Retail Ready Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 79.72 Billion |

| Market Size (2031) | USD 105.68 Billion |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

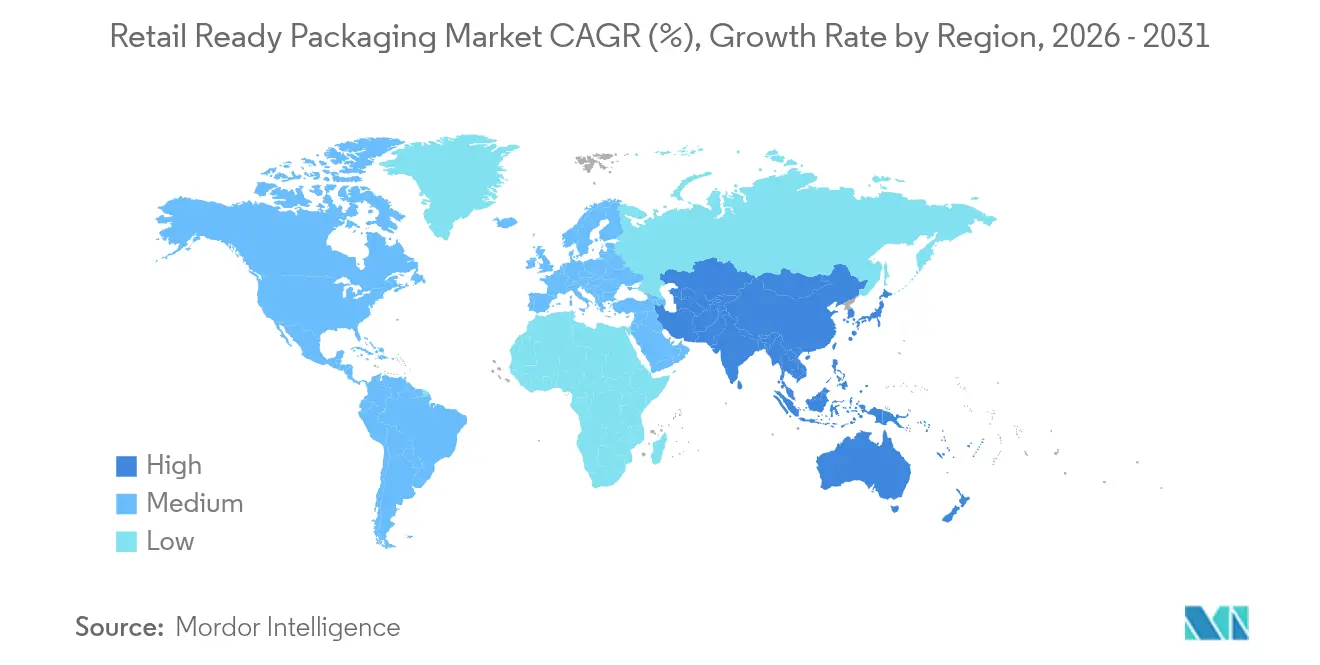

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Retail Ready Packaging Market Analysis by Mordor Intelligence

Retail ready packaging market size in 2026 is estimated at USD 79.72 billion, growing from 2025 value of USD 75.35 billion with 2031 projections showing USD 105.68 billion, growing at 5.8% CAGR over 2026-2031. Expanding e-commerce sales, growing retailer mandates for shelf-ready formats and acute in-store labor shortages keep demand elevated. Large chains now specify exact case dimensions and opening designs, cutting replenishment time by as much as 40%. At the same time, Extended Producer Responsibility schemes in Europe and multiple US states push suppliers toward single-material fiber solutions that reduce disposal costs and simplify recycling. Mergers such as Amcor’s union with Berry Global and Sonoco’s Eviosys acquisition expand vertically integrated platforms able to fund automation and rapid design customization, giving them an edge with global brand owners. In response, mid-tier converters increase spending on AI-enabled equipment that trims line-changeover from hours to minutes, unlocking profitable micro-batch runs that meet localized promotions

Key Report Takeaways

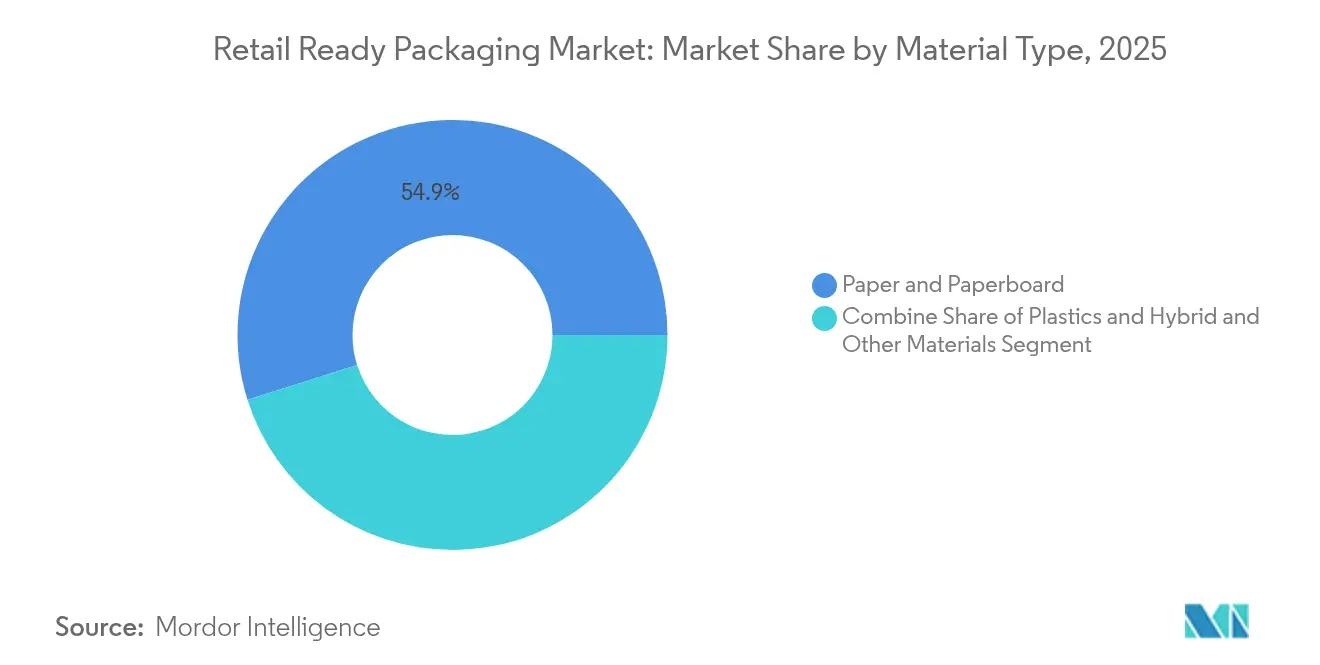

- By material type, paper and paperboard led with 54.86% of retail ready packaging market share in 2025; hybrid and other materials record the fastest 7.05% CAGR to 2031.

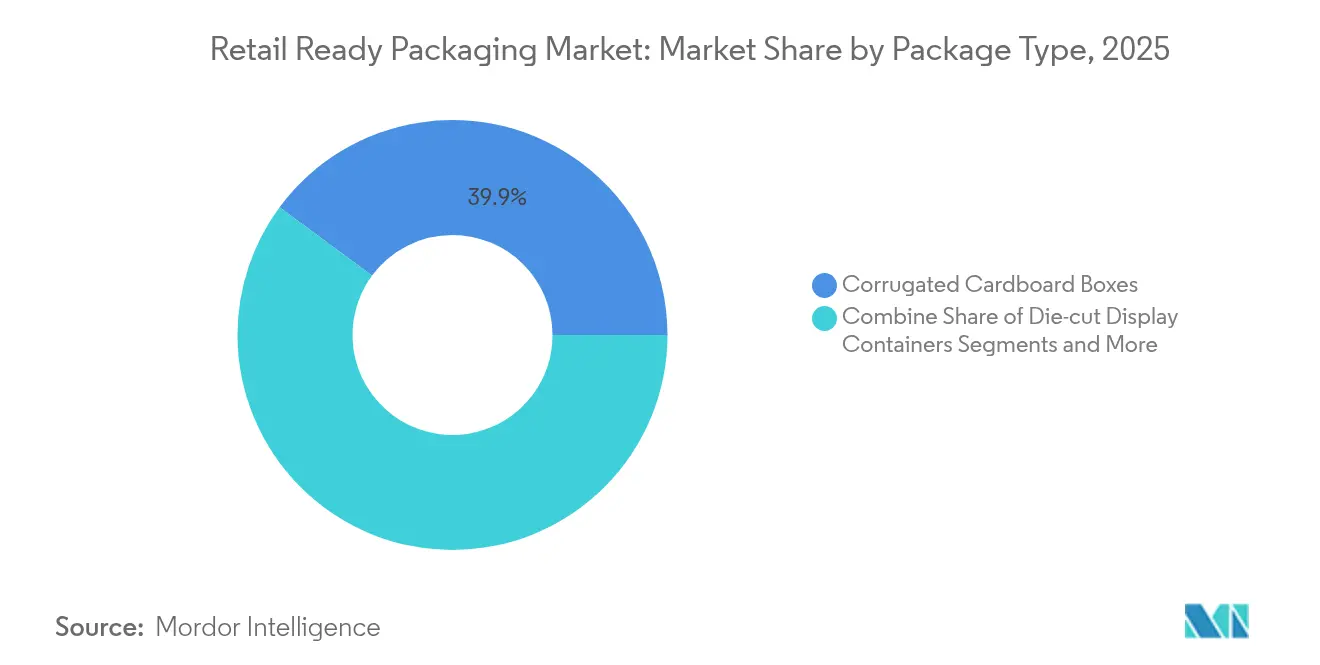

- By package type, corrugated cardboard boxes accounted for 39.88% retail ready packaging market size in 2025, while die-cut display containers grow the quickest at an 7.92% CAGR.

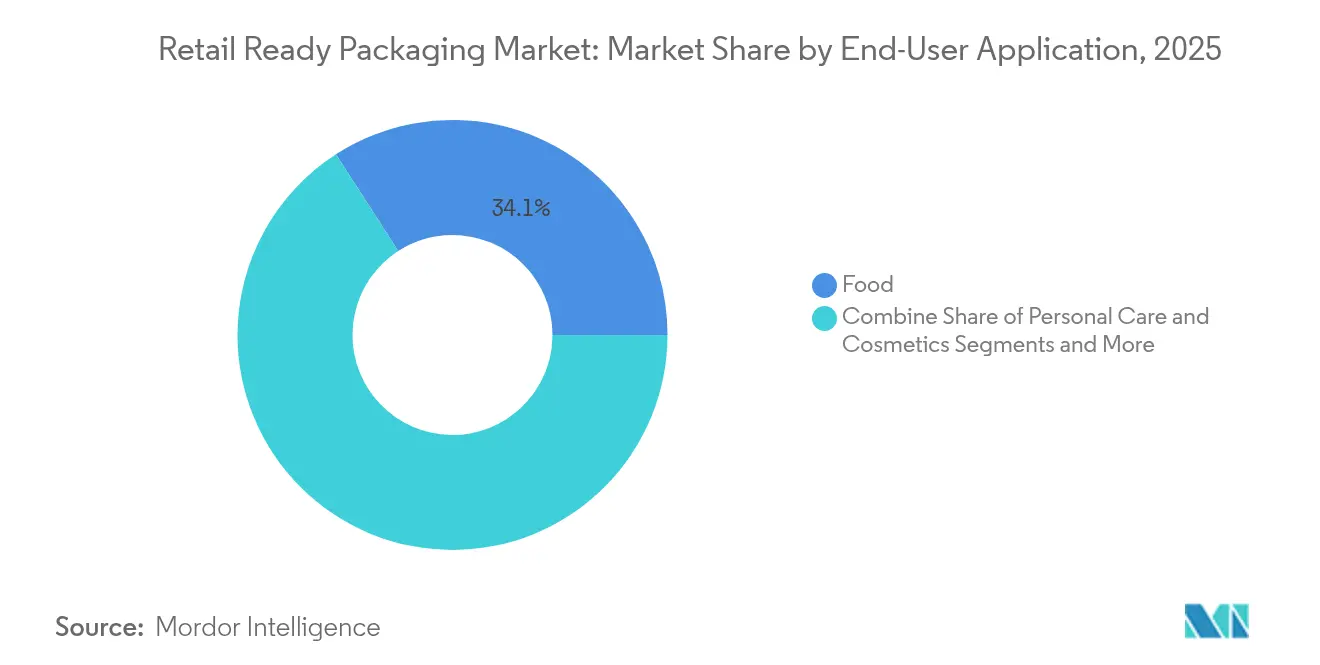

- By end-user application, the food segment captured 34.12% of the retail ready packaging market size in 2025; personal care & cosmetics is set to expand at a 7.45% CAGR through 2031.

- By geography, Europe retained 35.12% share of the retail ready packaging market in 2025; Asia-Pacific posts the highest 8.75% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Retail Ready Packaging Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Circular-economy regulations accelerating single-material fiber SRP adoption | +1.2% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| E-commerce hyper-growth raising shelf-ready packaging compliance demand | +1.8% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Retailer labor shortages driving SRP adoption for 40% man-hour reduction | +1.1% | North America and Europe core, emerging in Asia-Pacific | Medium term (2-4 years) |

| AI-enabled packaging line automation boosting changeover speed | +0.9% | Global, led by developed markets | Long term (≥ 4 years) |

| Branded manufacturers using SRP to lift on-shelf conversion rates | +0.7% | Global, emphasis on premium retail channels | Short term (≤ 2 years) |

| Digital-printing economics enabling micro-batch promotions in SRP | +0.5% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Circular-economy regulations accelerating single-material fiber SRP adoption

The European Union’s Packaging and Packaging Waste Regulation (PPWR) effective January 2025 introduces recyclability thresholds that make multi-layer laminates financially unattractive. Compliance fees on restricted combinations run as high as USD 739 per tonne, encouraging retailers and brand owners to converge on mono-fiber structures that slide seamlessly into existing curbside programs.[1]The Grocer,"EPR scheme base fees unveiled by Defra," thegrocer.co.uk Global consumer-goods companies standardize these formats across regions to avoid managing duplicate specifications, giving compliant converters first-mover advantage. Similar momentum builds in the United States where California’s SB 343 limits the use of recycling symbols to substrates proven recyclable at scale.As comparable rules emerge in Canada, Japan and key Latin American markets, single-material designs transition from regional preference to baseline requirement for global tenders.

E-commerce hyper-growth raising shelf-ready packaging compliance demand

Online order volumes strain fulfillment centers, so large retailers institute strict shelf-ready requirements and apply charge-back penalties that can exceed 3% of invoice value when suppliers ship non-compliant cases. Serialized 2D barcodes aligned with the GS1 Sunrise 2027 roadmap and expanding RFID mandates embed inventory accuracy directly into the case, allowing automated sortation and real-time stock checks. Packaging now acts as a data carrier that lowers costly manual scans, justifying higher-priced smart formats. Integrated NFC tags additionally let brands validate product authenticity and launch app-based promotions at the point of unboxing, creating an incremental marketing use-case for retail ready packaging market participants.

Retailer labor shortages driving SRP adoption for 40% man-hour reduction

Persistent staffing gaps in supermarkets and mass merchants mean replenishment speed is a critical KPI. Shelf-ready designs that open without knives, present goods in consumer-facing orientation and slide directly onto rails cut stocking time by up to 45% in European pilots.[2]Dentons,"High-Hazard Retailers: Are You Prepared for an OSHA Inspection," dentons.com Injury risk falls as knives and loose blades disappear from the aisle, aligning with new safety requirements such as the US Warehouse Worker Protection Act. Smaller regional chains lacking full automation adopt standardized SRP to offset limited headcount, driving incremental uptake in markets previously price-sensitive to format premiums.

AI-enabled packaging line automation boosting changeover speed

Brands trim SKU lifecycles and run frequent themed campaigns. AI-driven equipment learning from sensor data reconfigures feeders, print heads and case erectors in minutes. A cosmetics contract packer that implemented vision-guided robotics cut labor from 12 to 2 operators while doubling throughput consistency. Predictive maintenance algorithms schedule component swaps before failure, improving uptime on corrugated lines historically prone to jams. The resulting flexibility lets converters profitably produce 5,000-unit runs that were once uneconomic, opening fresh revenue for the retail ready packaging market.

Restraints Impact Analysis of Retail Ready Packaging Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corrugated containerboard price volatility | -0.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Lack of global SRP standardization inflating supply-chain costs | -0.6% | Global, most acute in emerging markets | Medium term (2-4 years) |

| RFID/smart-label integration costs in SRP formats | -0.4% | Developed markets initially, expanding globally | Long term (≥ 4 years) |

| Supermarket non-compliance fines and charge-backs | -0.3% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Corrugated containerboard price volatility

Linerboard prices moved 15–25% within a single year, and a USD 70 per-ton increase announced for January 2025 by a leading North American mill flows through converter invoices within weeks. Because finishing adds a further 20–30% mark-up, brand owners see case costs swing sharply, complicating promotion budgets.[3]Federal Reserve bank ,"Producer Price Index," fred.stlouisfed.orgVertically integrated majors smooth exposure by owning mills, yet small independents face margin compression or must pass on surcharges that hurt competitiveness in tenders. Volatility may ease once additional capacity comes online in Asia-Pacific, but elevated energy costs in Europe keep the input outlook uncertain.

Lack of global SRP standardization inflating supply-chain costs

European grocery chains favor 600 mm shelf depths and front-facing tear-strips, whereas North American retailers often require 48 in pallet patterns and top-opening designs. Multinationals thus manage parallel tooling and inventory, with die-set investments reaching USD 100,000 per SKU for complex cases. GS1 has proposed universal formats yet regional associations resist harmonization that could disrupt existing supplier ecosystems. Larger converters offset complexity through global design libraries and multi-plant production, but smaller firms limit export activity, narrowing choice for brand owners in secondary markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Retail Ready Packaging Market Segment Analysis

By Material Type:

Fiber dominance amid sustainability mandatesPaper and paperboard controlled 54.86% of retail ready packaging market share in 2025 and remains the default substrate for high-volume FMCG goods. Corrugated containerboard supplies durable transit protection while presenting printable kraft surfaces that align with branding and recyclability claims. Folding boxboard gains ground where premium graphics and rigidity coexist, notably in confectionery gift packs. Solid bleached sulfate safeguards chilled dairy launches that need grease resistance and bright whiteness. White-lined chipboard supports value-tier cereals and household staples that seek cost efficiency with acceptable shelf finish.

Hybrid and other materials expand at a 7.05% CAGR through 2031 as converters fuse bio-polymers, barrier coatings and sensor layers into single structures. PLA and PHA blends open compostable options for produce, and early commercial runs demonstrate shelf performance in humid supply chains. Smart labels relying on conductive inks integrate seamlessly onto PET windows, turning secondary packs into scan-ready commerce nodes. Although plastics retain niche roles demanding moisture or puncture protection, advances in aqueous dispersion coatings allow fiber substrates to challenge incumbent multilayer films even in freezer environments. The retail ready packaging market benefits as global brands adopt these hybrids to meet diverging regional waste-reduction targets without sacrificing functionality.

By Package Type:

Display innovation drives premium growthCorrugated cardboard boxes represented 39.88% of total demand in 2025. Standard regular slotted container (RSC) dimensions suit automated case erectors and deliver cost leadership across grocery, beverage and household categories. Handle-integrated variants gain traction in household chemicals and small appliances, offering ergonomic retrieval while retaining pallet integrity. Modified high-wall cases ease vertical merchandising of fresh produce, permitting rapid in-line replenishment.

Die-cut display containers, however, accelerate at an 7.92% CAGR as retailers reward solutions that unite transit protection with eye-level branding. Laser-scored tear lines ensure clean edges after opening, enhancing perceived quality. High-graphic pre-print techniques turn faces into billboard media, while post-print digital units personalize QR experiences by region. Shrink-wrapped trays remain relevant for promotional multipacks in beverages, yet compostable shrink alternatives edge into trial programs amid single-use plastic scrutiny. Rigid plastic trays serve closed-loop pool systems within fresh produce chains where durability and washability offset higher unit cost. Together, these formats give brand owners a menu of merchandising tactics calibrated to price point, sustainability pledge and shelf strategy.

By End-User Application:

Personal care accelerates premium positioningThe food category held 34.12% of retail ready packaging market size in 2025, encompassing ready-to-eat meals, cereals and fresh produce that require both protection and rapid shelf placement. Barrier papers with integrated EVOH continue to limit oxygen ingress in meat applications, extending sell-by dates and reducing shrink. Smart freshness sensors debut in high-value seafood packs, providing end-to-end temperature exposure logs.

Personal care & cosmetics post a 7.45% CAGR to 2031, the fastest among tracked sectors. Premium skin-care lines adopt die-cut cartons that form instant podiums on shelf, elevating brand stature and enabling storytelling through hidden interior prints. Micro-batch launches made possible by digital presses test seasonal fragrances without large inventory risk. Luxury hair treatments now ship in fiber-based tubes nested within single-material inserts, eliminating mixed plastic windows and supporting circular-economy claims. The retail ready packaging market thus captures incremental margin as aesthetic expectations rise and sustainability seals shift from bonus to baseline requirement. Home-care products remain steady on the strength of private-label penetration, with retailers demanding uniform case footprints that speed replenishment across cleaning aisles. Consumer electronics brands explore molded-pulp cradles inside corrugated outers to replace expanded polystyrene, balancing shock resistance with recyclability. Pet-food packs trial compostable barrier linings to court environmentally conscious owners, signaling cross-category diffusion of material innovation.

Geography Analysis

APAC Retail Ready Packaging Market

Asia-Pacific delivers the highest 8.75% CAGR through 2031 with China, India and Southeast Asia modernizing supply chains and installing automated fulfillment facilities. Local corrugators upgrade to multi-color flexo machines to target premium consumer electronics launches, while regional pulp-and-paper majors debottleneck containerboard mills to satisfy surging e-commerce case demand. Government policies in Australia and New Zealand banning certain single-use plastics accelerate fiber SRP adoption across dairy and produce exporters. Multinational converters expand design centers in Singapore and Shanghai to localize global brand imagery for regional cultural nuances, underpinning volume growth for the retail ready packaging market.

Europe Retail Ready Packaging Market

Europe retains 35.12% 2025 share, the largest single regional block. Strict recycling targets under PPWR take effect in 2025, driving standardized mono-fiber formats in Germany, France and the Nordics. Retail alliances such as the United Kingdom’s Courtauld Commitment elevate post-consumer content goals, spurring investment in closed-loop containerboard mills. Italy leverages heritage graphics to position high-value wine and confectionery exports, integrating embellished embossing into tear-open SRP. Spain’s greenhouse produce sector adopts vented die-cuts that optimize airflow from Andalusia packing sites to Northern European distribution hubs.

North America Retail Ready Packaging Market

North America exhibits mature but resilient demand as omnichannel retailing blends store pick-up and direct-to-consumer flows. US mass merchants broaden RFID rollouts to general merchandise, embedding serialized tags in secondary packs to cut out-of-stock rates. Canadian grocers pilot fiber-based meat trays laminated with aqueous coatings to comply with upcoming federal plastic reduction rules. Mexican maquiladoras benefit from nearshoring, stimulating corrugated case orders for cross-border shipments into the United States. Overall, automation investment remains the key lever for maintaining service levels in a tight labor market, sustaining healthy unit expansion for the retail ready packaging market.

Competitive Landscape

The retail ready packaging industry shows fragmentation as global leaders pursue scale and technology synergy. The July 2024 merger of Smurfit Kappa and WestRock forged a USD 34 billion revenue platform spanning mills, converting and graphics studios, enabling one-stop global tenders across fiber SRP. Sonoco’s USD 3.9 billion purchase of Eviosys expanded its metal packaging footprint in Europe, adding aerosol and food-can formats that can be integrated into mixed-material promotional displays. Amcor’s all-stock combination with Berry Global finalised in January 2025, pools flexible film know-how with rigid container expertise, boosting R&D outlays to USD 180 million and promising synergies of USD 650 million.

Privately owned converters meanwhile differentiate through rapid digital print turnaround and regional design services. Several mid-size European firms install single-pass inkjet corrugators that output photo-quality cases at eight-color precision, tapping premium beverage contracts. Asian entrants leverage low-cost labor and proximity to electronics assembly clusters to secure export case programs, though they face tightening sustainability rules on inbound shipments to Europe and North America.

Technology partnerships emerge as key strategy. Huhtamaki collaborates with machinery OEMs to co-develop fiber lids that withstand hot-fill temperatures for beverage cups, expanding capacity at its Lurgan, Northern Ireland site in October 2024 to meet brand demand. US-based OEMs offer plug-and-play AI modules retrofitting legacy erectors, democratising smart changeovers for independent plants. Patent filings on interlocking retail case blanks increase, with design tweaks that raise stacking strength while shaving grammage. Collectively, capability expansion, sustainability credentials and automation depth dictate negotiating power across the retail ready packaging market.

Retail Ready Packaging Industry Leaders

-

Mondi Group

-

Smurfit Westrock

-

International Paper Company

-

Georgia-Pacific LLC

-

Oji Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Retail Ready Packaging Market Companies Covered in this Report

- Mondi Group

- Smurfit Westrock

- International Paper Company

- Georgia-Pacific LLC

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Klabin S.A.

- Pratt Industries

- Graphic Packaging International

- STI Group

- Cardboard Box Company

- Weedon Group

- Caps Cases Limited

- Vanguard Packaging Inc.

- TricorBraun

- Huhtamaki Oyj

- Orora Limited

- Sealed Air Corporation

- Amcor PLC

- Sonoco Products Company

- Visy Industries

- Packaging Corporation of America

Recent Industry Developments in Retail Ready Packaging Market

- January 2025: Amcor and Berry Global completed their all-stock merger, creating a global leader in consumer packaging with expected annual synergies of USD 650 million.

- January 2025: Huhtamaki appointed Ralf K. Wunderlich as President and CEO to drive its 2030 growth agenda.

- January 2025: Amcor secured a European patent for AmFiber Performance Paper, a recyclable high-barrier paper fit for food and healthcare applications.

- December 2024: Sonoco closed its USD 3.9 billion acquisition of Eviosys, adding EUR 2.41 billion (USD 2.72 billion) in revenue and broadening metal can offerings.

Global Retail Ready Packaging Market Report Scope

Retail Ready Packaging Market (RRP) refers to the secondary packaging of retail products to go directly onto the shelf without unpacking inner contents. The market is tracked in terms of revenue generated from the sales of retail packaging products.

The Retail Ready Packaging Market is segmented by Material Type (Paper and Paperboard, Plastics), Type of Package (Die-cut Display Containers, Corrugated Cardboard Boxes, Shrink Wrapped Trays, Modified Cases, Plastic Containers), End-user Application (Food, Beverage, Household Products), and Geography (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

Segmentation Overview

| Paper and Paperboard | Corrugated Containerboard |

| Folding Boxboard (FBB) | |

| Solid Bleached Sulfate (SBS) | |

| White-lined Chipboard (WLC) | |

| Plastics | PET |

| HDPE | |

| PP | |

| Bio-plastics (PLA, PHA) | |

| Hybrid and Other Materials |

| Die-cut Display Containers | Standard RSC Die-cuts |

| High-graphic Pre-print Die-cuts | |

| Corrugated Cardboard Boxes | Shelf-ready RSC |

| Handle-integrated SRP | |

| Shrink-wrapped Trays | PE Shrink |

| Compostable Shrink | |

| Modified Cases | High Wall Cases |

| Retail-display Cases | |

| Plastic Containers | Nestable Crates |

| Rigid Plastic Trays | |

| Others (Stand-up Pouches, Re-usable Totes) |

| Food | Ready-to-eat Meals |

| Fresh Produce | |

| Meat and Poultry | |

| Bakery and Confectionery | |

| Beverage | Soft Drinks |

| Alcoholic Beverages | |

| Dairy Drinks | |

| Household and Home-care Products | |

| Personal Care and Cosmetics | |

| Consumer Electronics and Appliances | |

| Others (DIY and Garden, Pet Food) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Paper and Paperboard | Corrugated Containerboard | |

| Folding Boxboard (FBB) | |||

| Solid Bleached Sulfate (SBS) | |||

| White-lined Chipboard (WLC) | |||

| Plastics | PET | ||

| HDPE | |||

| PP | |||

| Bio-plastics (PLA, PHA) | |||

| Hybrid and Other Materials | |||

| By Package Type | Die-cut Display Containers | Standard RSC Die-cuts | |

| High-graphic Pre-print Die-cuts | |||

| Corrugated Cardboard Boxes | Shelf-ready RSC | ||

| Handle-integrated SRP | |||

| Shrink-wrapped Trays | PE Shrink | ||

| Compostable Shrink | |||

| Modified Cases | High Wall Cases | ||

| Retail-display Cases | |||

| Plastic Containers | Nestable Crates | ||

| Rigid Plastic Trays | |||

| Others (Stand-up Pouches, Re-usable Totes) | |||

| By End-User Application | Food | Ready-to-eat Meals | |

| Fresh Produce | |||

| Meat and Poultry | |||

| Bakery and Confectionery | |||

| Beverage | Soft Drinks | ||

| Alcoholic Beverages | |||

| Dairy Drinks | |||

| Household and Home-care Products | |||

| Personal Care and Cosmetics | |||

| Consumer Electronics and Appliances | |||

| Others (DIY and Garden, Pet Food) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the retail ready packaging market?

The retail ready packaging market stands at USD 79.72 billion in 2026 and is forecast to reach USD 105.68 billion by 2031.

Which region grows the fastest through 2031?

Asia-Pacific posts the highest 8.75% CAGR, driven by e-commerce investments and retail modernization.

Which material dominates the retail ready packaging industry?

Paper & paperboard leads with 54.86% 2025 share, benefitting from recyclability mandates.

What package format is expanding most rapidly?

Die-cut display containers grow at an 7.92% CAGR as brands seek stronger shelf impact.

How are regulations shaping material choices?

Extended Producer Responsibility fees and EU recyclability rules push converters toward single-material fiber solutions that lower end-of-life costs.

Why are converters investing in AI automation?

AI-enabled changeovers shrink downtime from hours to minutes, supporting profitable micro-batch runs and quicker response to promotional demands.

Page last updated on: