Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.51 Billion |

| Market Size (2031) | USD 49.83 Billion |

| Growth Rate (2026 - 2031) | 20.63% CAGR |

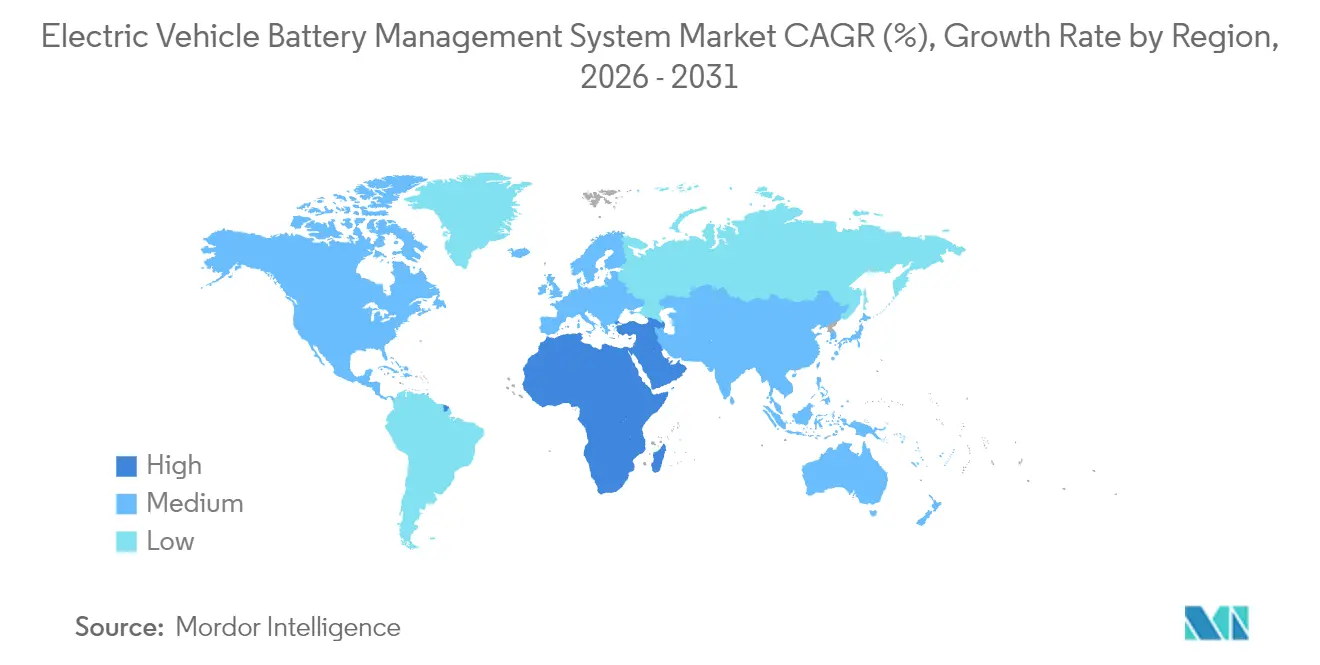

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

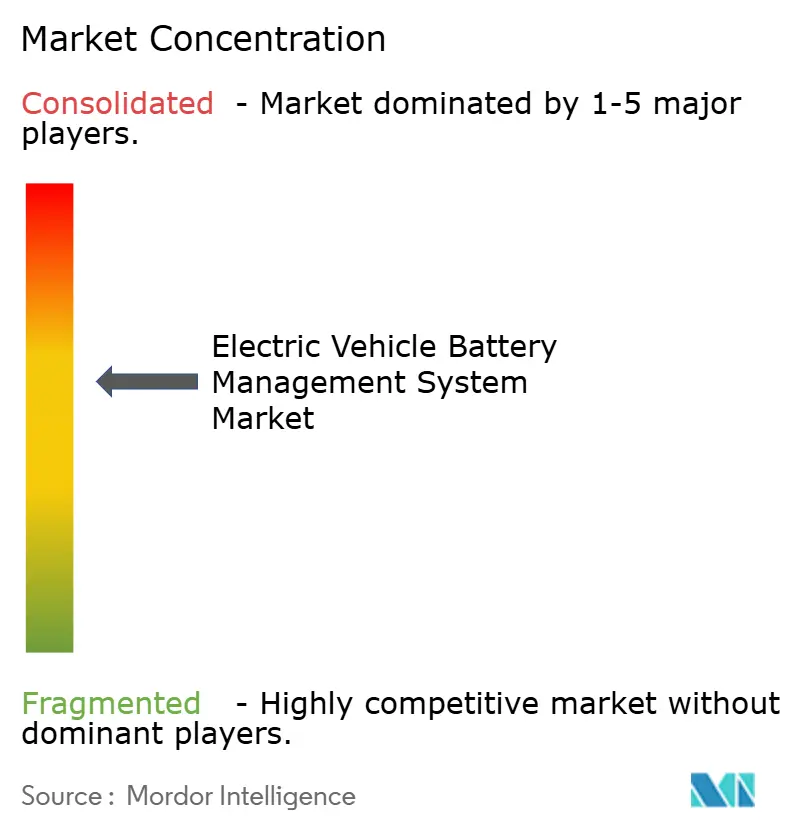

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle Battery Management System Market Analysis by Mordor Intelligence

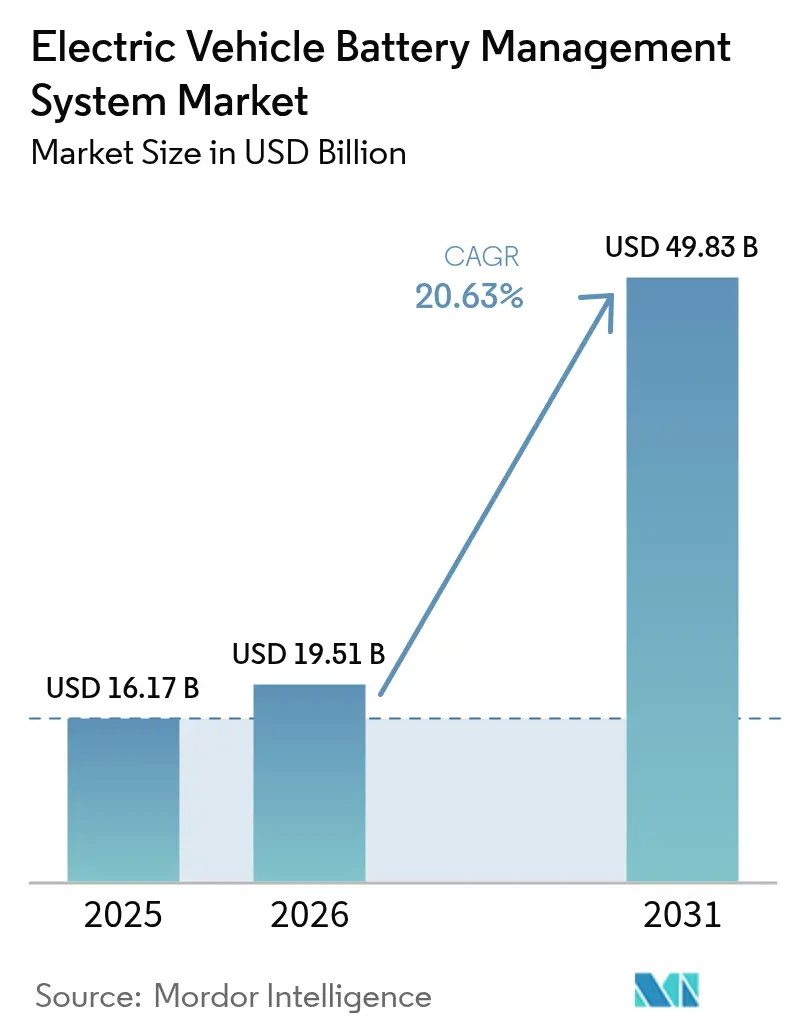

Electric Vehicle Battery Management System Market size in 2026 is estimated at USD 19.51 billion, growing from 2025 value of USD 16.17 billion with 2031 projections showing USD 49.83 billion, growing at 20.63% CAGR over 2026-2031. Demand is powered by rapid vehicle electrification, falling lithium-ion cell prices, and regulations that now push every new electric model toward ASIL-D safety compliance. OEMs favour lighter wireless topologies that cut up to 90% of wiring, enable over-the-air updates and simplify pack service, while tier-one suppliers bundle cloud analytics so fleets can monitor battery health in real time. Declining semiconductor shortages, government incentive schemes, and energy-density gains to 400–500 Wh/kg further expand addressable volumes.

Key Report Takeaways

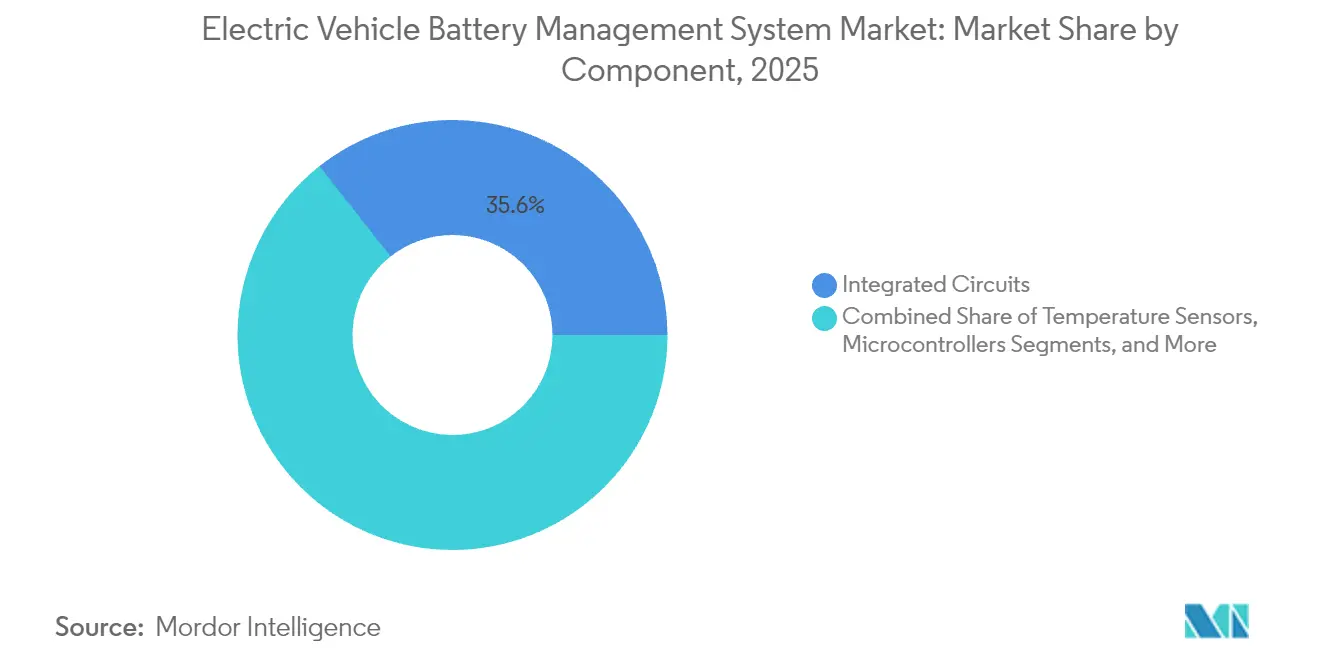

- By component, integrated circuits led with 35.62% revenue share in 2025; wireless communication ICs post the fastest growth at 21.05% CAGR to 2031.

- By battery chemistry, lithium-ion dominated with 87.35% of the battery management system market share in 2025, while solid-state batteries expand at 21.18% CAGR through 2031.

- By topology, modular systems held 42.55% of the battery management system market size in 2025; wireless architectures accelerate at 21.40% CAGR to 2031.

- By communication technology, wired CAN remained at 72.20% share in 2025; wireless RF registers 21.95% CAGR to 2031.

- By propulsion type, BEVs represented 67.80% revenue in 2025; FCEVs grow quickest at 21.30% CAGR.

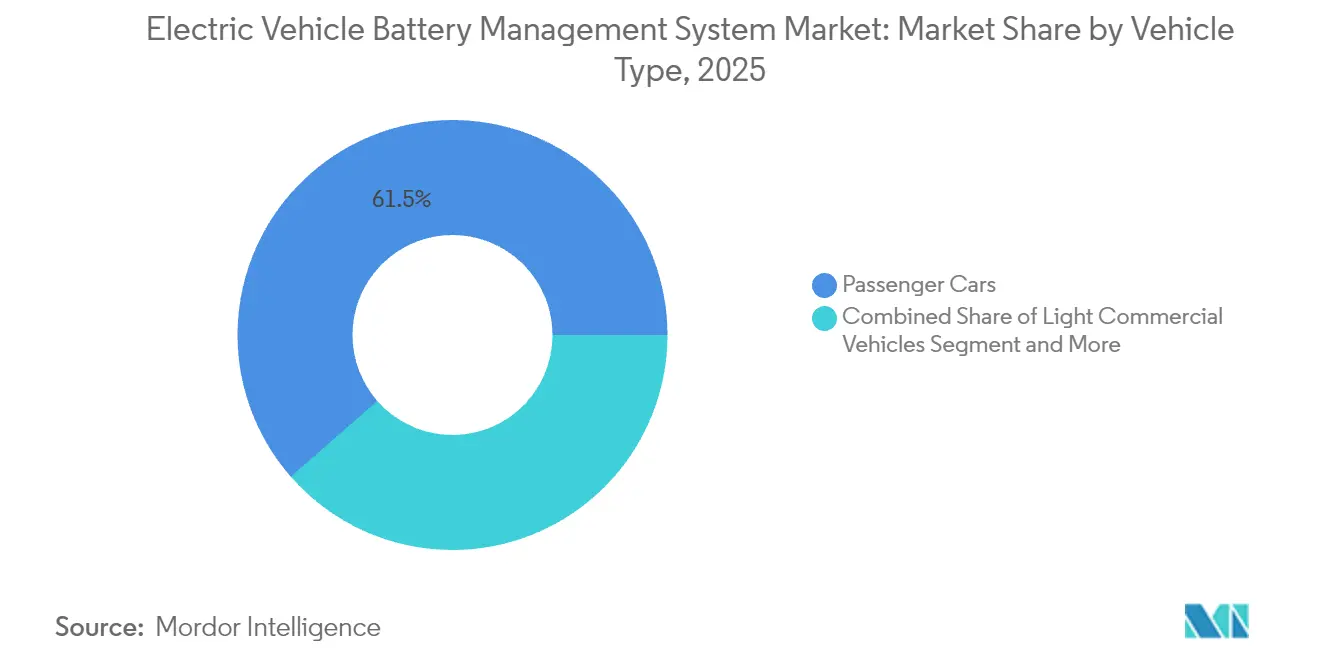

- By vehicle type, passenger cars accounted for 61.45% share of the battery management system market size in 2025; two-wheelers and micro-mobility gain 21.70% CAGR.

- By sales channel, OEM-fitted systems dominated with 84.60% in 2025; the retrofit channel climbs 21.80% CAGR to 2031.

- By geography, Asia-Pacific controlled 47.10% revenue in 2025; the Middle East and Africa region delivers the strongest 21.25% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Vehicle Battery Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Scale-up of Global EV Production | +4.2% | Global, with Concentration in China, Europe, North America | Medium term (2-4 years) |

| Declining Lithium-ion Battery Costs | +3.8% | Global, Particularly Benefiting Emerging Markets | Long term (≥ 4 years) |

| Stringent Safety Regulations | +3.1% | North America and EU, Expanding to APAC | Short term (≤ 2 years) |

| Government Incentives and Emissions Targets | +2.9% | Global, with Strongest Impact in China, EU, California | Medium term (2-4 years) |

| Shift Toward Wireless BMS Architectures | +2.7% | North America and EU Premium Segments, Scaling Globally | Medium term (2-4 years) |

| OEM Subscription-based Battery Analytics Services | +1.8% | North America and EU initially, Expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Scale-up of Global EV Production Volumes

Global EV battery consumption hit 285.4 GWh in the first five months of 2024, a 23% year-on-year jump. This surge forces manufacturers to adopt modular battery management system market architectures so that a single design works across multiple vehicle platforms. Transitioning to 800 V and even 1,200 V packs obliges BMS vendors to upgrade monitoring precision, thermal models and fault isolation logic. General Motors adopted a wireless BMS on its Ultium platform to standardize packs while removing heavy harnesses. Automated BMS test rigs replace manual validation to meet higher production cadence, and suppliers bundle cloud dashboards so fleets can view cell-level data remotely.[1]“Ultium Platform Overview,” General Motors, general-motors.com

Declining Lithium-ion Battery Costs and Energy-density Gains

Pack prices fell fast enough that AI chips, cloud modems and precision current sensors now fit inside mainstream EV price points. Rising energy density from 250–300 Wh/kg toward 400–500 Wh/kg compresses more heat into smaller volumes, so BMS firmware must react within sub-millisecond windows to avoid thermal runaway. CATL’s 500 Wh/kg condensed cell highlights the need for ±1% state-of-charge accuracy and real-time state-of-health prediction. Lower cell costs free capex for advanced microcontrollers, giving suppliers room to integrate on-chip neural nets that learn degradation patterns in the field.

Stringent Safety Regulations Mandating Advanced BMS

ASIL-D now sits in most RFQs, so BMS boards double up voltage and temperature channels and place hardware security modules inside master controllers. Certification pushes smaller vendors out because documentation, FMEA work and audit cycles can add 18–24 months and lift budgets 30–50%. In return, compliance becomes a pricing moat: validated suppliers win higher share of the battery management system market despite the added cost burden.

Government Incentives and Emissions Targets Accelerating EV Uptake

The U.S. Inflation Reduction Act, EU CO₂ limits and China’s NEV policy funnel long-run demand signals into OEM planning cycles. Vehicle makers lock in BMS volume agreements two to three years ahead, giving integrated-circuit vendors forward-visibility. California’s eight-year 70% capacity rule, for example, requires state-of-health tracking so owners can claim warranty remedies. Infrastructure investment that reduces range anxiety in turn raises BEV penetration, which then cycles back into bigger annual orders for battery management system market products.[2]“EV Battery Cost and Performance Trends,” U.S. Department of Energy, energy.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Shortages | -2.8% | Global, with Acute Impact in Automotive Supply Chains | Short term (≤ 2 years) |

| High Cost of ASIL-D Functional Safety | -2.1% | North America and EU primarily, Expanding Globally | Medium term (2-4 years) |

| Data-ownership Disputes | -1.5% | Global, with Concentration in Data-sensitive Regions | Medium term (2-4 years) |

| Stringent Cyber-security Certification Delaying Launches | -1.3% | North America and EU Leading, Expanding to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Semiconductor Shortages Inflating BMS IC Lead-times

Automotive-grade analog front ends and SiC gate drivers still face lead times beyond 52 weeks. Suppliers redesign boards to swap scarce dies for larger-geometry alternatives, yet those changes trigger fresh validation loops. Larger tier-ones leverage volume contracts while smaller firms queue, prompting industry consolidation. Scarcity spills into the battery management system market price stack because OEMs hold buffer stock that ties up working capital. Long-term capital expansion among foundries should ease pressure by late 2026, but uncertainty lingers around older 28 nm nodes that dominate powertrain electronics.

High Cost of ASIL-D Functional-safety Compliance

Reaching ASIL-D means exhaustive DFMEA, traceability audits and independent assessment. Programs often stretch an extra 18 months and lift spend by 30–50%. Smaller BMS specialists lack the headcount for redundant software teams and formal verification, so many either license reference designs or become acquisition targets. For those that succeed, compliance underpins premium margins and deepens customer loyalty, but development risk and certification backlog temper near-term supply in the battery management system market.[3]“ISO 26262 and ISO/SAE 21434 Implementation Guide,” International Organization for Standardization, iso.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Integrated Circuits Drive Innovation

Integrated circuits commanded 35.62% of 2025 revenue, signalling how much value has moved onto silicon. High-accuracy analog front ends, microcontrollers with AI accelerators and RF transceivers now live on the same die, trimming board area and cost. Wireless communication ICs record a 21.05% CAGR because they facilitate modular packs and slash harness weight, escalating adoption across OEMs that release multiple battery platforms per model cycle.

System-on-chip designs that fuse analog acquisition, wireless networking and cryptographic blocks enable smaller boards and faster certification. The density improvement lifts reliability, while automated calibration on the production line lowers end-of-line test time. Vendors pair these chips with firmware libraries for ISO 26262 compliance, reducing development cycles for tier-ones. In parallel, external fuel-gauge ICs integrate 24-bit ADCs that push state-of-charge error to ±1%, essential for packs moving from 250 Wh/kg toward 500 Wh/kg. As a result, component innovation remains the heartbeat of the battery management system market.

By Battery Chemistry: Lithium-ion Dominance With Solid-state Emergence

Lithium-ion held 87.35% share in 2025, underpinning almost every EV program. Its mature supply base, known ageing profile and falling cost curve keep it entrenched. Solid-state technologies, however, post a 21.18% CAGR to 2031 because they promise higher volumetric energy and intrinsic safety. Nickel-based packs survive in industrial traction where low-temperature performance matters, while lead-acid still backs 12 V auxiliaries on some platforms. Flow batteries appear mainly in stationary storage, but the modular nature of their cells invites reuse of automotive BMS logic, letting vendors repurpose designs and widen their serviceable opportunities inside the battery management system industry.

Chemistry shifts alter sensing requirements. Solid-state eliminates liquid electrolyte checks yet raises sensitivity to stack pressure and interface defects, so next-generation BMS integrates pressure and acoustic sensors. Lithium-ion modules increasingly rely on machine-learning balance algorithms that extend cycle life. Suppliers with electrochemistry know-how win design-in because they tune firmware to each cathode composition. The pivot from NMC to LFP in cost-sensitive segments also changes voltage windows, pushing boards to adopt 16-bit micro-controllers that handle wider ADC ranges without losing resolution. All told, chemistry diversity keeps the battery management system market vibrant and open to newcomers with niche expertise.

By Topology: Modular Systems Enable Scalability

Modular designs secured 42.55% of 2025 revenue because they balance cost, redundancy and ease of manufacturing. Their board-per-module approach standardizes pack construction across vehicle classes and simplifies field service. Wireless architectures, rising at 21.40% CAGR, remove most low-voltage wiring and reduce pack build times, a decisive benefit for high-throughput plants. Centralized layouts still appeal for low-energy applications such as micro-mobility, where a single board is cheapest. Distributed topologies serve buses, trucks and stationary storage that need graceful degradation if any node fails.

The shift toward modular and wireless schemes supports second-life repurposing. Decommissioned automotive modules can slot into home storage systems with minimal rework because each module carries its own controller. OEMs also leverage the same modular tooling across sedans, SUVs and vans, cutting capital expenditure. In parallel, wireless pico-gateways inside each module enable over-the-air updates that fine-tune balancing or add new chemistries after sale. As a result, topology choice shapes not just cost but long-run revenue streams, embedding value beyond hardware in the battery management system market.

By Communication Technology: Wireless RF Disrupts Traditional Protocols

Wired CAN commanded 72.20% revenue in 2025. Its deterministic timing and 1 Mbit/s rate meet legacy pack needs and plug into existing toolchains. Yet wireless RF links expand at 21.95% CAGR because they slash harnesses, allow pack form-factor flexibility and support mesh self-healing. Automotive Ethernet gains niche appeal where full-resolution cell data streams into AI loggers for advanced prognostics. Each step up the bandwidth ladder coincides with new service potential: higher rates allow voltage and impedance signatures to be pushed to the cloud for digital-twin simulations, bolstering predictive maintenance earnings inside the battery management system market.

Security now drives protocol selection. ISO 21434 pushes encryption and authentication, so vendors embed hardware root-of-trust into transceivers. 2.4 GHz mesh chips integrate AES-256 engines and random-number generators to satisfy regulation. Redundant channels mitigate interference and maintain sub-100 μs latency needed for safety trips. Transition costs slow adoption in cost-down vehicle classes, yet component prices fall as volumes ramp, paving the path for crossover models to adopt wireless by 2027.

By Propulsion Type: BEVs Lead with FCEV Growth Potential

Battery-electric vehicles accounted for 67.80% revenue in 2025 because they rely solely on packs for traction. Fuel-cell electric vehicles see 21.30% CAGR as hydrogen refuelling infrastructure rolls out for heavy-duty fleets, giving BMS suppliers entry points into small buffer packs that manage transient loads. Hybrids and plug-in hybrids continue to ship in regions where charging grids lag yet emissions norms tighten; their BMS designs differ, focusing on rapid cycling and high power pulses rather than deep energy throughput. Each propulsion class pushes unique algorithm tweaks, encouraging modular code libraries that OEMs license across platforms.

FCEV BMS tasks include tight power-sharing with fuel-cell controllers and frequent rapid charging from regenerative braking. Safety demands remain high even though pack energy is lower because hydrogen systems must avoid thermal cross-talk. Vendors that can tailor architectures without expensive hardware redesign unlocking faster FCEV launches will grow their footprint within the battery management system market.

By Vehicle Type: Passenger Cars Dominate with Micro-mobility Acceleration

Passenger cars delivered 61.45% share in 2025, reflecting broad consumer subsidies and model variety. Two-wheelers and micro-mobility vehicles log a 21.70% CAGR through 2031, pushed by urban congestion policies and the rise of battery-swap networks. Their packs are smaller but manufactured by the millions, so cost-optimized BMS single-chip solutions with Bluetooth interfaces are winning designs. Light commercial vans see steady orders as e-commerce insists on zero-emission last-mile fulfillment, raising the battery management system market size in duty-cycle-intensive segments.

Fleet operators ask for predictive analytics that guarantee eight-year pack life or 200,000 km service; BMS dashboards now integrate fleet management APIs. At the other end, heavy trucks and construction equipment order ruggedized boards that withstand vibration and higher ambient heat. Specialist niches such as mining vehicles seek intrinsically safe designs, while agricultural OEMs want cold-temperature resilience. These diversifying requirements fuel continuous innovation across the battery management system industry.

By Sales Channel: OEM Integration with Aftermarket Growth

OEM-installed solutions formed 84.60% of 2025 revenue as automakers bundle BMS boards during pack assembly to secure warranty integrity. Retrofits and aftermarket kits rise at 21.80% CAGR because owners look to upgrade early-generation EVs with new packs or extend range. Commercial fleets often swap degrading modules before a full vehicle refit, creating pull for drop-in BMS boards that learn existing cell chemistry without factory calibration. Second-life energy-storage integrators install stationary systems based on retired automotive packs, demanding BMS software that handles shallower depth of discharge and different thermal duty cycles.

Standardized connectors and auto-identification now allow plug-and-play swap boards, cutting installation time to under one hour. Regulatory inspection regimes, however, still favour OEM parts, so retrofit suppliers partner with certified workshops. The sales-channel mix therefore broadens but OEM dominance endures, reinforcing the high-volume base of the battery management system market.

Geography Analysis

Asia-Pacific retained 47.10% revenue in 2025. China’s cell giants CATL and BYD jointly shipped more than half of global batteries, anchoring a supply chain that extends from raw lithium processing to finished BMS assembly. Japan and South Korea supply precision semiconductors and software tools, while India hosts more than 60 local BMS firms that tailor boards to indigenous two-wheeler brands. Government funding through production-linked incentives and solid-state pilot lines keeps the battery management system market expanding at scale even as EV adoption in the region matures.

The Middle East and Africa post 21.25% CAGR, the fastest worldwide, because countries leapfrog traditional engine platforms. Ghana and Morocco promote two-wheeler electrification tied to solar micro-grids, spurring demand for affordable BMS single-board products. African start-ups collaborate with Asian IC vendors to design humidity-tolerant boards that handle rough roads and high ambient heat. Agency support lowers import duties on cell imports, so assemblers can focus capital on electronics that differentiate reliability. North America benefits from the Inflation Reduction Act, which links tax credits to local BMS content and cell sourcing. Chip-maker expansion in the United States pulls high-value analog front-end production closer to OEM plants, mitigating future supply shocks. Canada’s mining sector positions itself as a low-carbon nickel supplier, and Mexico’s assembly clusters attract tier-ones building pack lines with embedded wireless BMS. Europe concentrates on battery passports that require end-to-end traceability from 2026, pushing cloud-connected boards that stream life-cycle data into blockchain registries. Both regions grow steadily, yet Asia-Pacific scale advantages preserve its lead in the battery management system market.

Competitive Landscape

The market shows moderate concentration. Top semiconductor suppliers Texas Instruments, Infineon Technologies and Analog Devices dominate analog front ends and micro-controllers; battery makers CATL, LG Energy Solution and BYD increasingly design in-house BMS to align cell chemistries with control logic. Infineon’s USD 2.5 billion purchase of Marvell’s automotive Ethernet unit deepens its stack by adding high-bandwidth networking IP to MCU and power modules, positioning it as a one-stop platform supplier. LG Energy Solution’s B.around software achieves above 90% anomaly-detection accuracy using AI, converting hardware installations into subscription revenue.

Roughly 325 start-ups target specialization such as pressure sensing for solid-state packs, sub-10 USD micro-mobility boards or cloud analytics for fleet optimization. Yet ASIL-D certification cost and silicon shortages spur consolidation; smaller firms license IP or exit. Tier-ones form alliances: Stellantis and Infineon’s Joint Power Lab builds standardized power architecture that folds BMS requirements into the wider vehicle domain controller.

Meanwhile, vehicle OEMs like General Motors prefer wireless topologies for platform reuse, granting early suppliers high-volume purchase orders that lock in design wins across multiple model years. Competitive differentiation thus rotates around integration depth, safety pedigree and data-service potential within the battery management system market.

Electric Vehicle Battery Management System Industry Leaders

Renesas Electronics Corporation

NXP Semiconductors

Analog Devices Inc.

Texas Instruments

Infineon Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Infineon Technologies completed acquisition of Marvell Technology’s Automotive Ethernet business for USD 2.5 billion, combining micro-controller leadership with high-bandwidth networking.

- January 2025: FORVIA HELLA selected Infineon CoolSiC Automotive MOSFET 1200 V for next-generation 800 V DC-DC chargers, improving thermal performance and cost for high-voltage BMS.

- November 2024: Infineon Technologies and Stellantis opened Joint Power Lab to co-develop scalable EV power modules and intelligent distribution that streamline BMS integration.

- September 2024: LG Energy Solution launched B.around, an AI-driven battery management service delivering more than 90% safety-event detection accuracy to automakers.

Global Electric Vehicle Battery Management System Market Report Scope

An electric vehicle battery management system (BMS) is a system that monitors and controls the performance of the battery pack in an electric vehicle. The BMS helps to ensure the safety, longevity, and optimal performance of the battery by regulating charging and discharging, balancing cell voltages, and providing temperature control.

The Electric Vehicle Battery Management System Market is Segmented by Component (Integrated Circuits, Cutoff FETs and FET Driver, Temperature Sensor, Fuel Gauge/Current Measurement Devices, Microcontroller, and Other Components), Propulsion Type (Battery Electric Vehicles and Hybrid Electric Vehicles), Vehicle Type (Passenger Cars and Commercial Vehicles), and Geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The report offers market size and forecasts for the Electric Vehicle Battery Management System Market in value (USD million) for all the above segments.

By Component

| Integrated Circuits |

| Cut-off FETs and Drivers |

| Temperature Sensors |

| Fuel-Gauge/Current-Measurement Devices |

| Microcontrollers |

| Communication Interface ICs |

| Other Components |

By Battery Chemistry

| Lithium-ion |

| Solid-state |

| Nickel-based |

| Lead-acid |

| Flow Batteries |

By Topology

| Centralized |

| Modular |

| Distributed |

| Wireless (Cable-less) |

By Communication Technology

| Wired CAN |

| Wired Ethernet |

| Wireless RF |

By Propulsion Type

| Battery Electric Vehicles (BEV) |

| Hybrid Electric Vehicles (HEV) |

| Plug-in Hybrid Vehicles (PHEV) |

| Fuel-Cell Electric Vehicles (FCEV) |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Two-Wheelers and Micro-mobility |

| Off-highway and Specialty Vehicles |

By Sales Channel

| OEM-fitted |

| Aftermarket/Retrofit |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Integrated Circuits | |

| Cut-off FETs and Drivers | ||

| Temperature Sensors | ||

| Fuel-Gauge/Current-Measurement Devices | ||

| Microcontrollers | ||

| Communication Interface ICs | ||

| Other Components | ||

| By Battery Chemistry | Lithium-ion | |

| Solid-state | ||

| Nickel-based | ||

| Lead-acid | ||

| Flow Batteries | ||

| By Topology | Centralized | |

| Modular | ||

| Distributed | ||

| Wireless (Cable-less) | ||

| By Communication Technology | Wired CAN | |

| Wired Ethernet | ||

| Wireless RF | ||

| By Propulsion Type | Battery Electric Vehicles (BEV) | |

| Hybrid Electric Vehicles (HEV) | ||

| Plug-in Hybrid Vehicles (PHEV) | ||

| Fuel-Cell Electric Vehicles (FCEV) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Two-Wheelers and Micro-mobility | ||

| Off-highway and Specialty Vehicles | ||

| By Sales Channel | OEM-fitted | |

| Aftermarket/Retrofit | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the battery management system market?

The market reached USD 19.51 billion in 2026 and is projected to rise to USD 49.83 billion by 2031 at 20.63% CAGR.

Which component segment leads the battery management system market?

Integrated circuits led with 35.62% revenue share in 2025, reflecting their central role in cell monitoring and control.

Why are wireless BMS architectures important?

Wireless designs eliminate up to 90% of wiring, cut pack assembly time and enable over-the-air updates, driving a 21.40% CAGR to 2031.

Which region is the fastest-growing for battery management systems?

The Middle East and Africa record the highest 21.25% CAGR because of aggressive electrification policies and green-energy investments.

How do safety regulations influence BMS design?

Standards such as UN ECE R100-Rev3 and ISO/SAE 21434 require ASIL-D functional safety and cybersecurity, leading to redundant sensing and encrypted communications.

What is driving aftermarket demand for BMS solutions?

Owners and fleets seek to upgrade early EVs, extend vehicle life and repurpose retired packs for stationary storage, resulting in a 21.80% CAGR for retrofit systems.

Page last updated on: