Climate Control System For Commercial Vehicle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

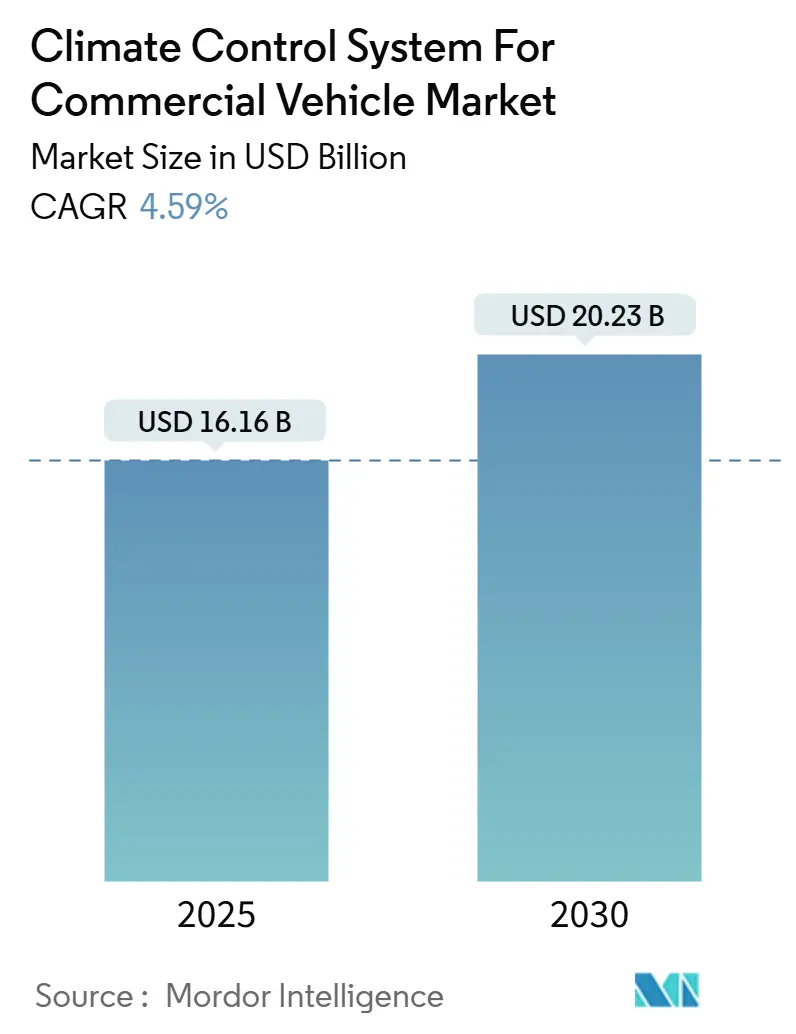

| Market Size (2025) | USD 16.16 Billion |

| Market Size (2030) | USD 20.23 Billion |

| Growth Rate (2025 - 2030) | 4.59% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Climate Control System For Commercial Vehicle Market Analysis by Mordor Intelligence

The Climate Control System for Commercial Vehicle market size reached USD 16.16 billion in 2025 and is projected to attain USD 20.23 billion by 2030, advancing at a 4.59% CAGR during the forecast period (2025-2030). Electromobility pressures and refrigerant-phase-down mandates reshape system design, compelling suppliers to balance battery-friendly energy efficiency with reliable cabin comfort. Electrified fleets are accelerating demand for heat-pump architectures, while cold-chain logistics expansion is boosting refrigeration adoption. Regulations such as Euro 7 and California’s zero-emission TRU rules tighten efficiency requirements, and semiconductor supply constraints continue influencing HVAC control module availability. Competitive differentiation revolves around 800 V coolant-heater platforms, CO₂ heat-pump systems, and software-defined predictive controls that optimize uptime.

Key Report Takeaways

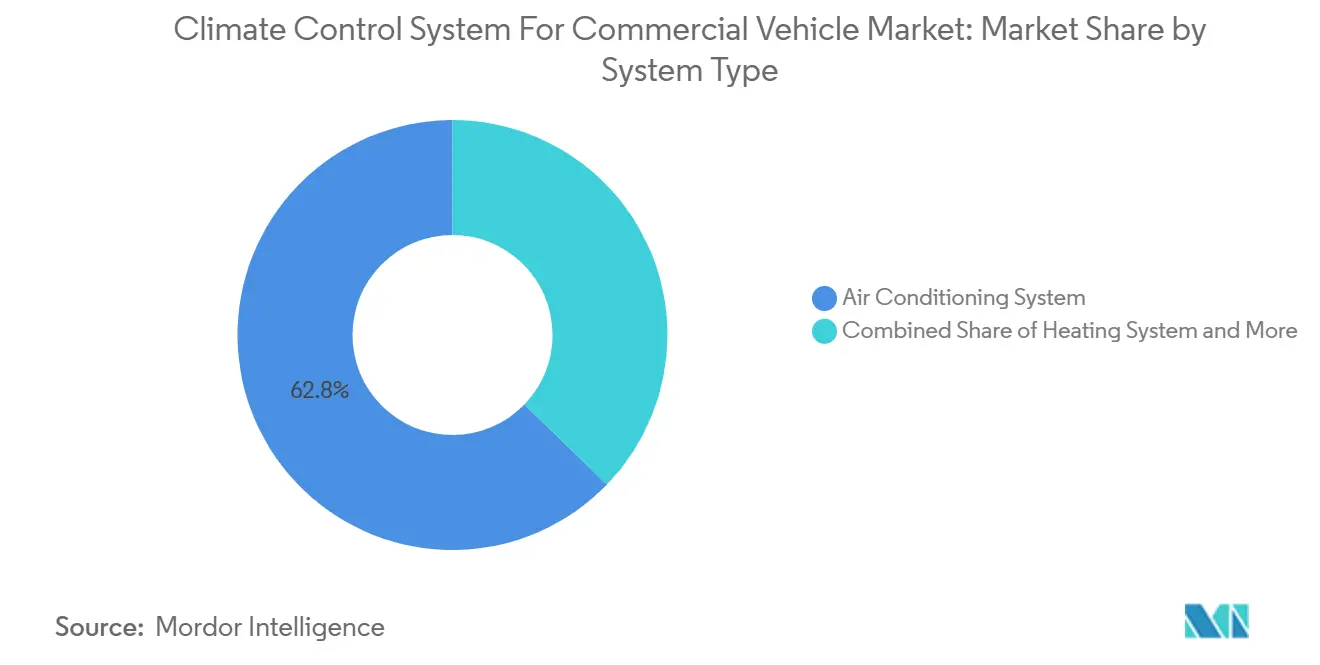

- By system type, air-conditioning systems led with 62.77% revenue share in the Climate Control System for Commercial Vehicle market in 2024; refrigeration is forecasted to expand at a 6.48% CAGR during the forecast period (2025-2030).

- By vehicle type, light commercial vehicles accounted for 38.47% of the Climate Control System for Commercial Vehicle market share in 2024. In contrast, the heavy commercial vehicles segment is expected to rise at a 5.75% CAGR during the forecast period (2025-2030).

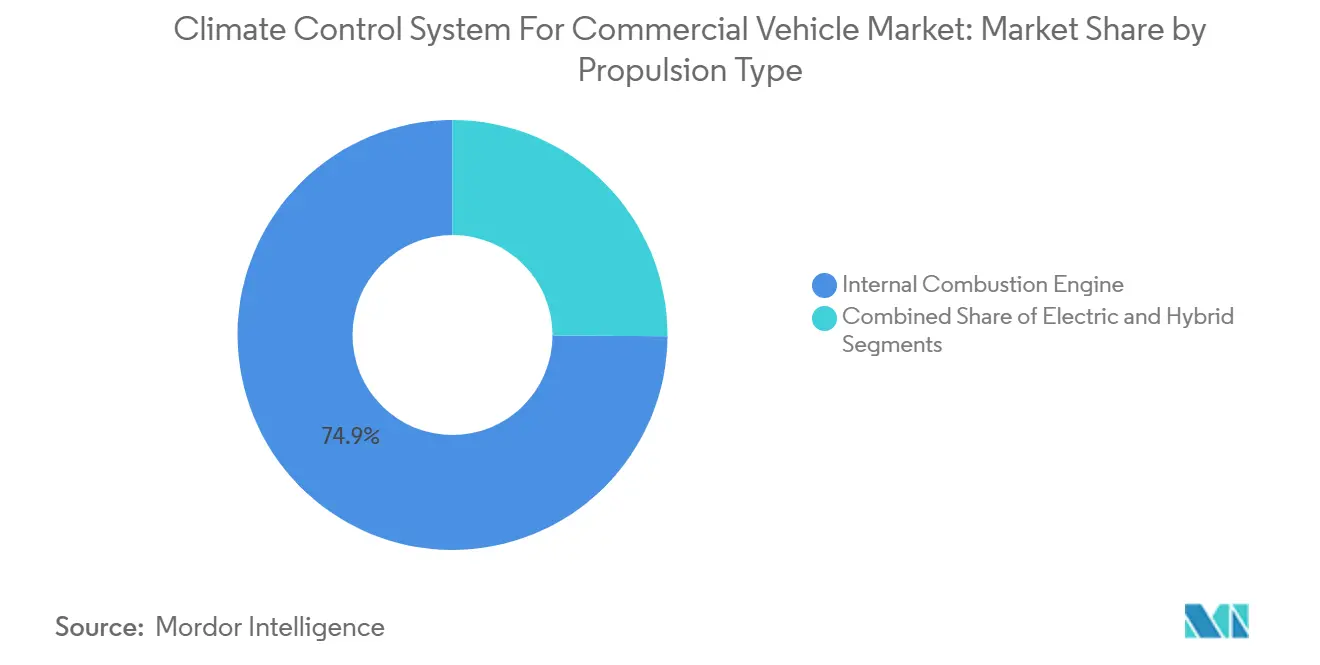

- By propulsion type, internal-combustion models retained 74.91% share of the Climate Control System for Commercial Vehicle market in 2024. Yet, electric variants are projected to grow at a 12.27% CAGR during the forecast period (2025-2030).

- By technology, conventional solutions held a 53.65% share of the Climate Control System for Commercial Vehicles market in 2024, while the smart climate control systems segment is expected to rise at an 8.16% CAGR during the forecast period (2025-2030).

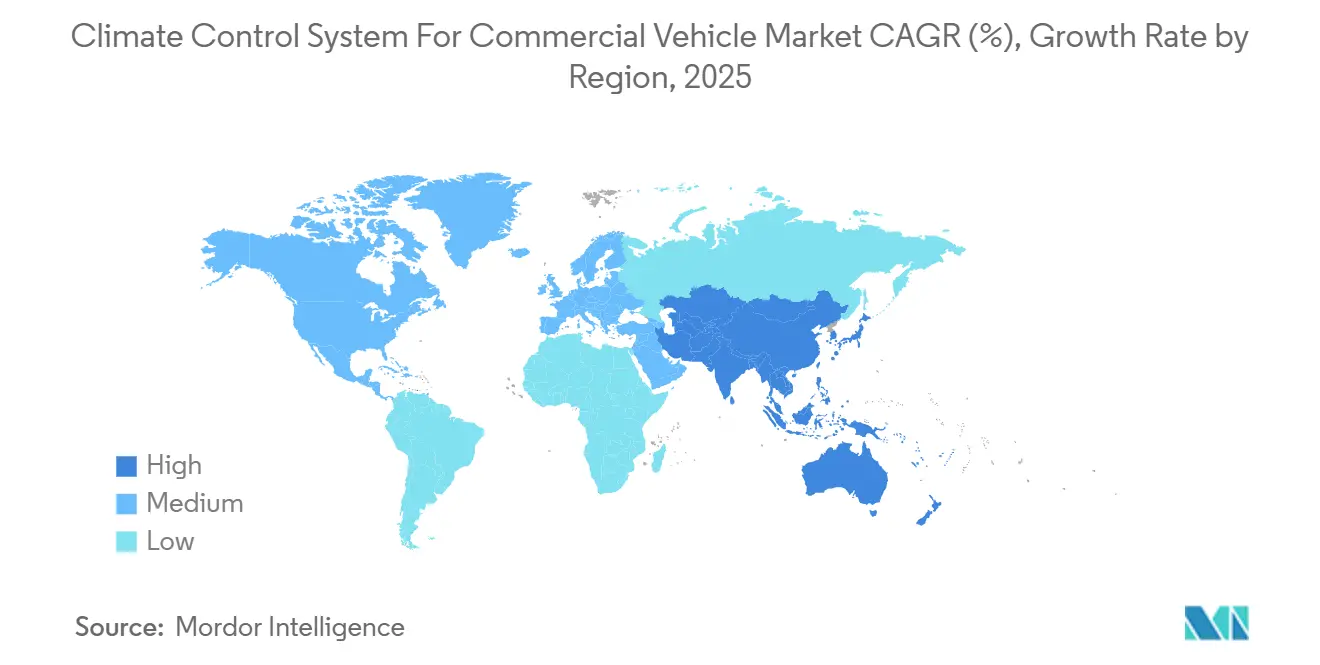

- By geography, Asia-Pacific captured 45.56% revenue share of the Climate Control System for Commercial Vehicle market in 2024; the region is expected to grow at a 5.13% CAGR during the forecast period (2025-2030).

Global Climate Control System For Commercial Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrified Commercial Fleets | +1.2% | Global, with APAC and Europe leading adoption | Medium term (2-4 years) |

| Cabin-Comfort and Driver-Safety Regulations | +0.8% | North America & EU, extending to APAC markets | Long term (≥ 4 years) |

| Cold-Chain Logistics and Last-Mile Delivery | +1.0% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| OTA-Enabled HVAC | +0.6% | North America & EU, with premium segment focus | Medium term (2-4 years) |

| 800-V Coolant-Heater | +0.4% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| CO₂ (R-744) Heat-Pump Systems | +0.7% | EU and North America, driven by F-gas regulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Electrified Commercial Fleets

In cold climates, electric truck batteries face heightened strain due to heating demands, underscoring the critical need for efficient heat-pump systems. Fleet operators, especially in China and Europe, are turning to integrated thermal platforms that regulate both cabin and battery temperatures. This transition not only boosts vehicle range but also reduces overall ownership costs. As new-energy commercial vehicles gain traction in China, there's a surging demand for sophisticated multi-loop thermal management solutions. Concurrently, heavy-duty trucks adopting high-voltage architectures are now aligning with rapid charging systems and can accommodate robust heating components, all while maintaining their range. Suppliers capable of delivering holistic, battery-centric HVAC modules are gaining preferred-vendor status in fleet tenders[1]“The Future of Heat Pumps in China – Executive Summary,” International Energy Agency, iea.org.

Stringent Cabin-Comfort and Driver-Safety Regulations

Euro 7 and forthcoming BS7 standards both require on-board energy-consumption monitoring, effectively making HVAC efficiency a reportable parameter. Regulators also link cab temperature stability to driver fatigue metrics, prompting fleets to install redundant cooling capacity and predictive maintenance analytics. Particulate filtration below 10 nm is becoming mandatory, stimulating uptake of multi-stage filters and intelligent airflow routing. These rules increase design complexity and favor platforms that provide real-time diagnostics, automated fault reporting, and secure data logging.[2]“Regulation (EU) 2024/1257,” Official Journal of the European Union, eur-lex.europa.eu

Expansion of Cold-Chain Logistics and Last-Mile Delivery

E-commerce and pharma shipments demand precise temperature control, fueling refrigerated-body sales and pushing HVAC suppliers into electric transport refrigeration units. California’s zero-emission TRU deadlines accelerate battery-powered reefer adoption, while depot-based pre-cooling strategies emerge to cut in-route energy use. System makers now integrate compartment zonal controls, regenerative braking recovery and lightweight insulation to maximize range and payload capacity. Urban fleets highlight quick-pull-down performance and noise mitigation as purchase criteria.

Predictive/OTA-Enabled HVAC for Uptime Optimization

Telematics connectivity allows cloud algorithms to fine-tune blower speeds, refrigerant metering, and heating profiles ahead of duty cycles, improving energy efficiency up to 15%. Over-the-air updates curtail workshop visits and align HVAC logic with evolving battery chemistries. Predictive analytics schedule filter and compressor service before costly roadside failures, a capability valued at more than USD 500 per day in avoided downtime. Cyber-secure gateways, required under global vehicle cybersecurity regulations, add hardware cost but also create subscription-revenue pathways for software-enhanced HVAC services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Installation and Maintenance Cost | -0.9% | Global, with greater impact in emerging markets | Short term (≤ 2 years) |

| Refrigerant-Transition Redesign Costs | -0.6% | EU and North America, extending globally | Medium term (2-4 years) |

| HVAC Energy-Penalty | -0.4% | Global, particularly in extreme climate regions | Long term (≥ 4 years) |

| Skilled CV-HVAC Technician Shortage | -0.3% | APAC and MEA, with spillover to South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Installation and Maintenance Cost of Advanced HVAC

Heat-pump and smart-control packages cost 40-60% more than legacy units, stretching fleet capex budgets. Installation often demands high-voltage certification, specialized tooling, and additional labor hours, especially where service centers lack EV-specific equipment. Replacement of multi-refrigerant components can cost significantly higher than conventional parts, extending payback periods to 3-4 years. Subsidy programs partly offset upfront costs but remain inconsistent across regions, dampening short-term adoption.

Shortage of Skilled CV-HVAC Technicians in Emerging Markets

Complexity surrounding A2L and CO₂ refrigerants, coupled with high-voltage safety requirements, creates a talent gap. A very small number of U.S. technicians currently hold hybrid/EV HVAC certification against the general mechanic pool, and ratios are lower in APAC and MEA. Training pipelines lag technology deployment, extending vehicle downtime for advanced system repairs and eroding fleet uptime gains. Industry bodies are rolling out modular e-learning and augmented-reality service guides, but technician throughput remains a bottleneck.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Refrigeration Drives Growth

Air-conditioning retained a 62.77% share of the Climate Control System for Commercial Vehicle market size in 2024, rooted in universal driver-comfort needs and evolving safety mandates. Refrigeration accounted for the fastest 6.48% CAGR between 2025 and 2030 as pharmaceutical distribution and grocery e-commerce expand globally. Refrigerated bodies now incorporate ejector cycles and waste-heat recovery, improving the coefficient of performance by up to 30%.

Heating architectures are transitioning from engine-waste-heat utilization to dedicated electrical heaters and reversible heat pumps, reshaping the bill of materials and supplier mix. Ventilation sub-systems gain relevance under Euro 7 particulate thresholds, integrating multi-stage filtration shelves. Suppliers offering modular platforms spanning AC, refrigeration, and heat-pump modes capture cross-segment synergies and reduce fleet maintenance complexity.

By Vehicle Type: Commercial Segments Accelerate

Light commercial vans held 38.47% of the Climate Control System for Commercial Vehicle market size in 2024 sales, owing to the surge in e-commerce deliveries and dense city routes, where fleets value compact, energy-efficient HVAC units that free up cargo space yet keep drivers comfortable. Heavy trucks are the clear growth story, set to advance 5.75% a year through 2030 as emissions rules push electrification and long-haul operators demand robust climate systems that protect driver alertness and cut fuel spend.

Medium commercial vehicles are moving to integrated thermal platforms that cool batteries, cabins, and cargo from a single unit, trimming parts count and saving energy. Passenger cars are nearing saturation in mature markets, but still ship in large numbers across emerging economies where conventional HVAC remains affordable. Niche uses, ambulances, mobile clinics, and other specialty rigs open the door for custom systems with backup power and tightly controlled temperature zones. Altogether, the tilt toward commercial fleets mirrors booming online retail and stricter safety rules that hold operators accountable when poor cab climate leads to driver fatigue and accidents.

By Propulsion Type: Electric Transformation Accelerates

Internal-combustion models dominated with 74.91% of the Climate Control System for Commercial Vehicle market share in 2024, largely because fleets can service familiar engines and spread upgrade costs over large installed bases. Even so, electric drivetrains are on a tear, projected to climb at a 12.27% CAGR through 2030 as battery prices fall and zero-emission regulations toughen across China, Europe, and key U.S. states. Losing access to engine waste heat forces electric trucks to rely on high-efficiency heat pumps and PTC heaters, which can draw up to 40% of a winter driving battery if not carefully managed. To protect range, suppliers are pairing cabin units with battery-cooling circuits so thermal energy is shared rather than duplicated, an approach that also simplifies packaging. Fleets adopting these integrated systems are already reporting lower maintenance bills because fewer hoses, pumps, and controllers translate into fewer leak points and diagnostic events.

Hybrids occupy the middle ground. They reclaim engine waste heat at cruising speeds yet swing to electric heating in traffic, so their HVAC needs span both high-voltage and belt-driven components. Vendors that offer modular toolkits, compressors, valves, and software that can toggle between energy sources, see growing interest from OEM engineering teams pressed for platform commonality. In emerging markets, the upfront price gap still tilts buyers toward internal-combustion trucks, but new carbon-credit programs in India and Brazil are beginning to narrow the difference. Over time, duty-cycle data gathered from connected trucks will refine sizing rules so operators can down-spec heaters for temperate routes, trimming battery cost and nudging more buyers toward electrified powertrains.

By Technology: Smart Systems Lead Innovation

Conventional setups accounted for 53.65% of 2024 revenue, yet smart climate control is the clear disruptor, projected to expand at an 8.16% CAGR through 2030. These connected platforms use cloud analytics and machine learning to precondition cabs, cutting energy consumption by up to 15% and extending electric-truck range. Automatic systems, which blend basic sensor feedback with fixed algorithms, still appeal to cost-sensitive buyers as a bridge between legacy and fully smart offerings. Fleets that operate in variable climates are the quickest adopters, valuing the hands-off comfort and reduced driver distraction.

Smart HVAC also unlocks recurring revenue: suppliers sell software subscriptions that deliver over-the-air updates, predictive maintenance alerts, and compliance reporting. Cyber-secure gateways add cost, but they now appear on most specification sheets as Euro 7 and similar rules demand data integrity. For conventional units to stay relevant, manufacturers are packing them with higher-efficiency compressors and low-GWP refrigerants to narrow the performance gap. As a result, the Climate Control System for Commercial Vehicle market size is tilting toward intelligence-driven solutions, while legacy technology remains entrenched in regions where upfront price trumps total operating cost.

Geography Analysis

Asia-Pacific captured 45.56% of 2024 revenue and is slated for a 5.13% CAGR through 2030. China’s commercial electrification momentum and India’s scheduled BS7 rollout amplify demand for battery-centric HVAC modules. Japan’s low-GWP mandate steers suppliers toward CO₂ refrigerant systems, catalyzing component innovation. Skilled labor shortages across Southeast Asia pose service bottlenecks, but government training incentives aim to narrow the gap.

North America is projected to log a 3.53% CAGR during the forecast period. EPA refrigerant-handling rules and state-level zero-emission mandates accelerate investment in compliant HVAC technologies. Supplier consolidation has intensified following high-profile acquisitions that strengthen North American manufacturing footprints. Urban fleet electrification, particularly in California and New York, is driving orders for high-voltage coolant heaters and predictive maintenance platforms.

Europe will expand at a 3.25% CAGR as the region enforces strict F-gas quotas and Euro 7 energy-monitoring requirements. CO₂ heat-pump adoption is accelerating, supported by tax incentives for low-GWP refrigerants. Fleets face increasing liability for comfort-related driver incidents, driving interest in redundant HVAC systems and real-time diagnostics. Secure over-the-air update frameworks are rapidly becoming a procurement prerequisite among EU fleet buyers.

Competitive Landscape

Market concentration reflects moderate fragmentation, yet leading players continue to hold enough scale to shape technology roadmaps. Strategic consolidation accelerated during 2024 and 2025, exemplified by Hanon Systems’ acquisition by Hankook & Company Group. These deals underline a shift toward larger balance sheets that can support parallel investments in software, electronics, and advanced materials. As a result, competitive intensity is rising, and suppliers lacking integrated R&D capabilities face growing barriers to entry. The trend also signals that private-equity owners may exit earlier than planned to lock in valuation premiums while the window for high-multiple deals remains open.

Technology differentiation now centers on electric-vehicle thermal management, predictive maintenance algorithms, and refrigerant-transition compliance. Suppliers must juggle power-dense architectures, stringent F-gas regulations, and aggressive unit-cost targets without compromising cabin comfort or battery longevity. White-space opportunities are most visible in 800 V coolant-heater systems for heavy-duty platforms and in CO₂ heat-pump units that maintain heating efficiency below –10 °C, a capability. Early-mover advantage in these niches is reinforced by patent portfolios covering heat-exchanger geometries and low-GWP refrigerants. Consequently, tier-one contracts are skewing toward vendors that can prove both regulatory headroom and lifecycle cost savings.

Emerging disruptors are pushing a software-defined HVAC paradigm that uses over-the-air updates and machine-learning optimization to trim energy demand by up to 15% per duty cycle. These start-ups monetize their algorithms through subscription models, eroding the hardware-linked revenue base of incumbent suppliers. At the same time, the industry’s pivot toward centralized E/E architectures makes it feasible to host climate-control logic on fusion chips that also govern ADAS and drivetrain functions. This convergence lowers latency, improves diagnostics, and opens the door for semiconductor companies to compete directly with traditional thermal specialists. Taken together, the landscape is evolving toward fewer but more deeply integrated players, with digital IP and power-electronic expertise determining long-term winners.

Climate Control System For Commercial Vehicle Industry Leaders

Denso Corporation

Valeo SA

Hanon Systems

MAHLE GmbH

Sanden Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Carrier Transicold unveiled the all-electric Pulsor eCool refrigeration unit in India, cutting precool time from 30 °C to −18 °C by 31%.

- September 2025: Grayson Thermal Systems showcased high-voltage RM-series rooftop HVAC modules for electric buses at Busworld Europe.

- June 2025: Tata Motors introduced factory-fitted air-conditioning across its complete truck portfolio, including cowl models.

- February 2025: Carrier Transicold launched the Vector S 15 semi-electric unit, delivering diesel-mode performance with lower fuel burn.

Global Climate Control System For Commercial Vehicle Market Report Scope

| Air Conditioning System |

| Heating System |

| Ventilation System |

| Refrigeration System |

| Light Commercial Vehicle |

| Medium Commercial Vehicle |

| Heavy Commercial Vehicle |

| Internal Combustion Engine |

| Electric |

| Hybrid |

| Conventional |

| Automatic Climate Control |

| Smart Climate Control |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By System Type | Air Conditioning System | |

| Heating System | ||

| Ventilation System | ||

| Refrigeration System | ||

| By Vehicle Type | Light Commercial Vehicle | |

| Medium Commercial Vehicle | ||

| Heavy Commercial Vehicle | ||

| By Propulsion Type | Internal Combustion Engine | |

| Electric | ||

| Hybrid | ||

| By Technology | Conventional | |

| Automatic Climate Control | ||

| Smart Climate Control | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Climate Control System for Commercial Vehicle market?

The Climate Control System for Commercial Vehicle market size reached USD 16.16 billion in 2025.

How fast is the market expected to grow toward 2030?

It is forecasted to register a 4.59% CAGR, reaching USD 20.23 billion by 2030.

Which region leads demand for commercial-vehicle HVAC systems?

Asia-Pacific dominated with a 45.56% revenue share in 2024 and is set for the fastest 5.13% CAGR to 2030.

Which system type is expanding the quickest?

Refrigeration systems are projected to advance at a 6.48% CAGR through 2030 due to cold-chain and e-commerce growth.

How are electric trucks influencing HVAC design?

Electric propulsion eliminates engine waste heat, compelling adoption of high-efficiency heat pumps and 800 V coolant heaters to preserve driving range.

Page last updated on: