Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

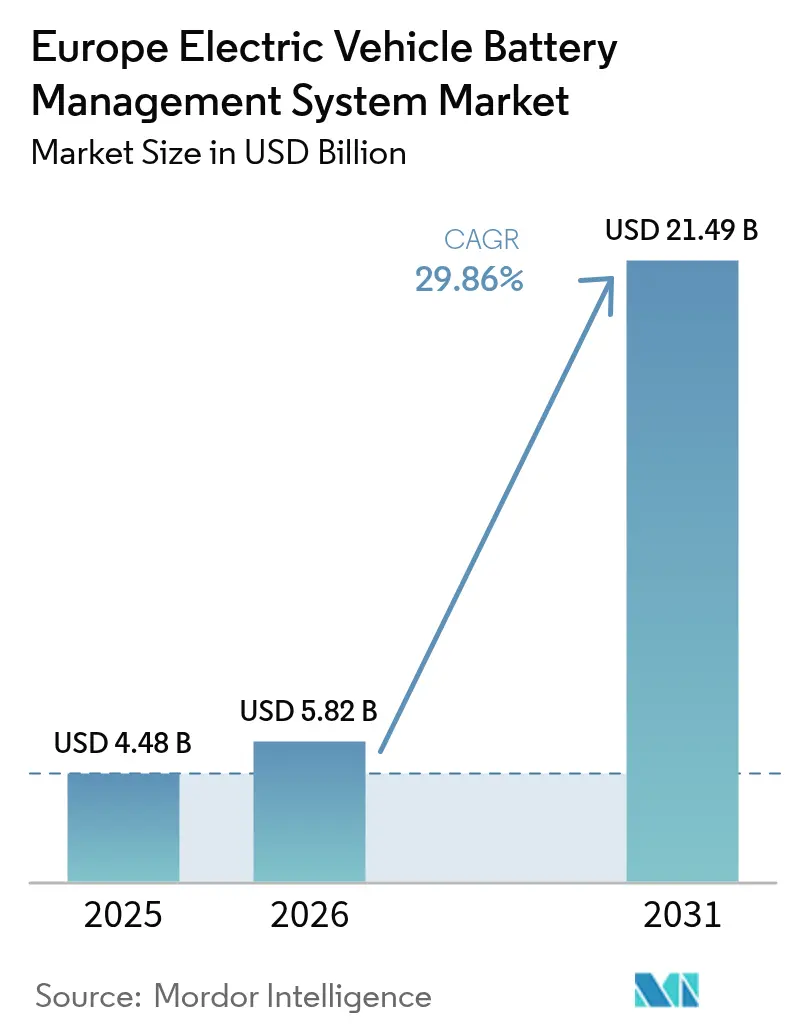

| Base Year Market Size (2025) | USD 4.48 Billion |

| Market Size (2026) | USD 5.82 Billion |

| Market Size (2031) | USD 21.49 Billion |

| Growth Rate (2026 - 2031) | 29.86% CAGR |

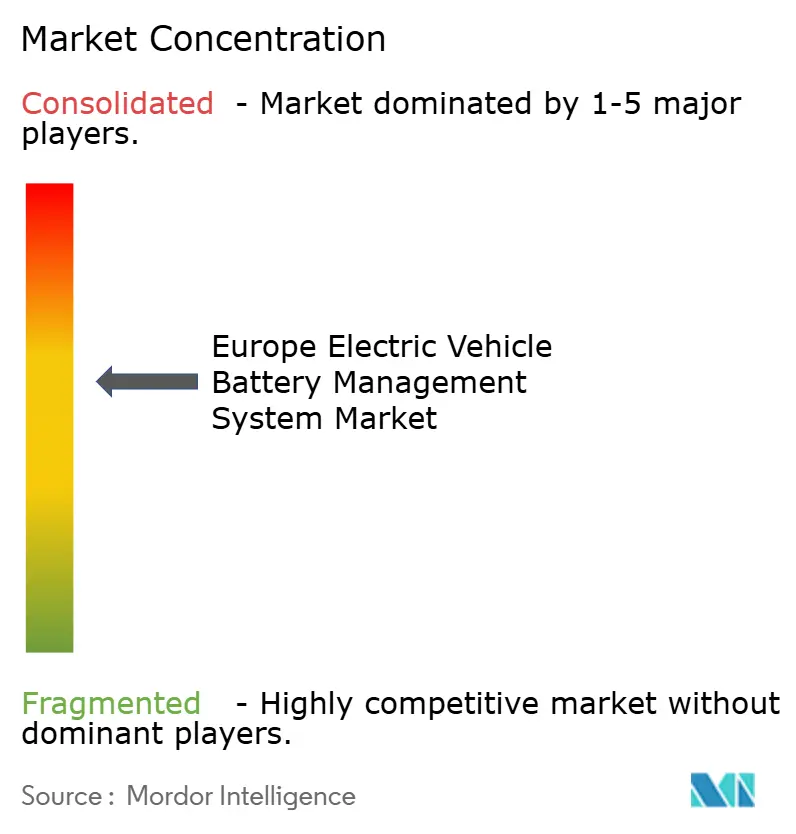

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Electric Vehicle Battery Management System Market Analysis by Mordor Intelligence

The Europe Electric Vehicle Battery Management System market size was valued at USD 4.48 billion in 2025 and estimated to grow from USD 5.82 billion in 2026 to reach USD 21.49 billion by 2031, at a CAGR of 29.86% during the forecast period (2026-2031). This expansion reflects forceful EU CO₂ fleet-emission limits that require all new passenger vehicles to be zero-emission by 2035, the premium segment’s brisk conversion to 800 V electrical platforms, and vigorous gigafactory construction across Central Europe. Demand also benefits from insurance-led battery-traceability rules and early battery-passport pilots that push OEMs to install more capable, cyber-secure battery management software. Added momentum comes from modular battery-pack architectures that lessen design cost and speed the rollout of multi-brand electric platforms. Pressures remain in semiconductor availability and high-voltage certification queues, yet most OEMs prioritize BMS investments to avoid heavy CO₂ penalties and recall costs tied to thermal runaway incidents.

Key Report Takeaways

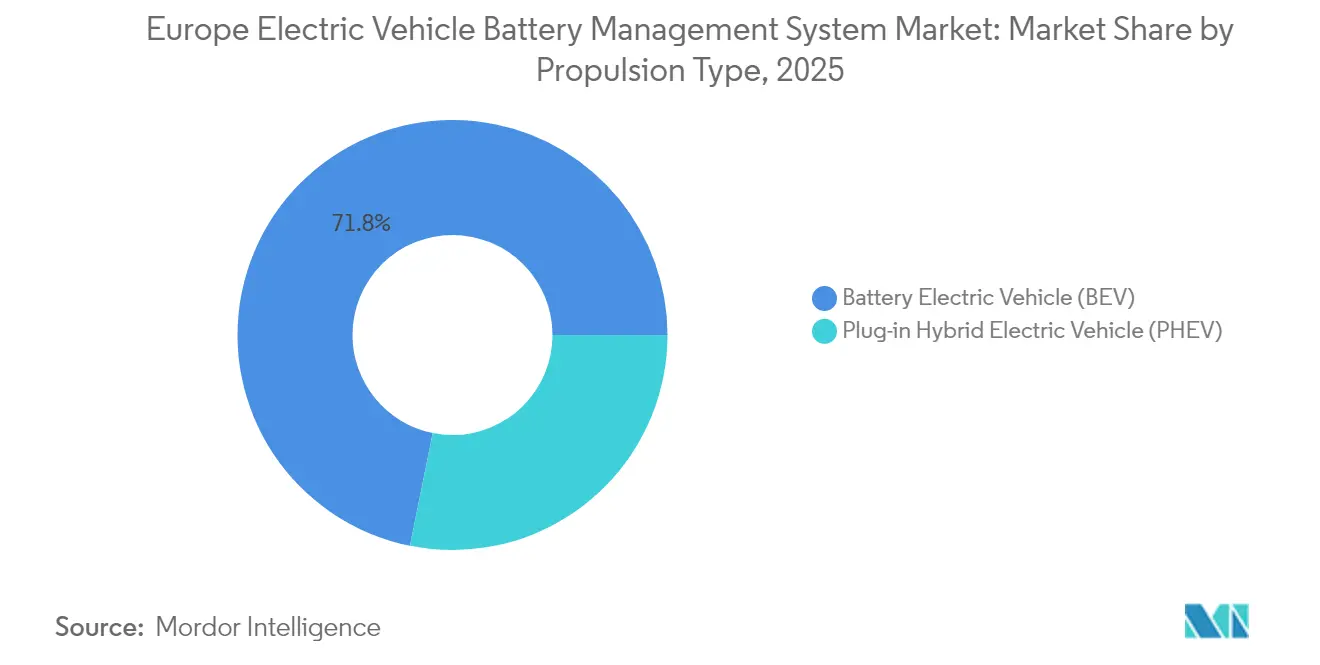

- By propulsion type, Battery Electric Vehicles led with 71.83% revenue share of the European electric Vehicle Battery Management System market in 2025 while posting a 31.10% CAGR through 2031.

- By vehicle type, passenger cars held 67.12% of the European electric Vehicle Battery Management System market demand in 2025; two-wheeler and micro-mobility solutions record the strongest 31.25% CAGR to 2031.

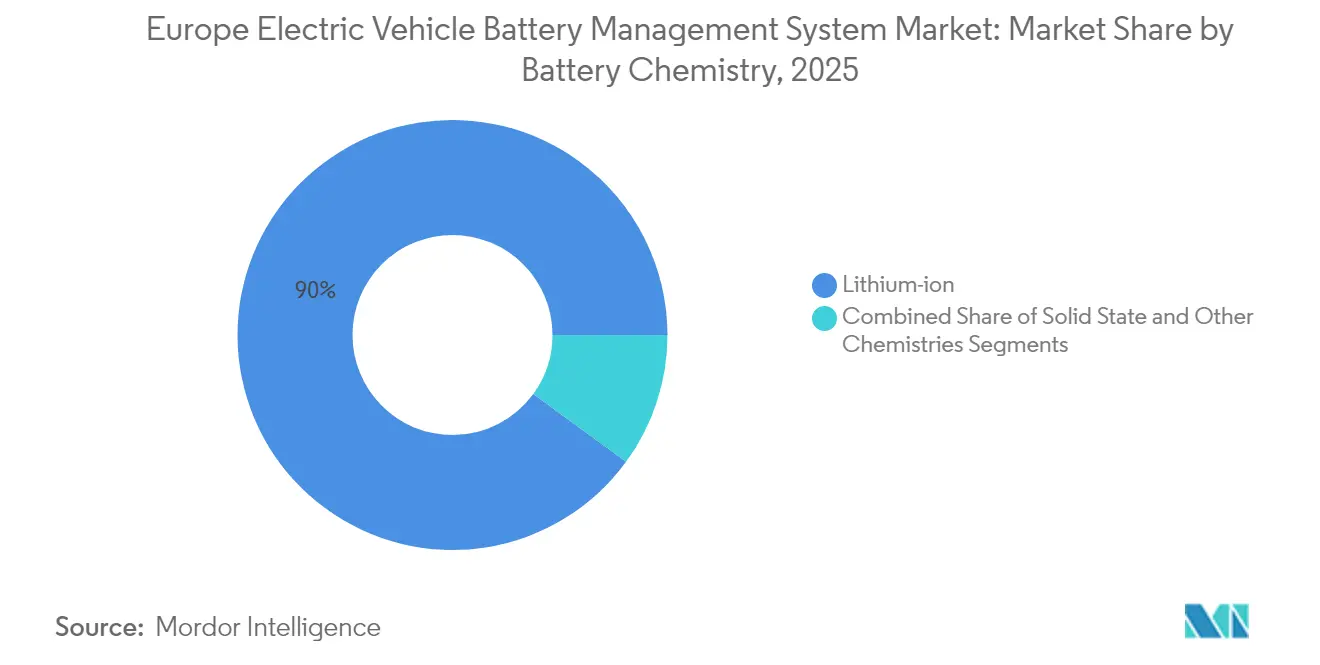

- By battery chemistry, lithium-ion commanded a 89.96% share of the Europe Electric Vehicle Battery Management System market size in 2025, whereas solid-state technology is projected to grow at 41.05% CAGR by 2031.

- By topology, modular systems captured 44.52% share of the European electric Vehicle Battery Management System market revenue in 2025 and remain the fastest segment, expanding at 31.02% CAGR.

- By country, the rest of Europe contributed a 37.10% share in the European electric Vehicle Battery Management System market revenue in 2025; Spain is the fastest-growing national market, accelerating at 33.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Electric Vehicle Battery Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-Only CO₂-Fleet Rules for 2035 | +8.5% | EU-wide, strongest in Germany, France | Long term (≥ 4 years) |

| Rapid OEM Shift to 800-V Architectures | +6.2% | Germany, Sweden, premium segments | Medium term (2–4 years) |

| Surging Gigafactory Build-Out in Central Europe | +5.8% | Slovakia, Czech Republic, Hungary, Poland | Medium term (2–4 years) |

| Cyber-Secure Over-the-Air (OTA) BMS Updates | +4.3% | Global, led by Germany and Nordic countries | Medium term (2–4 years) |

| Insurance-Mandated Battery Traceability Platforms | +3.1% | EU-wide, early adoption in Netherlands, Germany | Short term (≤ 2 years) |

| EU Battery Passport Pilots (Under CSRD) | +2.9% | EU-wide, pilot programs in Germany, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-only CO₂-fleet Rules for 2035

The European Union's mandate requiring 100% zero-emission vehicle sales by 2035 creates an irreversible demand catalyst for sophisticated BMS solutions, as automakers face EUR 95 per gram penalties for exceeding CO₂ thresholds[1]"Powering the EU's future: Strengthening the battery industry", European Parliament, europarl.europa.eu.. This regulatory framework forces manufacturers to accelerate BEV production beyond the current 13.5% market penetration, requiring a 14% annual growth rate that necessitates advanced battery management capabilities for larger pack sizes and higher energy densities. The regulation's secondary effect drives insurance companies to mandate comprehensive battery monitoring systems, creating additional revenue streams for BMS providers who can demonstrate predictive failure detection and warranty cost reduction. Premium automakers are responding by investing heavily in 800V architectures that require more sophisticated thermal management and cell balancing algorithms, directly benefiting BMS suppliers with advanced power electronics expertise. The compliance timeline creates a supply chain bottleneck where BMS certification becomes the critical path item, giving established players with ISO 26262 functional safety credentials significant competitive advantages over new entrants.

Rapid OEM Shift to 800-V Architectures

The automotive industry's migration to 800V electrical architectures represents a fundamental shift that demands entirely new BMS designs capable of managing higher voltage differentials and more complex thermal dynamics. BMW's partnership with Rimac Technology for next-generation battery packs and Volvo's collaboration with Vitesco Technologies demonstrate how premium manufacturers prioritize fast-charging capabilities requiring sophisticated voltage monitoring and cell balancing algorithms. This architectural transition creates significant barriers to entry for BMS suppliers lacking high-voltage expertise, as certification requirements under ISO 26262 become exponentially more complex at 800V operating levels. The shift enables 10-minute charging sessions for 200-mile range, but places extreme thermal stress on battery cells that traditional BMS designs cannot adequately manage, forcing suppliers to integrate advanced cooling algorithms and predictive thermal modeling. European automakers are leveraging this transition to differentiate from Chinese competitors who predominantly use 400V systems, creating a temporary technological moat that benefits local BMS suppliers with advanced power electronics capabilities.

Surging Gigafactory Build-out in Central Europe

Central Europe's emergence as a battery manufacturing hub creates concentrated demand for BMS solutions, with Slovakia hosting InoBat's partnership with Gotion, the Czech Republic expanding Vitesco Technologies' production, and Hungary attracting Samsung SDI and FORVIA-BYD investments. This geographic concentration enables BMS suppliers to achieve economies of scale through localized engineering support and shortened supply chains, benefiting from skilled automotive workforces and competitive labor costs. The region's strategic positioning between German automotive OEMs and emerging Eastern European markets creates natural logistics advantages for BMS distribution, particularly as manufacturers seek to reduce dependency on Asian suppliers following recent supply chain disruptions. Slovakia's battery production capacity alone is projected to exceed 40 GWh annually by 2027, requiring sophisticated BMS solutions for quality control and production line integration that traditional battery management approaches cannot address. The clustering effect accelerates technology transfer and innovation, as BMS suppliers establish regional R&D centers to serve multiple gigafactory customers simultaneously, creating sustainable competitive advantages through proximity and specialization.

Cyber-secure Over-the-air (OTA) BMS Updates

Integrating OTA update capabilities into BMS architecture represents a paradigm shift toward software-defined battery management, enabling manufacturers to optimize performance and address safety issues without physical recalls. HARMAN's development of ISO 24089-compliant OTA solutions demonstrates how cybersecurity requirements are becoming integral to BMS design, as connected vehicles create new attack vectors that could compromise battery safety systems. This capability becomes critical as thermal runaway incidents like those affecting Mercedes EQB and BMW Mini Cooper SE models could be mitigated through remote parameter adjustments and enhanced monitoring algorithms. LG Energy Solution's launch of the "B.around" battery management platform exemplifies how suppliers are monetizing OTA capabilities through subscription-based diagnostic services and predictive maintenance offerings[2]"LG Energy Solution to Pioneer Battery Safety Diagnostics Software Business, Exploring Unlimited Business Extension Opportunities", LG Energy Solution, lgensol.com. . The technology enables real-time charging profile optimization based on usage patterns and environmental conditions, extending battery life and improving vehicle performance in ways that static BMS configurations cannot achieve. European automakers are particularly focused on OTA security given GDPR compliance requirements and heightened cybersecurity awareness, creating opportunities for BMS suppliers who can demonstrate robust encryption and secure communication protocols.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Supply-Chain Squeezes | -4.7% | Global, acute in Germany automotive sector | Short term (≤ 2 years) |

| High-Voltage BMS Certification Bottlenecks | -3.2% | EU-wide, regulatory approval delays | Medium term (2–4 years) |

| Thermal-Runaway Recalls Hurting Consumer Trust | -2.8% | EU-wide, brand-specific impacts | Short term (≤ 2 years) |

| Scarcity of Functional-Safety Engineers | -2.1% | Germany, Nordic countries, skill shortage | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply-chain Squeezes

The global semiconductor shortage continues to constrain BMS production capacity, with automotive-grade chips experiencing lead times exceeding 26 weeks and creating cascading delays across European EV manufacturing schedules. This constraint particularly impacts advanced BMS designs that require specialized power management ICs and microcontrollers capable of handling 800V architecture and complex thermal algorithms. European BMS suppliers face additional pressure as they compete with consumer electronics manufacturers for limited chip allocation, often losing priority due to lower volume commitments than smartphone and computing applications. The shortage forces manufacturers to redesign BMS architecture around available components, potentially compromising performance optimization and extending development cycles by 12-18 months. Supply chain resilience becomes a critical competitive factor, with companies maintaining strategic inventory buffers and developing alternative sourcing relationships to ensure production continuity. The constraint creates opportunities for European semiconductor manufacturers to capture market share from Asian suppliers. Still, it requires significant capital investment and 2-3 year development timelines that may not address immediate supply needs.

High-voltage BMS Certification Bottlenecks

The transition to 800V architecture creates unprecedented certification challenges under ISO 26262 functional safety standards, as testing requirements become exponentially more complex at higher voltage levels and regulatory bodies lack sufficient capacity to process applications efficiently. European certification authorities are experiencing 6-12-month backlogs for high-voltage BMS approvals, creating critical path delays for automakers racing to meet 2025 CO₂ compliance deadlines. The bottleneck particularly affects smaller BMS suppliers who lack the resources to maintain dedicated regulatory affairs teams and navigate complex multi-jurisdictional approval processes across EU member states. Testing infrastructure limitations compound the problem, as specialized high voltage testing facilities operate at capacity and require month-long booking schedules for comprehensive safety validation. This constraint favors established players like Continental AG and Robert Bosch GmbH who have existing certification relationships and can leverage economies of scale across multiple product lines, potentially consolidating market share away from innovative startups with superior technology but limited regulatory experience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: BEVs Dominate Growth Trajectory

Battery Electric Vehicles command a 71.83% market share in 2025 and lead growth projections at 31.10% CAGR through 2031, reflecting the market's decisive shift toward pure electric powertrains as automakers abandon hybrid strategies in favor of platform simplification. The BEV segment's dominance stems from regulatory pressure under EU CO₂ fleet rules and consumer preference for simplified ownership experiences without range anxiety associated with plug-in hybrid complexity. Plug-in Hybrid Electric Vehicles (PHEVs) maintain relevance in commercial applications where operational flexibility remains critical. Still, face declining investment as manufacturers reallocate R&D resources toward BEV platforms that offer superior economies of scale. The segment dynamics reveal a critical inflection point where BMS requirements diverge significantly between propulsion types, with BEVs demanding sophisticated thermal management for larger battery packs. At the same time, PHEVs require complex power arbitration algorithms for dual-powertrain coordination.

Advanced BMS architectures for BEVs increasingly incorporate machine learning algorithms for predictive thermal modeling. LG Energy Solution's B.around platform analyzes data from over 130,000 battery cells to optimize charging profiles and extend pack life. This technological sophistication creates barriers to entry for traditional automotive suppliers lacking software expertise, enabling new entrants like Munich Electrification to capture market share through specialized BMS solutions for energy storage systems up to 1500V. The propulsion type segmentation increasingly reflects broader industry consolidation around BEV platforms, with implications for BMS suppliers who must choose between serving declining PHEV markets or investing heavily in next-generation BEV technologies.

By Vehicle Type: Commercial Fleets Drive Innovation

Passenger cars represent 67.12% of vehicle type demand in 2025. Still, the two-wheeler and micro-mobility segment exhibits a remarkable 31.25% CAGR growth through 2031, driven by urban logistics transformation and shared mobility platform expansion across European cities. Commercial vehicles occupy a strategic middle ground where BMS requirements emphasize durability and predictive maintenance over performance optimization, creating opportunities for suppliers who can demonstrate total cost of ownership advantages. The micro-mobility surge reflects fundamental changes in urban transportation patterns, where lightweight BMS designs must balance cost constraints with safety requirements for shared vehicle applications that experience intensive usage cycles and varied environmental conditions.

Fleet operators increasingly demand sophisticated battery analytics for predictive maintenance and operational optimization, driving the adoption of cloud-connected BMS solutions that aggregate performance data across vehicle populations and identify emerging failure patterns before they impact service availability. Daimler Truck's partnership with BMZ Poland for battery systems exemplifies how commercial vehicle manufacturers prioritize BMS suppliers who can provide comprehensive lifecycle management rather than standalone hardware solutions. The vehicle type segmentation reveals diverging technology requirements, where passenger car BMS focuses on performance and user experience while commercial vehicle systems emphasize reliability and cost efficiency. At the same time, micro-mobility applications demand ultra-compact designs with wireless connectivity for fleet management integration.

By Battery Chemistry: Solid-state Emergence Reshapes Landscape

Lithium-ion technology maintains an overwhelming 89.96% market dominance in 2025. Still, solid-state batteries command attention with a projected 41.05% CAGR growth through 2031, as Mercedes-Benz targets 2030 commercialization and Samsung SDI prepares for 2027 mass production capabilities. The chemistry landscape reflects a fundamental transition where traditional liquid electrolyte systems face inherent thermal management challenges that solid-state technology can potentially eliminate, requiring entirely new BMS architectures optimized for different failure modes and charging characteristics. Other battery chemistries serve specialized applications where cost optimization outweighs energy density requirements, particularly in commercial vehicle segments where operational economics drive technology selection over performance metrics.

Stellantis's demonstration fleet targeting 2026 deployment and PowerCo's landmark agreement with QuantumScape for 40 GWh annual production capacity demonstrate solid-state technology transitioning from laboratory curiosity to commercial reality. The chemistry segmentation creates strategic challenges for BMS suppliers who must simultaneously support existing lithium-ion deployments while developing next-generation capabilities for solid-state systems that operate under fundamentally different thermal and electrical characteristics. European manufacturers are leveraging this transition to establish technological differentiation from Chinese competitors who dominate traditional lithium-ion production, creating opportunities for specialized BMS suppliers who can navigate the complexity of multi-chemistry platform support.

By Topology: Modular Architecture Gains Momentum

Modular topology captured a 44.52% market share in 2025. It leads growth projections at 31.02% CAGR through 2031, reflecting automakers' preference for scalable architectures that enable cost-effective platform sharing across vehicle segments and simplified manufacturing processes. This topology advantage becomes critical as manufacturers like Hyundai implement Integrated Modular Architecture (IMA) and General Motors scales its Ultium platform across multiple brands, requiring BMS designs that can adapt to varying pack configurations without extensive re-engineering. Centralized systems maintain relevance in cost-sensitive applications where simplicity outweighs flexibility, while distributed architectures serve specialized requirements where individual cell monitoring provides safety advantages despite increased complexity and cost.

The modular approach enables manufacturers to optimize BMS functionality for specific applications while maintaining common hardware platforms, reducing development costs, and accelerating time-to-market for new vehicle variants. Tesla's continued use of centralized architecture demonstrates how topology selection reflects broader strategic choices about vertical integration and manufacturing philosophy. The topology segmentation increasingly reflects industry consolidation around modular platforms that can accommodate future technology transitions, including solid-state batteries and advanced thermal management systems, creating competitive advantages for BMS suppliers who can demonstrate architectural flexibility and scalability across multiple vehicle programs.

Geography Analysis

The rest of Europe captured 37.10% of the 2025 market value through a blend of mature German demand, Nordic cold-weather BMS specialties, and emerging Central European gigafactories. Spain leads growth at 33.95% CAGR, buoyed by Stellantis-CATL’s EUR 4.1 billion Valencia cell plant that embeds local BMS validation lines. Proximity to abundant solar power pools offers energy-cost advantages and strengthens the regional case for battery passport compliance from day one.

Germany retains the single-largest national revenue pool, supported by dense Tier 1 clustering and a deep bench of functional safety engineers. Yet labor-cost differentials accelerate capacity migration eastward, prompting Berlin to boost funding for high-voltage test infrastructure and silicon carbide power-semiconductor fabs. Nordic nations provide crucible conditions for extreme-temperature algorithms; Finnish winter trials help refine low-SoC heater control, then feed software updates back to southern fleets over the air.

France centers on circular-economy legislation that incentivizes second-life stationary storage, thus demanding BMS platforms able to grade used packs and report residual capacity. The United Kingdom navigates customs complexity post-Brexit; suppliers must certify under dual regimes while maintaining components traceable for EU battery passports. Italy’s Lombardy region, newly backed by Green Deal Industrial Plan allocations, emerges as a base for aluminum busbar machining, linking BMS providers to low-inductance conductor modules. Netherlands and Belgium differentiate through charging-network density, spurring demand for vehicle-to-grid capable firmware that schedules discharge when peak wholesale rates prevail.

Competitive Landscape

In 2024, Asian vendors are making notable inroads, intensifying the competition. European incumbents, including Bosch and Continental, are countering this trend. By bundling hardware, software, and certification services, they secure lucrative contracts and fortify their margins against the onslaught of low-cost imports. Globally, just seven suppliers have achieved the prestigious Tier One status from Benchmark Mineral Intelligence. Alarmingly, none of these are based in continental Europe, underscoring a pressing need for localized operations.

Scale advantages favor integrated cell-plus-BMS offerings from CATL Europe and BYD Europe, yet European OEMs seek dual sourcing to hedge geopolitical risk. Munich Electrification and TWAICE pursue differentiation through physics-based aging models and cloud analytics; landing design wins with premium brands eager for battery lifecycle insights. Software-first firms like Breathe Battery Technologies win traction on the promise of 20% faster charge speeds without cell redesign. This highlights a pivot toward recurring SaaS revenues inside the European electric Vehicle Battery Management System market.

Strategic moves reinforce this trend. Porsche acquired a controlling stake in VARTA’s V4Drive to lock in high-power cylindrical cells and co-develop matching BMS stacks. LG Energy Solution launched the “B.around” platform, bundling safety diagnostics and predictive maintenance as subscriptions. Meanwhile, QuantumScape aligned with Volkswagen’s PowerCo to secure 40 GWh of solid-state capacity paired with bespoke pressure-sensor BMS firmware. These actions underline a shift from commodity controllers toward data-rich energy-management ecosystems.

Europe Electric Vehicle Battery Management System Industry Leaders

-

Denso Corporation

-

Robert Bosch GmbH

-

Panasonic Corporation

-

LG Energy Solution

-

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: LG Energy Solution unveiled its next-gen grid-scale LFP ESS products with 15,000 cycle lifespans and pilot compliance with the Battery Passport. This highlights LG's commitment to European market leadership and adherence to EU battery traceability and sustainability regulations.

- April 2025: Nyobolt raised USD 30 million to scale its high-power battery technology, enabling 5-minute EV charging. The company reported USD 9 million in revenue, reflecting strong market traction. The investment highlights rising demand for advanced BMS capabilities to manage extreme charging rates while preserving battery life.

Europe Electric Vehicle Battery Management System Market Report Scope

An electric vehicle battery management system (BMS) is a crucial component that monitors and controls the performance of the battery pack in an electric vehicle. It ensures the optimal charging, discharging, and overall health of the battery, enhancing the safety, efficiency, and longevity of the electric vehicle's energy storage system.

The Europe electric vehicle battery management system market is segmented by propulsion type (plug-in hybrid electric vehicle and battery electric vehicle), vehicle type (passenger car and commercial vehicle), and country (Germany, United Kingdom, France, Norway, and the rest of Europe).

The report offers market size and forecasts for the Europe electric vehicle battery management system for all the above segments in value (USD).

By Propulsion Type

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Battery Electric Vehicle (BEV) |

By Vehicle Type

| Passenger Cars |

| Commercial Vehicles |

| Two-Wheeler and Micro-mobility |

By Battery Chemistry

| Lithium-ion |

| Solid-state (pre-commercial) |

| Other Chemistries |

By Topology

| Centralized |

| Distributed |

| Modular |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Norway |

| Netherlands |

| Sweden |

| Rest of Europe |

| By Propulsion Type | Plug-in Hybrid Electric Vehicle (PHEV) |

| Battery Electric Vehicle (BEV) | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| Two-Wheeler and Micro-mobility | |

| By Battery Chemistry | Lithium-ion |

| Solid-state (pre-commercial) | |

| Other Chemistries | |

| By Topology | Centralized |

| Distributed | |

| Modular | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Norway | |

| Netherlands | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the Europe Electric Vehicle Battery Management System market?

The Europe Electric Vehicle Battery Management System market will be USD 5.82 billion in 2026 and grow to USD 21.49 billion by 2031, recording a 29.86% CAGR.

Which propulsion type dominates demand?

Battery Electric Vehicles account for 71.83% revenue share in 2025 and are the fastest-growing propulsion segment at 31.10% CAGR.

Which country shows the highest growth rate?

Spain is the fastest-expanding national market with a 33.95% CAGR through 2031 due to large-scale cell-plant investments.

How do semiconductor shortages affect the market?

High-voltage BMS production faces delays due to chip lead times consistently exceeding 26 weeks, causing a noteworthy revision in the forecast CAGR.

Page last updated on: