Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 26.79 Billion |

| Market Size (2031) | USD 36.46 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

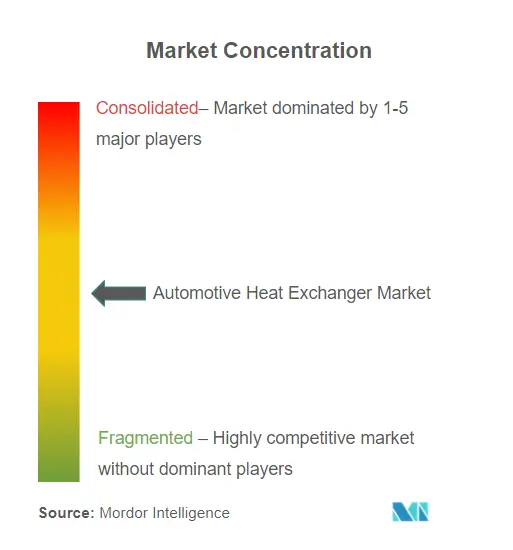

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Heat Exchanger Market Analysis by Mordor Intelligence

The Automotive Heat Exchanger Market size was valued at USD 25.19 billion in 2025 and estimated to grow from USD 26.79 billion in 2026 to reach USD 36.46 billion by 2031, at a CAGR of 6.36% during the forecast period (2026-2031). The shift from internal-combustion cooling loops to multi-loop architectures for battery, power electronics, and cabin climate control underpins this expansion across the automotive heat exchanger market. Electrified platforms demand components that prevent battery thermal runaway, manage 800-V charging loads, and conserve vehicle range[1]“Integrated Report 2024,” DENSO Corporation, denso.com. Strong electric-vehicle adoption in Asia-Pacific, Euro 7 durability rules, and heat-pump integration also elevate product complexity and value content in the automotive heat exchanger market. Suppliers are responding with micro-channel designs, corrosion-resistant alloys, and integrated heat-pump modules, while materials volatility in aluminum and copper continues to pressure margins across the automotive heat exchanger market.

Key Report Takeaways

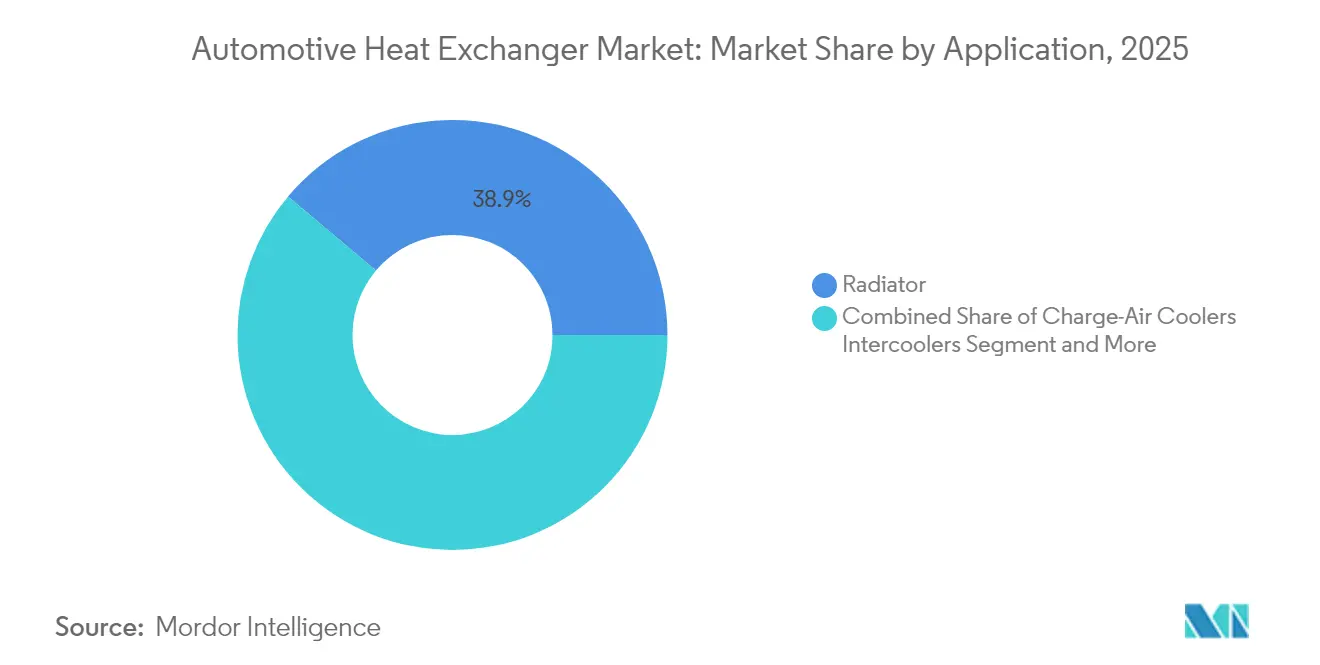

- By application, radiators led the automotive heat exchanger market with 38.86% of the share in 2025, while battery and power electronics coolers are advancing at a 12.74% CAGR through 2031.

- By design type, tube-fin configurations commanded a 46.92% share of the automotive heat exchanger market in 2025; plate-bar units are expected to grow at an 8.65% CAGR.

- By material, aluminum accounts for 72.84% share of the automotive heat exchanger market in 2025, whereas stainless steel is the fastest-growing material, forecast to expand at an 8.36% CAGR from 2026 - 2031.

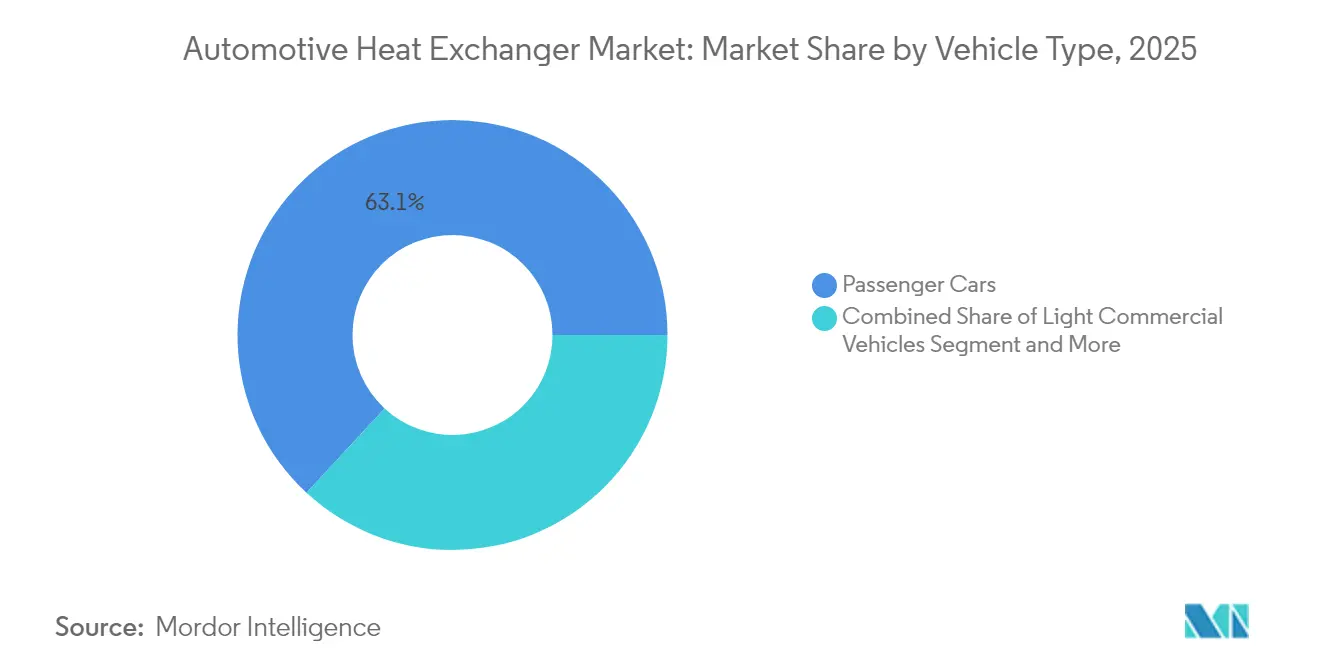

- By vehicle type, passenger cars held 63.12% of the automotive heat exchanger market share in 2025; light commercial and heavy vehicle segments are forecast to post the fastest collective CAGR at 8.61% to 2031.

- By powertrain, internal-combustion engines accounted for 51.96% of the automotive heat exchanger market size in 2025, whereas battery electric vehicles are expanding at a 14.97% CAGR.

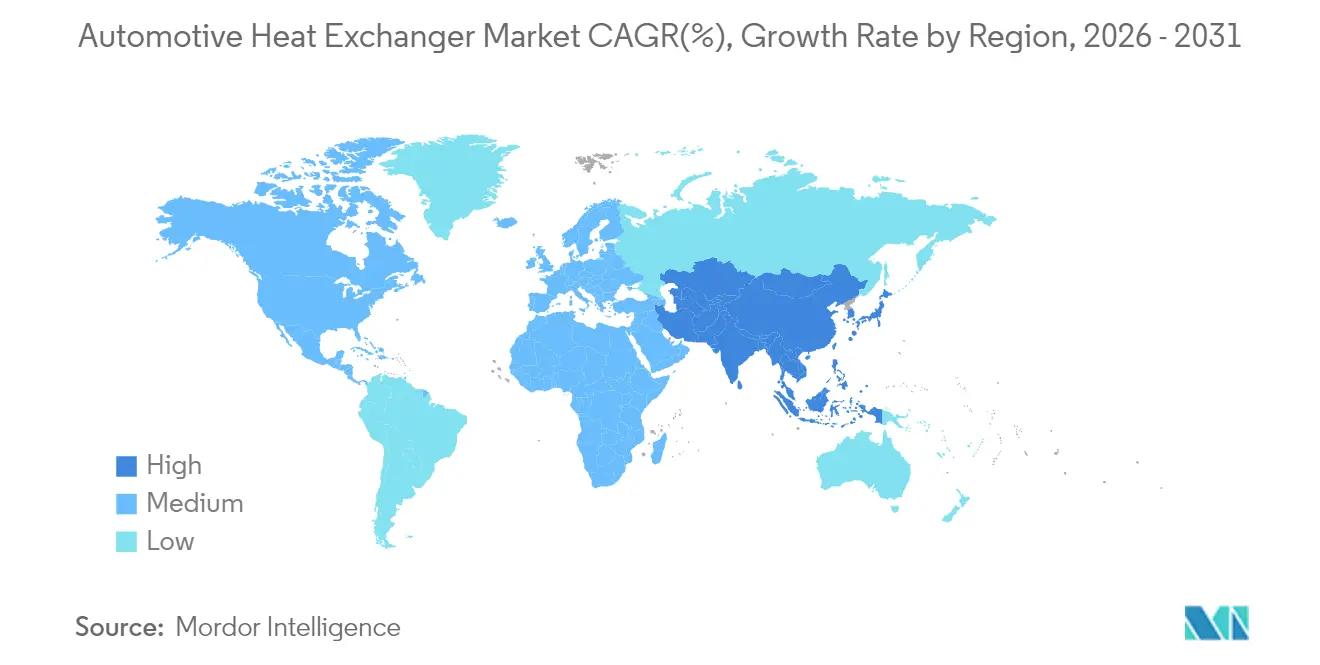

- By geography, Asia-Pacific captured 46.88% revenue in 2025 and remains the fastest-growing region with an 8.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Heat Exchanger Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Sales-Driven Demand For Advanced Thermal Management | +2.1% | Global, with APAC and Europe leading adoption | Medium term (2-4 years) |

| Stringent Global Emission Regulations | +1.8% | Europe and North America primary, spillover to APAC | Long term (≥ 4 years) |

| Heat-Pump System Integration In Electric Vehicles | +1.2% | Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Rising HVAC Penetration In Emerging Markets | +0.9% | APAC core, spillover to MEA and South America | Medium term (2-4 years) |

| 800-V High-Voltage XEV Architectures | +0.7% | Premium segments globally, mass market following | Long term (≥ 4 years) |

| Fuel-Cell Humidifier Exchanger Adoption | +0.3% | Japan, South Korea, select European markets | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

EV Sales-Driven Demand for Advanced Thermal Management

Electric vehicles require roughly 30% more aluminum than combustion cars, forcing the redesign of exchangers beyond radiator duty. Battery loops must keep cell temperatures within a 2 °C band to avoid runaway, while silicon-carbide inverters impose localized heat spikes handled by micro-channel cores[2]“Lightweight Aluminum Solutions for EVs,” MacDermid Enthone, macdermidenthone.com. Low-conductivity fluids, such as Prestone’s GB29743-2–compliant coolant shape alloy and coating choices, and direct-immersion cooling, open a niche for dielectric units that eliminate conductivity risk.

Stringent Global Emission Regulations

Euro 7 rules published in May 2024 unify tailpipe limits and add brake- and tire-particulate caps, indirectly raising thermal loads as automakers chase efficiency gains. Required battery durability pushes exchanger life targets beyond a decade, spurring corrosion-proof brazing sheets while onboard diagnostics enable predictive flow control. Program timelines to November 2026 tighten validation windows, favoring suppliers with pre-certified test benches.

Heat-pump System Integration in Electric Vehicles

Reversible heat-pump loops now pre-condition packs and cabin air. Hyundai’s radiant heating cuts energy draw by 17% through nanotube films, letting exchangers run cooler yet sustain comfort[3]“Next-Generation Radiant Heating Technology,” Hyundai Motor Group, hyundai.com. Valeo’s Smart eDrive 6-in-1 uses internal oil cooling to shrink radiator area, showing how integrated modules free vehicle packaging for larger batteries.

Rising HVAC Penetration in Emerging Markets

Demand for affordable climate control lifts combined cabin-and-powertrain modules in Asia. Hanon’s USD 300 million Canadian compressor plant targets 900,000 electric units annually, underlining volume growth. High recycling rates—secondary aluminum needs 95% less energy, which aligns with cost-sensitive buyers while meeting OEM decarbonization targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminum and Copper Price Volatility | -1.4% | Global, with particular impact on North America and Europe | Short term (≤ 2 years) |

| Micro-Channel Extrusion Supply Bottlenecks | -1.1% | Global manufacturing, concentrated in Asia-Pacific supply chains | Short term (≤ 2 years |

| Stringent Durability and Corrosion Validation Costs | -0.8% | Europe and North America regulatory markets | Medium term (2-4 years) |

| Declining Heat-Load In Solid-State Battery Packs | -0.6% | Premium segments initially, mass market following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aluminum and Copper Price Volatility

Electric models can contain up to 80 kg copper—four times that of combustion cars—making exchanger cost highly sensitive to spot prices. Automakers hedge with multiyear contracts and closed-loop recycling, yet regional premiums still skew sourcing strategies. Alloy innovation that lifts conductivity per unit weight helps limit primary metal demand, stabilizing costs when exchange rates spike.

Micro-channel Extrusion Supply Bottlenecks

High-precision dies and limited presses restrict micro-channel output to several Asian suppliers. Lead times lengthen during demand surges, slowing model launches. Additive manufacturing offers a workaround, as 3-D-printed lattice cores cut scrap and permit localized build-to-order production. Scaling that approach could rebalance bargaining power between OEMs and extrusion specialists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Battery Cooling Drives Thermal Innovation

Radiators accounted for the largest slice of the automotive heat exchanger market size, holding 38.86% revenue in 2025. Their share slips as battery and power-electronics coolers record a 12.74% CAGR to 2031, reflecting electrification priorities. Lithium-ion packs demand ±2 °C thermal stability for fast charging, prompting integrated chill plates and dielectric immersion modules in the automotive heat exchanger market. Charge-air systems keep pace with turbocharging, while oil coolers pivot toward e-axle lubrication. Cabin evaporators and condensers evolve into reversible heat-pump exchangers, and hydrogen fuel-cell humidifiers surface as a nascent niche.

The automotive heat exchanger market continues to prize radiator volumes. Yet, white-space lies in stack humidification modules for fuel-cell buses and trucks, where Eberspächer’s exhaust-air unit blends water recovery with acoustic damping. Hybrid exhaust-heat recovery remains relevant in Euro-7-compliant powertrains, giving suppliers a bridge product as pure battery adoption climbs.

By Design Type: Micro-channel Technology Gains Traction

Tube-fin cores represented 46.92% of automotive heat exchanger market share in 2025 owing to mature tooling and low cost. Plate-bar assemblies grow 8.65% CAGR as OEMs trade off thickness for crash packaging in skateboard chassis. The automotive heat exchanger market size for micro-channel flat tube units is scaling fastest because superior transfer coefficients enable slim modules around crowded battery trays. Heat pipes and vapor chambers appear in premium battery packs, a trend likely to cascade as solid-state cells lower heat loads but tighten temperature uniformity needs.

In high-pressure loops, shell-and-tube exchangers preserve a foothold, mainly in hydrogen fuel-cell and waste-heat recovery systems where robustness outweighs weight penalties. Concurrently, plate-bar variants adopt internal offset fins to temper flow velocity and noise, reinforcing their position in commercial-vehicle charge-air cooling.

By Material: Aluminum Dominance Persists, Stainless Steel Accelerates

Aluminum held 72.84% of the automotive heat exchanger market share in 2025, Electric vehicles require 30% more aluminum than combustion models, so secondary smelters that cut energy use by 95% help stabilize raw-material supply while cushioning cost swings. High extrusion throughput also keeps unit prices low, supporting radiator volumes that still dominate the automotive heat exchanger market size. Copper remains favored in high-flux zones but exposes OEMs to spot-price volatility, while brass use slips as light-weighting pressures mount. Polymer-coated aluminum tubes that resist coolant acidity enter mass production, extending exchanger life under Euro 7 durability rules.

Stainless steel is the fastest-growing material, forecast to expand at an 8.36% CAGR from 2026 - 2031 as Euro 7 pushes exhaust-gas heat-recovery and hydrogen fuel-cell stacks that demand corrosion resistance at temperatures above 700 °C. Its share rise comes despite higher density, because robustness outweighs weight penalties in heavy-duty and off-highway applications. Hybrid waste-heat recovery, fuel-cell humidifiers, and 350-bar hydrogen tanks favor stainless-steel plate-bar or shell-and-tube cores, carving a profitable niche inside the broader automotive heat exchanger market. Composites and carbon-fiber-reinforced polymers continue to attract R&D budgets owing to dielectric and weight benefits, yet automation and resin-infusion costs will likely confine them to premium programs until volume efficiencies improve.

By Vehicle Type: Commercial Electrification Accelerates

Passenger cars delivered 63.12% of the automotive heat exchanger market size in 2025 as multi-loop systems proliferate. Urban delivery fleets spur the electrification of light commercial vehicles, demanding exchangers tolerant of frequent rapid-charge cycles and payload swings allowing to grew at 8.61% CAGR . Heavy trucks and off-highway machinery add parallel coolant loops for 350-kW fuel-cell stacks, cementing long-term growth channels in the automotive heat exchanger market.

Prototype cycles for e-platforms continue compressing; TI Fluid Systems’ innovation hub cut sample lead times to two weeks, underscoring mounting time-to-market pressures. Fleet operators value total cost of ownership, creating a demand for durable, serviceable exchanger modules that sustain efficiency over the vehicle’s second life.

By Powertrain Type: Electric Surge Reshapes Demand

Internal-combustion engines still contributed 51.96% revenue in 2025, yet battery electric vehicles are racing ahead at a 14.97% CAGR. Hybrids pose the greatest complexity, merging engine, inverter, and pack loops; waste-heat scavenging recovers exhaust energy to preheat batteries and cabins. Fuel-cell stacks introduce humidifiers and high-temperature radiators, expanding the automotive heat exchanger market scope.

BorgWarner’s USD 400 million coolant-heater deal for a 400-V plug-in platform underlines how integrated heating functions complement classic exchangers. Toyota’s standardized 70-MPa tanks indicate hydrogen’s role in the 2030 power mix, keeping demand alive for stainless-steel and composite shell-and-tube units.

Geography Analysis

Asia-Pacific dominated the automotive heat exchanger market with 46.88% share in 2025 and is forecast to expand 8.62% CAGR. China exceeded 35 million vehicle builds in 2025, with EV sales up 50% yearly, benefiting vertically integrated aluminum extruders that produce micro-channel tubes at scale. Japan’s fuel-cell roadmap and South Korea’s radiant heating breakthroughs further diversify technical demand across the automotive heat exchanger market.

North America confronts mixed signals: softer retail EV demand led Ford to trim F-150 Lightning volumes, yet the Inflation Reduction Act spurs localized supply chains. Gentherm booked USD 400 million in new awards while achieving USD 354 million Q1 2025 revenue, reflecting resilience in climate-comfort niches. Domestic extrusion and brazing investment could cushion against foreign material shocks.

Europe’s share is shaped by Euro 7’s November 2026 compliance deadline. Automakers are boosting recycled aluminum use, leveraging a 76% collection rate. Onsemi’s USD 2 billion SiC facility in Czechia elevates regional heat-sink demand owing to higher junction temperatures. National funding also targets hydrogen truck corridors, keeping fuel-cell humidifier lines viable within the automotive heat exchanger market

Competitive Landscape

Competition remains fragmented, DENSO, MAHLE, and Valeo anchor global programs, while Hanon’s acquisition by Hankook strengthens Korean vertical integration. Wieland’s takeover of Onda broadens access to shell-and-tube cores for niche segments, and Aspen Aerogels’ PyroThin barrier award on Porsche’s 718 EV highlights material-science entrant.

Strategically, incumbents pursue micro-channel capacity, 3-D-printed lattice R&D, and low-conductivity coolant partnerships. Integrated module offerings—combining pump, valve, condenser, and control electronics—differentiate bids, particularly where space constraints dominate skateboard platforms. Currency-hedged aluminum contracts and closed-loop recycling help shield margins, yet raw-material volatility can still sway sourcing away from high-labor-cost regions.

Start-ups focus on direct-immersion battery cooling and fuel-cell condensate recycling, eyeing white space in commercial-vehicle duty cycles. Collaborations with inverter suppliers align design interfaces, and software-enabled prognostics open aftermarket revenue through predictive-maintenance subscriptions.

Automotive Heat Exchanger Industry Leaders

Hanon Systems

DENSO Corporation

Valeo SA

MAHLE GmbH

Modine Manufacturing Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BorgWarner won its largest North American high-voltage coolant-heater contract for 400-V plug-in hybrids, with SOP in 2027.

- November 2024: Hankook acquired Hanon Systems, adding a global thermal-management manufacturing footprint.

- October 2024: Hanon Systems opened a USD 300 million Ontario plant for 900,000 electric compressors annually from 2025.

- September 2024: Valeo unveiled Smart eDrive 6-in-1 unit with internal oil cooling, slated for 2026 production.

Global Automotive Heat Exchanger Market Report Scope

Automotive heat exchange helps in allowing the transfer of heat from one medium to another at varying temperatures. The two mediums contain fluids that flow to each other but are separated by a metal having good heat transfer properties. The hot liquid transfers heat to the freezing liquid as they both pass through the heat exchanger, thus decreasing the hot liquid's high temperature and raising the cold liquid's warmth.

The automotive heat exchanger market is segmented by application (radiators, oil coolers, intercoolers, air conditioning, exhaust gas, and other applications), design type (tube-fin, plate-bar, and other design types), vehicle type (passenger cars and commercial vehicles), powertrain type (IC engine vehicles, electric vehicles, and other vehicles), and geography (North America, Europe, Asia-Pacific, and Rest of the World).

The report offers market size and forecasts for the Automotive heat exchanger market in value (USD) for all the above segments.

By Application

| Radiators |

| Charge-Air Coolers / Intercoolers |

| Oil Coolers |

| EGR and Exhaust Gas Heat Recovery |

| Cabin HVAC (Evaporator and Condenser) |

| Battery / Power-electronics Coolers |

| Fuel-cell Humidifiers |

| Other Applications |

By Design Type

| Tube-Fin |

| Plate-Bar |

| Micro-channel Flat Tube |

| Shell-and-Tube |

| Others |

By Material

| Aluminum |

| Copper / Brass |

| Stainless Steel |

| Composites and Polymers |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial and Off-Highway Vehicles |

By Powertrain Type

| Internal Combustion Engine (ICE) |

| Hybrid Electric Vehicles (HEV/PHEV) |

| Battery Electric Vehicles (BEV) |

| Fuel-Cell Electric Vehicles (FCEV) |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Radiators | |

| Charge-Air Coolers / Intercoolers | ||

| Oil Coolers | ||

| EGR and Exhaust Gas Heat Recovery | ||

| Cabin HVAC (Evaporator and Condenser) | ||

| Battery / Power-electronics Coolers | ||

| Fuel-cell Humidifiers | ||

| Other Applications | ||

| By Design Type | Tube-Fin | |

| Plate-Bar | ||

| Micro-channel Flat Tube | ||

| Shell-and-Tube | ||

| Others | ||

| By Material | Aluminum | |

| Copper / Brass | ||

| Stainless Steel | ||

| Composites and Polymers | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial and Off-Highway Vehicles | ||

| By Powertrain Type | Internal Combustion Engine (ICE) | |

| Hybrid Electric Vehicles (HEV/PHEV) | ||

| Battery Electric Vehicles (BEV) | ||

| Fuel-Cell Electric Vehicles (FCEV) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Automotive Heat Exchanger Market?

The Automotive Heat Exchanger Market size is expected to reach USD 26.79 billion in 2026 and grow at a CAGR of 6.36% to reach USD 36.46 billion by 2031.

Which region leads revenue in the automotive heat exchanger market?

Asia-Pacific holds the largest share at 46.88% in 2025 and is also the fastest-growing region with an 8.62% CAGR.

How will Euro 7 regulations influence automotive heat exchangers?

Euro 7 raises durability and emissions-control requirements, driving the adoption of corrosion-resistant materials and data-driven predictive cooling strategies ahead of the November 2026 enforcement date.

Why are micro-channel heat exchangers gaining popularity?

Micro-channel designs deliver higher heat-transfer efficiency in compact packages, making them ideal for space-constrained electric-vehicle platforms where multiple cooling loops are required.

What strategic moves are suppliers making to stay competitive?

Key players are investing in micro-channel capacity, integrated heat-pump modules, recyclable alloys and additive manufacturing to meet evolving EV requirements and shorten development cycles.

Page last updated on: