Electric Vehicle Motor Controller Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

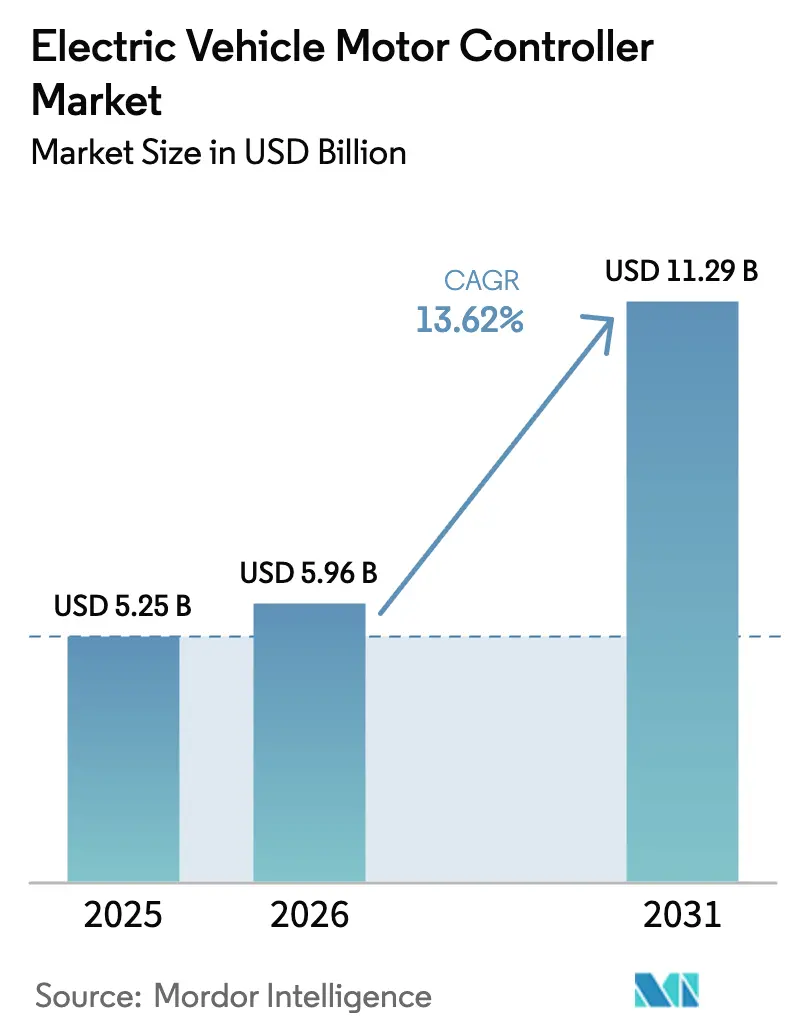

| Market Size (2026) | USD 5.96 Billion |

| Market Size (2031) | USD 11.29 Billion |

| Growth Rate (2026 - 2031) | 13.62% CAGR |

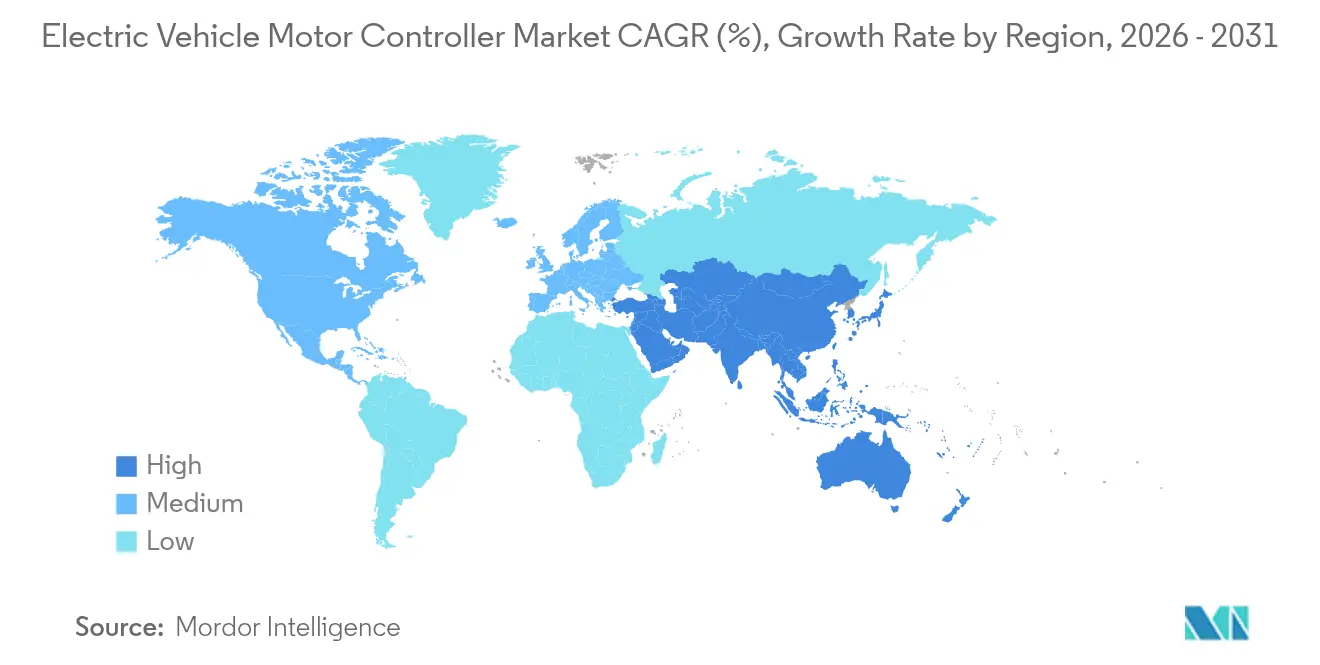

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

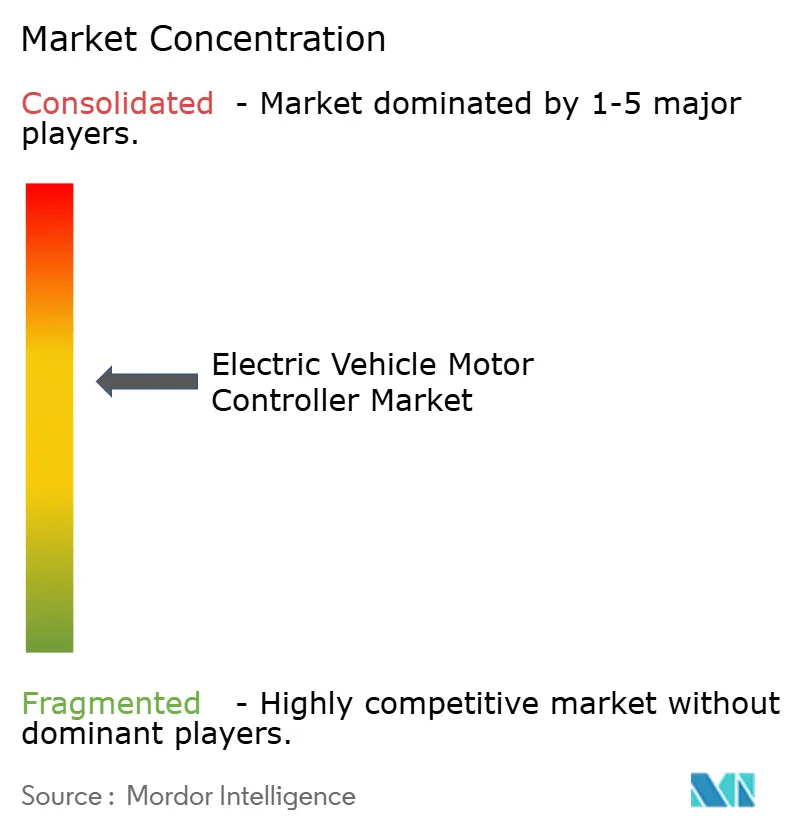

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle Motor Controller Market Analysis by Mordor Intelligence

Electric vehicle motor controller market size in 2026 is estimated at USD 5.96 billion, growing from 2025 value of USD 5.25 billion with 2031 projections showing USD 11.29 billion, growing at 13.62% CAGR over 2026-2031. Growth rests on strict global emissions rules, wider use of wide-bandgap semiconductors, and the steady move from hybrids to pure battery platforms. Asia Pacific leads demand on the back of sustained Chinese subsidies, dense supplier clusters, and rising mid-range passenger-car volumes. Silicon-carbide power devices are moving rapidly from premium cars into mainstream models, trimming switching losses and enabling 800 V architectures that cut charging time. Passenger cars still anchor volumes, yet heavy commercial vehicles post the fastest gains as fleet operators chase lower operating costs and regulatory compliance. Controller makers focusing on bidirectional V2G functions, thermal-management advances, and modular designs secure early design wins supporting scale and differentiation.

Key Report Takeaways

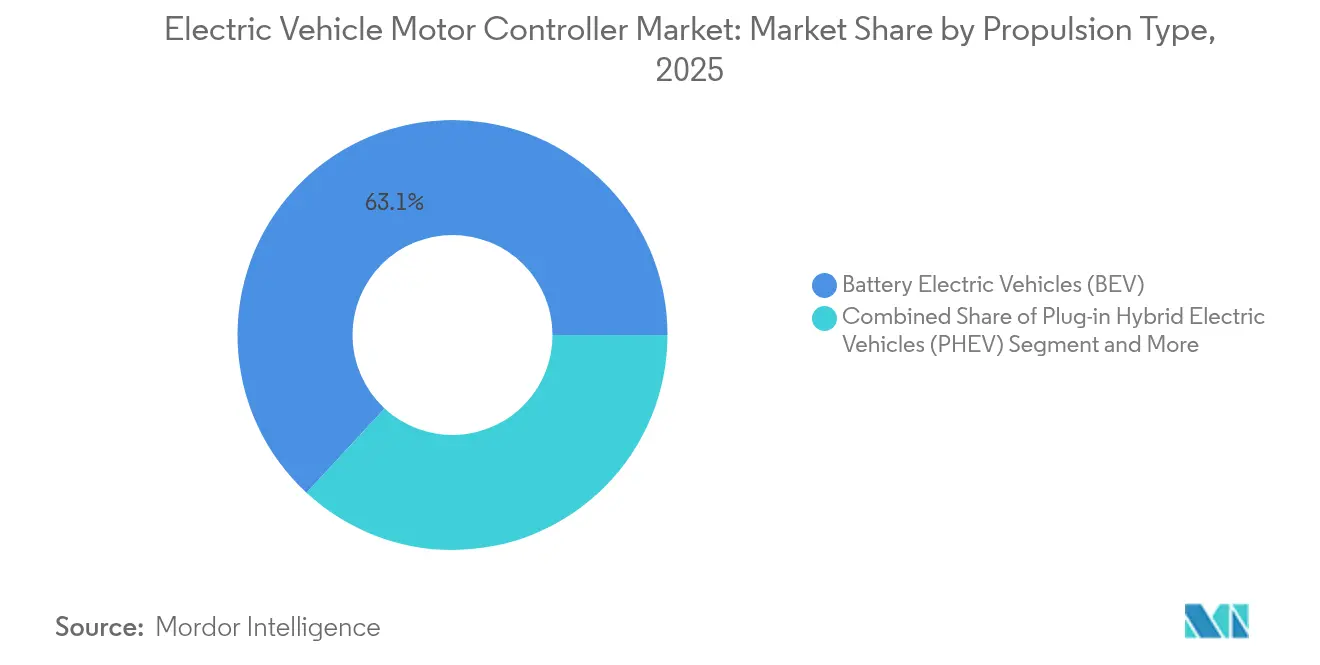

- By propulsion type, battery electric vehicles held 63.12% of electric vehicle motor controller market share in 2025, while fuel cell electric vehicles are projected to grow at 20.68% CAGR to 2031.

- By power output, the 40-80 kW segment controlled 44.62% share of the electric vehicle motor controller market size in 2025; output above 200 kW is the fastest-expanding range at 14.11% CAGR through 2031.

- By motor type, permanent-magnet synchronous motors led with a 57.86% share of the electric vehicle motor controller market size in 2025, while switched-reluctance designs are advancing at a 16.29% CAGR.

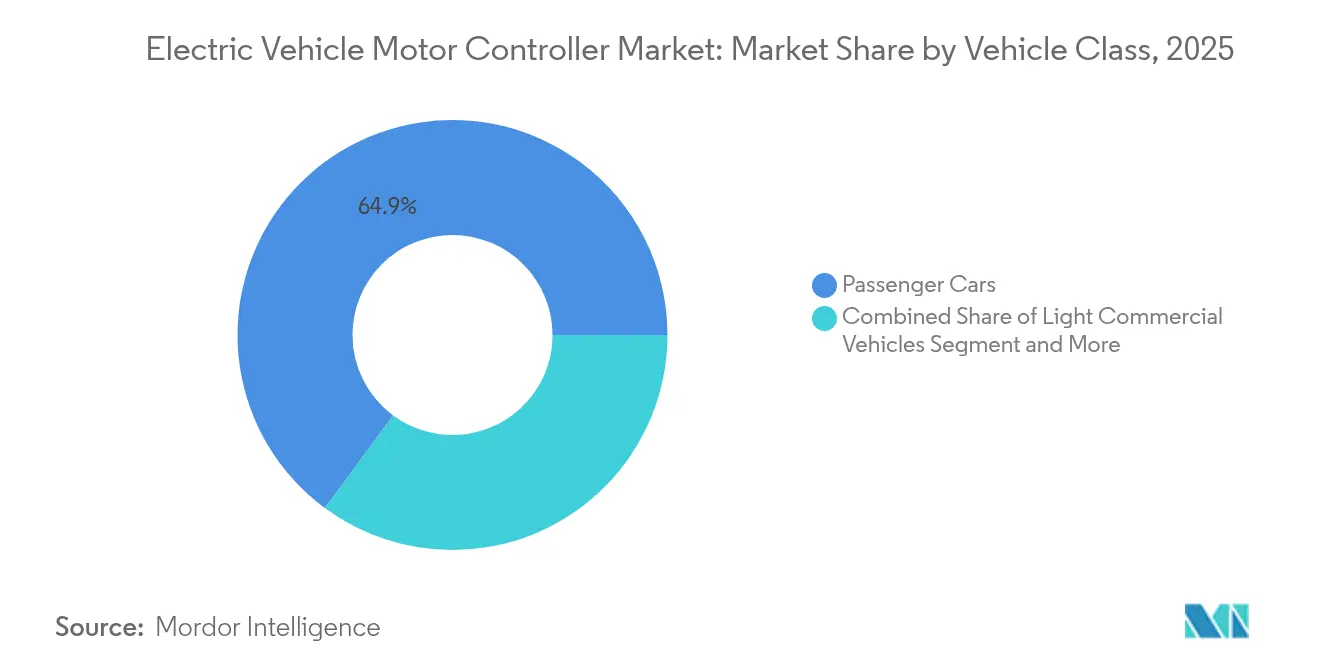

- By vehicle class, passenger cars accounted for 64.88% of the electric vehicle motor controller market share in 2025, while heavy commercial vehicles are increasing at 15.32% CAGR through 2031.

- By end use, OEM-fitted units dominated with 81.34% share of the electric motor vehicle controller market size in 2025; aftermarket retrofits are seeing 15.01% CAGR growth.

- By geography, Asia-Pacific captured 42.74% share of the electric motor vehicle controller market size in 2025, and is expected to grow at a CAGR of 13.54% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Vehicle Motor Controller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Electric Vehicles | +4.2% | Global, with APAC leading penetration | Long term (≥ 4 years) |

| E-Mobility Incentives and Mandates | +3.1% | Europe and North America regulatory frameworks, APAC subsidies | Medium term (2-4 years) |

| Declining Power-Electronics Cost | +2.3% | Global manufacturing hubs, concentrated in APAC | Medium term (2-4 years) |

| Sic MOSFET Penetration | +1.8% | Premium segments in North America and Europe, expanding to APAC | Long term (≥ 4 years) |

| V2G-Ready Bidirectional Controller Integration | +1.1% | Europe and California early adoption, expanding globally | Long term (≥ 4 years) |

| 800 V Platforms and Distributed-Drive Architecture | +0.9% | Premium automotive markets, luxury EVs globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Electric Vehicles

Global EV sales exceeded 14 million units in 2024, and China alone built more than 10 million vehicles, forcing a comparable surge in controller demand. Heavy-duty electric bus registrations rose 30% to more than 70,000 units, while electric truck volumes topped 90,000 vehicles[1]“Trends in Heavy-Duty Electric Vehicles – Global EV Outlook 2025,” International Energy Agency, iea.org. Norway’s 82% EV share in new cars signals the scale of transition once infrastructure, incentives, and consumer acceptance line up. Controller suppliers benefit from bigger production runs that lower unit cost and hasten product-refresh cycles.

Government E-Mobility Incentives and Mandates

Even as select European subsidies tapered off, new frameworks like Germany’s 2025 tax-relief scheme keep demand visibility high[2]“Germany Launches New Incentive Plans for Electric Vehicles,” European Alternative Fuels Observatory, alternative-fuels-observatory.ec.europa.eu. Japan’s 2035 zero-emission sales target and California’s tightened ZEV requirements guarantee long-term volume, while China’s vehicle-grid integration policy accelerates specification of bidirectional power stages.

Declining Power-Electronics Cost Curve

Device makers have cut silicon-carbide wafer prices by nearly 30% since 2024, pushing the technology beyond premium models and narrowing the cost gap with insulated-gate bipolar solutions. Battery pack prices are inching toward the USD 100 per kWh threshold, freeing budget for higher-spec power stages and improved thermal management without raising total system cost.

SiC MOSFET Penetration Boosts Controller Efficiency

The latest SiC MOSFET inverter boards reach 99.5% conversion efficiency and have roughly 41% lower losses than silicon IGBTs. At 1,200 V ratings, these devices sustain 200 kW peak power in compact footprints, enabling lighter e-axle packages and extended vehicle range. As volumes scale, performance metrics set in premium segments cascade into mid-tier passenger cars.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront System Cost | -2.1% | Global, particularly price-sensitive emerging markets | Short term (≤ 2 years) |

| Design Complexity and Reliability Validation | -1.4% | Advanced automotive markets with stringent safety standards | Medium term (2-4 years) |

| Sic and Gan Semiconductor Supply Constraints | -1.2% | Global supply chains, concentrated in Asia-Pacific production | Medium term (2-4 years) |

| Thermal-Management Limits | -0.8% | High-performance applications, premium vehicle segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront System Cost

Advanced SiC-based controllers still command price premiums that limit penetration in budget models. The economic burden is particularly acute in price-sensitive markets where total cost of ownership calculations favor internal combustion engines over shorter time horizons. Subsidy roll-backs in mature European markets heighten price sensitivity, forcing suppliers to refine designs, simplify cooling loops, and pursue innovative financing to sustain growth.

Design Complexity and Reliability Validation

Modern platforms integrate power conversion, safety monitoring, and bidirectional charging on a single board, stretching validation programs. Strict functional-safety targets raise development cost and delay launches, tilting advantage to incumbents with proven toolchains and deep OEM ties. The integration of bidirectional charging capabilities adds protocol complexity for V2G applications, requiring compliance with evolving ISO 15118 standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: BEVs Drive Market Evolution

Battery Electric Vehicles captured 63.12% of the electric vehicle motor controller market share in 2025, cementing their lead as charging networks mature and pack costs fall. Plug-in hybrids remain a transitional play but lose ground as brands pivot to all-electric lineups. Fuel-cell models, while small, post a 20.68% CAGR, thanks to heavy-duty logistics fleets that value long range and rapid refueling.

BEV controller designs emphasize high currents, regenerative-braking finesse, and 800 V readiness, creating room for differentiated cooling and software. FCEV solutions demand rapid load response and hydrogen-stack coordination, offering a niche for suppliers that master stack-to-motor energy management. Overall, strong BEV pull keeps the electric vehicle motor controller market on its expansion path.

By Power Output: Mid-Range Dominance Faces High-Power Disruption

Controllers rated 40-80 kW accounted for 44.62% of the electric vehicle motor controller market share in 2025, reflecting the predominance of passenger vehicle applications and urban mobility solutions. This range optimizes cost-performance trade-offs for mainstream EV adoption while providing adequate power for most driving scenarios. Above-200 kW units, however, are growing at 14.11% CAGR as performance cars and heavy trucks adopt dual-motor layouts.

Mid-range products balance cost and daily-drive power, benefitting from common hardware and software platforms. High-power segments push SiC and advanced cooling, yielding premium margins. As truck electrification accelerates, this tier will unlock fresh volume and shift supply-chain priorities toward ruggedized bus bars and thicker copper interconnects.

By Motor Type: PMSM Leadership Challenged by Innovation

Permanent-magnet synchronous Motors remained the mainstay, with 57.86% of the 2025 share within the electric vehicle motor controller market. Yet, price swings in rare-earth metals and geopolitical concerns give impetus to magnet-free designs. Switched-reluctance motors, free of rare-earth content, ride a 16.29% CAGR, supported by improving acoustic refinement and controller algorithms.

Controller suppliers are optimizing torque ripple and noise mitigation to make switched-reluctance acceptable in passenger cars while spurring adoption in buses and industrial EVs. The electric vehicle motor controller market size attached to PMSM units is still vast, but growth pivots will increasingly favor rare-earth-independent options.

By Vehicle Class: Commercial Vehicles Accelerate Electrification

Passenger cars contributed 64.88% of the electric vehicle motor controller market share in 2025. Yet, heavy trucks and buses show the quickest rise at 15.32% CAGR as regulators tighten diesel restrictions and operators pursue lower running costs. An electric bus market that exceeded 70,000 units in 2024 underpins robust controller demand. Light Commercial Vehicles represent an emerging growth opportunity as last-mile delivery electrification accelerates in urban markets.

Two-wheelers and three-wheelers remain bright spots in India and Southeast Asia, anchoring volume in the sub-40 kW bracket. Off-highway and industrial EVs, on the other hand, benefit from controlled operating environments that simplify controller requirements while enabling specialized performance optimization for specific applications.

By End Use: OEM Integration Dominates Market Structure

OEM-fitted systems dominated with an 81.34% of the electric vehicle motor controller market share in 2025, reflecting automakers’ preference for tightly integrated e-axle solutions that align with warranty and safety-case obligations. This dominance stems from the complexity of motor controller integration, which requires deep collaboration between vehicle manufacturers and component suppliers throughout the development process. Controller vendors winning early design slots for OEM programs secure multi-year volume that underpins scale in the electric vehicle motor controller industry.

Retrofit kits, however, grow at a 15.01% CAGR as fleets electrify legacy assets and enthusiasts seek performance upgrades. The aftermarket faces unique challenges, including compatibility with diverse vehicle platforms, certification requirements, and cost sensitivity. However, it values flexible software and broad vehicle-interface libraries to speed certification.

Geography Analysis

Asia Pacific accounted for 42.74% of the electric vehicle motor controller market share in 2025 and is advancing at 13.54% CAGR, fueled by China’s decade-long USD 230.8 billion investment in e-mobility and production volumes topping 10 million units. Japan’s plan for fully electrified sales by 2035 and significant subsidies for domestic SiC fabrication reinforce regional supply strength. India’s two-wheeler surge toward an expected 7-9 million annual units by 2030 ensures high-volume demand for low-power stages.

Europe is set for 10.22% CAGR through 2031, supported by new depreciation incentives, expanding charging grids, and clear CO₂ fleet-average deadlines. OEM–supplier collaboration on next-generation platforms, such as Volkswagen’s selection of SiC modules for future models, positions the region for rapid SiC penetration.

North America sees a similar growth rate, with California representing 35% of national EV registrations. Federal incentives and strengthening supply-chain policy drive domestic device manufacturing and joint ventures. South America, the Middle East, and Africa, though smaller, offer 7.6-9.9% growth, favoring simpler, lower-cost controller designs that tolerate harsher climates and grid constraints.

Competitive Landscape

The electric vehicle motor controller market exhibits moderate concentration, creating a competitive environment that balances scale advantages with innovation opportunities. Established Tier-1s such as Robert Bosch and DENSO leverage established OEM relationships and manufacturing capabilities to maintain strong positions. However, they face pressure from specialized power electronics companies and emerging Chinese competitors.

Strategic partnerships drive competitive differentiation, with Valeo collaborating with ROHM Semiconductor on next-generation power electronics and jointly developing magnet-free iBEE motor technology with MAHLE. Technology acquisition represents another competitive vector, exemplified by Magna's investment in Niron Magnetics for Clean Earth Magnets.

White-space growth appears in niche and off-highway domains. Suppliers increasingly tailor firmware to regional charging standards, from ISO 15118 V2G in Europe to China’s vehicle-grid-integration guidelines. Vendors that integrate hardware, embedded software, and cloud analytics under one stack are best positioned as electrification spreads beyond passenger cars.

Electric Vehicle Motor Controller Industry Leaders

BYD Co., Ltd.

Robert Bosch GmbH

Continental AG

DENSO Corporation

Tesla Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Mercedes-AMG unveiled the GT XX concept with three axial-flux motors delivering 1,340 hp and 850 kW charging capability, highlighting the performance ceiling of next-gen controllers.

- February 2025: BorgWarner won four electric-motor projects with Chinese OEMs covering 150–200 kW ranges for hybrid and pure-electric platforms.

- November 2024: Infineon introduced the ModusToolbox Motor Suite, offering integrated tools for configuring and monitoring motor-control applications.

- October 2024: SEDEMAC adopted Siemens Xcelerator software to accelerate design of motor-control units for e-mobility and power-tool applications.

Global Electric Vehicle Motor Controller Market Report Scope

The Motor Control Unit (MCU) serves as an essential electronic module that links batteries to motors . It is primarily tasked with controlling the speed and acceleration of electric vehicles (EVs) based on throttle input.

The Electric Vehicle Motor Controller Market has been segmented By Propulsion, By Power Output and Geography. By Propulsion, the market is segmented into BEV PHEV HEV. By Power Output 1-40 kW, 40-80 kW, above 80 kW. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. For each segment, the market size and forecast are made on the basis of value (USD).

| Battery Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Hybrid Electric Vehicles (HEV) |

| Fuel Cell Electric Vehicles (FCEV) |

| 1 to 40 kW |

| 40 to 80 kW |

| 80 to 200 kW |

| Above 200 kW |

| Permanent-Magnet Synchronous Motor (PMSM) |

| Brushless DC Motor (BLDC) |

| Induction Motor (IM) |

| Switched Reluctance Motor (SRM) |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two- and Three-Wheelers |

| Off-Highway and Industrial EVs |

| OEM-Fitted Controllers |

| Aftermarket Retrofits |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Propulsion Type | Battery Electric Vehicles (BEV) | |

| Plug-in Hybrid Electric Vehicles (PHEV) | ||

| Hybrid Electric Vehicles (HEV) | ||

| Fuel Cell Electric Vehicles (FCEV) | ||

| By Power Output | 1 to 40 kW | |

| 40 to 80 kW | ||

| 80 to 200 kW | ||

| Above 200 kW | ||

| By Motor Type | Permanent-Magnet Synchronous Motor (PMSM) | |

| Brushless DC Motor (BLDC) | ||

| Induction Motor (IM) | ||

| Switched Reluctance Motor (SRM) | ||

| By Vehicle Class | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Two- and Three-Wheelers | ||

| Off-Highway and Industrial EVs | ||

| By End Use | OEM-Fitted Controllers | |

| Aftermarket Retrofits | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the electric vehicle motor controller market?

The electric vehicle motor controller market size stood at USD 5.96 billion in 2026.

How fast is the market expected to grow?

The market is projected to rise at a 13.62% CAGR, reaching about USD 11.29 billion by 2031.

Which region leads sales?

Asia Pacific held 42.74% of 2025 revenue, led by China’s large-scale vehicle output and policy support.

Which vehicle class is growing the quickest?

Heavy commercial vehicles post the fastest expansion, recording a 15.32% CAGR over 2026-2031.

Why are silicon-carbide devices important for controllers?

SiC MOSFETs cut switching losses, enable 800 V architectures, and raise conversion efficiency to 99.5%, directly extending vehicle range.

Page last updated on: