Electric Vehicle Thermal Management System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

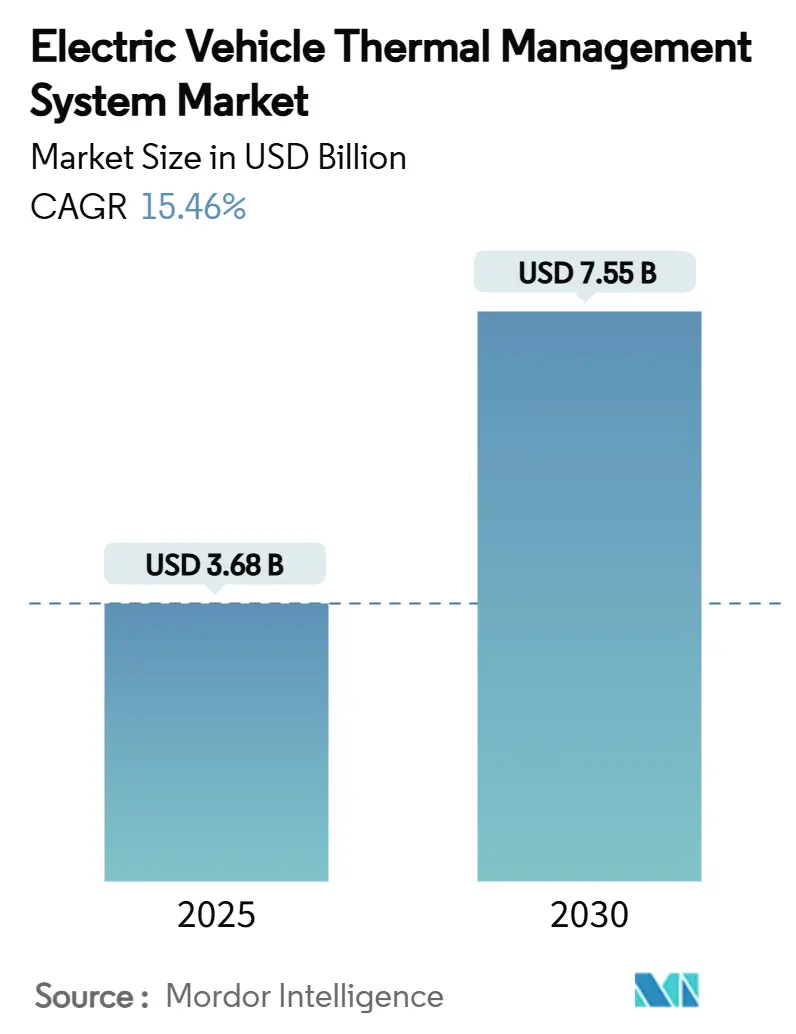

| Market Size (2025) | USD 3.68 Billion |

| Market Size (2030) | USD 7.55 Billion |

| Growth Rate (2025 - 2030) | 15.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle Thermal Management System Market Analysis by Mordor Intelligence

The electric vehicle thermal management system market size stands at USD 3.68 billion in 2025 and is forecast to reach USD 7.55 billion by 2030, expanding at a 15.46% CAGR. This upward curve is anchored in higher battery energy densities, the spread of 350 kW fast-charge networks, and stricter battery-safety rules that convert thermal subsystems from auxiliary parts to core value drivers. Battery-pack, inverter, and motor heat loads are rising in step with power-train efficiencies, so automakers now adopt multi-loop cooling, immersion fluids, and heat-pump HVAC to contain cell temperatures between 15 °C and 35 °C. Commercial-vehicle electrification adds further impetus because heavier packs and continuous duty cycles amplify cooling demand, pushing suppliers toward larger plate heat exchangers, dielectric coolants, and AI-enabled controllers. Supply security for low-conductivity coolants and advanced gap fillers remains a gating factor, yet investors see attractive scale economics as gigafactories design immersion-ready packs and integrated thermal loops.

Key Report Takeaways

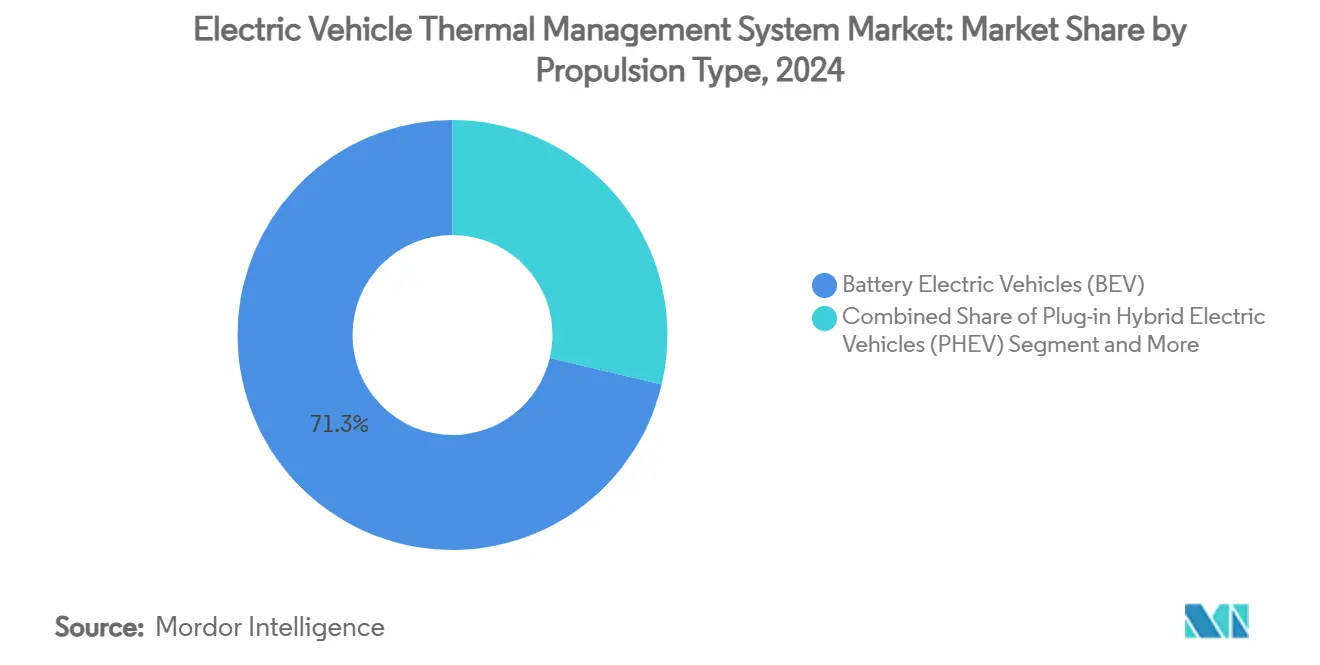

- By propulsion type, battery electric vehicles held 71.28% of the electric vehicle thermal management system market share in 2024; fuel-cell electric vehicles are projected to grow at a 16.06% CAGR through 2030.

- By application, battery cooling accounted for 42.35% of the electric vehicle thermal management system market size in 2024 and is advancing at a 15.89% CAGR to 2030.

- By cooling technology, active systems retained 58.77% revenue share in 2024, while hybrid/integrated loops are set for a 17.03% CAGR during the forecast period.

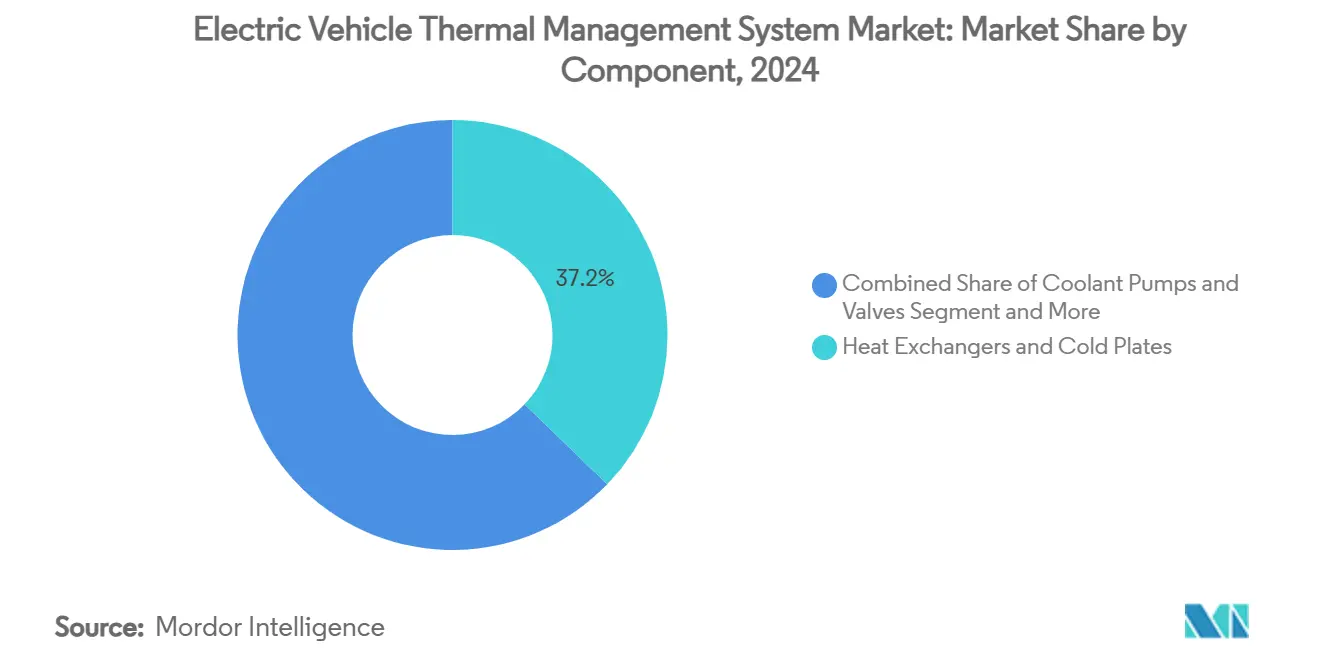

- By component, heat exchangers and cold plates commanded 37.24% revenue share in 2024; thermal interface and gap-filler materials are climbing fastest at a 16.55% CAGR.

- By vehicle type, passenger cars led with a 64.71% share in 2024, whereas heavy commercial vehicles are on track for a 17.35% CAGR from 2025-2030.

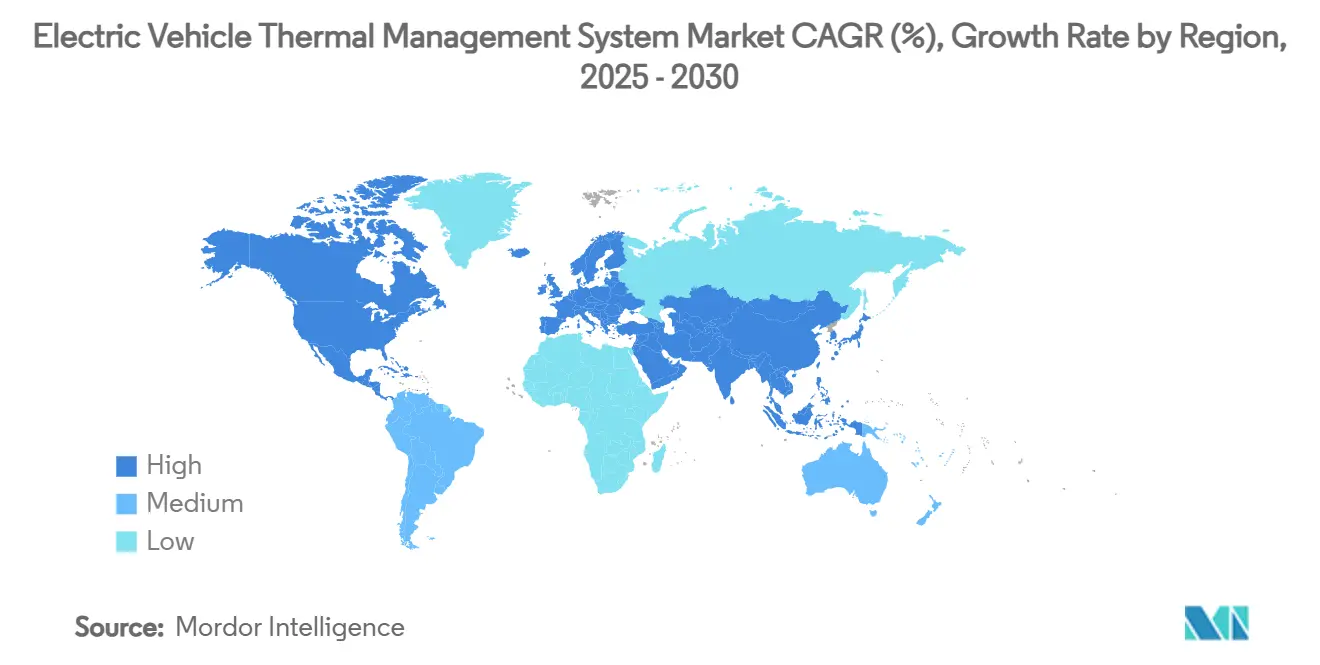

- Asia-Pacific captured 48.15% of the electric vehicle thermal management system market in 2024 and is expected to post a 16.94% CAGR through 2030.

Global Electric Vehicle Thermal Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Surge in BEV & PHEV Production | +3.2% | Global, APAC lead | Short term (≤ 2 years) |

| Tightening Battery Safety & Homologation Norms | +2.8% | EU, North America | Medium term (2-4 years) |

| Adoption of Heat-Pump HVAC for Winter Range | +2.1% | North America, EU | Medium term (2-4 years) |

| Rise in 350 kW+ Ultra-Fast Charging Networks | +1.9% | Germany, China, California | Short term (≤ 2 years) |

| AI-Based Predictive Thermal Management | +1.7% | APAC core | Long term (≥ 4 years) |

| Gigafactories Adopting Immersion-Cooled Pack Designs | +1.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global BEV and PHEV Production Volumes

Rising BEV and PHEV builds are pushing thermal loads beyond legacy auto cooling limits. Annual BEV output is expected to surpass 20 million units by 2030, lifting demand for multi-loop systems that keep cells within a narrow 15 °C-35 °C window. Honda’s CAD 15 billion Canadian supply-chain investment integrates thermal design upstream, illustrating how capacity scale brings cost leverage for advanced coolers. Commercial fleets add complexity because rapid-charge duty cycles drive hotter transient peaks, encouraging suppliers to automate plate brazing and vacuum-degassed coolant filling for consistency. These volumes also underpin capital spend on immersion-ready pack workshops that shorten manufacturing takt times.

Stringent Battery-Safety Regulations and Homologation Tests

NHTSA’s FMVSS 305a and comparable EU rules oblige automakers to stop thermal propagation between cells for passenger safety [1]National Highway Traffic Safety Administration, “Federal Motor Vehicle Safety Standard No. 305a,” nhtsa.gov. Compliance forces integrated sensing, isolation valves, and active coolant shunts capable of sub-second response. China’s pending GB 29743.2 caps fluid conductivity, spurring fluid formulators to suppress ion ingress while sustaining 0.5 W/m-K thermal conductance. The rule-setting cycle, therefore, widens the electric vehicle thermal management system market as retrofits join new-model demand, and promote ceramifiable silicone pads that retain dielectric strength even at 600 °C.

Adoption of Heat-Pump HVAC Architectures to Extend Winter Range

Heat pumps triple heating efficiency versus resistive elements, freeing 15-20% winter driving range while harvesting waste motor heat. Tesla’s system rollout across its portfolio validated field gains and set a benchmark other OEMs now pursue. Integrating the refrigerant loop with battery chillers, however, mandates precise valve staging so cabin comfort does not starve pack cooling. Tier-one suppliers answer with compact header modules that combine coolant, refrigerant, and low-GWP R290 management in one cast housing.

Surge in 350 kW+ Ultra-Fast Charging Infrastructure

Next-gen chargers dump more than 1 kW thermal load per module, so cells must be pre-conditioned to roughly 30 °C for ionic stability. Hyundai Mobis demonstrated pulsating heat pipes that raise surface heat-transfer coefficients tenfold inside a 0.8 mm envelope [2]Hyundai Mobis, “Pulsating Heat Pipe Solution for Ultra-Fast Charging,” mobis.co.kr. Infrastructure operators are exploring on-site chillers that exchange coolant through vehicle inlets during the charging session, a scenario that expands the electric vehicle thermal management system market beyond on-board hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Phase-Change and Gap-Filler | -2.4% | Global, cost-sensitive markets | Short term (≤ 2 years) |

| Packaging Complexity Within Skateboard Platforms | -1.8% | Premium EVs worldwide | Medium term (2-4 years) |

| Supply Bottlenecks for Specialty Dielectric Coolants | -1.6% | APAC shortages | Short term (≤ 2 years) |

| End-of-Life Recyclability Issues of Thermal Interface Materials | -1.1% | EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Phase-Change and Gap-Filler Materials

Automotive-grade PCMs and silicone gels can equal 15-20% of full thermal-system spend, raising the bill for volume EVs. Dow’s TC-3080 gel meets 6.5 W/m-K but trades above USD 50 per kg, squeezing entry-segment unit economics[3]Dow Inc., “DOWSIL TC-3080 Curable Thermal Gel Data Sheet,” dow.com. Material scientists pursue hybrid fillers, boron nitride plus graphite flakes, to shave cost while retaining dielectric breakdown margins. Larger pack formats in buses multiply dosage, amplifying this restraint inside the electric vehicle thermal management system market.

Packaging Complexity Within Skateboard Platforms

Flat-pack chassis free interior room yet crowd cooling lines, pumps, and valves into slim sill channels. Engineers often route three-way valves near side-crash zones, which inflates tooling for bracketry and crash testing. Premium brands address the issue with multi-functional cold plates doubling as structural ribs, but this refinement slows design cycles and raises validation outlay, tempering near-term electric vehicle thermal management system market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: FCEVs Drive Future Growth

FCEVs posted the fastest 16.06% CAGR while BEVs held 71.28% revenue in 2024, securing the largest slice of the electric vehicle thermal management system market size. Fuel-cell stacks, hydrogen tanks, and high-voltage batteries together spur triple-circuit architectures that lift the bill-of-materials and sensor count per vehicle. Mercedes-Benz patents map stack-specific plate channels that insulate humidified air zones from 80 °C coolant, signaling the high technical entry bar.

Thermal suppliers respond with modular cold-plate kits adaptable to BEV or FCEV duty to hedge volume uncertainty. Plug-in hybrids maintain a sizeable share yet lose capital priority as automakers steer R&D to pure electrics. This dynamic keeps the electric vehicle thermal management system market in a dual-track mode: scale business from BEVs and margin growth from FCEV specialization.

By Application: Battery Cooling Dominates Market

Battery cooling systems absorbed 42.35% of revenue in 2024 and carry the highest 15.89% CAGR, anchoring the electric vehicle thermal management system market share through 2030. Higher nickel chemistries and 4C charging intensify the need for fine-mesh micro-channel plates and immersion fluids. TI Fluid Systems estimates optimized coolers can add 20% driving range by shrinking temperature deltas.

Motor and inverter loops follow as inverter switching jumps to 800 V SiC. Cabin HVAC heat-pumps climb as regulation in cold-weather markets normalize range-retention metrics. Cross-linking these loads into unified loops lowers part count but raises control-logic complexity, a tradeoff that vendors meet with multi-zone controllers and cloud-fed predictive software.

By Cooling Technology: Hybrid Systems Gain Momentum

Active liquid and refrigerant solutions kept 58.77% revenue in 2024 yet hybrid architectures clock a 17.03% CAGR, the quickest inside the electric vehicle thermal management system market. Designers blend heat pipes and immersion baths to balance weight, energy draw, and spatial limits. MDPI research shows nanofluid-aided pipe plus immersion can cut peak cell temperature by 49.43% versus baseline plates.

Passive PCM panels still serve peak-shaving roles during hill climbs or trailer towing. Forced-air remains in motorcycles and entry scooters where pack capacities stay small. Over time, economies of scope favor integrated loops that share pumps and sensors across applications.

By Component: Thermal Interface Materials Lead Growth

Heat exchangers and cold plates retained 37.24% value in 2024, anchoring the electric vehicle thermal management system market, but thermal interface materials will grow 16.55% by 2030. Rongtai’s USD 41 million Thai mica line shows regional diversification to meet demand for 10 W/m-K fillers. Coolant pumps adopt brushless motors for variable flow, while smart valves integrate position sensors to orchestrate multi-loop mixers.

Software, firmware, and diagnostics gain weight as AI prediction enters the value stack. Suppliers bundle digital twins with hardware, creating recurring revenue by tuning flow set-points over-the-air. Hardware modularity plus software services reinforce the competitive moat.

By Vehicle Type: Commercial Vehicles Accelerate

Passenger cars still held 64.71% revenue in 2024; heavy commercial vehicles logged the swiftest 17.35% CAGR, adding fresh scale to the electric vehicle thermal management system market size. Packs above 300 kWh force dual-flow plates and redundant pumps for safety. Continuous operation exposes thermal fatigue, pushing vendors to stainless micro-channels and low-viscosity coolants for lower pressure drop.

Bus HVAC loads also climb, so integrators mount roof condensers with liquid-to-vapor ejector loops to cut compressor work at idle. Light vans trail yet surge with e-commerce demand, using standardized under-floor plate modules to ease upfitter conversions.

Geography Analysis

Asia-Pacific commanded 48.15% revenue in 2024 and is advancing at a 16.94% CAGR, underscoring the region’s centrality to the electric vehicle thermal management system market. China’s stimulus packages and looming GB 29743.2 dielectric rules push local suppliers toward low-conductivity fluids and high-throughput plate stamping. Japan nurtures compact heat-pump know-how, and India’s bus electrification tenders open volume lanes for ruggedized coolant modules.

North America benefits from CAD 15 billion in Honda investments and federal incentives that favor domestic content. Bosch’s USD 225 million Roseville fab will anchor SiC inverter and thermal-sensor output, closing supply loops. Stringent FMVSS 305a rules drive early adoption of cell-level fire-blockers and fast-response coolant valves, positioning the region as a compliance technology showcase within the electric vehicle thermal management system market.

Europe blends premium EV platforms with tough sustainability codes. Battery passports and recyclability mandates accelerate R&D on bio-sourced coolants and reversible TIM sheets. Germany’s InnoTherMS consortium pilots immersion cooling in 800 V sports cars, while France funds cryogenic gap-filler foam research. The region’s policy-tech mix shapes future benchmarks that ripple outward, sustaining global innovation cycles.

Competitive Landscape

The electric vehicle thermal management system market is moderately fragmented yet innovation-intensive. DENSO, Hanon Systems, MAHLE, Valeo, and Vitesco leverage tier-one footprints, securing multi-platform nominations and pooling R&D across powertrain and HVAC. Newcomers such as ZF’s TherMaS platform carve share through compact integrated modules announced in June 2025.

Strategic moves gravitate to vertical integration. Hanon Systems scales in-house dielectric fluid blending, while Dow pilots closed-loop silicone pad recycling. Partnerships proliferate: Vitesco aligns with Sanden on R290 refrigerant mini-compressors to marry eco-friendly fluids with heat-pump gains.

Patent filings reveal over 2,000 active families around immersion trays, phase-change pads, and AI controls, with Mercedes-Benz holding a deep stack of stack-cell cooling plates. Competitors invest in digital twins and cloud analytics to lock in life-cycle service contracts, widening revenue beyond hardware. Niche disruptors explore solid-state Peltier coolers and graphene spreaders, positioning for next-gen battery chemistries.

Electric Vehicle Thermal Management System Industry Leaders

DENSO Corporation

Hanon Systems

MAHLE GmbH

Valeo SE

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ZF introduced TherMaS, a compact thermal management module that improves system efficiency and lowers cost.

- April 2025: Infineon unveiled next-gen IGBT and RC-IGBT devices with enhanced thermal characteristics aimed at EV power systems.

- July 2024: TI Fluid Systems opened an e-Mobility Innovation Center in Michigan to cut prototype cycles for thermal subsystems.

- April 2024: Vitesco Technologies and Sanden International partnered on an integrated R290 refrigerant thermal management unit for BEVs.

Global Electric Vehicle Thermal Management System Market Report Scope

| Battery Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Hybrid Electric Vehicles (HEV) |

| Fuel-Cell Electric Vehicles (FCEV) |

| Battery Cooling System |

| Motor/Inverter Cooling |

| Cabin HVAC and Heat Pump |

| Transmission/Power-Electronics Cooling |

| Active (Liquid, Refrigerant-Based, Forced-Air) |

| Passive (PCM, Heat-Pipe, Graphite Sheet) |

| Hybrid/Integrated Thermal Loops |

| Coolant Pumps and Valves |

| Heat Exchangers and Cold Plates |

| Thermal Interface and Gap-Filler Materials |

| Sensors, Controllers and Software |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium Commercial Vehicles |

| Heavy Commercial Vehicles |

| Buses and Coaches |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Propulsion Type | Battery Electric Vehicles (BEV) | |

| Plug-in Hybrid Electric Vehicles (PHEV) | ||

| Hybrid Electric Vehicles (HEV) | ||

| Fuel-Cell Electric Vehicles (FCEV) | ||

| By Application | Battery Cooling System | |

| Motor/Inverter Cooling | ||

| Cabin HVAC and Heat Pump | ||

| Transmission/Power-Electronics Cooling | ||

| By Cooling Technology | Active (Liquid, Refrigerant-Based, Forced-Air) | |

| Passive (PCM, Heat-Pipe, Graphite Sheet) | ||

| Hybrid/Integrated Thermal Loops | ||

| By Component | Coolant Pumps and Valves | |

| Heat Exchangers and Cold Plates | ||

| Thermal Interface and Gap-Filler Materials | ||

| Sensors, Controllers and Software | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the electric vehicle thermal management system market?

The market stands at USD 3.68 billion in 2025 and is projected to double to USD 7.55 billion by 2030.

Which application generates the highest revenue?

Battery cooling leads with 42.35% of 2024 revenue and shows the fastest 15.89% CAGR through 2030.

Which region grows the fastest?

Asia-Pacific records a 16.94% CAGR driven by China’s manufacturing scale and policy support.

What technology trend shapes future thermal systems?

Hybrid cooling loops that blend liquid, refrigerant, and immersion techniques post a 17.03% CAGR as they match diverse heat-load profiles.

Page last updated on: