Shelf Stable Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

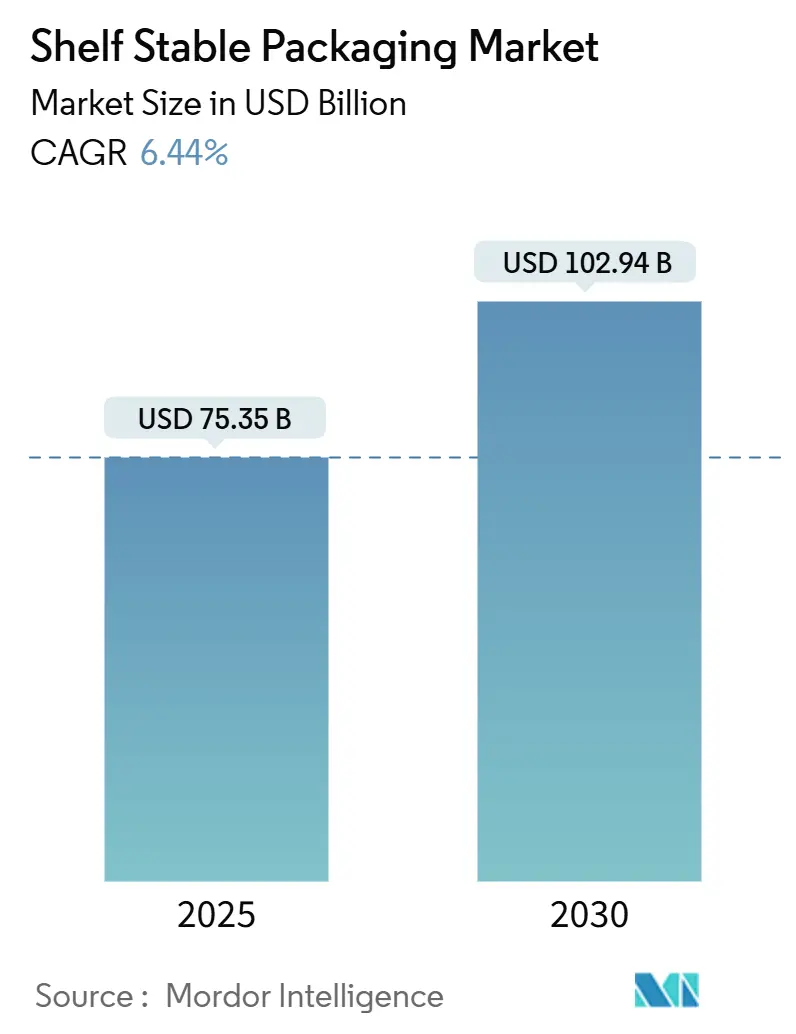

| Market Size (2025) | USD 75.35 Billion |

| Market Size (2030) | USD 102.94 Billion |

| Growth Rate (2025 - 2030) | 6.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Shelf Stable Packaging Market Analysis by Mordor Intelligence

The global Shelf Stable Packaging market size reached USD 75.35 billion in 2025 and is projected to increase to USD 102.94 billion by 2030, reflecting a 6.44% CAGR over the forecast period. Strong demand for ambient formats that avoid refrigerated logistics, rapid e-commerce adoption, and regulatory pressures to curb food waste are reshaping competitive dynamics in the s market. Manufacturers are redirecting capital toward aseptic and retort lines that preserve nutrients while extending shelf life, and converters are scaling up mono-material designs that withstand parcel shipping yet remain recyclable. Technology convergence, encompassing digital watermarking, edible barrier coatings, and high-barrier paper substrates, continues to open white-space opportunities, particularly for mid-sized innovators seeking licensing deals with global food brands. Major players are consolidating to secure resin supply and filling equipment, while regional specialists carve out share by offering low-minimum-order digital printing and fast-turn customization.

Key Report Takeaways

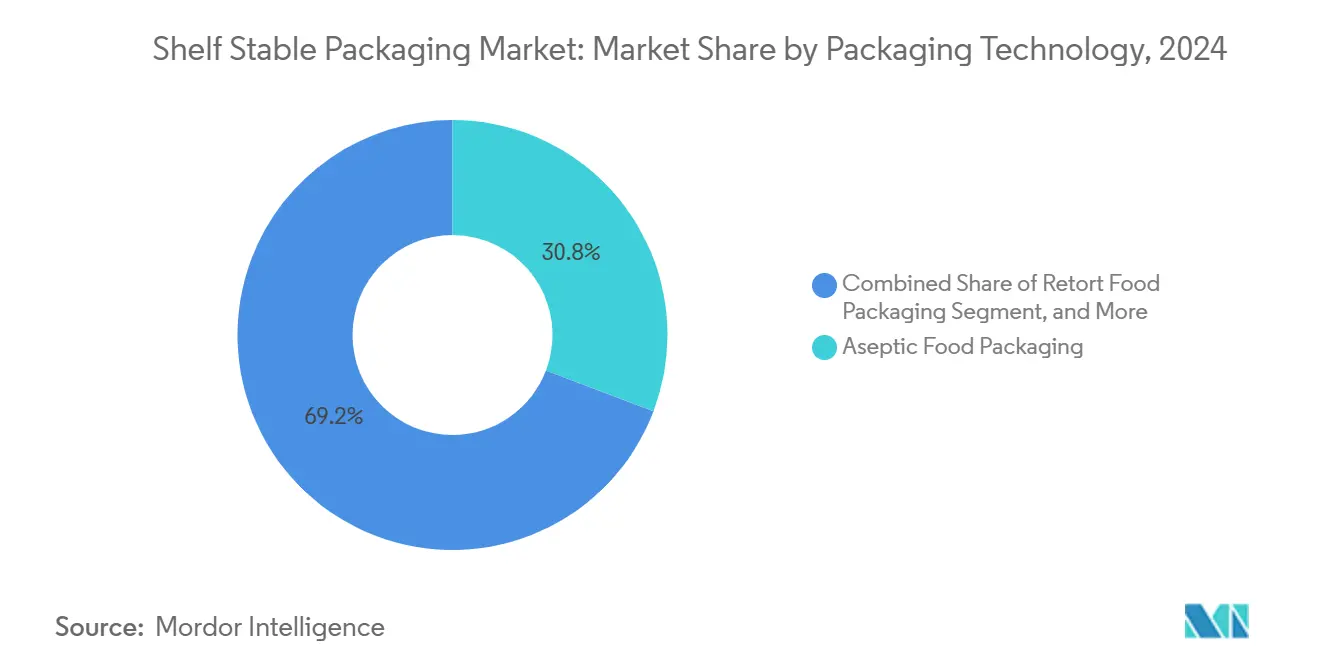

- By packaging technology, aseptic processing led with a 30.77% revenue share in 2024, and is forecast to grow at an 8.23% CAGR through 2030.

- By packaging format, flexible configurations captured 58.42% of the shelf-stable packaging market share in 2024 and are projected to advance at an 8.32% CAGR over the same period.

- By product type, pouches held a 38.42% revenue share in 2024; cartons are the fastest-growing segment, expanding at a 7.83% CAGR to 2030.

- By application, juice packaging is projected to experience the highest growth rate of 8.51% annually from 2025 to 2030.

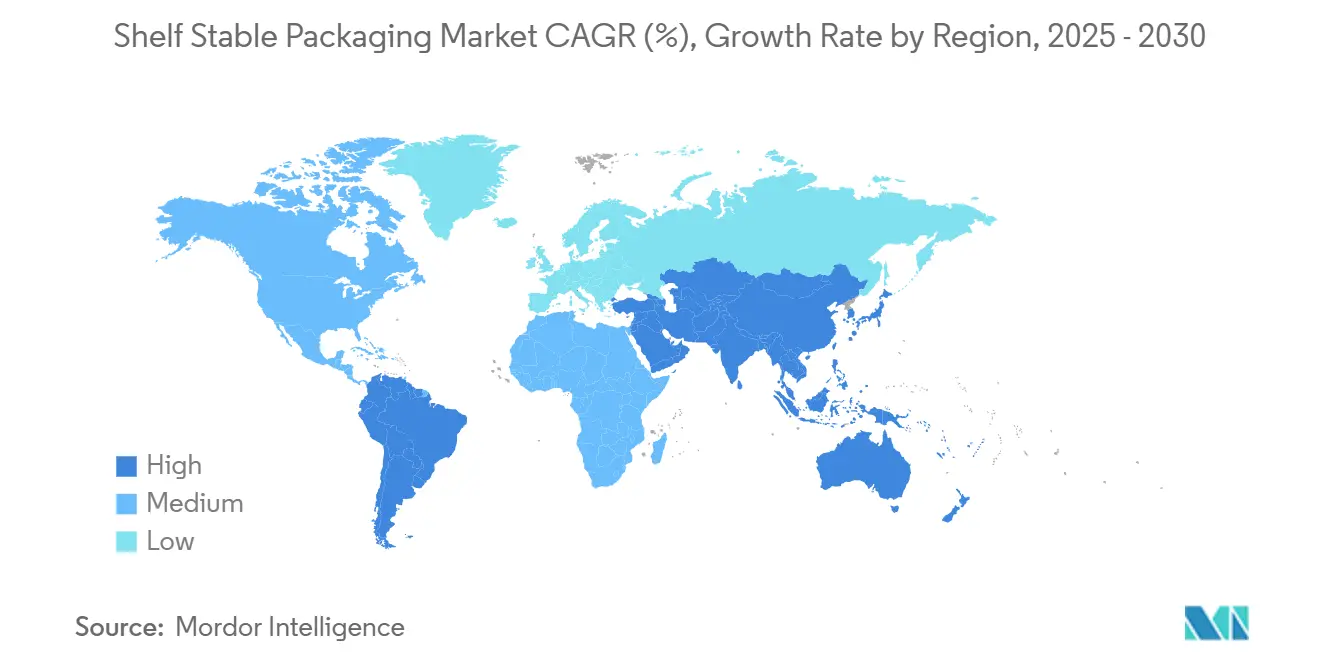

- By geography, the Asia-Pacific region dominated with 40.21% revenue in 2024 and is expected to expand at a 9.12% CAGR through 2030.

Global Shelf Stable Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand to Reduce Cold Chain Logistics Costs | +1.2% | Asia-Pacific, Middle East and Africa, Latin America | Medium term (2-4 years) |

| Growing Demand for Ready-to-Eat Food and Changing Consumer Lifestyle | +1.5% | Global, concentration in North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| E-Commerce Growth Driving Shelf-Ready Configurations | +0.9% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Regulatory Push for Food Waste Reduction | +0.8% | Europe, North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Emergence of Edible Barrier Coatings for Extended Shelf Life | +0.4% | North America, Europe pilot markets | Long term (≥ 4 years) |

| Integration of Digital Watermarks for Supply Chain Traceability | +0.3% | Europe, North America, select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand to Reduce Cold Chain Logistics Costs

Cold chain operations account for up to 40% of total distribution expenses in perishable categories, so brand owners are shifting toward ambient formats that eliminate the need for refrigeration. In India, cold chain penetration covers less than 10% of the country's agricultural output, prompting dairy cooperatives to install ultra-high-temperature lines that transport milk 600 kilometers without spoilage.[1]Tetra Pak, “Sustainability Update 2024,” TetraPak.com Energy price spikes drove up European refrigerated transport costs by 18% in 2024, prompting retailers to relaunch soups, sauces, and plant-based drinks in ambient aisles. Across Asia-Pacific, ambient packs now represent more than 60% of new stock-keeping units for sauces and ready meals, and the Shelf Stable Packaging market is capturing this redirected capex as firms upgrade filling halls rather than refrigerated warehouses.

Growing Demand for Ready-to-Eat Food and Changing Consumer Lifestyle

Global urbanization and the rise of dual-income households are driving a surge in heat-and-eat meals that fit seamlessly into work-from-anywhere routines. The United States Department of Agriculture reported a 12% year-over-year increase in packaged-meal spending in 2024. [2]United States Department of Agriculture, “Food Expenditure Report 2024,” ERS.USDA.gov Japan’s regulator lifted the process-temperature ceiling to 135 °C for retort packs, reducing sterilization cycles for curry and noodle pouches. [3]Ministry of Health, Labour and Welfare, “Food Contact Materials Approval Notice,” MHLW.go.jp Shelf stable packaging market players are investing in microwaveable cartons and single-serve pouches that retain texture, color, and flavor while staying safe on shelves for a year. Young professionals in North America, China, and Southeast Asia cite portion control and time savings as top purchase drivers, reinforcing demand for flexible, single-use packs.

E-Commerce Growth Driving Shelf-Ready Configurations

Online grocery penetration reached 15% of retail food sales in developed economies by 2024, and parcel networks impose severe drop, vibration, and compression stresses that legacy containers cannot withstand. Amazon’s packaging standard now demands 1.2-meter drop resistance and 200-kilogram compression for Frustration-Free certification, pushing converters to develop reinforced carton walls and puncture-resistant films. Stand-up pouches with resealable zippers cut dimensional weight charges by half, slashing shipping fees and carbon emissions. European trade body EXPRA urged the use of QR codes and digital watermarks for returns and deposit schemes, boosting track-and-trace adoption across the Shelf Stable Packaging market.

Regulatory Push for Food Waste Reduction

The United Nations tallied 1.05 billion metric tons of food wasted in 2023, with inadequate packaging driving one-fifth of losses. France adopted AGEC rules that require brands to prove measurable waste reduction, prompting a rapid shift to high-barrier, long-life packaging. Brazil synchronized aseptic standards with Codex references, opening import channels for ambient dairy and juice that bypass frozen logistics. In warmer, humid climates, shelf-stable packs preserve products far longer than chilled lines, directly aligning with Farm to Fork targets that aim to halve waste by 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Processing Requirements and Associated Costs | -0.7% | Global, acute for SMEs in emerging markets | Short term (≤ 2 years) |

| Volatility in Raw Material Prices | -0.9% | Global, especially North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Sustainability-Driven Restrictions on Multi-Material Laminates | -0.5% | Europe, North America, spillover to Asia-Pacific | Medium term (2-4 years) |

| Limited Recycling Infrastructure for Retort and Aseptic Formats | -0.4% | Global, acute in Middle East, Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw Material Prices

Average polyethylene terephthalate resin prices fluctuated between USD 1,200 and USD 1,550 per metric ton in 2024, while aluminum prices ranged from USD 2,400 to USD 2,900. Paperboard prices climbed 14% in Europe during the first half of 2024 as energy costs impacted pulping operations. Such gyrations have compressed converter margins, especially for mid-tier firms that lack hedging muscle or integrated resin output. Multinational food companies have added quarterly price adjustment clauses to their contracts, shifting commodity risk down the supply chain and injecting uncertainty into capital investment planning.

High Processing Requirements and Associated Costs

Aseptic and retort lines cost between USD 3 million and USD 8 million each, including steam generators, pressure vessels, sterile transfer tunnels, and ISO Class 5 cleanrooms. Small and medium processors in Southeast Asia struggle to access that capital, with less than 15% of local capacity equipped for ultra-high-temperature sterilization. Energy demand exceeds 2.5 megawatt-hours per metric ton for retort operations. Compliance hurdles such as U.S. Food and Drug Administration filings and scheduled audits add further complexity and cost. These barriers slow adoption and temper growth in the Shelf Stable Packaging market until financing solutions or shared-line models are expanded.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Material: Paper Substrates Gain Momentum Amid Recyclability Mandates

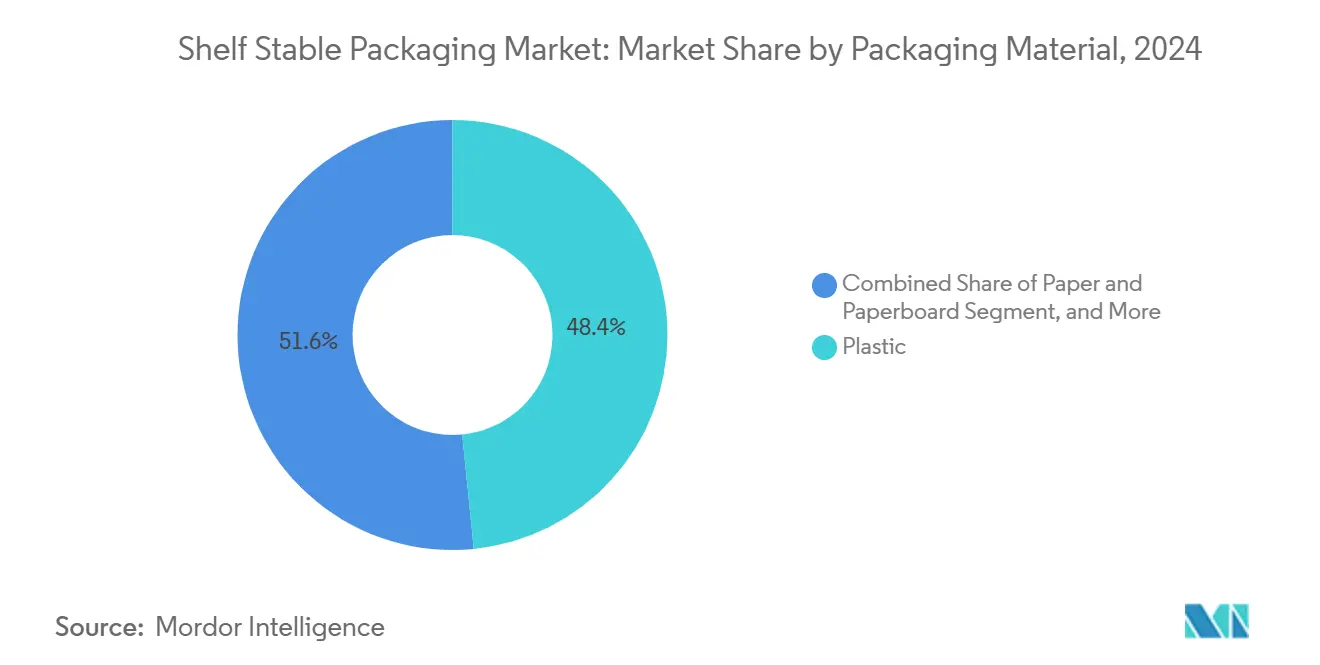

Paper and paperboard substrates are projected to expand at 7.43% per year from 2025 to 2030, eclipsing growth in plastics even though plastics commanded 48.43% share in 2024. The European Union’s Packaging and Packaging Waste Regulation encourages converters to adopt mono-material designs that can be easily processed through municipal waste streams, thereby catalyzing innovation in paper. Mondi’s recyclable retort pouch showcases progress, replacing aluminum foil with water-based coatings that enable an 18-month shelf life. In contrast, polyethylene and polypropylene films remain the workhorses for moisture-sensitive snacks, while polyethylene terephthalate bottles dominate hot-fill lines due to their ability to withstand 85 °C fills. Metal cans serve niche, high-temperature products where impact resistance is crucial, while glass retains a premium positioning, albeit its weight hampers e-commerce economics. The Shelf Stable Packaging market rewards suppliers that pair barrier performance with end-of-life compliance, and fiber-based composites are the current frontrunners for meeting both goals.

Paper’s rise is most visible in carton bricks and gable-tops for dairy and plant-based beverages, where fiber rigidity, printability, and renewable sourcing resonate with consumers. Integrated packagers layer thin polymer and, increasingly, edible coatings onto paperboard to block oxygen and oil migration, a formula that extends shelf life beyond nine months. Plastic materials still dominate flexible circuits; their lower density, heat-seal prowess, and compatibility with vertical-form-fill-seal systems deliver cost advantages that keep plastics essential to the Shelf Stable Packaging market. Avient’s 30% post-consumer polyolefin resins show how recyclate can close the sustainability gap. Going forward, substrate selection will hinge on how well suppliers balance mechanical protection, barrier integrity, and circularity targets without spreading costs beyond consumer tolerance.

By Packaging Format: Flexible Configurations Dominate Through Weight and Cube Efficiency

Flexible packaging owned 58.42% of revenue in 2024 and is forecast to compound at 8.32% through 2030, reflecting unrivaled weight-to-product ratios and superior cube utilization that lower shipping and warehousing spend. Stand-up and spouted pouches collapse during transit, enabling 40% more units per pallet than rigid equivalents, while DuPont’s latest EVOH grade drives oxygen transmission below 0.5 cc/m²-day. These gains align closely with the emissions-reduction targets that brands have pledged under the Science Based Targets initiative. Rigid formats retain performance edges where stacking, premium shelf signals, or oxygen-free metal walls remain essential; metal cans in soups and pet food, and glass jars in premium sauces persist despite cost and weight.

Innovation in flexible films centers on recyclable mono-material laminates and solvent-free adhesives that maintain hermetic seals in hot-fill applications. Rigid packs follow a parallel path of lightweighting, with average polyethylene terephthalate bottle weight dropping 15% since 2020. Cartons straddle both worlds, offering paperboard rigidity surrounding thin films, making them the preferred vessel for aseptic milk and juice. As parcel logistics redefine design constraints, demanding puncture resistance, low dimensional weight, and easy-open features, flexibles have become the de facto standard for new brand launches in the Shelf-Stable Packaging market.

By Product Type: Cartons Accelerate as Fiber-Based Alternatives Gain Traction

Pouches maintained leadership with a 38.42% revenue share in 2024, but cartons are expected to clock a 7.83% CAGR through 2030 as paperboard solutions gain regulatory favor. Tetra Pak’s 90% renewable carton, which replaces aluminum foil with plant-based polymers and features a fiber cap, embodies this shift toward climate-positive credentials. Cans perform reliably where 130 °C sterilization is nonnegotiable, yet flexible retort pouches challenge metal by weighing 30% less and flattening storage profiles. Bottles and jars persist in categories where consumer cues such as transparency, resealability, or gifting appeal drive purchase decisions.

Cartons’ acceleration is underpinned by SIG’s foil-free structure, which removes sorting complexity and surges through existing paper recycling systems. Meanwhile, pouches are surging in emerging economies as portion size affordability meets income levels. Across the Shelf Stable Packaging market, product-type choice increasingly reflects a mix of brand image, channel strategy, and recycling costs, rather than pure engineering feasibility.

By Packaging Technology: Aseptic Processing Leads Through Nutrient Retention and Shelf Life

Aseptic processing accounted for 30.77% of technology revenue in 2024 and is projected to rise by 8.23% annually to 2030, thanks to its unique ability to sterilize products and packages separately in sterile zones. Consumers value the near-fresh flavor retention in dairy and juice, while retailers appreciate one-year ambient distribution windows. Krones’ Dynafill HES achieves a throughput of 36,000 bottles per hour while operating water-free sterilization cycles, resulting in a 20% reduction in operating expenses in drought-prone geographies. Retort processing still dominates the production of particulate-heavy soups and stews; hot-fill remains a cost-effective option for high-acid juices and sauces.

Future growth in the Shelf Stable Packaging market hinges on hybrid systems that combine aseptic fills with subsequent mild retorts or active packaging inserts. Modified-atmosphere methods provide an additional layer of protection for oxygen-sensitive snacks that require minimal thermal load. Equipment makers now bundle artificial-intelligence vision systems that reject under-sterilized packs at a rate of 500 units per minute, thereby tightening quality control and reducing recall risk.

By Application: Juice Packaging Surges on Health Trends and Ambient Convenience

Dairy captured 28.53% of demand in 2024, but juice packaging is growing at 8.51% annually, driven by vitamin-retentive ambient formats and functional add-ins. The International Fruit and Vegetable Juice Association noted an 18% jump in cold-pressed juice sales in 2024. Ambient-safe cartons enable economical distribution to convenience stores and rural kiosks, thereby circumventing chilled supply constraints. Sauces and condiments come in flexible pouches that squeeze out nearly every drop, reducing food waste and aligning with France’s AGEC benchmarks.

Processed fruit and vegetables continue to rely on retort cans and trays that lock in color and texture for a two-year shelf life, while ready meals leverage microwave-safe bowls that heat from frozen or shelf-stable states. Across all end uses, the unifying consumer demands, transparency, convenience, and sustainability, keep driving package redesigns that favor lightweight and curbside recyclability. This set of preferences reinforces investment momentum in the Shelf Stable Packaging market.

Geography Analysis

The Asia-Pacific region dominated the Shelf Stable Packaging market, accounting for a 40.21% revenue share in 2024, and is projected to grow at a 9.12% CAGR through 2030. Rapid urban growth, rising disposable incomes, and a fragmented cold chain accelerate the adoption of ambient formats. China’s packaged food sector expanded 11% in 2024, with aseptic cartons making inroads in lower-tier cities where cooling remains inconsistent. India’s dairy cooperatives deployed USD 500 million in ultra-high-temperature facilities during 2024, extending milk reach beyond 48-hour chilled radii and lifting rural availability. Southeast Asia’s sachet culture drives the dominance of single-serve pouches in sauces, coffee, and condiments.

North America remains a mature yet innovative arena. The U.S. Food and Drug Administration now permits up to 50% recycled polyethylene terephthalate in food contact bottles, prompting large beverage brands to announce recycled-content milestones. Mexico’s proximity to United States consumer markets has sparked capital flows into flexible converting; Sealed Air and Printpack both expanded Mexican capacity in 2024. Canada’s federal plastics registry mandates volume and recycled-content reporting, fostering data-driven accountability.

Europe’s legislative backdrop is perhaps the most influential for design trends in the Shelf Stable Packaging market. The Packaging and Packaging Waste Regulation demands full recyclability by 2030, driving a pivot to mono-material or fiber-heavy formats. Germany extended deposit returns to juice and dairy cartons, achieving a 92% take-back rate within six months. In parallel, digital watermark pilots under HolyGrail 2.0 equip packs with invisible coding that guides sorting robots, raising overall recycling yields.

Emerging regions in South America, the Middle East, and Africa show large white-space potential tempered by infrastructure gaps. Brazil’s regulatory harmonization with Mercosur cleared bureaucratic hurdles for aseptic imports, while Gulf states invest in domestic metal-can capacity to shield against shipping disruptions. South Africa’s producer responsibility fees now penalize non-recyclable laminates, nudging converters toward fiber-based offerings. Nigeria and Kenya ride a sachet wave, where affordability trumps recyclability concerns, though local NGOs press for collection incentives. Across these geographies, brand owners calibrate package formats to match power grid reliability, waste-collection maturity, and income distribution.

Competitive Landscape

The Shelf Stable Packaging market is fragmented, including suppliers such as Amcor’s flexible lines, Tetra Pak’s cartons, SIG, and others. Consolidation pressure intensified when Pactiv Evergreen and Novolex announced their USD 10.5 billion merger, seeking resin-purchase leverage and unified sales coverage. Simultaneously, challengers who master digital printing or edible coating technology win turnkey contracts with emerging food brands eager for agile production.

Technology leadership distinguishes winners. Crown Holdings has patented a resealable metal-can end with a polymer membrane, transforming single-use cans into multi-serve containers. GS1’s watermark standard, adopted by over 50 companies, embeds data for track-and-trace as well as automated recycling. Quality certifications, such as ISO 22000 and BRC for Packaging, remain gating factors for entry into multinational supplier lists. With sustainability scorecards now embedded in sourcing metrics, converters unable to document their CO₂ and recycled-content footprints risk being delisted, regardless of their price competitiveness.

In response, global groups invest heavily in R&D. Tetra Pak allocated USD 150 million to its new Indian plant, embedding renewable energy and water recycling to trim emissions 40% against its legacy baseline. SIG and Mondi pour funds into foil-free barriers that aim to meet 12-month shelf life without multi-layer complexity. On the filling equipment side, Krones and Sidel compete on throughput and sterility validation, pitching artificial-intelligence-enabled vision systems that promise sub-ppm defect rates. The resulting innovation race keeps margins healthy for leaders even as raw materials fluctuate.

Shelf Stable Packaging Industry Leaders

Amcor Plc

Mondi Group

Huhtamaki Oyj

Silgan Holdings Inc.

Crown Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Pactiv Evergreen and Novolex unveiled a USD 10.5 billion merger plan, aiming to invest USD 300 million in recycling facilities and sustainable materials by 2027.

- October 2024: Tetra Pak inaugurated a USD 150 million aseptic carton plant in Chakan, India, adding 8 billion annual package capacity and incorporating on-site renewable power.

- September 2024: Amcor launched AmFiber, a paper-based retort pouch that meets FDA food-contact rules and delivers an 18-month shelf life without aluminum foils.

- August 2024: Crown Holdings completed a USD 200 million expansion at its Monterrey, Mexico, beverage can complex, introducing lightweight designs that trim aluminum use by 12%.

Global Shelf Stable Packaging Market Report Scope

The Shelf Stable Packaging Market refers to the industry focused on packaging solutions designed to extend the shelf life of products without the need for refrigeration. These packaging solutions utilize advanced materials and technologies to preserve the quality, safety, and freshness of various food and beverage products.

The Shelf Stable Packaging Market Report is Segmented by Packaging Material (Plastic, Metal, Glass, Paper and Paperboard, Other Multi-Layer Structures), Packaging Format (Flexible, Rigid), Product Type (Metal Cans, Bottles, Jars, Cartons, Pouches, Other Product Types), Packaging Technology (Aseptic, Retort, Hot Fill, Other Technologies), Application (Sauce and Condiment, Processed Fruit and Vegetable, Juice, Dairy Food, Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Plastic |

| Metal |

| Glass |

| Paper and Paperboard |

| Other Multi-Layer Structures |

| Flexible |

| Rigid |

| Metal Cans |

| Bottles |

| Jars |

| Cartons |

| Pouches |

| Other Product Types |

| Aseptic Food Packaging |

| Retort Food Packaging |

| Hot Fill Food Packaging |

| Other Packaging Technologies |

| Sauce and Condiment |

| Processed Fruit and Vegetable |

| Juice |

| Dairy Food |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Material | Plastic | ||

| Metal | |||

| Glass | |||

| Paper and Paperboard | |||

| Other Multi-Layer Structures | |||

| By Packaging Format | Flexible | ||

| Rigid | |||

| By Product Type | Metal Cans | ||

| Bottles | |||

| Jars | |||

| Cartons | |||

| Pouches | |||

| Other Product Types | |||

| By Packaging Technology | Aseptic Food Packaging | ||

| Retort Food Packaging | |||

| Hot Fill Food Packaging | |||

| Other Packaging Technologies | |||

| By Application | Sauce and Condiment | ||

| Processed Fruit and Vegetable | |||

| Juice | |||

| Dairy Food | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Shelf Stable Packaging market today?

The Shelf Stable Packaging market size reached USD 75.35 billion in 2025 and is forecast at USD 102.94 billion by 2030.

Which packaging format is growing fastest?

Flexible configurations, especially stand-up pouches, are advancing at an 8.32% CAGR through 2030 because they cut shipping weight and cube.

What drives aseptic technology adoption?

Aseptic lines preserve vitamins and flavors while offering 12-month ambient shelf life, pushing an 8.23% CAGR for the technology category.

Why is Asia-Pacific so important for shelf-stable packs?

Limited cold chain, rising incomes, and e-commerce growth give Asia-Pacific a 40.21% share and a 9.12% CAGR outlook.

How are regulations shaping material choices?

The EU’s recyclability mandate for 2030 is shifting investment toward mono-material or fiber-based packs that fit curbside recycling.

What is the main restraint on market growth?

Raw-material price volatility including aluminum, PET, and paperboard swings, cuts converter margins and complicates long-term pricing.

Page last updated on: