Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

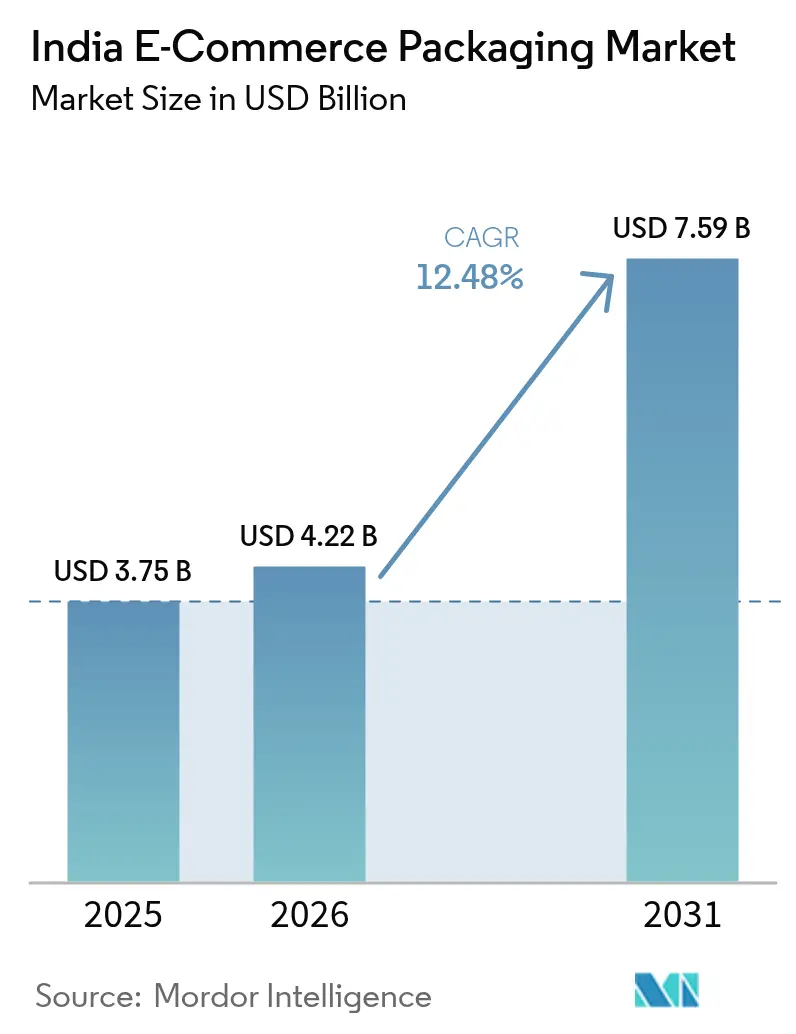

| Base Year Market Size (2025) | USD 3.75 Billion |

| Market Size (2026) | USD 4.22 Billion |

| Market Size (2031) | USD 7.59 Billion |

| Growth Rate (2026 - 2031) | 12.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India E-Commerce Packaging Market Analysis by Mordor Intelligence

India e-commerce packaging market size in 2026 is estimated at USD 4.22 billion, growing from 2025 value of USD 3.75 billion with 2031 projections showing USD 7.59 billion, growing at 12.48% CAGR over 2026-2031. Strong digital-commerce growth, government sustainability mandates, and widening 3PL networks are jointly expanding addressable demand while transforming packaging from a protective cost center into a strategic lever for customer retention. Supply-chain digitization is increasing call-off accuracy and lowering inventory buffers, which lets converters align production runs more closely with real-time order patterns. Quick-commerce players add further volume by favoring lightweight, right-sized formats that pass through micro-fulfillment hubs at speed. At the same time, paper substitution gains momentum as nationwide single-use-plastic bans push brands to migrate toward recyclable and compostable substrates.

Key Report Takeaways

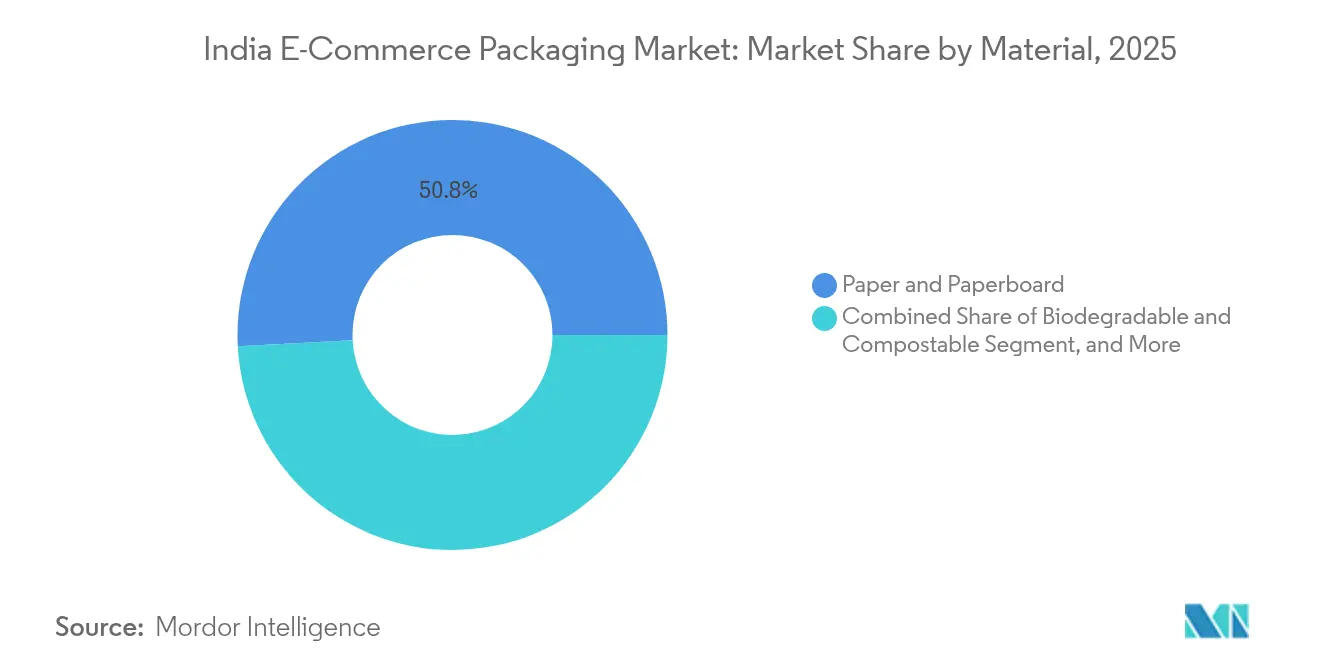

- By material, paper and paperboard held 50.83% of India e-commerce packaging market share in 2025, while biodegradable and compostable materials are projected to expand at a 14.08% CAGR through 2031.

- By packaging type, corrugated boxes led with a 45.73% share in 2025; flexible packaging is anticipated to record a 13.42% CAGR by 2031.

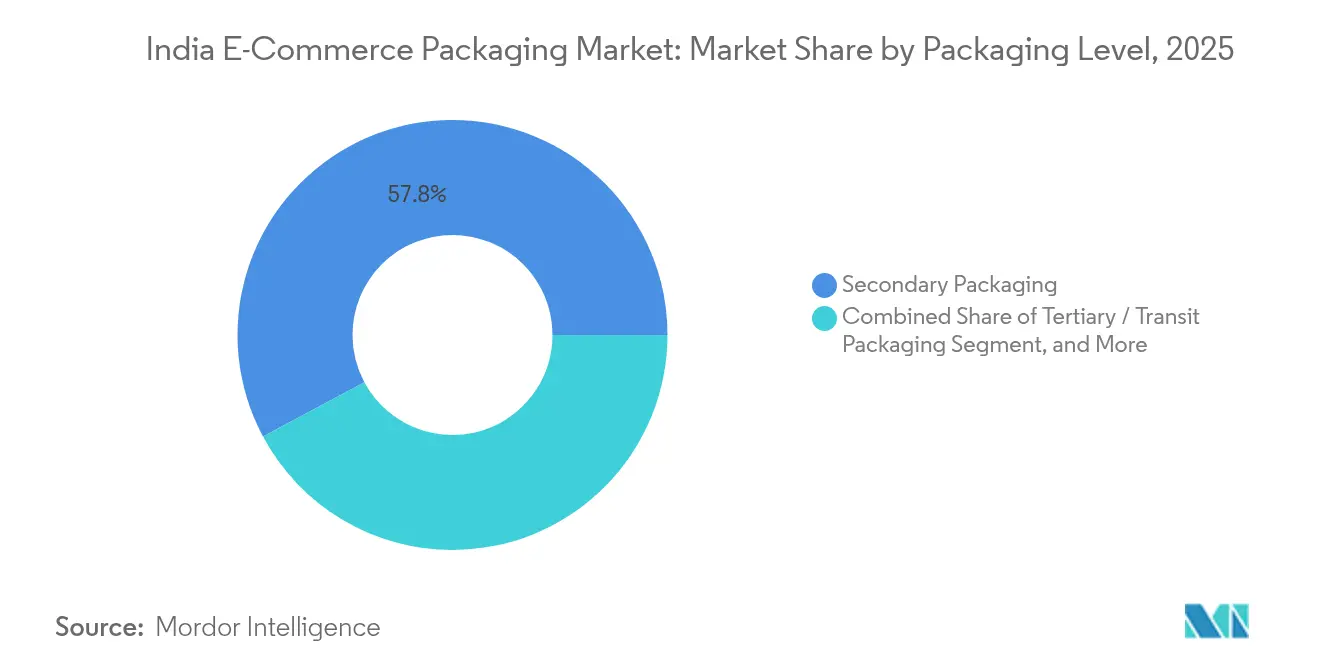

- By packaging level, secondary packaging commanded a 57.83% share in 2025; returnable and reusable formats are set to grow at a 13.54% CAGR over the same period.

- By end-user industry, personal care and cosmetics captured 27.88% of India e-commerce packaging market size in 2025, whereas fashion and apparel is forecast to register the fastest 13.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India E-Commerce Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid proliferation of online retail and omnichannel fulfillment | +3.2 | National, Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Government ban on single-use plastics accelerating paper solutions | +2.8 | Nationwide, stricter in metros | Short term (≤ 2 years) |

| Expansion of 3PL and last-mile networks lowering packaging lead-times | +2.1 | Delhi NCR, Mumbai, Bangalore | Medium term (2-4 years) |

| Quick-commerce models demanding micro-fulfillment packaging | +1.9 | Urban centers, spreading to Tier-2 | Short term (≤ 2 years) |

| AI-driven right-sizing and print-on-demand boxes | +1.4 | National, tech-enabled brands | Long term (≥ 4 years) |

| Subscription-focused D2C brands scaling recurring order volumes | +1.2 | National, beauty and nutrition hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Proliferation of Online Retail and Omnichannel Fulfillment

Omnichannel strategies oblige packaging that safeguards goods during courier shipment yet still looks retail-ready on shelf. Brand owners are re-engineering closures, liners, and outer formats to prevent leakage or scuffing, illustrated by ITC’s redesigned shower-gel caps and Parle’s extra outer wraps for bundled cookies.[3]Economic Times Bureau, “How consumer goods manufacturers adapt packaging design to dominate online sales,” economictimes.indiatimes.com QR-code integration turns boxes into gateways for loyalty programs, giving companies unmediated access to consumer behavior data. As product assortments multiply, packaging SKU counts rise, favoring suppliers able to offer modular, just-in-time solutions that minimize warehouse space.

Government Ban on Single-Use Plastics Accelerating Paper Solutions

Central and state authorities now penalize non-compliant polymers, tilting procurement toward recyclable and compostable papers. Converters are scaling barrier-coated kraft that mimics polyethylene performance yet qualifies for curbside recycling. Firms that can certify end-of-life pathways gain preferred-supplier status among large e-commerce portals. Domestic paper mills benefit from reduced import dependence, aligning with Make-in-India objectives and improving currency exposure for buyers

Expansion of 3PL and Last-Mile Networks Lowering Packaging Lead-Times

More than 250 fulfillment centers opened in 2024-2025, mainly across Tier-2 cities. Their distributed footprint enables just-in-time box deliveries that slash inventory-carrying costs for online sellers. Warehouse management systems increasingly embed packaging SKUs, prompting converters to preload stock at 3PL nodes. This embedded supplier model tempers the bullwhip effect during festive peaks and lets smaller regional plants secure anchor volumes without competing head-on with national conglomerates.

Quick-Commerce (≤ 15-min) Models Demanding Micro-Fulfillment Packaging

Ultra-fast grocery apps stipulate compact SKUs and easy-open seals to speed pick rates. Owing to minimal secondary wrapping, primary packs must resist drop shock over short courier rides. Temperature-sensitive items call for thin-wall insulated pouches that maintain cold chain without bulky outer liners. Standardized footprints allow high-density shelf stacking, elevating throughput per square foot and reducing slotting fees for brand owners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in kraft liner and recycled paper prices | −2.4 | National, paper-dependent producers | Short term (≤ 2 years) |

| Compliance burden of Extended Producer Responsibility targets | −1.8 | Nationwide, tighter in metros | Medium term (2-4 years) |

| Fragmented converting capacity causing quality variability | −1.3 | Smaller manufacturing clusters | Medium term (2-4 years) |

| Limited domestic supply of high-barrier mono-material films | −1.1 | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Kraft Liner and Recycled Paper Prices

Kraft liner spiked by up to 20% in 2024, reflecting global pulp squeezes and local currency depreciation. Many converters lack forward-buying programs, forcing quarterly renegotiations that erode gross margins. Irregular recycled fiber collection compels mills to hold extra safety stock, bloating working capital and compressing ROA during demand surges. Integrated players have started investing upstream to lock in fiber supply and stabilize cost curves.

Compliance Burden of Extended Producer Responsibility Targets

Smaller shops struggle with the reporting rigor attached to tracking plastic recovery volumes. Documentation, audit fees, and reverse-logistics spending divert capital from equipment upgrades. Brands must sometimes over-engineer packages to maximize recyclability, which can conflict with shelf-life or aesthetic requirements. Uncertainty surrounding future tightening of EPR ratios also delays capex on new substrate lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Paper Dominance Drives Sustainable Transition

Paper and paperboard accounted for 50.83% of India e-commerce packaging market share in 2025, a position underpinned by recyclability and consumer perception of natural credentials. Biodegradable and compostable variants, though currently niche, are set to grow at a 14.08% CAGR, reflecting advances in PBAT blends whose cost gap with polyethylene is narrowing. The India e-commerce packaging market size for these green materials is expected to double by 2031 as enforcement of plastic bans tightens in metropolitan jurisdictions.

Plastics retain relevance where barrier performance overrides disposal concerns, particularly for moisture-sensitive SKUs. Mono-material PE and PP laminates gain favor because they simplify mechanical recycling streams. Textile substrates like jute cater to premium gifting but remain volume-light. The Defense Research and Development Organisation’s PBAT film that degrades within three months is being licensed to more than 40 companies, suggesting domestic innovation could soon challenge imported compostables on both performance and price

By Packaging Type: Corrugated Boxes Lead Amid Flexible Packaging Innovation

Corrugated cartons delivered 45.73% of India e-commerce packaging market size in 2025 as their uniform form factor dovetailed with conveyor automation in large fulfillment hubs. Yet flexible mailers are projected to climb at a 13.42% CAGR because they save cubic space and freight cost for soft goods. Right-sized pouches also cut void fill, lowering the per-order material footprint.

Protective inserts such as molded pulp and air cushions cater to electronics and fragile categories. Tape-free locking cartons from Iinkclip Print and Cartons slash sealing time for 3PLs while eliminating adhesive waste. Bottle Buddie retail-ready packs marry e-commerce resilience with shelf visibility, proving converters can satisfy both digital and brick-and-mortar channels through modular designs.

By Packaging Level: Secondary Packaging Dominance Reflects Fulfillment Requirements

Secondary layers represented 57.83% of India e-commerce packaging market size in 2025 because items often pass through multiple handling stages before final delivery. Shippers accept the extra material cost to avoid reverse-logistics expense linked to breakage. Returnable totes and reusable mailers, although only a small base today, are advancing at a 13.54% CAGR as high-volume sellers strive for circularity.

Primary packs increasingly incorporate drop-test-qualified structures, thereby removing the need for additional outer wraps for mid-size cereals and snacks Bagrry’s shift to pouches is a case in point. Tertiary pallets remain essential for bulk B2B moves between regional consolidation centers, yet lightweight corner boards and recycled-content stretch wrap moderate overall tonnage growth.

By End-User Industry: Personal Care Leadership Amid Fashion Growth Acceleration

Personal care and cosmetics garnered a 27.88% slice of India e-commerce packaging market share in 2025. Consumers equate upscale primary packs with product efficacy, pushing brands to adopt high-gloss laminates and custom inserts. Subscription models for skincare replenish monthly, amplifying volume even when GDP growth wavers.

Fashion and apparel, posting a market-leading 13.72% CAGR, favors resealable poly-mailers that facilitate returns without repacking. Electronics demand anti-static cushioning, while food and beverage lean on high-barrier films to extend shelf life. Manjushree Technopack’s cap-and-closure acquisitions widened its SKU count, helping revenue more than double between FY18 and FY24, underlining how specialization by end-use can unlock margin uplift

Geography Analysis

Metropolitan zones anchor consumption, with Delhi NCR, Mumbai, and Bangalore together generating well over one-third of total shipments owing to dense online buyer bases and established hub-and-spoke logistics. Their proximity to converter clusters in Haryana, Maharashtra, and Karnataka accelerates sample iterations and order turnaround. Southern and western corridors exhibit earlier adoption of biodegradable formats as civic bodies rigorously enforce single-use bans.

Tier-2 agglomerations such as Jaipur, Coimbatore, and Indore are emerging as secondary demand nodes as quick-commerce players roll out dark-store networks beyond state capitals. In these cities, standardized corrugated SKUs often trump bespoke options because merchants focus on unit economics. Government Production Linked Incentive schemes spur converters to set up greenfield lines in resource-rich eastern states, diversifying geographic risk and shortening lead times to northeastern consumers.

Supply-side footprints follow raw-material logic. Paper mills congregate near forest belts in Odisha and port gateways in Gujarat to secure imported pulp. SRF’s relocation of newly acquired CPP lines from Kanpur to Indore reflects the quest for consolidated utilities, talent pools, and trunk-road access that can serve multiple regions from a single plant

Competitive Landscape

The India e-commerce packaging market remains moderately fragmented. Strategic moves increasingly revolve around vertical integration to blunt raw-material volatility; PAG’s back-to-back acquisitions of Manjushree Technopack and Pravesha Industries signal private-equity belief in scaling platforms that span rigid plastics and specialty films.[1]T. N. N. Raghunath, “PAG acquires packaging firm Pravesha Industries at enterprise value of ₹1,700 crore,” thehindubusinessline.com

Green credentials have become key differentiators. Players race to commercialize high-barrier mono-material laminates that tick recyclability boxes without sacrificing oxygen or moisture resistance. Patenting activity is brisk: Manjushree alone holds more than 50 registered designs covering tethered caps and light-weighting ribs, locking in supply contracts with multinational FMCG firms.

Mand A momentum shows no sign of cooling. 2025 has already logged six deals, including Swiss-based Wifag Polytype’s entry via Rajshree Polypack and Canpac Trends’ dual buyouts that added blister backing and folding-carton know-how.[2]PrintWeek Editorial, “Canpac Trends acquires Mumbai-based Saptagiri Packagings,” printweek.in Domestic paper groups like JK Paper are pivoting downstream to corrugation, seeking margin resilience against cyclical writing-and-printing grades

India E-Commerce Packaging Industry Leaders

Amcor plc

Mondi plc

Uflex Limited

Smurfit WestRock

Packman Packaging Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SRF Limited bought Kanpur Plastipack’s CPP business for INR 49.25 crore (USD 5.9 million), adding 7,200 tonnes of high-barrier film capacity.

- March 2025: Canpac Trends purchased Saptagiri Packagings, securing a Silvassa plant and blister-card capability.

- February 2025: JK Paper finalised its acquisition of Manipal Utility Packaging Solutions, broadening into corrugated cartons.

- January 2025: PAG invested USD 200 million to acquire Pravesha Industries, its second packaging platform in India.

India E-Commerce Packaging Market Report Scope

E-commerce is one of the largest end users of packaging in India, exploiting the opportunities in the packaging landscape with the rapid growth in the market driven by the fashion and apparel, consumer electronics, personal care industries.

The Indian e-commerce packaging market is segmented by type (boxes and protective packaging) and end-user industry (fashion and apparel, consumer electronics, food and beverage, and personal care products).

By Material

| Paper and Paperboard |

| Plastics |

| Biodegradable and Compostable |

| Textile-based Materials (Jute, Cotton) |

| Other Materials |

By Packaging Type

| Corrugated Boxes |

| Protective Packaging |

| Mailers and Envelopes |

| Flexible Packaging |

| Labels and Tapes |

| Other Packaging Types |

By Packaging Level

| Primary Packaging |

| Secondary Packaging |

| Tertiary / Transit Packaging |

| Returnable / Re-usable Packaging |

By End-user Industry

| Fashion and Apparel |

| Consumer Electronics |

| Food and Beverage |

| Personal Care and Cosmetics |

| Home and Kitchen |

| Pharmaceuticals and Healthcare |

| Other End-user Industries |

| By Material | Paper and Paperboard |

| Plastics | |

| Biodegradable and Compostable | |

| Textile-based Materials (Jute, Cotton) | |

| Other Materials | |

| By Packaging Type | Corrugated Boxes |

| Protective Packaging | |

| Mailers and Envelopes | |

| Flexible Packaging | |

| Labels and Tapes | |

| Other Packaging Types | |

| By Packaging Level | Primary Packaging |

| Secondary Packaging | |

| Tertiary / Transit Packaging | |

| Returnable / Re-usable Packaging | |

| By End-user Industry | Fashion and Apparel |

| Consumer Electronics | |

| Food and Beverage | |

| Personal Care and Cosmetics | |

| Home and Kitchen | |

| Pharmaceuticals and Healthcare | |

| Other End-user Industries |

Key Questions Answered in the Report

How large is India’s e-commerce packaging space today?

The India e-commerce packaging market size reached USD 4.22 billion in 2026 and is projected to grow at a 12.48% CAGR to USD 7.59 billion by 2031.

Which material leads demand among online sellers?

Paper and paperboard dominate with a 50.83% market share because they comply with single-use-plastic bans and align with consumer sustainability expectations.

What segment is expanding fastest?

Biodegradable and compostable materials are advancing at a 14.08% CAGR as more brands adopt PBAT and seaweed-based substrates to meet EPR goals.

How are quick-commerce models influencing packaging?

Fifteen-minute delivery services require smaller, easy-open packs that move rapidly through micro-fulfillment hubs, driving innovation in lightweight and temperature-stable formats.

Who are the main investors reshaping the sector?

PAG, SRF, JK Paper, and Wifag Polytype have recently led high-profile acquisitions, showing increasing private-equity and strategic interest in scaling packaging platforms.

Page last updated on: