Edge Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

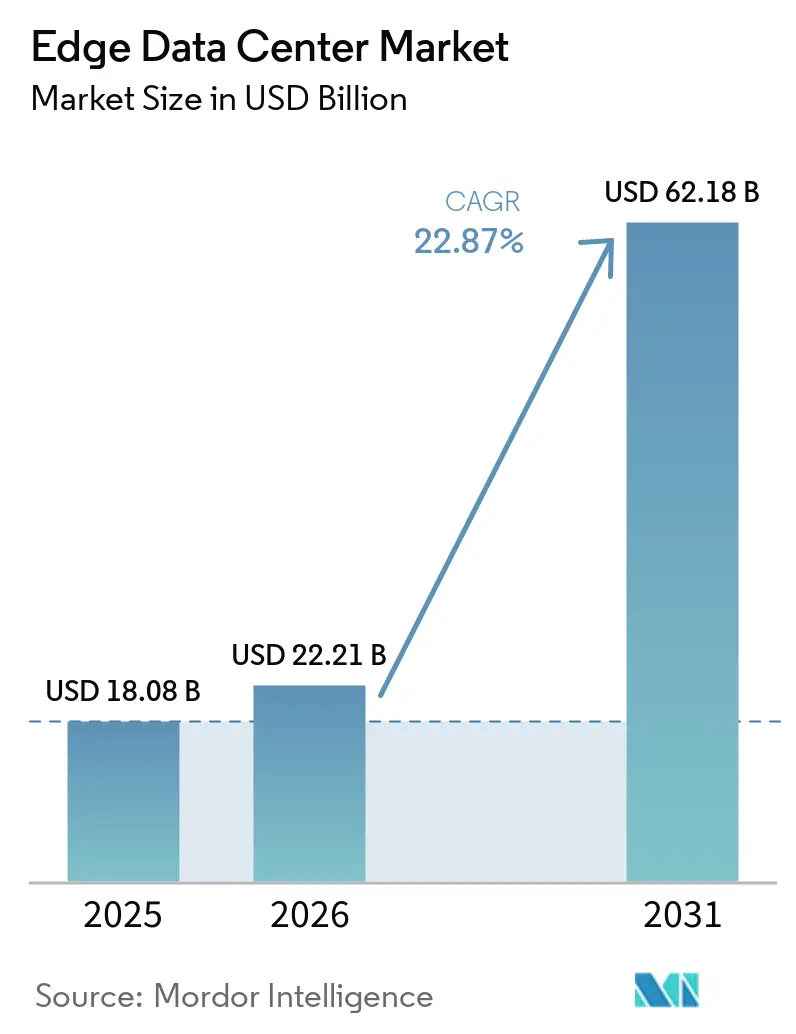

| Market Size (2026) | USD 22.21 Billion |

| Market Size (2031) | USD 62.18 Billion |

| Growth Rate (2026 - 2031) | 22.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Edge Data Center Market Analysis by Mordor Intelligence

The edge data center market size was valued at USD 18.08 billion in 2025 and estimated to grow from USD 22.21 billion in 2026 to reach USD 62.18 billion by 2031, at a CAGR of 22.87% during the forecast period (2026-2031). Growing demand for sub-10 millisecond response times, the rollout of 5G radios, and rapid AI workload migration keep construction pipelines full. Local-processing mandates in more than 40 countries continue to steer budgets toward distributed architectures that keep data within national borders. Operators also pursue renewable micro-grids that shave 15-20% from power bills, turning sustainability into a competitive lever. Moderate rivalry prevails as hyperscale incumbents such as Microsoft and Oracle clash with focused specialists, including EdgeConneX and Vapor IO, while capital flows stay strong despite short-term cost inflation.

Key Report Takeaways

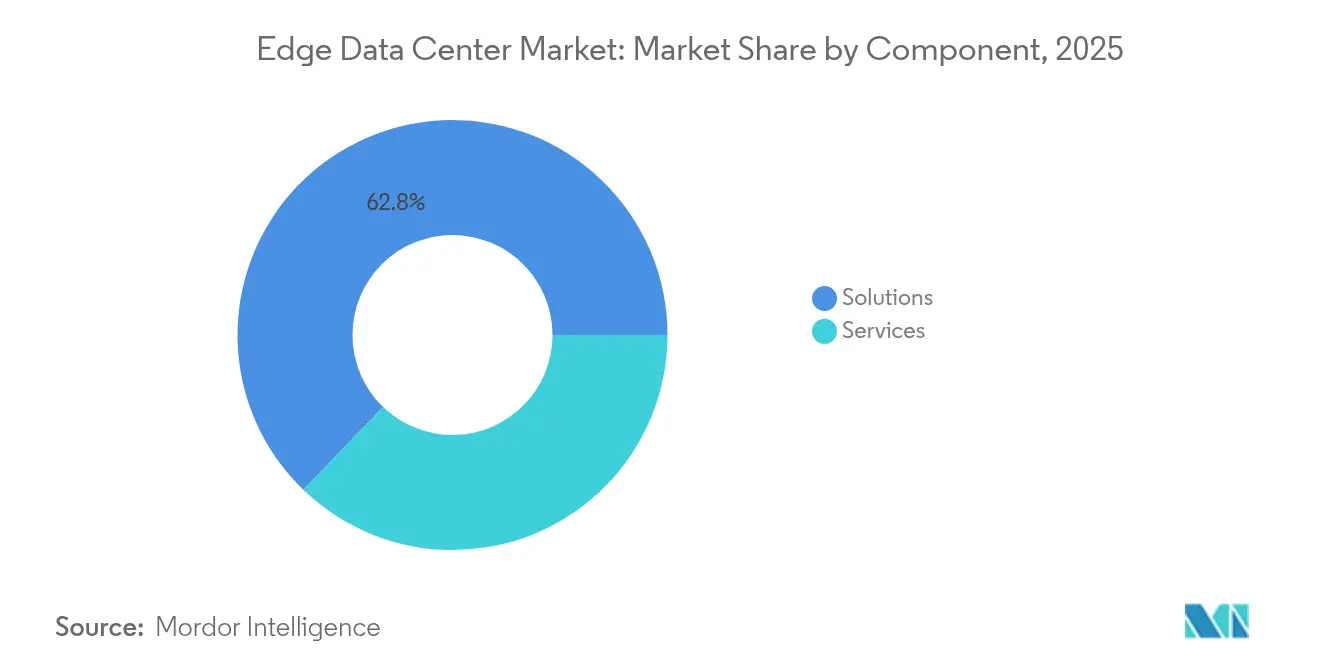

- By component, Solutions led with 62.80% of edge data center market share in 2025; Services is poised to grow at a 23.96% CAGR through 2031.

- By data-center size, Large facilities controlled 54.10% share of the edge data center market in 2025, yet Mega sites will expand fastest at 25.8% CAGR.

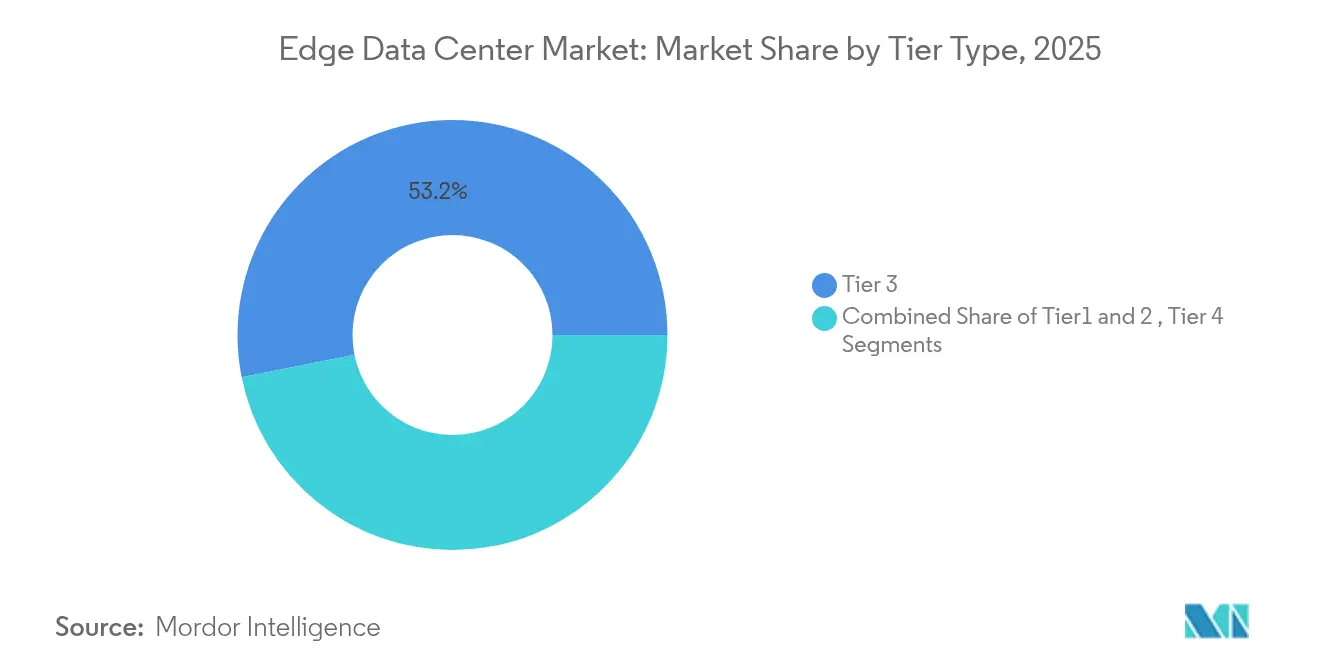

- By tier, Tier 3 held 53.15% share in 2025, while Tier 4 configurations are advancing at 25.3% CAGR through 2031.

- By end user, BFSI accounted for 28.85% share of the edge data center market size in 2025, whereas IT & Telecom will post the highest 23.7% CAGR through 2031.

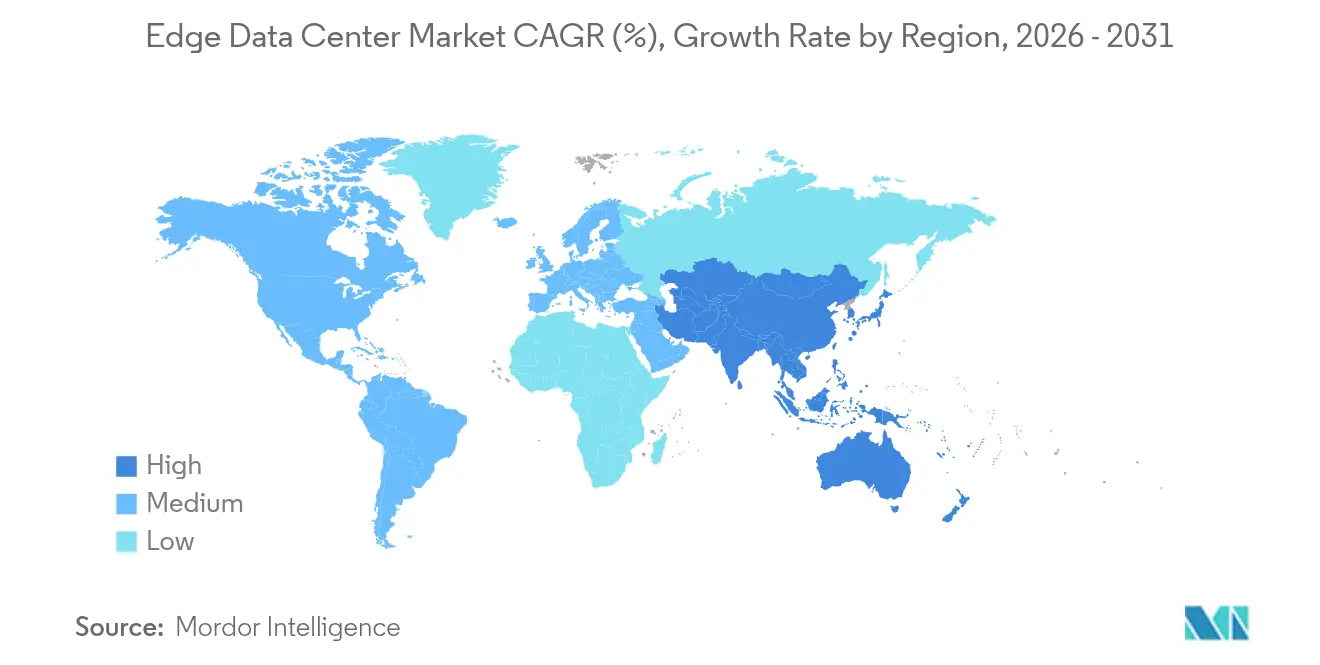

- By geography, North America captured 27.05% share in 2025; Asia-Pacific is projected to climb at a 24.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Edge Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of IoT and connected devices | +4.2% | Global / APAC lead | Medium term (2-4 years) |

| Surge in video / 5G-driven data traffic | +5.8% | North America and EU core, Asia-Pacific expansion | Short term (≤ 2 years) |

| Latency-critical AR/VR and autonomous apps | +3.1% | North America and EU early adoption | Long term (≥ 4 years) |

| Data-sovereignty regulations | +2.9% | EU primary, expanding to Asia-Pacific and MEA | Medium term (2-4 years) |

| AI inferencing workloads shifting to edge | +6.4% | North America and China lead | Short term (≤ 2 years) |

| Renewable-energy micro-grids at edge sites | +1.4% | Global / Nordic and LATAM advantages | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of IoT & connected devices

More than 21.5 billion edge-connected endpoints will be active in 2025, overwhelming centralized clouds and driving procurement of localized compute nodes. [1]StateTech Editorial Staff, “IoT Growth Spurs Edge Adoption,” statetechmagazine.com Emirates NBD boosted transaction throughput by 42% after relocating analytics to regional nodes. 3M trimmed machine downtime by 35% using Azure SQL Edge on factory floors, highlighting the cost advantage once sites generate over 10 TB of monthly data. Las Vegas’ smart-city partnership with Vapor IO and NVIDIA cut traffic-signal latencies from 200 ms to 20 ms.

Surge in video/5G-driven data traffic

Video already represents 82% of internet load, and 5G devices intensify pressure for sub-10 ms delivery. Verizon and NVIDIA are turning edge racks into AI-as-a-service hubs that monetize spectrum investments. BMW’s factory streams 4K footage from 200+ cameras to nearby nodes for defect detection in 50 ms versus 2–3 s in cloud paths, saving 15-20× on transmission fees. Global carriers are channeling USD 50 billion into such deployments.

Latency-critical AR/VR & autonomous apps

AR interfaces and driverless systems collapse if delays exceed 20 ms. NVIDIA’s Clara Guardian now processes imaging inside hospitals, guiding surgeons in real time. Mercedes-Benz synchronized assembly robots in 15 ms, down from 500 ms via cloud, preventing costly halts. Every 10 ms shaved from vehicle perception loops can avert USD 2–3 million in liabilities per model year.

AI inferencing workloads moving to edge

JPMorgan Chase invested USD 2 billion in private-edge resources, slicing fraud-detection cycles from 200 ms to 50 ms. Chery Automobile raised vision accuracy to 99.7% by training models locally, avoiding cloud lag. The International Energy Agency warns AI may consume 3–5% of global power by 2030, making on-prem inference essential for energy budgets.[2]International Energy Agency, “AI’s Growing Electricity Thirst,” iea.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for edge facility build-outs | -3.7% | Global / higher impact in emerging markets | Short term (≤ 2 years) |

| Interoperability and management gaps | -1.8% | Global / multi-vendor settings | Medium term (2-4 years) |

| Cyber and physical security risks | -2.3% | Global / critical infrastructure | Short term (≤ 2 years) |

| Skilled-labor shortage in tier-2/3 cities | -2.1% | North America & EU first, spreading globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capex for edge facility build-outs

Construction costs jumped 25-30% since 2024, driven by power-dense designs that run USD 8,000–12,000 per kW versus USD 4,000–6,000 in legacy halls. Vantage’s USD 13 billion plan shows single sites now price at USD 50–80 million.[3]White & Case LLP, “Financing Trends in the Data-Center Sector,” whitecase.com Lead times for switch-gear stretch to two years, swelling inventory costs and quality risks.

Interoperability & management gaps

Enterprises spend 6–12 extra months harmonizing dissimilar hardware and orchestration tools, adding 25–35% to total cost of ownership. The Linux Foundation’s Margo initiative seeks common APIs, yet overlapping ETSI and OpenFog standards still confuse buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services accelerate as solutions remain dominant

Solutions retained 62.80% of edge data center market share in 2025 as enterprises raced to install physical racks and orchestration software. The edge data center market will nevertheless see Services expand at a 23.96% CAGR, fueled by demand for managed operations that offset talent gaps. Outsourced monitoring can cut run-rate costs 30-40% versus in-house oversight, a fact underscored by Lumen’s AI-driven portfolio that yields 40-50% margins.

The trend signals a pivot from capital expenditure toward outcome-based models. As deployments multiply across hundreds of rooftops and retail closets, clients value guaranteed SLAs more than asset ownership. EdgeConneX’s Japan buildout exemplifies platforms engineered for service delivery over plain colocation.

By Data Center Size: Mega sites gain speed on large-site base

Large campuses captured 54.10% of the edge data center market in 2025 by balancing capacity with proximity. Yet Mega facilities are on track to post a 25.8% CAGR through 2031 as hyperscalers transplant design playbooks to metro-adjacent parcels. Deploying a single 100-MW node often reduces cooling and power costs 20-25% relative to scattering smaller rooms.

Telecom operators still lean on Medium enclosures for 5G edge lattices, but cloud majors favor Mega cells for regional service planes. Scala’s USD 500 million “AI City” in Brazil typifies the model, serving an urban region instead of a single district.

By Tier Type: Tier 4 reliability commands premium pricing

Tier 3 remains the workhorse with 53.15% share in 2025, but Tier 4 is scaling at 25.3% CAGR as financial-trading and healthcare workloads demand 99.995% uptime. Deutsche Bank’s distributed-cloud stack relies on Tier 4 redundancy to underpin algorithmic trades that span millions of daily orders.

Operators accept 25-35% higher build costs because downtime risks eclipse infrastructure savings. Insurers often grant premium discounts when proofs show Tier 4 certification, strengthening the business case for capital outlays.

By End-User: IT & Telecom overtakes BFSI growth

BFSI held 28.85% of the edge data center market size in 2025 owing to real-time fraud detection and low-latency trading. The IT & Telecom cohort, however, will grow faster at 23.7% CAGR as carriers monetize 5G through edge APIs and AI inference. Retail smart-shelf pilots and factory predictive-maintenance suites add diversified demand. Audi, for instance, lifted overall equipment effectiveness 12% by processing ML models locally.

Government and smart-city programs also adopt nodes for traffic control and public-safety analytics. India’s rural “Bank on Wheels” processes transactions offline, syncing once connectivity resumes—a proof that edge designs reach beyond urban cores.

Geography Analysis

North America controlled 27.05% of edge data center market share in 2025 on the back of early 5G launches and mature fiber backbones. Growth is now tilting toward secondary metros where land is cheaper and grid headroom ample. Core Scientific’s USD 4 billion plan to convert bitcoin farms in Texas shows how legacy assets can be reborn for AI inference. Developers still grapple with 25-35% higher construction costs compared with global norms and with acute technician shortages outside coastal hubs.

Asia-Pacific is forecast to log a 24.2% CAGR, making it the prime driver of edge data center market expansion. China’s “New Infrastructure” and India’s Digital India initiatives embed local-processing mandates in national strategies. Digital Edge secured USD 1.6 billion to scale regional footprints as Tokyo and Jakarta vie for hub status. Build budgets run 40-50% below North American equivalents, while vocational programs churn a growing cadre of certified engineers.

Competitive Landscape

The edge data center market features moderate concentration. Equinix, Digital Realty, and Microsoft anchor global portfolios, while EdgeConneX, Vapor IO, and Compass Datacenters specialize in distributed formats. Partnerships outweigh zero-sum rivalry: Verizon meshes its fiber access with NVIDIA GPUs to market turnkey AI hubs. Sustainability stands out as a tiebreaker; providers that overlay micro-grids and free-cooling routinely trim operating costs 15-20% and win ESG-minded tenants.

Niche innovators exploit gaps. PowerSecure pairs with Edged Energy to embed on-site generators, lowering grid dependence. Metrobloks raised USD 5.2 million for curb-side micro-data-centers in bustling urban cores. AI-assisted maintenance cuts trouble tickets by one-fifth and keeps staffing lean, advantages that resonate as wage inflation rises.

Edge Data Center Industry Leaders

American Tower Corporation

DartPoints

Digital Realty Trust

EdgeConneX

H5 Data Centers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Brazil’s Patria launched a USD 1 billion data-center platform targeting São Paulo and Mexico City markets.

- May 2025: Chesapeake Planning Commission rejected the city’s first large-scale data-center proposal after environmental pushback.

- January 2025: Brookfield opened talks to bring new investors into Ascenty, its Brazilian unit, to accelerate expansion.

- January 2025: TPA Group unveiled plans for a USD 5 billion, nine-building campus in Newton County, Georgia, for completion by 2030.

Global Edge Data Center Market Report Scope

An edge data center is a small data center that is located close to the edge of a network. It provides the same device found in traditional data centers but is contained in a smaller footprint, closer to end users and devices.

The edge data center market is segmented by component (solution, services), by facility (small and medium facility, large facility), by end-user (IT and telecom, BFSI, government, healthcare, manufacturing, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solution |

| Services |

| Small |

| Medium |

| Large |

| Massive |

| Mega |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| IT and Telecom |

| BFSI |

| Government |

| Healthcare |

| Manufacturing |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solution | ||

| Services | |||

| By Data Center Size | Small | ||

| Medium | |||

| Large | |||

| Massive | |||

| Mega | |||

| By Tier Type | Tier 1 and 2 | ||

| Tier 3 | |||

| Tier 4 | |||

| By End-user | IT and Telecom | ||

| BFSI | |||

| Government | |||

| Healthcare | |||

| Manufacturing | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the edge data center market?

The edge data center market size stands at USD 22.21 billion in 2026 and is projected to reach USD 62.18 billion by 2031.

Which component segment is growing fastest?

Services are expanding at a 23.96% CAGR as enterprises lean on managed offerings to offset talent shortages in distributed operations.

Why are Mega facilities gaining traction?

Mega sites deliver economies of scale that cut cooling and power costs up to 25% while still sitting close enough to users for sub-10 ms latency.

Which region will add the most capacity by 2031?

Asia-Pacific, supported by China’s “New Infrastructure” and India’s Digital India programs, is forecast to grow at a 24.2% CAGR, outpacing all other regions.

Page last updated on: