Miscanthus-Based Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 78.53 Million |

| Market Size (2031) | USD 115.67 Million |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Miscanthus-Based Packaging Market Analysis by Mordor Intelligence

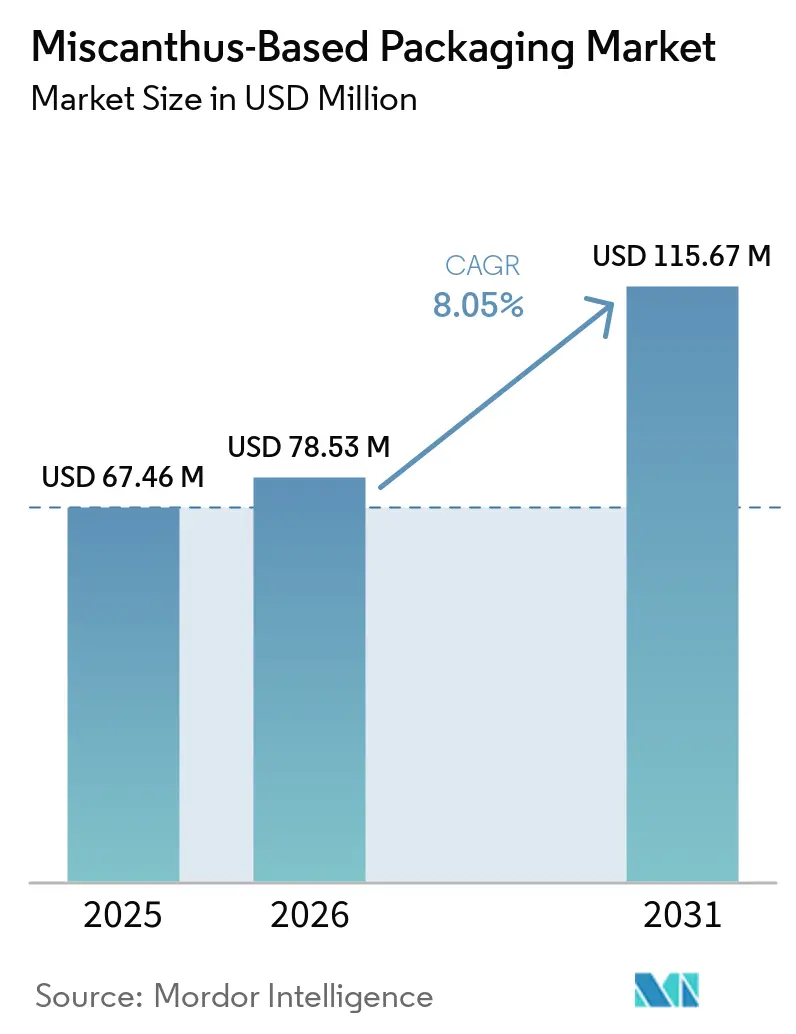

The Miscanthus-Based Packaging Market size is projected to be USD 67.46 million in 2025, USD 78.53 million in 2026, and reach USD 115.67 million by 2031, growing at a CAGR of 8.05% from 2026 to 2031.

Rising regulatory pressure against single-use plastics, rapid commercialization of molded-fiber technology, and brand-level commitments to regenerative agriculture are accelerating adoption across foodservice, retail fulfillment, and personal-care packaging. European Union rules that take full effect in August 2026 remove most conventional plastics from foodservice formats, creating time-bound demand for fiber alternatives. At the same time, volatile wood-pulp pricing is nudging converters toward diversified fiber inputs that stabilize raw-material costs and carbon narratives. The convergence of these forces positions the miscanthus-based packaging market as a credible growth pocket within the wider fiber-packaging ecosystem, even though processing infrastructure still trails commercial ambition.

Key Report Takeaways

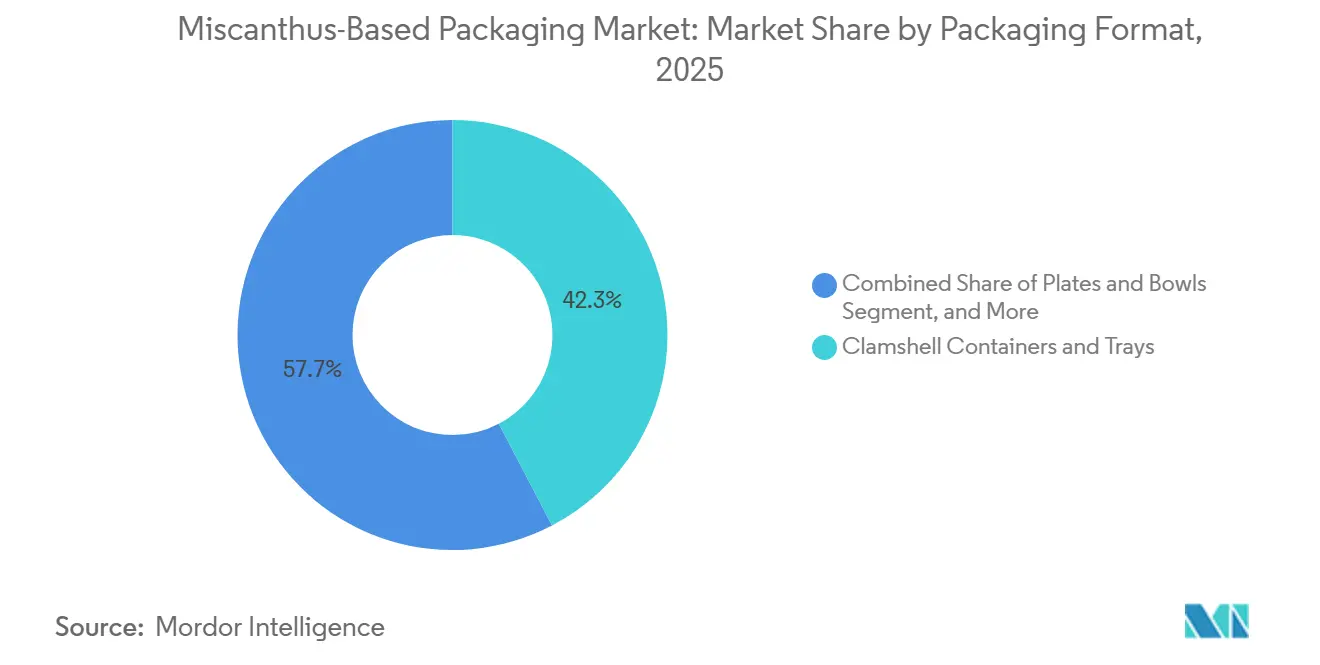

- By packaging format, clamshell containers and trays led with 42.34% of the miscanthus-based packaging market share in 2025, while protective packaging is forecast to expand at a 9.78% CAGR to 2031.

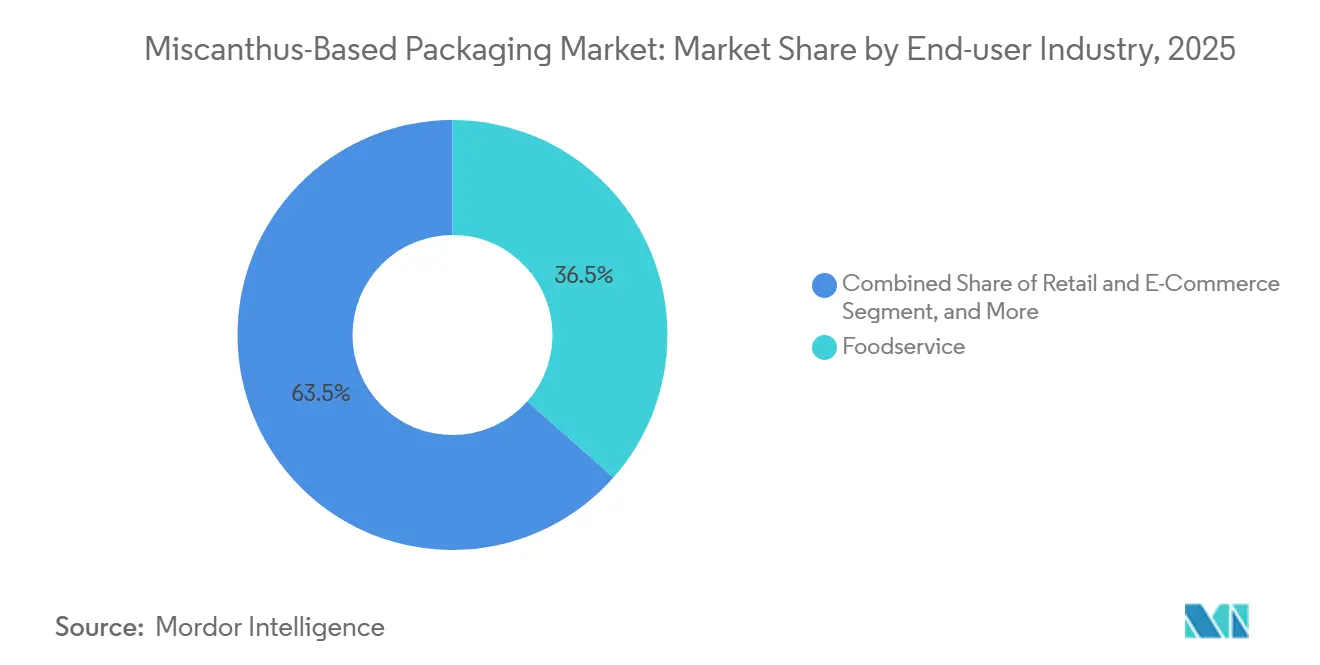

- By end-use industry, foodservice accounted for 36.54% of 2025 revenue, whereas retail and e-commerce applications are projected to grow at a 12.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Miscanthus-Based Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Push Toward Reduction of Plastic Packaging | +2.5% | Europe, North America, ASEAN core markets | Short term (≤ 2 years) |

| Expansion of Fiber-Based Alternatives to Expanded Polystyrene (EPS) | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Increasing Adoption of Non-Wood Fibers by Brands and Converters | +1.5% | Global, led by Europe and Asia-Pacific | Medium term (2-4 years) |

| Supply Chain Diversification Away from Wood-Based Raw Materials | +1.2% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Alignment with Regenerative Agriculture and Carbon Reduction Goals | +1.0% | Europe, North America | Long term (≥ 4 years) |

| Rising Investments in Regional Dry-Molded Fiber Capacity | +1.4% | Europe, Asia-Pacific, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push Toward Reduction of Plastic Packaging

The European Union Packaging and Packaging Waste Regulation obliges all packaging to be recyclable or compostable by 2030, effectively disqualifying multilayer plastics and most polystyrene items, and thereby forcing procurement teams to reassess substrate choices.[1]European Commission, “Regulation (EU) 2025/351 on Packaging and Packaging Waste,” eur-lex.europa.eu Seven U.S. states adopted extended producer-responsibility laws during 2024-2025, adding fee mechanisms that tilt economics in favor of compostable fiber alternatives and shorten decision cycles for national brands.[2]Product Stewardship Institute, “Extended Producer Responsibility Legislation in U.S. States,” productstewardship.us ASEAN member countries such as Vietnam and the Philippines already require EPR compliance, while Indonesia, Malaysia, and Thailand are phasing in similar mandates by 2027, giving regional retailers a clear regulatory horizon. These synchronized policies compress adoption timelines, making the two-year window before enforcement a critical commercialization phase for miscanthus converters. Because the material meets EN 13432 compostability without synthetic binders, producers avoid costly reformulation rounds that often delay wood-pulp solutions.

Expansion of Fiber-Based Alternatives to Expanded Polystyrene

Municipal polystyrene bans now apply in more than 200 jurisdictions worldwide, yet end users still demand thermal insulation and cushioning metrics that historically required EPS. PulPac’s dry-molded fiber process achieves 3.5-second cycle times, eliminates water-intensive drying, and yields complex geometries that match EPS drop-test performance while reducing energy consumption by 65%. Graphic Packaging earmarked USD 85 million in 2024 to install replicated capacity for cold-chain containers, confirming that large incumbents see molded fiber as an EPS successor for food and pharmaceuticals. Because miscanthus fiber has lower bulk density compared with hardwood pulp, finished inserts weigh less, which directly reduces freight fees on e-commerce parcel networks where dimensional weight influences cost. This shipping advantage resonates with logistics managers, giving the material a value proposition that extends beyond sustainability narratives.

Increasing Adoption of Non-Wood Fibers by Brands and Converters

Brand owners are embedding non-wood fiber quotas into supplier scorecards to hedge volatile wood-pulp prices and bolster regenerative-agriculture storytelling. Better Earth launched its Farmer’s Fiber Collection in 2025, sourcing miscanthus, switchgrass, and sorghum directly from U.S. growers, thereby bypassing traditional pulp-mill intermediaries and locking in full chain-of-custody transparency. Stora Enso purchased a minority stake in Matrix Pack the same year, granting access to eight molded-fiber sites that can rapidly integrate grass fiber into existing lines without duplicating capex. SIG and PulPac partnered in July 2025 to co-develop carton closures consisting of 90% paper content, illustrating how non-wood inputs are penetrating high-performance niches previously dominated by plastic. These moves help push the non-wood pulp market toward its projected USD 961 million valuation by 2032, raising the baseline demand that miscanthus suppliers can address.

Supply Chain Diversification Away from Wood-Based Raw Materials

Softwood and hardwood pulp traded between USD 800 and USD 1 200 per tonne during 2024-2025, with scarcity episodes triggered by European mill outages and North American wildfire seasons. Converters such as Ranpak responded by blending grass fiber with recycled paper, producing GrasiKraft void-fill that cuts basis weight by 40% while maintaining tensile integrity, which demonstrates a direct hedge against pulp price spikes. Ence invested EUR 35 million in 2025 to add a fluff-pulp line capable of processing eucalyptus and agricultural residues interchangeably, creating switching flexibility that cushions raw-material volatility. European farmers receive EUR 600-800 per hectare in Common Agricultural Policy subsidies for perennial energy crops, translating to predictable farm-gate prices that stabilize supply contracts for converters. Over a multi-year horizon, diversified fiber sourcing thus serves as both a risk-mitigation lever and a marketing differentiator for consumer-packaged-goods brands.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Industrial-Scale Processing and Pulping Infrastructure | -1.5% | Global, acute in North America and Asia-Pacific | Short term (≤ 2 years) |

| Cost Competitiveness Relative to Established Fiber Source | -1.2% | Global | Medium term (2-4 years) |

| Technical Limitations in Barrier Properties and Functional Coatings | -0.8% | Global, regulatory pressure in Europe | Short term (≤ 2 years) |

| Absence of Standardized Certification Frameworks for Non-Wood Fibers | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Industrial-Scale Processing and Pulping Infrastructure

Worldwide, fewer than 15 commercial non-wood pulping lines are operational, compared with more than 400 wood-pulp mills, underscoring a glaring scale deficit that constrains rapid miscanthus uptake. ANDRITZ partnered with Genera in 2025 to commission the first dedicated U.S. grass-fiber line, yet the 18-to-24-month installation window means meaningful volumes will not reach converters until late 2027. Equipment costs exceed wood-pulp analogs by 25-30% because silica embedded in grasses accelerates digester wear, adding to start-up hurdles and complicating financing models. Minerals Technologies opened three molded-fiber satellites in 2025 that still rely on imported non-wood pulp, illustrating how downstream capacity can race ahead of upstream processing assets. Closing the infrastructure gap quickly is therefore pivotal for maintaining the current adoption trajectory.

Cost Competitiveness Relative to Established Fiber Source

Although miscanthus feedstock can be secured at EUR 80-120 (USD 88-132) per tonne in Europe, pulping and conversion consume extra energy and chemicals, eroding the nominal price edge established at the farm gate. Pactiv Evergreen’s EarthChoice clamshells, introduced in 2023, retail for USD 0.12-0.15 per unit compared with USD 0.08-0.10 for polystyrene equivalents, a premium that remains difficult for cost-sensitive operators outside regulatory hot spots. TekniPlex earmarked USD 350 million through 2026 to automate fiber-forming lines and expects to narrow the residual premium to 5-10%, yet still concedes full parity may not arrive before 2028. Smurfit WestRock is leveraging merged purchasing power to lock long-term grass-fiber contracts at fixed prices, but such multi-year commitments remain unavailable to smaller converters, preserving structural cost asymmetry. Ultimately, the economics improve most in applications where lightweighting reduces freight expense, allowing logistics savings to offset higher material inputs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Format: Clamshells Dominate, Protective Inserts Accelerate

Clamshell containers and trays commanded 42.34% of miscanthus-based packaging market share in 2025, fueled by quick-service restaurants that moved early to replace polystyrene hinged boxes ahead of the August 2026 plastic bans in Europe and several U.S. municipalities. Huhtamaki expanded molded-fiber capacity across nine global plants between 2024 and 2025, aligning supply with anticipated spikes in compliant packaging demand and reflecting confidence in grass-fiber scalability. Sabert’s Pulp-it! line posted 30% sales growth in Asia-Pacific institutional catering during 2024, showing that adoption momentum is no longer confined to European markets. However, growth in Europe is beginning to plateau as early adopters delay reorder cycles to synchronize with PFAS-free coating availability, indicating that future volume gains will rely more on geographic expansion than on per-operator penetration. Consequently, the miscanthus-based packaging market size for clamshells is expected to rise steadily but at a moderating pace compared with nascent application areas.

Protective packaging is on a steeper trajectory, projected to grow 9.78% annually through 2031 as e-commerce fulfillment centers and electronics brands phase out EPS void-fill in favor of compostable molded-fiber inserts compliant with ASTM D6400. Storopack debuted grass-fiber cushioning in 2024, and Cascades allocated more than 60% of its USD 350 million molded-fiber capital plan to protective formats, underscoring how converters are prioritizing this high-growth niche. Miscanthus fiber’s inherently lower density enables lighter inserts that trim dimensional-weight charges imposed by parcel carriers, providing a hard-dollar economic incentive on top of sustainability credentials. Technology partnerships such as Fiberdom and Kiefel’s dry-forming initiative, scheduled for Q2 2026 pilot runs, expand protective applications into cosmetics trays requiring precise surface finishes and tight tolerances. As automated high-speed lines come online, protective packaging is poised to eclipse foodservice formats as the primary growth driver within the overall miscanthus-based packaging market.

By End-Use Industry: Foodservice Leads, E-Commerce Surges

Foodservice accounted for 36.54% of the miscanthus-based packaging market share in 2025 because single-use plastic bans created a direct substitution mandate for quick-service restaurants and institutional caterers, especially across Europe and several coastal U.S. states. Capacity expansions at Huhtamaki, Genera, and Pactiv Evergreen have kept pace with demand, yet ordering patterns are beginning to moderate as buyers wait for PFAS-free grease barriers that become compulsory in August 2026. Graphic Packaging is channeling USD 85 million into cold-chain bowls and insulated meal containers, indicating that near-term foodservice growth will pivot toward formats needing higher thermal performance. Because many early adopters already completed first-wave conversions, incremental volume now hinges on new geographies rather than deeper penetration within existing customer accounts. Foodservice therefore remains a large revenue base, but its forward growth slope is less steep than in earlier years.

Retail and e-commerce applications are forecast to expand at a 12.34% CAGR through 2031, positioning the channel as the chief accelerator for the miscanthus-based packaging market over the forecast window. Amazon, Walmart, and Alibaba continue phasing out EPS void-fill, prompting converters such as Storopack and Cascades to prioritize protective inserts that satisfy ASTM D6400 compostability criteria while delivering equivalent drop-test performance. Footprint secured USD 100 million in Series E funding during 2024 to scale custom inserts that create premium unboxing experiences for electronics and cosmetics brands, demonstrating that design aesthetics now complement sustainability as a purchase driver. Stora Enso’s Performa Lumi, launched in January 2026, blends non-wood fibers into lightweight folding boxboard that targets beauty labels seeking to cut transport emissions by trimming substrate grammage. Lower fiber density translates into lighter parcels, and those freight savings partially offset the residual material premium, thereby strengthening the total cost of ownership narrative for retail and e-commerce stakeholders.

Geography Analysis

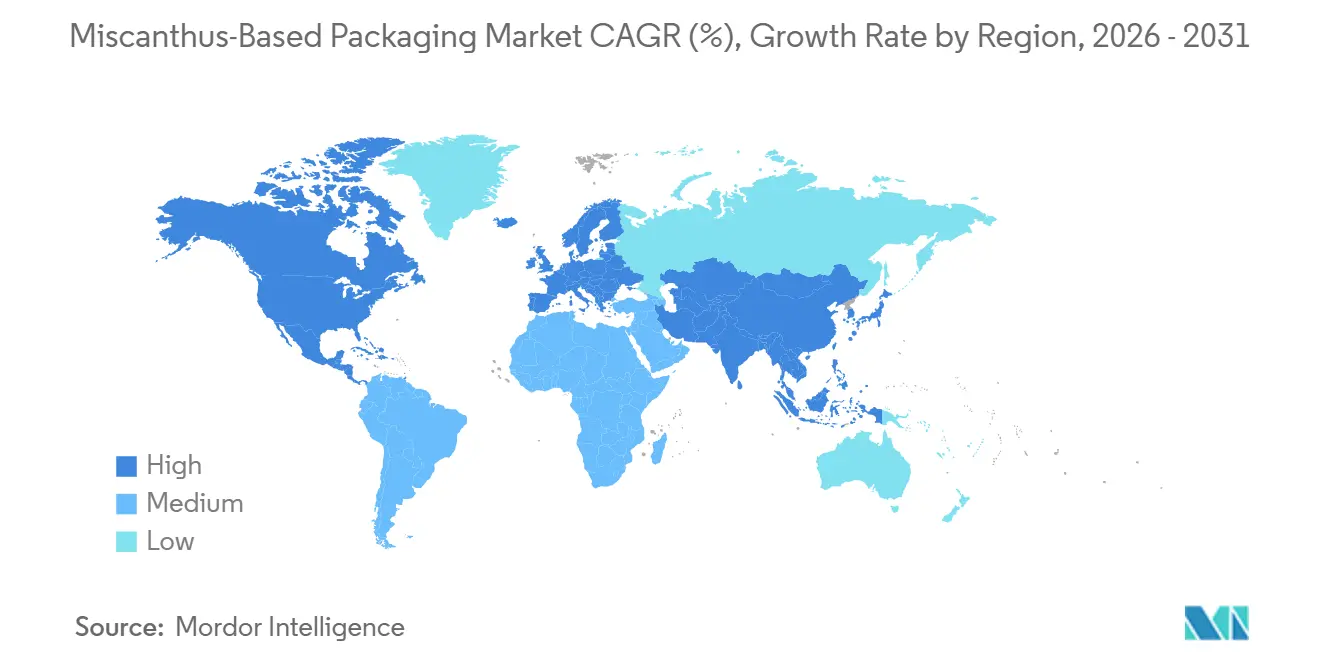

Europe retained a 38.21% revenue share in 2025, driven by a clear regulatory timetable that requires all packaging to be recyclable or compostable by 2030, forcing brands to lock in compliant supply well before enforcement. United Kingdom growers cultivated between 6,000 and 8,000 hectares of miscanthus in 2024, delivering feedstock under multiyear contracts to Fibrepac’s Lincolnshire plant that processes 10 000 tonnes annually using anaerobic-digestion power. Common Agricultural Policy subsidies pay farmers EUR 600-800 (USD 660-880) per hectare each year, underpinning stable farm-gate prices that de-risk long-term contracts for converters. Stora Enso’s 2025 minority stake in Matrix Pack grants immediate access to eight molded-fiber plants across three European subregions, tightening regional loops that cut logistics emissions. Institutional confidence is evident in the European Investment Bank’s EUR 20 million loan to PulPac for dry-forming automation that slices energy use by 65%, signaling continued backing for next-generation fiber technologies.[3]European Investment Bank, “EUR 20 Million Loan to PulPac,” eib.org

Asia-Pacific is projected to grow 10.45% annually through 2031 because more than USD 34 billion in fiber-packaging infrastructure is under construction, with China alone accounting for nearly USD 23 billion according to Minerals Technologies data. ASEAN members such as Vietnam and the Philippines already implemented extended producer responsibility in 2025, while Indonesia, Malaysia, and Thailand will finalize comparable mandates by 2027, creating a synchronized policy tailwind. Local miscanthus acreage remains small because biomass programs historically favored bamboo and switchgrass, so many converters rely on imported pulp, which lifts landed costs above European benchmarks. Matrix Pack’s Thai facility offers a partial hedge by shortening delivery routes for Southeast Asian foodservice buyers, yet consistent feedstock supply still depends on expanded regional cultivation. Governments are beginning pilot programs on marginal land, but meaningful scale may not materialize until the latter half of the forecast period.

North America is at an earlier commercialization stage, yet anchor investments point toward rapid catch-up once processing bottlenecks ease. Genera completed a USD 340 million expansion in Tennessee during 2025, creating the world’s largest grass-fiber packaging line with capacity exceeding 2 billion units annually. Seven U.S. states impose producer fees on non-recyclable packaging, pushing national restaurant chains and e-commerce retailers to trial molded fiber in coastal markets before rolling out inland. Better Earth’s Farmer’s Fiber Collection sources miscanthus directly from growers in the Midwest, pairing feedstock traceability with predictable pricing, while USDA cost-share grants lower establishment hurdles for new perennial biomass acreage.[4]USDA NRCS, “Cost-Share Programs for Perennial Biomass Crops,” nrcs.usda.gov Canada and Mexico monitor these developments but currently lack dedicated non-wood pulping lines, suggesting cross-border supply will dominate near-term trade flows. South America and the Middle East and Africa remain marginal today, although policymakers in Brazil and the United Arab Emirates are assessing European regulations as potential blueprints for future circular-economy initiatives.

Competitive Landscape

The miscanthus-based packaging market remains fragmented because fewer than ten pure-play converters operate at commercial scale, and the largest participant controls under 15% of global revenue. Genera exemplifies vertical integration by managing cultivation, pulping, and conversion within a single Tennessee complex, which allows tight cost control and rapid design iterations tailored to local customer feedback. Fibrepac follows a similar model in the United Kingdom, but differentiates itself by powering operations with on-site anaerobic digestion, closing energy loops and appealing to buyers that audit Scope 1 emissions. These vertically integrated pioneers highlight a strategy where geographic proximity to feedstock and renewable energy inputs provides both cost and carbon advantages that larger incumbents cannot immediately replicate. However, scaling beyond regional footprints will still require partnerships with distributors that can unlock multinational restaurant and retail contracts.

Large fiber-packaging incumbents are entering through minority-equity stakes and technology partnerships instead of building grass-fiber mills from scratch, thereby spreading capital risk. Stora Enso’s investment in Matrix Pack gives immediate access to eight molded-fiber facilities across the United States, United Kingdom, Greece, Bulgaria, and Thailand, enabling accelerated integration of miscanthus without the multi-year lead times of greenfield construction. SIG’s collaboration with PulPac focuses on developing carton closures composed of more than 90% paper, opening a billion-unit addressable market that previously relied on high-density polyethylene caps. Archroma’s PFAS-free Cartaseal OGB F10 and Michigan State University’s KIT 7-12 coating have become preferred barrier chemistries, illustrating how intellectual property around functionality is beginning to shape competitive advantage. The result is an ecosystem where converters, chemical innovators, and equipment suppliers form tight consortia to accelerate time-to-market for compliant products.

Technology providers such as PulPac and ANDRITZ are carving out influential positions because their dry-forming and grass-fiber digestion systems determine production economics for the wider industry. PulPac secured a EUR 20 million (USD 22 million) European Investment Bank loan and an OPTIMA equity injection in June 2025, funds earmarked for scaling equipment that achieves 3.5-second cycle times, which dramatically lowers unit energy consumption versus wet molding. ANDRITZ installed the first dedicated U.S. grass-fiber pulping line for Genera, proving that existing hardware expertise can be adapted to high-silica feedstocks with manageable wear-part costs. These vendors increasingly bundle automation, quality monitoring, and barrier-coating modules, turning capital equipment into a one-stop platform that lowers onboarding friction for new market entrants. As intellectual property around rapid forming and PFAS-free coatings matures, licensing structures may further consolidate bargaining power in favor of technology owners.

Miscanthus-Based Packaging Industry Leaders

Genera Inc.

Fibrepac

Mohawk (Fedrigoni Group)

The Green Revolution BV

Better Earth LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Emerald Ecovations expanded its Arkansas facility by 75,000 square feet, doubling miscanthus processing capacity to 20,000 tonnes annually.

- January 2026: Stora Enso launched Performa Lumi lightweight boxboard incorporating non-wood fibers for beauty and personal-care brands.

- November 2025: TIPA acquired SEALPAP, adding rigid molded formats to its compostable portfolio.

- November 2025: Ence began commercial production on a EUR 35 million (USD 38 million) fluff-pulp line processing eucalyptus and agricultural residues interchangeably.

- November 2025: Genera and ANDRITZ commissioned a grass-fiber line in Tennessee as part of Genera’s USD 340 million expansion.

Global Miscanthus-Based Packaging Market Report Scope

The Miscanthus-Based Packaging Market Report is Segmented by Packaging Format (Clamshell Containers and Trays, Plates and Bowls, Protective Packaging, and Other Packaging Formtas), End-Use Industry (Foodservice, Personal Care and Cosmetics, Retail and E-Commerce, Food and Beverage, and Other End-Use Industries), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Clamshell Containers and Trays |

| Plates and Bowls |

| Protective Packaging (Cushioning, Inserts) |

| Other Packaging Formats |

| Foodservice |

| Personal Care and Cosmetics |

| Retail and E-commerce |

| Food and Beverage |

| Other End-use Industries |

| North America |

| Europe |

| Asia-Pacific |

| South America |

| Middle East and Africa |

| By Packaging Format | Clamshell Containers and Trays |

| Plates and Bowls | |

| Protective Packaging (Cushioning, Inserts) | |

| Other Packaging Formats | |

| By End-use Industry | Foodservice |

| Personal Care and Cosmetics | |

| Retail and E-commerce | |

| Food and Beverage | |

| Other End-use Industries | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| South America | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the current size and projected growth of the miscanthus-based packaging market?

The market stands at USD 78.53 million in 2026 and is expected to reach USD 115.67 million by 2031, reflecting an 8.05% CAGR.

Which application area is forecast to grow fastest through 2031?

Retail and e-commerce protective packaging is projected to expand at a 12.34% CAGR, outpacing foodservice and other segments.

Why are companies blending miscanthus with other fibers instead of using wood pulp alone?

Grass fibers hedge volatile wood-pulp prices, enhance regenerative agriculture narratives, and deliver lighter packaging that lowers parcel freight costs.

How do PFAS regulations influence material and coating choices?

Imminent European limits ban fluorochemical treatments, so converters are adopting PFAS-free coatings such as Archroma’s Cartaseal OGB F10 to maintain grease and moisture resistance.

Where are the largest infrastructure gaps for miscanthus pulping today?

Asia-Pacific and North America face the most acute shortfalls, because fewer than fifteen non-wood pulping lines operate worldwide and many new molded-fiber plants still import pulp.

What strategies are leading companies using to secure reliable feedstock?

Vertical integrators like Genera cultivate their own grass crops, while groups such as Stora Enso form equity partnerships with existing molded-fiber plants to embed miscanthus into blended formulations.

Page last updated on: