Mobile Edge Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 3.88 Billion |

| Growth Rate (2026 - 2031) | 30.10% CAGR |

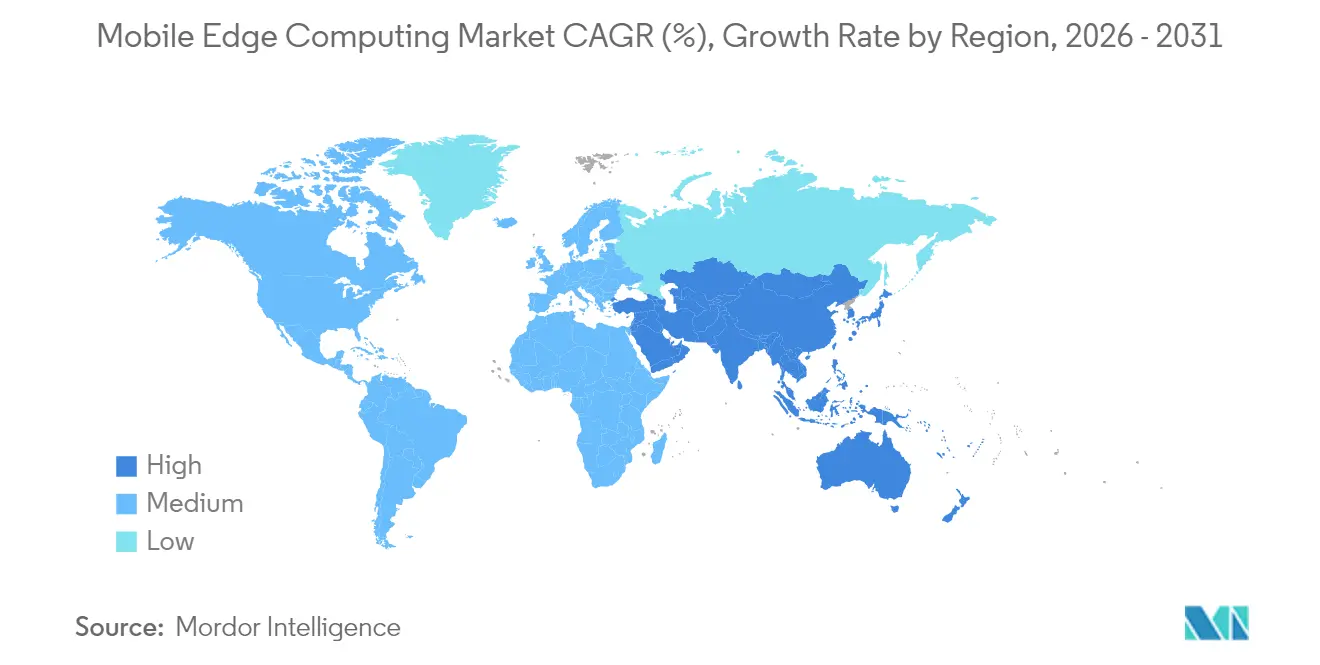

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Edge Computing Market Analysis by Mordor Intelligence

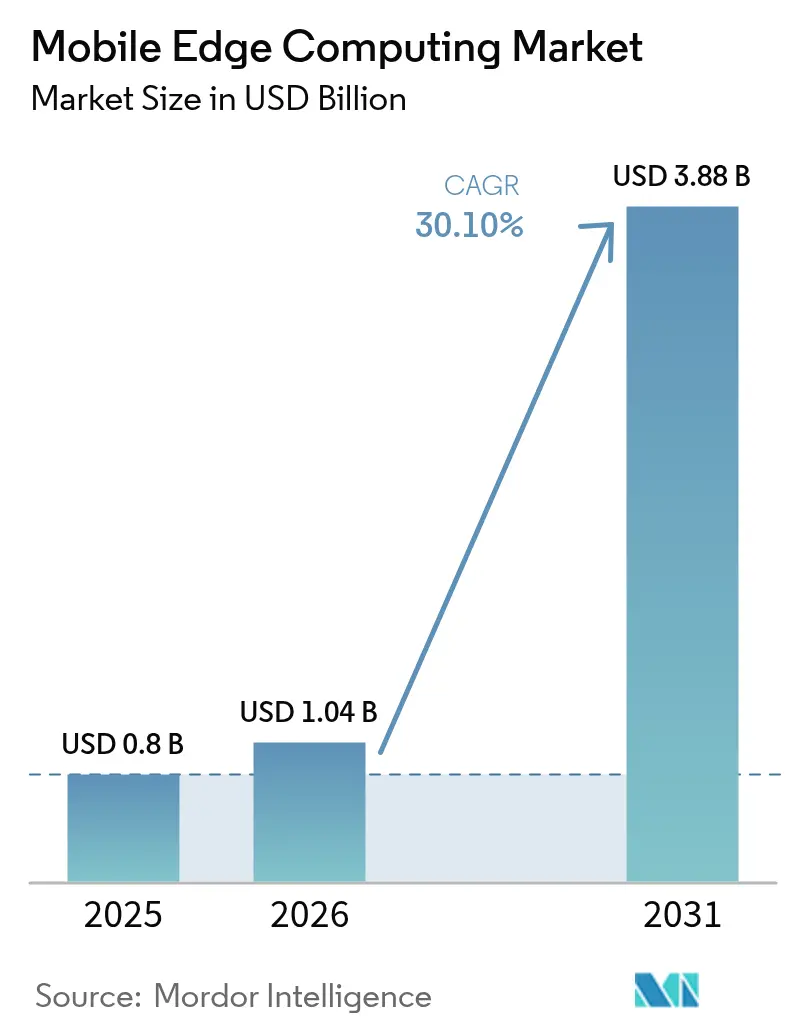

The mobile edge computing market size was valued at USD 0.80 billion in 2025 and estimated to grow from USD 1.04 billion in 2026 to reach USD 3.88 billion by 2031, at a CAGR of 30.10% during the forecast period (2026-2031). The intensifying demand for low-latency services, the maturation of 5G standalone (SA) networks, and the need to process ever-rising data volumes closer to end-users are accelerating adoption. Hardware continues to anchor spending, yet rapid progress in software-defined infrastructure, container orchestration, and AI inference is shifting the balance toward service-centric revenue streams. Telcos, hyperscalers, and specialist start-ups increasingly view edge capabilities as a core differentiator that underpins premium connectivity, new enterprise services, and cost-effective AI deployment. Regulatory interest in data sovereignty, coupled with standardization efforts led by the European Telecommunications Standards Institute (ETSI), is further influencing market architecture and vendor strategies. Convergence among connectivity, cloud, and AI domains is reshaping competitive boundaries, compelling players to pursue cross-domain partnerships and vertical-specific solutions.

Key Report Takeaways

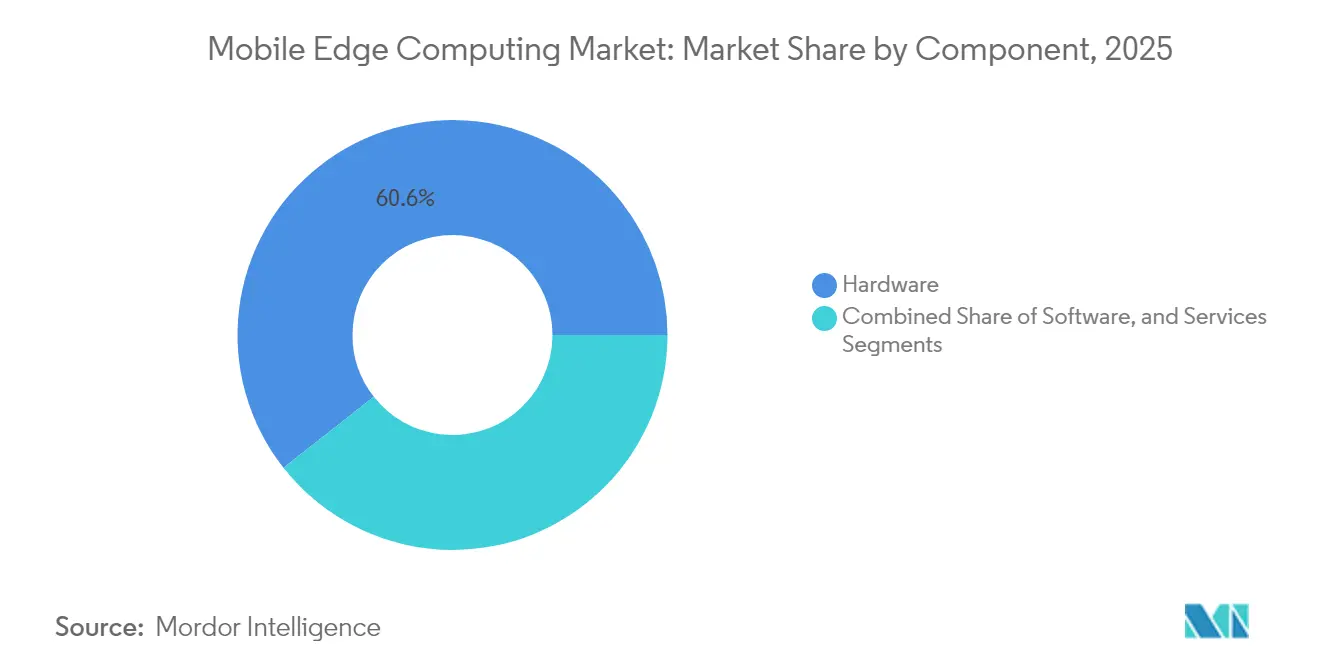

- By component, hardware led with 60.60% revenue share in 2025, while software is forecast to expand at a 36.2% CAGR through 2031.

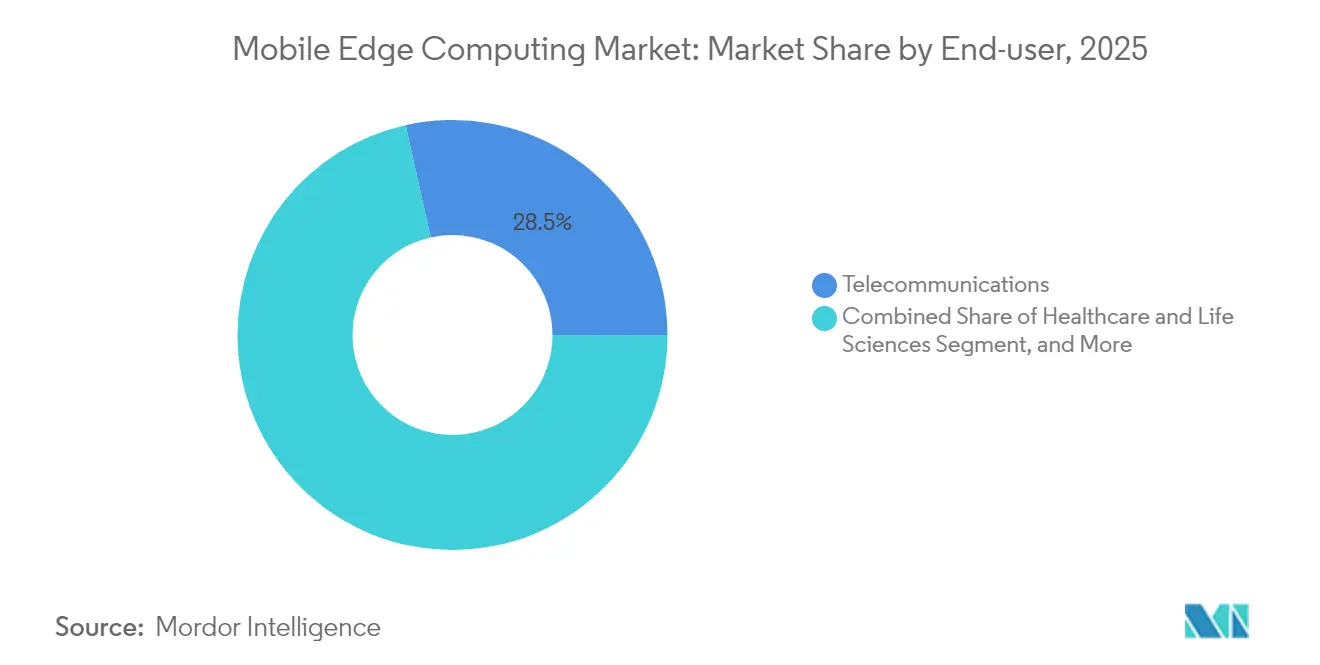

- By end-user, telecommunications accounted for 28.50% of the mobile edge computing market share in 2025; healthcare and life sciences are expected to grow at the fastest rate, with a 40.6% CAGR, from 2026 to 2031.

- By geography, North America accounted for 40.80% of the mobile edge computing market in 2025; Asia-Pacific is poised to grow at a 35.4% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile Edge Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Latency-critical consumer apps (AR/VR gaming, livestreaming) gaining traction in Asia | + 7.80% | Asia-Pacific, North America | Medium term (2-4 years) |

| Rapid 5G standalone roll-outs unlocking MEC monetization in North America | + 6.30% | North America, Europe | Short term (≤2 years) |

| Telco adoption of disaggregated Open RAN driving on-prem edge demand in Europe | +4.70% | Europe, North America | Medium term (2-4 years) |

| Industrial Time-Sensitive Networking mandates (IEC/IEEE 60802) in manufacturing hubs | +3.80% | Europe, North America, East Asia | Medium term (2-4 years) |

| Government smart-city megaprojects (NEOM, Saudi Arabia) embedding MEC | +3.10% | Middle East, Asia-Pacific | Long term (≥4 years) |

| AI-inferencing at the edge lowering cloud egress costs for hyperscalers | +2.50% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Latency-critical consumer apps (AR/VR gaming, livestreaming) gaining traction in Asia

AR/VR gaming and livestreaming continue to reshape network design by demanding sub-20 millisecond round-trip latency. Ericsson’s trials demonstrate that relocating game servers to edge nodes can reduce transport latency by 75%, enabling sustained fluid gameplay under fluctuating radio conditions. [1]Ericsson, “Cloud gaming over 5G SA,” ericsson.comTelecom operators in South Korea, where mobile gaming revenue exceeded USD 5.6 billion in 2024, have already deployed multi-access edge computing clusters near dense urban zones, enabling premium subscription tiers for latency-sensitive titles. Content providers benefit from higher retention and revenue per user, while operators monetize the differentiated quality of experience. Similar patterns are emerging in Japan, China, and select U.S. markets as 5G SA coverage expands and device adoption grows.

Rapid 5G standalone roll-outs unlocking MEC monetization in North America

Forty-nine operators in 29 countries had launched 5G SA by mid-2024, but North American carriers lead in national coverage. T-Mobile’s full-scale SA deployment permits deterministic network slicing aligned with edge workloads and underpins new service-level agreements for enterprise applications. Verizon targets sub-10 millisecond edge latency to enable VR, autonomous mobility, and real-time analytics. Revenue opportunities stem from pay-as-you-go exposure of network APIs, including quality-on-demand and location-based compute. Collaboration with hyperscalers accelerates application onboarding and shortens time-to-market for developers.

Telco adoption of disaggregated Open RAN driving on-prem edge demand in Europe

Vodafone’s pilot in Italy demonstrates how containerized baseband software running on Dell’s XR8000 server allows baseband processing and edge workloads to share the same rugged platform. The U.K. government targets 35% of nationwide traffic to pass through open networks by 2035, stimulating vendor diversity and localized compute. Open RAN’s reliance on standardized hardware pushes compute functions from centralized data centers to sites at or near radio units, creating fresh demand for compact edge servers and orchestration software.

Industrial Time-Sensitive Networking mandates (IEC/IEEE 60802) in manufacturing hubs

Manufacturers pursuing deterministic Ethernet rely on edge gateways to deliver sub-millisecond jitter and synchronized time across devices. Phoenix Contact demonstrated deterministic traffic scheduling via TSN edge switches that prioritize mission-critical packets while supporting concurrent IT traffic. Global TSN spending is forecast to reach USD 1.7 billion by 2028, and edge platforms capable of hosting AI-driven quality inspection models in real time are becoming mandatory in automotive, electronics, and pharmaceutical plants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absence of globally harmonized security & trust framework for multi-access edge | -4.70% | Global | Medium term (2-4 years) |

| Scarcity of ruggedized micro-data-center hardware in tropical & desert climates | -3.10% | Middle East, Southeast Asia, Latin America | Short term (≤2 years) |

| High TCO of edge orchestration platforms for Tier-2/3 mobile operators | -2.50% | Global (emerging markets) | Medium term (2-4 years) |

| Shortage of MEC-skilled DevOps talent delaying PoC-to-production conversions | -1.60% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Absence of globally harmonized security & trust framework for multi-access edge

Edge infrastructure widens the attack surface because workloads, data, and orchestration span thousands of unattended nodes. Academic studies show a surge in DDoS and lateral-movement threats targeting cached content and orchestration APIs. Regulated sectors hesitate to migrate sensitive workloads until zero-trust reference models, secure enclave support, and federated identity standards mature. ETSI MEC working groups are drafting inter-domain trust specifications, yet full consensus remains years away, prolonging integration cycles and increasing compliance costs for multinational deployments.

Scarcity of ruggedized micro-data-center hardware in extreme climates

Ambient temperatures above 45 °C, airborne dust, and saline humidity diminish equipment lifespan and force operators to derate performance. The U.S. Department of Defense’s Climate Adaptation Plan calls for resilience upgrades for edge compute used in field operations. In commercial contexts, power-efficient liquid cooling and sealed chassis designs carry a 20–30% cost premium, impeding ROI for projects in the Arabian Peninsula and equatorial Southeast Asia.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Outpaces Hardware Growth

In 2025 the hardware segment accounted for 60.60% of mobile edge computing market revenue, anchored by investments in servers, rugged enclosures, and specialized network interface cards. Nevertheless, software is projected to grow at a 36.2% CAGR between 2026 and 2031, significantly outpacing the overall mobile edge computing market growth rate, as orchestration, CI/CD pipelines, and AI frameworks enable flexible deployment models. Edge orchestration suites now combine service meshes with policy engines that translate network slices into compute and storage reservations, enabling operators to launch new services in hours instead of months.

By 2025, software-defined functions will embed AI-powered resource schedulers, predictive maintenance, and zero-touch provisioning. Akamai’s adoption of WebAssembly, alongside Fermyon, exemplifies lighter-weight execution that trims cold-start latency to sub-10 milliseconds, a prerequisite for interactive workloads. Consequently, hyperscalers and telcos are shifting their R&D budgets toward platform software, even as they continue to refresh edge hardware every four to five years. Services, consulting, integration, and managed operations are catching up as enterprises outsource complexity. The demand for multi-vendor blueprints is particularly high among healthcare and manufacturing clients that operate hybrid private/public edge footprints.

By End-user: Healthcare Leads Growth Trajectory

Telecommunications retained 28.50% of 2025 revenue because operators leverage existing network infrastructure to host edge computing. Yet, the healthcare and life sciences sector is expected to post a 40.6% CAGR to 2031, reflecting the sector’s increasing demand for real-time diagnostics, operating-room video, and patient monitoring in bandwidth-constrained environments. Providers harness edge AI to anonymize data onsite before sharing with research clouds, easing compliance with patient-privacy rules.

Financial institutions deploy edge nodes near trading venues to shave microseconds off order execution, while retailers adopt localized recommendation engines that raised basket sizes by 25% in pilot stores. Manufacturers integrate predictive maintenance algorithms on the shop floor, benefitting from deterministic TSN backbones. Energy operators count on low-latency edge analytics for grid balancing and leak detection across distributed assets. Emerging adopters include transportation agencies that are integrating edge-enabled V2X (vehicle-to-everything) data exchanges to enhance traffic flow and safety.

Geography Analysis

North America generated 40.80% of mobile edge computing market revenue in 2025, leveraged by nationwide 5G SA connectivity, dense fiber backbones, and strong hyperscaler presence. AWS Wavelength Zones and Microsoft Azure Edge Zones have been deployed in more than 40 metropolitan areas, offering developers sub-20 millisecond round-trip latency for consumer and industrial apps . Regulatory scrutiny of cloud concentration prompts carriers to diversify suppliers, spurring collaborative ventures with infrastructure companies and semiconductor vendors.

Asia-Pacific is expected to register the fastest growth, at a 35.4% CAGR during 2026-2031, driven by multi-billion-dollar smart-city investments, robust manufacturing bases, and the world’s highest mobile-gaming spending. China Mobile’s trials with Huawei illustrate nation-scale edge roll-outs supporting AR-assisted maintenance on high-speed rail. Japan’s telcos partner with console publishers to stream AAA titles without downloads, whereas India’s Jio integrates MEC to reduce backhaul congestion while expanding rural coverage.

Europe emphasizes industrial applications, privacy, and data localization. ETSI’s MEC standards assure cross-border service portability, and Vodafone’s commitment to deploy Open RAN across 30% of masts by 2030 underscores the region’s focus on supply-chain resilience. The Middle East advances giga-projects such as NEOM that embed cognitive edge infrastructure, while Africa and South America adopt MEC to alleviate latency for e-learning, telemedicine, and mining operations in remote zones.

Competitive Landscape

The mobile edge computing market features converging cohorts of network equipment vendors (Nokia, Ericsson, Huawei), cloud hyperscalers (AWS, Microsoft, Google), semiconductor firms (NVIDIA, Intel), and software-first innovators (Akamai, Fermyon). Strategic alliances have intensified; Vodafone’s 10-year pact with Microsoft couples Azure’s AI stack with carrier-grade edge sites across Europe, Africa, and the Asia-Pacific region. [3]Microsoft, “Vodafone-Microsoft strategic partnership,” microsoft.com

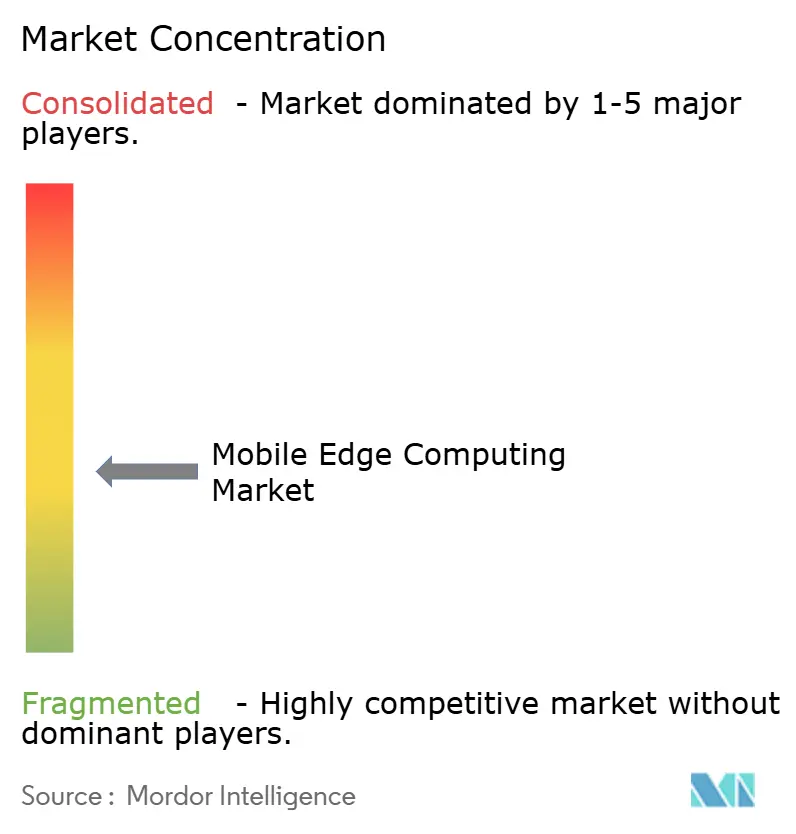

Product differentiation revolves around workload portability, AI acceleration, and industry-specific compliance. Equipment vendors leverage radio expertise to bundle MEC with Open RAN, promising operator-friendly integration. Hyperscalers attract developers via familiar DevOps tooling, while edge-native start-ups bet on ultralight serverless runtimes that reduce cost per function. The combined revenue share of the top five suppliers reached approximately 58% in 2024, reflecting moderate concentration yet leaving white-space for specialist providers that solve niche latency, security, or ruggedization challenges. Private-equity interest continues to fuel consolidation among regional data-center operators, indicating a path toward tighter aggregation.

Mobile Edge Computing Industry Leaders

Nokia Corporation

Telefonaktiebolaget LM Ericsson

AT&T Inc

Huawei Technologies Co. Ltd

Verizon Communications Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NXP Semiconductors acquired Kinara for USD 307 million to strengthen edge-AI portfolios in industrial and automotive domains

- April 2025: Advantech unveiled its “Edge Computing & WISE-Edge in Action” strategy, co-developing high-performance platforms with Intel and NVIDIA to accelerate digital transformation in smart manufacturing and healthcare

- March 2025: AWS introduced an Outposts server based on Graviton3 Arm chips, claiming 50–70% lower power draw for cloud RAN and MEC functions

- March 2025: Akamai and Fermyon partnered to deliver WebAssembly-based serverless and AI services with sub-millisecond cold starts on Akamai’s distributed cloud

Global Mobile Edge Computing Market Report Scope

Mobile edge computing (MEC) is evolving with integrated cloud services and resources closer to the user's proximity by leveraging the available resources in edge networks. The MEC platform aims to enable the billions of connected mobile devices to execute real-time compute-intensive applications directly at the network edge. It allows software applications to tap into local content, thereby accessing real-time information about local-access network conditions.

The Mobile Edge Computing Market is segmented by Component (Hardware and Software), End-User (Financial and Banking Industry, Retail, Healthcare and Life Sciences, Industrial, Energy and Utilities, and Telecommunication), and Geography. The report offers market forecasts and size in value (USD) for all the above segments.

| Hardware |

| Software |

| Services |

| Banking and Financial Services |

| Retail |

| Healthcare and Life Sciences |

| Industrial Manufacturing |

| Energy and Utilities |

| Telecommunications |

| Other End-users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By End-user | Banking and Financial Services | ||

| Retail | |||

| Healthcare and Life Sciences | |||

| Industrial Manufacturing | |||

| Energy and Utilities | |||

| Telecommunications | |||

| Other End-users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the Mobile Edge Computing Market?

The Mobile Edge Computing Market size is expected to reach USD 1.04 billion in 2026 and grow at a CAGR of 30.10% to reach USD 3.88 billion by 2031.

What is the current Mobile Edge Computing Market size?

In 2026, the Mobile Edge Computing Market size is expected to reach USD 1.04 billion.

What is driving the rapid growth of the mobile edge computing market?

Low-latency consumer apps, nationwide 5G standalone deployments, industrial Time-Sensitive Networking, and AI-inference cost savings collectively push the market toward a 30.10% CAGR through 2031.

Which component segment is growing fastest?

Software is projected to expand at a 36.2% CAGR as orchestration platforms, service meshes, and AI frameworks become essential for large-scale edge deployments.

Why is healthcare the fastest-growing end-user?

Edge computing enables real-time diagnostics, video analytics, and data privacy compliance in hospitals and remote clinics, supporting a 40.6% CAGR for healthcare applications.

How does 5G standalone influence edge adoption?

5G SA introduces network slicing and ultra-low latency, letting carriers monetize differentiated services that run on edge nodes positioned close to users.

What are the main challenges limiting adoption?

Lack of unified security standards, scarcity of ruggedized hardware for extreme climates, high orchestration platform costs for smaller operators, and shortages of MEC-skilled DevOps talent hinder wider rollout.

Who are the leading vendors in the market?

Ericsson, Nokia, Huawei, AWS, Microsoft, and Google jointly captured about 58% of 2024 revenue, reflecting moderate concentration with ongoing convergence among telecom, cloud, and semiconductor players.

Page last updated on: