Effervescent Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

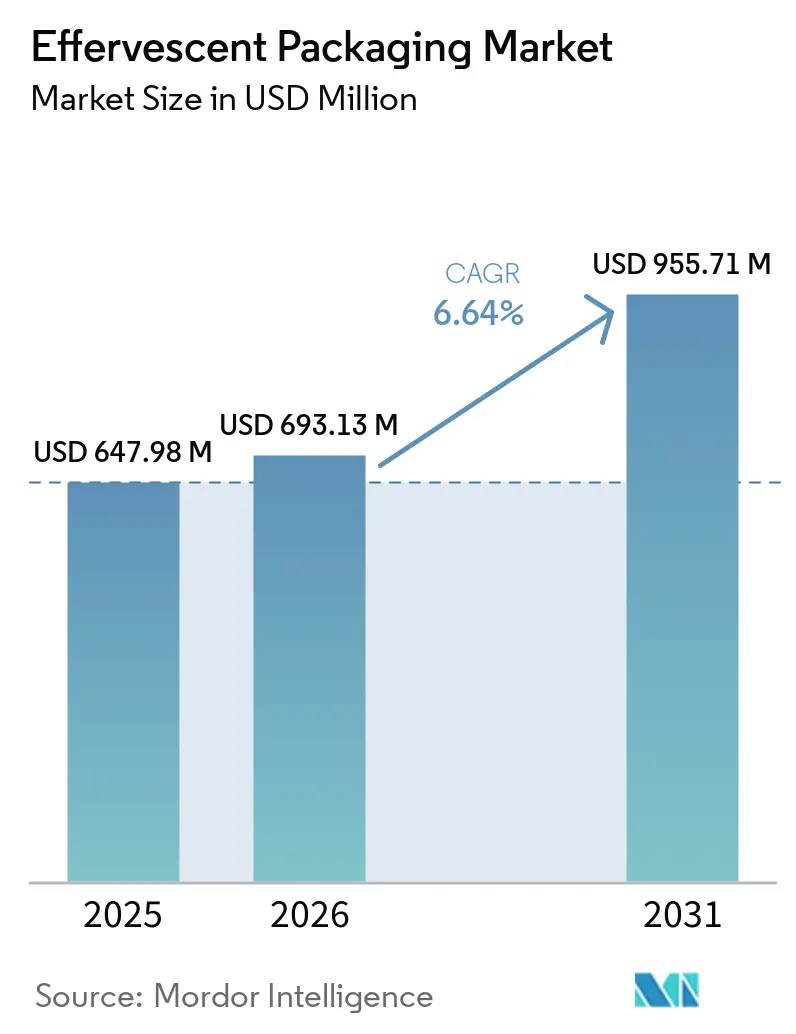

| Market Size (2026) | USD 693.13 Million |

| Market Size (2031) | USD 955.71 Million |

| Growth Rate (2026 - 2031) | 6.64% CAGR |

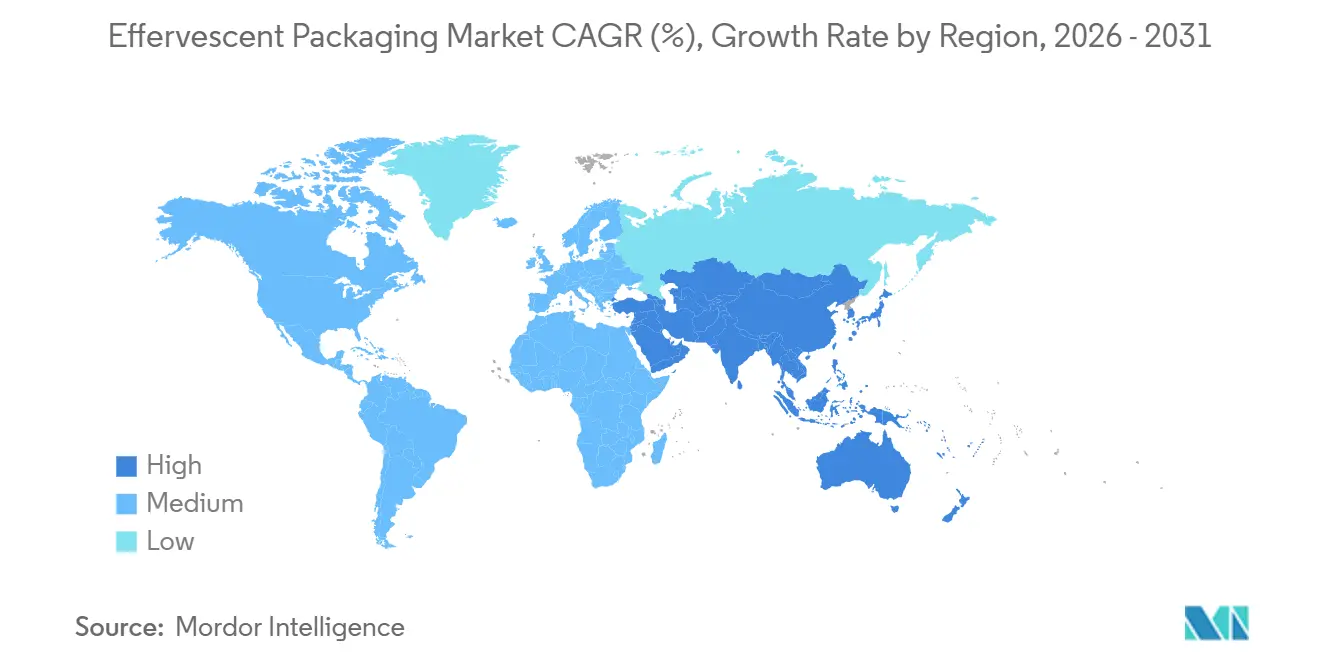

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

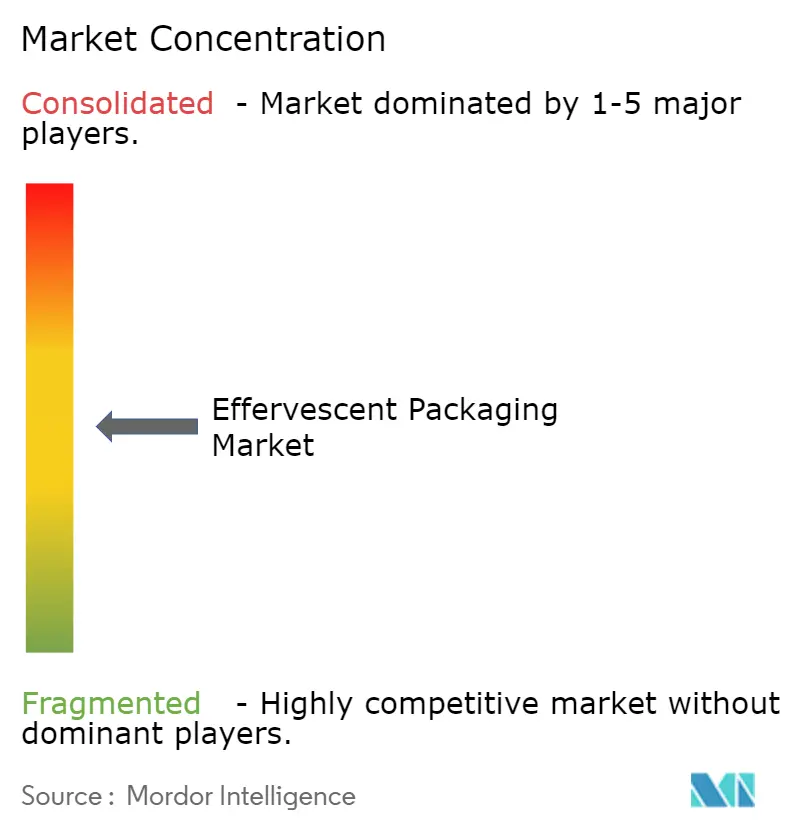

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Effervescent Packaging Market Analysis by Mordor Intelligence

The effervescent packaging market size is projected to be USD 647.98 million in 2025, USD 693.13 million in 2026, and reach USD 955.71 million by 2031, growing at a CAGR of 6.64% from 2026 to 2031. The effervescent packaging market is expanding as over-the-counter health products and functional supplements continue to gain wider consumer acceptance, especially where faster dissolution and easier intake support repeat use. Moisture control has become a central purchase criterion across the effervescent packaging market because product stability depends heavily on barrier performance, closure integrity, and reliable shelf-life. The regulatory cycle is also becoming more demanding, with recyclability rules in Europe and unit-level traceability requirements in the United States and Europe pushing the effervescent packaging market toward higher-value and more specification-driven formats. This is changing supplier selection across the effervescent packaging market, as converters with strong validation, desiccant integration, and serialization capabilities are gaining ground over format-generic competitors. Margin pressure from aluminum and specialty component costs is still a clear constraint, but it is also reinforcing consolidation and supporting investment in advanced packaging platforms across the effervescent packaging market.

Key Report Takeaways

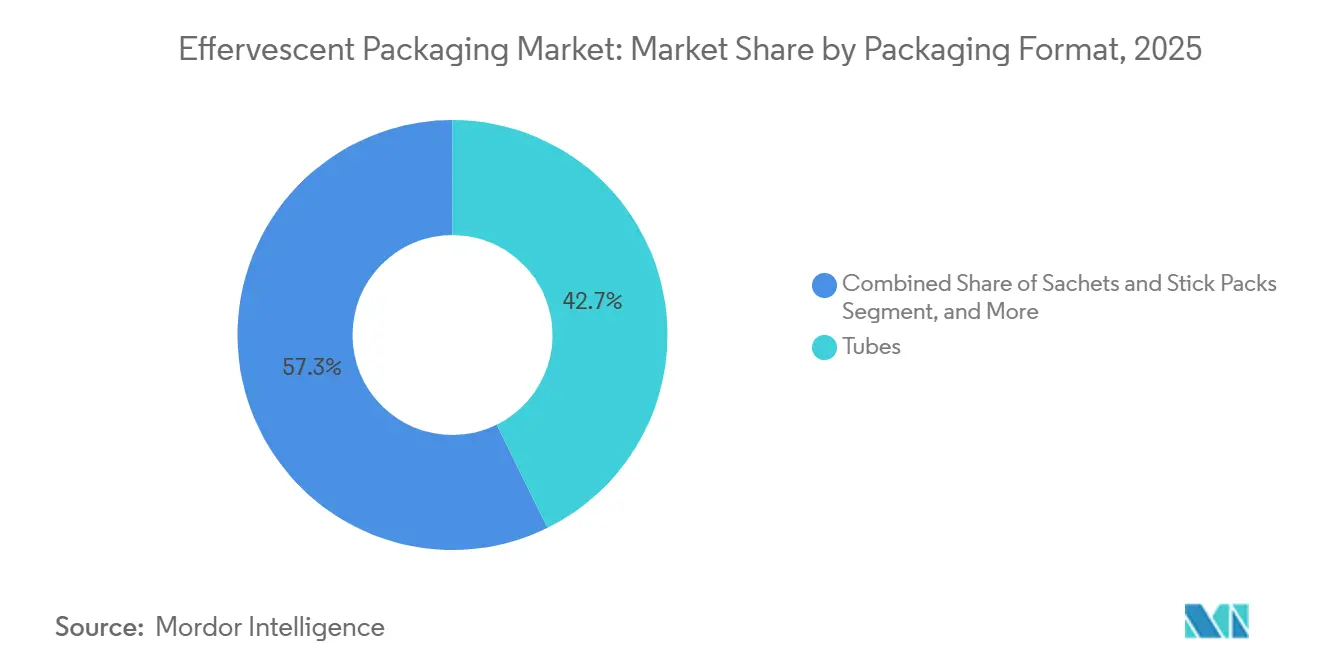

- By packaging format, tubes led with a 42.71% in the effervescent packaging market in 2025.

- By material type, the effervescent packaging market size for the aluminum segment is forecast to advance at a 7.81% CAGR through 2031.

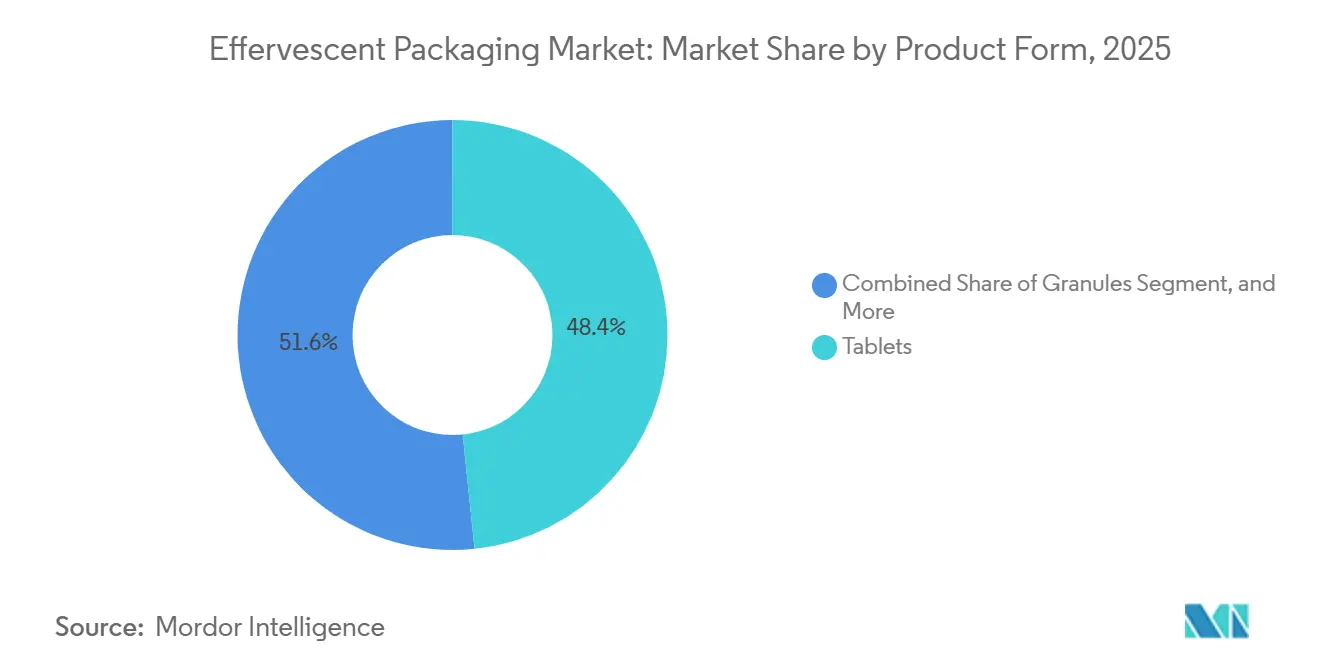

- By product form, tablets accounted for 48.37% in the effervescent packaging market in 2025.

- By end-user industry, the effervescent packaging market size for the nutraceuticals and dietary supplements segment is forecast to advance at a 7.36% CAGR through 2031.

- By geography, North America captured 32.74% of the effervescent packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Effervescent Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumption of Effervescent OTC And Supplement Products | +2.1% | Global, with intensity in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Growing Need for Moisture-Barrier Tubes, Blisters, And Desiccant Closures | +1.3% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Expansion of Sports Hydration and Electrolyte Tablet Formats | +0.9% | North America and Asia-Pacific core, spill-over to Europe and Middle East and Africa | Short term (≤ 2 years) |

| Shift Toward Senior-Friendly and Portable Unit Formats | +0.6% | Europe and North America, early gains in Japan and South Korea | Long term (≥ 4 years) |

| EU Recyclability Rules Accelerating Mono-Material Packaging Innovation | +0.4% | Europe, with spill-over to global export supply chains | Medium term (2-4 years) |

| Smart Traceability and Adherence Features Entering Oral Solid Dose Packs | +0.2% | North America, Europe, and national with early gains in urban Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumption of Effervescent OTC and Supplement Products

The effervescent packaging market is benefiting from a clear shift toward fast-dissolving, more palatable delivery systems for supplements and over-the-counter products. Patient preference for effervescent formats remains strong in use cases where swallowing conventional tablets is less convenient, and this supports repeat demand for specialized tubes, blisters, and sachets. Peer-reviewed work in RSC Pharmaceutics reported faster absorption and strong patient preference for effervescent forms of paracetamol, aspirin, and vitamins, supporting continued adoption of this format in the effervescent packaging market. Brand owners are also extending effervescent lines into adjacent wellness categories, which broadens the served base of the effervescent packaging market beyond traditional pharmacy demand. This shift matters because once these products move into more regulated or pharmacy-led channels, packaging specifications usually rise with them. The result is that the effervescent packaging market is growing in both volume and value, with procurement moving toward higher-performing, more presentation-sensitive pack formats.

Growing Need for Moisture-Barrier Tubes, Blisters, and Desiccant Closures

The effervescent packaging market relies on strong moisture protection because product reactivity makes stability highly sensitive to humidity. This is pushing converters and brand owners toward tubes with integrated desiccant closures and toward blister structures that can deliver more dependable barrier performance. Industry reports on pharmaceutical packaging indicate that integrated desiccant systems are gaining acceptance because they simplify pack architecture and help keep sorbent material out of direct patient contact. In practical terms, this changes the value proposition in the effervescent packaging market, because validated closure performance becomes as important as material choice. High-humidity markets in South and Southeast Asia also support premium demand for cold-form aluminum-based formats, where moisture protection is often treated as a non-negotiable requirement. Smart sorbent technologies are also entering qualification processes, indicating that the effervescent packaging market is moving beyond passive containment toward more active protection systems.

Expansion of Sports Hydration and Electrolyte Tablet Formats

The effervescent packaging market is also being supported by the spread of electrolyte tablets from sports nutrition into broader hydration and daily wellness use. This shift creates a separate volume stream for single-serve and portable formats, especially stick packs, sachets, and small multi-tablet tubes. It also creates a split in format expectations, because some packs must meet pharmacy-level barrier and safety needs while others are designed for gym, travel, and e-commerce channels.[1]Hermes Pharma, “New Pharma Packaging Is Child-Resistant and Senior-Friendly,” Hermes Pharma, hermes-pharma.com This raises average packaging value in the effervescent packaging market because suppliers are no longer competing only on convenience and print appeal. It also means the effervescent packaging market is seeing growth from a category that used to be more cost-led and less demanding of pack performance.

Shift Toward Senior-Friendly and Portable Unit Formats

The effervescent packaging market is seeing growing interest in packs that are easier to handle, read, and use in controlled-dosing routines. That is especially relevant in applications linked to older patients, dysphagia, and adherence-sensitive regimens where pack usability affects compliance as much as the dosage form itself. Accessibility-focused packaging commentary from pharmaceutical pack developers shows that child-resistance and senior-friendliness are increasingly treated as joint design targets rather than separate requirements. This is lifting demand for calendarized blisters, large-font layouts, tactile differentiation, and unit-dose formats that fit pharmacy and clinical settings. Portable and numbered blister formats are also well suited to physician sample programs and trial kits, where tracking and regimen clarity matter more than simple bulk dispensing. The effervescent packaging market, therefore, gains not only from aging demographics but also from the broader move toward packaging formats that support access, portability, and more reliable use behavior.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of High-Barrier Materials and Desiccant Components | -0.9% | Global, most acute in North America due to tariff exposure | Short term (≤ 2 years) |

| Moisture Sensitivity Raising Validation and Product-Failure Risk | -0.6% | Global, heightened impact in tropical South Asia and Southeast Asia | Medium term (2-4 years) |

| Fragmented Regulatory and Child-Resistance Requirements | -0.4% | Multi-market exporters in Europe and North America | Medium term (2-4 years) |

| Aluminum and Polymer Cost Volatility, Including Tariff Exposure | -0.3% | North America and Europe, Asia-Pacific secondary impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of High-Barrier Materials and Desiccant Components

The effervescent packaging market remains exposed to the high cost of premium barrier materials and specialized desiccant components. This is especially difficult for mid-sized nutraceutical and consumer health brands that need pharmaceutical-grade protection but lack the scale advantages of larger buyers. Trade reporting showed that U.S. Section 232 aluminum duties reached 50% by mid-2025, which sharply increased delivered aluminum costs for packaging applications. Additional reporting in 2026 also showed that the U.S. Midwest aluminum premium moved above USD 1 per pound, reinforcing the point that regional premiums can intensify cost pressure even when base metal exposure is hedged. This leaves smaller converters in a weaker position inside the effervescent packaging market, because they face both higher input costs and a tighter path to margin recovery. It also supports consolidation in the effervescent packaging market, as larger integrated players are better placed to manage procurement risk, reformulation costs, and longer customer qualification cycles.

Moisture Sensitivity Raising Validation and Product-Failure Risk

The effervescent packaging market has one of the most stringent validation burdens in oral solid-dose packaging, as even minor failures in barrier integrity can affect product performance. Problems such as weak closure seals, foil defects, or inconsistent desiccant function can lead to premature reaction, reduced potency, or visible tablet degradation. This lengthens validation timelines and raises the cost of entering regulated channels in the effervescent packaging market. In tropical distribution settings, the gap between controlled development conditions and on-shelf conditions can become more pronounced, increasing operational risk for manufacturers serving humid markets. Moisture-control specialists serving the pharma industry have emphasized that desiccant packaging remains central to stability management for solid oral dosage forms, especially where ambient moisture exposure is difficult to control throughout the wider supply chain. As a result, the effervescent packaging market continues to favor suppliers that can combine barrier performance, stability support, and validation-ready pack systems in a single offering.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Format: Blisters and Sustainable Tube Innovation Drive Format Evolution

Tubes held 42.71% of the effervescent packaging market share in 2025, while blisters are projected to advance at an 7.53% CAGR in the effervescent packaging market size outlook through 2031. Tubes remain central to the effervescent packaging market because they combine consumer familiarity with integrated desiccant closure capability and straightforward dispensing. That structure continues to work well in the pharmacy, supplement, and household channels, where multi-dose storage and moisture control must be in the same pack. Blisters, however, are moving faster in the effervescent packaging market because they support unit-dose control, calendarization, and traceability features that fit new compliance expectations and adherence goals. In tropical or high-humidity regions, cold-form blister solutions are also gaining acceptance where barrier performance overrides cost sensitivity.

Sachets and stick packs are adding incremental demand to the effervescent packaging market through sports hydration and functional food applications, where portability and single-serve convenience are central to product positioning. Hermes Pharma's validated child-resistant and senior-friendly stick pack showed that even this convenience-led part of the effervescent packaging market is moving toward more formal safety standards. Bottles, canisters, and strip packs keep a place in the effervescent packaging market where value pricing, larger fills, or emerging-market dose access still matter. At the same time, PPWR is pushing redesign work across the effervescent packaging market, with Sanner's tethered cap launch showing how converters are adapting tube formats to recycling requirements without forcing changes on existing filling lines.

By Material Type: Aluminum's Dual Position Faces Cost and Sustainability Pressure

Aluminum held a 33.28% share of demand in 2025, underscoring its strong presence in the effervescent packaging market across blister, strip pack, and tube structures. Its position remains strong because extremely low moisture transmission and oxygen protection are hard to match when formulations are highly sensitive and already tied to validated pack specifications. That creates a structural advantage for aluminum in the effervescent packaging market, especially in regulated pharmaceutical uses where material substitution moves slowly. At the same time, the cost profile has become more challenging due to tariff actions and regional premiums, which have increased sourcing pressure on converters and brand owners. This keeps aluminum strategically important in the effervescent packaging industry even while buyers explore lighter, more recyclable, or mixed-material alternatives.

Plastic remains the most widely used material by volume in the effervescent packaging market, especially in tubes and bottles, where polyethylene and polypropylene fit existing line economics and mainstream filling systems. PPWR is accelerating the shift toward mono-material plastic structures, meaning recyclability is now influencing material choice more directly than before. Paper-based development is also moving forward, with Neopac introducing its PaperX FiberTop concept and Mondi investing EUR 16 million (USD 18.7 million) in barrier paper capacity for applications where high-barrier paper can begin to replace more complex multi-material formats.[2]Neopac Unveils World's First Paper Tube Designed for Full Recyclability in the Paper Stream at IFPC Congress 2025,” Neopac, neopac.com Constantia Flexibles also invested EUR 50 million (USD 54 million) in capacity expansion at Constantia Teich, which shows that the effervescent packaging market is balancing supply assurance with a gradual search for more sustainable material pathways.

By Product Form: Tablets Lead While Powders Expand Through Portable Use Cases

Tablets represented 48.37% of demand in 2025, while powders are forecast to grow at an 7.46% CAGR through 2031. Tablet leadership remains deeply embedded in the effervescent packaging market because the format is familiar to consumers, straightforward to dose, and well-suited to high-speed production systems. Clinical and consumer acceptance also remain high, with pre-dosed forms preferred, and peer-reviewed evidence continues to support faster dissolution performance for effervescent tablets in several use cases. This keeps tablets at the center of the effervescent packaging market across pharmaceuticals, vitamins, and many OTC categories. It also reinforces demand for tubes and blisters that can protect unit integrity while maintaining ease of handling.

Powders are moving faster in the effervescent packaging market because stick packs and sachets fit hydration, sports, protein blends, and portable wellness occasions more naturally than rigid packs. That growth changes sourcing needs because powder systems often rely on multilayer barrier films that provide strong moisture and oxygen protection. This creates a notable tension in the effervescent packaging market between pack performance and the push for simpler recyclable structures. Granules remain smaller in volume, but they retain strategic value in pediatric and geriatric applications where dose flexibility and dissolution behavior require closer control, keeping the effervescent packaging market open to more specialized fill and closure solutions.

By End-User Industry: Pharmaceuticals Anchor Demand While Nutraceuticals Accelerate

Pharmaceuticals held a 33.41% share in 2025, while nutraceuticals and dietary supplements are forecast to expand at a 7.36% CAGR through 2031. Pharmaceuticals remain the volume anchor of the effervescent packaging market because barrier validation, serialization readiness, and regulatory discipline keep packaging requirements high and relatively stable. That favors tubes with integrated desiccants, cold-form blisters, and technically advanced strip packs that can meet more demanding traceability and shelf-life needs. The effervescent packaging market also benefits from reformulation efforts aimed at elderly users and dysphagia-related use cases, where improved ease of intake increases compliance and supports continued demand for effervescent delivery. In this part of the effervescent packaging industry, supplier differentiation depends less on pack cost and more on proof of performance, validation support, and compliance execution.

Nutraceuticals and dietary supplements are moving faster inside the effervescent packaging market because sports performance, hydration, immunity, and everyday wellness are increasingly overlapping in consumer purchasing behavior. This is pulling supplement brands toward pharmacy-style formats and away from simpler commodity packaging, especially when products enter organized retail or pharmacy channels. Food and beverage uses add another layer of demand in the effervescent packaging market through hydration tablets, drink sachets, and functional blends that require both barrier protection and stronger brand presentation. Household and personal care applications remain smaller, but they continue to matter where effervescent tablets are used for cleaning, water treatment, bath products, or portable care formats, and that supports a broader end-use mix for the effervescent packaging market overall.

Geography Analysis

North America held 32.74% of the effervescent packaging market share in 2025, while Asia-Pacific is forecast to expand at a 7.89% CAGR in the effervescent packaging market size outlook through 2031. North America leads the effervescent packaging market because its OTC distribution network is well established and its branded supplement channel is deep, organized, and highly visible in mass retail. The region also operates with a higher technical baseline for pharmaceutical packaging, and that supports demand for advanced blister, strip-pack, and desiccant-integrated tube formats. Sanner's opening of its Greensboro, North Carolina, facility in 2025 reflected the commercial value of U.S. local manufacturing, where shorter lead times and reduced tariff exposure can directly matter to pharmaceutical and nutraceutical customers.[3]Sanner Group, “Sanner at Pharmapack: New Developments and Capacity Expansions,” Sanner Group, sanner-group.com Canada and Mexico add to regional demand through pharmaceutical manufacturing and export activity, while near-shoring trends are helping North America retain strategic relevance inside the effervescent packaging market.

Europe remains a major center of the effervescent packaging market because regulation affects packaging design more directly there than in most other regions. The PPWR entered into force in February 2025 and applies from August 2026, which means converters serving the region are already balancing recyclable design targets with moisture-performance needs. Germany, the United Kingdom, France, Italy, and Spain continue to shape regional demand, with Germany standing out as a packaging conversion and pharmaceutical manufacturing hub. The United Kingdom adds a distinct layer of compliance through post-Brexit labeling requirements, which increases complexity for product lines that still need to move across both UK and EU settings.

Asia-Pacific is the fastest-growing regional block in the effervescent packaging market because rising incomes, urbanization, and broader health awareness are expanding the customer base for effervescent products. China and India are especially important to the effervescent packaging market because they combine domestic demand growth with large-scale pharmaceutical and nutraceutical manufacturing capacity. Japan and South Korea add a more mature demand profile, but they also support the effervescent packaging market through stricter quality expectations and strong interest in patient-friendly formats. Middle East and Africa and South America remain smaller in absolute size, yet humid climates and widening pharmacy networks create targeted opportunities for high-barrier and premium value-added formats in the effervescent packaging market.

Competitive Landscape

The effervescent packaging market is moderately fragmented, but it is not a low-barrier field. A limited group of specialists has built defensible positions in integrated desiccant closures, cold-form blister materials, and compliance-driven pack design, which gives the effervescent packaging market a more technical competitive profile than standard flexible packaging. Sanner strengthened its position through the acquisitions of Springboard in January 2024 and Gilero in September 2024, which expanded its development and manufacturing reach across device design, packaging, and medtech services. Amcor's completion of its USD 13 billion combination with Berry Global in April 2025 created a much larger platform with an expected revenue base of around USD 23 billion, and that scale can be directed toward higher-value pharmaceutical and nutraceutical formats.[4]Amcor plc, “Amcor Completes Combination with Berry Global; Positioned to Significantly Enhance Value for Customers and Shareholders,” SEC EDGAR, sec.gov These moves show that the effervescent packaging market is rewarding both technical depth and global manufacturing scale.

Mid-tier players are also using focused investment to strengthen their role in the effervescent packaging market. Constantia Flexibles announced more than EUR 100 million (USD 108 million) in European manufacturing investments, including EUR 50 million (USD 54 million) for capacity expansion at Constantia Teich, which supports pharmaceutical and nutraceutical substrate demand. introduced its SuperPod cold-form blister technology in January 2026, aiming to reduce cavity size and increase line efficiency without sacrificing full barrier performance, which is a clear example of engineering-led competition in the effervescent packaging market. Gerresheimer also moved into enhanced moisture-protection solutions through its partnership with Milliken in April 2026, showing how licensing and material science partnerships are becoming part of competitive strategy in the effervescent packaging market.

Another competitive theme in the effervescent packaging market is the search for recyclable high-barrier formats that do not weaken moisture protection. This is still an open field, especially in sachets and stick packs for sports nutrition and wellness uses, where compliance and sustainability goals can pull in different directions. Neopac's PaperX FiberTop and Sanner's tethered-cap development both show that converters are trying to win share through redesign rather than through price cuts alone. The effervescent packaging market therefore remains moderately concentrated in capability terms, even if formal market share data for top companies is not publicly detailed in the source draft.

Effervescent Packaging Industry Leaders

Sanner GmbH

AptarGroup, Inc.

NBZ Healthcare LLP

Hoffmann Neopac AG

Romaco Pharmatechnik GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Mondi partnered with Dreco to launch a new powder detergent flexible packaging structure integrating 50% post-consumer recycled plastic content, validated under ISCC PLUS mass-balance certification and designed to meet EU PPWR's 35% recycled-content mandate for this packaging category by 2030. The

- April 2026: Gerresheimer entered a technology partnership with Milliken to deploy LeneX UltraGuard technology across its pharmaceutical plastic packaging portfolio, targeting enhanced moisture protection and material performance for oral solid dosage products.

- February 2026: Gerresheimer formally initiated the sale process for Centor Inc., its U.S.-based prescription plastic vials and closures business, in a strategic portfolio-concentration move toward higher-margin pharmaceutical packaging and drug delivery segments.

- January 2026: Sanner launched its Tethered Cap, a sustainable closure for effervescent tablet tubes featuring an attached tamper-evident safety ring ensuring full plastic recyclability, at Pharmapack Europe 2026 in Paris.

Global Effervescent Packaging Market Report Scope

The scope of the report includes an analysis of the effervescent packaging market, which refers to the packaging solutions specifically designed for effervescent products. These products typically release carbon dioxide when dissolved in water, creating a fizzing effect. The study covers various packaging types, materials, and applications, providing insights into market trends, growth drivers, challenges, and opportunities during the forecast period.

The Effervescent Packaging Market is Segmented by Packaging Format (Tubes, Blisters, Sachets and Stick Packs, Bottles and Canisters, and Strip Packs), Material Type (Plastic, Aluminum, Glass, Paper-Based and Fiber-Based, and More), Product Form (Tablets, Powders, and Granules), End-User Industry (Food and Beverage, Pharmaceuticals, Personal Care and Cosmetics, Nutraceuticals and Dietary Supplements, Household, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Tubes |

| Blisters |

| Sachets and Stick Packs |

| Bottles and Canisters |

| Strip Packs |

| Plastic |

| Aluminum |

| Glass |

| Paper |

| Other Material Types |

| Tablets |

| Powders |

| Granules |

| Food and Beverage |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Nutraceuticals and Dietary Supplements |

| Household |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Format | Tubes | ||

| Blisters | |||

| Sachets and Stick Packs | |||

| Bottles and Canisters | |||

| Strip Packs | |||

| By Material Type | Plastic | ||

| Aluminum | |||

| Glass | |||

| Paper | |||

| Other Material Types | |||

| By Product Form | Tablets | ||

| Powders | |||

| Granules | |||

| By End-user Industry | Food and Beverage | ||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Nutraceuticals and Dietary Supplements | |||

| Household | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the effervescent packaging space?

The effervescent packaging market stands at USD 693.13 million in 2026 and is forecast to reach USD 955.71 million by 2031, growing at a 6.64% CAGR.

Which packaging format leads demand for effervescent products?

Tubes led demand in 2025 with a 42.71% share because they combine moisture protection, integrated desiccant closure options, and easy dispensing.

Which format is expanding the fastest through 2031?

Blisters are the fastest-growing format with an 7.53% CAGR, supported by unit-dose use, adherence benefits, and rising traceability requirements.

Why are moisture-barrier systems so important for effervescent products?

These products are highly sensitive to humidity, so barrier materials, closure integrity, and desiccant systems directly affect shelf life, stability, and compliance.

Which end-user group drives the largest share of demand?

Pharmaceuticals held the largest share at 33.41% in 2025 because validated barrier performance and compliance needs keep packaging standards high.

Which region offers the strongest growth outlook?

Asia-Pacific has the fastest growth outlook with a 7.89% CAGR through 2031, supported by rising health spending, urbanization, and expanding pharmaceutical and nutraceutical production.

Page last updated on: