Edible Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 691.05 Million |

| Market Size (2030) | USD 987.72 Million |

| Growth Rate (2025 - 2030) | 7.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

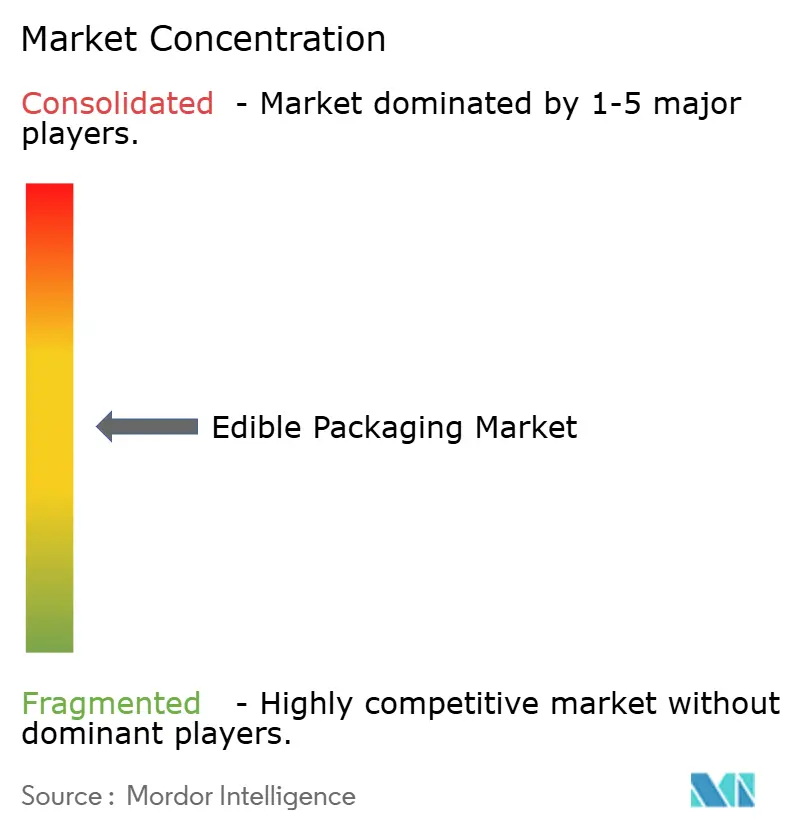

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Edible Packaging Market Analysis by Mordor Intelligence

The edible packaging market size is valued at USD 691.05 million in 2025 and is forecast to reach USD 987.72 million by 2030, advancing at a 7.41% CAGR. Tighter rules on single-use plastics, expanded ESG capital flows and improvements in plant-based barrier technologies are accelerating demand growth. Plant-derived films account for the bulk of current deployments as consumer acceptance of bio-derived formats rises and corporate buyers seek visible progress toward circular economy goals. Product developers are using nano-enabled composites to narrow the performance gap with petroleum plastics, while 3-D printing and layer-by-layer coating processes are opening bespoke formats for high-value food, nutraceutical and pharmaceutical applications. Upfront costs remain higher than incumbent materials, yet life-cycle economics are improving as disposal fees climb, carbon pricing mechanisms expand and brand owners quantify reputational gains from plastic-free portfolios. Venture capital inflows and corporate venture funds are therefore underwriting larger pilot lines and driving quicker iterations in formulation science, pushing the edible packaging market toward commercial scale.

Key Report Takeaways

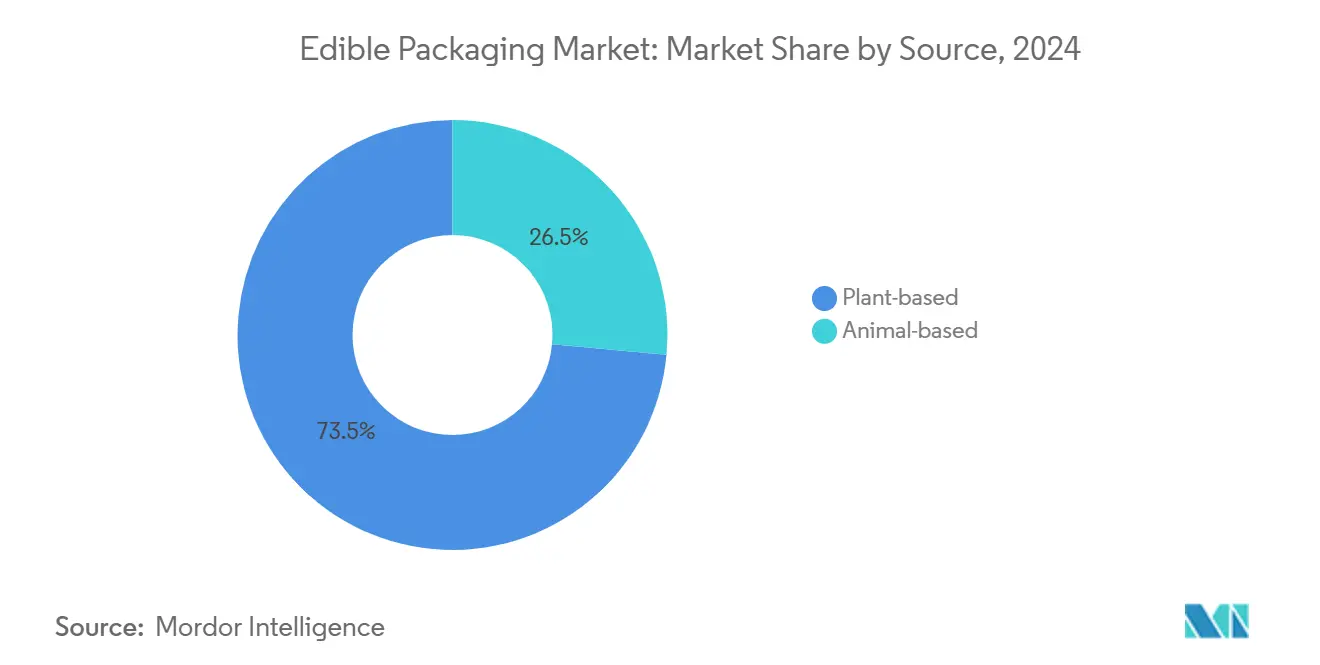

- By source, plant-based materials led with 73.53% of edible packaging market share in 2024, while animal-based sources trail due to supply and ethical constraints.

- By raw material, proteins captured 45.62% share of the edible packaging market size in 2024; polysaccharides are forecast to grow at 10.34% CAGR to 2030.

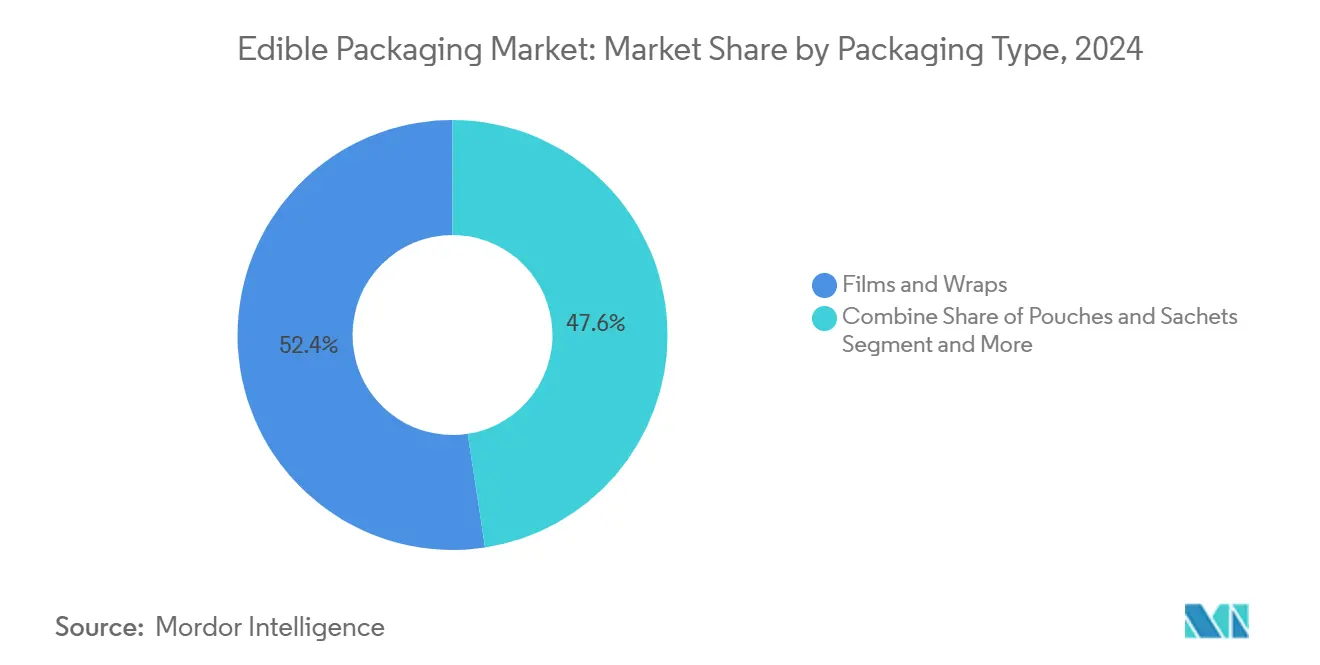

- By packaging type, films and wraps held 52.42% revenue share in 2024, whereas coatings and membranes are expanding at a 9.32% CAGR through 2030.

- By end-use, the food segment accounted for 35.23% of the edible packaging market size in 2024; pharmaceutical and nutraceutical applications are rising at 11.01% CAGR.

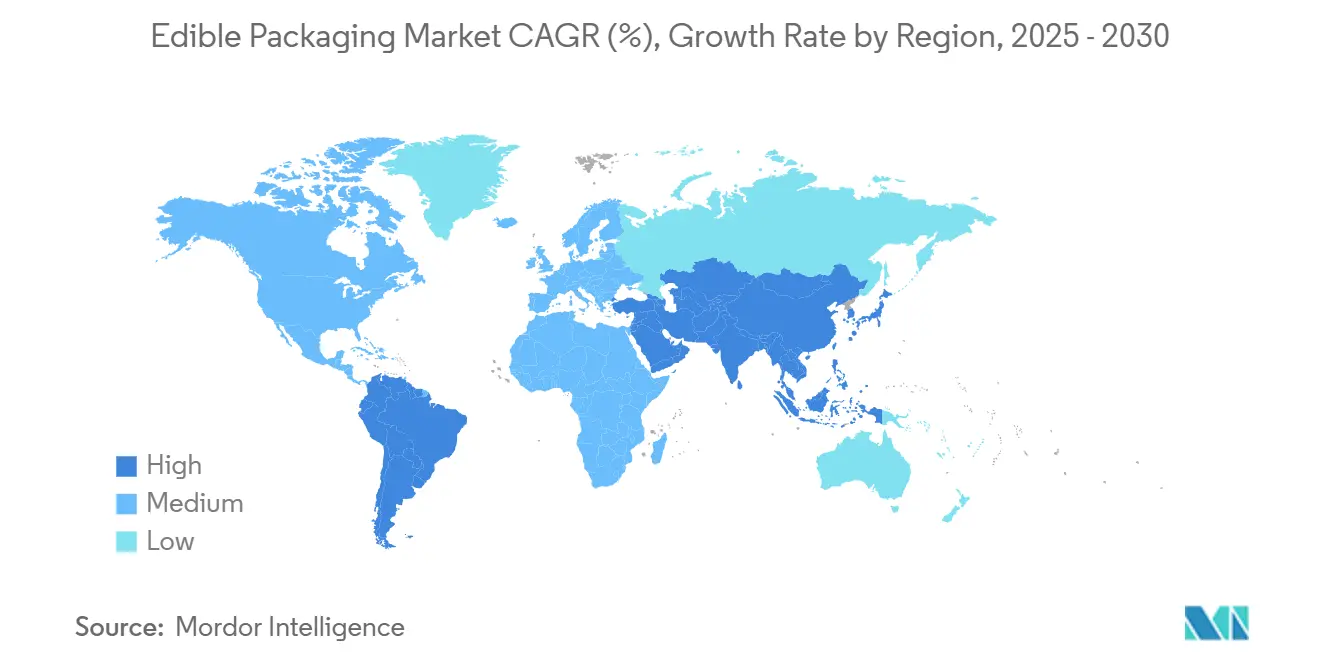

- By region, North America dominated with 32.45% share of the edible packaging market in 2024, while Asia-Pacific records the highest projected CAGR at 10.85% to 2030.

Global Edible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ban on single-use plastics and supportive regulation | +1.8% | Global, early uptake in EU and North America | Medium term (2-4 years) |

| Rising consumer demand for sustainable packaging | +1.5% | Global, strongest in developed markets | Long term (≥ 4 years) |

| Need to extend shelf life and cut food waste | +1.2% | Global, highly relevant in emerging markets | Medium term (2-4 years) |

| Integration of bio-actives into coatings | +0.9% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Advances in 3-D food printing for customized packs | +0.6% | North America and Europe, niche uses | Long term (≥ 4 years) |

| Surge in ESG-linked financing | +0.8% | Global, concentrated in venture hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ban on Single-Use Plastics and Supportive Regulation

Governments are phasing out conventional plastics with measures such as the European Union Single-Use Plastics Directive and similar statutes now enacted in more than sixty countries. The 2024 FDA guidance clarified safety pathways for edible formats, reducing approval uncertainty in the United States. China’s updated rules effective January 2025 recognise edible films for food-service applications, making regulatory compliance more straightforward in the world’s largest consumer market. Financial incentives such as tax credits and faster permitting further improve the business case.

Rising Consumer Demand for Sustainable Packaging

A 2024 global survey found 67% of consumers under 35 willing to pay a premium for edible packaging compared with 23% in 2019. Confectionery and snack categories post the highest acceptance as the pack becomes part of the eating experience. Leading food brands align procurement with net-zero targets, translating sustainability pledges into tangible orders. Taste, texture and allergy issues still influence purchase intent, so formulators invest in masking agents and allergen-free substrates to broaden reach.

Need to Extend Shelf Life and Cut Food Waste

Polysaccharide-based edible coatings extend shelf life of fresh produce by 20-35%, reducing spoilage where refrigeration is limited. [1]Neus Teixidó, “Fundamentals of Edible Coatings and Combination with Biocontrol Agents,” mdpi.com Given food waste exceeds USD 1 trillion each year, even moderate spoilage cuts create material savings for growers and retailers. Formulations incorporating essential oils deliver active antimicrobial benefits, and controlled-release systems maintain produce quality without chilling infrastructure.

Integration of Bio-Actives into Coatings

Encapsulation techniques now maintain probiotic viability during storage and release nutrients upon ingestion. Edible films also carry pharmaceutical actives, improving patient adherence compared with tablets. Food makers use antioxidant-rich matrices to upgrade product nutrition without altering recipes, securing competitive differentiation in functional food aisles.[2]Maria Baldassarre and Giulia De Marco, “Edible Coatings for Fish Preservation,” pmc.ncbi.nlm.nih.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost vs conventional plastics | -2.1% | Global, acute in price-sensitive markets | Medium term (2-4 years) |

| Limited mechanical and barrier performance | -1.3% | Global, challenging in humid climates | Long term (≥ 4 years) |

| Allergen and dietary-compliance challenges | -0.8% | Global, stricter in EU and North America | Medium term (2-4 years) |

| Cold-chain moisture and temperature sensitivity | -0.6% | Global, critical in tropical regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Cost vs Conventional Plastics

Edible films currently cost two to three times more than polyethylene due to specialty inputs and low volumes. Complex process controls around humidity and sterility add capital expense. Scale benefits are emerging but remain uneven because formulations differ widely by application. Rising landfill fees and carbon pricing narrow the gap in total cost of ownership, though the shift varies by region and buyer profile.

Limited Mechanical and Barrier Performance

Water vapor transmission rates for many edible films are still 10-50 times higher than polyethylene, restricting use in humid supply chains. Nano-reinforced composites now bring the delta to 20-30%, yet costs increase accordingly. Developers balance improved stiffness with retention of edibility, often using multilayer hybrids that complicate regulatory review and scale-up.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Strong Growth for Plant-Based Materials

Plant-based substrates hold 73.53% of edible packaging market share in 2024, buoyed by plentiful feedstocks like corn starch, wheat gluten and cellulose. Animal-derived options represent 26.47% and remain niche where religious or vegan preferences restrict adoption. Plant variants advance at 8.45% CAGR through 2030 as agrifood by-products enter circular valorisation streams. The edible packaging market size for plant-based formats is projected to widen steadily as microalgae protein coatings and fruit-pomace matrices move from pilot to production, adding antioxidant and antimicrobial properties that raise shelf-life performance. [3]Luisa López-Ortiz, “Composite Edible Coating from Arabic Gum and Mango Peel Hydrocolloids,” mdpi.com

Animal proteins retain roles in premium pharmaceutical films because of predictable dissolution profiles and high tensile strength. Gelatin and casein layers deliver reliable payload release for drug delivery or nutrient applications. Ethical supply and cost challenges keep volume modest, yet these attributes command premium pricing where performance is paramount. Composite structures pairing plant polysaccharides with fish gelatin or whey protein illustrate hybrid paths that leverage strengths of both sources while mitigating single-material limits.

By Raw Material: Protein Dominance with Polysaccharide Momentum

Proteins account for 45.62% of edible packaging market share in 2024, reflecting superior film-forming capability and mechanical integrity. Corn zein and soy isolates remain workhorses although pea and algae proteins are scaling to satisfy allergen-free and vegan claims. Polysaccharides register the highest growth at 10.34% CAGR, underpinned by chitosan, alginate and pectin upgrades that add antimicrobial actions and oxygen barriers. The edible packaging market size for polysaccharide films is set to expand rapidly as nano-chitosan or nanocellulose reinforcements lift strength and moisture resistance to near-plastic levels.

Lipids remain useful in moisture control layers yet oxidation sensitivity restricts shelf life in hot supply chains. Innovation focuses on multi-layer laminates that sandwich lipid barriers between protein or polysaccharide skins. Patent filings describe bilayer stacks where inner protein strata deliver strength and outer waxy lipids block water ingress, narrowing the performance gap to polyethylene while preserving edibility.

By Packaging Type: Films Lead, Coatings Surge

Films and wraps accounted for 52.42% of edible packaging market share in 2024 because extrusion lines adapt readily from plastic to bio-based resins. Integrated label printing and lamination systems already installed at converters favour film rollstock. Coatings and membranes rise at a 9.32% CAGR, leveraging spray or dip processes that coat produce or prepared foods in-line, saving material and freight versus discrete wrappers. The edible packaging market size for coatings benefits from retail grocers adopting minimal-pack formats to hit plastic reduction targets.

Layer-by-layer nano-coatings deposit sequential polysaccharide and protein layers only nanometres thick, producing high gas barriers with negligible weight addition. Pouches, sachets and water-soluble caps occupy niche spaces such as instant beverages or seasoning kits where the package itself dissolves during use. Heat-seal innovations in starch blends now allow true hermetic seals, widening potential for ready-meal inserts and portion-controlled condiments.

By End-Use Industry: Food Holds Lead, Pharma Accelerates

Food applications captured 35.23% of edible packaging market size in 2024, led by fresh produce, confectionery and snack uses where the pack enhances convenience and reduces waste. Ready-to-eat meals and salad kits now trial antimicrobial coatings that add two or more days to shelf life, giving retailers longer merchandising windows. Beverage uses remain emergent, with soluble lids and inner coatings for edible cups under pilot scale trials.

Pharmaceutical and nutraceutical uses grow at 11.01% CAGR. Thin oral films deliver APIs with rapid dissolution, simpler swallowing and controlled dosing, ideal for paediatric and geriatric care. Personal care remains niche but edible lip balms and toothpaste tabs illustrate early moves toward ingestible packs. Pet food and agri-feed sectors are exploring edible liners that add micronutrients or probiotics directly into feed ration packaging, though volumes remain experimental.

Geography Analysis

North America leads with 32.45% share of the edible packaging market in 2024 thanks to clear regulatory guidance, robust R&D and deep pools of sustainability investment. The FDA framework issued in 2024 gives processors a defined route to approval, reducing project risk for converters. High consumer environmental awareness and strong retailer commitments drive purchase orders. Start-ups such as Apeel Sciences secure strategic investments from large grocers seeking longer shelf life and reduced shrink.

Asia-Pacific posts the fastest CAGR at 10.85% through 2030 as urban populations and income levels climb. China’s 2025 regulations expressly permit edible service ware in restaurants, stimulating local capacity build-outs. Japan and South Korea leverage advanced food tech sectors and consumers willing to try novelty formats. India brings abundant agricultural feedstocks, yet price sensitivity remains a hurdle, so developers target high-value exports and hospitality chains first. Australia pairs strong environmental sentiment with government plastic-free targets, creating early adopter demand.

Europe retains a large share underpinned by Single-Use Plastics Directive mandates, circular economy policies and eco-label programmes. Germany and the United Kingdom host leading research clusters focused on barrier nanocomposites, while France’s gourmet sector values premium edible wraps that integrate flavours. Italy’s produce exporters experiment with chitosan coatings to cut waste during long-haul shipping. Emerging uptake in the Middle East and Africa relates to limited cold-chain coverage where edible coatings prolong shelf life of fruit and vegetables without refrigeration. South America explores supply synergies between abundant crops and local packaging demand, though macroeconomic volatility tempers large capital outlays.

Competitive Landscape

The edible packaging market remains consolidated. Start-ups bring novel seaweed, algae and fruit-waste solutions, while established film converters retrofit lines for bio-based resins. Funding momentum is strong; Notpla scaled from lab to commercial sheet lines after its 2024 raise whereas AlterPacks channels seed capital into quick-service restaurant formats. Technology differentiation centres on moisture control, oxygen barriers and bio-active loading without compromising edibility.

Strategic alliances underpin market entry. Material innovators partner with contract packers to trial films under actual processing conditions, de-risking scale transition. Corporate venture arms from global food brands take minority stakes to secure first-mover packaging rights. Intellectual property filings cluster around nano-reinforced bilayers, microalgae antioxidants and controlled release of probiotics, indicating a pipeline of functional packs beyond basic protection.

Process optimisation aims to lower cost. Continuous casting lines with in-line drying reduce energy use, while enzymatic extraction of plant proteins from waste streams cuts raw input expense. Manufacturers also explore vertical integration into feedstock sourcing, especially where supply chain traceability bolsters brand narratives. Market entry hurdles include compliance testing for allergen disclosure and achieving mechanically sound packs at humidity ranges typical in global logistics.

Edible Packaging Industry Leaders

Tipa Corp Ltd.

Nagase America LLC (Nagase & Co., Ltd.)

Evoware (PT. Evogaia Karya Indonesia)

Notpla Limited

TSUKIOKA FILM PHARMA CO., LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Loliware obtained technical assistance from the Subnational Climate Fund for a Guatemala seaweed packaging project.

- October 2024: AlterPacks raised USD 1.6 million to accelerate plant-based formats for quick-service restaurants and food delivery chains.

- September 2024: Notpla Limited secured GBP 20 million (USD 22.6 million) Series A+ funding to scale seaweed packaging lines and pursue bio-active variants.

- May 2024: GO-Eco advanced graphene oxide barriers that could replace PFAS in food wraps.

Global Edible Packaging Market Report Scope

Edible packaging is a sustainable solution designed to be eaten or biodegraded, commonly made from plant- or animal-based sources. Edible packaging works as an alternative to plastic packaging and helps reduce plastic waste as everything is eaten or biodegraded. It helps reduce waste and reduces the need for recycling. Continuous research and development (R&D) are carried out by the vendors operating in the market to offer better product offerings adhering to the end-user industry requirement. The edible packaging market is expected to experience more innovation in the coming years, and mergers and acquisitions are expected in the industry. New brands have gained traction in the last few years due to the quality of their offerings.

The edible packaging market is segmented by source (plant and animal), raw material (protein, polysaccharides, lipids, and other raw materials), end-user industry (food, beverage, and pharmaceutical), and Geography (North America [United States and Canada], Europe [Germany, United Kingdom, France, Italy, and Rest of Europe], Asia-Pacific [China, Japan, India, Australia and New Zealand, and Rest of Asia Pacific], Latin America, Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| Plant-based |

| Animal-based |

| Proteins |

| Polysaccharides |

| Lipids |

| Composite / Multilayer |

| Other Materials |

| Films and Wraps |

| Pouches and Sachets |

| Coatings and Membranes |

| Caps and Lids |

| Other Packaging Types |

| Food |

| Beverage |

| Pharmaceutical and Nutraceutical |

| Cosmetics and Personal Care |

| Other End-use Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Source | Plant-based | ||

| Animal-based | |||

| By Raw Material | Proteins | ||

| Polysaccharides | |||

| Lipids | |||

| Composite / Multilayer | |||

| Other Materials | |||

| By Packaging Type | Films and Wraps | ||

| Pouches and Sachets | |||

| Coatings and Membranes | |||

| Caps and Lids | |||

| Other Packaging Types | |||

| By End-Use Industry | Food | ||

| Beverage | |||

| Pharmaceutical and Nutraceutical | |||

| Cosmetics and Personal Care | |||

| Other End-use Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the edible packaging market?

The market is valued at USD 691.05 million in 2025 and is forecast to approach USD 1 billion by 2030 at a 7.41% CAGR.

Which source material dominates edible packaging today?

Plant-based substrates dominate with 73.53% share in 2024, thanks to established agricultural supply chains and growing consumer acceptance.

Why are coatings the fastest-growing packaging type?

Spray-on and dip-coat technologies use less material than discrete wraps, boost shelf life and fit easily into existing food processing lines, supporting a 9.32% CAGR to 2030.

Which region is expanding the fastest in edible packaging?

Asia-Pacific posts the highest projected growth at 10.85% CAGR through 2030 because of supportive regulations, urbanisation and rising environmental awareness.

What is the main barrier to wider adoption of edible packaging?

Current production costs remain 2-3 times higher than traditional plastics, although falling disposal fees for plastics and improved economies of scale are narrowing the gap.

How are bio-actives influencing market growth?

Encapsulating probiotics, vitamins or pharmaceuticals into edible films creates functional packaging that commands higher prices and opens new applications in health and wellness.

Page last updated on: