Electric Vehicle Motor Communication Controller Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

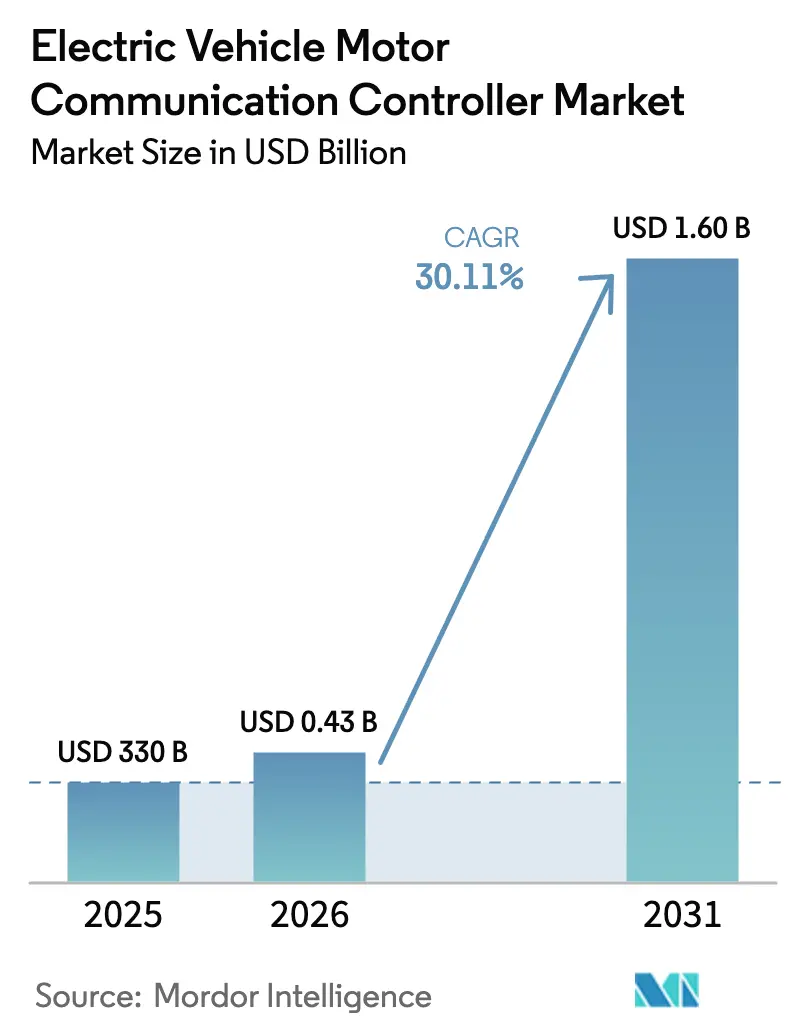

| Market Size (2026) | USD 0.43 Billion |

| Market Size (2031) | USD 1.6 Billion |

| Growth Rate (2026 - 2031) | 30.11% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

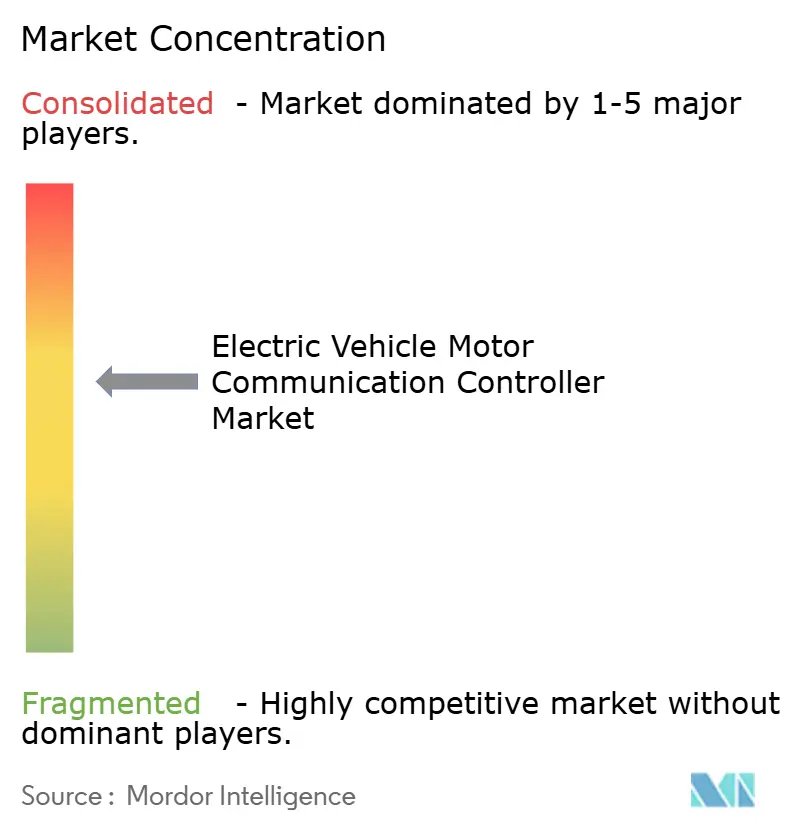

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle Motor Communication Controller Market Analysis by Mordor Intelligence

The Electric Vehicle Motor Communication Controller market size is expected to grow from USD 330 million in 2025 to USD 430 million in 2026 and is forecast to reach USD 1.6 billion by 2031 at 30.11% CAGR over 2026-2031. High-voltage 800 V battery systems, falling silicon-carbide device costs, and stringent drivetrain-efficiency regulations collectively accelerate controller adoption. In parallel, automakers’ transition to zonal electrical-electronic (E/E) architectures and the move toward software-defined vehicles expand bandwidth, functional-safety, and cybersecurity requirements that only advanced controllers can meet.

Key Report Takeaways

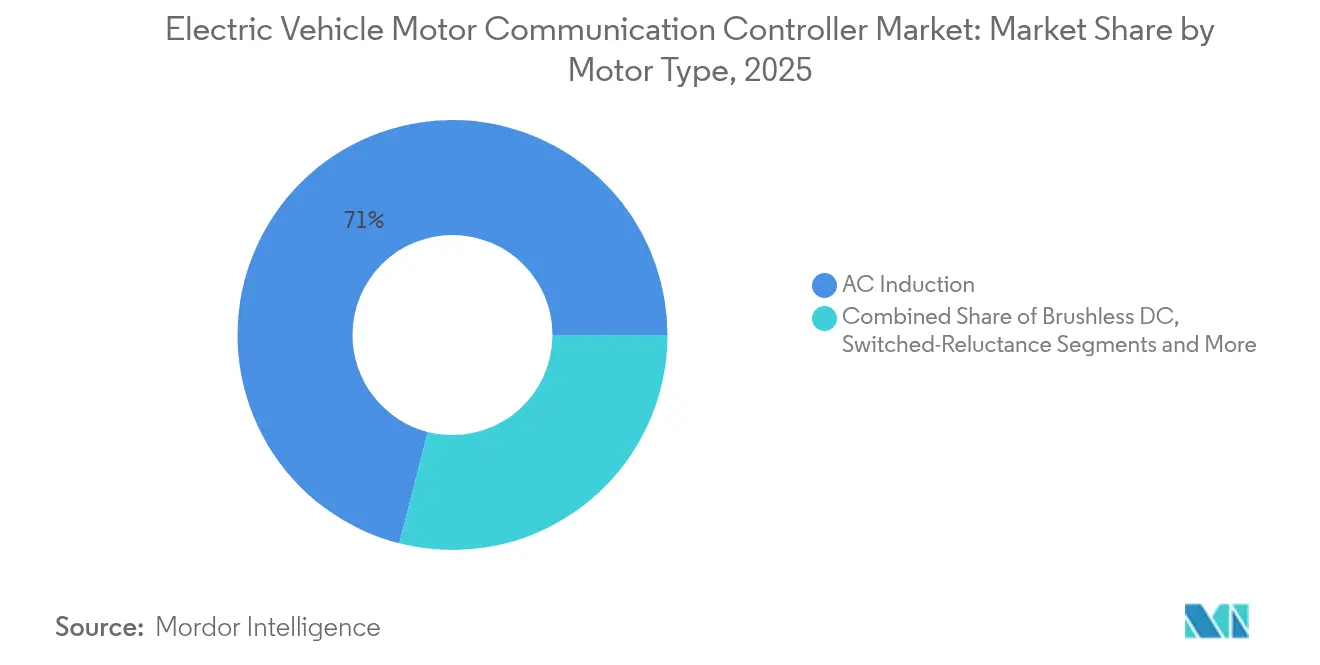

- By motor type, AC Induction motors led with 71.02% of electric vehicle motor communication controller market share in 2025, while Brushless DC motors are projected to post the fastest 33.95% CAGR through 2031.

- By communication protocol, CAN 2.0 accounted for 62.85% of the electric vehicle motor communication controller market size in 2025; Automotive Ethernet is forecast to expand at 31.74% CAGR between 2026 and 2031.

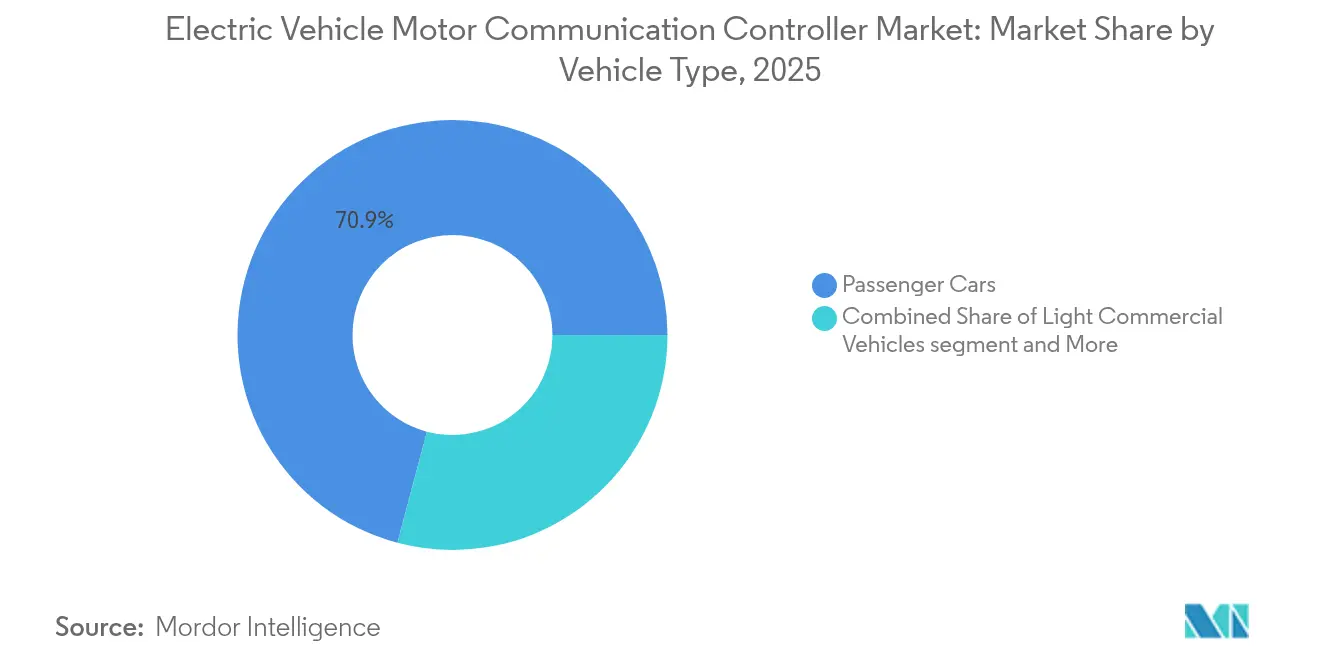

- By vehicle type, passenger cars held 70.88% share of the electric vehicle motor communication controller market size in 2025, whereas medium and heavy commercial vehicles are poised for the highest 32.85% CAGR to 2031.

- By propulsion type, Battery Electric Vehicles commanded a 73.10% share in 2025; Fuel-Cell Electric Vehicles are expected to grow at a 30.70% CAGR through 2031.

- By geography, Asia-Pacific captured 49.20% of electric vehicle motor communication controller market share in 2025 and is advancing at a 34.19% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Vehicle Motor Communication Controller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Global EV Production Volumes | +8.2% | Global, with APAC leading | Short term (≤ 2 years) |

| Shift to 800V Architectures | +6.8% | North America & EU premium segments, expanding to APAC | Medium term (2-4 years) |

| Falling SiC & IGBT Costs | +5.4% | Global, with manufacturing concentration in APAC | Medium term (2-4 years) |

| Stricter Drivetrain-Efficiency Regulations | +4.1% | EU & North America, extending to China | Long term (≥ 4 years) |

| OEM Move to Zonal E/E Architectures | +3.7% | Global, led by premium OEMs | Medium term (2-4 years) |

| Software-Defined-Vehicle Monetisation | +2.9% | North America & EU initially, global expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Global EV Production Volumes

Electric-car output rose to 17.3 million units in 2024, with China producing 12.4 million vehicles and exceeding 70% of global volume.[1]“Global EV Outlook 2024,” International Energy Agency, iea.org This unprecedented scale magnifies the need for resilient, high-bandwidth controllers to coordinate dual and tri-motor configurations, battery-management systems, and central vehicle computers. It has been estimated that traction-motor output will surpass 120 million units by 2034, controller demand grows proportionally, cementing the electric vehicle motor communication controller market as a cornerstone of electrified powertrains.

Shift to 800 V Architectures

BMW’s Neue Klasse platform and ZF’s EVSys800 demonstrate how 800 V systems raise computational throughput by an order of magnitude while imposing harsher electromagnetic and thermal loads.[2]“EVSys800 High-Voltage Propulsion,” ZF Group, zf.com Controllers must therefore implement advanced time-sensitive networking and support silicon-carbide inverter coordination, steering premium OEMs toward Ethernet-based or proprietary protocols capable of deterministic, real-time exchange.

Falling SiC & IGBT Costs

STMicroelectronics holds majority of the share in SiC power devices, and the automotive SiC market is projected to growth at a modest rate by 2026, driving controller cost reduction and feature expansion. Infineon’s partnership with FORVIA HELLA on 1200 V CoolSiC MOSFETs shows how lower semiconductor prices unlock new 800 V DC-DC and inverter applications, reinforcing uptake in the electric vehicle motor communication controller market.

Stricter Drivetrain-Efficiency Regulations

European Union CO₂ mandates and North American efficiency rules oblige OEMs to squeeze additional kilometers from each kilowatt-hour, elevating the role of predictive algorithms embedded in the controller. ABB’s three-level topology inverters for electric buses, which cut harmonic losses by up to 75%, exemplify regulatory-driven innovation requiring higher-bandwidth control loops.[3]“Three-Level Topology Inverter for eBus,” ABB, new.abb.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Power-Semiconductor Supply Volatility | -4.6% | Global, with APAC manufacturing concentration | Short term (≤ 2 years) |

| ISO 26262 Compliance Costs | -3.2% | Global, with higher impact in regulated markets | Medium term (2-4 years) |

| Cyber-Security Certification Delays | -2.8% | EU & North America primarily | Medium term (2-4 years) |

| Thermal-Interface Material Shortages | -1.9% | Global, affecting high-power applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Power-Semiconductor Supply Volatility

New Chinese licensing rules on rare-earth exports threaten up to 98% of Europe’s magnet supply, replicating the 2021-2023 chip shortages that idled assembly lines at Ford and Suzuki. High-quality SiC wafer yields remain below 60%, delaying controller availability for 800 V platforms and exposing OEM programmes to prolonged validation cycles.

ISO 26262 Compliance Costs

Certification to ASIL D elevates documentation, traceability, and verification overheads, often extending controller development by up to two years. NXP’s SafeAssure methodology illustrates how only suppliers with mature functional-safety processes can absorb the cost and meet programme timing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: AC Induction Dominance Faces Efficiency Challenge

AC Induction motors held the majority, 71.02%, of the electric vehicle motor communication controller market share in 2025, cementing their role in cost-sensitive segments. Yet, Brushless DC motors, advancing at 33.95% CAGR, spur demand for high-speed sensing and sophisticated commutation algorithms that stretch CAN FD capacity.

Emerging rare-earth-free initiatives such as ZF’s I2SM motor and Renault’s cooperation with Valeo on electrically excited synchronous motors reshape control-loop requirements. As OEMs evaluate mixed motor strategies—pairing induction drives on front axles with permanent-magnet units at the rear—controller suppliers can harmonise multi-motor mix gain share.

By Communication Protocol: Ethernet Emergence Challenges, CAN Dominance

CAN 2.0 carried 62.85% of the electric vehicle motor communication controller market size in 2025, but Automotive Ethernet is racing ahead at 31.74% CAGR as vehicles migrate to gigabit backbones. Ethernet’s compatibility with time-sensitive networking and power over data lines enables controller consolidation and wiring reductions, critical to premium platforms targeting 800 V architectures. CAN-FD extends legacy networks by lifting payloads to 64 bytes and data rates to 8 Mbps, offering a low-risk upgrade path in vehicle low-voltage zones.

FlexRay persists in redundant brake-by-wire loops, while LIN remains for body-control tasks, yet both face flat growth as OEMs streamline bus topologies. On the horizon, CAN XL promises 20 Mbit/s throughput, but adoption hinges on silicon readiness and test-tool availability. Tesla’s time-division multiple access scheme underscores the scope for proprietary alternatives that could segment the electric vehicle motor communication controller market along vertical-integration lines.

By Vehicle Type: Commercial Vehicles Drive Innovation

Passenger Cars dominated 70.88% of the electric vehicle motor communication controller market size in 2025, but emission mandates push Heavy Commercial Vehicles to the fastest 32.85% CAGR. High-voltage, high-torque duty cycles for buses and trucks necessitate redundant controllers with advanced thermal derating algorithms. Propelled by urban delivery demand, Light Commercial Vehicles integrate predictive-maintenance data streams to reduce downtime.

Fleets value diagnostics, so controllers embed edge analytics to compress operating data before cloud uplink, enhancing total-cost-of-ownership benefits. Two- and three-wheelers in Asia diversify the electric vehicle motor communication controller market, yet their low price points constrain feature sets, compelling suppliers to reuse passenger-car ASICs where possible.

By Propulsion Type: Fuel-Cell Systems Emerge as Growth Driver

Battery Electric Vehicles secured 73.10% market share in 2025, but fuel-cell platforms are scaling at 30.70% CAGR because hydrogen’s energy density suits long-haul trucking. While observing hydrogen-safety protocols, controllers must orchestrate high-frequency communication between fuel-cell stacks, buffer batteries, and traction inverters. Plug-in hybrids maintain relevance in markets with sparse charging infrastructure and extend controller complexity by combining internal-combustion diagnostics with electric drive coordination.

Bosch and Vitesco Technologies' fuel-cell projects demonstrate how the electric vehicle motor communication controller industry adapts to multi-source propulsion. Code-base modularity, galvanic isolation, and hydrogen-purge management become design prerequisites. Suppliers offering unified controller architectures across battery and fuel-cell drivetrains improve programme economics as regulators tighten tank-to-wheel carbon metrics.

Geography Analysis

Asia-Pacific holds 49.20% of market share in 2025 and the region’s scale, government incentives, and tight coupling between motor, inverter, and controller factories generate cost efficiencies unmatched elsewhere. However, export controls on rare-earth elements and regional geopolitical tensions force OEMs to dual-source semiconductors outside China, adding logistic complexity to the electric vehicle motor communication controller market. Regional universities and state-funded institutes accelerate the development of automotive Ethernet and cybersecurity protocols, supplying a steady engineering pipeline.

North America grows at a robust CAGR of 30.65% through 2031, leverages the Inflation Reduction Act credits to localise battery and controller production. General Motors’ USD 4 billion investment in Detroit-Hamtramck and Siemens’ CAD 150 million AI R&D centre in Canada exemplify capital flows into vertically integrated EV supply chains. These facilities prioritise high-power 800 V trucks and premium SUVs, translating into controller demand for high current-sensing precision and advanced thermal modelling.

Europe’s legacy in premium vehicles and regulatory leadership spurs high-value controller requirements, including mandatory cybersecurity management systems under UNECE R155, growing at a CAGR of 27.85% till 2031. Investments such as Vitesco’s EUR 576 million Ostrava plant support high-voltage electronic modules, keeping Europe competitive amid cost pressure from imported Chinese components. The electric vehicle motor communication controller market in Europe also benefits from regional standardisation efforts that accelerate cross-OEM interoperability.

Competitive Landscape

Global suppliers like Bosch, Siemens, and Infineon control critical layers—power semiconductors, firmware, and functional safety libraries—allowing rapid platform scaling across multiple OEM programmes. These incumbents exploit capital depth to certify ASIL D products and secure early-adopter slots on premium 800 V platforms. Specialist firms such as Vector Informatik concentrate on Automotive Ethernet stacks and test automation, carving niche revenue streams within the electric vehicle motor communication controller market.

Infineon works with Typhoon HIL on hardware-in-the-loop validation, while STMicroelectronics collaborates with suppliers on SiC module packaging to mitigate thermal bottlenecks. Proprietary protocols emerge as differentiation levers, with Tesla’s TDMA system replacing legacy CAN and triggering a counter-movement among standardisation bodies. Cybersecurity compliance under ISO/SAE 21434 confers moat-like advantages, prompting mergers or dissolutions of smaller players unable to finance penetration testing and lifecycle support.

Looking ahead, white-space lies in controller platforms that unify battery, motor, and fuel-cell communication while exposing cloud-native APIs for predictive analytics. Players combining silicon-level IP with over-the-air update frameworks gain optionality, positioning themselves to capture incremental SaaS revenue tied to propulsion analytics. Patent filings indicate intensifying competition around zonal architecture gateway controllers, underscoring a market where firmware adaptability equals hardware performance.

Electric Vehicle Motor Communication Controller Industry Leaders

LG Innotek

Robert Bosch GmbH

Vitesco Technologies Group AG

Infineon Technologies AG

Denso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Siemens opened a Global AI Manufacturing Technologies R&D Center for Battery Production in Canada with CAD 150 million investment, targeting advanced quality control for EV battery lines.

- February 2025: BorgWarner won four electric-motor contracts with three Chinese OEMs for 400 V hairpin motors, with production starting in August 2025 for hybrids and March 2026 for pure EVs.

- January 2025: FORVIA HELLA chose Infineon’s CoolSiC Automotive MOSFET 1200 V for next-gen 800 V DC-DC converters that use top-side cooling to improve thermal performance.

- September 2024: Siemens and E.ON signed a framework to deploy at least 1,000 high-power public chargers each year across Europe using SICHARGE D hardware and Sifinity Control backend.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the electric-vehicle motor communication controller market as the value of factory-installed electronic units that mediate data flow between a traction motor's control electronics and the wider vehicle network, enabling torque commands, diagnostics, and safety interlocks. These controllers typically support CAN 2.0, CAN-FD, LIN, FlexRay, or Automotive Ethernet protocols and are counted in USD value at the point of vehicle assembly.

Scope exclusion: After-sale retrofits, stand-alone motor inverters, and supply-equipment communication controllers positioned inside charging stations are outside our modeling horizon.

Segmentation Overview

- By Motor Type

- AC Induction

- Permanent-Magnet Synchronous (PMSM)

- Brushless DC

- Switched-Reluctance

- By Communication Protocol

- CAN 2.0

- CAN-FD

- Automotive Ethernet

- FlexRay

- LIN

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Two and Three-Wheelers

- Off-Highway & Specialty EVs

- By Propulsion Type

- Battery Electric Vehicles

- Plug-in Hybrid Electric Vehicles

- Fuel-Cell Electric Vehicles

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with power-electronics engineers, tier-one supplier product heads, and OEM sourcing managers across Asia-Pacific, Europe, and North America allowed us to validate controller attach rates, clarify evolving voltage platforms, and stress-test preliminary forecasts. Email surveys with charging-architecture specialists further refined assumptions on protocol migration from CAN 2.0 to Automotive Ethernet.

Desk Research

We began by screening open datasets such as the International Energy Agency EV stock tables, OICA light-duty production logs, UN Comtrade tariff lines for HS 850300 and HS 853710, and patent families retrieved via Questel that map to ISO 15118 compliant controller designs. Trade association white papers from the Society of Automotive Engineers, China EV100, and ZVEI helped us benchmark protocol adoption rates. Company 10-Ks, investor decks, and press releases provided average selling price (ASP) signals that we cross-checked against D&B Hoovers and Dow Jones Factiva. This list is illustrative; many additional publications were consulted for triangulation and clarification.

Market-Sizing & Forecasting

A top-down build starts with regional EV production, subtracts hybrid shares lacking dedicated motor controllers, and applies protocol-specific penetration and weighted ASPs. Selective bottom-up checks using sampled supplier revenue and channel feedback serve as guardrails. Core variables include: 1) battery-electric vehicle output, 2) average motors per vehicle, 3) controller ASP by protocol, 4) shift toward 800 V architectures, and 5) regional content-localization ratios. Multivariate regression anchored on these drivers, blended with scenario analysis for policy shocks, yields the 2025-2030 outlook. Where bottom-up samples diverged by over five percent, gap-fills were guided by median ASPs derived from customs invoices.

Data Validation & Update Cycle

Outputs pass automated variance flags, senior-analyst peer review, and a manager sign-off. Models refresh yearly, with interim revisions triggered by material events such as a new communication-protocol mandate. Clients therefore receive the most current baseline before every report release.

Why Mordor's Electric Vehicle Motor Communication Controller Baseline Commands Reliability

Published market sizes often differ because firms pick unique component scopes, currency bases, and refresh cadences.

Key gap drivers include whether supply-equipment controllers are bundled, how aggressively wide-bandgap ASP deflation is assumed, and whether 48 V mild hybrids are mistakenly classified. Mordor analysts restrict scope to on-board motor communication units, use actual 2024-2025 trade invoices for ASP trends, and update models annually, which reduces overstatement seen in infrequent updates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.33 Bn (2025) | Mordor Intelligence | - |

| USD 0.97 Bn (2025) | Global Consultancy A | Bundles charging-station controllers and assumes flat ASPs through 2030 |

| USD 0.80 Bn (2025) | Industry Research B | Uses EV sales targets rather than production and omits regional content localization |

| USD 0.22 Bn (2025) | Trade Journal C | Excludes high-voltage platforms and applies conservative motor-per-vehicle factors |

In sum, our disciplined scope selection, variable transparency, and yearly refresh schedule give decision-makers a balanced, reproducible baseline they can trust for strategic planning.

Key Questions Answered in the Report

What is the projected value of the electric vehicle motor communication controller market by 2031?

The market is expected to reach USD 1.6 billion by 2031, growing at a 30.11% CAGR from its 2025 base of USD 330 million.

Which motor type currently dominates controller demand?

AC Induction motors remain dominant, accounting for 71.02% of controller demand in 2025, although Brushless DC motors are the fastest-growing segment, with a 33.95% CAGR.

Why is Automotive Ethernet gaining traction over traditional CAN bus?

Automotive Ethernet supports gigabit data rates, time-sensitive networking, and power over data lines, features essential for 800 V architectures and zonal E/E designs that exceed CAN 2.0 bandwidth limits.

How do ISO 26262 and ISO/SAE 21434 influence market entry?

These standards impose rigorous functional-safety and cybersecurity requirements that elevate development cost and complexity, favouring suppliers with established certification infrastructure and consolidating market share.

Which region offers the strongest growth prospects through 2031?

Asia-Pacific leads both in current share and growth, holding 49.20% of 2025 revenue and expanding at a 34.19% CAGR, driven primarily by China’s production scale and Southeast Asian capacity build-out.

What technological shift is driving controller redesign in premium EV platforms?

The migration to 800 V battery systems requires controllers capable of managing higher voltage, faster power-device switching, and advanced thermal management. This will accelerate the adoption of high-bandwidth protocols and silicon-carbide-based electronics.

Page last updated on: