Edge Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

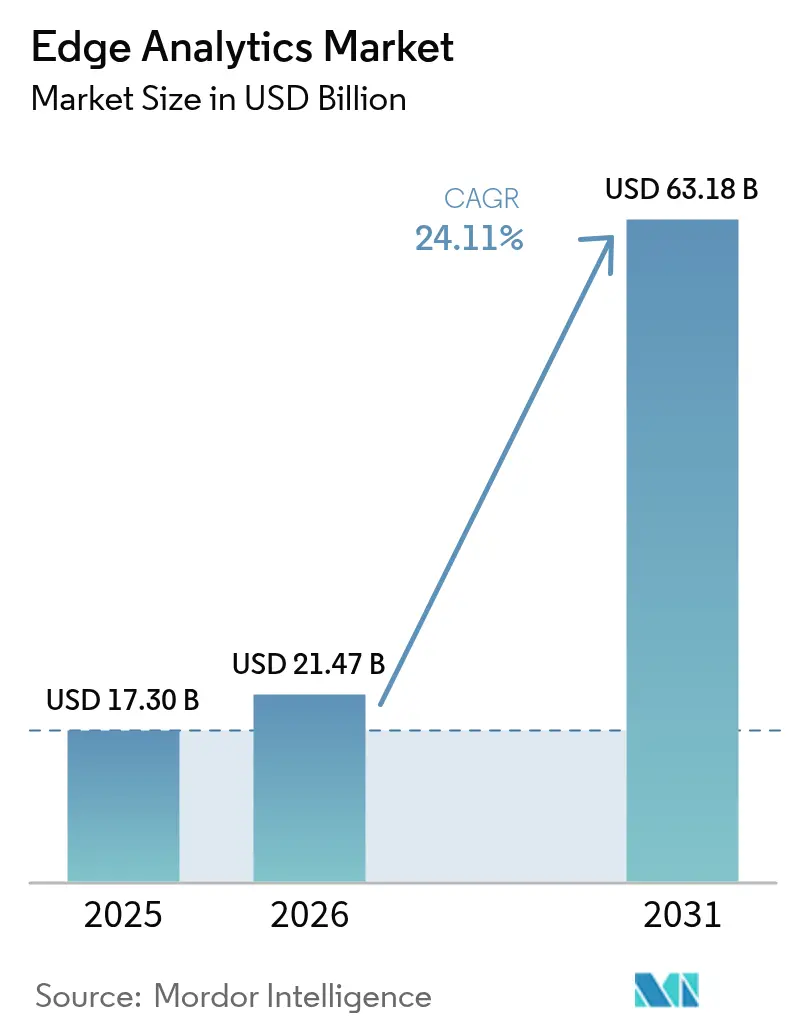

| Market Size (2026) | USD 21.47 Billion |

| Market Size (2031) | USD 63.18 Billion |

| Growth Rate (2026 - 2031) | 24.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Edge Analytics Market Analysis by Mordor Intelligence

The edge analytics market size is expected to grow from USD 17.30 billion in 2025 to USD 21.47 billion in 2026 and is forecast to reach USD 63.18 billion by 2031 at 24.11% CAGR over 2026-2031. Growth is propelled by the rapid expansion of IoT end-points, wider 5G coverage that supports low-latency data paths, and ongoing advances in AI-enabled silicon that places inference engines at the network edge. Vendors are prioritizing ruggedized micro-data centers, liquid-cooling designs, and federated learning frameworks that keep sensitive data local while still training global models. Enterprises are also integrating cloud-native orchestration tools to standardize application delivery across thousands of edge nodes, thereby compressing deployment cycles and raising ROI expectations. The edge analytics market is further influenced by regulatory drives toward data-sovereign architectures, especially in healthcare and finance where real-time decision support must coexist with strict privacy mandates.

Key Report Takeaways

- By deployment, on-premises solutions held 55.23% of the edge analytics market size in 2025, whereas cloud-based deployments are advancing at a 26.79% CAGR.

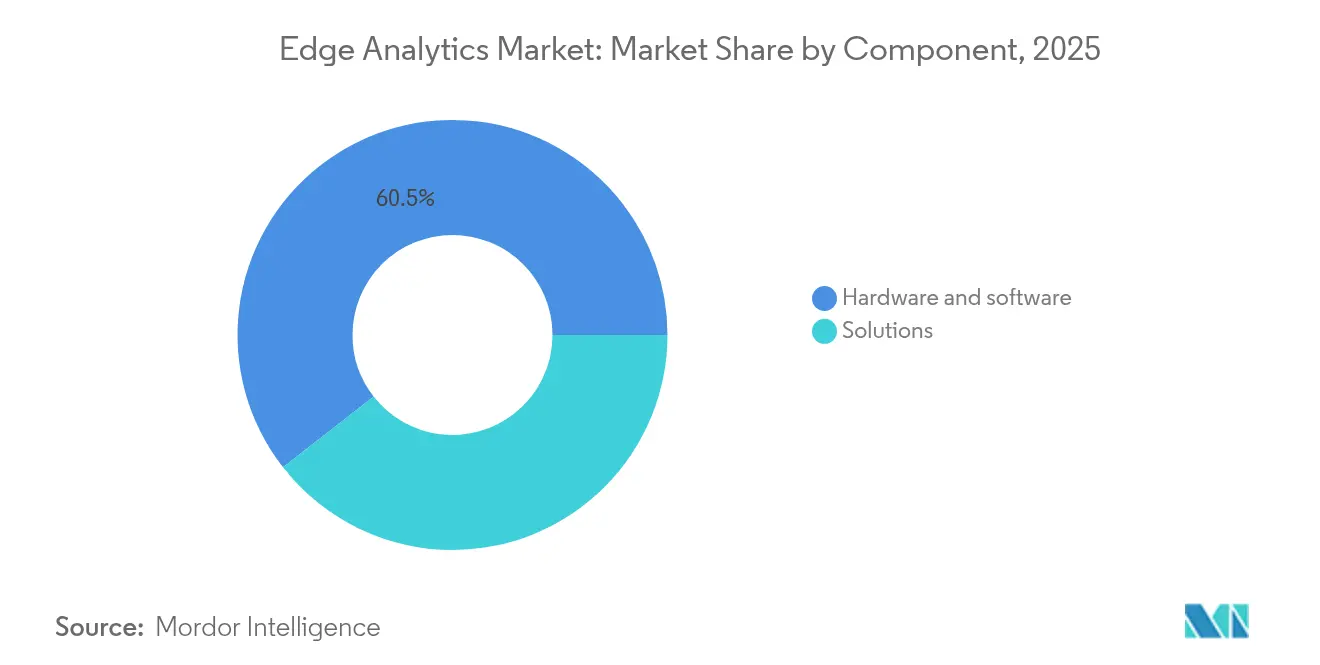

- By component, solutions commanded a 60.55% share of the edge analytics market size in 2025; services exhibit the highest projected CAGR at 28.58% to 2031.

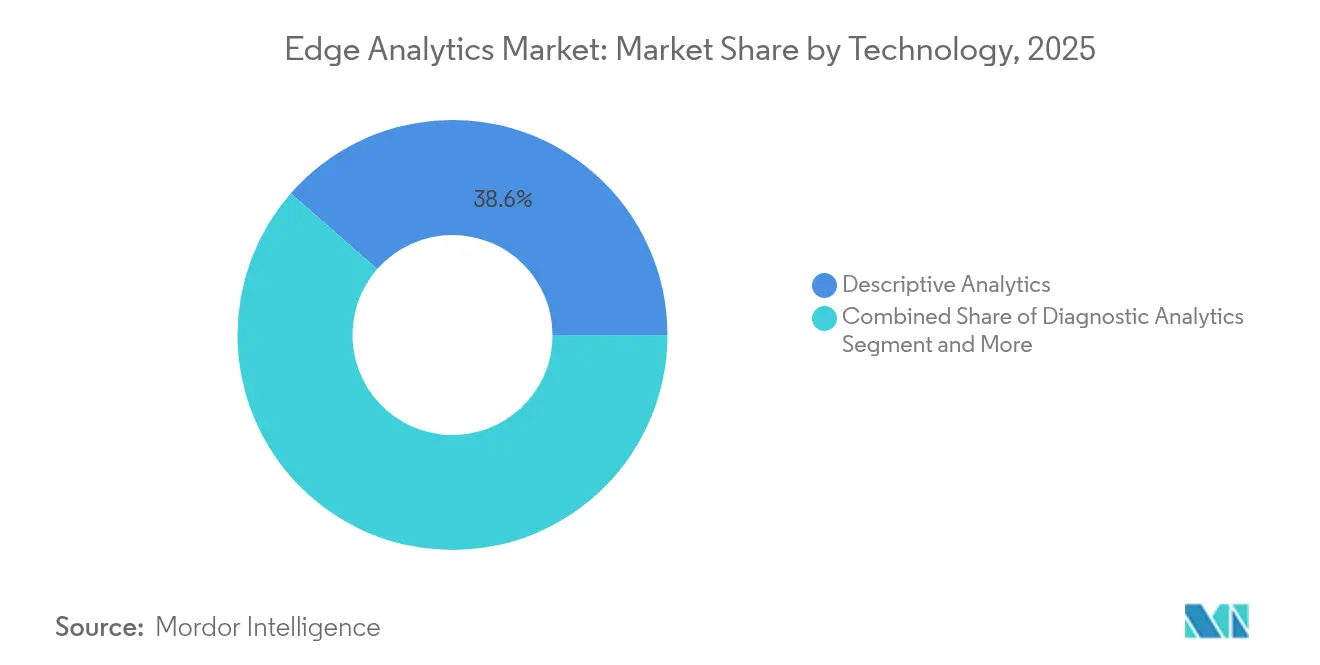

- By technology, descriptive analytics captured 38.55% revenue share in 2025; prescriptive analytics is forecast to expand at a 24.63% CAGR to 2031.

- By end-user industry, manufacturing led with 27.85% revenue share in 2025; healthcare is growing fastest at a 30.74% CAGR through 2031.

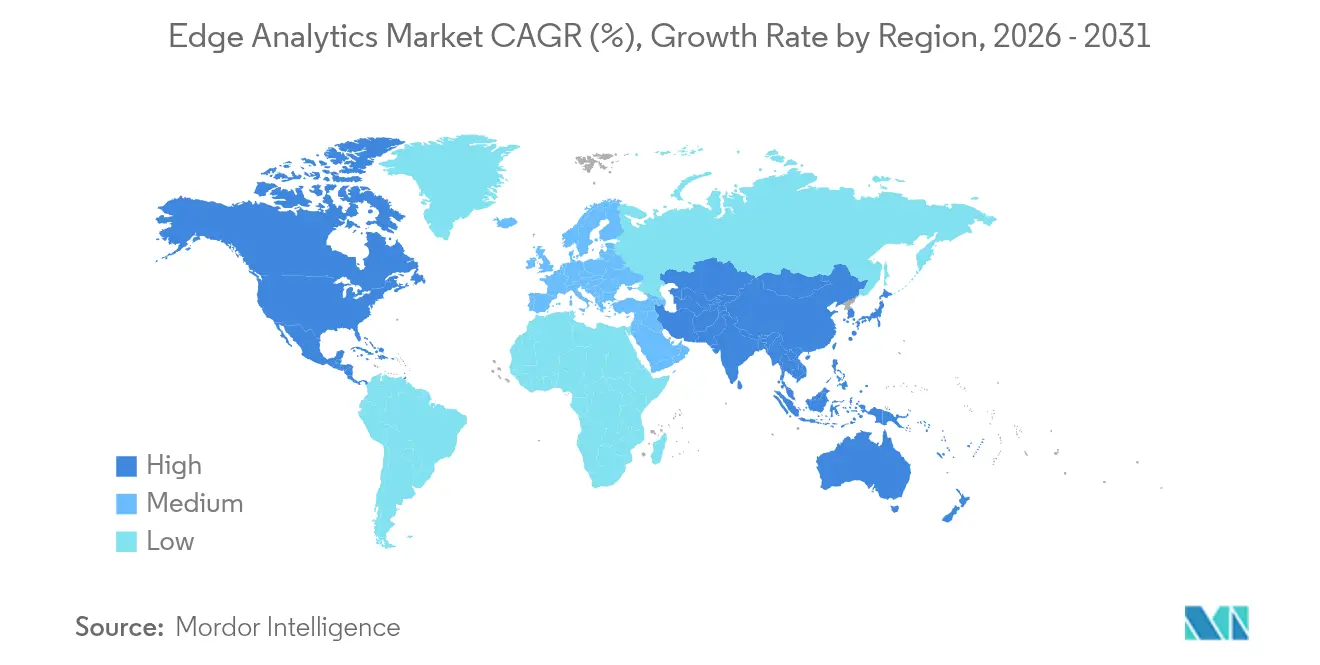

- By geography, North America led with 42.55% of edge analytics market share in 2025, while Asia Pacific is set to post the fastest 26.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Edge Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of IoT end-points | +4.8% | Global, higher in North America, and the Asia-Pacific | Medium term (2-4 years) |

| Demand for ultra-low-latency analytics | +4.0% | Global, manufacturing, and healthcare | Short term (≤ 2 years) |

| Rapid 5G roll-out, unlocking edge use-cases | +3.5% | North America, Europe, developed Asia-Pacific | Medium term (2-4 years) |

| Cloud-native toolchains are simplifying edge deployments | +2.7% | Global, early North America | Short term (≤ 2 years) |

| On-device federated learning enhancing data privacy | +3.0% | Europe, North America, and regulated markets | Medium term (2-4 years) |

| Liquid-cooling micro-data-centres enabling thermal-dense AI | +4.5% | North America, Europe, and advanced Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of IoT end-points

The global device base is generating 328.77 million TB of data every day, forcing analytics to migrate toward local processing so that bandwidth is conserved and insights arrive in real time. Industrial plants now stream vibration and temperature metrics from millions of sensors, and edge accelerators running optimized models handle this influx with sub-10 ms latency. As predictive maintenance checks extend from heavy machinery to medical wearables, the edge analytics market gains a larger operational footprint and becomes an indispensable layer in enterprise data strategy.

Demand for ultra-low-latency analytics

Autonomous robots, tele-surgery rigs, and collision-avoidance systems need decisions within 5 ms, a target unattainable when packets traverse distant clouds. Edge analytics eliminates the 50-150 ms round-trip and lowers the risk of mission-critical failures. Manufacturers that moved defect-detection algorithms from regional data centers to on-site nodes report double-digit yield improvements, reinforcing the business case for distributed intelligence.

Rapid 5G roll-out unlocking edge use-cases

Network slicing delivers guaranteed throughput for AR maintenance or live video security feeds. As tier-1 carriers push 5G to dense urban zones, enterprises deploy cameras and sensors that stream high-resolution data to adjacent edge servers. Smart-city pilots in Europe are demonstrating traffic-signal timing optimizations that cut congestion by 30%, a showcase of how synchronized 5G and edge platforms multiply value[1]AIOTI, “AI, IoT and Edge Continuum impact and relation on 5G/6G,” aioti.eu.

Cloud-native toolchains simplifying edge deployments

Kubernetes extensions now provision and heal containers across micro-data centres, letting developers apply the same CI/CD pipelines used in public clouds. This standardization shrinks time-to-pilot from months to weeks, encouraging mid-market firms to experiment with localized AI. Early adopters cite faster feature roll-outs and easier over-the-air updates for vision models that grade assembly-line output.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data-security & sovereignty risks | −4.7% | Global, highest in Europe, and regulated verticals | Short term (≤ 2 years) |

| Integration complexity with brownfield OT systems | −3.8% | Manufacturing, energy, utilities | Medium term (2-4 years) |

| Scarcity of tiny-ML / edge-AI engineering talent | −3.2% | Global, acute in emerging markets | Medium term (2-4 years) |

| ESG-driven power-cap caps on distributed compute nodes | −2.5% | Europe, North America, green-policy regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent data-security & sovereignty risks

Each edge gateway introduces an attack surface that adversaries can exploit through physical access or unpatched firmware. Finance and healthcare operators must also align with location-based data residency mandates, prompting adoption of trusted execution environments and zero-trust overlays that encrypt traffic end-to-end.

Integration complexity with brownfield OT systems

Factories built on legacy PLCs lack modern APIs, so middleware bridges consume project budgets and extend deployment timelines. Custom protocol translators help, yet the limited pool of engineers versed in both Modbus registers and Kubernetes manifests slows rollout velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Prescriptive Analytics Driving Strategic Value

Prescriptive engines are the fastest-advancing layer in the edge analytics market, growing at a 24.63% CAGR. They add decision automation to basic descriptive visibility, recommending the next best action once anomalies are detected. In 2025, descriptive modules still held 38.55% of revenue, but user demand has clearly pivoted toward higher-order insights that lift output and minimize risk. Edge devices now host compact reinforcement-learning agents that optimize robotics pathing on the fly, illustrating the commercial pull behind the transition.

Predictive algorithms remain a bridge between current dashboards and full automation. They enable forecast maintenance windows and inventory needs by correlating temperature spikes or traffic surges. Diagnostic analytics, though smaller, supplies root-cause clarity that prevents recurrence. Together these stacks help vendors package tiered offerings, embedding descriptive dashboards as entry points and layering prescriptive add-ons for premium subscribers. In turn, the edge analytics industry continues to mature toward outcome-based contracting.

By Deployment Type: Hybrid Architectures Gaining Momentum

On-premises nodes accounted for 55.23% of the edge analytics market size in 2025. They remain the first choice for data-sensitive sectors that cannot export personally identifiable or national-security information. Hospital networks, for instance, maintain imaging servers in-house so radiologists access scans without traversing external links. However, cloud-managed edges are scaling quicker, charting a 26.79% CAGR to 2031 as providers launch regional zones that meet residency rules.

Hybrid topology is emerging as the long-term norm. Sensitive workloads infer locally while batch trend analytics run in centralized clouds overnight. Central consoles push container updates, harmonize policy, and collect aggregated insights for executive dashboards, thereby delivering control without sacrificing agility. The arrangement reduces infrastructure duplication and keeps compute near data origin, aligning with both budget and compliance targets.

By Component: Services Growth Outpacing Solutions

Hardware and software solutions formed 60.55% of 2025 revenue, underpinned by AI-capable gateways, fan-less edge servers, and lightweight inference runtimes. Vendors differentiate through ruggedization levels, GPU density, and compatibility with open-source orchestration. Nonetheless, services revenue is rising faster at 28.58% CAGR because enterprises struggle with blueprinting, roll-out, and life-cycle governance.

Consultancies design reference architectures that integrate MES, SCADA, and public cloud APIs within 90-day sprints. Managed-service providers then operate the edge fleet, perform model drift checks, and execute patching windows across thousands of locations. This recurring service layer deepens customer lock-in and shifts value capture from one-time hardware margins to multi-year contracts, a trend reshaping vendor portfolios across the edge analytics market.

By End User Industry: Healthcare Innovations Accelerating Adoption

Manufacturers commanded 27.85% of edge analytics market share in 2025 by embedding real-time SPC charts and predictive maintenance loops on assembly lines. Output quality improved and unplanned downtime fell, generating quick paybacks that spurred further rollouts. Firms now attach power-optimized cameras that run vision models locally, classifying defects on conveyor belts without shipping frames to remote clouds.

Healthcare is the breakout growth story with a projected 30.74% CAGR through 2031. Bedside monitors pipe vitals to edge nodes that flag deterioration signs seconds before conventional alerts, enabling timely intervention. Edge-resident image classifiers review CT scans, highlighting possible anomalies so radiologists focus on high-risk sections first. Beyond the clinic, telehealth wearables sync via 5G to neighbourhood micro-clusters, upholding privacy while allowing continuous chronic-care analytics. These use cases demonstrate how clinical outcomes and operational efficiencies converge to accelerate investment.

Geography Analysis

North America retained leadership with 42.55% revenue in 2025 thanks to a mature hyperscale data-center footprint and early 5G monetization strategies. Telcos widened coverage to secondary metros, letting retailers place micro-data centers closer to suburban stores. Government incentives encouraged manufacturers to adopt smart-factory programs, embedding AI-driven process control at the line edge. Privacy rulings remain receptive to innovation provided encryption and audit trails meet industry norms. Policy clarity shortens procurement cycles and underpins steady demand across healthcare, retail, and energy domains.

Asia Pacific is the fastest-growing territory, forecast to log a 26.07% CAGR during 2026-2031. China scales provincial edge facilities that ingest sensor feeds from smart traffic lights and industrial robotics. Japan’s automotive majors deploy predictive quality loops that slice rework costs, while India's mobile operators leverage new spectrum to launch private 5G campuses for logistics parks. Diverse regulatory positions on cross-border data flows push multinationals toward localized deployments, often using open-source stacks to avoid vendor lock-in. Investments in domestic semiconductor fabs further support a self-sustaining regional supply chain and embed resilience into edge projects.

Europe shows robust but measured uptake, guided by GDPR and proposed AI liability laws. Germany pioneers Industrie 4.0 projects that retrofit heritage plants with OPC UA gateways and containerized inference, balancing innovation with risk governance. France leads smart-transport pilots where real-time video analytics on roadside units improve public-safety response times. Nordic operators prioritize green hydrogen-powered edge sites to respect ESG mandates. Standard-setting bodies collaborate on secure boot, remote attestation, and data-exchange frameworks, fostering an interoperability ethos that benefits the wider edge analytics market.

Regulatory Landscape

Edge analytics deployments are increasingly shaped by horizontal cybersecurity requirements for edge hardware and by AI-specific governance for embedded inference. In the European Union, the Artificial Intelligence Act (Regulation (EU) 2024/1689) sets risk-based obligations such as technical documentation, logging, and data governance for in-scope AI systems, with full application dated to 2 August 2026. That timeline pushes providers to harden lifecycle controls for models running on gateways, micro-data centers, and on-premises edge stacks.

In parallel, the EU Cyber Resilience Act (Regulation (EU) 2024/2847) introduces security-by-design expectations for products with digital elements, bringing edge gateways and software components into a compliance regime that emphasizes vulnerability handling and software transparency practices such as SBOM-aligned documentation. In the United States, NIST updates also influence procurement and configuration practices for edge infrastructure, including NIST SP 800-70 Revision 5 (National Checklist Program guidance) and NIST SP 800-234 (HPC Security Overlay) published in May 2026, which reinforce standardized configuration baselines and security control tailoring for performance-intensive analytics environments.

Value Chain Analysis

The edge analytics value chain starts with silicon and systems components (AI-optimized processors, accelerators, ruggedized servers, and storage), then extends into connectivity and hosting layers (telcos, CSP edge zones, CDNs, and colocation micro-data centers) that put compute close to data sources. On top of this, platform and software vendors provide orchestration (container and fleet management), data pipelines and streaming, analytics/AI runtimes, and security layers (zero-trust, device attestation, and policy controls), while services partners integrate into OT/IT systems (MES, SCADA, and enterprise applications) and run ongoing operations (patching, model monitoring, and SLA management).

Collaboration and federation are becoming more visible, with European operators (Deutsche Telekom, Orange, Telefonica, TIM, and Vodafone) demonstrating the European Edge Continuum as a federated edge cloud in February 2026, which creates a multi-operator distribution channel for edge workloads. Infrastructure and platform co-design is also tightening the chain: NVIDIA and T-Mobile announced work with Nokia and developers in March 2026 to integrate physical AI applications over distributed AI-RAN-ready edge networks, and Akamai expanded edge AI capacity by deploying an NVIDIA AI Grid reference design across 4,400 edge locations in July 2026. These moves raise the importance of pre-integrated reference architectures, validated security configurations, and repeatable deployment blueprints as edge analytics shifts from isolated sites to fleets spanning thousands of nodes.

Competitive Landscape

Global competition remains fragmented, with no supplier topping a 10% revenue slice in 2024. Mega-vendors such as Cisco, IBM, and Microsoft combine networking stacks, AI tools, and cloud extensions, appealing to enterprises that prefer single-throat accountability. Hyperscalers extend serverless functions and ML pipelines to colocation cages near population centers, lowering barriers for developers already fluent in cloud APIs. Meanwhile, industrial heavyweights like Siemens and GE Digital tailor verticalized offerings that integrate with SCADA and historian databases, providing deep domain value.

Start-ups concentrate on niche gaps such as tiny-ML model optimization or remote fleet orchestration at scale. Their agility spurs partnerships with incumbents seeking to complement portfolios without lengthy R&D cycles. Cross-industry consortiums emerge so devices authenticate once and receive signed workloads regardless of hardware brand, simplifying multi-vendor estates. The rise of open telemetry standards also reduces switching costs, encouraging healthy competition on service quality rather than proprietary lock-in.

Strategic alliances define differentiation more than feature checklists. IBM’s edge ecosystem rallies over thirty hardware and software partners who pre-integrate networking, security, and analytics components to shrink proof-of-concept timelines. Cloud providers team with telcos to embed container environments in base-band units, giving customers a one-click edge deployment option. Hardware makers embed cryptographic roots-of-trust so cloud consoles verify device integrity before offloading workloads. This orchestration-driven model accelerates adoption, deepens vendor stickiness, and steers the battlefield toward outcome-centric value propositions.

Edge Analytics Industry Leaders

Cisco Systems Inc.

Oracle Corporation

SAS Institute Inc.

IBM Corporation

Apigee Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary whitespace area is operationalizing edge analytics at scale, where enterprises want consistent deployment, governance, and update mechanics across large, heterogeneous fleets. This is reinforced by observable movement from pilots into production-oriented programs and platforms, including survey evidence reported in March 2026 showing broad executive positioning of edge AI as core to business strategy and meaningful penetration of active production deployments. The opportunity centers on EdgeOps capabilities (zero-touch provisioning, remote lifecycle management, and policy enforcement) that reduce the integration burden highlighted in brownfield OT environments, while also supporting hybrid patterns where training stays centralized and inference runs locally for latency and data-sovereignty needs.

Standards progress also creates room for interoperable industrial-grade edge analytics. IEEE published IEEE/IEC 60802-2026 (time-sensitive networking profiles for industrial automation) and approved IEEE 2805.3-2026 (protocols for cloud-edge collaboration for machine learning applications) in June 2026, which provide clearer technical anchors for deterministic data transport and coordinated ML workflows across cloud and edge nodes. In parallel, industry bodies such as the Open Industry 4.0 Alliance provide development and conformance guidance for open edge computing products (2025 publications), supporting vendor-neutral implementations that manufacturers can adopt when modernizing legacy plants and when regulated verticals need auditable, standardized deployment patterns.

Recent Industry Developments

- July 2026: Akamai deployed an NVIDIA AI Grid reference design across 4,400 edge locations to add GPU-backed capacity for AI workloads delivered from its distributed edge platform. The build-out expands where low-latency analytics and inference can run, strengthening CDN-based routes to production edge analytics beyond traditional data centers.

- March 2026: Cisco expanded its Secure AI Factory with NVIDIA, extending support for NVIDIA RTX PRO 4500 Blackwell Server Edition GPUs across the Cisco Unified Edge portfolio. The update ties edge infrastructure and security controls more tightly to GPU-driven inference, addressing deployment complexity for distributed analytics stacks that span many sites.

- November 2025: Cisco introduced the Cisco Unified Edge Platform for distributed agentic AI workloads, combining platform software with edge-ready infrastructure elements for running and managing AI at the network edge. This positioned Cisco to sell a more integrated edge analytics foundation that aligns networking, compute, and management into a single operational model.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the edge analytics market includes software and services used to analyze data at or near where it is created, such as on devices, gateways, or local servers, before data is sent to a central cloud or data center.

Scope exclusions: We exclude pure data storage, connectivity hardware sold without analytics, and general cloud analytics that does not run at the edge.

Segmentation Overview

- By Deployment Type

- On-Premises

- Cloud

- By Component

- Solutions

- Services

- By End-User Industry

- BFSI

- IT & Telecommunication

- Manufacturing

- Healthcare

- Retail

- Others

- By Technology

- Descriptive Analytics

- Diagnostic Analytics

- Predictive Analytics

- Prescriptive Analytics

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clear picture of where edge analytics demand comes from and how it is purchased across industries. We leaned on public sources such as NIST publications on edge and IoT security, FCC spectrum and connectivity updates, US Census and Eurostat digitization indicators, and OECD or World Bank data for industry output and enterprise IT adoption. To anchor the technology side, we also reviewed patent databases and peer-reviewed papers covering edge processing, distributed AI inference, and streaming analytics.

After that, the desk layer is used to shape assumptions that can be tested in interviews. We reviewed company filings, investor presentations, product documentation, and trusted press coverage to map common pricing models (license, subscription, and service bundles) and to cross-check growth signals such as data-creation trends and edge device rollouts. A selective paid subscription for company financials and intelligence, plus a news and financials database, helped confirm revenue mix cues and major contract announcements. The desk research sources named above are illustrative only, and other public references were used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to validate what qualifies as edge analytics revenue, how solutions are packaged with services, and how adoption differs by verticals like manufacturing, healthcare, retail, BFSI, and telecom. We spoke with a mix of solution providers, system integrators, and enterprise buyers across major regions so assumptions on penetration, pricing direction, and deployment mix could be checked and then adjusted where needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 39% |

| Mid tier: 50% | Functional/Unit leaders: 30% | EMEA: 37% |

| Smaller Players: 21% | Managers: 58% | Americas: 24% |

Market-Sizing & Forecasting

The sizing model is built using top-down and bottom-up logic, with the top-down layer reconstructing addressable spend by tracking edge-executed analytics adoption across key end user industries and then applying realistic penetration at the edge. Since the market is often bundled, selective bottom-up checks are used to corroborate totals, using sampled supplier revenue cues, channel feedback on deal sizes, and an ASP times volume approximation where the purchase unit is clear.

In practice, inputs are driven by a few market fingerprints that are observable and can be revisited each refresh. These include the installed base of connected devices and gateways, the share of workloads moving to edge nodes versus centralized cloud, average contract values for edge analytics solutions plus professional or managed services, and the pace of 5G and industrial IoT rollouts that typically pull compute closer to assets. We also track deployment mix shifts (on-premise versus cloud managed edge) because they change price realization and service attach rates. Where bottom-up evidence is patchy for smaller providers, gaps are handled through conservative revenue banding and normalization to the same inclusion rules used across the model.

For forecasting, scenario analysis is used, and it is tied to drivers that experts can sanity-check, such as enterprise digitization budgets, adoption of latency sensitive use cases, data-egress cost pressure, and security requirements that keep processing local. Assumptions are then tuned so the forecast remains consistent with observed adoption curves across the main verticals and regions.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, then through stepwise variance checks before sign off. Outputs are compared against adoption indicators, deal activity, and the revenue direction reflected in public disclosures, and large swings trigger a deeper review of pricing, penetration, and deployment mix assumptions. When a mismatch persists after internal checks, follow up calls are initiated to confirm whether it is a scope mismatch, a one-time contract, or a timing effect.

Each report is refreshed annually, and interim updates are made when material events occur, such as major regulatory shifts, large platform releases, or sudden demand changes in a key vertical. Before delivery, the model is re-run with the latest inputs and a final analyst pass is completed so clients receive an updated view that matches the current market context.

Mordor Intelligence's Edge Analytics Market Size Compared Against Other Published Estimates

Published market numbers for edge analytics often do not line up because researchers do not count the same things, and they also pick different base years and growth windows. Differences usually come from what is included as edge analytics, whether services are counted fully, and how pricing is converted and projected over time.

The benchmark table shows a wide spread versus 2025, and in Mordor Intelligence's model the value is built from edge executed analytics software plus related professional and managed services, and it is kept separate from broader edge computing stacks and general cloud analytics that does not execute at the edge. Some other estimates start from a smaller 2024 base and then apply faster growth assumptions, or they shift the headline to 2026 and make year to year comparisons less direct. Currency timing and whether deployments counted are limited to on-device, gateway, and local server use cases, or also include adjacent centralized processing, also changes the final number.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.30 B (2025) | |

| Global Consultancy A | USD 11.58 B (2025) | Uses a 2024 base and a narrower revenue capture that can undercount services attach and multi site deployments, thereby landing at a smaller 2025 value. |

| Industry Research Group B | USD 11.60 B (2026) | Starts at a later base year and runs a longer horizon forecast, which shifts the headline to 2026 and makes year to year comparisons less direct. |

Across the three figures, the main drivers of variance are the base year choice, whether services are fully included, and how adjacent analytics delivered outside the edge is treated. By keeping inputs tied to observable adoption and pricing signals, and by using repeatable inclusion rules, we can explain each step and keep the estimate practical to validate in future updates.

Key Questions Answered in the Report

What is the current value of the edge analytics market?

The edge analytics market size is USD 21.47 billion in 2026 and is projected to reach USD 63.18 billion by 2031.

Which region leads edge analytics adoption today?

North America accounts for 42.55% of 2025 revenue due to early 5G roll-outs and strong investments in edge infrastructure.

Which end-user sector is expanding fastest?

Healthcare shows the highest momentum, advancing at a 30.74% CAGR as hospitals deploy real-time patient monitoring and imaging analytics.

Why are hybrid edge architectures gaining traction?

Hybrid deployments balance on-premises data control with cloud scalability, offering secure local inference while centralizing batch analytics for cost efficiency.

Page last updated on: