Deepfake AI Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

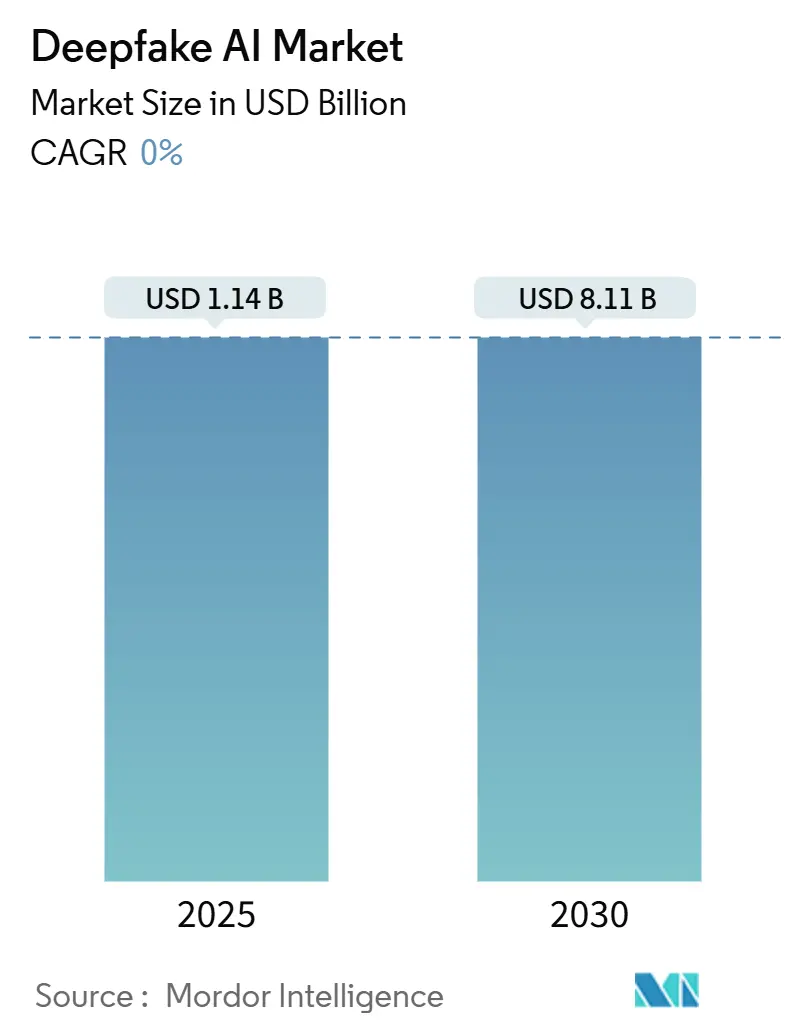

| Market Size (2025) | USD 1.14 Billion |

| Market Size (2030) | USD 8.11 Billion |

| Growth Rate (2025 - 2030) | 0.00% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Deepfake AI Market Analysis by Mordor Intelligence

The deepfake AI market size reached USD 1.14 billion in 2025 and is projected to escalate to USD 8.11 billion by 2030, translating into a robust 48.06% CAGR during the forecast period. Explosive revenue growth aligns with rapid advances in generative adversarial networks, rising regulatory scrutiny of synthetic media misuse, and expanding enterprise budgets for identity-centric cybersecurity solutions. Cloud hyperscalers have made GAN-as-a-Service widely accessible, shrinking barriers for mid-sized firms that previously lacked the compute capacity to experiment with synthetic media. Parallel demand for deepfake detection tools has surged across banking, government, and media workflows, as 347% more fraud attempts used deepfakes in 2024 than in 2023. Tightening regulatory frameworks in Europe and North America are now complemented by large-scale investments in Asia Pacific, most notably China’s National AI Development Plan, which earmarks USD 15 billion for AI research by 2030.

Key Report Takeaways

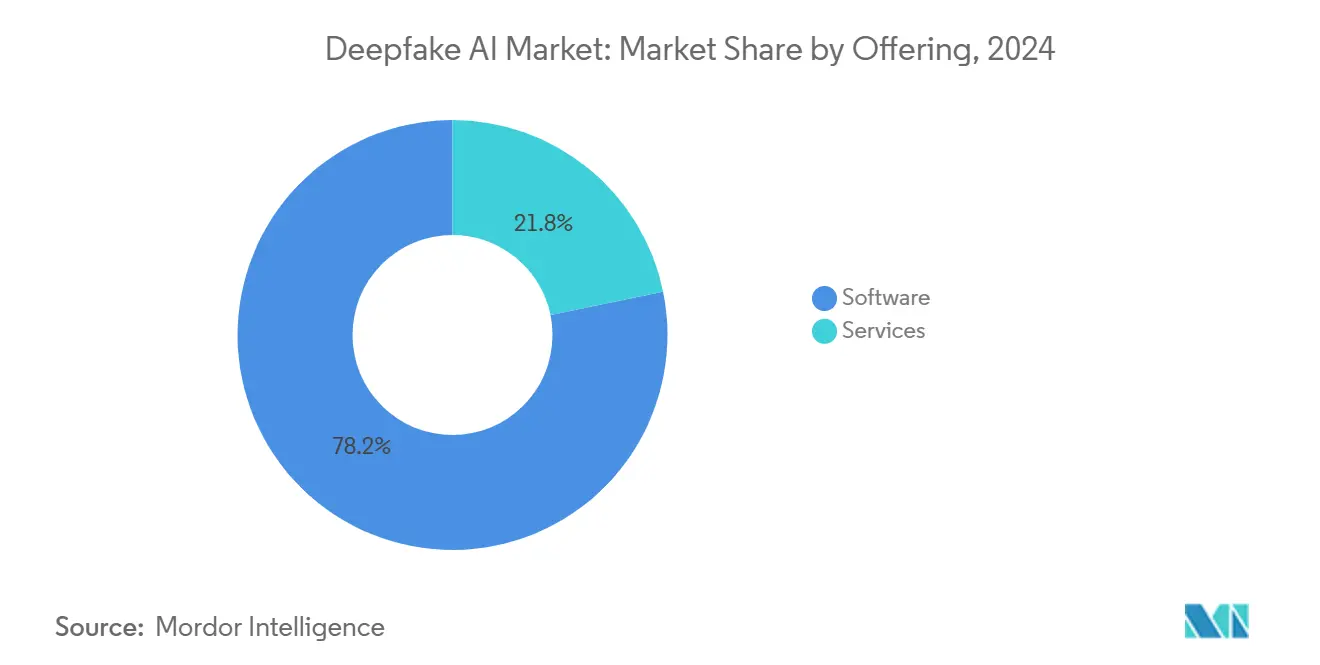

- By offering, software retained a 78.22% revenue share of the deepfake AI market in 2024; however, services are forecast to expand at a 49.12% CAGR to 2030.

- By technology, generative adversarial networks held 69.46% of the deepfake AI market share in 2024, while transformer models are expected to accelerate at a 50.54% CAGR through 2030.

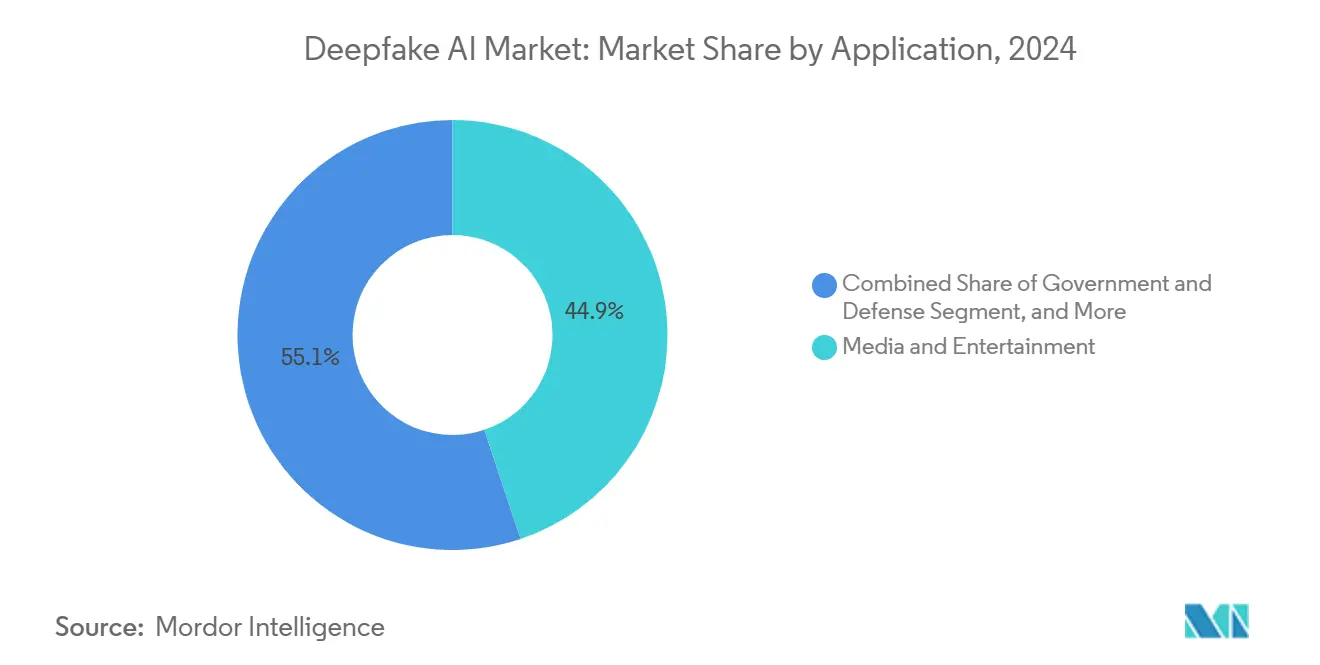

- By application, media and entertainment commanded 44.86% of the deepfake AI market size in 2024, whereas banking and financial services are set to grow at a 49.66% CAGR to 2030.

- By deployment mode, cloud deployment captured 69.66% revenue share of the deepfake AI market in 2024 and is poised to widen its lead with a 51.86% CAGR through 2030.

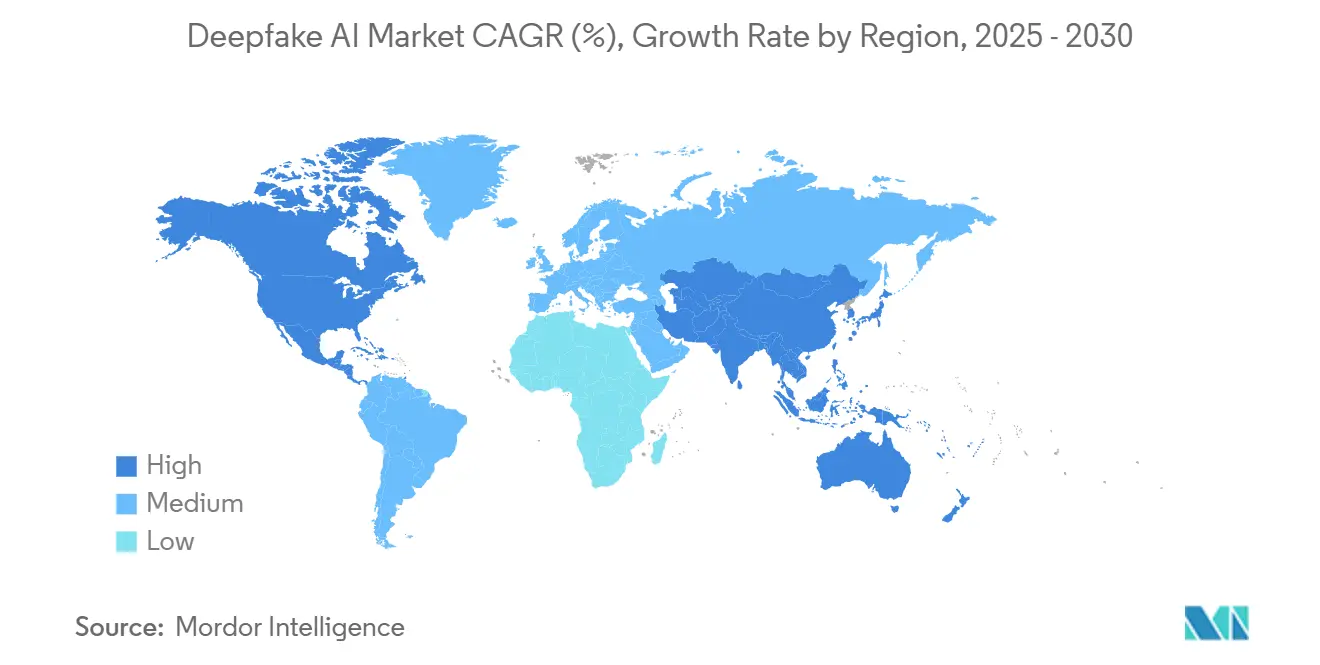

- By geography, North America led the deepfake AI market with a 44.12% revenue share in 2024; the Asia Pacific is projected to record a 49.48% CAGR from 2024 to 2030.

Global Deepfake AI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Advancements in Generative Adversarial Networks | +8.2% | Global, with concentration in North America and Asia Pacific | Medium term (2-4 years) |

| Rising Demand for Personalized Synthetic Media in Marketing and Entertainment | +6.8% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Surge in Deepfake-Enabled Financial Fraud Driving Investment in Detection Solutions | +9.1% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Government Procurement of Deepfake Detection for Defense and Law-Enforcement Operations | +5.4% | North America, Europe, Asia Pacific core markets | Medium term (2-4 years) |

| Integration of Multimodal Deepfake Forensics into eKYC Pipelines of Crypto Exchanges | +4.7% | Global, with early adoption in Asia Pacific and Europe | Medium term (2-4 years) |

| Availability of Large Open-Source Multimodal Deepfake Datasets Accelerating Start-Up Innovation | +3.9% | Global, concentrated in tech hubs across regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Advancements in Generative Adversarial Networks

StyleGAN3 and related architectures now generate 4K video with 40% less compute overhead than prior models, enabling real-time applications on mainstream cloud instances. Attention-augmented adversarial training improves frame-to-frame coherence, elevating professional uses in film, gaming, and marketing. Cloud vendors have packaged these models into turnkey APIs, slashing pilot deployment timelines from months to days. Broader access expands the deepfake AI market as small creative studios adopt synthetic media to lower production budgets. The same innovations, however, raise stakes for detection vendors that must keep pace with higher-fidelity fakes.

Personalized Synthetic Media for Marketing and Entertainment

Marketers now tailor video content to individual consumers at scale, after production costs fell 60% from 2023 to 2024 due to more efficient models and cloud pricing. Coca-Cola’s 2024 multilingual campaign delivered localized spokespeople in 47 languages, trimming video budgets by 65%. Streaming platforms use deepfake dubbing and age-progression to extend catalog lifecycles, while movie studios report 30% savings on visual-effects budgets. High engagement metrics in A/B tests reinforce advertiser confidence, funneling more capital toward generative media vendors and accelerating the deepfake AI market.

Surge in Deepfake-Enabled Financial Fraud

Incident volumes jumped 347% year on year, with voice and video spoofs circumventing legacy identity checks. JPMorgan Chase allocated USD 200 million in 2024 to integrate multimodal detection across call centers and mobile banking apps. Federal Deposit Insurance Corporation guidance now mandates detection protocols by December 2025, making compliance non-optional for U.S. banks. European regulators are drafting parallel rules, creating synchronized demand across both continents. Rising losses averaging USD 1.2 million per incident make ROI for detection solutions clear, propelling the deepfake AI market.

Government Procurement for Defense and Law-Enforcement

The U.S. Department of Defense directed USD 87 million to DARPA’s Media Forensics program in 2024, prioritizing tools that flag manipulated battlefield imagery. [1]U.S. Department of Defense, “DARPA Media Forensics Program Receives USD 87 Million Funding,” defense.gov NATO established common deepfake detection protocols, stimulating vendor opportunities across 31 member states. Police agencies embed detection software in digital-evidence labs, achieving 156 felony convictions tied to synthetic media in 2024. Stable government budgets offer counter-cyclical revenue streams, enhancing visibility for vendors and anchoring long-term demand across the deepfake AI market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Uncertainty and Fragmented Legal Frameworks | -4.3% | Global, particularly affecting cross-border operations | Medium term (2-4 years) |

| High Computational Costs for Real-Time High-Resolution Deepfake Generation and Detection | -3.8% | Global, with greater impact in cost-sensitive markets | Short term (≤ 2 years) |

| Erosion of Consumer Trust Reducing Monetization of Synthetic Media Platforms | -2.9% | North America and Europe primarily | Medium term (2-4 years) |

| Shortage of Diverse Training Data Causing Detection Bias in Non-Western Languages | -2.1% | Asia Pacific, Middle East, Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Uncertainty and Fragmented Legal Frameworks

The European Union’s AI Act imposes disclosure labels and risk audits, while the United States relies on a patchwork of state statutes California targets political deepfakes, Texas focuses on intimate imagery.[2]European Parliament, “EU AI Act First Regulation on Artificial Intelligence,” europarl.europa.eu Enterprises operating in multiple jurisdictions face 25-30% higher compliance costs to reconcile divergent rules. China’s draft law requires security reviews before commercial release of synthetic-media tools, slowing foreign market entry. These inconsistencies delay projects, divert budget to legal consulting, and temper the near-term expansion of the deepfake AI market.

High Computational Costs for Real-Time, High-Resolution Processing

Generating or detecting 4K video deepfakes at 30 frames per second can demand GPU clusters costing USD 50,000-200,000, while live-stream analysis consumes 40-60% more compute than generative workloads. Monthly cloud spend for a mid-tier financial institution monitoring all video calls can exceed USD 10,000. Rising energy prices and sustainability targets increase scrutiny of data-center footprints, prompting CFOs to weigh deployment timing. Edge accelerators and AI-specific chips offer relief yet remain too expensive for small businesses, restraining deepfake AI market adoption in cost-sensitive sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Acceleration Despite Software Dominance

Software contributed 78.22% of revenue in 2024, reflecting entrenched adoption of generation platforms, detection algorithms, and modular APIs that slot easily into existing enterprise stacks. The segment benefits from standardized SDKs, broad developer communities, and extensions from major cloud ecosystems. Platform subscription models have shifted revenue from perpetual licenses to recurring streams, enhancing vendor valuation multiples. In contrast, professional and managed services are scaling faster at a 49.12% CAGR, a dynamic propelled by the need for bespoke model training, compliance consulting, and 24 x 7 detection monitoring in regulated industries.

Service providers now bundle ethical-AI governance workshops, red-team adversarial testing, and end-user training to satisfy board-level accountability mandates. Demand spikes as mid-market banks outsource multimodal forensics to specialists rather than building seven-figure in-house teams. This momentum suggests services could approach one-third of the deepfake AI market by 2030, even if software retains absolute revenue leadership.

By Technology: Transformer Models Disrupting GAN Supremacy

Generative adversarial networks preserved 69.46% ownership of the technology landscape in 2024, anchoring the deepfake AI market share owing to a decade of peer-reviewed progress and open-source toolchains. Their image and video fidelity remains competitive for short-form content, while optimized variants run efficiently on commodity GPUs. Transformer models, however, are expanding at a 50.54% CAGR, bolstered by seamless integration with large language models that unlock text-to-video and cross-modal creativity. Early benchmarks indicate 15-20% better temporal coherence in long-form video at equivalent resolutions, albeit with 30-40% greater compute demands.

Enterprise adoption of transformers accelerates as firms piggyback on existing NLP investments; internal legal teams also favor their interpretability features for audit trails. Diffusion hybrids and variational autoencoders occupy niche roles in compression, watermarking, and feature extraction pipelines where explainability outweighs raw fidelity. The competitive interplay among architectures ensures multi-stack strategies will dominate through 2030, keeping the deepfake AI market technologically diverse.

By Application: Banking Momentum Challenges Media Leadership

Media and entertainment anchored 44.86% of revenue in 2024, leveraging deepfakes for de-aging actors, real-time lip-sync dubbing, and immersive gaming characters. Studios report 30% production cost savings, and social platforms observe higher engagement from AI-generated avatars. Yet banking, financial services, and insurance is scaling at a 49.66% CAGR, driven by an urgent need to authenticate customer identities and thwart synthesized fraud attempts. Bank of America allocated USD 150 million in 2024 to deploy detection pipelines across onboarding and contact-center flows.

Mandatory regulatory deadlines crystallize demand: U.S. banks must meet FDIC guidelines by end-2025, while the European Banking Authority is drafting companion standards. Government and defense ranks third, propelled by disinformation countermeasures and training simulations. Healthcare is experimenting with synthetic patients for clinical training but faces slower approval cycles. Advertising firms increasingly fuse deepfakes with first-party data, yet they confront looming transparency mandates that may temper adoption pace after 2026.

By Deployment Mode: Cloud Dominance Accelerates on Scalability

The cloud captured 69.66% of adoption in 2024 and is forecast to grow at 51.86% CAGR as organizations favor elastic pricing and managed security patches. Amazon Web Services, Microsoft Azure, and Google Cloud have introduced deepfake detection APIs that charge as little as USD 0.10 per analysis minute, lowering the entry threshold for mid-market enterprises.[3]Amazon Web Services, “Amazon SageMaker Deepfake Detection Service Launch,” aws.amazon.comCustomers report 40-60% total-cost reductions compared with on-premises alternatives, particularly for bursty or experimental workloads.

On-premises and private-cloud deployments persist in defense, government, and tier-one banking, where air-gapped networks remain non-negotiable. Hybrid architectures training in public clouds, inferencing on local servers are growing popular as data-sovereignty rules tighten. Edge computing rounds out the mix, supporting mobile devices and real-time broadcast systems that cannot tolerate cloud latency. Vendors able to orchestrate seamless workload portability across these modes stand to capture outsized shares of the deepfake AI market.

Geography Analysis

North America retained leadership at 44.12% share in 2024, supported by federal grants exceeding USD 500 million and enterprise-scale deployments inside entertainment, finance, and defense. From 2025 onward the region’s CAGR is projected to reach 47%, reflecting continuous upgrades by cloud providers and tighter anti-fraud regulations. Canada’s AI hubs in Toronto and Montréal feed talent pipelines, while Mexico offers cost-effective engineering that further embeds the deepfake AI market across the continent.

Asia Pacific’s rise is driven by China’s state-backed ventures, India’s IT outsourcing surge, and South Korea’s 5G-enabled edge computing. The region already hosts more than 40% of global deepfake startups and is forecast to capture nearly one-third of revenue by 2030. China’s National AI Development Plan secures long-term capital, whereas Japan exploits deepfakes for robotics and immersive entertainment. Australia, New Zealand, and Singapore function as regulatory sandboxes, inviting responsible-AI pilots that influence international standards.

Europe demonstrates steady but cautious growth, balancing innovation with strict governance. Germany leverages industrial AI for automotive digital twins, the United Kingdom embeds detection in fintech compliance stacks, and France channels cultural-heritage digitization into synthetic-media tools. The EU AI Act may initially slow rollouts but is expected to create trusted product differentiation after 2026, drawing privacy-sensitive buyers from the United States and Asia Pacific.

Competitive Landscape

The deepfake AI market remains moderately fragmented, with no single vendor accounting for more than a 10% revenue share. Cloud hyperscalers, including Amazon, Microsoft, and Google, bundle generation and detection into their existing ML suites, leveraging scale economics and broad channel reach. Specialized firms, such as Synthesia, D-ID, and Reality Defender, differentiate themselves through domain focus, rapid iteration, and proprietary datasets. Semiconductor leaders NVIDIA and Intel monetize GPU and edge-AI silicon required for both creation and detection workloads, while cybersecurity vendors Pindrop and Truepic secure voice and image channels, respectively.

Strategic patterns highlight platform consolidation: Microsoft embedded real-time detection into Microsoft Teams, while Google’s Gemini Pro Vision exposed detection APIs for third-party developers. Vertical focus also intensifies; Reality Defender targets financial services compliance, whereas Sensity supports social network moderation. Mergers and acquisitions are likely as cloud providers seek to internalize niche capabilities and as banks acquire startups to shore up proprietary eKYC stacks. Long-term winners will combine multimodal generation, watermarking, and forensic authentication within a unified dashboard, simplifying vendor management for enterprises that demand end-to-end governance of synthetic media.

Recent venture activity underscores momentum. Synthesia’s USD 90 million Series C round at a USD 1 billion valuation signals investor confidence in avatar-centric adoption models. Reality Defender’s USD 33 million Series B funding supports European expansion, tapping into the growing demand for EU compliance. Meanwhile, NVIDIA’s Omniverse Avatar Cloud Engine monetizes hardware pull-through by offering turnkey digital-human creation on an hourly GPU-compute basis. Collectively, these moves reflect a market shifting from experimental pilots to production-scale rollouts, reinforcing the growth trajectory of the deepfake AI market.

Deepfake AI Industry Leaders

Synthesia Limited

D-Id Ltd.

Sentinel Labs Oü

Reality Defender Inc.

Reface Ai Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Intel Corporation updated the OpenVINO toolkit with optimized deepfake detection models for edge devices, enabling real-time analysis without discrete GPUs.

- March 2025: D-ID Ltd. partnered with Zoom Video Communications to embed personalized AI avatars in virtual meetings and presentations.

- February 2025: Truepic Inc. achieved SOC 2 Type II certification for its content authenticity platform, boosting adoption in finance and healthcare sectors.

- January 2025: Pindrop Security Inc. expanded deepfake voice detection support to 47 additional languages, meeting global call-center fraud-prevention needs.

Global Deepfake AI Market Report Scope

| Software |

| Services |

| Generative Adversarial Networks |

| Transformer Models |

| Autoencoders |

| Other Technologys |

| Media and Entertainment |

| Banking, Financial Services and Insurance |

| Government and Defense |

| Healthcare and Life Sciences |

| Advertising and Marketing |

| Cloud |

| On-Premises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Offering | Software | |

| Services | ||

| By Technology | Generative Adversarial Networks | |

| Transformer Models | ||

| Autoencoders | ||

| Other Technologys | ||

| By Application | Media and Entertainment | |

| Banking, Financial Services and Insurance | ||

| Government and Defense | ||

| Healthcare and Life Sciences | ||

| Advertising and Marketing | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the deepfake AI market in 2025?

The deepfake AI market size reached USD 1.14 billion in 2025 and is projected to compound at 48.06% annually through 2030.

Which technology leads current adoption?

Generative adversarial networks dominate with 69.46% share, although transformer models are the fastest-growing technology at a projected 50.54% CAGR.

What drives banking demand for deepfake tools?

A 347% spike in deepfake-enabled fraud and new FDIC guidance have pushed banks to invest heavily in multimodal detection across onboarding and customer-service channels.

Why is Asia Pacific growing faster than North America?

Large government AI budgets, expanding digital infrastructure, and a surge of domestic vendors position Asia Pacific to grow at 49.48% CAGR, outpacing North America despite the latter’s current lead.

What role do cloud providers play?

Cloud hyperscalers offer deepfake generation and detection APIs that cut compute costs by up to 60%, making them the primary deployment mode and accelerating enterprise adoption.

How fragmented is the competitive landscape?

No vendor controls more than 10% of revenue, so the market scores a 3 on a 10-point concentration scale, favoring partnerships and specialized niche strategies.

Page last updated on: