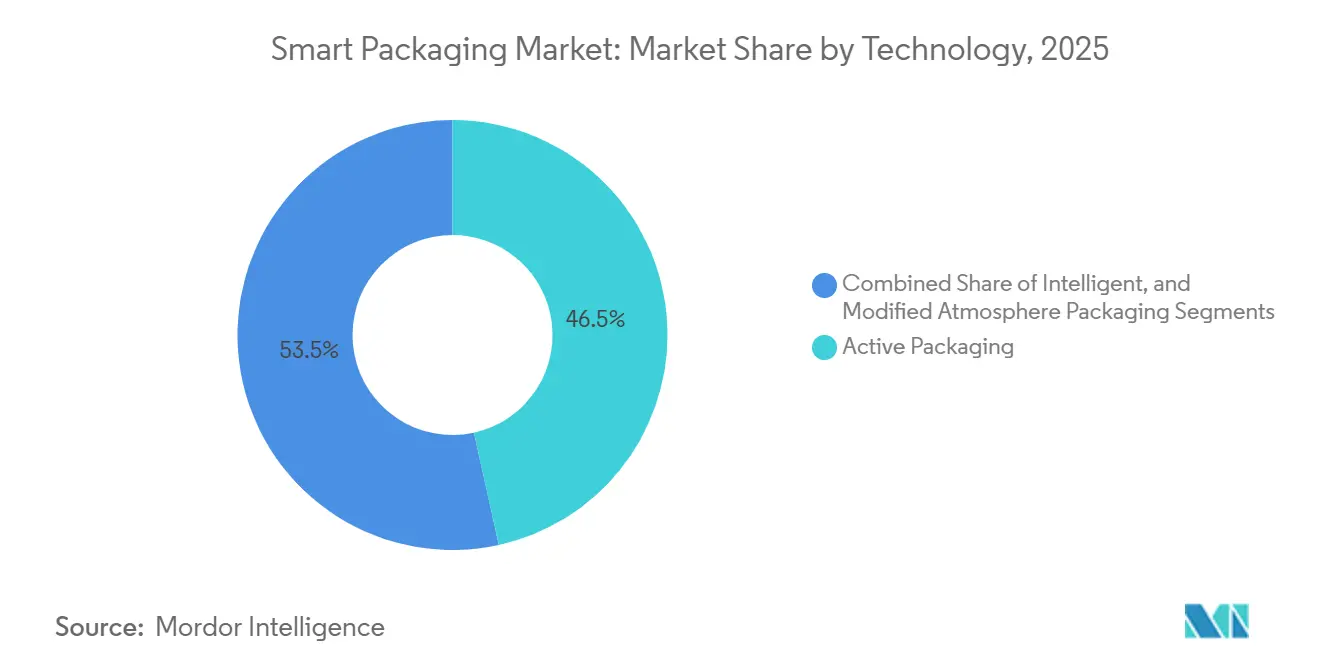

- By technology, active formats led with 46.54% smart packaging market share in 2025, while intelligent formats are on course for the fastest 9.23% CAGR through 2031.

- By material, plastics commanded 42.43% share of the smart packaging market size in 2025; biodegradable polymers are forecast to post the strongest 8.43% CAGR between 2026 and 2031.

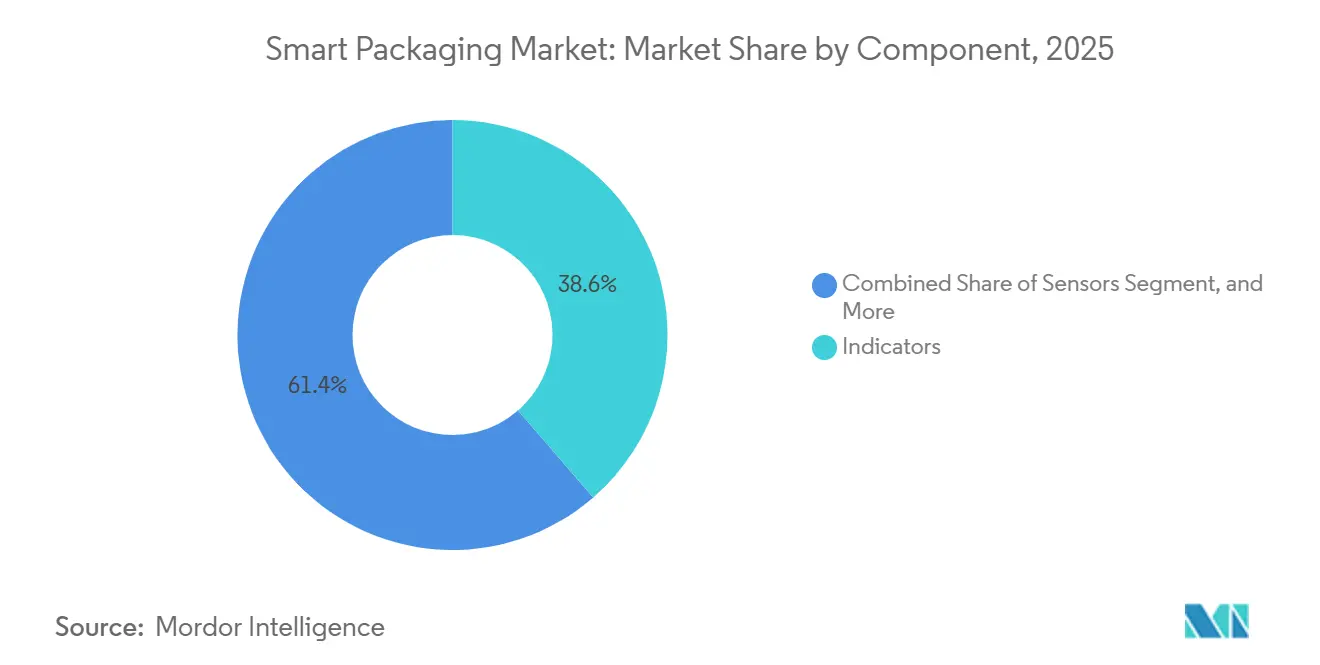

- By component, indicators contributed 38.64% revenue in 2025, and sensors are tracking an 8.83% CAGR through 2031.

- By end-user, food accounted for 28.76% of demand in 2025, whereas pharmaceuticals are set to expand at an 8.76% CAGR to 2031.

- By geography, North America remained the largest regional contributor with 39.74% revenue share in 2025; Asia-Pacific is poised for the fastest 9.76% CAGR out to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Smart Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancement in Printed Electronics Enabling Cost-effective RFID and NFC Tags | +1.2% | Global, with early adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing Demand for Real-time Food Quality Monitoring in E-commerce Cold Chains | +1.5% | North America, Europe, and urban Asia-Pacific | Short term (≤2 years) |

| Stringent Anti-counterfeiting Regulations in Pharmaceutical Supply Chains | +1.3% | North America, Europe, with spillover to South America and Middle East | Long term (≥4 years) |

| Consumer Preference for Sustainable Packaging with Integrated Freshness Indicators | +0.9% | Europe, North America, and Australia | Medium term (2-4 years) |

| Adoption of IoT-enabled Packaging by CPG Brands for Direct-to-Consumer Engagement | +1.0% | North America, Western Europe, and Japan | Medium term (2-4 years) |

| Rapid Growth of Smart Retail Shelves Requiring Embedded Intelligent Packaging | +0.8% | North America, Europe, and select Asia-Pacific metros | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Advancement in Printed Electronics Enabling Cost-effective RFID and NFC Tags

Roll-to-roll printing of conductive inks on flexible plastic has reduced the per-tag cost by roughly 60% since 2024, pushing passive RFID below the USD 0.05 threshold that retailers deem viable for item-level tracking.[1]Pragmatic Semiconductor, “FlexIC Platform,” pragmaticsemi.com The resulting economics allow apparel, cosmetics, and even mid-priced fast-moving goods to carry unique identifiers that feed real-time inventory dashboards. Printed circuits now survive standard flexographic temperatures, so converters add antennas during the same press pass that applies graphics, eliminating a secondary assembly stage. NFC tags, which harvest power from smartphones, are being integrated into pharmaceutical blister packs to authenticate origin and trigger dose-reminder apps, an approach that will be scaled across several EU markets in 2025.[2]Avery Dennison Corporation, “Intelligent Labels Solutions,” averydennison.com Luxury spirits producers also embed encrypted batch data in NFC chips, providing consumers with a direct verification path that deters diversion and enhances brand engagement.

Growing Demand for Real-time Food Quality Monitoring in E-commerce Cold Chains

Doorstep grocery delivery revealed gaps in last-mile temperature control. A 2025 study showed 12% of refrigerated shipments exceeded 4 °C for more than 30 minutes, accelerating spoilage risks.[3]U.S. Department of Agriculture, “Food Safety and Cold Chain,” usda.gov Color-change time-temperature labels now let shoppers reject compromised items, curbing liability for retailers and cutting waste. One solution embeds CO₂ sensors in modified-atmosphere trays and transmits alerts to warehouse systems, letting operators reroute at-risk inventory to nearby stores. Cold-chain providers increasingly back these sensors with blockchain ledgers, creating immutable temperature records that assist regulators and insurers. The approach, proven in biologics distribution, is migrating to high-margin proteins and organic produce.

Stringent Anti-counterfeiting Regulations in Pharmaceutical Supply Chains

Full enforcement of the U.S. Drug Supply Chain Security Act requires every prescription package to carry a unique serialized code verified at each hand-off. Europe’s Falsified Medicines Directive established a parallel framework, and over 9 billion packs had been authenticated via a centralized hub by late 2025.[4]European Medicines Agency, “Falsified Medicines Directive,” ema.europa.eu India amended its Drugs and Cosmetics Rules to mandate track-and-trace for Schedule H drugs, pushing local manufacturers toward RFID-enabled cartons. Compliance demands foster steady demand for converters that can print 2D barcodes, embed RFID, and add tamper-evident closures on the same line. Technology vendors supplying readers and cloud platforms report rising revenue from life-science clients.

Consumer Preference for Sustainable Packaging with Integrated Freshness Indicators

A 2025 survey found that European consumers are willing to pay a 7% premium for packs that combine biodegradability with visual spoilage cues. Solutions include polylactic acid films infused with pH-sensitive dyes and paperboard trays bearing water-based freshness inks that meet the EN 13432 compostability standards. By eliminating multi-material laminates, these packs glide through industrial composting lines without manual separation, advancing circular economy targets. Brands are adding QR codes that link to carbon-footprint dashboards, a transparency feature piloted on ice cream products in 2025. The forthcoming EU Packaging and Packaging Waste Regulation, scheduled for adoption in 2026, will make recyclability or compostability mandatory by 2030, thereby reinforcing investment in single-substrate intelligent labels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Expenditure for Smart Packaging Production Lines | -0.7% | Global, with acute impact in emerging Asia-Pacific and South America | Short term (≤2 years) |

| Limited Recycling Infrastructure for Multi-material Active Packaging | -0.5% | Global, particularly acute in North America and developing Asia | Medium term (2-4 years) |

| Privacy Concerns Over Consumer Data Collected via Connected Packaging | -0.3% | Europe, North America, and Australia | Medium term (2-4 years) |

| Absence of Global Interoperability Standards for Sensor-based Packaging | -0.4% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure for Smart Packaging Production Lines

Retrofitting extrusion lines with sensor deposition and chip-placement stations often exceeds USD 15 million per site, a cost that sidelines small and mid-size converters. Payback periods lengthen when order volumes fluctuate seasonally, pushing breakeven beyond six years in some emerging markets. Rapid innovation also triggers technology-obsolescence risk; equipment installed in 2024 may face write-offs before full depreciation if next-gen flexible circuits dominate. Equipment-as-a-service contracts from machinery makers reduce upfront cash demands, yet adoption remains limited where commercial-lending ecosystems are thin and currency volatility is high.

Limited Recycling Infrastructure for Multi-material Active Packaging

Hybrid constructions bonding barrier films, sensor layers, and paper often confuse optical sorters and end up in residual waste streams, exacerbating extended producer responsibility fees in France and Germany. Pilot enzymatic delamination projects show promise; one process dissolved adhesive layers in PET films carrying RFID tags, but commercial roll-out lags outside a handful of cities, pending municipal-industry partnerships. Asia-Pacific faces a sharper infrastructure gap, with informal picker networks unable to separate intelligent layers, leading to landfill leakage. Some brands now adopt mono-material polyethylene pouches with printed sensors, trading barrier performance for recyclability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Active Formats Lead, Intelligent Momentum Builds

Active formats held 46.54% of smart packaging market share in 2025, anchored by oxygen scavengers and antimicrobial films that cut spoilage in meat and bakery channels. Intelligent solutions are expected to post a 9.23% CAGR, buoyed by low-cost RFID and demand for real-time inventory insight. Modified-atmosphere packaging bridges the categories, offering shelf-life gains without data capture, and remains popular with mid-tier processors hesitant to overhaul equipment. Dual-function films launched in 2025 that merge scavenging with color-changing ripeness indicators illustrate a convergence that lets converters upsell layered capabilities.

The technology mix reflects end-user priorities. Pharmaceutical shippers favor desiccants and temperature labels that document compliance, while consumer-goods producers chase NFC tags that unlock recipes or loyalty programs. Regulatory hurdles differ: antimicrobial agents require U.S. FDA food-contact clearance, adding six to twelve months to launch cycles, whereas RFID incurs no such review. As a result, RFID adoption outpaces antimicrobial roll-outs in non-regulated categories.

By Material: Plastic Dominance Faces Biopolymer Uptick

Plastic brought in 42.43% of material revenue in 2025 thanks to flexible processing windows and compatibility with sensor lamination. Biopolymers are set to expand at 8.43% CAGR, spurred by European single-use rules that steer converters toward polylactic acid and polyhydroxyalkanoate substrates. These resins now match polyethylene in moisture barrier, yet their higher melt index forces extrusion-line upgrades costing USD 2-4 million per unit. Paper still dominates dry-goods packs, backed by well-established recycling loops; one leading fiber company cited an 87% recovery rate for its corrugated formats in 2025.

Glass and metal remain niche but illustrate possibilities: a pilot aluminum can with thermochromic ink signals ideal drinking temperatures without compromising scrap-metal valorization. Material strategy also aligns with supply-chain resilience. Resin disruptions in 2024 pushed converters to diversify feedstocks and invest in fermentation-derived polymers despite a 20-30% cost premium.

By Component: Indicator Leadership Meets Sensor Surge

Indicators captured 38.64% revenue in 2025 because time-temperature labels piggyback on existing printing lines at minimal cost. Sensors are poised for an 8.83% CAGR as miniaturized gas detectors and pH probes reach cost thresholds palatable for unit-level deployment. Data carriers such as RFID and NFC benefit from serialization laws and omnichannel inventory models, delivering steady double-digit shipment growth to technology suppliers. Antimicrobial agents remain important for produce and ready-meals but face nano-silver migration limits that slow new approvals inside the European Union.

Regional preferences vary. North America leans heavily on RFID for supply-chain visibility, Europe favors compostable indicators aligned with circular goals, and Asia-Pacific values antimicrobial films to combat warm-climate spoilage. Lack of harmonized calibration standards still hampers global sensor deployment, an issue ISO’s Technical Committee 122 is tackling.

By End-user Industry: Food Leads, Pharma Gains Pace

Food held 28.76% of demand in 2025, driven by modified-atmosphere trays that double shelf life for meat and bakery categories. Pharmaceuticals are expected to clock an 8.76% CAGR through 2031, pulled by serialization, cold-chain, and tamper-evidence rules. Beverage brands adopt thermochromic inks on aluminum and glass to flag chill points, enhancing shelf impact. Cosmetics use NFC-enabled bottles to combine anti-counterfeiting with interactive tutorials, as shown in a 2025 foundation launch that sent personalized shade tips to users’ phones.

Outside these anchors, electronics packaging adds RFID to high-value chips for warranty tracking, while small-batch organics trial freshness indicators on premium SKUs. Adoption correlates with margin structure: pharmaceuticals and cosmetics absorb USD 0.10-0.20 unit costs, whereas price-sensitive food brands roll out intelligent layers only on premium lines.

Geography Analysis

North America held a 39.74% revenue share in 2025, underpinned by early RFID mandates from big-box retailers and full DSCSA enforcement, which serialized every prescription pack. Canada’s Safe Food for Canadians Regulations further spurred the adoption of time-temperature tracking by requiring traceability for fresh produce. Mexico’s role as a near-shoring hub accelerated local label capacity as multinational FMCG firms installed smart-label lines to serve U.S. distribution routes.

Asia-Pacific is projected to deliver the fastest 9.76% CAGR through 2031. China’s 14th Five-Year Plan earmarked CNY 500 billion for refrigerated logistics and mandated real-time temperature monitoring for vaccines. India’s pharmaceutical sector, which is responsible for 40% of global generic output, now utilizes RFID and 2D codes on export cartons to comply with new domestic regulations. Japan pilots NFC-linked adherence packs that alert caregivers to missed doses, while South Korea expands track-and-trace to health supplements. Australia and New Zealand make recyclability a prerequisite, favoring mono-substrate intelligent labels that separate cleanly during sortation.

Europe combines sustainability mandates with rigorous anti-counterfeiting measures. The upcoming Packaging and Packaging Waste Regulation aims for universal recyclability or compostability by 2030, encouraging paper-based RFID labels with water-soluble adhesives. Germany’s VerpackG tiers license fees by material complexity, nudging brands toward single-substrate formats. The U.K. plastic-packaging tax penalizes content with under 30% recycled resin, accelerating demand for mechanically recycled films carrying printed sensors. The Middle East and Africa remain small but show promise; United Arab Emirates smart-city pilots and Saudi Arabia’s Vision 2030 diversification plan both include cold-chain smart packs for imported biologics. South Africa now requires serialization on antiretrovirals, creating a beachhead for smart labels.

Competitive Landscape

The top ten players accounted for nearly 45% of the revenue in 2025, indicating moderate concentration. Scale converters like Amcor and Sealed Air synchronize oxygen-scavenging know-how with global plant footprints, winning multi-year contracts from food and pharma brands.

Technology specialists such as Pragmatic Semiconductor and Thin Film Electronics push printed IC costs below USD 0.05, unlocking item-level tagging for mass retail. Patent data points to focus areas, including a filing by Avery Dennison for a tamper-evident NFC strip that self-destructs when peeled, targeting drug safety, while a major chemical supplier patented a dual-function film that scavenges oxygen and signals pH shifts.

Biodegradable intelligent packs form a hotly contested niche. Stora Enso and Huhtamaki are piloting paperboard substrates with embedded circuits that meet EN 13432 composting rules. Interoperability remains a hurdle as ISO works toward unified calibration protocols, yet regional divergence in data privacy and waste-handling priorities slows consensus. White space persists in artisan food and emerging-market drug channels, where run lengths are short, and capital is tight, leaving opportunities for modular, lease-based equipment providers.

Smart Packaging Industry Leaders

Sealed Air Corporation

Amcor PLC

Ball Corporation

BASF SE

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Amcor allocated USD 120 million to add roll-to-roll RFID label capacity in Ghent, Belgium, with operations slated for Q3 2026.

- November 2025: Sealed Air and IBM linked blockchain ledgers to Cryovac intelligent packs to log cold-chain custody in premium protein flows.

- October 2025: BASF released a biodegradable film blending polylactic acid with oxygen scavengers that extends salad shelf life by 40% while meeting EN 13432.

- September 2025: Avery Dennison took a minority stake in Wiliot to advance battery-free Bluetooth tags for item-level tracking.

Global Smart Packaging Market Report Scope

Smart packaging refers to systems with embedded sensor technology used with foods, pharmaceuticals, and many other products.

The Smart Packaging Market Report is Segmented by Technology (Active Packaging, Intelligent Packaging, and Modified Atmosphere Packaging), Material (Paper and Paperboard, Plastic, Glass, Metal, and Biodegradable Polymers), Component (Sensors, Indicators, Data Carriers, and Antimicrobial Agents), End-user Industry (Food, Beverage, Pharmaceuticals, Cosmetics and Personal Care, Electronics, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Active Packaging |

| Intelligent Packaging |

| Modified Atmosphere Packaging |

| Paper and Paperboard |

| Plastic |

| Glass |

| Metal |

| Biodegradable Polymers |

| Sensors |

| Indicators |

| Data Carriers |

| Antimicrobial Agents |

| Food |

| Beverage |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Electronics |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Technology | Active Packaging | ||

| Intelligent Packaging | |||

| Modified Atmosphere Packaging | |||

| By Material | Paper and Paperboard | ||

| Plastic | |||

| Glass | |||

| Metal | |||

| Biodegradable Polymers | |||

| By Component | Sensors | ||

| Indicators | |||

| Data Carriers | |||

| Antimicrobial Agents | |||

| By End-user Industry | Food | ||

| Beverage | |||

| Pharmaceuticals | |||

| Cosmetics and Personal Care | |||

| Electronics | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the smart packaging market in 2026 and what growth is expected?

The smart packaging market size reached USD 25.84 billion in 2026 and is forecast to hit USD 36.94 billion by 2031, delivering a 7.41% CAGR.

Which technology segment is expanding the fastest?

Intelligent formats, driven by low-cost RFID and real-time data needs, are forecast to grow at a 9.23% CAGR through 2031.

What is fueling smart packaging demand in pharmaceuticals?

Unit-level serialization mandates in the United States, European Union, and India push converters to embed RFID or 2D codes and temperature indicators, supporting an 8.76% CAGR through 2031 for pharmaceutical applications.

Why are biodegradable smart packs gaining traction?

EU regulations require all packaging to be recyclable or compostable by 2030, prompting brands to shift to polylactic-acid and paperboard substrates that integrate compostable freshness indicators.

Which region will grow the quickest?

Asia-Pacific is projected to register the highest regional CAGR at 9.76% thanks to China’s cold-chain investments and India’s serialization drive.

What is the chief barrier for new entrants?

High capital expenditure, often topping USD 15 million per line for sensor integration and chip placement, extends payback periods and limits participation from smaller converters.

Page last updated on: