Electric Vehicle Communication Controller Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

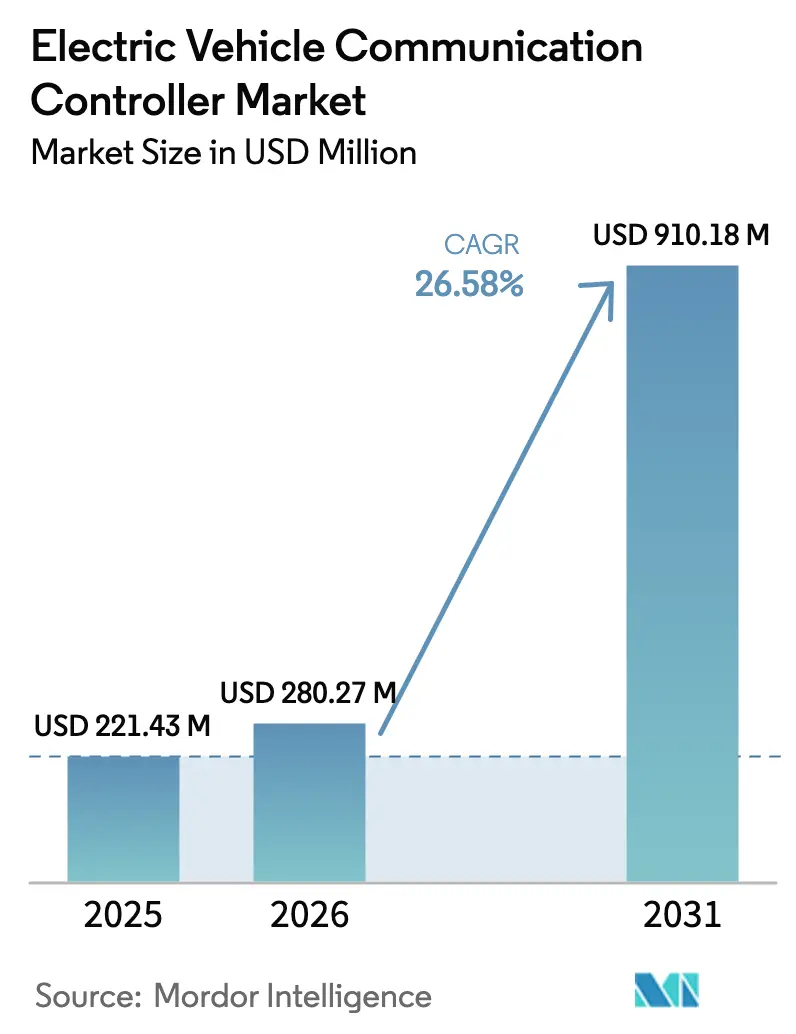

| Market Size (2026) | USD 280.27 Million |

| Market Size (2031) | USD 910.18 Million |

| Growth Rate (2026 - 2031) | 26.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle Communication Controller Market Analysis by Mordor Intelligence

The electric vehicle communication controller market size was valued at USD 221.43 million in 2025 and estimated to grow from USD 280.27 million in 2026 to reach USD 910.18 million by 2031, at a CAGR of 26.58% during the forecast period (2026-2031). Strong demand stems from the rapid worldwide shift toward battery-powered mobility, government mandates for standardized plug-and-charge protocols, and the migration of vehicle networks to high-bandwidth Ethernet backbones. Together, these forces elevate the communication controller from a basic interface to the orchestration hub for charging, power-flow, and data-exchange functions that underpin software-defined vehicles. Corporations with deep semiconductor know-how are moving aggressively into this systems space while traditional Tier 1 suppliers race to embed secure firmware and energy-management algorithms into their controller lines. Standardization battles between Tesla’s North American Charging Standard (NACS) and legacy Combined Charging System (CCS) solutions add transitional complexity yet ultimately accelerate volume growth as harmonized designs reduce per-unit costs and facilitate global rollouts.

Key Report Takeways

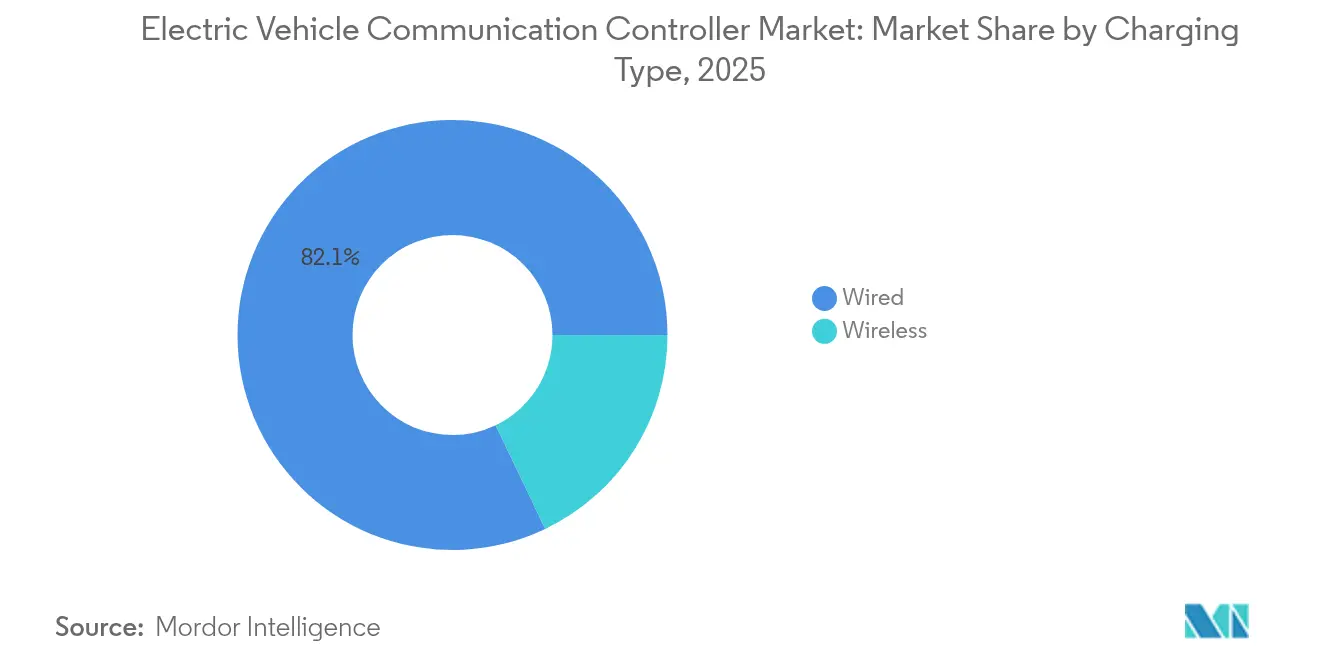

- By charging type, wired systems led with 82.10% of electric vehicle communication controller market share in 2025; wireless solutions are on track for a 31.62% CAGR through 2031.

- By EV type, battery electric vehicles commanded 61.55% of the electric vehicle communication controller market share in 2025, while plug-in hybrids are advancing at 29.58% CAGR to 2031.

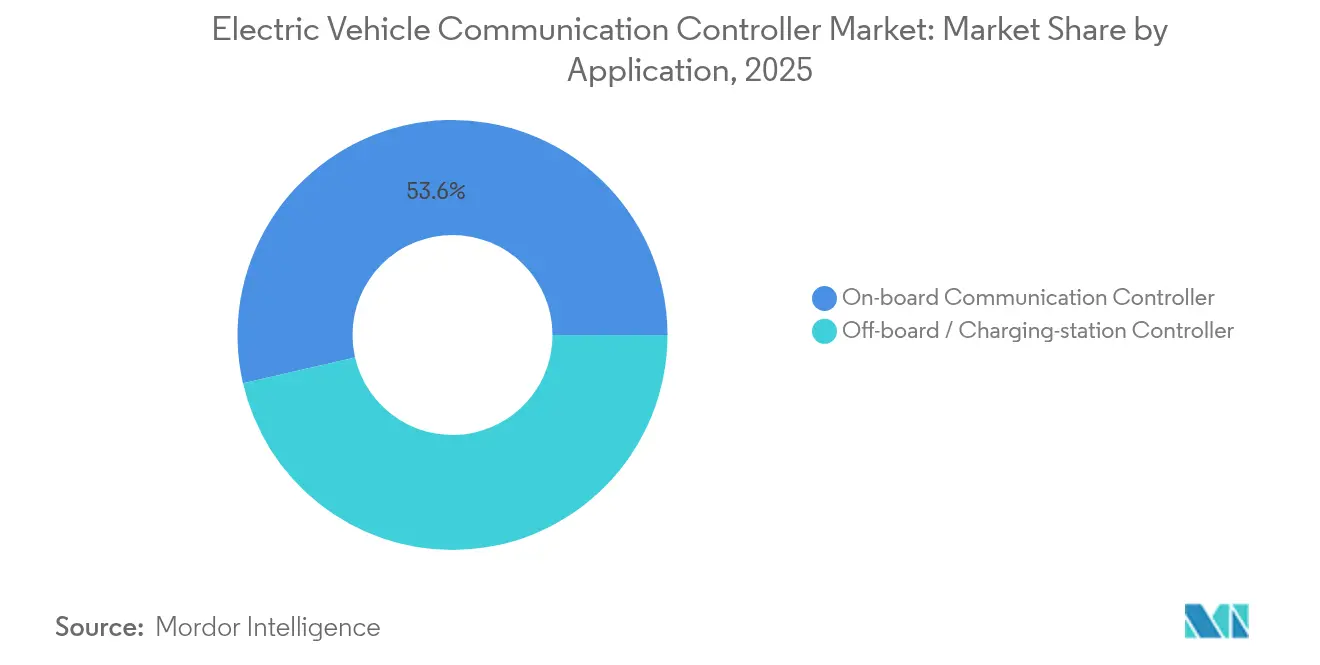

- By application, on-board controllers held 53.60% of the electric vehicle communication controller market size in 2025; off-board station controllers are expanding at a 29.15% CAGR to 2031.

- By communication protocol, ISO 15118/CCS maintained a 43.60% share in 2025, yet OCPP 2.0.1 is the fastest growing at 27.44% CAGR through 2031.

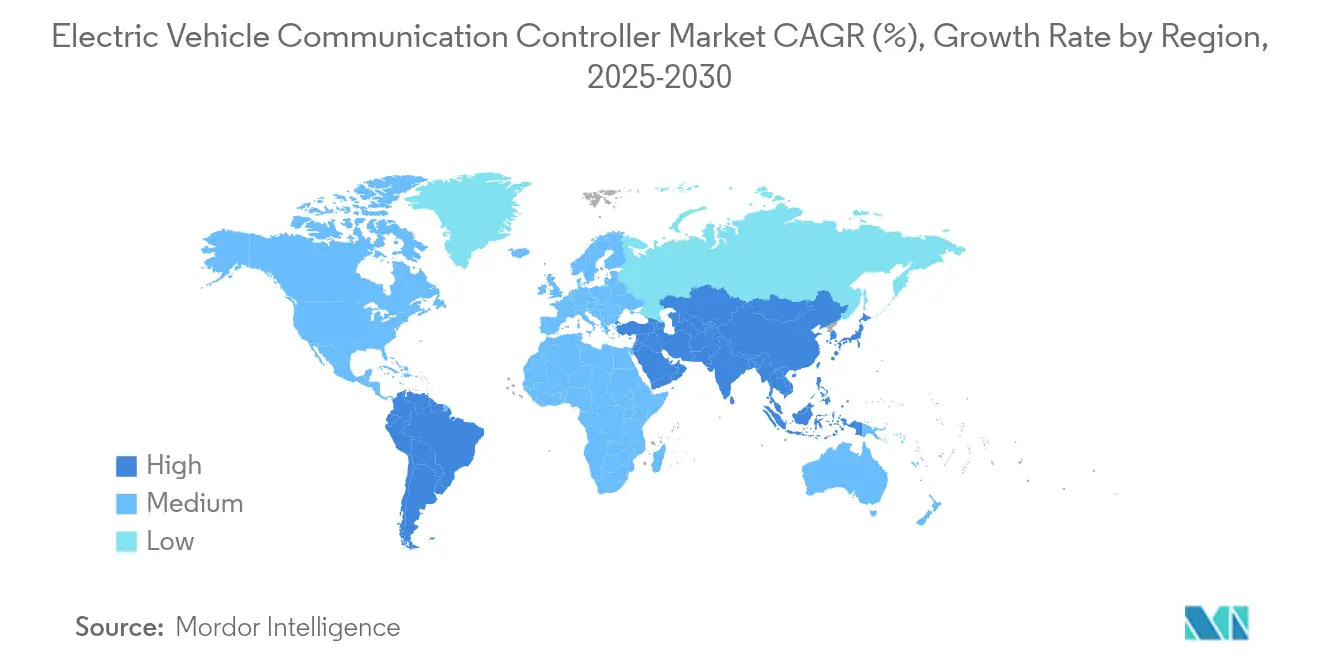

- By geography, Asia Pacific accounted for 46.30% revenue share in 2025 and is projected to post the highest 30.88% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Vehicle Communication Controller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Adoption Surge | +8.5% | Global with APAC leading | Medium term (2-4 years) |

| ISO 15118/OCPP Mandates | +6.2% | North America & EU | Short term (≤ 2 years) |

| Fast-DC Charger Expansion | +5.8% | Global urban corridors | Medium term (2-4 years) |

| Cheaper EV Comms Modules | +3.1% | Global manufacturing hubs | Long term (≥ 4 years) |

| Vehicle-to-Grid Scaling | +2.7% | North America & EU | Long term (≥ 4 years) |

| Auto Ethernet Migration | +1.9% | OEMs worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Electric Vehicles

Electric light-duty deliveries continue to set records, with China’s BYD alone planning 5.5 million units in 2025—all requiring multiple communication controllers for on-board and charging-station integration. Controller volumes rise faster than vehicle counts because modern EVs employ zonal compute and redundant charging pathways that demand additional gateways per platform. Each new architecture also increases data-throughput requirements; a single EV now hosts upwards of 8,000 chips, many reserved for network and security tasks. Semiconductor suppliers, therefore, treat the electric vehicle communication controller market as a growth engine inside the broader USD 88 billion automotive chip space forecast for 2027.

Government Mandates for ISO 15118 / OCPP Plug-and-Charge

North America’s National Electric Vehicle Infrastructure (NEVI) program ties federal funding to OCPP 2.0.1 compliance, forcing charge-point operators to deploy controllers that handle encrypted certificates, real-time billing, and remote diagnostics. Europe similarly hard-codes ISO 15118-20 requirements into public tenders, creating a single-path compliance route and cutting procurement risk for fleets. The shared imperative shortens design cycles and propels controller upgrades into 2026 model lines as suppliers pre-certify hardware for multiple transport agencies.

Expansion of Fast-DC Charging Infrastructure

Urban corridors are rolling out 400 kW to 1 MW chargers that can refill large battery packs in minutes, sparking demand for controllers capable of high-speed handshakes, thermal-loop monitoring, and dynamic load balancing. Delta Electronics debuted a 3 MW system that divides power across 16 outputs, each governed by a modular gateway to protect batteries and local grids [1]“3 MW Megawatt Charging Solution,” Delta Electronics, deltaww.com. Europe’s Germany Network project adds 9,000 fast-charging points by 2028, all requiring multi-protocol controllers that can pivot between CCS, NACS, and future wireless links.

Cost Decline of EV Communication Modules

Battery pack prices dipped more than 25% in 2024, freeing budget headroom for smarter electronics that improve charging experiences. Infineon’s EiceDRIVER gate ICs bundle isolation and diagnostics, lowering external component counts and helping controller makers hit cost targets for mass-segment vehicles. Wireless battery-management chips that remove 90% of harness wiring also trim system weight and assembly labor, indirectly supporting cheaper communication builds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost & Integration | -4.3% | Global tier-2 suppliers | Short term (≤ 2 years) |

| Fragmented Standards | -3.7% | Global, North America and Europe | Medium term (2-4 years) |

| Chip Supply Constraints | -2.8% | Asia-Pacific, Europe | Short term (≤ 2 years) |

| Cyber-Security Compliance | -2.1% | Global OEM base | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Costs & Complex Integration

Small suppliers wrestle with the capital needed to redesign circuitry for multi-protocol support, advanced encryption, and zonal compute alignment. Wireless battery-management architectures, while reducing wiring by up to 90%, impose brand-new RF validation steps that add months to development. Simulation-heavy workflows and combined FPGA-CPU boards further raise investment thresholds beyond the reach of niche players.

Lack of Unified Global Standards

Competing charging formats force OEMs to engineer multiple controller variants per vehicle platform, elevating bill-of-material counts and integration testing hours. Tesla’s NACS momentum in the United States, CCS prevalence in Europe, and CHAdeMO strongholds in Japan illustrate the fragmentation that inflates cost and delays launches. China’s plan to issue 70 exclusive chip standards by 2030 risks introducing a parallel ecosystem that global producers must also serve [2]“China to Set 70 Auto Chip Standards by 2030,” Nikkei Asia, asia.nikkei.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charging Type: Wireless Revolution Accelerates Despite Wired Dominance

Wired systems accounted for 82.10% of electric vehicle communication controller market share in 2025, supported by entrenched CCS and NACS infrastructure. Wireless platforms, however, are posting a blistering 31.62% CAGR that nudges the electric vehicle communication controller market size higher by unlocking unattended, cable-free top-up scenarios. Advances such as Oak Ridge National Laboratory’s 270 kW demo achieved 95% transfer efficiency with a Porsche Taycan . As SAE formalizes standards, more OEMs integrate induction coils at the factory line, cutting mechanical wear on charge ports.

Wired solutions are upgrading to 1 MW outputs for commercial vehicles, thereby forcing controller suppliers to embed advanced thermal and fault-ride-through logic. Wireless contenders counter by promoting curbside pads that integrate with city microgrids and autonomous taxis. Suppliers now design unified boards that auto-detect coil or plug connections and negotiate optimal power profiles, signaling a convergence phase that will redefine revenue splits after 2028.

By EV Type: PHEVs Surge as Automakers Hedge Electrification Strategies

Battery electrics retained 61.55% electric vehicle communication controller market share during 2025, yet plug-in hybrids are racing ahead at 29.58% CAGR as OEMs hedge against charging-network gaps. Hybrids require dual-mode controllers that juggle battery SOC, engine load, and regenerative braking maps, expanding addressable silicon content per vehicle. The electric vehicle communication controller market size for PHEV platforms is therefore widening faster than headline units as designers opt for domain controllers rather than discrete gateways.

Pure BEVs benefit from simpler architecture but increasingly incorporate bidirectional AC functions and thermal-loop coordination with heat pumps. Meanwhile, PHEV suppliers must also satisfy evaporative emissions diagnostics, pushing firmware complexity. Controller makers that pre-integrate engine ECU data paths with ISO 15118 plug-and-charge stacks gain a unique selling proposition for transitional fleets.

By Application: Off-board Controllers Drive Infrastructure Transformation

On-board modules captured 53.60% of the electric vehicle communication controller market size in 2025 as every EV carries at least one such gateway. Off-board station controllers, advancing at 29.15% CAGR, are rising quickly because operators scale dense charger clusters needing hierarchical load orchestration. A single depot may host 50 heads, each routed through a master controller that shapes demand curves to avoid peak tariffs. That growth trajectory is cementing a supplier base specializing in rugged, outdoor-rated boards with hot-swap I/O and edge AI accelerators.

Vehicle fleets lean on off-board intelligence for predictive maintenance, dynamic queueing, and grid-service bidding. Integrators now specify dual-core safety microcontrollers with Linux sidecars to run containerized apps, enabling revenue-sharing business models. This pushes higher recurring software value even as hardware margins compress, expanding lifetime revenues for forward-looking vendors.

By Communication Protocol: OCPP 2.0.1 Emerges as Next-Generation Standard

ISO 15118/CCS held a 43.60% share in 2025, underpinning most public DC units. OCPP 2.0.1 is accelerating at 27.44% CAGR because NEVI and similar schemes tie subsidies to their secure WebSocket sessions. The electric vehicle communication controller market size attached to OCPP-capable hardware grows rapidly as operators retrofit legacy chargers. Interface cards with hardware root-of-trust modules meet rising certificate-exchange volumes and cut handshake times to under one second.

CHAdeMO remains notable in Japan, and AC-focused SAE J1772 persists for workplace charging. Multi-protocol gateways, therefore, dominate purchase orders, fostering demand for flexible abstraction layers. Upcoming universal plug-and-charge frameworks will likely blend ISO 15118 token exchange with OCPP transaction flows, cementing the need for field-upgradable firmware images.

Geography Analysis

Asia Pacific led the electric vehicle communication controller market with 46.30% share in 2025 and is projected to expand at 30.88% CAGR through 2031. China’s aggressive EV quotas, semiconductor self-reliance push, and rapid fast-charger buildout underpin this dominance. BYD, SAIC, and Geely collectively shipped more than 4 million EVs in 2024, each platform embedding multitier gateways tuned for local grid codes. National targets covering 70 indigenous automotive chip standards by 2030 further stimulate domestic controller design pipelines.

North America benefits from bipartisan infrastructure funding that ties station reimbursement to open protocols, triggering record purchase orders for OCPP-ready units. The shift by Ford, GM, and several import brands to NACS ports requires adaptive controllers capable of CCS-to-NACS translation during a multiyear overlap period. Vehicle-to-grid pilots in Massachusetts and California, supported by utility incentive schedules, create secondary revenue streams for bidirectional firmware specialists.

Europe maintains a cohesive charging landscape anchored around ISO 15118 while investing EUR 2 billion to reach 1 million public chargers by 2030. The region’s strong cybersecurity legislation accelerates adoption of ISO/SAE 21434-compliant designs. Germany’s tender rules already require certificate-based authentication, nudging suppliers to bundle secure-element silicon and Linux containers for remote patching. Meanwhile, the European Chips Act aims to de-risk supply chains by seeding new fabs that will service emerging demand for Ethernet PHYs and AI coprocessors.

Competitive Landscape

Continental, Bosch, and Siemens leverage decades-long OEM relationships to remain preferred system integrators, bundling power electronics with controller firmware. Infineon, NXP, and STMicroelectronics integrate microcontrollers, PHYs, and security cores on single substrates, reducing board area and latency. Their foundry leverage lowers cost curves, making it difficult for smaller ASIC startups to secure allocation.

Infineon’s 2025 purchase of Marvell’s Automotive Ethernet business couples MCU heritage with 10 Gbps switching intellectual property, enabling turnkey zonal gateways that rival bespoke in-house architectures. NXP’s S32 CoreRide platform extends silicon into an open software stack, attracting ecosystem partners such as BlackBerry QNX and Valeo for domain-controller co-development.

Mid-size software vendors are entering hardware through reference-design partnerships. Vector’s AUTOSAR-capable switch board merges Marvell’s Brightlane silicon with embedded IDS, letting carmakers deploy intrusion detection without separate boxes. Startups concentrate on niche gains like quantum-resistant key exchange or cloud analytics for charger fleets, hoping to license IP to Tier 1s eager for differentiated cyber features.

Electric Vehicle Communication Controller Industry Leaders

Sensata Technologies

Ficosa International S.A.

Delta Electronics

Continental AG

Vector Informatik GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Infineon confirmed a USD 2.5 billion acquisition of Marvell’s Automotive Ethernet portfolio, bringing high-throughput switching IP in-house to accelerate zonal controller rollouts.

- January 2025: Infineon and Flex unveiled a modular zone-controller reference platform at CES 2025, targeting software-defined vehicles with scalable power-distribution layers.

- August 2024: Elektrobit partnered with NETA Auto and HiRain to co-design an advanced gateway controller that integrates secure cloud connectivity for over-the-air updates.

- March 2024: NXP launched S32 CoreRide, an open vehicle OS and networking platform positioned for 2027 production vehicles and supported by Accenture, BlackBerry QNX, and Valeo.

Global Electric Vehicle Communication Controller Market Report Scope

The electric vehicle communication controller (EVCC) acts as the central communication hub in electric vehicles, enabling data exchange among various vehicle components, charging infrastructure, and external systems. The Electric Vehicle Communication Controller Market encompasses the production, development, and integration of electric vehicle communication controllers (EVCCs).

The Electric Vehicle Communication Controller Market has been segmented by Charging Type, EV Type and geography. By Charging Type, the market is segmented into Wired and Wireless. By Charging Type the market is segmented into BEV and PHEV. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. For each segment, the market size and forecast are made on the basis of value (USD).

| Wired |

| Wireless |

| BEV |

| PHEV |

| On-board Communication Controller |

| Off-board / Charging-station Controller |

| ISO 15118 / CCS |

| CHAdeMO |

| SAE J1772 |

| OCPP 2.0.1 and later |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Charging Type | Wired | |

| Wireless | ||

| By EV Type | BEV | |

| PHEV | ||

| By Application | On-board Communication Controller | |

| Off-board / Charging-station Controller | ||

| By Communication Protocol | ISO 15118 / CCS | |

| CHAdeMO | ||

| SAE J1772 | ||

| OCPP 2.0.1 and later | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving the fast growth of the electric vehicle communication controller market?

Rapid EV adoption, mandated plug-and-charge standards such as ISO 15118, and the rollout of high-power charging infrastructure are collectively propelling the market at a 26.58% CAGR.

Which charging type segment is expanding the quickest?

Wireless charging controllers are advancing at 31.62% CAGR through 2031, outperforming wired systems despite the latter’s larger installed base.

How will vehicle-to-grid adoption influence controller demand?

Bidirectional pilots already show 1.5 MW of aggregated storage capacity, and broader V2G rollouts will require controllers that manage grid communication, dynamic pricing, and cybersecurity.

Why is Asia Pacific the leading regional market?

China’s large EV production volumes, coordinated charger buildouts, and semiconductor self-sufficiency programs give Asia-Pacific 46.30% market share and the highest regional CAGR.

Page last updated on: