E-commerce Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

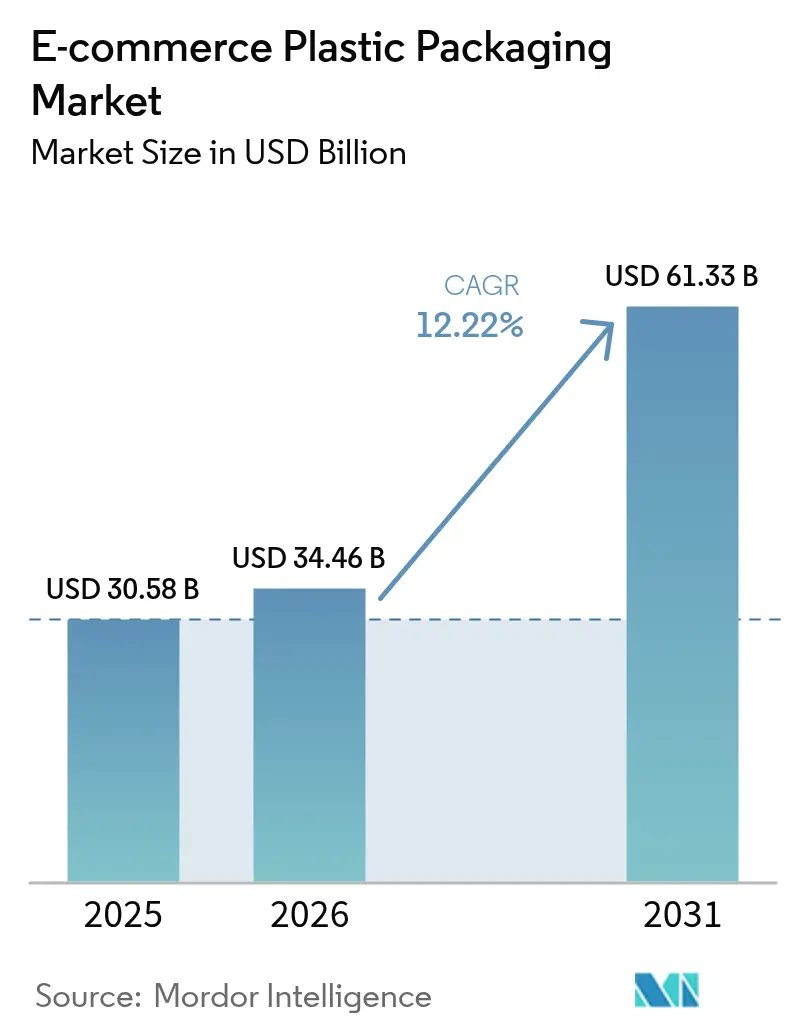

| Market Size (2026) | USD 34.46 Billion |

| Market Size (2031) | USD 61.33 Billion |

| Growth Rate (2026 - 2031) | 12.22% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-commerce Plastic Packaging Market Analysis by Mordor Intelligence

The e-commerce plastic packaging market size is projected to be USD 30.58 billion in 2025, USD 34.46 billion in 2026 and reach USD 61.33 billion by 2031, growing at a CAGR of 12.22% from 2026 to 2031. A worldwide pivot to omnichannel retail is replacing large regional distribution centers with thousands of micro-fulfillment nodes, forcing converters to supply lighter-gauge films that suit both in-store replenishment and parcel delivery. Brand-owner environmental, social and governance commitments are lifting demand for certified-compostable resins even though these materials are 30–50% more expensive than conventional polyethylene. Automated warehouses are shifting rapidly to nano-layer stretch films that trim pallet weight by up to 30%, a change that lowers carrier surcharges and expands converter margins. Asia Pacific remains the revenue anchor, but the Middle East is now the fastest growing geography, aided by Saudi Arabia’s Vision 2030 logistics investments and the United Arab Emirates’ cross-border hub strategy.

Key Report Takeaways

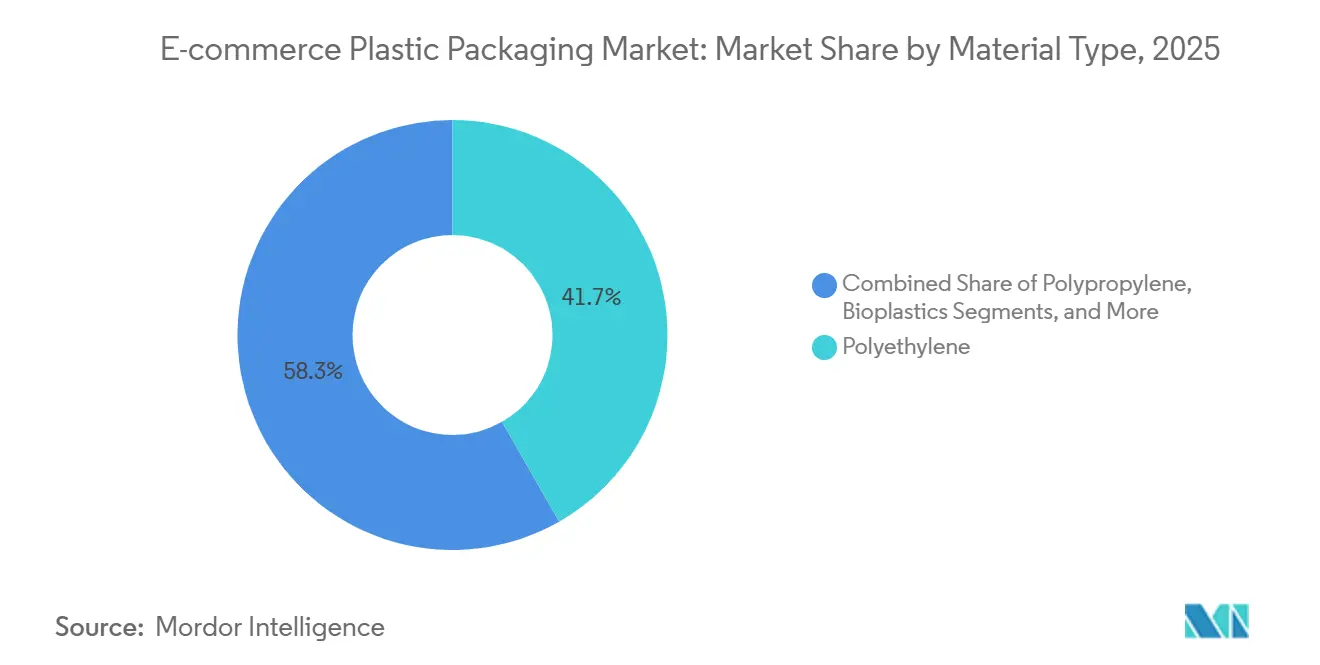

- By material type, polyethylene held 41.74% of revenue in 2025, while bioplastics are on course for a 12.84% CAGR through 2031.

- By product type, pouches and bags led with 37.61% share in 2025; protective formats are forecast to expand at a 12.55% CAGR to 2031.

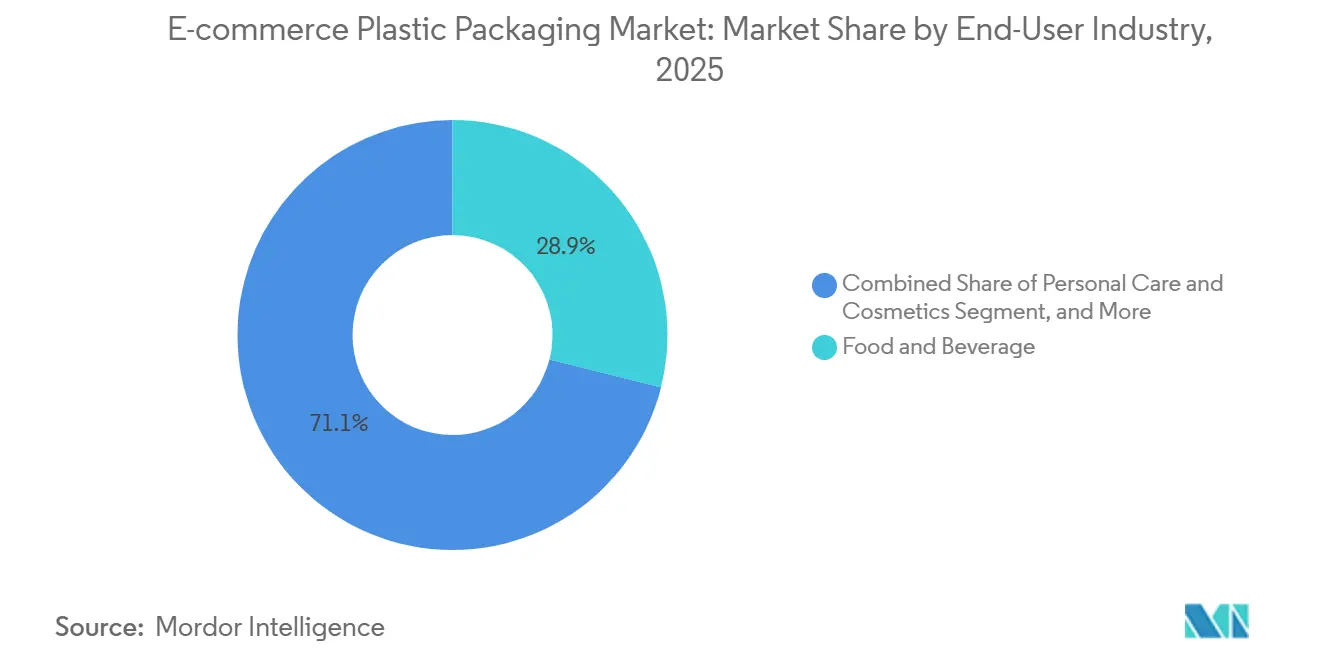

- By end-user industry, food and beverage commanded 28.93% of 2025 sales, yet personal care and cosmetics record a 13.12% CAGR to 2031.

- By packaging function, secondary packaging captured 45.83% of 2025 revenue, while palletization and stretch wrap grow fastest at 12.91% through 2031.

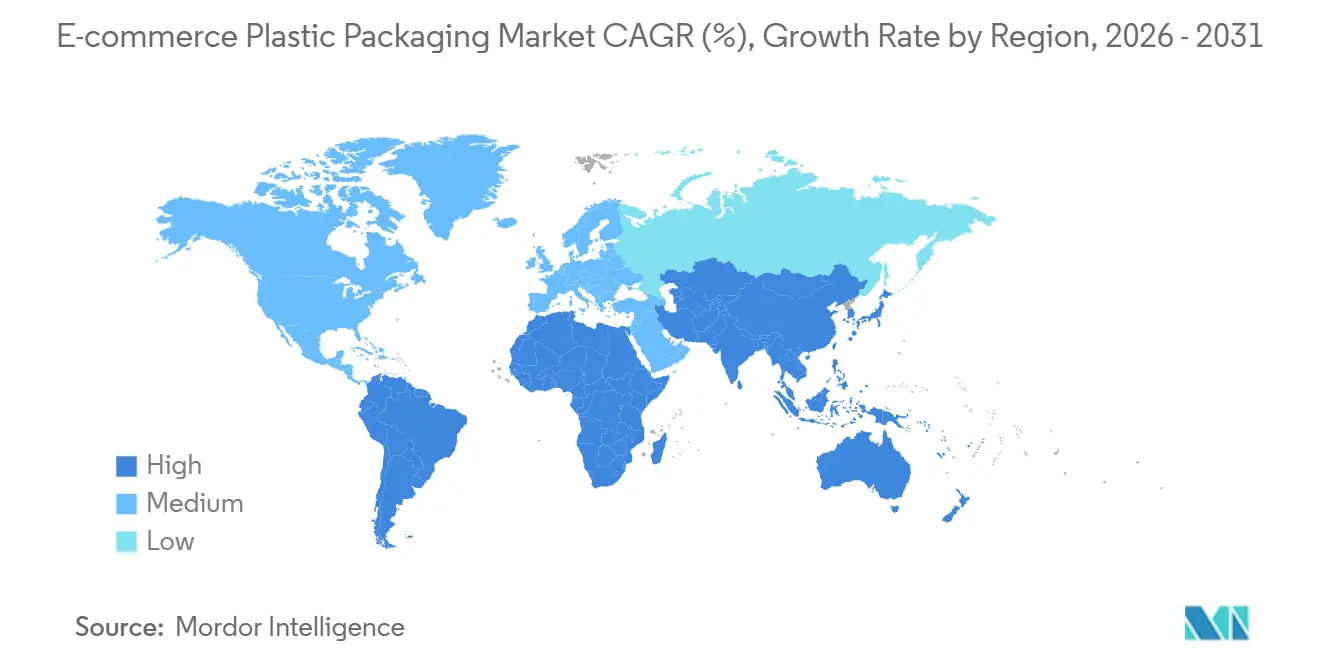

- By geography, Asia Pacific took 34.57% of 2025 revenue; the Middle East advances at a 13.04% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global E-commerce Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising penetration of online retail | +2.8% | Global, with APAC and Middle East leading | Medium term (2-4 years) |

| Growth in lightweight flexible formats | +2.1% | North America and Europe core, expanding to APAC | Short term (≤ 2 years) |

| Proliferation of omnichannel fulfillment nodes | +1.9% | North America and Western Europe, spillover to APAC | Medium term (2-4 years) |

| Brand demand for printable, design-rich plastics | +1.4% | Global, concentrated in personal care and cosmetics | Short term (≤ 2 years) |

| Surge in temperature-controlled grocery delivery | +1.7% | APAC and Middle East, emerging in Latin America | Medium term (2-4 years) |

| Rapid scaling of reusable packaging loops | +1.3% | Europe and North America pilot markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Penetration of Online Retail

China’s e-commerce gross merchandise value surpassed USD 2.8 trillion in 2025 and India is on track for USD 350 billion by 2030, creating dependable volume for the e-commerce plastic packaging market. Platform operators aggregate packaging purchases to unlock scale discounts, so converters must now bundle mailers, cushioning and thermal liners in turnkey kits.Halal labeling and Arabic text requirements limit converter options, which tilts bids toward suppliers with in-house flexographic capacity. Southeast Asian return rates of 20–30% push some brands to single-use plastics despite public sustainability goals. Seventy-six percent of United States shoppers now identify free two-day delivery as a decisive factor, compressing replenishment lead times for packaging stock-keeping units.[1]Ryder, “2024 E-commerce Consumer Study,” ryder.com

Growth in Lightweight Flexible Formats

Downgauging has cut average film thickness from 20–23 microns to 12–15 microns in three years, trimming resin usage by roughly 25% while preserving puncture resistance through nano-layer co-extrusion.[2]Manuli Stretch, “Nano-Layer Stretch Film Technology,” manuli.com Flexible stand-up pouches weigh 40% less than comparable folding cartons, saving shippers USD 0.50–1.00 per parcel on long-haul routes.[3]Amcor, “Investor Presentation 2025,” amcor.com The European Union’s 50% void-space cap accelerates uptake of on-demand air pillows that inflate on site and curbside-recyclable mailers such as Pregis EverTec Renew. Mondi’s peel-and-reseal zippers support subscription programs that justify a 15–20% premium for branded pouches. Berry Global’s 2025 stretch film with 50% post-consumer recycled content shows how recycling advances are closing the gap to virgin polyethylene in load-stability applications.

Proliferation of Omnichannel Fulfillment Nodes

North American retailers managed an average of 12 ship-from-store outlets per brand in 2025, up from 7 in 2020. Automated micro-fulfillment centers demand dispenser-ready rolls of air pillows that cut picking labor by 30%. Third-party logistics providers invite converters to co-locate extrusion lines inside warehouse campuses, trimming lead times from ten days to under 48 hours. Click-and-collect now represents 18% of European e-commerce transactions, driving need for tamper-evident resealable pouches consumers can inspect in store. Cross-border e-commerce equals 22% of online sales and forces converters to juggle multiple material-composition mandates across regions.

Brand Demand for Printable, Design-Rich Plastics

Fifty-nine percent of shoppers say visually distinctive, sustainable packaging influences repeat purchase decisions. Polypropylene mailers deliver the gloss and color fidelity beauty brands desire while shaving total pack weight by 35–40%. Pregis EverTec Poly mailers balance post-consumer recycled content with vivid print quality. Single-pass inkjet presses now cut order-to-delivery cycles to under ten days, empowering smaller converters to land short-run contracts. The upcoming European ban on per- and polyfluoroalkyl substances for food-contact packaging is pushing suppliers like CCL Industries toward water-based barrier coatings co-developed with Dow Chemical.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans and taxes on single-use plastics | -1.8% | Europe and select APAC markets, expanding globally | Short term (≤ 2 years) |

| Volatility in virgin polymer prices | -1.4% | Global, acute in regions dependent on imported resins | Short term (≤ 2 years) |

| E-commerce reverse-logistics damage rates | -0.9% | North America and Europe, emerging in APAC | Medium term (2-4 years) |

| Brand-owner ESG pledges favoring fiber formats | -1.2% | North America and Europe core, spillover to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans and Taxes on Single-Use Plastics

The European Union now requires every packaging format to be recyclable by 2030 and sets recycled-content floors up to 35%, compelling converters to re-engineer multi-layer films and buy stakes in chemical-recycling ventures. Chile, Brazil and Argentina add new fees or reverse-logistics mandates that raise converter costs 3–5% of revenue. India’s draft rules call for 20% recycled content in flexibles by 2026, yet only 60% of post-consumer plastic there is currently collected. Smaller suppliers often lack the capital to fund required retrofits, which tilts competition toward scale players.

Volatility in Virgin Polymer Prices

Polyethylene prices swung 25% in 2024, dropping from USD 1,500 to USD 1,100 per metric ton and slicing converter margins 200–300 basis points. Polypropylene followed, sliding to USD 900–1,100 per metric ton as crude prices and Chinese demand gyrated. Post-consumer recycled polyethylene commands a 10–20% premium in Europe, a gap that narrows only when crude climbs above USD 90 per barrel. Converters lacking hedging programs face working-capital stress, prompting contract renegotiations and sector consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Certified-Compostable Resins Erode Polyethylene Dominance

Polyethylene retained the largest stake in 2025, yet bioplastics’ 12.84% CAGR signals steady migration of procurement budgets toward compostable grades. Low-density polyethylene still rules void-fill and bubble applications, while high-density variants thrive in mailers and thin stretch wrap that target downgauging. Polypropylene solves printability demands for temperature-controlled grocery mailers and cosmetic pouches, and polyethylene terephthalate is limited to rigid clamshells in consumer electronics.

Bioplastic suppliers such as EcoEnclose and Notpla won ASTM D6400 certification in 2025, but municipal composters accept fewer than 30% of incoming items, restraining volume growth. Monash University demonstrated polyhydroxyalkanoate films derived from food waste with mechanical strength within 10% of low-density polyethylene, though scale-up hinges on fermentation capacity. Regulatory phase-outs push polyvinyl chloride and polystyrene below a combined 3% share by 2031.

By Product Type: Protective Formats Capture High-Damage Categories

Pouches and bags held a 37.61% share in 2025 because parcel carriers price shipments on dimensional weight, favoring lighter packs. Protective packaging grows at 12.55% as brands over-engineer cushioning to counter reverse-logistics damage rates approaching 30%.

Bubble wrap drops share to on-demand air pillows that reduce warehouse storage 95% and now contain 50% recycled content. Nano-layer stretch films gauge down to 12–15 microns and still secure pallets, saving 30% resin. Ranpak and Storopack accelerate paper-based cushioning, but plastic formats integrate into bundled kits that fuse an outer mailer with inner air cells, an offering ProAmpac scaled after its PAC Worldwide deal.

By End-User Industry: Personal Care Leads the Growth Curve

Food and beverage drove 28.93% of 2025 revenue through temperature-controlled grocery deliveries that require 2–8 °C mailers. Personal care and cosmetics show the quickest rise at a 13.12% CAGR as beauty brands replace rigid cartons with printable polypropylene pouches that cut parcel weight 40%.

Consumer electronics is settling into maturity; slower smartphone upgrades and streaming adoption reduce demand for rigid clamshells. Apparel retailers migrate to paper mailers to meet 2030 virgin-plastic-reduction promises even in humid climates. Niche sectors such as pharmaceuticals lean on specialized multilayer films that satisfy air-cargo rules, a space dominated by Sonoco ThermoSafe.

By Packaging Function: Palletization Surges on Micro-Fulfillment Adoption

Secondary formats captured 45.83% of 2025 revenue because they protect primary packs in multi-modal channels. However, palletization and stretch wrap outpace all functions with a 12.91% CAGR as retailers multiply micro-fulfillment centers and chase freight savings from 30% lighter pallets.

Primary packaging inches forward with direct-to-consumer models that drop wholesalers, exemplified by Mondi recyclable pouches with peel-and-reseal tapas. Void-fill systems split into on-demand and pre-formed; the on-demand share rises because 95% storage savings free warehouse space, a fact that boosts Pregis AirSpeed roll sales.

Geography Analysis

Asia Pacific contributed 34.57% of global revenue in 2025 thanks to China’s 52% online penetration rate and India’s surging gross merchandise value. E-commerce plastic packaging market share gains in the region rest on large domestic converter networks that localize polyethylene film supply and bypass currency swings.

North America supplied about 28% of 2025 sales, but volume moderates as plastic mailers are swapped for fiber solutions in apparel and media shipments. Retailers now manage 12 ship-from-store locations on average, fragmenting packaging demand across dozens of stock-keeping units. Europe held roughly 24% of sales yet faces the stiffest regulatory burden, with a binding 2030 recyclability mandate that forces converters to invest heavily in chemical recycling.

The Middle East advances fastest at 13.04% CAGR, powered by Saudi logistics corridors and United Arab Emirates hub-and-spoke fulfillment models that require temperature-controlled mailers and Arabic printed polypropylene pouches. South America wrestles with producer-responsibility fees that add 3–5% to converter operating costs and accelerate consolidation. Africa remains nascent but mobile-payment growth and port upgrades funded by Chinese investors create early demand for low-cost mailers.

Competitive Landscape

The top five converters—Amcor, Sealed Air, Pregis, Mondi and Berry Global—control about 35% of global capacity, indicating a moderately fragmented e-commerce plastic packaging market. Sealed Air’s pending USD 10.3 billion sale to CD&R, the April 2025 Amcor-Berry merger, and ProAmpac’s 2024 PAC Worldwide acquisition highlight a private-equity drive to bundle protective-packaging assets into integrated contracts that cross-sell mailers, air pillows and stretch films.

Regional specialists win share by installing extrusion lines inside third-party logistics campuses and guaranteeing 24-hour replenishment. Technology also separates winners: nano-layer co-extrusion chops resin use 30%; on-demand inflation collapses storage footprints by 95%; single-pass digital presses shrink delivery windows under 10 days.

Disruptors such as EcoEnclose and Returnity prove reusable loops can survive 20 or more trips, pushing incumbents to pilot take-back programs. Patent filings concentrate on PFAS-free grease barriers, where CCL Industries and Dow Chemical lodged a 2025 application under the Patent Cooperation Treaty. FlexiPack and similar challengers employ co-manufacturing deals that waive high minimums, letting subscription-box startups order fewer than 50,000 units and bypass the scale converters’ thresholds.

E-commerce Plastic Packaging Industry Leaders

Amcor plc

Sealed Air Corporation

Pregis LLC

Sonoco Products Company

Storopack Hans Reichenecker GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Sealed Air’s USD 10.3 billion acquisition by CD&R is expected to close mid-year, consolidating air-pillow and mailer portfolios under one roof

- April 2025: Amcor completed its merger with Berry Global, creating a USD 24 billion revenue leader in flexible pouches and stretch films with USD 650 million synergy upside

- March 2025: ProAmpac bought PAC Worldwide’s mailer operations, adding 200 million units of annual capacity and a flexographic press co-located in a Midwest distribution hub

- February 2025: Mondi launched FlexiBag Recyclable, a polyethylene pouch with peel-and-reseal closure certified by the Association of Plastic Recyclers

Global E-commerce Plastic Packaging Market Report Scope

E-commerce plastic packaging refers to plastic-based materials specifically designed to pack, protect, ship, and deliver products sold through online retail channels. Unlike traditional retail packaging (which focuses on shelf display), e-commerce packaging prioritizes durability, lightweighting, cost efficiency, and product protection during transit.

The E-commerce Plastic Packaging Market Report is Segmented by Material Type (Polyethylene including LDPE and HDPE, Polypropylene, PET, Bioplastics, Other Material Types), Product Type (Pouches and Bags, Mailers and Envelopes, Shrink and Stretch Films, Protective Packaging including Bubble Wrap, Air Pillows, Foam-in-Place, Other Product Types), End-user Industry (Consumer Electronics and Media, Food and Beverage, Personal Care and Cosmetics, Fashion and Apparel, Home Care and Furnishing, Other End-user Industries), Packaging Function (Primary Packaging, Secondary Packaging, Void-Fill and Cushioning, Palletization/Stretch Wrap), and Geography (North America, South America, Europe, APAC, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Polyethylene (PE) | Low-Density PE (LDPE) |

| High-Density PE (HDPE) | |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Bioplastics | |

| Other Material Types |

| Pouches and Bags | |

| Mailers and Envelopes | |

| Shrink and Stretch Films | |

| Protective Packaging | Bubble Wrap |

| Air Pillows | |

| Foam-in-Place | |

| Other Product Types |

| Consumer Electronics and Media |

| Food and Beverage |

| Personal Care and Cosmetics |

| Fashion and Apparel |

| Home Care and Furnishing |

| Other End-user Industries |

| Primary Packaging |

| Secondary Packaging |

| Void-Fill and Cushioning |

| Palletization / Stretch Wrap |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Material Type | Polyethylene (PE) | Low-Density PE (LDPE) |

| High-Density PE (HDPE) | ||

| Polypropylene (PP) | ||

| Polyethylene Terephthalate (PET) | ||

| Bioplastics | ||

| Other Material Types | ||

| By Product Type | Pouches and Bags | |

| Mailers and Envelopes | ||

| Shrink and Stretch Films | ||

| Protective Packaging | Bubble Wrap | |

| Air Pillows | ||

| Foam-in-Place | ||

| Other Product Types | ||

| By End-user Industry | Consumer Electronics and Media | |

| Food and Beverage | ||

| Personal Care and Cosmetics | ||

| Fashion and Apparel | ||

| Home Care and Furnishing | ||

| Other End-user Industries | ||

| By Packaging Function | Primary Packaging | |

| Secondary Packaging | ||

| Void-Fill and Cushioning | ||

| Palletization / Stretch Wrap | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the e-commerce plastic packaging market be by 2031?

It is expected to reach USD 61.33 billion, growing at a 12.22% CAGR from 2026 to 2031.

Which material type is growing fastest?

Certified-compostable bioplastics post a 12.84% CAGR as brands pivot to ESG-aligned resins.

Why is palletization demand rising so quickly?

Automated micro-fulfillment facilities prefer thinner nano-layer stretch films that cut pallet weight 30% without sacrificing load security.

Which region shows the highest growth through 2031?

The Middle East leads with a 13.04% CAGR, supported by Saudi and UAE logistics investments.

What is driving consolidation among converters?

Private-equity sponsors are bundling protective formats into single contracts to cross-sell mailers, air pillows and stretch films while gaining scale efficiencies.

How are regulations reshaping product design?

The European Union’s 2030 recyclability mandate and recycled-content floors compel converters to re-engineer multi-layer films and invest in chemical-recycling capacity.

Page last updated on: