Industrial Edge Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

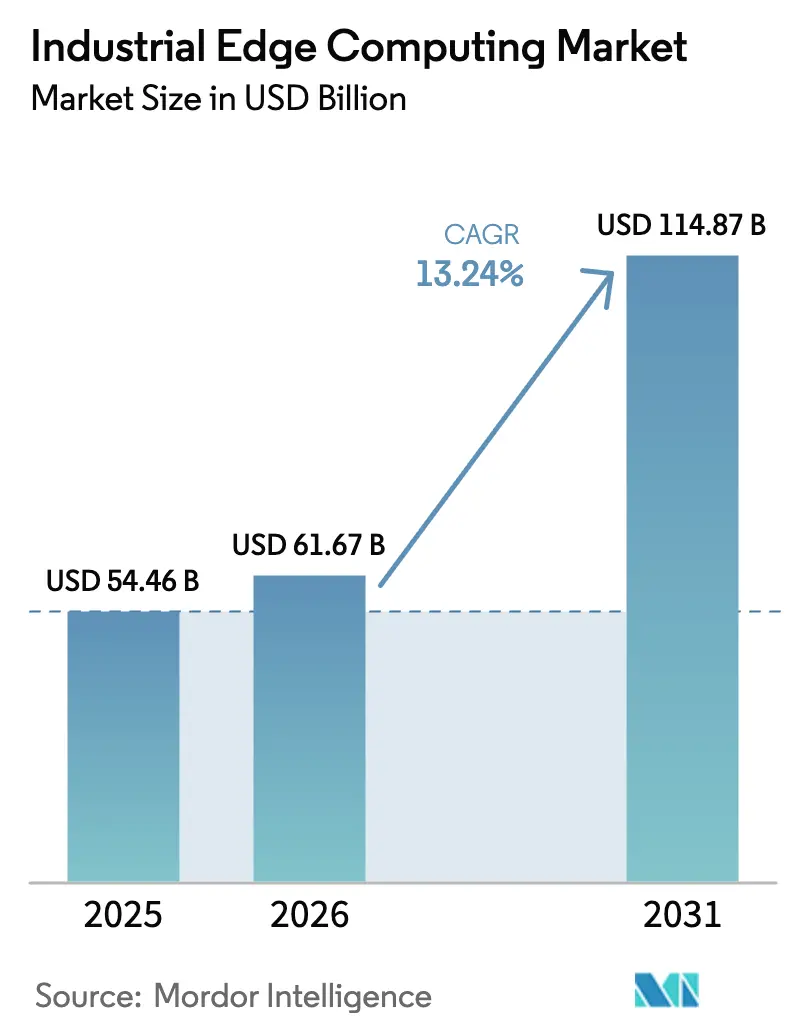

| Market Size (2026) | USD 61.67 Billion |

| Market Size (2031) | USD 114.87 Billion |

| Growth Rate (2026 - 2031) | 13.24% CAGR |

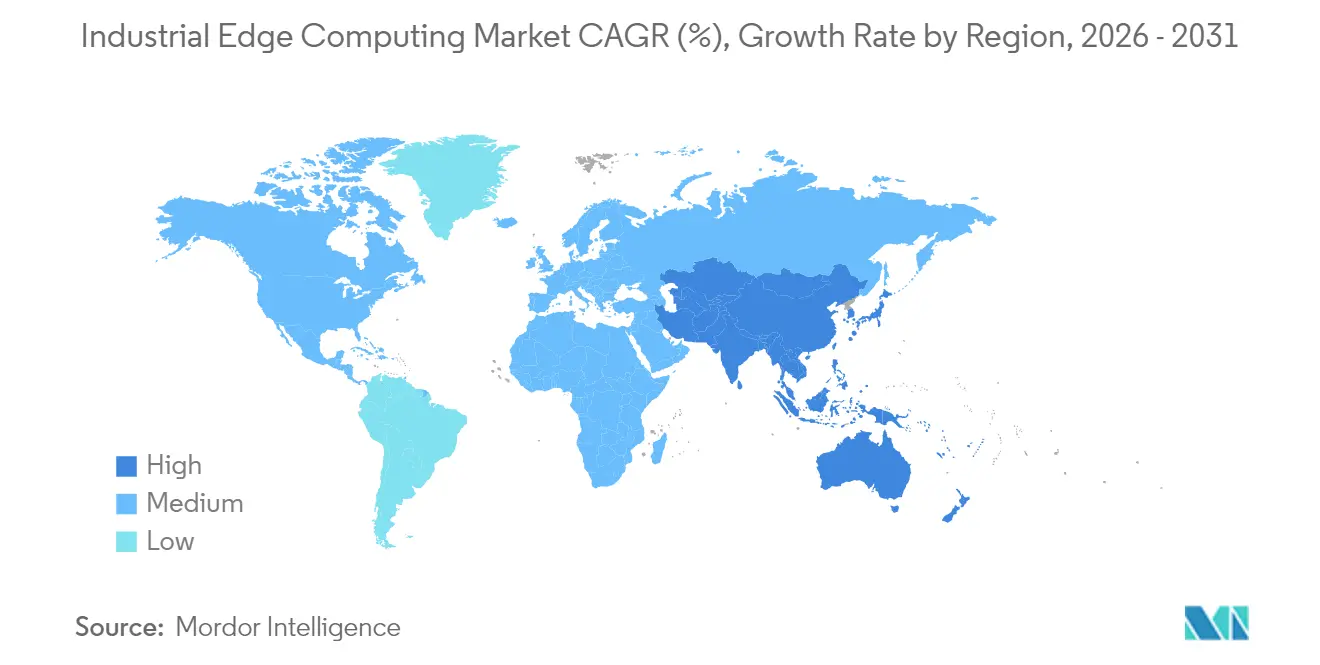

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Edge Computing Market Analysis by Mordor Intelligence

The Industrial Edge Computing market size is expected to grow from USD 54.46 billion in 2025 to USD 61.67 billion in 2026 and is forecast to reach USD 114.87 billion by 2031 at 13.24% CAGR over 2026-2031. Latency-sensitive automation, private-5G availability, and data-sovereignty mandates are motivating enterprises to process data at production sites instead of remote clouds.[1]Ericsson AB, “Private 5G Networks Portfolio,” ericsson.com Hardware demand remains healthy, yet software-defined orchestration is scaling faster as containerization turns existing gateways into compute nodes. Enterprises are also reevaluating total cost of ownership as cyber-insurance discounts reward on-premise analytics. Finally, sustainability-linked financing is tilting capital expenditure toward solutions that optimize energy use in real time

Key Report Takeaways

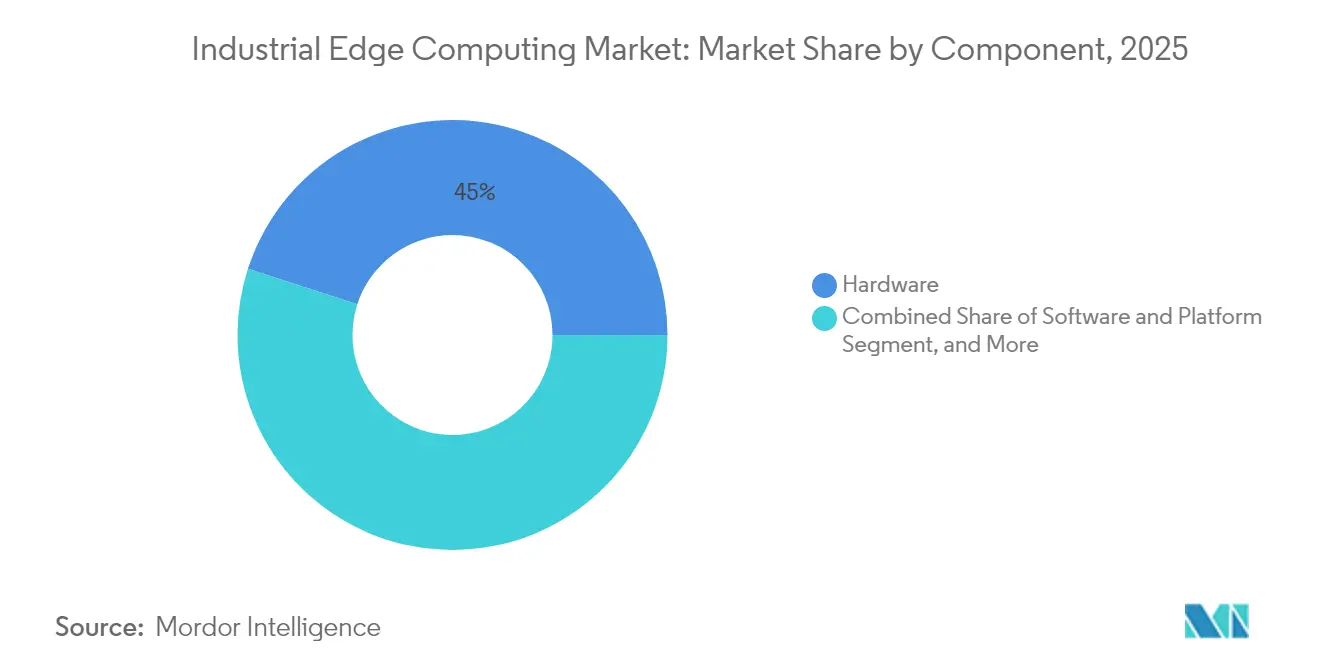

- By component, hardware led with 45.02% revenue share in 2025 in the Industrial Edge Computing market; software and platform solutions are advancing at a 13.95% CAGR through 2031.

- By end-user industry, manufacturing commanded 42.10% of the Industrial Edge Computing market share in 2025, while transportation and logistics posted the fastest 13.96% CAGR to 2031.

- By deployment model, on-premise edge appliances held 54.05% of the Industrial Edge Computing market size in 2025, and managed edge platform-as-a-service is projected to rise at a 14.08% CAGR.

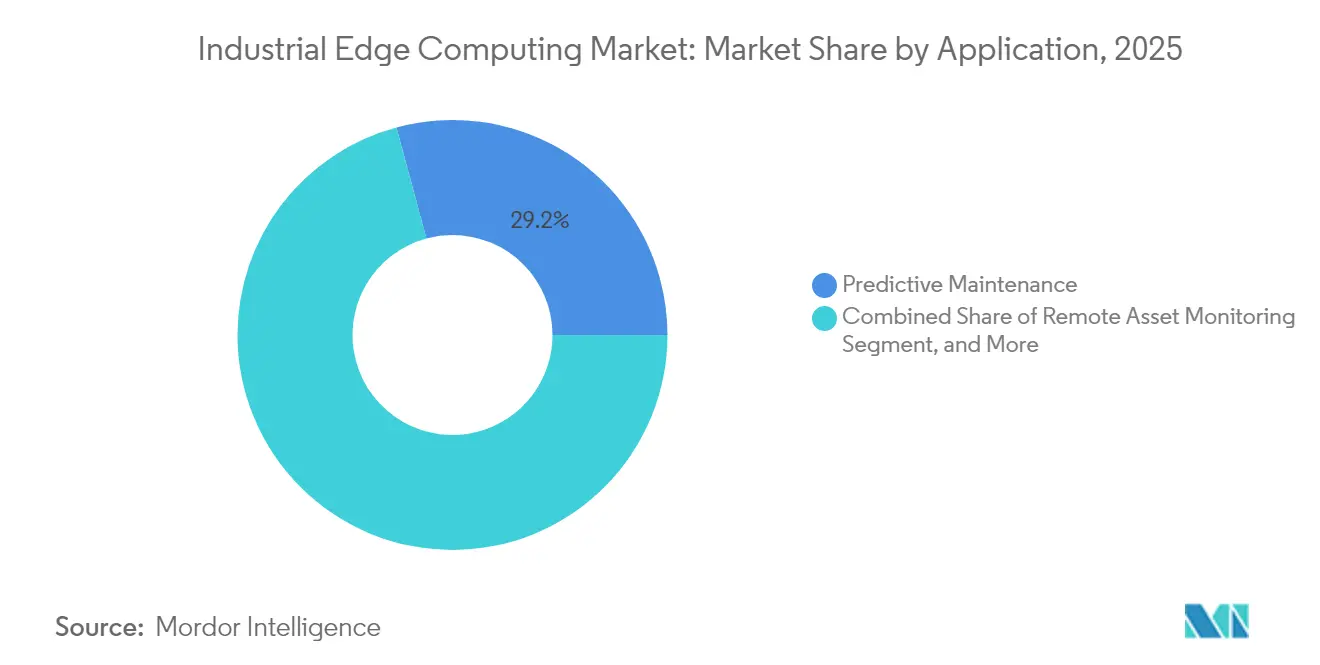

- By application, predictive maintenance accounted for 29.20% of 2025 revenues in the Industrial Edge Computing market, yet quality inspection and machine vision is expanding at 13.52% CAGR.

- By geography, North America delivered 39.45% revenue share in 2025 in the Industrial Edge Computing market as Asia Pacific records the strongest 13.62% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Edge Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in IIoT-sensor deployments and factory automation | +2.1% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Rapid adoption of low-latency analytics in smart manufacturing | +1.8% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Roll-out of private-5G industrial networks | +1.6% | North America and EU core, APAC following | Medium term (2-4 years) |

| Containerized workloads on existing OT network equipment | +1.4% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Cyber-insurance discounts for on-premise edge analytics | +0.9% | North America and EU primarily | Long term (≥ 4 years) |

| Sustainability-linked financing favouring local energy optimisation | +0.7% | EU leading, North America and APAC following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in IIoT-sensor deployments and factory automation

Enterprises are attaching millions of sensors to machines, conveyors, and utilities, generating torrents of telemetry that overwhelm cloud backhauls if processed remotely.[2]Siemens AG, “Industrial Edge Solutions,” siemens.com Edge nodes eliminate that bottleneck by applying real-time filtering and analytics within the factory walls. Discrete manufacturers are particularly sensitive to microsecond delays, driving uptake among automotive, electronics, and packaging lines. The pattern reinforces itself: every new sensor multiplies data interactions, accelerating demand for local compute. As AI models for optimization run directly beside controllers, edge platforms shift from optional add-ons to core infrastructure.

Rapid adoption of low-latency analytics in smart manufacturing

Smart-manufacturing pilots show how milliseconds translate into millions of dollars. ExxonMobil’s open-process testbed cut a 15-second loop to roughly 40 milliseconds by relocating analytics to the edge. Faster feedback prevents quality drift and reduces scrap in continuous industries such as chemicals and metals. Firms often start by monitoring noncritical assets, then migrate to mission-critical loops once confidence grows. Vision-based inspection is a prime catalyst because any lag between camera capture and corrective action lets defects propagate down the line.

Roll-out of private-5G industrial networks

Dedicated 5G networks combine deterministic latency, spectrum control, and network slicing, making them natural backbones for distributed edge clusters. Early installations at auto plants, food facilities, and brownfield refineries allow thousands of sensors to connect without congestion. Ultra-reliable low-latency links ensure that multiple edge nodes coordinate workloads safely, enabling autonomous robots and AGVs. 5G’s security profile also satisfies OT engineers who resist exposing production traffic to public carriers.

Containerized workloads on existing OT network equipment

Industrial gateways, PLCs, and rugged servers increasingly ship with container engines so operators can deploy analytics like any other microservice. This “brownfield-friendly” method removes the rip-and-replace barrier that historically hindered modernization. Over-the-air updates shrink maintenance windows, while centralized registries push new models to thousands of sites simultaneously. Kubernetes and similar orchestrators are migrating from IT datacenters into control rooms, turning edge applications into software-defined assets that live alongside deterministic control logic.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OT-IT skills gap for edge integration | -1.2% | Global, particularly acute in developed markets | Medium term (2-4 years) |

| High upfront hardware and retro-fit costs | -0.8% | Global, with higher impact in cost-sensitive markets | Short term (≤ 2 years) |

| Fragmented middleware standards hindering portability | -0.9% | Global, with standardization efforts ongoing | Long term (≥ 4 years) |

| Long-term security-patch obligations raising TCO | -0.6% | Global, with regulatory compliance driving costs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OT-IT skills gap for edge integration

Effective deployment demands professionals fluent in industrial protocols, cybersecurity, and cloud-native stacks, yet fewer than 15% of engineers possess that mix.[3]Cisco Systems Inc., “Manufacturing Internet of Things Solutions,” cisco.com Hiring shortages extend project timelines and inflate consulting fees. Smaller plants feel the pinch more acutely, often postponing projects until integrators package turnkey offerings. Although certification programs are growing, workforce development lags technology rollout, keeping the skills gap a mid-term drag on the Industrial Edge Computing market.

High upfront hardware and retrofit costs

Rugged servers, hardened switches, and environmental enclosures can run tens of thousands of dollars per line, squeezing SME budgets. Retrofit-heavy brownfield sites also require power upgrades and structured cabling that add hidden costs. Managed edge-as-a-service models turn CapEx into OpEx, but some firms balk at relinquishing data custody, leaving them to absorb upfront spending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Faces Software Disruption

Hardware captured 45.02% revenue in 2025 as factories invested in gateways, vision accelerators, and rugged servers able to withstand vibration, dust, and temperature swings. Those purchases anchor the current Industrial Edge Computing market, ensuring deterministic performance near production lines. Software and platform offerings, however, are scaling faster at a 13.95% CAGR because they decouple workloads from proprietary iron. Enterprises can now install a digital-twin microservice on the same node that hosts a PLC, then redeploy it to a different plant through a centralized registry. Subscription pricing also aligns with operating budgets, giving finance teams predictable expense curves.

The growing availability of container runtimes on control hardware blurs the boundary between device and application. Softing Industrial’s 2025 OPC UA expansion, supporting more than 60 companion models, illustrates how standardized information models boost software value. As orchestration maturity improves, buyers increasingly weigh platform flexibility and lifecycle automation over processor counts. Services remain the smallest slice but influence purchasing decisions because integration partners tie disparate assets into a unified management plane.

By End-user Industry: Manufacturing Leadership Under Transportation Pressure

Manufacturing held 42.10% of global spending in 2025 as early Industry 4.0 adopters sought microsecond decision loops for robotics and process control. The Industrial Edge Computing market resonates with this sector because downtime costs can exceed USD 25,000 per minute in automotive stamping lines. Yet transportation and logistics is climbing fastest at a 13.96% CAGR, propelled by fleet telematics, terminal automation, and autonomous yard vehicles requiring compute at depots. Oil and gas remain substantial due to remote field assets where satellite latency is prohibitive.

Life sciences plants are also accelerating deployments as FDA guidance endorses advanced manufacturing technologies that ensure lot-level traceability. Mining, metals, and utilities apply edge analytics to worker safety and grid-stability use cases. Food and beverage plants deploy real-time vision inspection to comply with stringent labeling and allergen regulations. While each vertical value offers latency reduction, compliance reporting, and energy savings that often tip the business case, broadening the Industrial Edge Computing industry’s addressable base.

By Application: Predictive Maintenance Maturity Enables Vision Analytics Growth

Predictive maintenance contributed 29.20% of 2025 revenue, proving its ROI by cutting unplanned downtime. Vibration and thermal-imaging data analyzed locally enables earlier fault detection than SCADA alarms, and algorithms continuously refine thresholds as they ingest new data. Quality inspection and machine vision, racing ahead at a 13.52% CAGR, rely on GPU-accelerated inferencing at the edge to flag defects within the takt time of high-speed lines. Real-time process optimization remains pivotal because energy costs and carbon metrics face regulatory scrutiny.

Edge AI vision analytics is the newest frontier. Dell Technologies and Cognex combine inference accelerators with domain-trained models to deliver millisecond rejection decisions on paint defects. Remote asset monitoring extends coverage to offshore platforms and mountain sub-stations, where intermittent backhaul limits cloud reliance. Safety and compliance analytics round out the mix by automating OSHA reporting and detecting PPE violations through cameras and LiDAR.

By Deployment Model: Managed Services Challenge On-premise Dominance

On-premise edge appliances accounted for 54.05% of the 2025 Industrial Edge Computing market size because regulated industries insist on local custody of intellectual property. Racks of micro-data-center nodes sit near assembly lines and process skids, providing deterministic latency and air-gapped resilience. Managed platform-as-a-service models are gaining at a 14.08% CAGR as vendors bundle hardware, orchestration, and 24×7 monitoring under service-level agreements, converting capital purchases to pay-as-you-go subscriptions.

Integrated edge on network equipment appeals to cost-sensitive factories that piggyback compute cycles on existing switches. Modular micro-data-centers such as Crusoe Spark deploy within weeks, supporting GPU-heavy workloads without full facility refurbishments. Hybrid models flourish as firms segment workloads: safety-critical loops stay on-premise, while noncritical analytics move to managed platforms to conserve internal resources.

Geography Analysis

North America’s 39.45% 2025 share reflects a confluence of early private-5G adoption, robust cyber-insurance frameworks, and corporate sustainability targets that incentivize on-premise analytics. Multinationals like ExxonMobil validate open architectures that blend legacy DCS with containerized microservices, cementing customer trust. Revenue growth now tilts toward mid-sized plants modernizing brownfield lines rather than flagship pilots, extending the Industrial Edge Computing market beyond early adopters.

Asia Pacific records the fastest 13.62% CAGR, underscored by China’s Made-in-China 2025 program and Japan’s Society 5.0 vision. Greenfield factories integrate edge capabilities from initial design, bypassing retrofit bottlenecks. Sustainability-linked loans, often priced 20–30 basis points lower, reward real-time energy optimization achieved through local analytics. The region’s export-driven manufacturers view latency-free quality control as a strategic differentiator in global supply chains.

Europe remains pivotal thanks to IEC 62443 cyber mandates and GDPR-driven data-locality rules that privilege on-premise processing. Automotive and food producers lead, supported by Horizon-funded research that subsidizes pilot deployments. Meanwhile, South American mines and Middle East oilfields deploy rugged edge nodes to cut unplanned downtime on remote assets, illustrating how the Industrial Edge Computing market scales across disparate economic environments.

Competitive Landscape

The Industrial Edge Computing market is moderately fragmented. Automation incumbents such as Siemens, ABB, and Rockwell Automation leverage installed bases to upsell edge nodes embedded with proprietary libraries. Their domain expertise and service networks form a barrier for IT-centric challengers. Still, hyperscalers like Microsoft and Amazon Web Services penetrate through hybrid stacks that extend cloud services onto factory floors, capturing workloads that benefit from cloud-native toolchains.

Specialized platform vendors differentiate via open standards, lifecycle automation, and vertical templates. Participation in bodies like the Open Process Automation Forum enables interoperability, positioning smaller players as ecosystem orchestrators rather than point-product sellers. Partnerships multiply; Verizon teams with NVIDIA on private-5G edge AI while Qualcomm aligns with Palantir for industrial analytics accelerators. System integrators emerge as power brokers, bundling converged hardware, platform licensure, and managed security into turnkey contracts.

Strategic moves increasingly focus on bridging the OT-IT skills gap. Vendors deliver low-code orchestration dashboards and reference architectures that pre-validate cybersecurity controls. Subscription models proliferate, locking in annual recurring revenue and allowing buyers to expense solutions through operating budgets. Intellectual-property custodianship remains a battleground: regulated industries lean toward on-premise offerings, while cost-focused sectors accept managed services, creating room for dual-strategies. As of 2025, the combined share of the top five vendors is estimated near 45%, underscoring mid-tier fragmentation but still granting incumbents significant influence.

Industrial Edge Computing Industry Leaders

General Electric Company

ZEDEDA

International Business Machines Corporation

Siemens AG

Rockwell Automation, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Crusoe Energy launched Spark modular AI data centers designed for industrial edge computing applications, offering containerized infrastructure capable of supporting intensive workloads at production sites.

- April 2025: Softing Industrial expanded OPC UA functionality across four product lines, enabling standardized data integration for manufacturing execution systems and industrial IoT applications.

- March 2025: Qualcomm Technologies announced collaboration with Palantir Technologies to develop edge AI solutions for industrial applications, combining Qualcomm’s platforms with Palantir’s analytics.

- December 2024: Verizon Business and NVIDIA Corporation expanded their partnership to deliver private-5G edge AI solutions for industrial customers.

Global Industrial Edge Computing Market Report Scope

Industrial edge computing (IEC) is a subset of edge computing that uses high-speed data analytics within a localized, on-site system to help address all types of industrial manufacturing challenges.

The industrial edge computing market is segmented by component (hardware, software, and services), end user (manufacturing, oil and gas, mining), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa).

The market sizes and forecasts are provided in terms of value USD for all the above segments.

| Hardware |

| Software and Platform |

| Services |

| Manufacturing |

| Oil and Gas |

| Mining and Metals |

| Utilities and Energy |

| Transportation and Logistics |

| Pharmaceuticals and Life Sciences |

| Food and Beverage |

| Other End-user Industries |

| Predictive Maintenance |

| Quality Inspection and Machine Vision |

| Real-time Process Optimisation |

| Remote Asset Monitoring |

| Safety and Compliance Analytics |

| Edge AI Vision Analytics |

| On-premise Edge Appliances |

| Integrated Edge on Network Equipment |

| Managed Edge Platform-as-a-Service |

| Industrial Edge Micro-Data-Centers |

| North America |

| South America |

| Europe |

| Asia Pacific |

| Middle East and Africa |

| By Component | Hardware |

| Software and Platform | |

| Services | |

| By End-user Industry | Manufacturing |

| Oil and Gas | |

| Mining and Metals | |

| Utilities and Energy | |

| Transportation and Logistics | |

| Pharmaceuticals and Life Sciences | |

| Food and Beverage | |

| Other End-user Industries | |

| By Application | Predictive Maintenance |

| Quality Inspection and Machine Vision | |

| Real-time Process Optimisation | |

| Remote Asset Monitoring | |

| Safety and Compliance Analytics | |

| Edge AI Vision Analytics | |

| By Deployment Model | On-premise Edge Appliances |

| Integrated Edge on Network Equipment | |

| Managed Edge Platform-as-a-Service | |

| Industrial Edge Micro-Data-Centers | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the current valuation of the Industrial Edge Computing market?

The market stood at USD 61.67 billion in 2026 and is projected to reach USD 114.87 billion by 2031, reflecting a 13.24% CAGR.

Which segment contributes the largest revenue within Industrial Edge Computing?

Hardware remains the largest contributor, accounting for 45.02% of 2025 revenue.

Which region is expanding the fastest for Industrial Edge Computing deployments?

Asia Pacific exhibits the highest 13.62% CAGR as greenfield factories incorporate edge capabilities from the outset.

Why are private-5G networks important for industrial edge use cases?

Dedicated 5G networks provide deterministic latency and security, enabling synchronized processing across distributed edge nodes.

How are cyber-insurance incentives shaping Industrial Edge Computing adoption?

Insurers offer premium discounts for on-premise analytics, improving ROI and accelerating on-site deployment decisions.

Page last updated on: