Edge Computing In Automotive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

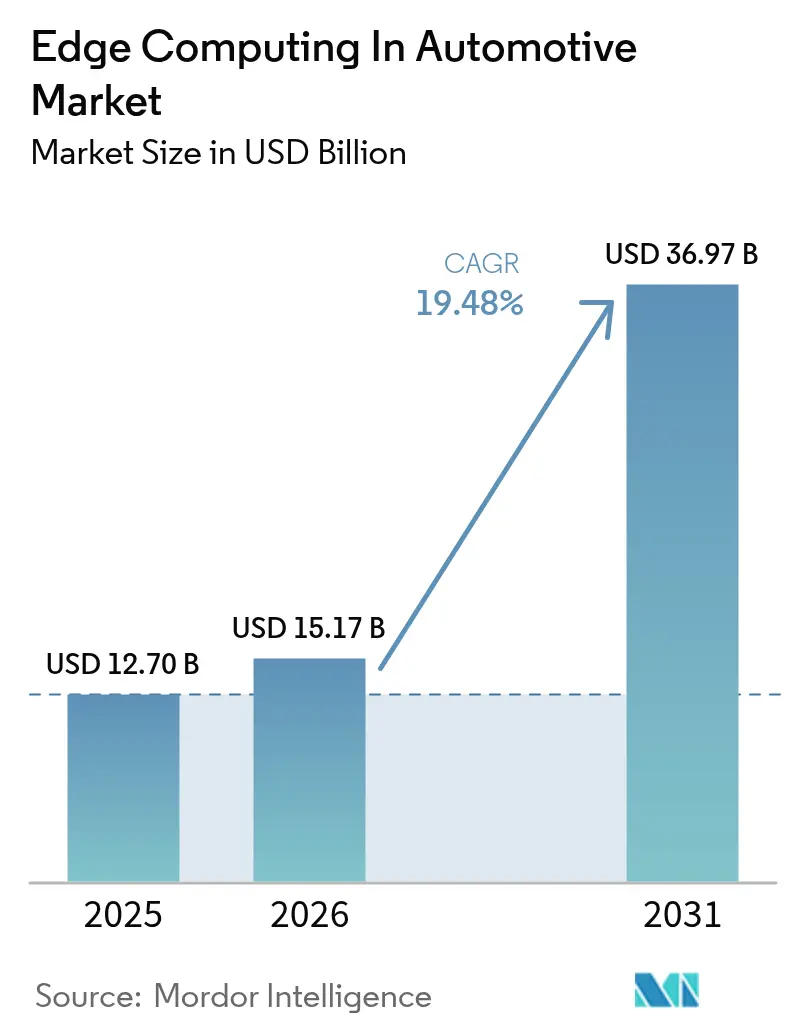

| Market Size (2026) | USD 15.17 Billion |

| Market Size (2031) | USD 36.97 Billion |

| Growth Rate (2026 - 2031) | 19.48% CAGR |

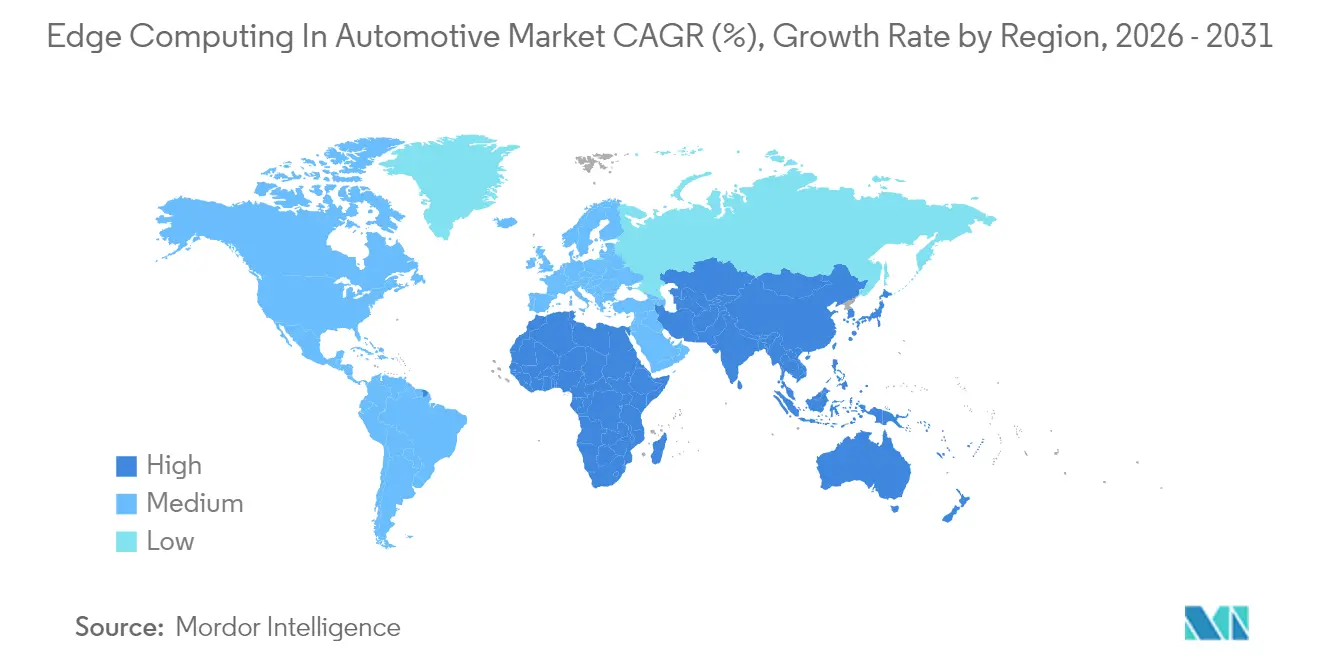

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Edge Computing In Automotive Market Analysis by Mordor Intelligence

The edge computing in automotive market size in 2026 is estimated at USD 15.17 billion, growing from 2025 value of USD 12.7 billion with 2031 projections showing USD 36.97 billion, growing at 19.48% CAGR over 2026-2031. Growth springs from the swelling volume of vehicle-generated data, the spread of 5G low-latency networks, and safety regulations that make real-time Vehicle-to-Everything processing non-negotiable. Carmakers now redesign vehicles around software rather than mechanics, which pushes processing out of remote clouds and into distributed in-vehicle and roadside nodes. Hardware keeps the revenue lead because purpose-built silicon must meet harsh automotive requirements, yet services expand fastest as manufacturers outsource integration and lifecycle support. Regional demand pivots toward Asia-Pacific where electric-vehicle uptake, government incentives, and smart-city spending converge to reshape deployment economics.[1]Deutsche Telekom, “Car2MEC Project Achieves Low Latency for V2X,” telekom.com

Key Report Takeaways

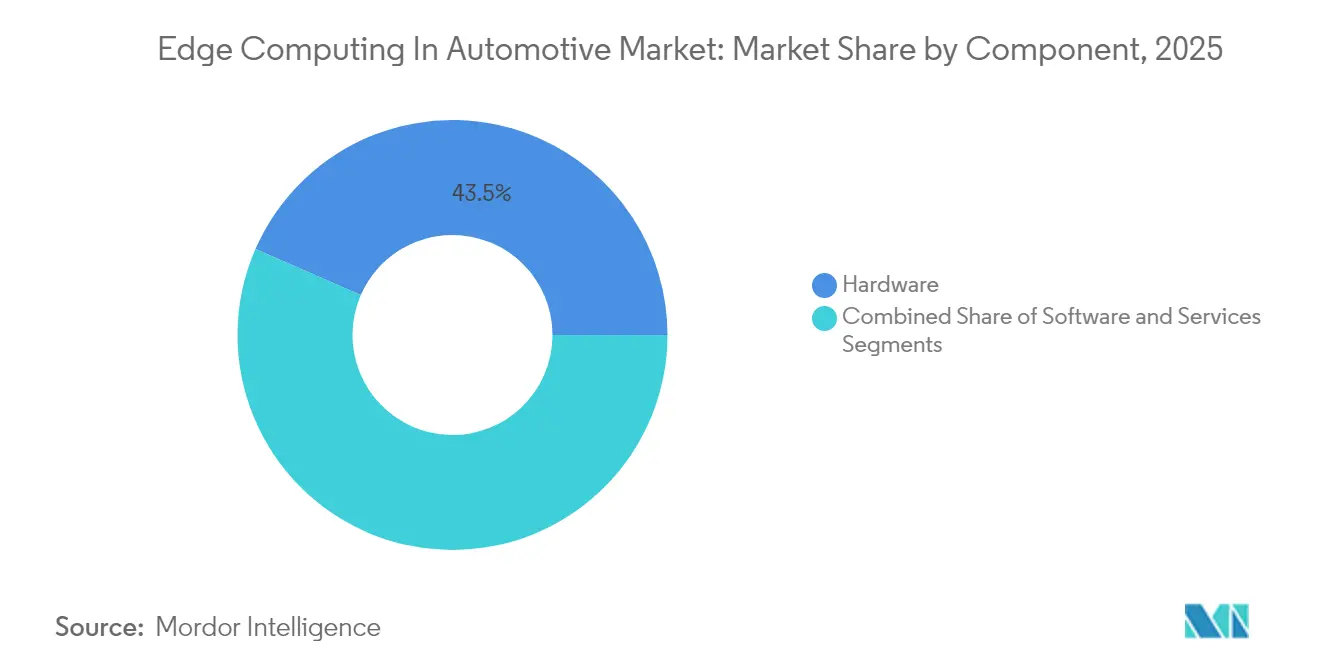

- By component, hardware led with 43.45% of the edge computing in automotive market share in 2025, while services are on track for a 24.89% CAGR through 2031.

- By deployment model, on-board vehicle edge held 46.02% of the edge computing in automotive market share in 2025, infrastructure edge is set to grow at 21.55% CAGR to 2031.

- By vehicle type, passenger cars accounted for 50.55% of the edge computing in automotive market share in 2025; heavy commercial vehicles are poised for a 22.05% CAGR between 2026-2031.

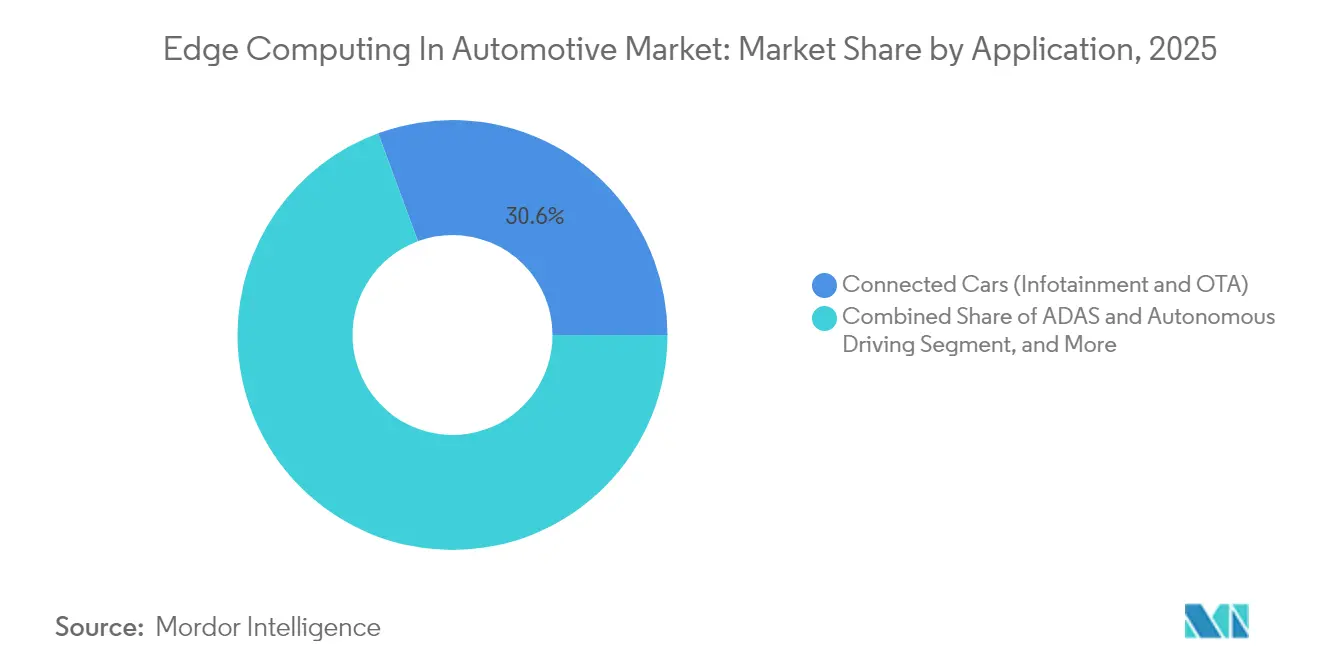

- By application, connected-car features retained a 30.62% of the edge computing in automotive market share in 2025, autonomous-driving workloads will accelerate at 25.74% CAGR to 2031.

- By geography, North America commanded 34.95% of the edge computing in automotive market share in 2025, whereas Asia-Pacific is projected to log a 24.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Edge Computing In Automotive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of vehicle sensors and 5G roll-outs | +4.20% | Global, with early gains in North America, EU, and China | Medium term (2-4 years) |

| OEM shift toward software-defined vehicles | +3.80% | Global, led by premium segments in North America and Europe | Long term (≥ 4 years) |

| Regulatory support for V2X safety mandates | +2.90% | North America and EU regulatory zones, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rising IoT data traffic per car | +2.10% | Global, concentrated in connected vehicle markets | Short term (≤ 2 years) |

| Deployment of curb-side micro-edge nodes by cities | +1.80% | Smart cities in North America, EU, and select Asia-Pacific metros | Long term (≥ 4 years) |

| Battery-friendly in-vehicle AI accelerators cut TCO | +1.60% | Electric vehicle markets globally, led by China and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mainstream – Proliferation of Vehicle Sensors and 5G Rollouts

Modern cars host up to 200 sensors that stream 25 GB of data per hour, a volume that overwhelms legacy architectures. 5G radio access now delivers sub-10 ms latency, demonstrated when Deutsche Telekom and Nokia cut V2X delays below 30 ms in the Car2MEC trials. Carmakers therefore embed local processing to classify, compress, and react to hazards before forwarding essential insights to the cloud. The outcome is a decisive tilt from central to distributed compute, which underpins rising hardware demand and reinforces the edge computing in automotive market’s rapid CAGR.

Mainstream – OEM Shift Toward Software-Defined Vehicles

Manufacturers rewrite their business models around code updates and digital features. Bosch and Volkswagen’s Cariad arm assigned 1,000 engineers to co-develop AI platforms slated for 2025 vehicles. Always-connected cars now require secure, over-the-air software pipes plus high-performance in-vehicle compute to validate and roll back code safely. These workflows enlarge service revenue pools and elevate the edge computing in automotive market as a core monetization pillar.[2]Bosch, “Bosch and Cariad Expand Automated Driving Alliance,” bosch.com

Under-the-radar – Curb-side Micro-edge Nodes by Cities

Municipalities discreetly retrofit lamp posts and traffic lights with compact compute boxes. Peachtree Corners, Georgia invested USD 4 million in Qualcomm-based roadside units that run on the 5.9 GHz safety band and optimize intersections in real time. Offloading heavy analytics to curb-side nodes trims vehicle hardware budgets, introduces redundancy, and opens ad-supported revenue streams for cities.[3]Qualcomm, “Peachtree Corners Deploys C-V2X Roadside Units,” qualcomm.com

Under-the-radar – Battery-friendly In-vehicle AI Accelerators Cut TCO

Start-ups refine neural-processing units that sip energy yet match inference throughput. Expedera secured USD 20 million to commercialize such IP, enabling continuous driver-monitoring cameras without eroding electric-vehicle range. Lower power draw shrinks cooling systems and battery packs, softening total cost of ownership and drawing fleets into the edge computing in automotive market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront infrastructure capex | -2.80% | Global, particularly affecting emerging markets | Short term (≤ 2 years) |

| Cyber-security and data-sovereignty risks | -2.10% | Global, with heightened concerns in EU and China | Medium term (2-4 years) |

| Scarcity of automotive-grade edge silicon supply | -1.90% | Global supply chain, acute in Asia-pacific manufacturing hubs | Short term (≤ 2 years) |

| Fragmented MEC interoperability standards | -1.40% | Global, with regional variations in implementation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mainstream – High Upfront Infrastructure Capex

Complete edge stacks bundle compute nodes, private 5G, and hardened security, a combination that pushed Verizon and Audi’s German test site budget past USD 10 million. Capital intensity deters smaller OEMs and stalls projects in price-sensitive regions. Consequently, deployments prioritize functions that yield immediate safety payback while broader optimization waits for cost curves to drop.

Mainstream – Cyber-security and Data-sovereignty Risks

Distributed nodes multiply attack vectors and expose safety systems to remote intrusion. New UNECE WP.29 mandates drive continuous risk management and local data storage inside EU borders, tightening the compliance burden. OEMs are compelled to harden every micro-edge box, inflating costs and stretching scarce cybersecurity talent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Faces Services Disruption

Hardware captured 43.45% revenue in 2025, underscoring the essential role of rugged processors, AI accelerators, and thermal solutions inside vehicles. This slice translates to the largest edge computing in automotive market share thanks to silicon that tolerates vibration and 125 °C ambient. In dollar terms the edge computing in automotive market size for hardware will still climb, yet services enjoy a steeper 24.89% CAGR as integrators manage over-the-air rollouts for mixed global fleets. Automakers gravitate toward turnkey services because the learning curve for functional safety, cybersecurity, and real-time scheduling is steep. Suppliers such as Intel—after absorbing Silicon Mobility—bundle chips with middleware and long-term update contracts. The shift channels margin away from pure-play hardware and pushes platform vendors to partner with cloud operators for joint lifecycle offerings, reinforcing service momentum.

By Deployment Model: Infrastructure Edge Challenges Vehicle-Centric Approaches

On-board compute retained 46.02% of 2025 revenue, underlining OEM confidence in self-contained reliability. Still, infrastructure nodes are tracking a 21.55% CAGR as smart-city budgets finance roadside boxes that extend awareness beyond a single car. This growth enlarges the edge computing in automotive market size for public edge assets and invites telecom carriers and municipalities into revenue-sharing schemes. Hybrid topologies are emerging whereby vehicle, network, and curb-side processors cooperate. The Automotive Edge Computing Consortium promotes such split-compute frameworks to optimize cost and latency. Carmakers must now certify software across heterogeneous domains, elevating interoperability toolchains and driving standards activity.

By Application: Autonomous Driving Outpaces Connected-Car Growth

Connected-car services held 30.62% share in 2025, a legacy anchored by infotainment and telematics. Autonomous-driving stacks however will sprint at 25.74% CAGR, lifting their weight inside the overall edge computing in automotive market size. NVIDIA’s DRIVE Hyperion integrates multiple AI accelerators that together process six cameras, five radars, and three lidars in real time. Embedded language models such as Cerence CaLLM Edge now run entirely on-board, removing dependence on cellular coverage and keeping response latency below 200 ms. Growing compute density inside vehicles shifts data-plan economics and creates fresh licensing revenue for software IP vendors.

By Vehicle Type: Commercial Vehicles Drive Autonomous Edge Adoption

Passenger cars delivered 50.55% of 2025 turnover, primarily because of volume production. Yet heavy commercial vehicles will notch a 22.05% CAGR to 2031, making them the fastest climber within the edge computing in automotive market. Route-based fleets can amortize premium compute over predictable mileage, and autonomous freight pilots, such as Aurora’s Dallas-Houston corridor, show payback through driver cost avoidance.

Off-highway machinery taps edge nodes for autonomy in mines or farms where connectivity is sparse. Volvo’s VNL Autonomous truck platform layers dual redundant computers to meet an SAE Level 4 operational-safety envelope. These use cases cement the edge computing in automotive industry’s diversification beyond consumer mobility.

Geography Analysis

North America led with 34.95% revenue in 2025, supported by early 5G rollouts, orderly spectrum policy, and tight OEM-tech partnerships. Tesla, General Motors, and Ford pair with Intel, NVIDIA, and Qualcomm to co-design application-specific processors and testing regimes. Verizon’s private-network program underscores the region’s readiness to scale low-latency automotive workloads. Funding incentives at state and federal levels further anchor edge labs and pilot corridors. Asia-Pacific is forecast to register a 24.12% CAGR to 2031. China merges electric-vehicle subsidies, vast consumer volumes, and city-led smart-transport schemes, creating a fertile edge computing in automotive market. Huawei’s launch of 100 autonomous 5G-A mine trucks in Inner Mongolia illustrates industrial-grade deployment under harsh conditions. Japan and South Korea supply advanced semiconductor nodes, while India positions talent hubs that write in-vehicle software for global OEMs. Europe maintains momentum through premium marques and strict safety law. UNECE WP.29 and GDPR force rigorous cybersecurity and data-localization, raising the baseline for edge solutions. Bosch and Microsoft now co-produce generative-AI toolchains that comply with ISO 26262 functional-safety standards. Pan-EU digital strategies and cross-border 5G corridors allow continuous roaming for autonomous trucks between Germany, Austria, and Italy.

Regulatory Landscape

Regulation increasingly ties edge computing architecture to vehicle type-approval, software update governance, and cybersecurity-by-design. In the European Union, the EU AI Act (Regulation (EU) 2024/1689) entered into force on August 1, 2024, and classifies certain automotive AI systems integrated into regulated products as high-risk, prompting OEMs and suppliers to embed risk management, robustness, and documentation processes into their in-vehicle and roadside edge stacks.

Globally, UNECE WP.29 regulations remain core compliance anchors for connected, updateable vehicles. UN Regulation No. 155 requires a Cyber Security Management System (CSMS) for type approval, and UN Regulation No. 156 requires a Software Update Management System (SUMS), commonly implemented using ISO/SAE 21434 practices. In the United States, the Department of Transportation highlighted accelerated autonomous vehicle rulemaking activity in its 2026 regulatory agenda, reinforcing the need for auditable, safety-aligned data processing and secure OTA workflows across distributed automotive edge nodes.

Value Chain Analysis

The value chain spans automotive-grade silicon and modules (processors, AI accelerators, automotive Ethernet, and secure elements), middleware and virtualization (real-time OS, hypervisors, safety middleware, OTA clients), and system integration into vehicle E/E architectures (domain and zonal controllers). It is followed by validation and certification against functional safety and cybersecurity requirements. OEMs and tier-1 suppliers then operationalize these platforms through toolchains for fleet rollout, monitoring, and incident response, often using cloud platforms for simulation, CI/CD, and digital-twin pipelines that connect to in-vehicle and roadside edge runtimes.

Coordination across the chain is tightening around reference architectures and long-horizon supply relationships. The Automotive Edge Computing Consortium (AECC) published an Industry Blueprint in February 2026 to align interoperable edge, 5G, API, and cloud layers for connected-vehicle services, while ITU-T Supplement 86 (approved in January 2025) defines functional architecture elements for edge-enabled connected vehicle formations. In commercialization, Volkswagen Group signed a letter of intent with Qualcomm in January 2026 for Snapdragon Digital Chassis solutions supporting a zonal SDV architecture, and Stellantis expanded its collaboration with Qualcomm in May 2026 to adopt Snapdragon Digital Chassis platforms across next-generation vehicle architectures, highlighting how compute, connectivity, and software platforms are bundled and sourced as integrated edge building blocks.

Competitive Landscape

The edge computing in automotive market features moderate fragmentation. Semiconductor majors, Intel, NVIDIA, Qualcomm, invest in automotive-grade nodes, whereas tier-one suppliers like Continental, Bosch, and Aptiv weave those chips into domain controllers. Cloud hyperscalers AWS and Microsoft leverage edge containers and digital-twin pipelines to secure OEM design wins. Competitive advantage hinges on vertical integration that marries silicon lifecycles to 15-year vehicle platforms, safety certification, and global update orchestration.

NVIDIA’s DRIVE platform bundles hardware, SDK, and validation tools, shortening time-to-market for SAE Level 3 functions. Continental aligns its new High-Performance Computer with Android Automotive OS, targeting cockpit consolidation. Infineon’s USD 2.5 billion buyout of Marvell’s automotive Ethernet unit enhances bandwidth between sensors and processors. Partnerships—not standalone products—are emerging as the dominant route to volume deployment, particularly where fleet operators demand turnkey uptime guarantees.

Edge Computing In Automotive Industry Leaders

Cisco Systems, Inc.

Amazon Web Services, Inc.

Huawei Technologies Co., Ltd.

Hewlett Packard Enterprise Development LP

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity lies in moving pilot-grade connected and autonomous functions into repeatable, interoperable deployments across mixed fleets and mixed infrastructure ownership (OEM, telecom, city). The AECC Industry Blueprint 1.0 (February 2026) provides a vendor-neutral system requirements baseline across connectivity, computation, data management, and security, creating whitespace for vendors to productize compliant messaging, policy, and orchestration layers that work across on-board vehicle edge, network/MEC edge, and roadside infrastructure edge.

Edge AI in software-defined vehicles is also extending beyond perception into energy, calibration, and maintenance workflows that benefit from local latency and data sovereignty. SAE International Technical Paper 2026-26-0686 (January 2026) details in-vehicle edge AI use cases such as adaptive energy management, real-time powertrain calibration, and predictive diagnostics, supporting demand for automotive-grade AI runtimes and lifecycle services (model updates, validation, rollback) delivered through secure OTA pipelines. As architectures shift toward hybrid in-vehicle and infrastructure edge, suppliers that can arbitrate workloads across edge-to-cloud boundaries, while maintaining cybersecurity and type-approval traceability, gain a clearer route to scale alongside OEM SDV programs.

Recent Industry Developments

- July 2026: SiMa.ai and Cisco announced a go-to-market collaboration to integrate the SiMa.ai Modalix AI platform with Cisco IE3500 industrial switches for edge AI deployments, including automotive manufacturing environments. The pairing targets on-premise inference and rugged networking at the factory edge, supporting faster AI-enabled quality and process control that feeds back into automotive software and compute roadmaps.

- April 2026: Huawei said it planned to invest 18 billion yuan in smart driving R&D during 2026. The commitment reinforces a full-stack push spanning in-vehicle compute, software, and intelligent driving capabilities, increasing competitive pressure on automotive edge platforms in China-centric ecosystems.

- January 2026: AWS and AUMOVIO announced a strategic agreement that positions AWS as the preferred cloud provider for AUMOVIOs autonomous driving development work, including simulation and AI tooling tied to vehicle programs. The agreement strengthens cloud-to-edge development pipelines used to build, validate, and continuously update ADAS and autonomous workloads that ultimately run on in-vehicle and distributed edge nodes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers spending linked to computing and analytics done near automotive data sources, either inside the vehicle or in nearby network and roadside locations, where low latency and local decision making matter. Revenues are counted across solutions used by the automotive ecosystem for connected, assisted, and autonomous use cases.

Scope exclusions: Pure cloud-only processing that occurs in centralized data centers without an edge execution layer is excluded from this sizing.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Deployment Model

- On-board Vehicle Edge

- Network/MEC Edge

- Infrastructure Edge (Road-side and Smart City)

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Off-highway and Specialty Vehicles

- By Application

- Connected Cars (Infotainment and OTA)

- ADAS and Autonomous Driving

- Traffic Management and V2I

- Fleet and Logistics Optimisation

- Smart Cities Services

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Israel

- Africa

- South Africa

- Nigeria

- Egypt

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the real demand pool and keep assumptions realistic before any forecasting was attempted. We leaned on public sources such as NHTSA and Euro NCAP materials for safety feature adoption signals, ITU and 3GPP releases for connectivity direction, and UNECE vehicle cybersecurity and software update regulations to understand compliance-driven deployments.

We also used sources such as national transport departments and customs and trade statistics for electronics and telecom equipment flows, peer reviewed papers on in-vehicle compute architectures, and patent databases to spot where edge inference and vehicle gateway designs are being prioritized. Company filings, investor decks, and reputable automotive and telecom press helped confirm product timing, pricing direction, and partnership structures. For cross-checks, paid subscriptions were used selectively for company financials and intelligence, news and financials, and patent coverage. These examples are not exhaustive, and many other public and paid sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually being deployed at the vehicle edge, network edge (MEC), and roadside edge, and then confirming how revenues are recognized across hardware, software, and services. We spoke with a mix of automotive OEM and supplier functions, telecom and infrastructure stakeholders, and solution architects across APAC, EMEA, and the Americas to pressure-test adoption timing, typical attach rates, and pricing trends.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 15% | APAC: 43% |

| Mid tier: 57% | Functional/Unit leaders: 32% | EMEA: 37% |

| Smaller Players: 18% | Managers: 53% | Americas: 20% |

Market-Sizing & Forecasting

Sizing started with a top-down build where vehicle production and parc, combined with connectivity readiness, were used to reconstruct the addressable pool for edge-enabled automotive use cases by region. From there, the model applied penetration curves for key deployments, and then translated them into value using typical system pricing and recurring software and service charges.

Inputs that mattered in this market included connected vehicle penetration, ADAS and domain controller fitment rates, cellular and V2X rollout progress, average compute content per vehicle platform, and the share of workloads pushed to on-board versus MEC or roadside nodes. Because pricing moves quickly, ASP paths were adjusted using interview feedback on compute module cost-down, software licensing approaches, and services attach.

The forecast relied mainly on scenario analysis, with base, conservative, and aggressive cases tied to regulation timing, OEM software roadmaps, and telecom edge coverage maturity. Results were corroborated with selective bottom-up approximations like sampled ASP time-volume for representative vehicle programs and channel checks on edge software deployments, and then gaps were handled by using proxy fitment rates from similar platforms where direct disclosure was limited.

Data Validation & Update Cycle

Validation was done through several checks so the totals stayed consistent with real-world signals. We compared outputs against independent indicators like connected car shipments, ADAS feature installation rates, and regional telecom edge investment patterns, and then reviewed outliers at the segment and region level before sign-off.

When a variance looked material, assumptions were rechecked and respondents were re-contacted to clarify pricing, bundling, or timing shifts. Reports are refreshed annually, and interim updates are made when material events occur, such as regulation changes, major platform launches, or sudden supply constraints. Before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's Automotive Edge Computing Market Size Measured Against Other Published Estimates

Published market sizes for automotive edge computing often do not match because the counted items, the year used as the starting point, and the way recurring software and services are treated can vary from one source to another. Differences also show up when one estimate leans heavily on forward-looking adoption promises instead of checking them against current vehicle programs and network rollout realities.

Cloud-only centralized analytics is excluded here, and it sits outside Mordor Intelligence's scope for this market, which is one reason some larger totals are not directly comparable. On the other side, some smaller totals happen when only in-vehicle hardware is counted and MEC, roadside edge nodes, and related software and services are left out, or when currency conversion timing and inflation treatment differ across the same year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.17 B (2026) | |

| Global Consultancy A | USD 14.70 B (2025) | Uses an earlier base year and a broader umbrella that commonly blends adjacent compute layers and spending buckets, which can shift totals even when CAGR looks similar. |

| Industry Publisher B | USD 5.84 B (2025) | Tends to emphasize a narrower definition closer to platform or in-vehicle deployments, which can undercount network edge and roadside use cases, along with recurring software and services. |

The spread mainly comes from what gets counted as edge in automotive and how quickly adoption is assumed to scale across vehicle lines and regions. By keeping the inputs tied to observable vehicle fitment, connectivity readiness, and realistic ASP paths, the estimate stays traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the edge computing in automotive market?

The market stands at USD 15.17 billion in 2026 and is projected to reach USD 36.97 billion by 2031, reflecting a 19.48% CAGR.

Which component segment grows fastest?

Services are projected to expand at 24.89% CAGR through 2031 as manufacturers outsource integration and lifecycle support.

Why are commercial vehicles critical for growth?

Heavy trucks face driver shortages and high fuel costs; autonomous-ready edge platforms promise operational savings, driving a 22.05% CAGR for the segment.

Which region will record the highest growth rate?

Asia-Pacific is forecast to post a 24.12% CAGR thanks to China’s EV momentum, expansive 5G rollouts, and smart-city investments.

What are the main restraints facing adoption?

High upfront infrastructure costs, cybersecurity compliance, silicon shortages, and fragmented MEC standards together shave several percentage points off the forecast CAGR.

How fragmented is the competitive landscape?

Moderately: semiconductor leaders, tier-one automotive suppliers, and cloud hyperscalers all compete, with the top five firms controlling roughly 60% of revenue.

Page last updated on: