Automotive Thermal Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

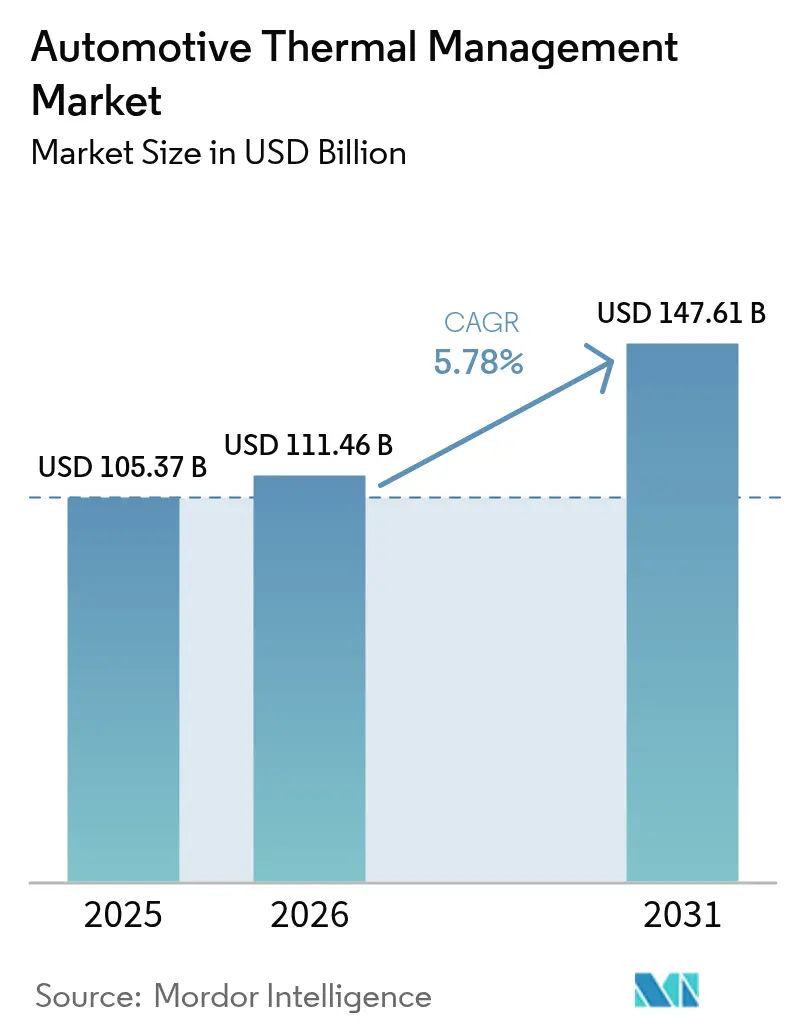

| Market Size (2026) | USD 111.46 Billion |

| Market Size (2031) | USD 147.61 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

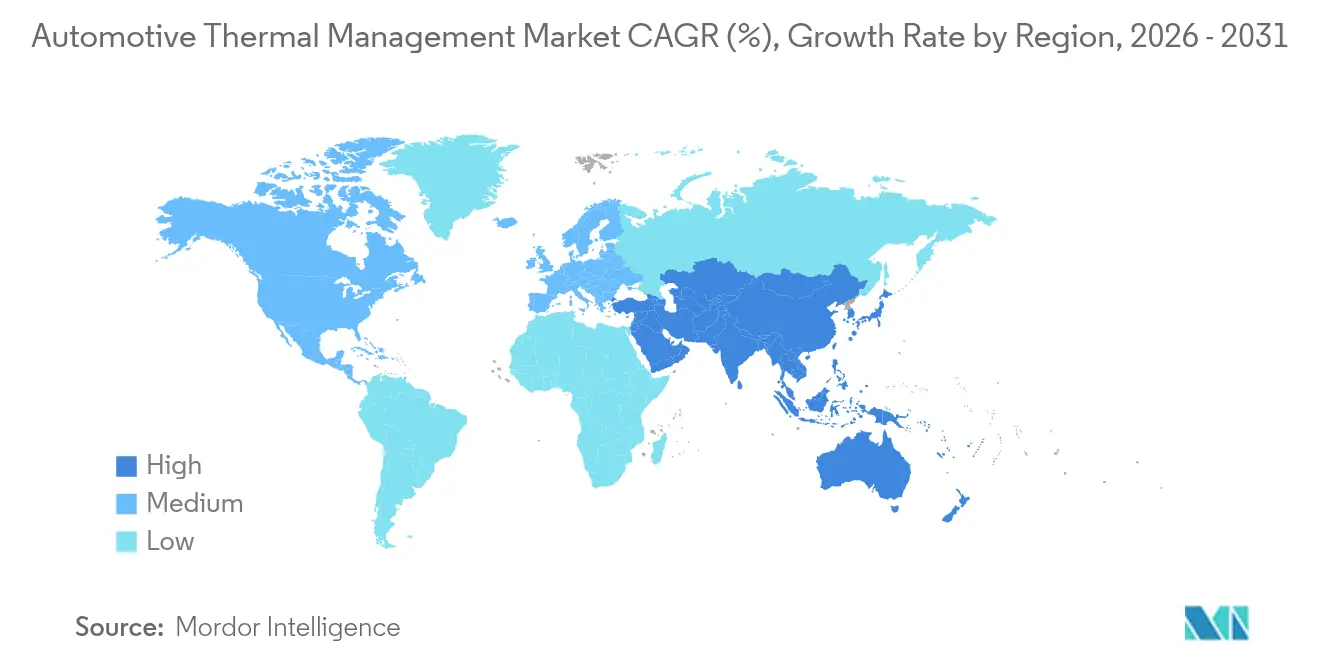

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Thermal Management Market Analysis by Mordor Intelligence

Automotive Thermal Management Market size in 2026 is estimated at USD 111.46 billion, growing from 2025 value of USD 105.37 billion with 2031 projections showing USD 147.61 billion, growing at 5.78% CAGR over 2026-2031. Growth stems from rapid electrification, stricter global CO₂ and CAFE rules, and rising demand for integrated battery-cooling, cabin HVAC, and power electronics thermal loops. Battery electric vehicles (BEVs) require two-fifths more thermal content per unit than internal-combustion cars, forcing suppliers to redesign architectures that hold battery temperatures in the optimal 15–35 °C band, extend pack life, and support 800 V fast-charge hardware. Competitive pressures, particularly in Asia-Pacific, accelerate innovation in immersion cooling, multi-circuit modules, and PFAS-free refrigerant heat-pumps that improve vehicle range, comfort, and regulatory compliance.

Key Report Takeaways

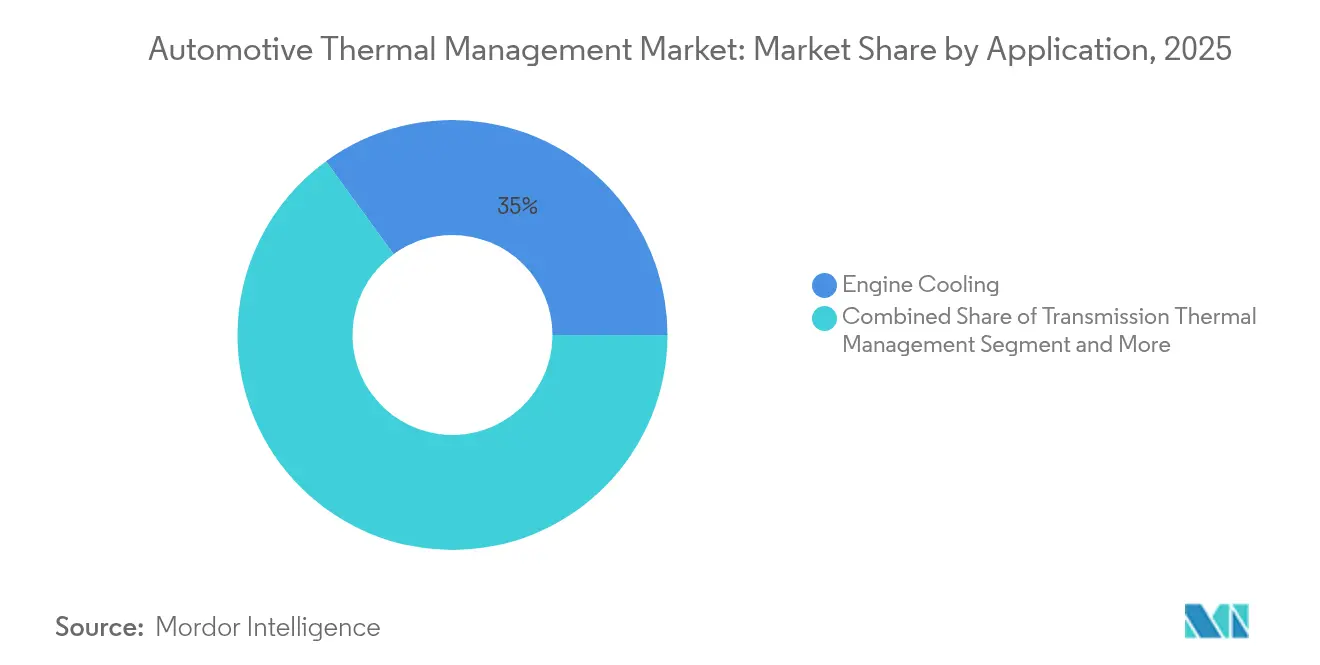

- By application, engine cooling led with 35.01% of the automotive thermal management market share in 2025; battery thermal management is expanding at a 5.83% CAGR by 2031.

- By technology, liquid indirect cooling held 42.77% of the automotive thermal management market share in 2025, whereas direct/immersion cooling records the highest 5.82% CAGR by 2031.

- By component, heat exchangers accounted for 46.48% of the automotive thermal management market share in 2025, and compressors and pumps posted the fastest 5.85% CAGR by 2031.

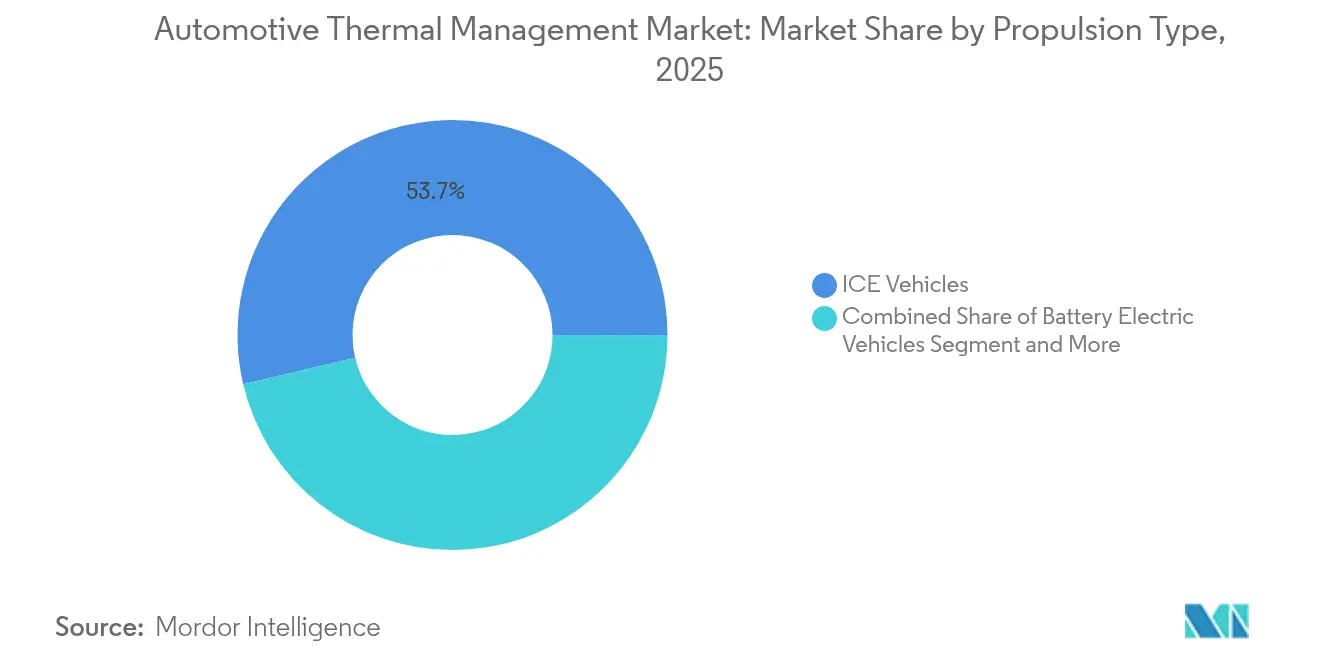

- By propulsion, internal-combustion vehicles retained 53.67% of the automotive thermal management market share in 2025, yet BEVs deliver the quickest 5.89% CAGR by 2031.

- By vehicle type, passenger cars captured 66.51% of the automotive thermal management market share in 2025; heavy trucks and buses are advancing at a 5.90% CAGR by 2031.

- By geography, Asia-Pacific commanded 39.17% of the automotive thermal management market share in 2025 and is projected to post the fastest 5.86% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Thermal Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream EV Adoption | +1.2% | Global, with Asia Pacific and EU leading adoption | Medium term (2-4 years) |

| Luxury & Comfort Features | +1.1% | North America and EU premium segments | Long term (≥ 4 years) |

| Under-Hood 800V Architectures | +1.0% | Asia Pacific core, spill-over to EU and North America | Long term (≥ 4 years) |

| ICE Turbo-Downsizing | +0.9% | Global, particularly emerging markets | Medium term (2-4 years) |

| Stricter CO₂ / CAFE Norms | +0.8% | EU primary, North America secondary | Short term (≤ 2 years) |

| PFAS-Phase-Out Forcing Switch To Natural-Refrigerant Heat-Pumps | +0.8% | EU primary, global regulatory follow-through | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mainstream EV Adoption Boosting Battery-Thermal Content

Battery packs now consume one-fifth of total thermal budgets, up from minimal in conventional cars. Hyundai Mobis introduced pulsating heat pipes in recent times that deliver ten-fold higher heat transfer than standard plates, trim thickness to 0.8 mm, and improve temperature uniformity by 20 °C, sharply lowering runaway risk. Integrated heat-pump HVAC recovers waste heat, adding minimal winter range to BEVs, and suppliers bundling battery, cabin, and inverter cooling in unified modules are booking multi-platform awards.

Under-Hood 800 V Architectures Accelerating SiC Inverter Cooling

Premium EVs now rely on 800 V silicon-carbide inverters capable of 175 °C junction temperatures. Immersion dielectric cooling keeps thermal resistance under 0.1 °C/W, enabling charge rates above 350 kW and safeguarding reliability over 150,000 cycles. Reference designs recently released by NXP and Wolfspeed embed these liquid loops, underlining the shift from air to direct liquid cooling in high-power applications.

Stricter CO₂ / CAFE Norms Driving Multi-Circuit Cooling

The EU’s 49.5 g CO₂/km 2030 rule and the decision to credit air-conditioning efficiency from 2025 spur OEMs to specify thermal packages that shave 2–4 g CO₂/km. Modules blending engine, transmission, and after-treatment cooling capture one-third price premiums versus discrete parts. Similar logic applies in North America, where CAFE incentives lift demand for smart pumps, electronically controlled valves, and deep-learning controllers that match cooling capacity to transient loads.

PFAS Phase-Out Forcing Switch to Natural-Refrigerant Heat-Pumps

EU restrictions on PFAS refrigerants starting in 2028 spark early moves to propane (R290) and CO₂ (R744) systems. Ford declares R290 as one of the best options for thermal systems, adding gas-leak detection and revised service protocols to manage flammability [1]“Propane Refrigerant Implementation in Electric Vehicles,” Ford Motor Company, ford.com. CO₂ cycles run at 70–100 bar yet offer superior heat capacity, pushing compressor, valve, and exchanger re-design. Suppliers mastering PFAS-free lines stand to win share as regulations tighten.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High BOM Cost Of Integrated Thermal Modules | -0.7% | Global, particularly cost-sensitive segments | Short term (≤ 2 years) |

| Reliability & Leak-Path Risks | -0.6% | Global, with higher impact in commercial vehicles | Medium term (2-4 years) |

| Scarcity Of Low-GWP Refrigerant Supply Chains | -0.5% | EU primary, global secondary impact | Medium term (2-4 years) |

| Limited Service-Technician Capabilities | -0.4% | Global, particularly emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High BOM Cost of Integrated Thermal Modules

Unified modules integrate multiple components into a single housing, but this approach significantly increases costs compared to using separate pieces. This creates challenges for vehicles operating within a limited thermal content budget. To address this, suppliers are focusing on strategies such as platform-standardization, vertical integration, and automated assembly processes to achieve cost efficiency and reach volume breakeven.

Reliability & Leak-Path Risks in Liquid/Immersion Systems

Liquid loops, containing numerous joints, are designed to remain sealed for an extended period, withstanding extreme temperature variations ranging from very low to very high levels. High-voltage zones are particularly vulnerable to issues caused by leaks, which can result in operational shutdowns and significant daily financial losses for fleets. Although solutions such as accelerated aging processes, advanced fluorinated elastomer seals, and predictive leak detection technologies are available, these measures tend to increase the time required for validation considerably.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Battery Thermal Management Drives Electrification

Engine cooling held a 35.01% of the automotive thermal management market share in 2025 as the backbone for ICE fleets. Battery systems, however, are scaling fastest at a 5.83% CAGR, reflecting OEM reallocations toward pack, module, and cell-level loops that now command almost half of BEV thermal budgets.

Stellantis’ Intelligent Battery Integrated System bundles cooling plates, inverters, and chargers, boosting energy efficiency by 10% and power density by minimal. Cabin HVAC remains steady, aided by dual-source heat pumps, while waste-heat recovery and EGR modules grow in commercial sectors. Motor and inverter cooling races ahead as 800 V drivetrains proliferate, each demanding up to 200 W/cm² heat removal.

By Technology Type: Direct Cooling Gains Traction

Liquid indirect loops commanded 42.77% of the automotive thermal management market share in 2025, bolstered by mature radiators, reservoirs, and pumps. The automotive thermal management market size tied to immersion cooling is increasing at a 5.82% CAGR, reflecting physics advantages that elevate allowable power density tenfold.

Hyundai’s nano-film air technology cut cabin temperatures by 12.5 °C and saved significant energy, proving air cooling’s niche in lightweight systems. Phase-change materials buffer cells during peak load, and hybrid loops interlink multiple media, selecting optimal paths through AI supervision.

By Component: Heat Exchangers Lead, Pumps Accelerate

Heat exchangers supplied 46.48% of the automotive thermal management market share in 2025, emblematic of the enduring need for radiators, condensers, and oil coolers. Compressors and pumps top growth tables at 5.85% CAGR, mirroring electrified cooling circuit counts per car. Automotive thermal management market share for smart electric pumps is projected to reach one-third by 2031.

Sensor-rich manifolds route flows in milliseconds, while high-voltage coolant heaters deliver 5–7 kW to warm cabins without engine waste heat. AI-enhanced controllers cut energy draw by a certain amount compared with fixed-map logic, unlocking new SaaS revenue trails for hardware makers.

By Propulsion Type: ICE Dominance Yields to EV Growth

ICE vehicles retained 53.67% of the automotive thermal management market share in 2025, yet BEVs exhibited a 5.89% CAGR as regulatory timelines firm. The automotive thermal management market size associated with BEVs is expected to grow exponentially by 2031. Hybrid models add complexity by merging engine and battery loops, and fuel-cell stacks introduce 80 °C steady-state cooling and freeze-proofing challenges.

Due to battery, power-electronics, and heat-pump loads, BEVs need 40–60% more thermal hardware than ICE equivalents. This creates a dual-speed ecosystem where suppliers juggle declining ICE volumes while scaling EV content per unit.

By Vehicle Type: Passenger Cars Lead, Trucks Accelerate

Passenger cars produced 66.51% of the automotive thermal management market share in 2025, yet heavy trucks and buses outperform on growth at 5.90% CAGR as fleet electrification mandates sweep China, the EU, and North America. The automotive thermal management market size for heavy trucks is forecast to grow exponentially in 2031.

Electrified Class 8 trucks carry battery packs above 500 kWh, generating 500 kW heat peaks during fast charge. Thermal solutions must control cell temperatures, cool SiC inverters, and warm cabins, all within tight weight ceilings, elevating the strategic value of high-capacity immersion loops and heat-pump HVAC.

Geography Analysis

Asia-Pacific held 39.17% of the automotive thermal management market share in 2025 and led growth at a 5.86% CAGR, powered by China’s EVs built by BYD in 2024 and a considerable target for 2025 . Hanon Systems’ massive compressor expansion supports North American assembly while leveraging low-cost Asian supply lines. Japanese and Korean Tier 1s push breakthroughs such as pulsating heat pipes, keeping the region technologically competitive.

North America secures the second spot, bolstered by stringent fuel efficiency standards and significant EV capital commitments from major automakers such as Ford, GM, and Tesla. The rapid adoption of advanced platforms drives increased demand for silicon carbide inverter cooling and predictive thermal control technologies. While Mexico's cost-effective manufacturing base continues to attract investments in pumps, valves, and exchangers, a shortage of skilled technicians creates challenges for managing complex EV service operations.

Europe combines strict regulatory frameworks with a strong engineering tradition. Ambitious emissions reduction targets and the phase-out of certain chemicals are accelerating the transition to environmentally friendly refrigerants. Ford recently introduced its propane-based system, showcasing innovation in thermal management. German manufacturers are prioritizing integrated modules and exhaust gas recirculation heat recovery systems, while France's aggressive push for battery electric vehicles is significantly increasing the demand for battery cooling solutions. This premium market positioning supports higher thermal management spending per vehicle, ensuring sustained profitability for suppliers.

Competitive Landscape

Consolidation is reshaping the automotive thermal management market. Hankook & Company Group’s buyout of Hanon Systems in 2024, plus ABC Technologies’ pending acquisition of TI Fluid Systems, strengthen global footprints and allow cross-segment coverage [3]“Acquisition of Hanon Systems,” Hankook & Company Group, hankook.com . Top players Denso, Valeo, MAHLE, Robert Bosch, and Hanon jointly held signifcant revenue in 2024, signaling moderate concentration.

Suppliers focus on platform standardization, automated quality assurance, and software-defined thermal control to enhance operational efficiency and meet evolving industry demands. Meanwhile, AI-driven modules are emerging as key players, offering substantial energy savings that align with OEM range targets, thereby addressing critical performance and sustainability goals.

There's a growing interest in immersion systems, graphene thermal interface materials, and PFAS-free heat pump hardware, as these technologies present significant potential for innovation and market growth. Additionally, disruptors providing turnkey 800 V cooling stacks and predictive maintenance analytics are actively sought after for partnerships or acquisitions, as they offer advanced solutions to optimize system performance and reduce downtime.

Automotive Thermal Management Industry Leaders

BorgWarner Inc.

Mahle GmbH

Hanon Systems

Valeo

Denso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Valeo signed contracts with Chinese OEMs for next-generation HVAC heat-pump systems using advanced refrigerant management.

- March 2025: NXP and Wolfspeed launched an 800 V silicon-carbide traction inverter reference design with enhanced liquid cooling.

- January 2025: nVent divested its Thermal Management business to Brookfield for USD 1.7 billion, sharpening focus on electrical products while Brookfield gains automotive thermal capabilities.

Global Automotive Thermal Management Market Report Scope

An automotive thermal management system (TMS) monitors and controls the operating temperature of various automotive systems, such as power electronics, transmission, battery, electric drive units, engine, and passenger cabin areas, to improve efficiency and prevent damage to the components.

The automotive thermal management market has been segmented by application type, vehicle type, and geography. By application, the market has been segmented into engine cooling, cabin thermal management, thermal transmission management, waste heat recovery/exhaust gas recirculation (EGR) thermal management, battery thermal management, and motor and power electronics thermal management. By vehicle type, the market has been segmented into passenger cars and commercial vehicles. By geography, the market has been segmented into North America, Europe, Asia-Pacific, and the Rest of the World. The report offers the market size in value (USD Billion) and forecasts for all the above segments. The report also provides market sizing and forecast for all the above-mentioned segments.

| Engine Cooling |

| Cabin / HVAC Thermal Management |

| Transmission Thermal Management |

| Waste-Heat Recovery / EGR |

| Battery Thermal Management |

| Motor & Power-Electronics Cooling |

| Air Cooling & Heating |

| Liquid Indirect Cooling |

| Direct / Immersion Liquid Cooling |

| Phase-Change / PCM Systems |

| Hybrid & Integrated Loops |

| Heat Exchangers (Radiator, CAC, Oil Cooler) |

| Compressors & Pumps |

| Thermal Control Valves & Manifolds |

| High-Voltage Coolant Heaters |

| Sensors & Controllers |

| ICE Vehicles |

| Hybrid Electric Vehicles |

| Plug-in Hybrid Vehicles |

| Battery Electric Vehicles |

| Fuel-Cell Electric Vehicles |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Trucks & Buses |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| UAE | |

| Turkey | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Application | Engine Cooling | |

| Cabin / HVAC Thermal Management | ||

| Transmission Thermal Management | ||

| Waste-Heat Recovery / EGR | ||

| Battery Thermal Management | ||

| Motor & Power-Electronics Cooling | ||

| By Technology Type | Air Cooling & Heating | |

| Liquid Indirect Cooling | ||

| Direct / Immersion Liquid Cooling | ||

| Phase-Change / PCM Systems | ||

| Hybrid & Integrated Loops | ||

| By Component | Heat Exchangers (Radiator, CAC, Oil Cooler) | |

| Compressors & Pumps | ||

| Thermal Control Valves & Manifolds | ||

| High-Voltage Coolant Heaters | ||

| Sensors & Controllers | ||

| By Propulsion Type | ICE Vehicles | |

| Hybrid Electric Vehicles | ||

| Plug-in Hybrid Vehicles | ||

| Battery Electric Vehicles | ||

| Fuel-Cell Electric Vehicles | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Trucks & Buses | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| UAE | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the automotive thermal management market in 2026?

The automotive thermal management market totaled USD 111.46 billion in 2026 and is forecast to reach USD 147.61 billion by 2031.

Which application is growing fastest within thermal management?

Battery thermal management is the fastest-growing application, advancing at a 5.83% CAGR as EV adoption accelerates.

What region dominates demand for thermal management systems?

Asia-Pacific leads with 39.17% market share in 2025, backed by China’s dominant EV production volumes.

Why are 800 V architectures essential for cooling suppliers?

800 V platforms use silicon-carbide inverters that run hotter than legacy silicon, requiring immersion or advanced liquid cooling to protect devices at 175 °C junction temperatures.

How will PFAS regulations affect thermal management components?

EU PFAS restrictions will phase out current refrigerants, forcing a switch to natural options like propane and CO₂, driving redesigns of compressors, heat pumps, and safety systems.

Which components show the highest growth rate?

Compressors and pumps rise the fastest, charting a 5.85% CAGR as electrified cooling circuits multiply in BEVs and hybrids.

Page last updated on: