Eco-friendly Food Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

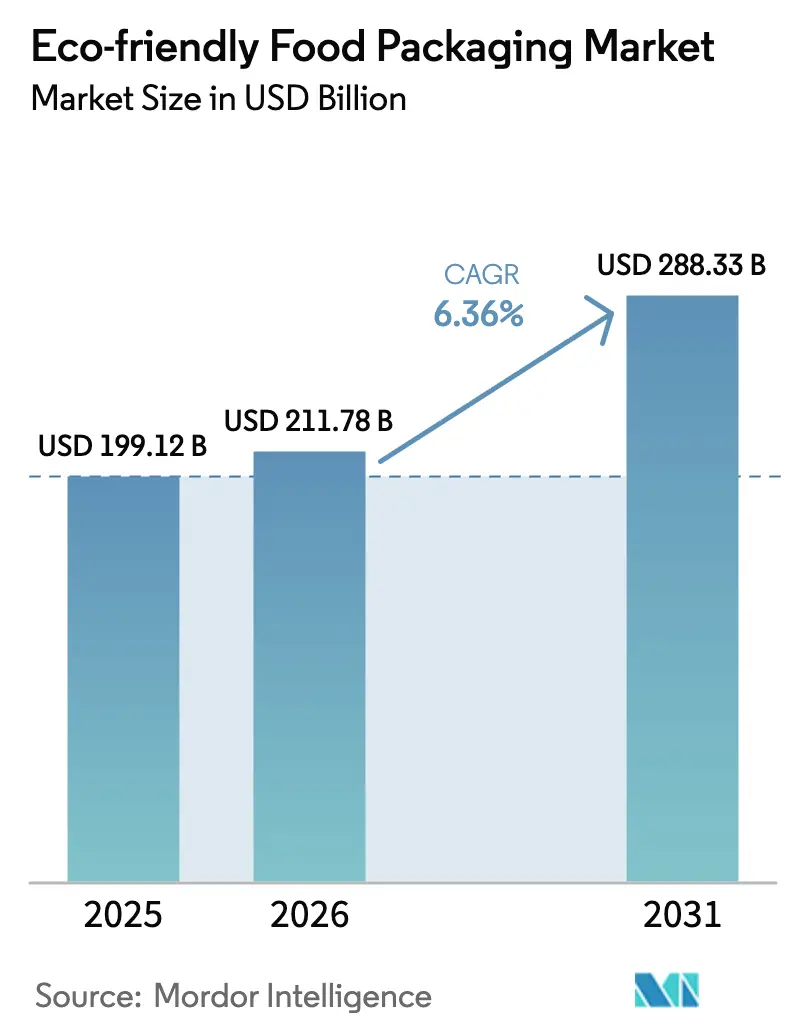

| Market Size (2026) | USD 211.78 Billion |

| Market Size (2031) | USD 288.33 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Eco-friendly Food Packaging Market Analysis by Mordor Intelligence

The eco-friendly food packaging market size was valued at USD 199.12 billion in 2025 and estimated to grow from USD 211.78 billion in 2026 to reach USD 288.33 billion by 2031, at a CAGR of 6.36% during the forecast period (2026-2031). Widening legislative mandates, breakthrough materials science and measurable consumer preference shifts are simultaneously re-wiring procurement decisions across brand owners, retailers and food-service operators in every major region. Regulatory measures—from the European Union’s Regulation 2025/351 to the U.S. Food & Drug Administration’s withdrawal of 35 PFAS food-contact clearances—are giving clear market signals that accelerate the substitution of legacy plastics. Technology adoption trends now include AI-driven “right-weight” design, fiber-based high-barrier laminates and integrated freshness sensors that extend shelf life, reduce waste and shrink total cost of ownership. Capital formation is flowing into recycled PET capacity in Asia and Latin America, molded fiber automation in Europe, and biodegradable polymer scale-up in North America, collectively reinforcing the eco-friendly food packaging market’s upward trajectory. Investors view the category as a resilient adjacency to core food production, underpinned by policy certainty and a demonstrable path to cost parity for multiple substrates.

Key Report Takeaways

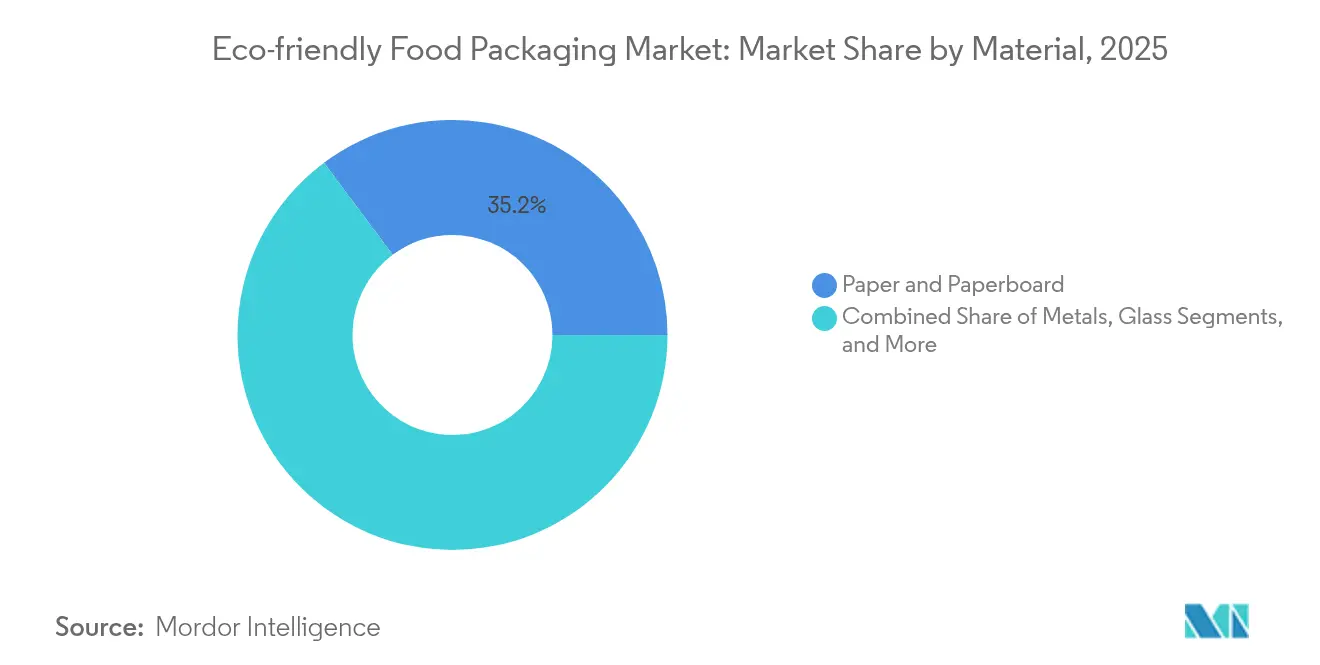

- By material, paper and paperboard led with 35.20% of eco-friendly food packaging market share in 2025, whereas bioplastics are expanding at a 9.52% CAGR through 2031.

- By food product, bakery and confectionery captured 30.10% of the eco-friendly food packaging market size in 2025, while ready-to-eat convenience meals are forecast to climb at a 10.28% CAGR to 2031.

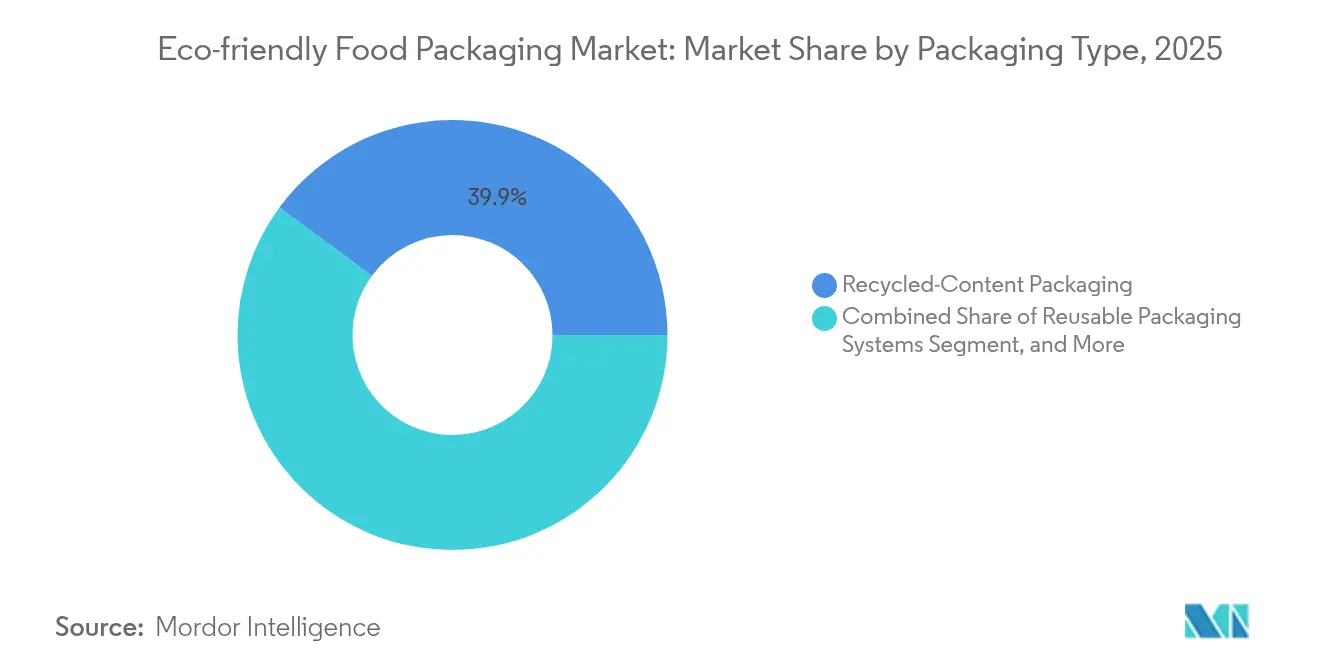

- By packaging type, recycled-content solutions accounted for 39.90% share of the eco-friendly food packaging market size in 2025; active and intelligent eco-packs are advancing at a 9.58% CAGR during the outlook period.

- By end-user, food manufacturers and processors held 49.60% share of the eco-friendly food packaging market in 2025, yet quick-service and casual restaurants register the fastest growth at 10.06% CAGR.

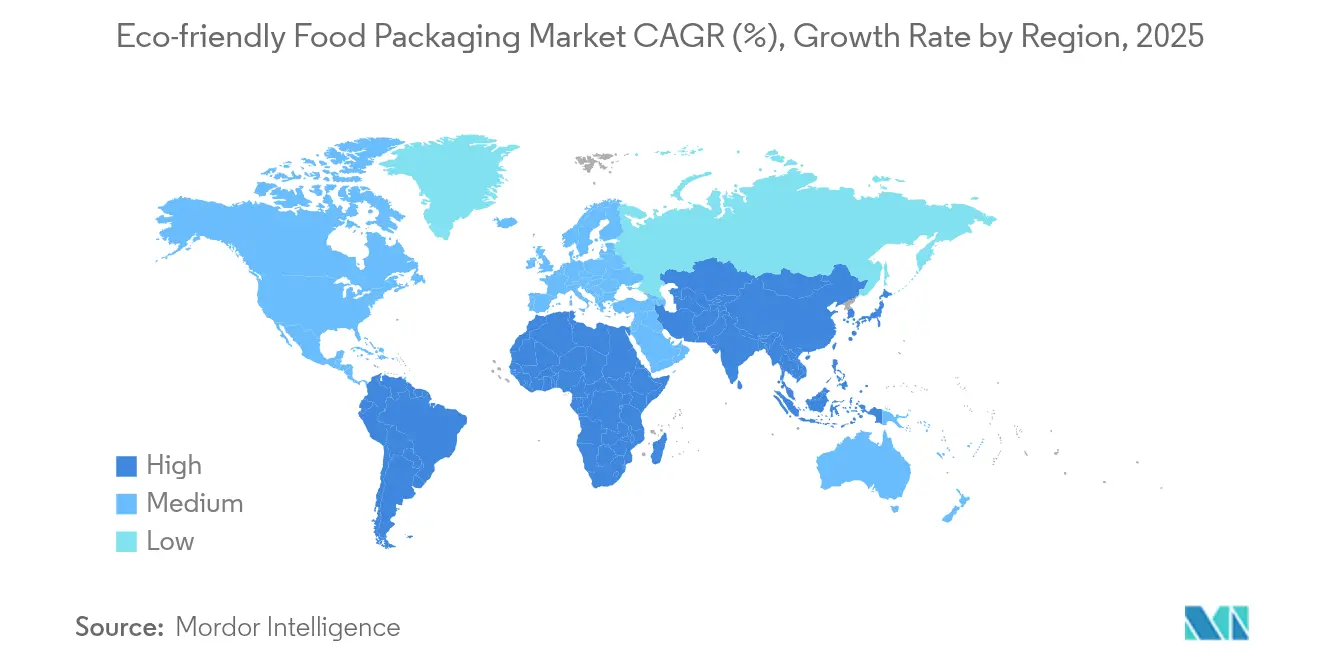

- By geography, North America retained 37.10% share of the eco-friendly food packaging market in 2025, while Asia-Pacific remains the quickest-growing region at a 10.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Eco-friendly Food Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on single-use plastics | +1.8% | Global; early rollout in EU, California, Australia | Short term (≤ 2 years) |

| Retailer scorecards favoring circularity | +1.2% | North America, EU, extending to Asia-Pacific | Medium term (2-4 years) |

| Price parity for recycled PET and paperboard | +0.9% | United States, Germany, Japan, selective Asia-Pacific markets | Short term (≤ 2 years) |

| Food-grade rPET build-out in Asia & LatAm | +0.7% | India, Indonesia, Brazil, Mexico | Medium term (2-4 years) |

| AI-enabled “right-weight” design | +0.5% | Global; early adoption in North American QSR chains | Medium term (2-4 years) |

| Waste-buyback models for agri-biomass | +0.3% | North America, EU, emerging Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans on Single-Use Plastics

Coordinated policy action has reached a tipping point. The EU’s Regulation 2025/351, enforced in March 2025, introduces stricter purity thresholds, traceability obligations and migration limits for plastic food-contact materials, effectively pushing converters toward recycled or bio-based inputs. Complementary measures inside the Packaging and Packaging Waste Regulation set phased recycling targets and prohibit several single-use formats by 2030, moving producers toward fully recyclable or compostable formats. In parallel, Australia’s statewide bans on polystyrene food containers and barrier bags, effective September 2024, prove the global contagion effect of regulation.[1]South Australia Government, “Single-use plastic products prohibited from September 1 2024,” replacethewaste.sa.gov.au Brand owners now redirect capital expenditure into compliant substrates, reshaping converter tendering processes and accelerating line changeovers. The net effect is rapid demand expansion in compliant materials, lifting overall eco-friendly food packaging market demand even before consumer preferences are factored in.

Shifting Retailer Scorecards Toward Circular Packaging

Institutional buyers—led by Walmart and Target—have integrated circularity metrics into supplier evaluations, turning sustainability from a marketing objective into a revenue-qualifying requirement. Scorecards gauge recycled-content percentages, end-of-life recovery rates and greenhouse-gas reductions, incentivizing suppliers to adopt recyclable mono-material laminates and low-carbon inputs. Collaborative platforms such as Amcor’s Lift-Off initiative allocate up to USD 500,000 per startup to accelerate breakthrough concepts. Producers see clear return on investment: corrugated produce trays deliver 35% lower shrink versus clamshells, enabling retailers to recoup premium material costs through waste savings. As leading retailers expand their private-label assortments, suppliers unprepared for circularity risk delisting, establishing a structural demand lift for eco-friendly packaging across multiple grocery categories.

Price Parity Achieved for Recycled PET and Paperboard

Economies of scale, better collection rates and upgraded wash-flake processes have drawn rPET prices into parity with virgin PET in 15 jurisdictions, including the United States, Germany and Japan. PT Amandina Bumi Nusantara’s 42,000-tonne annual facility in Indonesia supplies Coca-Cola’s 100% rPET bottles at competitive prices, illustrating how targeted infrastructure supports global beverage commitments. Similar capacity adds by Ganesha Ecopet in India have reduced feedstock risk and improved raw-material cost predictability. Paperboard has followed suit as water-based barrier coatings eliminate performance gaps and comply with PFAS regulations. Price convergence neutralizes a key objection to recycled inputs, reinforcing their role in the eco-friendly food packaging market.

Food-Grade rPET Capacity Build-Out in Asia and Latin America

Extended Producer Responsibility (EPR) mandates now require 30% recycled content in PET bottles in India by 2025, escalating to 60% by 2029, driving local feedstock demand. New decontamination installations in Indonesia, Brazil and Mexico deploy enhanced sorting and super-clean recycling modules to meet stringent food-safety criteria. Decentralized capacity reduces freight emissions by situating wash plants near consumption centers. Multinationals lock in offtake agreements to secure resin supply, leading to multi-year price visibility and supporting scaled roll-outs of recycled-content packaging across carbonated soft drinks, dairy and sauces. The wave of installations underpins a sustained raw-material funnel for the eco-friendly food packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bio-resin cost volatility | –1.4% | Global; pronounced where sugarcane & corn must be imported | Short term (≤ 2 years) |

| Infrastructure gaps for multilayer flexibles | –0.8% | Worldwide; acute in emerging Asia-Pacific | Long term (≥ 4 years) |

| Food-contact compliance delays | –0.5% | North America, EU, selective Asia-Pacific | Medium term (2-4 years) |

| Greenwashing litigation exposure | –0.3% | North America, EU, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Volatility of Bio-Resins Tied to Sugarcane and Corn Futures

Sugarcane and corn futures swung 25–30% in 2024, directly affecting polylactic acid (PLA) and polyhydroxyalkanoate (PHA) production costs. Aviation biofuel expansion intensifies competition for feedstocks, while climate-related crop variability amplifies price shocks. Converters hold only limited hedging tools, translating volatility into unpredictable quotes for brand owners. Manufacturers mitigate impact through second-generation feedstocks such as corn stover-derived ethanol, yet industrial-scale output remains limited. The uncertainty tempers rapid substitution of fossil polymers, introducing friction into eco-friendly food packaging market adoption curves.

Recycling Infrastructure Bottlenecks for Multilayer Flexibles

Multilayer films deliver moisture and oxygen barriers essential for shelf-life, but 83% remain incompatible with conventional mechanical recycling. Chemical recycling pilots show promise yet face scaling challenges, regulatory scrutiny and elevated capex. India’s Design for Recycling Guidance pushes mono-material structures, but the retrofit cycle for laminated snack packaging remains lengthy. Without infrastructure parity, flexible formats risk regulatory penalties and brand-owner phase-outs, restraining the eco-friendly food packaging market’s full potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Paper Strength Meets Bioplastic Momentum

Paper and paperboard captured 35.20% of eco-friendly food packaging market share in 2025, a position built on robust recycling networks and consumer familiarity. The eco-friendly food packaging market size for paper substrates is projected to grow steadily as high-barrier coatings give fiber formats moisture, grease and oxygen resistance approaching that of legacy plastics. Amcor’s AmFiber Performance Paper, patented in January 2025, offers PVDC-free, multilayer functionality while preserving curbside recyclability. Capital investment now flows into extrusion-coated cup stock and molded-fiber forming lines, reinforcing paper’s baseline dominance.

Bioplastics exhibit the fastest trajectory at 9.52% CAGR, propelled by life-cycle performance gains and widening compostability mandates. Corbion’s PLA expansion strategy in Asia-Pacific, for example, integrates regional feedstock sources to cut logistics emissions. Biopolymer producers are refining crystallinity for microwave-ready trays while reducing oxygen transmission rates to protect high-fat foods. Metals, glass and edible films round out the material spectrum, each serving premium or niche performance needs in the broader eco-friendly food packaging market.

By Food Product: Convenience Culture Catalyzes Packaging Shifts

Bakery and confectionery applications accounted for 30.10% of eco-friendly food packaging market size in 2025, leveraging paper-based wrappers and recyclable thermoforms that align with premium branding. Mondelez’s rollout of paper multipacks demonstrates momentum, replacing oriented polypropylene flow-wraps without compromising barrier performance. In the meat, fish and poultry segment, vacuum shrink bags adopt thinner gauges and higher recycled-content films, meeting carbon-footprint targets while extending shelf life.

Ready-to-eat convenience meals sit at the apex of growth with 10.28% CAGR, driven by urbanization and on-the-go eating patterns. QSR chains and chilled-meal producers favor molded fiber bowls and industrially compostable cutlery to comply with plastic bans, accelerating substrate transition in this high-volume category. Dairy, frozen desserts, and fresh produce show incremental growth as barrier technologies improve and retail initiatives promote mono-material trays. Together these shifts underpin a diversified demand profile within the eco-friendly food packaging market.

By Packaging Type: Intelligence Infuses Sustainable Formats

Recycled-content solutions dominated at 39.90% in 2025 as EPR statutes and brand pledges converge on minimum-recycled thresholds. Mondelez’s Cadbury range now features 80% certified recycled plastic wrappers, reflecting a tangible design-for-circularity milestone. Reusable containers, supported by deposit schemes, slowly scale in beverage and quick-service channels, while degradable and compostable systems gain traction for foodservice disposables.

Active and intelligent eco-packs are the fastest-growing class, posting a 9.58% CAGR as printed electronics, spoilage sensors and antimicrobial layers merge with recyclable substrates. Smart labels allow distributors to dynamically manage temperature excursions, cutting shrink and boosting the eco-friendly food packaging market’s value proposition. Edible coatings remain exploratory yet promising, particularly in fresh-cut produce, where wipe-on pullulan films delay browning without landfill impact.

By End-Users: Restaurants Push Front-of-House Transformation

Food manufacturers and processors held 49.60% share in 2025, anchoring the eco-friendly food packaging market through multi-year supply agreements and high-volume demand for film, rigid, and flexible formats. Their investments focus on integrating rPET and paper solutions at scale, backed by automated filling infrastructure upgrades.

Quick-service and casual restaurants, growing at 10.06% CAGR, wield disproportionate influence because packaging is frontline consumer touchpoint. McDonald’s lid-free dessert cups and Huhtamaki-supplied fiber hot cups exemplify visible sustainability cues that shape public perception. Institutional caterers and modern grocery retailers mirror these shifts, embedding compostable trays and recyclable thermoforms into their assortments. The cascading effect cements long-term volume growth inside the eco-friendly food packaging market.

Geography Analysis

North America retained a 37.10% stake in the eco-friendly food packaging market in 2025, underpinned by early PFAS restrictions, GSA single-use plastic curbs and robust curbside recycling infrastructure. Federal-level clarity emboldens converters to accelerate capital deployment for mechanical recycling upgrades, while state initiatives in California and Maine fast-track fluorochemical phase-outs. Major brand owners headquartered in the region further reinforce demand through aggressive public commitments and rapid SKU conversions.

Europe sustains momentum via stringent legislative frameworks, notably the Packaging and Packaging Waste Regulation that mandates incremental recycling targets and design-for-reuse provisions. Country-specific actions, such as Germany’s reusable requirement for take-away food and drinks, drive local innovation in molded fiber lids and glass jar leasing schemes. High public environmental awareness, combined with mature segregation systems, allows Europe to pilot complex circular models at scale, sustaining its critical role within the global eco-friendly food packaging market.

Asia-Pacific is projected to record a 10.75% CAGR through 2031, the fastest across regions. Rapid EPR adoption, capacity investments in bottle-to-bottle rPET and government subsidies for high-barrier paperboard lines coalesce to position India, Indonesia and Vietnam as rising hubs of manufacturing innovation. PT Amandina’s monthly 3,000-tonne recycled-resin output feeds national and export markets, ensuring feedstock availability for brand commitments. Infrastructure growth is complemented by rising disposable incomes and evolving consumer attitudes toward environmental stewardship, collectively expanding the eco-friendly food packaging market size in the region.

Competitive Landscape

The eco-friendly food packaging market remains moderately fragmented, though consolidation is accelerating as players chase scale benefits and technology portfolios. Amcor, Mondi and Sealed Air deepen vertical integrations—Amcor inked a mechanically recycled polyethylene supply pact with NOVA Chemicals to secure feedstock, while Mondi allied with traceless for agricultural residue coatings.[3]Mondi, “Mondi and traceless team up to develop a ground-breaking coating solution from agricultural by-products,” mondigroup.com Active corporate venturing is evident: Amcor’s Lift-Off funnels up to USD 3 million annually into startups such as Bloom Biorenewables, whose lignin-based intermediates aim to displace fossil aromatics.

Strategic moves underscore technology leadership. Metsä Group partners with Amcor to commercialize molded-fiber trays capable of hot-fill, aligning fiber supply strength with converting expertise. Dow collaborates with New Energy Blue for corn-stover-derived polyethylene, enabling brands to cut Scope 3 emissions without feedstock price exposure. Huhtamaki unites with Xampla to deliver PFAS-free grease-barrier coatings for take-away segments, mitigating regulatory risk in fluorochemical hotspot states.

Patent filings concentrate around high-barrier, recycle-ready paper and retort pouches, as well as antimicrobial peptides anchored within bio-based matrices. New entrants exploit niche technologies: Bpacks uses bark fibers for rigid containers, securing EUR 1 million to scale pilot capacity. Industry incumbent advantage persists in distribution reach and integrated substrate portfolios, yet nimble innovators influence incumbent R&D budgets, elevating overall innovation cadence across the eco-friendly food packaging market.

Eco-friendly Food Packaging Industry Leaders

Huhtamaki Oyj

Amcor PLC

Smurfit WestRock

International Paper

Mondi Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Metsä Group and Amcor announce strategic alliance to commercialize molded-fiber food packaging solutions.

- April 2025: Bloom Biorenewables closes USD 14 million Series A as Amcor Lift-Off winner to upscale lignin-based PET enhancements.

- March 2025: EU Regulation 2025/351 on plastic food-contact material purity enters force, compliance due September 2026.

- February 2025: Dow and New Energy Blue unveil corn-residue-based polyethylene project in Iowa targeting 275,000-tonne feedstock.

Global Eco-friendly Food Packaging Market Report Scope

Eco-friendly food packaging refers to packaging materials and designs that minimise environmental impact throughout their lifecycle. These packaging solutions are typically made from renewable, recyclable, or biodegradable materials. They aim to reduce waste, conserve resources, and lower carbon emissions associated with production, transportation, and disposal processes. Eco-friendly food packaging often incorporates sustainable practices such as using recycled content, minimising material usage, and designing for easy recycling or composting.

The eco-friendly food packaging market is segmented by material (paper and paperboard, plastic, metal, glass), by application (bakery confectionery products, convenience foods, meat, fish, and poultry, fruits and vegetables, dairy products and other food products) by packaging type (recycled content packaging, degradable packaging market, reusable packaging), by geography (North America [United States, Canada], Europe [Germany, United Kingdom, France, Spain and Rest of Europe], Asia [China, Japan, India, Australia and New Zealand, Rest of Asia Pacific], Latin America [Brazil, Mexico, Columbia, Rest of Latin America], the Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa and Rest of Middle East and Africa]) The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Paper and Paperboard |

| Recycled Plastics (rPET, rPE, rPP) |

| Bioplastics (PLA, PHA, PBS) |

| Biodegradable/Compostable Fiber Moulded |

| Metals (Aluminium, Steel) |

| Glass |

| Edible Films and Coatings |

| Bakery and Confectionery |

| Dairy and Frozen Desserts |

| Meat, Fish and Poultry |

| Fruits and Vegetables |

| Ready-to-Eat/Convenience Meals |

| Sauces, Dressings and Condiments |

| Other Food Product |

| Recycled-Content Packaging |

| Reusable Packaging Systems |

| Degradable/Compostable Packaging |

| Active and Intelligent Eco-packs |

| Edible Packaging |

| Food Manufacturers and Processors |

| Quick-Service and Casual Restaurants |

| Other End-users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material | Paper and Paperboard | ||

| Recycled Plastics (rPET, rPE, rPP) | |||

| Bioplastics (PLA, PHA, PBS) | |||

| Biodegradable/Compostable Fiber Moulded | |||

| Metals (Aluminium, Steel) | |||

| Glass | |||

| Edible Films and Coatings | |||

| By Food Product | Bakery and Confectionery | ||

| Dairy and Frozen Desserts | |||

| Meat, Fish and Poultry | |||

| Fruits and Vegetables | |||

| Ready-to-Eat/Convenience Meals | |||

| Sauces, Dressings and Condiments | |||

| Other Food Product | |||

| By Packaging Type | Recycled-Content Packaging | ||

| Reusable Packaging Systems | |||

| Degradable/Compostable Packaging | |||

| Active and Intelligent Eco-packs | |||

| Edible Packaging | |||

| By End-Users | Food Manufacturers and Processors | ||

| Quick-Service and Casual Restaurants | |||

| Other End-users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the eco-friendly food packaging market?

The market reached USD 211.78 billion in 2026 and is projected to climb to USD 288.33 billion by 2031.

Which material leads the eco-friendly food packaging market?

Paper and paperboard led with 35.20% share in 2025, supported by mature recycling systems and new high-barrier technologies.

Which segment is growing fastest by food product?

Ready-to-eat convenience meals are expanding at a 10.28% CAGR as quick-service restaurants and meal-kit brands pursue compostable and recyclable formats.

Why is Asia-Pacific the fastest-growing region?

Regulatory adoption, large-scale rPET capacity investments and rising consumer eco-awareness combine to drive a 10.75% regional CAGR.

What are the major restraints for the market?

Key restraints include bio-resin feedstock price volatility, limited recycling infrastructure for multilayer flexibles, and compliance delays for next-generation coatings.

How are leading companies sustaining a competitive edge?

Market leaders invest in vertical integration, patentable barrier innovations and venture funding of start-ups to secure feedstock, technology and intellectual-property advantages across the value chain.

Page last updated on: